Abstract

This study empirically investigates the relationships of control levers (belief and boundary systems, Simons 1995) and control context (social and performance management context, Gibson and Birkinshaw 2004) with contextual ambidexterity and firm performance. Based on cross-sectional survey data from 198 listed companies in Austria, Germany, and Switzerland, a structural equation model is used to test the hypothesized relationships. We find that the emphasis on formal boundary systems and an informal social context are positively related to contextual ambidexterity, which positively affects firm performance. In contrast, belief systems and performance management context do not influence contextual ambidexterity. Further, we find no support for dynamic tensions, neither between the two control levers nor in the control context.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

The idea that successful organizations in a dynamic environment are ambidextrous—aligned in managing their current business demands while being adaptable to changes in the environment—frequently recurs in various organizational literature streams (e.g., Duncan 1976; Gibson and Birkinshaw 2004; Tushman and O’Reilly 1996). Organizations require certain capabilities to enable resilience including both flexibility for adapting as well as robustness to remain solid when confronted with adversity (Iborra et al. 2020; Wang et al. 2021). Resilience as a multifaceted and multi-level construct is relevant on an individual, a team, as well as on an organizational level. We focus here on resilience on an organizational level, where it is increasingly emphasized that successful organizations manage alignment and adaptability simultaneously in order to reach a high level of resilience (Duncan 1976; Gibson and Birkinshaw 2004; He and Wong 2004; Lubatkin et al. 2006; Raisch and Birkinshaw 2008; Tushman and O’Reilly 1996). The capability to manage the two activities simultaneously is defined as contextual ambidexterity (Gibson and Birkinshaw 2004).

Our study investigates the role of the organizational context for resilience building by involving systems, processes, and beliefs that facilitate individual behaviors of managers and employees (Burgelman 1983; Ghoshal and Bartlett 1994; Gibson and Birkinshaw 2004) to achieve contextual ambidexterity. First, we argue that Gibson and Birkinshaw’s (2004) performance management and social contexts, realizable in the long term, can facilitate contextual ambidexterity. Second, our study expands the concept of Gibson and Birkinshaw’s (2004) supportive organizational context, acknowledging that additional short-term implementable antecedents are necessary for a holistic, supportive context. Drawing on Simons’ (1995) levers of control framework, we explored whether the two control levers belief and boundary systems are antecedents of contextual ambidexterity, complementing the control context consisting of social and performance management context. We understand contextual ambidexterity as a key strategic priority of organizations to build resilience (e.g., Bedford 2015) and consider the application of the control levers and the specific control context as ways to execute the strategy through the creation of contextual ambidexterity (Lorange 1998). Thus, we empirically investigate the relationship between control levers (belief and boundary systems) and control context (social and performance management context)—together considered as organizational context—contextual ambidexterity and firm performance.

Our results suggest that a formal boundary system and an informal social context positively relate to contextual ambidexterity. In contrast, belief systems and performance management context do not influence contextual ambidexterity. To support our results, we tested dynamic tensions between belief and boundary systems, representing a combined approach for the short-term control lever and between the social and performance management context, reflecting the long-term control context. We found no support for dynamic tensions.

We contribute to the existing control and ambidexterity literature in several ways. First, this study examines several antecedents of contextual ambidexterity, including performance management context, social context, boundary, and belief system, and their effects on firm performance. By adding to the work of Bedford (2015) and Kruis et al. (2016), we contribute to the understanding of how the levers of control framework foster ambidexterity on a company level and expand the concept of the organizational context of Gibson and Birkinshaw (2004). Second, building on dynamic tensions the study contributes how antecedents operate jointly to develop contextual ambidexterity.

The paper proceeds as follows. We review the existing literature on contextual ambidexterity and explain our understanding of an organizational context. We then present the conceptual model. Subsequently, we summarize the empirical analysis of the hypotheses with a structural equation modeling approach. Finally, we evaluate the results, discuss the limitations, and indicate avenues for future research.

2 Theoretical Background

2.1 Contextual Ambidexterity

Organizations engage in two activities, aligning existing capabilities and adapting to environmental changes (Duncan 1976; Gibson and Birkinshaw 2004; Tushman and O’Reilly 1996). An organization’s ability to manage those two activities is referred to as ambidexterity, the term first used by Duncan (1976). Gibson and Birkinshaw (2004) developed the framework of contextual ambidexterity. Alignment refers to the coherence of all activities of an organization, whereas adaptability describes the capability to react to changing demands by reconfiguring operational activities (Gibson and Birkinshaw 2004). Contextual ambidexterity establishes “both/and-thinking” in terms of an organization’s or business unit’s behavioral capability to simultaneously focus on alignment and adaptability (Gibson and Birkinshaw 2004). Processes or systems that enable and encourage employees to judge individually about dividing their time build the basis of the behavioral capability to simultaneously focus on alignment and adaptability (McDonough and Leifer 1983; Tushman and O’Reilly 1996).

Contextual ambidexterity is characterized by decentralized decision-making at the business front line. Hence, the management’s role is to develop a supportive organizational context in which individuals act. To safeguard an appropriate organizational context, the management board, in coordination with the supervisory board, has to decide on the necessary actions to be taken. This organizational context involves systems, processes, and beliefs facilitating individual behaviors (Burgelman 1983; Ghoshal and Bartlett 1994; Gibson and Birkinshaw 2004). It requires more flexible systems and structures that allow motivated employees to act and decide quickly in the company’s best interest when new opportunities arise (Gibson and Birkinshaw 2004). Gibson and Birkinshaw (2004, p. 211) emphasize the “need for a behavioral orientation” i.e., the design of a supportive organizational context (see Sect. 2.2).

Prior literature has subsequently explored the positive effects of ambidexterity in the area of sales growth (e.g., He and Wong 2004; Lin et al. 2007), firm performance (e.g., Gibson and Birkinshaw 2004; Han and Celly 2008; Lubatkin et al. 2006; Luger et al. 2018; Stouthuysen et al. 2017), innovation (e.g., Adler et al. 1999; Del Giudice et al. 2021; Revilla and Rodríguez-Prado 2018; Rothaermel and Alexandre 2009), research and development activities (e.g., Geerts et al. 2018; McCarthy and Gordon 2011), market valuation (e.g., Wang and Li 2008), firm survival (e.g., Cottrell and Nault 2004; Hill and Birkinshaw 2014), and cost of equity capital (Matthews et al. 2022). March (1991) argues that an organization focusing on two conflicting activities runs the risk of being mediocre at both, and simultaneously balancing two activities increases the organization’s reconcilement cost (e.g., Benner and Tushman 2002). Other empirical studies have claimed that ambidexterity has no effect on firm performance (e.g., Ebben and Johnson 2005; O’Reilly and Tushman 2013). Their reasoning contradicts the argument that companies that focus solely either on alignment or adaptability will be confronted with problems and tensions due to invariably or inflexibilities since focusing on one of these is always at the expense of the other (March 1991). We follow the argumentation that ambidexterity is a key driver of the short- and long-term success of organizations due to resilience (Gibson and Birkinshaw 2004; Iborra et al. 2020; Lubatkin et al. 2006; Wang et al. 2021).

2.2 Organizational Context

Ghoshal and Bartlett (1994) classify organizational context into four behavioral attributes: discipline, stretch, support, and trust. Gibson and Birkinshaw (2004) formed a performance management context in which discipline and stretch represent behavioral components and support and trust represent a social context. Discipline relates to the organizational context and objectives to commit employees to voluntarily meet all expectations. It establishes clear standards of performance and behavior; a system of open, candid, and rapid feedback; and consistency in applying sanctions support the establishment of discipline. Stretch induces members to strive for ambitious objectives voluntarily through sharing the same ambitious goals, having a collective identity, and having the sense to work together for organizational purposes (Gibson and Birkinshaw 2004). Support refers to mechanisms that encourage employees to assist and support others. Trust in management activities encourages employees to rely on the commitment of management and each other (Ghoshal and Bartlett 1994; Gibson and Birkinshaw 2004).

Gibson and Birkinshaw (2004) do not explicitly specify the time horizon required to implement a performance management context and a social context within an organization. Rather, they emphasize the importance of achieving a balance between the constructs to prevent unintentional overbalancing. Thus, we assume a long period to establish an environment that encourages individuals to push for ambitious goals within a cooperative environment. We refer to it as a long-term implementable control context.

In addition, an organization has significant control levers to influence the organizational context in the short term. We concentrate on Simons’ (1995) belief and boundary systems, as they contribute to the design of a supportive organizational context: “Beliefs systems create norms and serve as cultural ideals. The rules embodied in boundary systems both create and are created by the culture of an organization” (Simons 1995, p. 57). The organization can exercise the control lever boundary system by influencing the boundaries of employees’ actions (Simons 1995) or developing a context by shaping methodologies and processes in accordance with an organization’s objectives (McNulty and Pettigrew 1999). The belief system can be elaborated by appointing and dismissing the management board members, supervised activities, and the management board’s advice and involvement in the company’s strategy. This results in considerable organizational design opportunities to achieve contextual ambidexterity.

3 Conceptual Model and Hypothesis Development

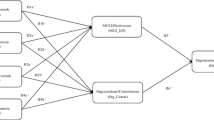

We hypothesize that belief systems, boundary systems, a performance management context, and a social context positively relate to contextual ambidexterity (Chap. 3.1). Moreover, the model assumes a positive relationship of performance management context and contextual ambidexterity with firm performance (3.2). Fig. 1 illustrates the theoretical model.

Hypothesized structural model

3.1 Organizational Context and Contextual Ambidexterity

3.1.1 Belief Systems

Belief systems address the behavioral component of management controls with an “explicit set of organizational definitions that senior managers communicate formally and reinforce systematically to provide basic values, purpose, and direction for the organization” (Simons 1995, p. 34). Simons argues that belief systems, such as mission statements, credos, and statements of purpose (Simons 1994, 1995), have an explicit effect on the motivation and encouragement of employees (Widener 2007). Thus, belief control systems are presumed to positively affect a firm’s capability for aligning and adapting activities. They positively force employees to align with firm values to achieve business goals and encourage them to approach new ideas, as “the purpose of a belief system is to inspire organisational search and discovery without prescribing the precise nature of the activities” (Mundy 2010, p. 501). Belief systems motivate individuals, which prevents organizational inertia (Simons 1995). Ideally, motivation leads to an “internalization of values and strategic intent” (Bedford 2015, p. 16) to streamline valuable projects and efforts. Belief systems are, thus, assumed to play a vital role in contributing to corporate entrepreneurship by encouraging people of the entire organization to use their creativity (Davila et al. 2009). Especially a highly competitive environment requires employees “to discover and make emerge the big ideas of the future”, which are especially important “to attract and retain entrepreneurs within large established firms or to help people become more ambidextrous” (Davila et al. 2009, p. 300). The long-term success of an organization thus might depend on intrapreneurs and their ambidextrous orientation. Heinicke et al. (2016) further argue that the more organizations emphasize a flexible culture, the more they focus on belief controls. Building on Henri (2006a), a flexible culture emphasizes flexibility values. As a positive and inspirational control, belief systems allow employees to respond quickly to new market developments and a changing business environment according to flexibility values (Heinicke et al. 2016; Henri 2006a). However, to foster ambidexterity, “a clear and compelling vision, relentlessly communicated by a company’s senior team, is crucial in building ambidextrous designs” (O’Reilly and Tushman 2004, p. 81). Also, Jansen et al. (2008) emphasize the relevance of a strong shared vision for ambidextrous organizations.

Consequently, we propose:

H1

The use of belief systems positively affects contextual ambidexterity.

3.1.2 Boundary Systems

The boundary systems describe formal control mechanisms referring to the organizational activity (Simons 1995). Boundary systems set rules for employees’ behavior and specify strategic activities by predefining the scope of opportunity search, directing employees’ attention towards business operations (Simons 1995) that positively influence firm performance (Frow et al. 2010). To limit opportunity-seeking behavior, organizations use negative or minimum terms to establish boundaries (Simons 1995). By communicating these, employees are in a better position to work towards an organization’s goal without wasting resources; therefore, they “help to direct activities to a meaningful end-point, preventing employees from seeking continual improvements beyond optimal and timely solutions” (Mundy 2010, p. 501). Although boundary systems may restrict the organization’s scope of maneuver, the presence of boundary systems does not necessarily need to be accompanied by employees’ loss of motivation or empowerment (Adler and Chen 2011; Frow et al. 2010). Instead, budgets, for example, help companies by serving as a control system, as the benefits of budgets tend to exceed the costs. In addition, budgets allow organizations to continuously adjust to internal and external requirements and strategic goals (Libby and Lindsay 2010). Budgets, therefore, also create an important opportunity to enhance employees’ motivation and participation through decentralized decision-making structures and the implementation of lean processes. This constrained autonomy encourages employees to focus on pivotal performance aspects with respect to short- and long-term operations (Bedford 2015). Best practices may guide employees to achieve organizational goals but still provide sufficient space for flexibility or adjustments while relying on prior accumulated knowledge and reliable routines. Organizational learning literature has shown that repeated activities and their incremental improvement increase effectiveness and efficiency (Levinthal and March 1993; Levitt and March 1988; March 1991). It is assumed that boundary systems force managers to unlearn yesterday’s procedures to adapt to tomorrow’s challenges, which indicates a direct relationship with adaptation (Bedford 2015; Simons 1994). As strategic renewal is fundamental for organizations to secure their survival, boundary systems “permit discovery and learning, but within clearly defined limits of freedom” (McCarthy and Gordon 2011, p. 247). In addition, boundary systems provide direction as feedback control (Bedford 2015; McCarthy and Gordon 2011). Hence, we expect a positive influence of boundary systems in terms of aligning and adapting activities of an organization.

Consequently, we propose:

H2

The use of boundary systems positively affects contextual ambidexterity.

3.1.3 Social Context

More complex market circumstances force companies to avert strategic inertia by continuously developing and evolving new competencies. From a behavioral perspective, for example, management-employee alertness, openness to change, and knowledge exchange allow organizations to explore new strategic renewal approaches (Hess and Hess 2016). Continuous development of dynamic capabilities must complement strategies to escape organizational inertia (Doz 2007; Floyd and Lane 2000; Huff et al. 1992). The social context and behavioral orientation are important to reconfigure knowledge and competencies toward an organization’s strategic renewal and adaptability. Bottom-up learning and internal selection precede successful changes in the organizational domain (Burgelman 1991). However, this approach is difficult to achieve, as employees tend to focus on aligning competencies rather than developing new ones (Levinthal and March 1993; March 1991). The social context, therefore, serves as an important catalyst and support function for implementing ambidextrous behavior (Gibson and Birkinshaw 2004; Hess and Hess 2016). We assume that the collaborative component of support in management activities fosters the development of alignment, for example, by the collaborative access of resources and the approach of providing guidance and helping others. We also hypothesize that a high level of support helps establish adaptability, for example, by prioritizing freedom of employees’ initiatives on a lower level. Furthermore, it is assumed that a high level of trust in management activities positively influences the development of alignment, such as the involvement of employees in decisions and activities affecting them. Trust-related mechanisms, such as revolutionary decisions on staffing vacancies with employees who were not seen to have the required capabilities for the new role, positively affect adaptability (Ghoshal and Bartlett 1994; Gibson and Birkinshaw 2004).

Consequently, we propose:

H3

The more a firm’s social context is characterized by support and trust, the higher the level of contextual ambidexterity.

3.1.4 Performance Management Context

The establishment of behavioral components in management processes is defined as performance management context, representing a combination of discipline and stretch (Gibson and Birkinshaw 2004). The attribute discipline establishes an open feedback system and clear standards of behavior. Thus, discipline is expected to have a positive influence on alignment. It is assumed that a high level of stretch fosters the establishment of alignment through the development of collective identity and a shared ambition. Furthermore, the attribute stretch has a positive association with adaptability likely due to the voluntary tendency to achieve more ambitious objectives (Ghoshal and Bartlett 1994; Gibson and Birkinshaw 2004). The overarching common goal to exceed expectations enhances and contributes to understanding organizational effectiveness and efficiency. Alignment and adaptability within contextual ambidexterity must be attained simultaneously by individuals deciding how to divide their time between both activities (Gibson and Birkinshaw 2004). Myopic decisions occur if individuals are neither disciplined nor stretched, resulting in decreased efficiency and effectiveness. Besides the assumed positive effect on firm performance, establishing discipline and stretch in organizational contexts is supposed to foster the development of alignment and adaptability, resulting in contextual ambidexterity.

Consequently, we propose:

H4

The more a firm’s performance management context is characterized by discipline and stretch, the higher the level of (a) firm performance and (b) contextual ambidexterity.

3.2 Contextual Ambidexterity and Firm Performance

Following the concept of contextual ambidexterity, both alignment and adaptability are key drivers for companies to sustain future success (Gibson and Birkinshaw 2004). Aligning activities foster sustainable performance in the short term, whereas adapting activities enable firm performance in the long term (Gibson and Birkinshaw 2004). A significant body of research has discussed the balance between alignment and adaptability in different approaches (Bedford 2015; Levinthal and March 1993; March 1991; McCarthy and Gordon 2011; Oehmichen et al. 2017; O’Reilly and Tushman 2013; Raisch et al. 2009). March (1991) argues that not focusing on alignment and adaptability simultaneously prevents adaptive business units from capturing the cost of experimentation along with proper corresponding results, which fosters the fractionation of an organization. Consequently, a balance is critical for firm survival (March 1991). As a result, contextual ambidexterity should be a key driver of firm performance, considering both a short-term and long-term perspective of business success (Gibson and Birkinshaw 2004).

Consequently, we hypothesize:

H5

The higher the level of contextual ambidexterity, the higher the level of firm performance.

4 Research Methodology

This study’s research methodology and design requires verifying theoretical and logical derived relationships between various unobservable variables. Consequently, the applied research requires a structure-testing methodology being suitable (a) evaluate an a‑priori defined system of hypotheses, whereas the direction and strength of the effects are quantified, and simultaneously (b) perform the hypotheses testing, leading to indirect effects and complex relationships. Structural equation modeling (SEM), as multivariate data analysis, meets these requirements, and we thus applied it as this study’s research methodology (Hair et al. 2010).

4.1 Data and Sampling

A structured questionnaire was developed to test the formulated hypotheses, ensuring high representativeness of the study. Data were collected between January and June 2015 via online and paper-based questionnaires to increase the response rate.Footnote 1 The surveys were administered to supervisory board members from listed companies in Germany, Austria, and Switzerland. Supervisory board members also play a pivotal role in designing an organizational context and ambidextrous organization. They can apply this via their formal and informal role (Katz and Kahn 1978) and social relationships (Carpenter 2002; Dutschkus and Lukas 2022). The board members can decide their role-making or role-taking based on the respective organization, ownership structure, self-understanding of the board, relationships with management, and other variables. Formally they are obliged to take an active role in enabling and shaping contextual ambidexterity. Role responsibilities in supervision and their effects on decisions are formalized in different intensities based on the national legal system. In Germany and Austria, the board system is two-tiered. A supervisory board controls and advises the management board (GCGCFootnote 2 principle 6; Sect. 111 para. 1 GSCAFootnote 3; Sect. 95 para. 1 ASCAFootnote 4). It is involved in aligning important organizational decisions with the management board (GCGC principle 2; ACGCFootnote 5 III. 11.) and appointing and dismissing the management board (Sect. 84 para. 1 GSCA; Sect. 84 para. 3 GSCA; Sect. 75 para. 1 ASCA; Sect. 75 para. 4 ASCA). The Swiss board is a one-tier system responsible for the overall management and control of the company (art. 716a para. 1 COFootnote 6). An additional duty is to appoint and dismiss persons entrusted with managing and representing the company (art. 716a para. 1 CO).Footnote 7 The platform Amadeus Orbis was used to identify the listed companies. Selected firms had to have a minimum of € 20 million in revenue or market capitalization or at least 1000 employees to ensure that organizational and structural variables were applied (Miller 1987) and advanced control systems were present (Bouwens and Abernethy 2000; Henri 2006b).

Approximately 4500 supervisory board members from 898 companies were contacted and invited to participate in the online or paper-based survey. The questionnaire was pre-tested by six academic professionals and six supervisory board members, resulting in minor changes involving the rewording and reordering of the questions. Several reminder emails were sent out to the invited supervisory board members to increase the study’s response rate.Footnote 8 The process yielded 274 responses from 198 firms with an effective response rate of 22.04% on a company level.Footnote 9 We tested for non-response respectively early-late response bias, as late respondents are assumed to have comparable characteristics to non-respondents (Van der Stede et al. 2006). Table 1 shows no statistical differences between early and late respondents.

Most responses were from the Industrials industry (26.8%), Financials industry (15.2%), and Consumer Services industry (14.1%). Table 2 provides an overview of the participating industries represented in the data. The respondents’ industry structure did not materially deviate from the sample’s industry structure.

4.2 Measurement of Reflective Constructs

We used reflective and previously validated multi-item constructs measured on a seven-point Likert scale to test our model. Gibson and Birkinshaw’s (2004) items were included to operationalize the social and performance management context. The items were adopted from Ghoshal and Bartlett’s (1994) instrument to capture the effects of the organizational context created by managerial actions on a company’s management processes. Although Gibson and Birkinshaw (2004) identified the distinctive dimensions of discipline, stretch, support, and trust, they adapted and combined the questions to represent the performance management context by discipline and stretch and social context by support and trust, as their factor analysis yielded a two-factor approach. In the next step, we combined both measures. We formed an interaction term to model a joint effect of performance management and social context to address dynamic tensions between the two constructs. Considering both constructs from a not substitutable perspective, this variable represents our measure for control context which is operationalized as a product term (Kenny and Judd 1984).

Concerning the management control perspective of the organizational context, we used Widener’s (2007) previously validated measures of belief systems and boundary systems. Managers communicate the company’s core values, mission statement, and core purpose they want their employees to embrace. These belief systems shape the organization’s value proposition (Simons 1995; Widener 2007). In contrast, boundary systems “set limits on opportunity-seeking behavior” (Simons 1995, p. 7). The variable comprises four items that ask respondents about the presence of a code of business conduct, off-limits behaviors, and risks to be avoided. Furthermore, we investigate the interaction between belief systems and boundary systems representing our control lever because the combination of management controls creates dynamic tensions (Henri 2006b; Mundy 2010; Simons 1995).

Following Gibson and Birkinshaw (2004), we measured contextual ambidexterity with the two constructs alignment and adaptability with three items each. Alignment captures the extent to which management systems work coherently to support the company’s overall objectives and people working towards the same goals, avoiding conflicting and unproductive activities. To reflect a company’s adaptability, we measured the flexibility of management systems to respond quickly to changes in markets and people’s capability to challenge outmoded traditions and practices.

We combined both constructs to analyze the effects of each organizational context construct on contextual ambidexterity, as contextual ambidexterity assumes their combined effects. Studies have used different approaches to model contextual ambidexterity out of alignment and adaptability, such as a product term of the two (Cao et al. 2009; Gibson and Birkinshaw 2004; He and Wong 2004), taking the difference between the two (He and Wong 2004), or adding the two (Cao et al. 2009; Lubatkin et al. 2006). Lubatkin et al. (2006) empirically concluded that the additive approach leads to superior results, as the information loss is minimized by aggregating alignment and adaptability into a single latent variable. We followed this procedure and measured contextual ambidexterity out of alignment and adaptability (i.e., all six indicators). The Cronbach’s alpha of this single latent variable contextual ambidexterity is 0.873.

We expected most participants to be reluctant to provide detailed accounting data. Therefore, we applied subjective, self-reported performance measures. Research has demonstrated that subjective performance measures correlate highly with objective performance measures (Dess and Robinson 1984; Robinson and Pearce 1988; Venkatraman and Ramanujam 1987). Organizational performance is a fundamental domain of management research and must address two important aspects: (1) the accurate dimensionality of performance and (2) the appropriate performance measurement (Richard et al. 2009). Our performance measure comprises five items reflecting financial and non-financial dimensions. Respondents evaluated the company’s performance relative to their main competitors for each item. Relative performance measures consider performance differences due to external and internal environment influences (Garg et al. 2003). Therefore, the indicators sales, market share, profitability, customer satisfaction, and employee satisfaction were assessed on a seven-point Likert scale to measure low and high performance (1 = ‘Much Worse’ for low; 7 = ‘Much better’ for high). We asked the participants to evaluate the performance measures over the last three years to control for short-term performance effects.

4.3 Reliability, Validity, and Common Measurement Bias for the Reflective Constructs

We used existing and validated measurements for all constructs and verified the range of responses, exploratory and confirmatory factor analysis, and reliability measures for the reflective constructs. All Cronbach’s alpha coefficients exceed the commonly accepted threshold of 0.7, validating the reliability of the internal consistency of the questionnaire (Nunnally 1978). All factor loadings are significant (p < 0.001), all individual item reliabilities exceed the threshold of 0.4 (Bagozzi and Baumgartner 1994), all composite item reliabilities exceed the threshold of 0.6 (Bagozzi and Yi 1988), and the variance extracted exceeds the threshold of 0.5 (Hair et al. 2010). Table 3 summarizes the results. The correlation matrix between the constructs is displayed in Table 4.

Since survey research is prone to a common measurement bias (Chang et al. 2010; Podsakoff et al. 2003), we addressed the problem ex-ante through the survey design and ex-post using statistical control measures. Harman’s single factor test conducted with all items showed that the common factor accounts for 40% of the common variance, which is below the common threshold of 50%. Hence, we conclude little indication of common measurement bias. Although our respondents were conscious of questions assessing the organizational context, they were not likely to know that we are investigating the relationship between organizational context, contextual ambidexterity, and firm performance, reducing the likelihood of response bias. In addition, we pre-tested the questionnaire with experts to provide a clear and comprehensive assessment. To analyze the remaining bias after the data collection, we performed an exploratory factor analysis illustrated in Table 5.

5 Data Analysis

5.1 Statistical Method

We use the AMOS software program, version 27, to investigate a system of relations described in the conceptual model and hypothesis development section. Therefore, a structural equation model was estimated to investigate the underlying equations with the maximum likelihood estimation approach. According to Hair et al. (2011), the covariance-based structural equation modeling method is more robust and precise for theory testing than other methods, such as the variance-based approaches (partial least square method) or multiple regression analysis. The covariance-based method assesses the global model fit and the entire equation system instead of only single regression paths between the latent variables. According to Kline (2016), structural equation models force a decision about a model’s satisfaction and provide the opportunity to investigate both manifest or observed and latent or unobserved constructs (Byrne 2010). To evaluate the model fit, we use the common goodness-of-fit indices, Chi-Square divided by the degrees of freedom (χ2/df), the comparative fit index (CFI), and the root mean squared error of approximation (RMSEA). All goodness-of-fit-statistics meet the commonly accepted thresholds, indicating that the hypothesized model fit the data well.

5.2 Structural Equation Model

We test our developed hypotheses using a structural equation model (SEM). Table 6 presents the SEM path coefficients for the base model. The goodness-of-fit-statistics for the model meet the commonly accepted minimum thresholds (χ2/df = 1.910; CFI = 0.942; RMSEA = 0.068) and indicates a significant χ2 (χ2 = 446.830; p < 0.001) (Browne and Cudeck 1992; Byrne 1989; Hair et al. 2010; Hu and Bentler 1999). Thus, we conclude a good fit between the hypothesized model and the empirical data.

H1 posits that the belief system is positively related to contextual ambidexterity. The result is negative and insignificant. Thus, the hypothesis is not supported. This means that a common vision or mission of the company does not influence contextual ambidexterity. The results reveal a positive and significant association between boundary system and contextual ambidexterity (H2: coef. = 0.252, p = 0.001), providing support for H2. The results indicate that the social context is positively and significantly associated with contextual ambidexterity (H3: coef. = 0.737, p < 0.001), providing support for H3. H4a proposes that the performance management context is positively related to firm performance. The results show no direct relationship.

The coefficient for H4b is insignificant; therefore, the hypothesis is not supported. H5 is supported, as the effect of contextual ambidexterity on firm performance is positive (H5: coef. = 0.390, p < 0.001). The trimmed model includes only the significant relationships of boundary systems and social context with contextual ambidexterity and between contextual ambidexterity and firm performance. The trimmed model confirms the results revealing significant relationships between the boundary system and contextual ambidexterity (coef. = 0.227, p < 0.001), social context and contextual ambidexterity (coef. = 0.657, p < 0.001), and contextual ambidexterity and firm performance (coef. = 0.446, p < 0.001). The final trimmed model has a good fit, with χ2/df = 2.102; CFI = 0.9557; RMSEA = 0.075. To check our results for robustness, we use additional models that account for dynamic tensions between organizational context variables.Footnote 10 We run the models with both individual constructs and the dynamic tension term. We, first, assume a dynamic tension between the belief and boundary systems, also referred to as the control lever. A positive association between control levers and contextual ambidexterity is not indicated. Second, a dynamic tension between social and performance management context, considered as control context is also not confirmed.

6 Discussion and Conclusion

An important topic for management research is the capability to be resilient, to overcome from, and to move forward when faced with a threatening and challenging external event (Iborra et al. 2020; Wang et al. 2021). To achieve resilience contextual ambidexterity, the ability to simultaneously manage aligning and adapting activities, is considered a necessity to efficiently respond to the changing environments. The main objective of this study is to provide empirical evidence for the relationship between control levers (belief and boundary systems) and control context (social and performance management context)—together considered as organizational context—contextual ambidexterity and firm performance. We used structural equation modeling to gain insights into the antecedents and influence of contextual ambidexterity in organizations. The model supports the existence of a positive relationship between contextual ambidexterity and firm performance. Our theory and findings have several implications for theory and practice.

First, contextual ambidexterity mediates the relationship of social context and boundary systems with performance. In contrast, belief systems and performance management context do not affect contextual ambidexterity. The results indicate that a common mission and vision do not set the direction of an organization, which is, instead, embedded in a long-term social context, where managers use various instruments, such as information sharing, employee development, or a culture of constructive criticism, to achieve an organization’s goals. A further explanation could be that social context requires a long period to become embedded in organizational culture. The social context thus might be superior to other antecedents, as managers and employees come to appreciate prevailing norms that serve as guidance (Bedford and Malmi 2015; Chatman 1991; Harrison and Carroll 1991). A social context characterized by trust and support seems more relevant than a performance management context characterized by discipline and stretch. A supervisory board member should be an informed discussion partner for top management and not only an approval body. This implies that board members should not serve only a supervisory role but also actively and responsibly shape the control context. Thus, our paper extends the work of Gibson and Birkinshaw (2004) by adding the two control levers, boundary, and belief system (Simons 1995), highlighting the importance of giving clear directions and providing leeway for implementation. Taking a look at the effects’ strength, the social context seems to be much stronger than boundary systems—not very surprisingly, as we assume resilient companies to have a strong focus on social context aspects within their organizational context.

Second, following Gibson and Birkinshaw’s (2004) results, we expected a dynamic tension between performance management context and social context. Our study fails to support this hypothesis. Furthermore, we investigate the relationship between belief and boundary systems by modeling a dynamic tension. Simons (1994, 1995) states that a company’s belief and boundary systems work as yin and yang to implement a strategy effectively. Our study found no association between the dynamic use of belief and boundary systems concerning contextual ambidexterity. This is in line with the results of Bedford (2015); however, it contradicts our prediction that balance is important and can be reached via either control levers or control context. Instead of a dynamic tension, the social context might dominate the performance management context. The same might apply for the relationship between the belief and boundary system.

Although our study increases the understanding of contextual ambidexterity, it has limitations. The study examines the relationship between contextual ambidexterity and firm performance by applying part of Simon’s (1995) levers of control framework and the organizational context framework based on Ghoshal and Bartlett (1994). However, incorporating other factors that support the mediation of contextual ambidexterity could lead to a more comprehensive understanding. Studies focusing on the TMT research field (e.g., Koryak et al. 2018; Mihalache et al. 2014; Shi Tang et al. 2021; Van Neerijnen et al. 2021), CEO (Kiss et al. 2020; e.g., Ou et al. 2018; Wang et al. 2019) or individual-specific characteristics (e.g., Kauppila and Tempelaar 2016; Revilla and Rodríguez-Prado 2018; Tempelaar and Rosenkranz 2019; Zimmermann et al. 2018) have also identified an effect on (contextual) ambidexterity. Further, the measurement of latent variables might ignore additional aspects that contribute to a more holistic understanding. Especially, a company’s social context might differ across countries. Hence, the results of the study are limited to sample firm’s that are listed in Austria, Germany, and Switzerland. Cross-sectional studies or the investigation of industry-specific aspects might produce different results. Applying a structural equation model using the covariance approach depends on the number of observations, which in our case did not allow group or industry comparisons. Even though we took special care to validate the questionnaire with scientific experts and practitioners, we are also well aware of the difficulties of collecting the data via an online survey, as common method bias might have affected the results. Nevertheless, statistical tests do not indicate common method bias concerns.

Despite the aforementioned limitations, our results have important implications, also for practice. Key success factors for the development of contextual ambidexterity can guide organizations towards a successful corporate structure in terms of organizational context. The effect of the control lever boundary systems indicates that limiting risks within a company is important. Boundary systems, including proscriptive and negative systems, allow decision delegation and flexibility within an organization (Simons 1995). As Gibson and Birkinshaw (2004) indicate, contextual ambidexterity on the business unit level leads to superior performance, providing further evidence to tackle contextual ambidexterity on the company level.

In summary, contextual ambidexterity appears to be a dynamic capability for organizations to foster their resilience and thus their short- and long-term success. The complex organizational context factors that must be managed within the company’s environment show mixed results. Accordingly, future studies could aim to obtain a more granular view of contextual factors shaping an ambidextrous organization to reach a high degree of resilience.

Notes

Eight respondents chose the paper-based option.

German Corporate Governance Code (Deutscher Corporate Governance Kodex, “GCGC”).

German Stock Corporation Act (Aktiengesetz, “GSCA”).

Austrian Stock Corporation Act (Aktiengesetz, “ASCA”).

Austrian Corporate Governance Code (Österreichischer Corporate Governance Kodex, “ACGC”).

Swiss Code of Obligations (Obligationenrecht, “CO”).

To make sure that this does not affect our data analysis, we have also run the model without the Swiss companies. No significant differences were found.

The investor relations department was asked via phone to forward the invitation to the supervisory board member. In addition, email addresses were retrieved from the company’s websites. We don’t know how many supervisory board members actually received the questionnaire.

As the study focuses on the company level, the questionnaires were aggregated. The maximum number of received questionnaires did not exceed seven responses per company. Irrational and incomplete questionnaires were excluded for statistical and logical reasons. Only two questionnaires were excluded overall.

To operationalize dynamic tension, we apply the factor method suggested by Henri (2006b). Therefore, we used a product term, multiplying each latent indicator of the construct social context with each of the latent indicator of the construct performance management context. Following Cortina et al. (2001), this product term can be treated without any theoretical meaning to test an interaction between the two constructs without theoretical foundation of the construct. We apply the same procedure with respect to the creation of a dynamic tension between belief and boundary systems. Concerning the contextual ambidexterity, we incorporate the joint effect using an additive term suggested by Lubatkin et al. (2006).

References

Adler, P.S., and C.X. Chen. 2011. Combining creativity and control: Understanding individual motivation in large-scale collaborative creativity. Accounting, Organizations and Society 36(2):63–85. https://doi.org/10.1016/j.aos.2011.02.002.

Adler, P.S., B. Goldoftas, and D.I. Levine. 1999. Flexibility versus efficiency? A case study of model changeovers in the Toyota production system. Organization Science 10(1):43–68. https://doi.org/10.1287/orsc.10.1.43.

Bagozzi, R.P., and H. Baumgartner. 1994. The evaluation of structural equation models and hypothesis testing. In Principles of Marketing Research, 386–422.

Bagozzi, R.P., and Y. Yi. 1988. On the evaluation of structural equation models. Journal of the Academy of Marketing Science 16(1):74–94. https://doi.org/10.1007/BF02723327.

Bedford, D.S. 2015. Management control systems across different modes of innovation: Implications for firm performance. Management Accounting Research 28:12–30. https://doi.org/10.1016/j.mar.2015.04.003.

Bedford, D.S., and T. Malmi. 2015. Configurations of control: An exploratory analysis. Management Accounting Research 27:2–26. https://doi.org/10.1016/j.mar.2015.04.002.

Benner, M.J., and M.L. Tushman. 2002. Process management and technological innovation: A longitudinal study of the photography and paint industries. Administrative Science Quarterly 47(4):676–707. https://doi.org/10.2307/3094913.

Bouwens, J., and M.A. Abernethy. 2000. The consequences of customization on management accounting system design. Accounting, Organizations and Society 25(3):221–241. https://doi.org/10.1016/S0361-3682(99)00043-4.

Browne, M.W., and R. Cudeck. 1992. Alternative ways of assessing model fit. Sociological Methods & Research 21(2):230–258. https://doi.org/10.1177/0049124192021002005.

Burgelman, R.A. 1983. A model of the interaction of strategic behavior, corporate context, and the concept of strategy. The Academy of Management Review 8(1):61. https://doi.org/10.2307/257168.

Burgelman, R.A. 1991. Intraorganizational ecology of strategy making and organizational adaptation: Theory and field research. Organization Science 2(3):239–262. https://doi.org/10.1287/orsc.2.3.239.

Byrne, B.M. 1989. A primer of LISREL basic applications and programming for confirmatory factor analytic models. New York: Springer. https://doi.org/10.1007/978-1-4613-8885-2.

Byrne, B.M. 2010. Structural equation modeling with AMOS: Basic concepts, applications, and programming, 2nd edn., London: Routledge.

Cao, Q., Z. Simsek, and H. Zhang. 2009. Modelling the joint impact of the CEO and the TMT on organizational ambidexterity. Journal of Management Studies https://doi.org/10.1111/j.1467-6486.2009.00877.x.

Carpenter, M.A. 2002. The implications of strategy and social context for the relationship between top management team heterogeneity and firm performance. Strategic Management Journal 23(3):275–284. https://doi.org/10.1002/smj.226.

Chang, S.-J., A. van Witteloostuijn, and L. Eden. 2010. From the Editors: Common method variance in international business research. Journal of International Business Studies 41(2):178–184. https://doi.org/10.1057/jibs.2009.88.

Chatman, J.A. 1991. Matching people and organizations: Selection and socialization in public accounting firms. Administrative Science Quarterly 36(3):459. https://doi.org/10.2307/2393204.

Cortina, J.M., G. Chen, and W.P. Dunlap. 2001. Testing interaction effects in LISREL: Examination and illustration of available procedures. Organizational Research Methods 4(4):324–360. https://doi.org/10.1177/109442810144002.

Cottrell, T., and B.R. Nault. 2004. Product variety and firm survival in the microcomputer software industry. Strategic Management Journal 25(10):1005–1025. https://doi.org/10.1002/smj.408.

Davila, A., G. Foster, and D. Oyon. 2009. Accounting and control, entrepreneurship and innovation: Venturing into new research opportunities. European Accounting Review 18(2):281–311. https://doi.org/10.1080/09638180902731455.

Del Giudice, M., V. Scuotto, A. Papa, S.Y. Tarba, S. Bresciani, and M. Warkentin. 2021. A self-tuning model for smart manufacturing SMEs: Effects on digital innovation. Journal of Product Innovation Management 38(1):68–89.

Dess, G.G., and R.B. Robinson. 1984. Measuring organizational performance in the absence of objective measures: The case of the privately-held firm and conglomerate business unit. Strategic Management Journal 5(3):265–273. https://doi.org/10.1002/smj.4250050306.

Doz, Y.L. 2007. The evolution of cooperation in strategic alliances: Initial conditions or learning processes? Strategic Management Journal 17(S1):55–83. https://doi.org/10.1002/smj.4250171006.

Duncan, R. 1976. The ambidextrous organization: Designing dual structures for innovation. In The ambidextrous organization: Designing dual structures for innovation, ed. R.H. Killmann, L.R. Pondy, and Sleven, 167–188.

Dutschkus, F., and C. Lukas. 2022. Social relationships and group dynamics within the supervisory board and their influence on CEO compensation. Schmalenbach Journal of Business Research 74(2):163–200. https://doi.org/10.1007/s41471-022-00130-2.

Ebben, J.J., and A.C. Johnson. 2005. Efficiency, flexibility, or both? Evidence linking strategy to performance in small firms. Strategic Management Journal 26(13):1249–1259. https://doi.org/10.1002/smj.503.

Floyd, S.W., and P.J. Lane. 2000. Strategizing throughout the organization: Managing role conflict in strategic renewal. Academy of Management Review 25(1):154–177. https://doi.org/10.5465/amr.2000.2791608.

Frow, N., D. Marginson, and S. Ogden. 2010. “Continuous” budgeting: Reconciling budget flexibility with budgetary control. Accounting, Organizations and Society 35(4):444–461. https://doi.org/10.1016/j.aos.2009.10.003.

Garg, V.K., B.A. Walters, and R.L. Priem. 2003. Chief executive scanning emphases, environmental dynamism, and manufacturing firm performance. Strategic Management Journal 24(8):725–744. https://doi.org/10.1002/smj.335.

Geerts, A., B. Leten, R. Belderbos, and B. Van Looy. 2018. Does spatial ambidexterity pay off? On the benefits of geographic proximity between technology exploitation and exploration. Journal of Product Innovation Management 35(2):151–163.

Ghoshal, S., and C.A. Bartlett. 1994. Linking organizational context and managerial action: The dimensions of quality of management. Strategic Management Journal 15(S2):91–112. https://doi.org/10.1002/smj.4250151007.

Gibson, C.B., and J. Birkinshaw. 2004. The antecedents, consequences, and mediating role of organizational ambidexterity. Academy of Management Journal 47(2):209–226. https://doi.org/10.2307/20159573.

Hair, J.F., W.C. Black, B.J. Babin, and R.E. Anderson (eds.). 2010. Multivariate data analysis: A global perspective, 7th edn., London: Pearson.

Hair, J.F., C.M. Ringle, and M. Sarstedt. 2011. PLS-SEM: Indeed a silver bullet. Journal of Marketing Theory and Practice 19(2):139–152. https://doi.org/10.2753/MTP1069-6679190202.

Han, M., and N. Celly. 2008. Strategic ambidexterity and performance in international new ventures. Canadian Journal of Administrative Sciences/Revue Canadienne Des Sciences de l’Administration 25(4):335–349. https://doi.org/10.1002/cjas.84.

Harrison, J.R., and G.R. Carroll. 1991. Keeping the faith: a model of cultural transmission in formal organizations. Administrative Science Quarterly 36(4):552. https://doi.org/10.2307/2393274.

He, Z.-L., and P.-K. Wong. 2004. Exploration vs. exploitation: An empirical test of the ambidexterity hypothesis. Organization Science 15(4):481–494. https://doi.org/10.1287/orsc.1040.0078.

Heinicke, A., T.W. Guenther, and S.K. Widener. 2016. An examination of the relationship between the extent of a flexible culture and the levers of control system: The key role of beliefs control. Management Accounting Research 33:25–41. https://doi.org/10.1016/j.mar.2016.03.005.

Henri, J.-F. 2006a. Organizational culture and performance measurement systems. Accounting, Organizations and Society 31(1):77–103. https://doi.org/10.1016/j.aos.2004.10.003.

Henri, J.-F. 2006b. Management control systems and strategy: A resource-based perspective. Accounting, Organizations and Society 31(6):529–558. https://doi.org/10.1016/j.aos.2005.07.001.

Hess, M.F., and A.M. Hess. 2016. Stakeholder-driven strategic renewal. International Business Research 9(3):53. https://doi.org/10.5539/ibr.v9n3p53.

Hill, S.A., and J. Birkinshaw. 2014. Ambidexterity and survival in corporate venture units. Journal of Management 40(7):1899–1931. https://doi.org/10.1177/0149206312445925.

Hu, L., and P.M. Bentler. 1999. Cutoff criteria for fit indexes in covariance structure analysis: Conventional criteria versus new alternatives. Structural Equation Modeling: A Multidisciplinary Journal 6(1):1–55. https://doi.org/10.1080/10705519909540118.

Huff, J.O., A.S. Huff, and H. Thomas. 1992. Strategic renewal and the interaction of cumulative stress and inertia. Strategic Management Journal 13(S1):55–75. https://doi.org/10.1002/smj.4250131006.

Iborra, M., V. Safon, and C. Dolz. 2020. What explains the resilience of SMEs? Ambidexterity capability and strategic consistency. Long Range Planning 53(6):101947. https://doi.org/10.1016/j.lrp.2019.101947.

Jansen, J.J.P., G. George, F.A.J. Van den Bosch, and H.W. Volberda. 2008. Senior team attributes and organizational ambidexterity: the moderating role of transformational leadership. Journal of Management Studies 45(5):982–1007. https://doi.org/10.1111/j.1467-6486.2008.00775.x.

Katz, D., and R.L. Kahn. 1978. The social psychology of organizations, 2nd edn. Wiley.

Kauppila, O., and M.P. Tempelaar. 2016. The social-cognitive underpinnings of employees’ ambidextrous behaviour and the supportive role of group managers’ leadership. Journal of Management Studies 53(6):1019–1044.

Kenny, D.A., and C.M. Judd. 1984. Estimating the nonlinear and interactive effects of latent variables. Psychological Bulletin 96(1):201–210. https://doi.org/10.1037/0033-2909.96.1.201.

Kiss, A.N., D. Libaers, P.S. Barr, T. Wang, and M.A. Zachary. 2020. CEO cognitive flexibility, information search, and organizational ambidexterity. Strategic Management Journal 41(12):2200–2233.

Kline, R.B. 2016. Principles and practice of structural equation modeling, 4th edn., New York: Guilford.

Koryak, O., A. Lockett, J. Hayton, N. Nicolaou, and K. Mole. 2018. Disentangling the antecedents of ambidexterity: Exploration and exploitation. Research Policy 47(2):413–427.

Kruis, A.-M., R.F. Speklé, and S.K. Widener. 2016. The levers of control framework: An exploratory analysis of balance. Management Accounting Research 32:27–44. https://doi.org/10.1016/j.mar.2015.12.002.

Levinthal, D.A., and J.G. March. 1993. The myopia of learning. Strategic Management Journal 14(S2):95–112. https://doi.org/10.1002/smj.4250141009.

Levitt, B., and J.G. March. 1988. Organizational learning. Annual Review of Sociology 14(1):319–338. https://doi.org/10.1146/annurev.so.14.080188.001535.

Libby, T., and R.M. Lindsay. 2010. Beyond budgeting or budgeting reconsidered? A survey of North-American budgeting practice. Management Accounting Research 21(1):56–75. https://doi.org/10.1016/j.mar.2009.10.003.

Lin, Z.J., H. Yang, and I. Demirkan. 2007. The performance consequences of ambidexterity in strategic alliance formations: Empirical investigation and computational theorizing. Management Science 53(10):1645–1658. https://doi.org/10.1287/mnsc.1070.0712.

Lorange, P. 1998. Strategy implementation: the new realities. Long Range Planning 31(1):18–29.

Lubatkin, M.H., Z. Simsek, Y. Ling, and J.F. Veiga. 2006. Ambidexterity and performance in small-to medium-sized firms: The pivotal role of top management team behavioral integration. Journal of Management 32(5):646–672. https://doi.org/10.1177/0149206306290712.

Luger, J., S. Raisch, and M. Schimmer. 2018. Dynamic balancing of exploration and exploitation: The contingent benefits of ambidexterity. Organization Science 29(3):449–470.

March, J.G. 1991. Exploration and exploitation in organizational learning. Organization Science 2(1):71–87. https://doi.org/10.1287/orsc.2.1.71.

Matthews, L., M.L.M. Heyden, and D. Zhou. 2022. Paradoxical transparency? Capital market responses to exploration and exploitation disclosure. Research Policy 51(1):1–17.

McCarthy, I.P., and B.R. Gordon. 2011. Achieving contextual ambidexterity in R&D organizations: A management control system approach: Achieving contextual ambidexterity in R&D organizations. R&D Management 41(3):240–258. https://doi.org/10.1111/j.1467-9310.2011.00642.x.

McDonough, E.F., and R. Leifer. 1983. Using simultaneous structures to cope with uncertainty. Academy of Management Journal 26(4):727–735. https://doi.org/10.5465/255918.

McNulty, T., and A. Pettigrew. 1999. Strategists on the board. Organization Studies 20(1):47–74. https://doi.org/10.1177/0170840699201003.

Mihalache, O.R., J.J.P. Jansen, F.A.J. Van den Bosch, and H.W. Volberda. 2014. Top management team shared leadership and organizational ambidexterity: a moderated mediation framework: TMT shared leadership and ambidexterity. Strategic Entrepreneurship Journal 8(2):128–148. https://doi.org/10.1002/sej.1168.

Miller, D. 1987. The structural and environmental correlates of business strategy. Strategic Management Journal 8(1):55–76. https://doi.org/10.1002/smj.4250080106.

Mundy, J. 2010. Creating dynamic tensions through a balanced use of management control systems. Accounting, Organizations and Society 35(5):499–523. https://doi.org/10.1016/j.aos.2009.10.005.

Nunnally, J.C. 1978. Psychometric theory, 2nd edn., New York: McGraw-Hill.

Oehmichen, J., M.L.M. Heyden, D. Georgakakis, and H.W. Volberda. 2017. Boards of directors and organizational ambidexterity in knowledge-intensive firms. The International Journal of Human Resource Management 28(2):283–306. https://doi.org/10.1080/09585192.2016.1244904.

O’Reilly, C.A., and M.L. Tushman. 2004. The ambidextrous organization. Harvard Business Review 82(4):74–140.

O’Reilly, C.A., and M.L. Tushman. 2013. Organizational ambidexterity: Past, present, and future. Academy of Management Perspectives 27(4):324–338. https://doi.org/10.5465/amp.2013.0025.

Ou, A.Y., D.A. Waldman, and S.J. Peterson. 2018. Do humble CEOs matter? An examination of CEO humility and firm outcomes. Journal of Management 44(3):1147–1173.

Podsakoff, P.M., S.B. MacKenzie, J.-Y. Lee, and N.P. Podsakoff. 2003. Common method biases in behavioral research: A critical review of the literature and recommended remedies. Journal of Applied Psychology 88(5):879–903. https://doi.org/10.1037/0021-9010.88.5.879.

Raisch, S., and J. Birkinshaw. 2008. Organizational ambidexterity: Antecedents, outcomes, and moderators. Journal of Management 34(3):375–409. https://doi.org/10.1177/0149206308316058.

Raisch, S., J. Birkinshaw, G. Probst, and M.L. Tushman. 2009. Organizational ambidexterity: Balancing exploitation and exploration for sustained performance. Organization Science 20(4):685–695. https://doi.org/10.1287/orsc.1090.0428.

Revilla, E., and B. Rodríguez-Prado. 2018. Bulding ambidexterity through creativity mechanisms: Contextual drivers of innovation success. Research Policy 47(9):1611–1625.

Richard, P.J., T.M. Devinney, G.S. Yip, and G. Johnson. 2009. Measuring organizational performance: Towards methodological best practice. Journal of Management 35(3):718–804. https://doi.org/10.1177/0149206308330560.

Robinson, R.B., and J.A. Pearce. 1988. Planned patterns of strategic behavior and their relationship to business-unit performance. Strategic Management Journal 9(1):43–60. https://doi.org/10.1002/smj.4250090105.

Rothaermel, F.T., and M.T. Alexandre. 2009. Ambidexterity in technology sourcing: The moderating role of absorptive capacity. Organization Science 20(4):759–780. https://doi.org/10.1287/orsc.1080.0404.

Simons, R. 1994. How new top managers use control systems as levers of strategic renewal. Strategic Management Journal 15(3):169–189. https://doi.org/10.1002/smj.4250150301.

Simons, R. 1995. Levers of control: How managers use innovative control systems to drive strategic renewal. Boston: Harvard Business School Press.

Stouthuysen, K., H. Slabbinck, and F. Roodhooft. 2017. Formal controls and alliance performance: The effects of alliance motivation and informal controls. Management Accounting Research 37:49–63.

Tang, S., S. Nadkarni, W. Liqun, and S.X. Zhang. 2021. Balancing the yin and yang: TMT gender diversity, psychological safety, and firm ambidextrous strategic orientation in Chinese high-tech SMes. Academy of Management Journal 64(5):1578–1604.

Tempelaar, M.P., and N.A. Rosenkranz. 2019. Switching hats: The effect of role transition on individual ambidexterity. Journal of Management 45(4):1517–1539.

Tushman, M.L., and C.A. O’Reilly. 1996. Ambidextrous organizations: Managing evolutionary and revolutionary change. California Management Review 38(4):8–29. https://doi.org/10.2307/41165852.

Van der Stede, W.A., C.W. Chow, and T.W. Lin. 2006. Strategy, choice of performance measures, and performance. Behavioral Research in Accounting 18(1):185–205. https://doi.org/10.2308/bria.2006.18.1.185.

Van Neerijnen, P., M.P. Tempelaar, and V. Van de Vrande. 2021. Embracing Paradox: TMT paradoxical processes as a steppingstone between TMT reflexivity and organizational ambidexterity. Organization Studies 00(0):1–22.

Venkatraman, N., and V. Ramanujam. 1987. Measurement of business economic performance: An examination of method convergence. Journal of Management 13(1):109–122. https://doi.org/10.1177/014920638701300109.

Wang, H., and J. Li. 2008. Untangling the effects of overexploration and overexploitation on organizational performance: The moderating role of environmental dynamism. Journal of Management 34(5):925–951. https://doi.org/10.1177/0149206308321547.

Wang, S.L., Y. Luo, V. Maksimov, J. Sun, and N. Celly. 2019. Achieving temporal ambidexterity in new ventures. Journal of Management Studies 56(4):788–822.

Wang, Y., F. Yan, F. Jia, and L. Chen. 2021. Building supply chain resilience through ambidexterity: An information processing perspective. International Journal of Logistics Research and Applications https://doi.org/10.1080/13675567.2021.1944070.

Widener, S.K. 2007. An empirical analysis of the levers of control framework. Accounting, Organizations and Society 32(7–8):757–788. https://doi.org/10.1016/j.aos.2007.01.001.

Zimmermann, A., S. Raisch, and L.B. Cardinal. 2018. Managing persistent tensions on the frontline: A configurational perspective on ambidexterity. Journal of Management Studies 55(5):739–769.

Funding

The authors declare that no funds, grants, or other support were received to conduct this study.

Author information

Authors and Affiliations

Contributions

All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Conflict of interest

K. Möller, F. Schmid, T.M. Seehofer and P. Wenig declare that they have no competing interests.

Additional information

Availability of data and material

The datasets analyzed in the current study are available from the corresponding author upon reasonable request.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Möller, K., Schmid, F., Seehofer, T.M. et al. How the Design of an Organizational Context Helps to Attain Contextual Ambidexterity. Schmalenbach J Bus Res 74, 603–629 (2022). https://doi.org/10.1007/s41471-022-00142-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41471-022-00142-y