Abstract

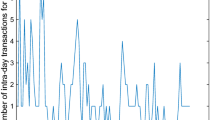

This paper introduces a non-stationary bivariate integer-valued auto-regressive process of order p (BINAR(p) with non-stationary moments. The BINAR(p) uses the conventional binomial thinning procedure and the cross correlation between the two related series is induced from the paired innovation terms. The conditional maximum likelihood (CML) approach is used to estimate the model parameters. Monte Carlo simulation experiments with bivariate Poisson innovations are implemented to assess the consistency and asymptotic properties of the proposed BINAR(p). In the application part, we consider two bivariate time series: The Ask and bid quotes from AT &T and the intra-day transactions of Mauritius Commercial Bank (MCB) and State Bank of Mauritius Holdings (SBMH). These series were fitted using the BINAR(p) with paired Poisson, Negative Binomial and Poisson-Lindley innovations and the results demonstrate that BINAR(p) with Negative Binomial yield better fitting and slightly lesser mean square error.

Similar content being viewed by others

References

Al Osh M, Alzaid A (1987) First-order integer-valued autoregressive process. J Time Ser Anal 8:261–275

Bulla J, Chesneau C, Kachour M (2017) A bivariate first-order signed integer-valued autoregressive process. Commun Stat-Theory Methods 46(13):6590–6604

Bulla J, Chesneau C, Kachour M (2017) A bivariate first-order signed integer-valued autoregressive process. Commun Stat-Theory Methods 46:6590–6604

Chen H, Zhu F, Liu X (2022) A new bivariate INAR (1) model with time-dependent innovation vectors. Stats 5(3):819–840

Chen H, Zhu F, Liu X (2023) Two-step conditional least squares estimation for the bivariate-valued INAR (1) model with bivariate skellam innovations. Commun Stat-Theory Methods 1–22

Du J, Li Y (1991) The integer-valued autoregressive (INAR(p)) model. J Time Ser Anal 12:129–142

Freeland R, McCabe B (2004) Analysis of low count time series data by Poisson autoregression. J Time Ser Anal 25(5):701–722

Freeland R, McCabe B (2004) Forecasting discrete valued low count time series. Int J Forecast 20:427–434

Fu T (2011) A review on time series datamining. Eng Appl Artif Intell 24:164–181

Jowaheer V, Mamode Khan N, Sunecher Y (2017b) A BINAR(1) time series model with cross-correlated COM-Poisson innovations. Commun Stat-Theory Methods

Karlis D, Ntzoufras I (2003) Analysis of sports data by using bivariate Poisson models. J R Stat Soc: Series D (The Statistician) 52(3):381–393

Khan NM, Oncel Cekim H, Ozel G (2020) The family of the bivariate integer-valued autoregressive process (BINAR (1)) with Poisson–Lindley (PL) innovations. J Stat Comput Simul 90(4):624–637

Kim H, Park Y (2008) A non-stationary integer-valued autoregressive model. Stat Pap 49:485–502

Kocherlakota S, Kocherlakota K (1992) Bivariate discrete distributions, vol 132. CRC Press, Boca Raon

Li Q, Chen H, Liu X (2021) A new bivariate random coefficient INAR (1) model with applications. Symmetry 14(1):39

Mamode Khan N, Sunecher Y, Jowaheer V (2016) Modelling a non-stationary BINAR(1) Poisson process. J Stat Comput Simul 86:3106–3126

Marshall A, Olkin I (1990) Multivariate distribution generated from mixtures of convolution and product families. Topics in Statistical Dependence, Block, Sampson y Sanits (Eds), Institute of Mathematical Statistics

McKenzie E (1986) Autoregressive moving-average processes with negative binomial and geometric marginal distrbutions. Adv Appl Probab 18:679–705

McKenzie E (1988) Some ARMA models for dependent sequences of Poisson counts. Adv Appl Probab 20:822–835

Minkova L, BalaKrishnan N (2014) Type-II bivariate Polya-Aeppli distribution. Stat Probab Lett 88:40–49

Nyholm K (2003) Inferring the private information content of trades: a regime-switching approach. J Appl Econom 18(4):457–470

Pedeli X, Karlis D (2011) A bivariate INAR(1) process with application. Stat Model: Int J 11:325–349

Pedeli X, Karlis D (2013) On estimation of the bivariate Poisson INAR process. Commun Stat-Theory Methods 35:514–533

Ristic M, Popovic B (2019) A new bivariate binomial time series model. Markov Process Related Fields 25:301–328

Schweer S, Weiss C (2014) Compound poisson INAR(1) processes: stochastic properties and testing for overdispersion. Comput Stat Data Anal 77:267–284

Silva N, Pereira I, Silva ME (2009) Forecasting in INAR (1) model. REVSTAT-Stat J 7(1):119–134

Steutel F, van Harn K (1979) Discrete analogues of self-decomposability and statibility. Ann Probab 7:3893–899

Steutel F, van Harn K (1986) Discrete operator self-decomposability and queing networks. Stoch Model 2:161–169

Su B, Zhu F (2021) Comparison of BINAR (1) models with bivariate negative binomial innovations and explanatory variables. J Stat Comput Simul 91(8):1616–1634

Sunecher Y, Mamodekhan N, Jowaheer V (2017) A GQL estimation approach for analysing non-stationary over-dispersed BINAR(1) time series. J Stat Comput Simul 87(10):1911–1924

Weiss C (2008) The combined INAR(p) models for time series of counts. Stat Probab Lett 78(13):1817–1822

Acknowledgements

This work is also part of my Post-Doctoral Fellowship on “The Family of Bivariate Integer-Valued Autoregressive Models” at the University of Bahia, Brazil. I am thankful to Prof. Paulo Jorge Canas Rodrigues and to the anonymous reviewers for their suggestions.

Funding

No funding was received for this research work.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no conflicts of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Sunecher, Y., Mamode Khan, N., Bakouch, H.S. et al. On Some Non-stationary Bivariate INAR(p) Models with Applications to Intra-day Stock Transaction Series. J Indian Soc Probab Stat (2024). https://doi.org/10.1007/s41096-024-00177-w

Accepted:

Published:

DOI: https://doi.org/10.1007/s41096-024-00177-w