Abstract

It is well known among practitioners that the seasonal adjustment applied to economic time series involves several decisions to be made by the econometrician. As such, it would always be desirable to have an informed opinion on the risks taken by each of those decisions. In this paper, I assess which disaggregation strategy delivers the best results for the case of the Chilean 1986–2009 GDP quarterly dataset (base year: 2003). This is done by performing an aggregate-by-disaggregate analysis under different schemes, as the fixed base year dataset allows this fair comparison. The analysis is based on seasonal adjustment diagnostics contained in the X-12-ARIMA program plus some statistical tests for robustness. This exercise is relevant for conjunctural economic assessment, as it concerns signal extraction from seasonal, noisy series, direction of change detection, and econometric applications based on reliable and accurate unobserved variables. The results show that it is preferable, in terms of stability, to use the first block of supply-side disaggregation, while demand-side disaggregation tends to be less reliable. This result carries important implications for policymakers aiming to evaluate its short-term effectiveness in both households and firms.

Source: Author’s elaboration based on Central Bank of Chile’s database

Source: Author’s elaboration

Source: Author’s elaboration

Similar content being viewed by others

Notes

Astolfi et al. (2001).

Notice that this article already offers an analysis with linked-chain dataset for robustness purposes.

See Findley et al. (1990) for more details on sliding spans diagnostics.

This assumption also refers to comparisons with same data vintages without revisions.

See, in the empirical application section, the cases of the supply sectors Capture fishery and Electricity, gas and water, to name a few, with respect to the case of GDP itself.

“Appendix C” displays the share of every sector of real GDP at 2003 prices, while “Appendix D” displays some typical statistics of sectors with the full sample for the transformations used in the analysis. “Appendix E” depicts all aggregation components in log levels to provide a general overview of their shape in the time domain.

There are several (pay licensed) software alternatives to estimate the spectrum. For instance, using the command pergram in Stata, or the command periodogram in Matlab.

Note that this component, despite its name, does not necessarily match the concept of trend in the traditional economics usage.

Whether the indirect adjustment performs better than the direct method is a matter treated in Sect. 2.1. In particular, for this case, some arguments are the use of different filters across the disaggregations and ad-hoc forecasting models with better out-of-sample performance.

References

Astolfi, R., Ladiray, D., & Mazzi, G. L. (2001). Seasonal adjustment of European aggregates: Direct versus indirect approach. Working Document 14 2001, Theme 1 General Statistics, Eurostat.

Banco Central de Chile. (2010). Cuentas Nacionales de Chile 2003–2009. Available at https://si3.bcentral.cl/estadisticas/Principal1/informes/CCNN/ANUALES/ccnn_2003_2009.pdf.

Bobbitt, L., & Otto, M. C. (1990). Effects of forecasts on the revisions of seasonally adjusted values using the X-11 seasonal adjustment procedure. In Proceedings of the business and economic statistics section. American Statistical Association (pp. 449–453).

Di Fonzo, T. (2005). The OECD project on revisions analysis: First elements for discussion. OECD short-term economic statistic expert group report.

Findley, D. F., Monsell, B. C., Bell, W. R., Otto, M. C., & Chen, B.-C. (1998). New capabilities and methods of the X-12-ARIMA seasonal-adjustment program. Journal of Business and Economic Statistics, 16(2), 127–152.

Findley, D. F., Monsell, B. C., Shulman, H. B., & Pugh, M. G. (1990). Sliding spans diagnostics for seasonal and related adjustments. Journal of the American Statistical Association, 85(410), 345–355.

Gómez, V., & Maravall, A. (1997). Programs TRAMO and SEATS, instructions for user (Beta Version: September 1996), Working Paper 9628, Bank of Spain.

Granger, C. W. J. (1979). Seasonality: Causation, interpretation, and implications. In A. Zellner (Ed.), Seasonal analysis of economic time series. New York: National Bureau of Economic Research.

Hood, C. C. H. (2007). Assessment of diagnostics for the presence of seasonality. In Proceedings of the international conference on establishment surveys III, June 2007.

Hood, C. C. H., & Findley, D. F. (2001). Comparing direct and indirect seasonal adjustments of aggregate series. In American statistical association proceedings.

Hood, C. C. H., & McDonald-Johnson, K. M. (2009). Getting started with X-12-ARIMA diagnostics. Catherine Hood Consulting. http://www.catherinechhood.net/papers/gsx12diag.pdf.

Kendall, M., & Ord, J. K. (1990). Time series (3rd ed.). Oxford: Oxford University Press.

Ladiray, D., & Mazzi, G. L. (2003). Seasonal adjustment of european aggregates: Direct versus indirect approach. In M. Manna & R. Peronacci (Eds.), Seasonal adjustment. Frankfurt: European Central Bank.

Lothian, J., & Morry, M. (1978). A set of quality control statistics for the X-11-ARIMA seasonal adjustment method. Research Paper. Statistics Canada

Maravall, A. (2002). An application of TRAMO-SEATS: Automatic procedure and sectoral aggregation. The Japanese Foreign trade series, Documento de Trabajo 0207, Banco de España.

Maravall, A. (2005). An application of the TRAMO-SEATS automatic procedure; direct versus indirect adjustment. Documento de Trabajo 0524, Banco de España.

Medel, C. A. (2014) A Comparison between direct and indirect seasonal adjustment of the Chilean GDP 1986-2009 with X-12-ARIMA. Working Paper 57053, Munich Personal RePEc Archive.

Otranto, E., & Triacca, U. (2002) A distance-based method for the choice of direct or indirect seasonal adjustment, mimeo. Istituto Nazionale di Statistica, Italy.

Otto, M. C. (1985). Effects of forecasts on the revisions of seasonally adjusted data using the X-11 seasonal adjustment procedure. In Proceedings of the business and economic statistics section. American Statistical Association (pp. 463–466).

Peronacci, R. (2003). The seasonal adjustment of euro area monetary aggregates: Direct versus indirect approach. In M. Manna & R. Peronacci (Eds.), Seasonal Adjustment. Frankfurt: European Central Bank.

Scheiblecker, M. (2014). Direct versus indirect approach in seasonal adjustment. Working Paper 460, Austrian Institute of Economic Research.

Soukup, R. J., & Findley, D. F. (1999). On the spectrum diagnostics used by X-12-ARIMA to indicate the presence of trading day effects after modeling for adjustment. American Statistical Association Proceedings.

Stanger, M. (2007). Empalme del PIB y de los Componentes del Gasto: Series Anuales y Trimestrales 1986–2002, Base 2003, Estudio Económico Estadístico 55, Banco Central de Chile.

US Census Bureau. (2011). X-12-ARIMA reference manual, version 0.3. Available at http://www.census.gov/srd/www/x12/.

Author information

Authors and Affiliations

Corresponding author

Additional information

I thank Rodrigo Alfaro, Carlos Alvarado, Mario Giarda, Pablo Medel, Michael Pedersen, Pablo Pincheira, Damián Romero, and two anonymous referees for comments and suggestions. I also thank Applied Econometrics II (second semester 2012) students at the University of Chile for comments. Finally, I thank Consuelo Edwards for editing services. X-12-ARIMA is a product of the US Census Bureau. This article constitutes an independent analysis on the use of a seasonal adjust procedure applied to a vintage of the Quarterly National Accounts of Chile. It does not reflect the official manner in which the Central Bank of Chile conducts the official data issuance nor a recommendation on how it should be performed. The views and ideas expressed in this paper do not necessarily represent those of the Central Bank of Chile or its authorities. Any errors or omissions are the author’s exclusive responsibility.

Appendices

Chilean GDP by Demand Side

See Table 8.

Chilean GDP by Supply Side

See Table 9.

Shares of Sectorial Components on Real GDP

See Table 10.

Typical Statistics of Time Series

GDP Components: Original Series in Levels

See Fig. 4.

Source: Author’s elaboration based on Central Bank of Chile’s database

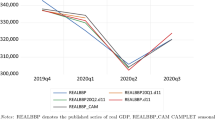

Chilean GDP—Original series in logarithmic levels.

Diagnostic Result 1

1.1 Spectral Plots of Final Seasonally Adjusted and Irregular Series

Source: Author’s elaboration

Spectral plots of final seasonally adjusted series. 10 \({\times }\) (log-diff.). Bartlett window length = 30.

Source: Author’s elaboration

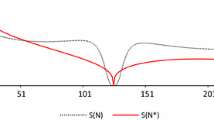

Spectral plots of irregular series. Bartlett window length = 30.

Diagnostic Result 3

1.1 Revision History of Trend-Cycle and Final Seasonally Adjusted Series

Source: Author’s elaboration

Revision history of trend-cycle series (log-differenced). \({\blacktriangledown }\) = Most recent.

Source: Author’s elaboration

Revision history of seasonally adjusted series (log-differenced). Aggregation 3 contains an outlier at 2008.III: from − 106.9 (concurrent) to − 0.4 (most recent) \({\blacktriangledown }\) = Most recent.

Diagnostic Result 1: Linked-Chain Dataset

1.1 Spectral Plots of Final Seasonally Adjusted and Irregular Series

Source: Author’s elaboration

Spectral plots of final seasonally adjusted series. 10 \({\times }\) (log-diff.). Bartlett window length = 30.

Source: Author’s elaboration

Spectral plots of irregular series. Bartlett window length = 30.

Rights and permissions

About this article

Cite this article

Medel, C.A. A Comparison Between Direct and Indirect Seasonal Adjustment of the Chilean GDP 1986–2009 with X-12-ARIMA. J Bus Cycle Res 14, 47–87 (2018). https://doi.org/10.1007/s41549-018-0023-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41549-018-0023-3