Abstract

Anthropogenic greenhouse gas (GHG) emissions coming mainly from fossil fuel combustion for energy use are causing air temperature increases resulting in climate change. This study employs an environmentally extended input–output model to conduct an economy-wide assessment of GHG emissions in the European Union (EU). Model results indicate that the assumed growth of economic activity by 2030 will lead to a large increase in GHG emissions by 89%, assuming no technological change and no additional policy mitigation efforts. The electricity sector and agriculture create the highest direct and indirect GHG emissions per unit of economic output across the 27 EU member states (EU-27); for every 1-million-euro-increase in the final demand for the products and services of the electricity sector and agriculture, 2198 and 1410 additional tons of GHG emit, respectively. Regional climate projections under a low-decarbonisation pathway (RCP8.5), in accordance with our economic analysis, indicate a further increase of regional warming, combined with pronounced changes in the hydrological cycle. Contrariwise, following a strong mitigation pathway (RCP2.6) will result in warming levels lower than 1.5 °C with respect to the 1986–2005 reference period. Our findings reveal the importance of both direct and indirect contribution of economic sectors in the generation of GHG emissions, taking into consideration the size of the sectors and the assumed growth rates. The design and implementation of sectoral emission reduction policies from the perspective of the whole production supply chain can effectively contribute to GHG emission reduction commitments.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Economic and population growth have contributed to increasing demand for resources, including energy. Anthropogenic greenhouse gas (GHG) emissions, coming mainly from fossil fuel combustion for energy production (mainly coal and crude oil), are causing air temperature increases resulting in climate change (IPCC 2013). According to the Intergovernmental Panel on Climate Change (IPCC 2018), human-induced global warming, reached approximately 1.0 °C above pre-industrial levels in 2017 (with a likely range of 0.8 °C and 1.2 °C). In the absence of ambitious mitigation policies in the coming years that could lead to a sharp decline in GHG emissions by 2030, global warming is likely to surpass 1.5 °C sometime between 2030 and 2045 (IPCC 2018).

The Paris Agreement, achieved at the 21st United Nations Climate Change Conference (COP21) in Paris in 2015, aims to substantially reduce global GHG emissions and limit the temperature increase by the end of this century to well below 2 °C above the pre-industrial levels, while pursuing efforts to limit the global warming to less than 1.5 °C (UNFCCC 2021). In the European Union (EU), the Governance of the Energy Union and Climate Action Regulation sets out the legislative framework for achieving the 2030 energy and climate targets in line with the Paris Agreement (Reg. (EU) 2018/1999 2018). Member states are obliged to prepare and submit integrated National Energy and Climate Plans (NECPs). These plans aim to support the binding objective for an overall economy-wide reduction of at least 40% of GHG levels by 2030 compared to 1990 (European Council 2014). The European Commission has recently proposed an EU-wide net GHG emissions reduction target of at least 55% by 2030, compared to 1990 levels, to put the EU on a balanced pathway to reach climate neutrality by 2050 (European Commission 2020a). The EU Green Deal, the major initiative to move to a net-zero GHG emissions economy by 2050, aims to achieve decarbonisation in the EU within the coming years (European Commission 2020b).

Across the 27 EU countries (EU-27), there is a general downward trend of GHG emissions during the last 3 decades. In particular, emissions in the EU-27 declined by 16% between 1995 and 2018, while the gross domestic product (GDP) of the EU-27 economy increased by 48% (Fig. 1—left panel). This figure shows that the EU is on track to fulfil its commitments to meet the 2020 climate and energy package targets (European Commission 2009), i.e. to meet its 20% GHG emissions reduction target for 2020 compared to 1990 levels. Within the same period, the GHG emission intensity of the EU-27 economy has decreased by 43%, highlighting the efforts of the EU member states to decarbonise their economies (Fig. 1—right panel) (Eurostat 2021b; EEA 2021). The contribution of the individual production sectors to the GHG emission generation substantially varies in size and from year to year. The largest emitting sectors in the EU, that is, the electricity production and the manufacturing sectors, decreased their GHG emissions between 2008 and 2019 by 31% and 22%, respectively (Eurostat 2021a). On the other hand, the agriculture-related emissions (about 15% of the total GHG emissions) have decreased by only 3%, while in other sectors, such as air transport and health services, GHG emissions have increased by 19% and 10%, respectively.

The relationship between economic activity and GHG emissions has been widely studied. A large part of the literature focuses on investigating the relationship between economic growth, energy use and GHG emissions, testing the validity of the Environmental Kuznets Curve hypothesis that postulates an inverted U-shaped relationship between environmental degradation and per capita income (Acaravci and Ozturk 2010; Lee et al. 2015; Manta et al. 2020). Bottom-up studies examining alternative approaches for reducing GHG emissions, including specific technological and managerial options per sector (Neuhoff 2005; Worrell et al. 2001), typically provide detailed information about emission reduction potential within certain sectors, but they do not capture systemic effects (Mundaca et al. 2019). Less effort has been devoted in exploring the relationship between economic structure, climate change and GHG emissions. Capturing the sectoral-level emission effects is critical to identify the key emitters and so contribute to the overall reduction of GHG emissions.

A clear understanding of any economic structure requires a sectoral categorization and an analysis of the inter-industry commodity flows (Ghosh and Roy 1998). Input–output analysis (IOA) has been considered a valid approach for studying such interdependencies between the production sectors in an economy (Miller and Blair 2009), and it has been extensively applied for policy impact analysis, structural and technical change analysis (Giannakis and Bruggeman 2017; Taliotis et al. 2020). The environmental extension of IOA models has consequently become a valuable technique for analysing interdependency among industries and GHG emissions (Hawkins et al. 2015). Tracing the GHG emissions embodied in the flows of intermediates along production supply chains can provide a more thorough understanding of how GHG are driven through economic activity (Peters 2008) and an integrated assessment of the contribution of the production sectors in the generation of GHG emissions (Suh 2006).

Computable General Equilibrium (CGE) models have also been used in the literature to study the interrelationships of production sectors and their impact on climate change (Eboli et al 2010). CGE models, unlike IO models, capture supply-side effects and allow for more flexibility, due to their non-linearity, regarding substitution effects and relative price changes (Koks et al. 2016). Optimization models, such as the TIMES (The Integrated MARKAL-EFOM System) and the MESSAGE (Model for Energy Supply Strategy Alternatives and their General Environmental Impacts), and accounting models, such as the LEAP (Long-range Energy Alternatives Planning system) and the GACMO (Greenhouse Gas Abatement Cost Model) have also been used for the development of the Nationally Determined Contributions (NDCs) worldwide (Haydock and McCullough 2017).

Given the highly uneven sectoral annual GHG emission generation and reduction potentials (Blok et al. 2020), an economy-wide assessment of the contribution of production sectors in the generation of GHG emissions is of major relevance. This paper aims to assess the direct and indirect contribution of economic sectors to GHG emissions, accounting for all monetary inter-sectoral transactions. Specifically, an environmentally extended input–output (EE-IOA) model is developed to explore the economy-wide effects of the growth of the production sectors on the GHG emissions generated in the EU-27. The paper is structured as follows: Sect. 2 outlines the methodology of the study, while Sect. 3 presents the results of the analysis. Section 4 presents complementary information on regional climate change projections for Europe under two concentration pathways for the future. The paper ends with a discussion of the results and conclusions drawn from the analysis.

2 Methods

2.1 Environmentally Extended Input–Output Analysis

The basic structure of an IOA model consists of a system of linear equations that account for the way in which the output of each sector i is distributed through sales to other sectors for intermediate use and final demand as follows (Miller and Blair 2009):

where \({x}_{i}\) is the total output of sector \(i\) \(\left(i=1,\dots ,n\right)\); \({x}_{ij}\) describes the inter-industry sales of sector \(i\) to all sectors \(j \left(j=1,\dots ,n\right)\); \({y}_{i}\) is the final demand for sector \({i}^{^{\prime}}s\) product.

The technical coefficients \(\left({a}_{ij}\right)\) represent the value of the output from sector \(i\) that is required to produce one unit of output in sector \(j\) as follows:

Equation (1) can then be rewritten in matrix notation as follows:

where \(A\) is the technical coefficients matrix. Solving Eq. (3) for \(X\), we obtain Eq. (4):

where \({\left(I-A\right)}^{-1}=L\) is the Leontief inverse or the total (direct and indirect) requirements matrix. The \(L\) matrix quantifies the direct and indirect impacts exerted by changes in final demand \(\left(\Delta Y\right)\) on the output of each sector \(\left(\Delta X\right)\). The output multiplier for an individual sector \(j\) is defined as the column sums of the \(L\) matrix \(\left(\sum_{i=1}^{n}{l}_{ij}\right)\).

The environmental extension of the basic IOA model can be obtained by introducing an exogenous vector of emission intensity, here denoted as \(D=\left[{d}_{i}\right]\), that is, the amount of GHG emissions \(\left({g}_{i}\right)\) per unit output of each sector \(i\) \(\left({x}_{i}\right)\) as follows (Camanzi et al. 2017; Giannakis et al. 2019):

The total (direct and indirect) GHG emissions \(\left(G\right)\) can be calculated as follows:

2.2 Data

The EU-27 symmetric IOA table for the year 2019 was derived from the Eurostat database (Eurostat 2021c). The initial scheme of 65 sectors of economic activity (Appendix Table 2) was aggregated into 25 economic sectors (Appendix Table 3). The sectoral GHG emission data were obtained by the Eurostat (2021a). Sources of uncertainty typically associated with EE-IOA include: (a) the assumption of constant returns to scale, (b) the assumption of fixed input structure, (c) the assumption of homogenous prices, (d) the assumption that the imported goods are produced with the same domestic technology, (e) uncertainties in source data (Wiedmann 2009).

In this study, we used the long-term outlook of the EU Reference Scenario 2016, that is, one of the key modelling tools of the European Commission for projecting economic activity, to estimate sectoral growth rates in the EU (Capros et al. 2016). Specifically, we explore the direct and indirect impact of the increase in the final demand for the output of the individual production sectors in the GHG emissions in the EU-27 from 2019 to 2030.

Considering the rapid warming over the region and in addition to the input–output analysis presented in the previous sections, we analysed state-of-the-art regional climate projections for the twenty-first century to assess the importance of adopting timely mitigation measures and reducing GHG emissions and concentrations. Following the temporal horizon of the IOA, we focus on the near-term changes (2021–2040), while for comparison, we also present mid-twenty-first-century (2041–2060) projections for temperature and precipitation. These projections are based on a large ensemble of high-resolution regional simulations (0.11 × 0.11°) that is part of the EURO-CORDEX initiative (Jacob et al. 2020). Our model selection is similar to Cherif et al. (2020) and is presented in Table 4 (Appendix). Our analysis is complementary to Jacob et al. (2014) and is an update in terms of future scenarios and ensemble size.

In the present study, we have assessed two future scenarios. The first Representative Concentration Pathway (RCP), RCP2.6 (Van Vuuren et al. 2011), is representative of scenarios leading to low GHG concentration levels. It is a so-called ‘peak’ scenario, in the sense that its radiative forcing first reaches a value around 3.1 W/m2 (mid-century), returning to 2.6 W/m2 by 2100. To reach such radiative forcing levels, GHG emissions and concentrations have to be reduced substantially over time. According to the latest Assessment Report of IPCC (2013), global warming under RCP2.6 stays below 2 °C above 1850–1900 levels throughout the twenty-first century, clearly demonstrating the potential of mitigation policies. This pathway closely meets the main targets of the Paris Agreement, aiming at keeping global warming less than 2 °C above pre-industrial levels. The second pathway, RCP8.5 (Riahi et al. 2007), is representative of scenarios that lead to high GHG concentration levels. It is considered as a high-emission pathway, which, however, at least for parts of the region, is following the observed temperature trends (Zittis et al. 2019). Notably, the two pathways under investigation start to deviate significantly after the 2030s.

3 Results

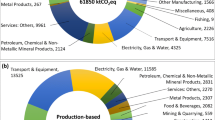

The IOA multiplier analysis identified the most important sectors of economic activity in view of their capacity to generate economic output throughout the EU economy (Table 1). The food industry has the highest output multiplier (O-M: 2.42), that is, for every 1-million-euro-increase in the final demand for the industry’s products, the total output of the economy will increase by 2.42 million euro. Similarly, the machinery and equipment sector (O-M: 2.17) also creates strong multiplier effects in the EU-27 economy, considering its high contribution to total economic output formation, that is, 10% (Fig. 2). On the other hand, service sectors such as real estate (O-M: 1.44) and education (O-M: 1.33) create low backward linkages with the other economic sectors.

Sectoral economic output and greenhouse gas (GHG) emission shares (%)

The EE-IOA multiplier analysis identified the contribution of the twenty-five economic sectors in the generation of GHG emissions (Table 1). The electricity sector has the highest GHG multiplier (GHG-M: 2198 tn/M€) in the EU, that is, for every 1-million-euro-increase in the final demand for the products and services of the sector, 2198 additional tons of GHG emit. Agriculture (GHG-M: 1410 tn/M€), air transport (GHG-M: 1223 tn/M€), chemical and plastic products (GHG-M: 1210 tn/M€) and shipping (GHG-M: 1057 tn/M€) are also significant (direct and indirect) GHG emitters. Similar to the IOA analysis, service sectors, such as education (GHG-M: 62 tn/M€) and health (GHG-M: 32 tn/M€), generate low GHG emissions.

In 2019, the EU-27’s sectors emitted 3049 megatons of GHG (CO2 equivalent). The assumed growth of EU economic sectors by 2030, assuming no change in technology \(\left({a}_{ij}\right)\) and no explicit policies and measures to reduce GHG emissions, results in a total (direct and indirect) increase of GHG emissions by 89% relative to 2019. Significant increases in the emissions of GHG are presented in the industrial sectors of machinery and equipment (332%) and chemical and plastic products (69%), which emit about 10.7% of the total GHG emissions in the EU-27. Several service sectors also exhibit large increases in their GHG emissions, such as trade (427%) and transportation warehousing services (259%); however, their share in the generation of GHG emissions is less than 3.7%. The relatively low increase of GHG emissions of agriculture (4%) and electricity (11%) sectors, i.e. the largest GHG emitters in absolute terms (Fig. 2), is mainly due to the assumed low growth rates by 2030.

4 Climate Change in Europe with and Without Decarbonisation

The regional implications of anthropogenic warming have been widely observed in Europe, and these are most profound over the last 3 decades (Kovats et al. 2014). These manifestations include an overall warming, faster than the global mean rates (Fig. 3). Particularly in the last four decades, the warming trend is 0.41 °C/decade, or 1.5 times higher than the global average (0.27 °C/decade). This regional temperature increase is mainly driven by the global concentration levels of greenhouse gases (mainly CO2). These gases have a long lifetime and are, therefore, well-mixed in the atmosphere. Besides some decarbonization efforts in Europe, global GHG concentrations have increased substantially (Olivier and Peters 2020), contributing to the observed warming trend, in addition to further positive climatic feedbacks. Past precipitation changes are mostly driven by natural climate variability (e.g. Zittis 2018), however, the role of anthropogenic climate change and external forcing is projected to become more evident, as drier (wetter) conditions are expected for southern (northern) Europe (Zittis et al. 2019; Coppola et al. 2021).

Observed global and European temperature anomalies with respect to the 1961–1990 historical reference period based on CRU-TS4.04 data (Harris et al. 2020). Linear trends for the last four decades (1981–2019) are also indicated

Mean annual temperature projections, with respect to the 1986–2005 historical reference period, are presented in the maps of Fig. 4. Under the strong mitigation pathway (RCP2.6), the projected changes for temperature will likely not exceed 1.5 °C (Fig. 4—left panels). This is the case for both time horizons under investigation. Exceptions are the northern parts of Scandinavia, where due to positive climate feedbacks, the projected warming is somehow higher (up to 3 °C in mid-century). In contrast, a high-emission pathway of low decarbonization rates (RCP8.5) indicates a much stronger European warming, particularly for the middle of the twenty-first century (Fig. 4—right panels). For the hot-spot areas (for example, the Alps and Scandinavia), the temperature increase could reach levels of 4–5 °C. Such warming levels and reduced snow cover imply severe impacts in a range of critical socio-economic sectors, including tourism, agriculture, hydropower and more (Gobiet et al. 2014; Jacob et al. 2018). The snow-albedo positive feedback (Winter et al. 2017) is likely dominant in these areas since, in a warmer future, smaller areas are expected to be covered by snow during the winter and spring seasons. Since we have used a relatively recent reference period, about 0.6–0.7 °C should be added to these projections to approximate the regional warming levels with respect to the pre-industrial era. This comparison highlights the need for timely decarbonization at the European and global scales. For specific hot-spot areas (for example, Scandinavia, Iberia, East Europe, Anatolia, North Africa), the milder warming (about 0.5 °C less), projected under a more sustainable pathway (i.e. RCP2.6), is already evident in the next 2 decades.

Projected annual temperature change for the near future (NEAR: 2021–2040) and the middle of the twenty-first century (MID: 2041–2060) with respect to the historical reference period (REF: 1986–2005), based on the EURO-CORDEX ensemble of regional climate projections. Pathway RCP2.6 is presented in the left panels and pathway RCP8.5 in the right panels

Future precipitation projections for Europe are presented in Fig. 5. Under pathway RCP2.6, mild changes (± 10%) are expected throughout the region (Fig. 5—left panels). In this scenario, with respect to the reference period (1986–2005), most of Europe is expected to become wetter, except for some Mediterranean countries. The high-emission pathway RCP8.5 implies similar precipitation changes for the near-future period (2021–2040). By the middle of the current century (2041–2060), the projected signal is expected to intensify with increased precipitation (10–20%) in northeast Europe and Scandinavia and strong drying (decreases of 10–30%) for Mediterranean Europe (Fig. 5—right panels).

Projected annual precipitation change for the near future (NEAR: 2021–2040) and the middle of the twenty-first century (MID: 2041–2060) with respect to the historical reference period (REF: 1986–2005), based on the EURO-CORDEX ensemble of regional climate projections. Pathway RCP2.6 is presented in the left panels and pathway RCP8.5 in the right panels

The projected precipitation changes for southern and northern Europe are mainly attributed to changes in atmospheric circulation and thermodynamics. Under rising greenhouse gas concentrations, climate models project that the Hadley Cell circulation will change, the tropics will expand, and the mid-latitude westerlies and associated storm tracks will likely shift poleward (Cherif et al. 2020). This is expected to enhance subsidence and reduce storminess at the latitudes of southern Europe and the Mediterranean region, with a resulting reduction in precipitation (Fig. 5). This poleward shift of storm tracks, in addition to changes in thermodynamics, can explain the projected precipitation increase in northern Europe. For example, the Clausius–Clapeyron relationship predicts an increase in the water holding capacity of air (the saturation water vapor pressure) of approximately 7%/°C rise in temperature (Held and Soden 2006).

5 Discussion and Conclusions

In this study, we empirically analysed the relationship between the production activities of the EU-27’s economic system and GHG emissions at the macroeconomic level. Our analysis shows the level of GHG emissions that would occur in the EU-27 by 2030 in the absence of any further policy mitigation effort and without any technological progress. In particular, the results of the EE-IOA model indicate that the assumed growth of economic activity will lead to a large increase in GHG emissions, that is, around 89%.

Our regional climate projections under a high-emission pathway of low decarbonisation (RCP8.5), in accordance with our economic analysis, indicate a considerable increase of European warming levels while for a strong mitigation pathway (RCP2.6), warming will not surpass 1.5 °C, with respect to our reference period (or about 2–2.5 °C since pre-industrial levels). Near and mid-term climate projections for precipitation indicate changes of the range of ± 10% for both pathways. These ranges agree with previous assessments for the region (Gobiet et al. 2014; Jacob et al. 2018; Zittis et al. 2019; Coppola et al. 2021). Moreover, the identified hot-spot areas (for example, northeast Europe and parts of the Mediterranean) corroborate previous studies (Giorgi 2006; Giorgi and Lionello 2008). Both analyses highlight the crucial role of sectoral climate change mitigation policies and decarbonisation technologies to ameliorate the negative effects of economic growth in the generation of GHG emissions and to meet EU GHG emission reduction targets.

The results of the EE-IOA multiplier analysis revealed that the electricity and the agricultural sectors create the highest direct and indirect GHG emissions in the EU-27 per unit (million euro) of economic output produced. Electricity, agriculture and the industrial sectors of metal and non-metal products and chemical and plastic products are also the largest GHG emitters in absolute terms (tons). Our analysis reveals the importance of both direct and indirect contribution of economic sectors in the generation of GHG emissions, taking into consideration the size of the sector in terms of economic output formation and GHG emissions generation, and the assumed growth rates.

Our findings are aligned with the results of Liu et al. (2020), who found with the use of EE-IOA models that agriculture and electric power generation sectors have high-emission intensities and a strong effect on other industries in Canada. The electricity, the metal and non-metal products and the land transport sectors are the most important CO2 emitters in Cyprus (Giannakis et al. 2020). Morán and González (2007) found that the largest CO2 emitters in Spain are the electricity and the metal and non-metal products sectors. Alcántara and Padilla (2020) showed that the sectors inducing more GHG emissions from other sectors in the Spanish economy are food manufacturing, wholesale and retail trade and construction. The metal products, the chemical products and the coal mining and petroleum processing products are the key GHG-emitting sectors in China (Guo et al. 2018; Shen et al. 2018; Yuan et al. 2020).

Identifying key GHG-emitting sectors, including both direct and indirect emissions, is, thus, crucial for formulating effective energy and environmental policies. Our findings stress the importance of an effective enforcement regime for reducing GHG emissions to counterbalance the adverse effects of economic growth. Moreover, they highlight the need for deploying advanced technologies to reduce sectoral emission intensities and contribute to the EU’s medium- and long-term ambitious decarbonization targets. A broad portfolio of clean energy technologies will be needed to decarbonize all sectors of the economy, including further advancements in renewables, energy efficiency and storage and hydrogen-producing electrolyzers (IEA 2020).

Sectoral emission intensities are expected to vary greatly in the near future. Thus, if the focus is on individual GHG-emitting sectors, ignoring the complicated relations and linkages between different GHG-emitting sectors, the effectiveness of mitigation policies will be limited as less attention will be paid to sectors with low direct GHG emissions but high indirect linkages that drive other sectors to release emissions. The formulation and implementation of industrial emission reduction policies from the perspective of the whole industrial chain can be more efficient than policies focusing on specific individual sectors (Xie et al. 2016). Future research could analyse the emission intensities of the production sectors with their associated GHG abatement costs to explore the cost-effectiveness of abatement options within certain sectors to meet GHG emission reduction targets.

References

Acaravci A, Ozturk I (2010) On the relationship between energy consumption, CO2 emissions and economic growth in Europe. Energy 35(12):5412–5420

Alcántara V, Padilla E (2020) Key sectors in greenhouse gas emissions in Spain: an alternative input–output analysis. J Ind Ecol 24(3):577–588

Blok K, Afanador A, Van Der Hoorn I, Berg T, Edelenbosch OY, Van Vuuren DP (2020) Assessment of sectoral greenhouse gas emission reduction potentials for 2030. Energies 13(4):943

Camanzi L, Alikadic A, Compagnoni L, Merloni E (2017) The impact of greenhouse gas emissions in the EU food chain: a quantitative and economic assessment using an environmentally extended input–output approach. J Clean Prod 157:168–176

Capros P, De Vita A, Tasios N, Siskos P, Kannavou M, Petropoulos A, Evangelopoulou S et al (2016) EU reference scenario 2016: energy, transport and GHG emissions trends to 2050. Publications Office of the European Union, Luxembourg

Cherif S, Doblas-Miranda E, Lionello P, Borrego C, Giorgi F, Iglesias A, Jebari S, Mahmoudi E, Moriondo M, Pringault O, Rilov G, Somot S, Tsikliras A, Vila M, Zittis G (2020) Drivers of change. In: Climate and environmental change in the Mediterranean Basin—current situation and risks for the future. In: Cramer W, Guiot J, Marini K (eds) First Mediterranean Assessment Report, Union for the Mediterranean, Plan Bleu, UNEP/MAP, Marseille, France, pp 59–128

Coppola E, Nogherotto R, Ciarlo JM, Giorgi F, van Meijgaard E, Kadygrov N, Iles C, Corre L, Sandstad M, Somot S, Nabat P, Vautard R, Levavasseur G, Schwingshackl C, Sillmann J, Kjellström E, Nikulin G, Aalbers E, Lenderink G, Christensen OB, Boberg F, Sørland SL, Demory ME, Bülow K, Teichmann C, Warrach-Sagi K, Wulfmeyer V (2021) Assessment of the European Climate Projections as simulated by the large EURO-CORDEX regional and global climate model ensemble. J Geophys Res Atmos 126(4):1–20

Eboli F, Parrado R, Roson R (2010) Climate-change feedback on economic growth: explorations with a dynamic general equilibrium model. Environ Dev Econ 15(5):515–533

EEA (2021) EEA greenhouse gas. European Environmental Agency, 2021. https://www.eea.europa.eu/data-and-maps/data/data-viewers/greenhouse-gases-viewer. Accessed 2 Feb 2021

European Commission (2009) Communication from the Commission to the Council, the European Parliament, the European Economic and Social Committee and the Committee of the Regions—limiting global climate change to 2 degrees Celsius—the way ahead for 2020 and beyond, Brussels, 10.1.2007 COM(2007) 2 final

European Commission (2020a) Communication from the Commission to the European Parliament, the Council, the European Economic and Social Committee and the Committee of the Regions ‘Stepping up Europe’s 2030 climate ambition Investing in a climate-neutral future for the benefit of our people’, Brussels, 17.9.2020 COM(2020) 562 final

European Commission (2020b) Communication from the Commission to the European Parliament, the European Council, the Council, the European Economic and Social Committee and the Committee of the Regions ‘The European Green Deal’, Brussels, 11.12.2019 COM(2019) 640 final

European Council (2014) Conclusions. EUCO 169/14. https://www.consilium.europa.eu/media/24561/145397.pdf. Accessed 15 Feb 2021

Eurostat (2008) Statistical classification of economic activities in the European Community. NACE Rev. 2. Office for Official Publications of the European Communities, Luxembourg

Eurostat (2021a) Air emissions accounts by NACE Rev. 2 activity [env_ac_ainah_r2]. https://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=env_ac_ainah_r2&lang=en. Accessed 1 Mar 2021

Eurostat (2021b) GDP and main components (output, expenditure and income) [nama_10_gdp]. https://appsso.eurostat.ec.europa.eu/nui/show.do?dataset=nama_10_gdp&lang=en. Accessed 1 Mar 2021

Eurostat (2021c) Symmetric input–output table at basic prices (product by product) [naio_10_cp1700]. https://ec.europa.eu/eurostat/databrowser/view/naio_10_cp1700/default/table?lang=en. Accessed 1 Mar 2021

Ghosh S, Roy J (1998) Qualitative input–output analysis of the Indian economic structure. Econ Syst Res 10(3):263–274

Giannakis E, Bruggeman A (2017) Economic crisis and regional resilience: evidence from Greece. Pap Reg Sci 96(3):451–476

Giannakis E, Kushta J, Giannadaki D, Georgiou GK, Bruggeman A, Lelieveld J (2019) Exploring the economy-wide effects of agriculture on air quality and health: evidence from Europe. Sci Total Environ 663:889–900

Giannakis E, Serghides D, Dimitriou S, Zittis G (2020) Land transport CO2 emissions and climate change: evidence from Cyprus. Int J Sustain Energy 39(7):634–647

Giorgi F (2006) Climate change hot-spots. Geophys Res Lett 33(8):L08707

Giorgi F, Lionello P (2008) Climate change projections for the Mediterranean Region. Global Planet Change 63(2–3):90–104

Gobiet A, Kotlarski S, Beniston M, Heinrich RJ, Stoffel M (2014) 21st Century climate change in the European Alps—a review. Sci Total Environ 493:1138–1151

Guo J, Zhang YJ, Zhang KB (2018) The key sectors for energy conservation and carbon emissions reduction in China: evidence from the input–output method. J Clean Prod 179:180–190

Harris I, Osborn TJ, Jones P, Lister D (2020) Version 4 of the CRU TS monthly high-resolution gridded multivariate climate dataset. Sci Data 7:1–18

Hawkins J, Ma C, Schilizzi S, Zhang F (2015) Promises and pitfalls in environmentally extended input–output analysis for China: a survey of the literature. Energy Econ 48:81–88

Haydock H, McCullough A (2017) Methodological approach towards the assessment of simulation models suited for the economic evaluation of mitigation measures to facilitate NDC implementation. Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH, Bonn

Held IM, Soden BJ (2006) Robust responses of the hydrological cycle to global warming. J Clim 19(21):5686–5699

IEA (2020) Batteries and hydrogen technology: keys for a clean energy future, International Energy Agency, Paris. https://www.iea.org/articles/batteries-and-hydrogen-technology-keys-for-a-clean-energy-future. Accessed 5 Apr 2021

IPCC (2018) Global warming of 1.5 °C. In: Masson-Delmotte V, Zhai P, Pörtner HO, Roberts D, Skea J, Shukla PR, Pirani A, Moufouma-Okia W, Péan C, Pidcock R, Connors S, Matthews JBR, Chen Y, Zhou X, Gomis MI, Lonnoy E, Maycock T, Tignor M, Waterfield T (eds) An IPCC special report on the impacts of global warming of 1.5 °C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty

IPCC (2013) Climate Change 2013: the physical science basis. In: Stocker TF, Qin D, Plattner G-K, Tignor M, Allen SK, Boschung J, Nauels A, Xia Y, Bex V, Midgley PM (eds) Contribution of working group I to the fifth assessment report of the Intergovernmental Panel on Climate Change. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA, p 1535

Jacob D, Petersen J, Eggert B et al (2014) EURO-CORDEX: new high-resolution climate change projections for European impact research. Reg Environ Change 14:563–578

Jacob D, Kotova L, Teichmann C et al (2018) Climate impacts in Europe under + 1.5 °C global warming. Earth Future 6:264–285

Jacob D, Teichmann C, Sobolowski S, Katragkou E et al (2020) Regional climate downscaling over Europe: perspectives from the EURO-CORDEX community. Reg Environ Change 20:51

Koks EE, Carrera L, Jonkeren O, Jeroen C, Aerts JC, Husby TG, Thissen M, Standardi G, Mysiak J (2016) Regional disaster impact analysis: comparing input–output and computable general equilibrium models. Nat Hazard 16(8):1911–1924

Kovats RS, Valentini R, Bouwer LM, Georgopoulou E, Jacob D, Martin E, Rounsevell M, Soussana JF (2014) Europe. In: Barros VR, Field CB, Dokken DJ, Mastrandrea MD, Mach KJ, Bilir TE, Chatterjee M, Ebi KL, Estrada YO, Genova RC, Girma B, Kissel ES, Levy AN, MacCracken S, Mastrandrea PR, White LL (eds) Climate change 2014: impacts, adaptation, and vulnerability. Part B: regional aspects. Contribution of Working Group II to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA, pp 1267–1326.

Lee JM, Chen KH, Cho CH (2015) The relationship between CO2 emissions and financial development: evidence from OECD countries. Singap Econ Rev 60(05):1550117

Liu L, Huang G, Baetz B, Cheng G, Pittendrigh SM, Pan S (2020) Input–output modeling analysis with a detailed disaggregation of energy sectors for climate change policy-making: a case study of Saskatchewan, Canada. Renew Energy 151:1307–1317

Manta AG, Florea NM, Bădîrcea RM, Popescu J, Cîrciumaru D, Doran MD (2020) The Nexus between carbon emissions, energy use, economic growth and financial development: evidence from Central and Eastern European countries. Sustainability 12(18):7747

Miller RE, Blair PD (2009) Input–output analysis: foundations and extensions. Cambridge University Press

Morán MAT, del Río GP (2007) A combined input–output and sensitivity analysis approach to analyse sector linkages and CO2 emissions. Energy Econ 29(3):578–597

Mundaca L, Ürge-Vorsatz D, Wilson C (2019) Demand-side approaches for limiting global warming to 1.5 °C. Energ Effi 12:343–362. https://doi.org/10.1007/s12053-018-9722-9

Neuhoff K (2005) Large-scale deployment of renewables for electricity generation. Oxf Rev Econ Policy 21(1):88–110

Olivier JGJ, Peters JAHW (2020) Trends in global CO2 and total greenhouse gas emissions: 2020 report. PBL Netherlands Environmental Assessment Agency, The Hague

Peters GP (2008) From production-based to consumption-based national emission inventories. Ecol Econ 65(1):13–23

Regulation (EU) 2018/1999 of the European Parliament and of the Council of 11 December 2018 on the Governance of the Energy Union and Climate Action, amending Regulations (EC) No 663/2009 and (EC) No 715/2009 of the European Parliament and of the Council, Directives 94/22/EC, 98/70/EC, 2009/31/EC, 2009/73/EC, 2010/31/EU, 2012/27/EU and 2013/30/EU of the European Parliament and of the Council, Council Directives 2009/119/EC and (EU) 2015/652 and repealing Regulation (EU) No 525/2013 of the European Parliament and of the Council

Riahi K, Grübler A, Nakicenovic N (2007) Scenarios of long-term socio-economic and environmental development under climate stabilization. Technol Forecast Soc Change 74:887–935

Shen L, Lou Y, Huang Y, Chen J (2018) A driving–driven perspective on the key carbon emission sectors in China. Nat Hazards 93(1):349–371

Suh S (2006) Are services better for climate change? Environ Sci Technol 40(21):6555–6560

Taliotis C, Giannakis E, Karmellos M, Fylaktos N, Zachariadis T (2020) Estimating the economy-wide impacts of energy policies in Cyprus. Energy Strategy Rev 29:100495

UNFCCC (2021) What is the Paris agreement? https://unfccc.int/process-and-meetings/the-paris-agreement/what-is-the-paris-agreement. Accessed 6 Apr 2021

van Vuuren DP, Stehfest E, den Elzen MGJ, Kram T, van Vliet J, Deetmanc S, Isaac M, Goldewijk KK, Hof A, Mendoza Beltran A, Oostenrijk R, van Ruijven B (2011) RCP26: exploring the possibility to keep global mean temperature increase below 2 °C. Clim Change 109(1):95–116

Wiedmann T (2009) A review of recent multi-region input–output models used for consumption-based emission and resource accounting. Ecol Econ 69(2):211–222

Winter KJPM, Kotlarski S, Scherrer SC, Schär C (2017) The Alpine snow-albedo feedback in regional climate models. Clim Dyn 48:1109–1124

Worrell E, Price L, Martin N (2001) Energy efficiency and carbon dioxide emissions reduction opportunities in the US Iron and steel sector. Energy 26(5):513–536

Xie X, Shao S, Lin B (2016) Exploring the driving forces and mitigation pathways of CO2 emissions in China’s petroleum refining and coking industry: 1995–2031. Appl Energy 184:1004–1015

Yuan Y, Wang Y, Chi Y, Jin F (2020) Identification of key carbon emission sectors and analysis of emission effects in China. Sustainability 12(20):8673

Zittis G (2018) Observed rainfall trends and precipitation uncertainty in the vicinity of the Mediterranean, Middle East and North Africa. Theor Appl Climatol 134:1207–1230

Zittis G, Hadjinicolaou P, Klangidou M et al (2019) A multi-model, multi-scenario, and multi-domain analysis of regional climate projections for the Mediterranean. Reg Environ Change 19:2621–2635

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

On behalf of all authors, the corresponding author states that there is no conflict of interest.

Appendix

Appendix

See Tables

2,

3 and

4.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Giannakis, E., Zittis, G. Assessing the Economic Structure, Climate Change and Decarbonisation in Europe. Earth Syst Environ 5, 621–633 (2021). https://doi.org/10.1007/s41748-021-00232-7

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41748-021-00232-7