Abstract

This article examines the relationship between firm age and acquisition activity and how family and non-family firms differ in the number of acquisitions they undertake. Inspired by previous research requiring firm age as a focal aspect and literature studying the antecedents of acquisitions, we draw on the SEW perspective to test our hypotheses based on the analysis of the acquisition activity of Asia-Pacific public firms. Our empirical findings support a U-shaped relationship between firm age and acquisition activity. Moreover, the findings reveal that family firms engage in fewer acquisitions than non-family firms irrespective of the age of the firm.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

As far as we know, no prior work has examined in depth the relationship between firm age and acquisition activity. This study addresses this research gap in the literature. Today, firm age is emerging as a booming and prolific field of research, with an increasing number of studies focused on the effects of firm age on different performance dimensions, such as growth, innovation or internationalization (e.g. Anyadike-Danes & Hart, 2018; Naldi & Davidsson, 2014; Pellegrino, 2018). Scholars from this nascent field highlight certain research gaps regarding how firm behaviour varies as firms grow older (Coad et al., 2013). This growing interest in firm age and its effect on firm performance is underpinned by the consideration of firm age as more than a control variable and by its prominent characteristic of not being susceptible to causality concerns because it cannot be shaped nor manipulated (Coad et al., 2018). In short, these contemporary studies claim that firm age should be considered as an independent variable when analysing firm performance (Cowling et al., 2018), contending that both young and old firms co-exist and might contribute differently to firm performance (Coad et al., 2018).

Despite the unsurprising negative effect of the coronavirus pandemic on the M&A global activity, there were 43,596 deals worth USD 1,746,601 million in the opening six months of 2020 (Bureau Van Dijk, 2020). Acquiring firms is one of the most recurrent ways to gain size and competitiveness. Opting for an acquisition strategy allows firms to benefit from economic and financial synergies (Zozaya-González, 2007). Thus, firms may grow faster, obtain better results (turnover, market share, customer base, etc.) and reduce costs through scale economies much more quickly in the short term. In addition, acquisitions may produce higher cash-flows, increase debt leverage and lower the cost of capital (Candra et al., 2021). Along with the former worldwide strategic and economic relevance, acquisition activity has progressively become a prominent topic in several knowledge fields (Barkema & Schijven, 2008). In this sense, literature on acquisition activity has examined several antecedents that offer explanations about how and why acquisitions happen, which can fall broadly in four categories (Haleblian et al., 2009): value creation, managerial self-interest, environmental factors, and firm features. Particularly, among those studies focused on firm characteristics, the management research has been mainly interested in the impact of acquisition experience (e.g. Barkema & Schijven, 2008) and firms’ strategic positions and intentions (e.g. Graebner & Eisenhardt, 2004). The deterrent or fostering effect of the above factors can vary as firms age. For instance, the youngest firms may consider acquisitions as an opportunity to grow inorganically to become more efficient and competitive when organic growth is proven insufficient (Cartwright & Schoenberg, 2006). On the contrary, middle-aged firms may have more incentives to pay out dividends regularly than to promote growth through acquisitions (DeAngelo & DeAngelo, 2007). Finally, for elderly firms, conditions such as acquisition experience, resource endowment, and slack availability may positively influence acquisitions (King et al., 2004). Therefore, research on age and acquisitions may be of interest to firms trying to plan ahead for acquisitions, or to counter the effects of aging on acquisition activity. Moreover, it might be also interesting for policy-makers to better comprehend the needs and challenges of firms of different ages for addressing acquisitions, and to scheme more effective policies that can be targeted to firms of specific age groups (Coad, 2018).

Further, even though research on firm acquisitions has increasingly grown over the last decades, we really do not know the theoretical arguments that may explain why family and non-family firms differ in their acquisition activity over time. Therefore, a related research question in the relationship between firm age and acquisitions that this study discusses theoretically is: why do family firms engage in acquisition activity distinctly to their non-family counterparts as they grow older? Certainly, the socioemotional wealth (hereafter, SEW) theoretical approach (Gomez-Mejia et al., 2007), claims that when family members deal with strategic decision making, such as those related to acquisitions, they contemplate each option’s implications in terms of their affective endowment (Berrone et al., 2012; Gomez-Mejia et al., 2007; Martínez-Romero & Rojo-Ramírez, 2016). That is, family firms consider not only economic, but also non-economic family goals (Chrisman et al., 2012; Zellweger & Nason, 2008), which in turn impact on acquisition strategies (Gomez-Mejia et al., 2018). Engaging in acquisitions implies assuming that their negative effects in terms of SEW (e.g. loss of family control or augmented risk aversion) will outweigh their potential positive SEW-related benefits (e.g. source of family employment), which often results in family firms being less likely to develop acquisitions (Caprio et al., 2011; Diéguez-Soto et al., 2021; Gomez-Mejia et al., 2018). In this sense, and using the SEW approach, a very recent study addresses the question of how family firms avoid SEW losses by engaging in a lower volume of acquisitions (Cuevas-Rodríguez et al., 2023).

Over time, relevant changes take place in the organization (Fang et al., 2018) and the attributes, needs and governance structures of family firms vary (Bammens et al., 2008; De Massis et al., 2018; Hülsbeck et al., 2019). Likewise, family’s capabilities and priorities significantly diverge when family firms age, so their influence on strategic decision-making also evolve (Debellis et al., 2023a, 2023b). For instance, previous literature has confirmed that the relevance attached to SEW and financial goals change as family firms age (Gomez-Mejia et al., 2011; Fang et al., 2018). SEW is dynamic, as both resource endowments through continuous ebbs and flows (Chua et al., 2015) and SEW reference points (Nason et al., 2019), vary over time. Thus, the chrono context, “which consists of the life courses of the family and business systems and encompasses factors that lead to evolutionary or punctuated changes along the family’s and the business’s life” (De Massis et al., 2018, p. 12), may also play a fundamental role in explaining acquisitions in family firms, given that SEW seems to not remain constant over time (Martínez-Romero & Rojo-Ramírez, 2016; Swab et al., 2020). Despite some prior research has studied the impact of family status on acquisitions from a SEW perspective (e.g. Gomez-Mejia et al., 2018; Cuevas-Rodríguez et al., 2023; Pinelli et al., 2023), the question of how family firms protect SEW from losses when undertaking acquisitions over time has not yet been analyzed.

This study aims to examine the influence of firm age on acquisition activity and how family and non-family firms differ in the number of acquisitions they undertake. We were inspired by prior emerging literature considering firm age as a focal variable and research analysing acquisition antecedents for examining the age-acquisition association, and we draw on the SEW perspective (Gomez-Mejia et al., 2007) and the chrono context (De Massis et al., 2018) for investigating the family firm effect.

The research gaps highlighted in this study are addressed by analysing the acquisition activity of public firms from the Asia Pacific region. This context offers an intriguing research setting characterized by the great relevance of M&A -4 out of 10 deals in global M&A activity- (Bureau Van Dijk, 2020), by being home to the world’s oldest still operating companies (BusinessFinancing.co.uk, 2021) and by the overwhelming presence of family firms, comprising 85% of overall companies (EY, 2014).

This article attempts to make several contributions to the literature. First, by identifying age as a previously unexplored antecedent of acquisition activity, this study adds to the research streams on acquisitions (Haleblian et al., 2009) and on firm age (Coad, 2018), shedding new light on how acquisition activity evolves, as firms grow older. Second, this study also contributes to the family firm research field, by considering firms’ chrono context, namely firm age, to theoretically discuss why family firms overall engage in a lower number of acquisitions than non-family firms. Third, we respond to the call for further research on the effect of SEW variations throughout the firm’s life on strategic decisions (Swab et al., 2020). Finally, this study crosses the boundaries of prior acquisition research focused on European (e.g. Caprio et al., 2011) and US public firms (e.g. Miller et al., 2010), by addressing a unique context, i.e. the Asia-pacific region (Eddleston et al., 2020), to enrich our understanding about acquisition activity.

The rest of the paper is organised as follows. The next section presents the theoretical background and hypotheses development. Then, we present the data and the methods used in our analysis. Finally, we show the empirical results and discuss our findings.

2 Theoretical framework and hypotheses development

2.1 Firm age, performance and inorganic growth

The influence of age on firm performance is well documented but shows mixed findings (Durand & Coeurderoy, 2001). Some studies present a positive impact of age on firm performance once the firm has managed to survive for a sufficient period of time (e.g. Audretsch, 1995), arguing that as age increases, firms’ experience in their businesses will also be higher (Geroski, 1995). However, other studies found a negative effect of age on firm performance (e.g. Durand & Coeurderoy, 2001), postulating that older firms will be more inclined to ossify their routines, to have non-learning processes and blindness or to be opposed to changes (e.g. Szulanski, 1996). Older firms can also suffer from ‘liabilities of age’, like for example lower levels of commitment and engagement compared to younger firms (Churchill & Lewis, 1983).

Prior research has also addressed the relationship between age and firm growth (Coad et al., 2013), a common measure of firm performance and one of the most relevant factors for continuity and transgenerational wealth creation (Kellermanns et al., 2008; Martínez-Alonso et al., 2022). The vast majority of studies have shown a negative influence of age on organic firm growth (Coad et al., 2013; Fariñas & Moreno, 2000). In this regard, the youngest firms usually have greater growth rates because their main objective is reaching a minimum level of efficiency that assures their survival. Lotti et al. (2009) go further and specify that the negative influence of age on firm growth becomes non-significant as firms are getting older. Yet, a few studies found a favourable impact of age on firm growth (Shanmugam & Bhaduri, 2002). Finally, other studies (e.g. Fotopoulos & Giotopoulos, 2010) revealed that once firms achieve a size target that allows them to attain their survival, they are inclined to diminish their growth, showing an inverted U-shaped relationship between the variables.

As growth is a heterogeneous phenomenon and firms can grow in a wide range of ways (e.g. McKelvie, 2010), literature is centering its attention on specific forms of growth (Naldi & Davidsson, 2014). Thus, several papers have been focused on inorganic growth, evidencing that there is greater acquisition activity for firms that have recently carried out IPOs (Celikyurt et al., 2010; Maksimovic et al., 2013). In this same research stream, Arikan and Stulz (2016) investigate whether corporate acquisitions, as a function of their age relative to the IPO date, varies over the firm’s life cycle. These authors find a U-shape relationship between the firm life cycle and the acquisition rate, in such a way that the acquisition rate decreases intensely early on, keeps relatively invariable for a period of time and then augments. Their study confirms that, acquisitions are carried out by higher-performing firms and firms with greater investment opportunities. That is, as firms get older, their levels of Tobin’s q are lower, and then they acquire less. Nevertheless, when firms are more mature and some of their rare assets become underemployed, they are more willing to carry out diversifying acquisitions to make the most of their scarce valuable assets (Maksimovic et al., 2013).

Considering previous research on how firm acquisitions evolve over time, our study is the first attempt, to the best of our knowledge, to advance the understanding of how firm age relates to inorganic firm growth, namely acquisitions, considering firm age as the number of years since its foundation. Furthermore, to improve the comprehension of the effect of firm age on acquisitions, this work also analyses the differences between family and non-family firms on their acquisition activity.

2.2 Hypothesis development

2.2.1 Firm age and acquisition activity

Prior literature suggests that as a firm ages many of its characteristics vary, such as its strategic goals, acquisition experience or resources availability, and altogether these variations impact on its decision-making and routines (Coad, 2018; Kieschnick & Moussawi, 2018). Inspired by the former statement, we propose a U-shaped relationship between firm age and acquisition activity.

First, the youngest firms will have as a key objective achieving a minimum size through growth, as it is an indispensable condition to be efficient, competitive and, therefore, to assure their permanence in the markets (e.g. Jovanovic, 1982). At the beginning of their lives, firms tend to maintain small, so they should grow. Initially, they opt for growing organically, by increasing their sales (PwC, 2017). But when this type of growth is insufficient and companies have enough resources and skills, they may consider inorganic growth as a more probable choice. Firms may perceive that when facing business opportunities, they should compete more efficiently (Porter, 1985) and contemplate acquisitions as an opportunity to secure and gain market share, to offer their clients better deals and to access to more relevant agreements (Geiger & Schiereck, 2014). In short, the youngest firms may face challenges in future growth and one solution is acquisition, which accelerates and strengthens their corporate development (Cartwright & Schoenberg, 2006). These firms will be able to achieve higher growth rates if they seize proper acquisition opportunities, compared to organic growth only.

However, after some acquisition activity at the first stages of their live, middle-age firms may have a higher interest in paying out dividends regularly (DeAngelo & DeAngelo, 2007) to promoting growth through acquisitions, due to different reasons, such as the mitigation of agency conflicts (e.g. Baker & Wurgler, 2004; Bhattacharyya, 2007). In addition, middle-age firms may need some time to integrate the target companies they have previously acquired and to improve their efficiency (Hitt et al., 1993). To this end, there is a relevant strand of literature concerning the post-acquisition process. The influence of acquisitions on both individual and firm culture -organizational behaviour- (e.g. Janson, 1994) or the role of managers to cope with the post-acquisition process in an effective way -process perspective- (e.g. Greenwood et al., 1994), are some of the literature streams that have already been studied (Birkinshaw et al., 2000). Consequently, firms that have developed prior acquisition activity may also need time to have some reflection over the lessons learned during the acquisition process. Furthermore, firms may be short of financial resources after making a great economic effort to carry out acquisitions. Thus, middle-age firms will require a period of time to assimilate the novelties associated to prior acquisitions and to recover some key factors diminished after the first wave of acquisitions, such as the ability to efficiently integrate the target’s assets and know-how (Barkema & Schijven, 2008) and to finance sufficiently and properly new acquisitions (Hayward, 2002). Therefore, we expect that the number of acquisitions will decrease in middle-age firms.

Finally, following a period of time without acquisitions, the oldest firms will again have the resources available to decide on which new companies to acquire. Hence, more mature firms, which usually have lower possibilities of growing internally generating self-financing but often dispose of more cash-flow ready for use, may be willing to grow more through acquisitions (Arikan & Stulz, 2016). Furthermore, their acquisition experience will also have a positive impact on making new acquisitions, due to both organizational routine and persistence (Haleblian et al., 2006). Acquisition experience actually increases acquisition efficiency and diminish the relevance and level of risk inherently joint to this type of activity (Diéguez-Soto et al., 2021). Therefore, we establish that for elderly firms, conditions such as acquisition experience, resource endowment, and slack availability, will impact again favourably on acquisition activity (King et al., 2004).

Summing up, this study proposes that the effect of firm age on acquisitions is curvilinear. We expect that the youngest and the oldest firms will be more willing to make acquisitions, while middle-age firms will be less willing to carry out acquisitions. In light of the above argumentation, we state formally the following hypothesis:

H1

The relationship between firm age and the number of acquisitions can be graphed as a U-shaped curve.

2.2.2 Family firms and acquisition activity

We have previously stated that as firms age, their acquisition activity will vary, in such a way that, the youngest firms will carry out a large number of acquisitions, the number of acquisitions will decrease in middle-age firms, and finally, the oldest firms will again increase the number of acquisitions. Here, we argue that family and nonfamily firms will differ in the number of acquisitions they undertake because family firms are mainly concerned with SEW goals (Berrone et al., 2012; Gomez-Mejia et al., 2007, 2018; Hussinger & Issah, 2019). Specifically, we postulate that the strategy of embarking on acquisition will be peculiar for family firms at different ages, due the family control concerns, their reluctance to hire external professionals, and their aim of preserving the family firm emotional endowment (Swab et al., 2020). That is, the relevance of the former arguments might change over time, suggesting that family firms’ chrono-context may have a significant influence on how their changing preferences impact on the acquisition activity of family firms (De Massis et al., 2018; Debellis et al., 2023a).

Family firms are characterised by their long-term orientation and their desire to pass on the business to subsequent generations (Lumpkin & Brigham, 2011). Accordingly, the preservation of ownership in family hands is a main concern for family firms (Berrone et al., 2012; Gomez-Mejia et al., 2007). From the earliest stages of their lives, family firms are known for developing fewer acquisitions than their nonfamily counterparts (e.g. (Bauguess & Stegemoller, 2008; Miller et al., 2010), due to the fear of losing control as a result of family stake reduction (Caprio et al., 2011). As family firms age -middle-age and elderly family firms-, the family control concerns associated with acquisition strategies are likely to increase. Certainly, preserving a family ownership stake is usually more challenging, because different family branches get involved in the firm (Jaffe & Lane, 2004) and there is often a reduction of the family held shares (Franks et al., 2012; Gersick et al., 1997). In line with the above, middle-age, and especially the oldest family firms, may perceive more obstacles to carry out acquisitions as their decreased ownership stake might become insufficient to preserve control after finalizing the transaction (Caprio et al., 2011; Shim & Okamuro, 2011). Moreover, as family firms age, their aversion to dilution caused by the requirement for external funds (Gomez-Mejia et al., 2014; Westhead, 2003) to finance acquisitions is expected to be even higher. In addition, acquisitions imply short-term risks due to significant upfront costs, although they have the potential for long-term benefits (Haleblian et al., 2009), such as the preservation of the family dynasty, which secures the business for incumbent family members while providing increased opportunities for future generations (Menéndez-Requejo & Feito-Ruiz, 2008; Strike et al., 2015). According to this logic, the youngest family firms may develop more acquisitions than the middle-age and the oldest family firms, as they are supposed to better overcome the short-term risks derived from acquisitions with the aim of unlocking the potential for long-term benefits. As family firms get older, the potential scenario of a failed operation may diminish their willingness to embark in acquisitions because they will avoid decisions that may endanger transgenerational family control and the legacy they pass on to future generations (Gomez-Mejia et al., 2018; Strike et al., 2015). Nevertheless, although there are differences among family firms regarding acquisition over time, family firms will be expected to undertake a lower volume of acquisitions than non-family firms across all ages to retain a lock on control and dictate corporate policies. In summary, family firms will be more afraid than non-family firms of the ownership dilution and of jeopardising the transfer of family control that acquisitions may entail at every stage of the firm’s life, that is, at every firm age.

Family firms are known for being reluctant to hire external professionals (Gedajlovic & Carney, 2010; Schulze et al., 2001), especially the youngest family firms (Muñoz-Bullon et al., 2018), as their recruitment processes are usually based on family ties and emotional criteria rather than on objective reasons (Bennedsen et al., 2007; Claessens et al., 2002). However, middle-age and elderly family firms become more complex and might require external experts, both managers and directors, due to the need of higher level of professionalization (Casillas et al., 2010; Kraiczy et al., 2015; McConaughy & Phillips, 1999). Indeed, middle-age and the oldest family firms perceive professionalism as a manner of ensuring the firm’s long-term continuity and not as a threat to family control (Muñoz-Bullon et al., 2018). As family firms grow older, they are expected to be more willing to allow the entrance of non-family experts, which may be required for successfully developing acquisition strategies (Diéguez-Soto et al., 2021; Requejo et al., 2018). In short, the youngest family firms opt for not recruiting external executive talent, based on their risk-averse preferences regarding decisions that may threaten the family control over the firm (Gedajlovic et al., 2012). However, middle-age and the oldest family firms display higher willingness to attract, promote and retain external professionals in an attempt to remain competitive, to ensure their continuity and to preserve their family control and influence (Casson, 1999). Therefore, family firms are, in terms of professionalization, more similar to non-family firms as they age. Nevertheless, the lower level of professionalization that characterizes family firms across all ages, leads them to developing a lower acquisition activity than their non-family counterparts.

Family firms are also distinguished by their interest in preserving the business emotional endowment (Berrone et al., 2012; Gomez-Mejia et al., 2007; Martínez-Romero & Rojo-Ramírez, 2017). This emotional endowment can be damaged, e.g., in reputational terms, as a result of lay-offs provoked by acquisitions, especially in horizontal transactions. Moreover, the emotional endowment is likely to become weaker in the older than in the younger and middle-age family firms (Le Breton-Miller & Miller, 2013), as certain emotional dimensions, such as family identity, reputation and continuity are attenuated, as firms age (Le Breton-Miller & Miller, 2013; Miller et al., 2014; Schulze et al., 2003). Family ties become weaker as family firms grow old because members of different family branches get involve in the firm (Ensley & Pearson, 2005; Gersick et al., 1997). Thus, as family firms age, the number of family members increase, the importance attached to the firms’ emotional considerations will be lower and the sense of belonging to the firm will be undermined (Arrondo-García et al., 2016; Cruz & Nordqvist, 2012; Sciascia et al., 2014). Moreover, in middle-age and elderly family firms, there will be a greater diversity of corporate goals because family branches pursue divergent needs and agendas (Davis & Harveston, 1999; Schulze et al., 2003; Sciascia et al., 2014) and thus, there will be an increased difficulty in reaching consensus regarding strategic decisions (Le Breton-Miller & Miller, 2013; Pittino et al., 2019), such as acquisitions. Although as family firms grow older, their emotional endowment concern, a key factor that separates family firms from nonfamily firms, will be lower (Gomez-Mejia et al., 2018), this issue continues being a primary frame of reference at every stage of their lives. Thus, at all ages, family firms will develop fewer acquisitions than non-family firms driven by a desire to preserve and improve their emotional endowment.

To sum up, the youngest family firms will be more reluctant to engage in acquisitions than their nonfamily counterparts due to mainly their lower level of professionalization and due to relevant emotional concerns. Middle-age and older family firms, will develop less acquisitions than their nonfamily counterparts due to principally controlling dilution and transgenerational concerns. Grounded on the reasoning and empirical literature noted above, it may be expected that, irrespective of the age of the firm, the family SEW would be disrupted by acquisition activity. In this regard, we introduced the chrono context to better explain how the effect of SEW on the volume of acquisitions does not always have the same intensity and sense over time. Accordingly, and with this caveat in mind, we argue that SEW protection is likely to lower the number of acquisitions in family firms in relation to non-family firms, regardless the firms’ age. Therefore, it can be stated that the family nature of the firm undermines the firm acquisition activity. Stated formally:

H2

Family firms develop less acquisition activity than non-family firms irrespective of the age of the firm.

3 Data and methods

We use public manufacturing companies included in the S&P Capital IQ Platform and settled in the Asia-Pacific region (Australia, Japan, Hong Kong, New Zealand, Singapore and South Korea). The S&P Capital IQ database offers financial data over 88,000 public companies, with 45,000 active public companies representing the 99% of the market capitalization worldwide. It also covers specific information on transactions with detailed coverage of acquisitions agreements, among others. We particularly obtained information on firm’s governance and economic-financial data from 2009 to 2016 to test our hypotheses, excluding those companies, which are not currently operating in and those firms without data available for the period analysed. The final sample is a panel dataset of 3,855 observations from 1,096 companies.

3.1 The Asia-Pacific context

Despite several aspects, such as the global COVID 19 pandemic, have unfavourably influenced M&A deal-making targeting companies in the Asia Pacific region, this geographical context represents 39 per cent of total global M&A volume (43,596 deals) and 36 per cent of total global M&A value (USD 1,746,301 million) in the opening six months of 2020 (Bureau Van Dijk, 2020).

Furthermore, the importance of family firms in the Asia Pacific region is also indisputable, representing 85% of companies in this area (EY, 2014). Additionally, 17.4% of the world’s 500 largest family-owned firms are located in Asia Pacific, of which 86,2% are publicly traded companies, and are, on average, 58.9 years old (EY, 2017). Furthermore, previous literature has also highlighted a high level of coincidence between the controlling family owners and the top managers of Asian family firms (Globerman et al., 2011), which shows the great level of influence of the family members on the firm’s strategic decisions.

Finally, the model of multi-generational family-run firms in the Asia Pacific context has been an essential characteristic of this setting for decades. For instance, in South Korea “dynastic” family firms, family members keep a predominant level of control/influence over decision-making and members of the second or later generations who are in control are the prevailing group (Davarzani et al., 2014). Likewise, in Japan, some of the oldest multi-generation family firms worldwide can be found (Mehrotra et al., 2013), with an estimation of more than 33,000 Japanese firms with a history of over one hundred years (Shinise firms) (Lufkin, 2020).

3.2 Dependent variable

Acquisition activity. Acquisition activity (AA) is the number of acquisitions carried out by a given firm as a buyer in the analysed year (Sanders, 2001; Shi et al., 2017a; Shi, Zhang, & Hoskisson, Shi et al., 2017a, b). To assess the acquisitions activity, we selected in the Capital IQ database the transaction type “Merger/Acquisition”, and additionally, we added the screening criteria of “Acquisition of majority stake”. Therefore, acquisition activity provides information regarding the number of transactions in which a firm, as a buyer, acquired a majority stake in another firm. We did not apply an additional filter demanding a minimum transaction value, as some have previously done (e.g. Gomez-Mejia et al., 2018), because most transactions are reported without a disclosed value. Accordingly, using the scale of acquisition as a filter would have required obviating most acquisitions, leading to biased results (Sanders, 2001).

Our study analyses the impact of firm age on acquisition activity, and hence choosing a count dependent variable is coherent with the hypothesis development. Our study is therefore different from previous literature mainly focused on analyzing the likelihood to engage in acquisitions (the occurrence of acquisitions or the acquisition propensity) and which used a dummy variable as main dependent variable, and therefore, logit regression models (e.g. Caprio et al., 2011; Gomez-Mejia et al., 2018; Hussinger & Issah, 2019). Furthermore, taking into account the number acquisitions allows us to compare our results with those other articles which also used this count variable (e.g. Diéguez-Soto et al., 2021; Hussinger & Issah, 2019; Miller et al., 2010). Nevertheless, we also use a binary variable (likelihood of acquisitions), which takes the value of 1 if the firm has conducted at least one acquisition involving a majority stake in year t and 0 if otherwise, to show the robustness of our findings (e.g. Hussinger & Issah, 2019).

3.3 Independent variable

Firm age. We measure the age of the firm (Age) as the natural log of the time between the analysed year and the year of firm foundation (Coad et al., 2013).

3.4 Moderating variable

Family firm (FF). We measure the family firm nature as a binary variable that is equal to 1 for family firms and 0 if otherwise, where a firm is considered a family firm when both of the following conditions are met: family members control a minimum of 5% of the firm shares and at least one family member is serving as a top-level executive or member of the board. For robustness tests, we utilize alternatively family ownership stake (FOS). FOS is defined as a variable truncated on the left. The variable is set to 0 if family ownership is less than 5% and/or no family member is involved in executive or board leadership. When ownership is greater than 5% and at least one family member is involved in leadership, then the percentage of family equity is coded as a continuous variable.

3.5 Control variables

To control for firm-level inclinations to acquire, we consider the variables prior acquisition activity, firm size, and firm performance (Gomez-Mejia et al., 2018). Moreover, we take into account the firm’s liquidity as another relevant variable relative to the occurrence of financial constraints (Bauweraerts et al., 2020). The variable free cash-flow generation was also considered because of its influence on acquisition activity (Requejo et al., 2018). Furthermore, we considered R&D effort as a proxy for the organization’s readiness to take risks and to undertake long-term investments, such as acquisitions (Hussinger & Issah, 2019). We also controlled for industry effects, because there are differences across sectors in terms of operational and strategic objectives (Martínez-Alonso et al., 2023; Ortiz García de las Bayonas et al., 2023). Finally, we controlled for year and country effects, as macroeconomic conditions and countries’ legal system (shareholders’ legal protection), respectively, may influence acquisition decisions (Cuevas-Rodriguez et al., 2023).

Table 1 displays the description of all the variables used to develop this study.

4 Results

Table 2 shows the mean, median and number of observations for the dependent, independent and control variables used in the econometric specifications for the 2009–2016 period, differentiating between full sample, non-family and family firms. Likewise, Table 2 presents the results of the mean (Student t) and median (Mann-Whitney) tests. The family nature of the firm affects all the variables except age. The number of acquisitions is lower if the business is a family firm. In addition, family firms are characterized by lower size, performance and free cash-flow generation, than non-family firms. However, family firms are more liquid and more R&D intensive than their non-family counterparts.

In Table 3, we observe the behaviour of the variables with regards to a firms’ age. We distinguished three different subpopulations: under 38 years old (first quartile), from 38 to 85 years old (third quartile) and over 85 years old. To find out whether these subpopulations are equal on average, we apply both parametric (ANOVA) and non-parametric (Kruskal-Wallis) tests. The ANOVA results may have reliability problems due to the heterogeneity of variances. Therefore, the Kruskal-Wallis test is also applied. It is remarkable how the number of acquisitions is higher in firms under 38 and over 85, that is, in the extreme quartiles.

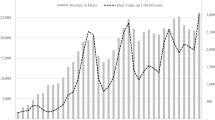

Figure 1 shows how Age influences AA. In building Fig. 1, outliers have been removed to better appreciate the shape of the distribution. In addition, we distinguish between family (grey colour) and non-family firms (black colour). The point cloud represents the actual values of acquisition activity, while the quadratic lines of the parabolas have been fitted for both family and non-family firms. In the family firm group the curvature is hardly appreciable due to the greater amplitude of the parabola. Yet, there is no doubt that the family firm curve is lower than that of non-family firms at all ages, showing that family firms engage in less acquisition activity than their non-family counterparts throughout all stages of their lives.

Mean value of the number of acquisitions versus the firm’s age (outliers omitted)

As usual in multivariate analysis, we show in Table 4, the correlation matrix as well as the mean and the standard deviation values for each and every analysed variable. The correlations are low, except for the family involvement variables (Family firm and Family ownership stake, as we could expect). It is also observed that the relative dispersion is high, which it is not rare, considering that we are working with business data. Particularly, we can see that in our sample, the age variable has a very wide range, including both very young and very aged firms.

Hypothesis 1 proposes that the relationship between Age and AA can be graphed as a U-shaped curve. Additionally, Hypothesis 2 establishes that the fact of being a family firm negatively impacts the acquisition activity at all ages. We estimated several count regressions for panel data with random effects. The model specification to test the hypotheses is the following:

The dependent variable is acquisition activity (AA), while firm age (Age), firm age squared (Age2) and family firm (FF) are the independent variables. We also introduced several control variables in the model: Prior acquisition activity (PAA), Size, Liquidity, Performance, Free cash-flow generation (FCF), R&D effort and the indicators for industry, year and country. We lagged our independent and control variables one year so that they were used to explain acquisition activity in the following year, which allows to minimize concerns for reverse causality.

As we stated above, to assess acquisition activity we confided on count data, for which OLS models are not considered an appropriate estimation technique. The Poisson regression and the negative Binomial are usually considered to be suitable methods when there is a count dependent variable (Verbeek, 2004). As the assumption of equidispersion (mean equals variance) is not often met, and certainly not in our case (see Table 4), we opted for the negative binomial regression which allows to handle overdispersion (Cameron & Trivedi, 2010, p. 627) and has often been considered in family business literature to face the former issue (e.g. Block et al., 2013).

We apply random effects negative binomial panel regressions (Hilbe, 2011). We choose random effects because one of our independent variables, FF variable, is binary and time invariant (Cameron & Trivedi, 2010).

Table 5 presents the results using AA as the dependent variable. Hypothesis 1 proposes that the relationship between Age and AA can be graphed as a U-shaped curve. In Model 0, the results of the basic regression are displayed only considering the control variables. In Model 1 the lagged variables Age, Age2 and FF are added to capture the effect of both the observed quadratic relationship between AA and Age and the family firm nature. Model 0 reveals that prior acquisition activity (PAA) (β = 0.058, p-value = 0.000), Size (β = 1.745, p-value = 0.000), Performance (β = 0.071, p-value = 0.001) and R&D effort (β = 9.355, p-value = 0.057) favourably impact on acquisition activity. Overall, the estimated coefficients in Model 1 suggest a significant U-shaped relationship between Age and Acquisition Activity (Age: β =-0.009, p-value = 0.027; Age2: β = 0.00004, p-value = 0.033) and also a negative influence of FF on AA (β = -0.764, p-value = 0.013). In short, all the obtained findings indicate that Hypotheses 1 and 2 are supported.

4.1 Robustness checks

To confirm the robustness of the results, we use two different approaches. First, we observe the results sensitivity when using an alternative estimation method, such as the Generalized Estimation Equations (GEE). Thus, we also test our hypotheses using GEE, which accommodates the generalized linear models for panel data (Cameron & Trivedi, 2005) and has been used by prior literature when working with count and panel data (Mazelli et al., 2016). As there is no general agreement as to which method is better for handling panel count data, the negative binomial regression or the GEE estimator (Cameron & Trivedi, 2005, pp.809), we decide to use both methods: first, the negative binominal regressions to explain our main results and, second, the GEE approach to assess and demonstrate the robustness of our findings. In the last columns of Table 5, we display the same models verified through negative binomial regressions but using the GEE estimator. In these estimations, there are no changes in the coefficient signs and there is complete agreement as to which variables are significant, demonstrating the robustness of the findings.

Second, in Table 6, we test how the results vary using an alternative way of measuring our independent variable FF: we used Family Ownership Stake (FOS). When estimating all models using FOS instead of FF, the findings remain qualitatively similar to those we have previously reported for both the non-linear random effects panel regressions and the GEE.

Finally, in Table 7 we also test the robustness of our findings by using an alternative measure of the dependent variable, i.e., Likelihood of Acquisitions, which takes the value 1 if the firm has conducted at least an acquisition in the analyzed year and 0 otherwise. The estimations have been carried out using both Logit models with random effect and Generalized Estimation Equations (GEE). The signs and the coefficients’ significance show a very similar behavior to that of Tables 5 and 6, which indicates that the estimates are not altered by small variations in model assumptions.

5 Discussion

This study examines the previously unexplored relationship between firm age and acquisition activity in a specific and peculiar under-researched context, the Asia-Pacific region. Moreover, this study also investigates whether family firms diverge from non-family firms in their acquisition activity. The empirical findings support our theoretical predictions of a curvilinear relationship between firm age and acquisitions, with younger and older firms developing a higher number of acquisitions than middle-age firms. Furthermore, the obtained results confirm that family firms follow different patterns than non-family firms with regard to their acquisition activity (Diéguez-Soto et al., 2021; Gomez-Mejia et al., 2018; Hussinger & Issah, 2019). Specifically, the findings reveal that being a family firm undermines acquisition activity at every age.

5.1 Contributions

Our study offers important contributions to the literature. First, to the best of our knowledge, this is a pioneering study investigating firm age as an antecedent of acquisition activity. Concerning this, although prior research has identified many acquisition precedents, such as value creation, environmental factors or firm characteristics like acquisition experience or firm strategy (Haleblian et al., 2009), no study has considered the impact of age on acquisitions, remaining unclear so far how acquisition activity evolves as firms age. Drawing on the recent theoretical and empirical literature in firm age (Coad, 2018), which emphasizes the need to further study the influence and effects of firm age to better comprehend strategic decision making and its effects on firms’ outcomes (Coad et al., 2018), we include firm age as a precursor of acquisitions, to improve the understanding of firms’ acquisition activity at distinct ages.

Second, this paper also contributes to the family firm research field, as the acquisition strand within this field has hardly been studied, with remarkable exceptions (Cuevas-Rodríguez et al., 2023; Gomez-Mejia et al., 2018; Hussinger & Issah, 2019; Miller et al., 2010), the dissimilarities in acquisition activity between family and nonfamily firms. By providing theoretical arguments about the differences in acquisition activity between family and non-family firms derived from the chrono context (De Massis et al., 2018), we deepen on the circumstances in which family firms make this type of strategic decision. Additionally, we did not only use the family firm dichotomous categorization as previous research has traditionally done (Gomez-Mejia et al., 2018; Hussinger & Issah, 2019), but also performed robustness checks by using the level of family ownership, responding in this manner to the recent call for research of Hussinger and Issah (2019) on the degree of family influence on acquisition activity.

Third, in line with previous studies analysing family firms’ strategic decisions related to acquisitions (e.g. Gomez-Mejia et al., 2018), we account for the family firms’ emotional endowment to explain why they are differently disposed to acquisitions than their non-family counterparts. Thus, although we draw on the SEW perspective, our study goes further by considering how changes in SEW endowment as firms age (Brigham & Payne, 2019; Chua et al., 2015; Martínez-Romero & Rojo-Ramírez, 2016) may condition family firms’ behaviour with regards to acquisitions. In this vein, we contribute to the stream of research focused on the dynamism of SEW as firms evolve (Swab et al., 2020), taking into consideration the impact of SEW variations on family firms’ strategic decisions (Murphy et al., 2019; Nason et al., 2019). Thus, we extend previous literature analysing the impact of family influence on acquisitions based on the SEW approach (e.g. Cuevas-Rodríguez et al., 2023; Diéguez-Soto et al., 2021), by theoretically discussing how the chrono context, namely firm age, may vary the significance and direction of SEW when acquiring. In short, as well as very recent research has done (Cuevas-Rodríguez et al., 2023), our study makes a contribution to the comprehension of the SEW approach as complementary to the economic perspective, in unfolding strategic behaviour in family firms. However, our study differs from this latter work in that we theoretically argue how the SEW effects on acquisition activity may be chrono context dependent (Chua et al., 2015).

Finally, the specific context in which this study is developed, the Asia-pacific region, is a contribution per se, in as much as firms is this region differ from those in other regions of the world (Eddleston et al., 2020). Hence, previous research focused on acquisitions has been centred on either European (e.g. Menéndez-Requejo & Feito-Ruiz, 2008) or US (e.g. Strike et al., 2015) public firms, leaving aside Asia-pacific firms. Given the importance of M&A and the prevalence and longevity of family firms in this region, more research regarding the acquisition activity of Asia-pacific firms was urgently required (Chen et al., 2009; Worek, 2017). Indeed, prior research has evidenced that contextual, legal and institutional factors are conditions to be considered in family firm acquisition studies (Menéndez-Requejo & Feito-Ruiz, 2008; Requejo et al., 2018). Thereby, these boundary factors might clarify why family firms develop fewer acquisitions than their non-family counterparts (Diéguez-Soto et al., 2021; Gomez-Mejia et al., 2018). Additionally, the specificities of a region’s culture might explain the differential emphasis placed on SEW (Yang et al., 2020), conditioning thus, firms’ willingness towards acquisitions.

5.2 Practical implications

Our study offers some practical implications, which provide knowledge that is extensively applicable by managers, practitioners, policy makers and researchers. First, firm managers should consider the effect of age on different strategic decisions, such as acquisitions, whether they want to plan ahead, to continue to grow or to counter the effects of aging. Moreover, policy-makers require a good understanding of the firms needs and challenges at different ages, to design more effective policies targeted to a certain age group (Coad, 2018). In this sense, the requirements of young firms to carry out acquisitions, for example in terms of advice, will not be the same as those required by elderly firms, which might have developed previous acquisitions. Therefore, taking into consideration the inflection pointFootnote 1 in the relationship between firm age and number of acquisitions can be of utmost importance to knowing from which age firms’ needs, in terms of advice towards acquisitions, change. Moreover, this inflection point provides meaningful insights: the rate of acquisitions is reduced with firm age up to 100 years, when the rate is reversed. Therefore, in most cases the relationship between firm age and acquisition activity is negative and only in firms older than 100 years does the number of acquisitions start to increment. Accordingly, our sample of Asia-Pacific firms, with a great number of long-lived firms, is highly suitable to test the proposed model. Indeed, the obtained findings have methodological implications related to the need of including the full range of scores on the predictor variable when considering U-shaped models (Pierce & Aguinis, 2013). Regarding this, researchers are likely to derive conflicting conclusions regarding the firm age-acquisition relationship and overlook the presence of the quadratic effect when their data do not include the entire range of predictor scores (Pierce & Aguinis, 2013). Furthermore, the family nature of firms should be taken into consideration in the design of policies to promote acquisitions, as the needs and goals of family firms will differ from those of non-family firms. Governments should be conscious of the importance attached by family firms to their control concerns, professionalism challenges and emotional endowment when designing plans to foster efficient acquisitions, in an attempt to diminish these firms’ aversion to acquisitions. Our study also has practical implications for researchers, as it reveals a non-linear effect of age on acquisitions, justifying empirical approaches using quadratic terms for age (Coad, 2018). Finally, for family firm researchers the recognition of firm age as an independent variable, with important consequences on strategic decisions, also justifies empirical studies analysing its effects.

5.3 Limitations and future research avenues

The present study is not free of limitations, which in turn, provide opportunities for future research avenues. First, this work focuses on firm age as an antecedent of acquisition activity. Although this relationship is of utmost importance because it has not been investigated so far (Haleblian et al., 2009), it would be very interesting to go further and analyse the effects of such relationship on alternative firm performance indicators, by contemplating the acquisition activity as a mediating variable in the underexplored age-performance relationship (Coad, 2018). In relation to the above, we have measured firm age as the number of years since the firm was founded, which is considered “the gold standard for measuring firm age” (Coad, 2018 p.28). Nevertheless, other possibilities exist for measuring firm age, such as the number of years since the first time a firm opens a trading account with the bank (Coad et al., 2014), entries in a focal industry (Agarwal et al., 2004), or starts trading on a stock market (Demirel & Mazzucato, 2012). Second, while our variable for measuring acquisitions, i.e. number of acquisitions, is richer than the dummy variable used by prior research (Gomez-Mejia et al., 2018; Requejo et al., 2018; Strike et al., 2015), we were unable to measure some relevant acquisitions’ characteristics. In this vein, future research might deepen on acquisition heterogeneity by analysing aspects related to the announcement date, the volume of the deal, the method of payment, or even stage-wise acquisitions. To get “inside” the acquisition phenomenon, studies should focus on one particular event or a small set of acquisitions, and develop in-depth interviews, surveys and case studies (Haleblian et al., 2009).

Finally, although we justify the different family firms’ willingness to embark in acquisitions in comparison to non-family firms as they age, based on the SEW approach, we were unable to measure SEW directly. Nevertheless, our dichotomous family firm variable, as well as that considering the level of family ownership, accounts not only for family ownership, but also for family presence on the firm management and/or on the board. In any case, to the extent that our measures of family firms are based on archival data, a common practice in studies analysing acquisitions (Gomez-Mejia et al., 2018; Haleblian et al., 2009; Strike et al., 2015), we encourage future researchers to directly measure the different SEW dimensions (Berrone et al., 2012) and investigate their effects on family firms’ acquisition activity.

Notes

We calculate the inflection point of the negative binomial by applying the formula developed by Haans et al. (2016), i.e. \(\frac{{-\beta }_{2}}{{2\beta }_{3}}\), resulting in 100 years (Model 1 GEE, Table 5). This inflection point can be considered a robustness check of the U-shaped relationship between firm age and acquisition activity (Haans et al., 2016).

References

Agarwal, R., Echambadi, R., Franco, A., & Sarkar, M. (2004). Knowledge transfer through inheritance: Spin-out generation, development, and survival. Academy of Management Journal, 47(4), 501–522.

Anyadike-Danes, M., & Hart, M. (2018). All grown up? The fate after 15 years of a quarter of a million UK firms born in 1998. Journal of Evolutionary Economics, 28(1), 45–76.

Arikan, A. M., & Stulz, R. M. (2016). Corporate acquisitions, diversification, and the firm’s life cycle. Journal of Finance, 71(1), 139–194.

Arrondo-García, R., Fernández-Méndez, C., & Menéndez-Requejo, S. (2016). The growth and performance of family businesses during the global financial crisis: The role of the generation in control. Journal of Family Business Strategy, 7(4), 227–237.

Audretsch, D. B. (1995). Innovation, growth and survival. International Journal of Industrial Organization, 13(4), 441–457.

Baker, M., & Wurgler, J. (2004). A catering theory of dividends. He Journal of Finance, 59(3), 1125–1165.

Bammens, Y., Voordeckers, W., & Van Gils, A. (2008). Boards of directors in family firms: A generational perspective. Small Business Economics, 31(2), 163–180.

Barkema, H., & Schijven, M. (2008). Restructuring toward unlocking the full potencial of acquisitions: The role of organizational restructuring. Academy of Management Journal, 51(4), 696–722.

Bauguess, S., & Stegemoller, M. (2008). Protective governance choices and the value of acquisition activity. Journal of Corporate Finance, 14(5), 550–566.

Bauweraerts, J., Diaz-Moriana, V., & Arzubiaga, U. (2020). A mixed gamble approach of the impact of family management on firm ’ s growth: A longitudinal analysis. European Management Review, 17(3), 747–764.

Bennedsen, M., Nielsen, K., Perez-Gonzalez, F., & Wolfenzon, D. (2007). Inside the family firm: The role of families in succession decisions and performance. The Quarterly Journal of Economic, 122(2), 647–691.

Berrone, P., Cruz, C., & Gomez-Mejia, L. (2012). Socioemotional wealth in family firms: theoretical dimensions, assessment approaches, and agenda for future research. Family Business Review, 25(3), 258–279.

Bhattacharyya, N. (2007). Dividend policy: A review. Managerial Finance, 33(1), 4–13.

Birkinshaw, J., Bresman, H., & Håkanson, L. (2000). Managing the post-acquisition integration process: How the human iintegration and task integration processes interact to foster value creation. Journal of Management Studies, 37(3), 395–425.

Block, J., Miller, D., Jaskiewicz, P., & Spiegel, F. (2013). Economic and technological importance of innovations in large family and founder firms: An analysis of patent data. Family Business Review, 26(2), 180–199.

Brigham, K. H., & Payne, G. T. (2019). Socioemotional wealth (SEW): Questions on construct validity. Family Business Review, 32(4), 326–329.

Bureau Van Dijk (2020). Global M&A Review H1 2020.

Cameron, A., & Trivedi, P. K. (2005). Microeconometrics using stata. Stata Press.

Cameron, A., & Trivedi, P. K. (2010). Microeconometrics. Methods and applications. Cambridge University Press.

Candra, A., Priyarsono, D., Zulbainarni, N., & Sembel, R. (2021). Literature review on merger and acquisition. Estudios De Economia Aplicada, 39(4), 1–12.

Caprio, L., Croci, E., & Del Giudice, A. (2011). Ownership structure, family control, and acquisition decisions. Journal of Corporate Finance, 17(5), 1636–1657.

Cartwright, S., & Schoenberg, R. (2006). Thirty years of mergers and acquisitions re- search: Recent advances and future opportunities. British Journal of Management, 17(S1), S1–S5.

Casillas, J. C., Moreno, A. M., & Barbero, J. L. (2010). A configurational approach of the relationship between entrepreneurial orientation and growth of family firms. Family Business Review, 23(1), 27–44.

Casson, M. (1999). The economics of the family firm. Scandinavian Economic History Review, 47(1), 10–23.

Celikyurt, U., Sevilir, M., & Shivdasani, A. (2010). Going public to acquire? The acquisition motive in IPOs. Journal of Financial Economics, 96(3), 345–363.

Chen, Y. R., Huang, Y. L., & Chen, C. N. (2009). Financing constraints, ownership control, and cross-border M&As: Evidence from nine East Asian economies. Corporate Governance: An International Review, 17(6), 665–680.

Chrisman, J., Chua, J., Pearson, A., & Barnett, T. (2012). Family involvement, family influence, and family-centered non-economic goals in small firms. Entrepreneurship: Theory and Practice, 36(2), 267–293.

Chua, J. H., Chrisman, J. J., & De Massis, A. (2015). A closer look at socioemotional wealth: Its flows, stocks, and prospects for moving forward. Entrepreneurship Theory and Practice, 39(2), 173–182.

Churchill, N. C., & Lewis, V. (1983). The five stages of small business growth. Harvard Business Review, 61(3), 30–50.

Claessens, S., Djankov, S., Fan, J. P. H., & Lang, L. H. P. (2002). Disentangling the incentive and entrenchment effects of large shareholdings. The Journal of Finance, 57(6), 2741–2771.

Coad, A. (2018). Firm age: A survey. Journal of Evolutionary Economics, 28(1), 13–43.

Coad, A., Segarra, A., & Teruel, M. (2013). Like milk or wine: Does firm performance improve with age? Structural Change and Economic Dynamics, 24(1), 173–189.

Coad, A., Frankish, J. S., Nightingale, P., & Roberts, R. G. (2014). Business experience and start-up size: Buying more lottery tickets next time around? Small Business Economics, 43(3), 529–547.

Coad, A., Holm, J. R., Krafft, J., & Quatraro, F. (2018). Firm age and performance. Journal of Evolutionary Economics, 28(1), 1–11.

Cowling, M., Liu, W., & Zhang, N. (2018). Did firm age, experience, and access to finance count? SME performance after the global financial crisis. Journal of Evolutionary Economics, 28(1), 77–100.

Cruz, C., & Nordqvist, M. (2012). Entrepreneurial orientation in family firms: A generational perspective. Small Business Economics, 38(1), 33–49.

Cuevas-Rodríguez, G., Pérez-Calero, L., Gomez-Mejia, L., & Kopoboru Aguado, S. (2023). Family firms’ acquisitions and politicians as directors: A socioemotional wealth approach. Family Business Review. https://doi.org/10.1177/08944865231162404. Advance online publication.

Davarzani, B. L., Purdy, M., & Narsalay, R. (2014). Flying the nest in their own way. the internationalization of family firms in Asia Retrieved from https://www.accenture.com/in-en/_acnmedia/Accenture/Conversion-Assets/DotCom/Documents/Global/PDF/Dualpub_22/Accenture-Flying-NestOwn-Way-Internationalization-Family-Firms-Asia.

Davis, P., & Harveston, P. (1999). In the founder’s shadow: Conflict in the family firm. Family Business Review, 12(4), 311–323.

De Massis, A., Frattini, F., Majocchi, A., & Piscitello, L. (2018). Family firms in the global economy: Toward a deeper understanding of internationalization determinants, processes, and outcomes. Global Strategy Journal, 8(1), 3–21.

DeAngelo, H., & DeAngelo, L. (2007). Payout policy pedagogy: What matters and why. European Financial Management, 13(1), 11–27.

Debellis, F., Pinelli, M., Hülsbeck, M., & Heider, A. (2023a). Ownership, governance, and internationalization in family firms: A replication and extension. Small Business Economics. Advance online publication. https://doi.org/10.1007/s11187-023-00736-8

Debellis, F., Torchia, M., Quarato, F., & Calabrò, A. (2023b). Board openness and family firm internationalization: A social capital perspective. Small Business Economics, 60, 1431–1448.

Demirel, P., & Mazzucato, M. (2012). Innovation and firm growth: Is R&D worth it? Industry and Innovation, 19(1), 45–62.

Diéguez-Soto, J., López-Delgado, P., & Mariño-Garrido, T. (2021). The influence of family ownership on acquisition activity: The moderating role of acquisition experience. Journal of Small Business Management, 59(4), 819–851.

Durand, R., & Coeurderoy, R. (2001). Age, order of entry, strategic orientation, and organizational performance. Journal of Business Venturing, 16(5), 471–494.

Eddleston, K. A., Jaskiewicz, P., & Wright, M. (2020). Family firms and internationalization in the Asia-Pacific: The need for multi-level perspectives. Asia Pacific Journal of Management, 37(2), 345–361.

Ensley, M. D., & Pearson, A. W. (2005). An exploratory comparison of the behavioral dynamics of top management teams in family and nonfamily new ventures: Cohesion, conflict, potency, and consensus. Entrepreneurship Theory and Practice, 29(3), 267–284.

EY (2014). EY family business yearbook Retrieved from http://familybusiness.ey.com/pdfs/page-72–73.pdf

EY (2017). EY Family Business Yearbook. Retrieved from https://familybusiness.ey-vx.com/fb-yearbook-flipbook-2017/mobile/index.html#p=1

EY (2020). EY Family Business Yearbook. Family Business in Asia-Pacific: Facts and Figures

Fang, H., Kotlar, J., Memili, E., & Chrisman, J. J. (2018). The pursuit of international opportunities in family firms: Generational differences and the role of knowledge-based resources. Global Strategy Journal, 8(1), 136–157. & De Mas- sis

Fariñas, J. C., & Moreno, L. (2000). Firms’ growth, size and age: A nonparametric approach. Review of Industrial Organization, 17, 249–265.

Fotopoulos, G., & Giotopoulos, I. (2010). Gibrat’s law and persistence of growth in Greek manufacturing. Small Business Economics, 35, 191–202.

Franks, J., Mayer, C., Volpin, P., & Wagner, H. F. (2012). The life cycle of family ownership: International evidence. Review of Financial Studies, 25(6), 1675–1712.

Gedajlovic, E., & Carney, M. (2010). Markets, hierarchies and families: Toward a transaction cost theory of the family firm. Entrepreneurship Theory and Practice, 34(6), 1145–1172.

Gedajlovic, E., Carney, M., Chrisman, J. J., & Kellermanns, F. W. (2012). The adolescence of family firm research: Taking stock and planning for the future. Journal of Management, 38(4), 1010–1037.

Geiger, F., & Schiereck, D. (2014). The influence of industry concentration on merger motives—empirical evidence from machinery industry mergers. Journal of Economics and Finance, 38(1), 27–52.

Geroski, P. A. (1995). What do we know about entry? International Journal of Industrial Organization, 13, 450–456.

Gersick, K. E., Davis, J. A., Hampton, M. M., & Lansberg, I. (1997). Generation to generation: Life cycles of the family business. Harvard Business School Press.

Globerman, S., Peng, M. W., & Shapiro, D. M. (2011). Corporate governance and Asian companies. Asia Pacific Journal of Management, 28(1), 1–14.

Gomez-Mejia, L. R., Haynes, K., Núñez-Nickel, M., Jacobson, K., & Moyano-Fuentes, J. (2007). Socioemotional wealth and business risks in family-controlled firms: Evidence from Spanish olive oil mills. Administrative Science Quarterly, 52(1), 106–137.

Gomez-Mejia, L. R., Cruz, C., Berrone, P., & De Castro, J. (2011). The bind that ties: Socioemotional wealth preservation in family firms. The Academy of Management Annals, 5(1), 653–707.

Gomez-Mejia, L. R., Campbell, J. T., Martin, G., Hoskisson, R. E., Makri, M., & Sirmon, D. G. (2014). Socioemotional wealth as a mixed Gamble: Revisiting family firm R&D investments with the behavioral agency model. Entrepreneurship: Theory and Practice, 38(6), 1351–1374.

Gomez-Mejia, L. R., Patel, P. C., & Zellweger, T. M. (2018). In the horns of the dilemma: Socioemotional wealth, financial wealth, and acquisitions in family firms. Journal of Management, 44(4), 1369–1397.

Graebner, M. E., & Eisenhardt, K. M. (2004). The seller’s of the story: Adquisition as courtship and governance as syndicate in entrepreneurial firms. Administrative Science Quarterly, 49(3), 366–403.

Greenwood, R., Hinings, C. R., & Brown, J. (1994). Merging professional service firms. Organization Science, 5(2), 239–257.

Haans, R. F. J., Pieters, C., & He, Z. L. (2016). Thinking about U: Theorizing and testing U- and inverted U‐shaped relationships in strategy research. Strategic Management Journal, 37, 1177–1195.

Haleblian, J., Kim, J., & Rajagopalan, N. (2006). The influence of acquisition experience and performance on acquisition behavior: Evidence from the U. S. Commercial Banking Industry. Academy of Management Journal, 49(2), 357–370.

Haleblian, J., Devers, C. E., McNamara, G., Carpenter, M. A., & Davison, R. B. (2009). Taking stock of what we know about mergers and acquisitions: A review and research agenda. Journal of Management, 35(3), 469–502.

Hayward, M. L. A. (2002). When do firms learn from their acquisition experience? Evidence from 1990–1995. Strategic Management Journal, 23(1), 21–39.

Hilbe, C. (2011). Local replicator dynamics: A simple link between deterministic and stochastic models of evolutionary game theory. Bulletin of Mathematical Biology, 73(9), 2068–2087.

Hitt, M. A., Harrison, J. S., Ireland, R., & Best, A. (1993). Lifting the veil of success in mergers and acquisitions. Chicago.

Hülsbeck, M., Meoli, M., & Vismara, S. (2019). The board value protection function in young, mature and family firms. British Journal of Management, 30(2), 437–458.

Hussinger, K., & Issah, A. B. (2019). Firm acquisitions by family firms: A mixed gamble approach. Family Business Review, 32(4), 354–377.

Jaffe, D. T., & Lane, S. H. (2004). Sustaining a family dynasty: Key issues facing complex multigenerational business- and investment-owning families. Family Business Review, 17(1), 81–98.

Janson, L. (1994). Towards a dynamic model of post-acquisition cultural integration. In A. Sjögren, & L. Janson (Eds.), Culture and management. Institute ofInternational Business.

Jovanovic, B. (1982). Selection and the evolution of industry. Econometrica, 50, 649–670.

Kellermanns, F. W., Eddleston, K. A., Barnett, T., & Pearson, A. (2008). An exploratory study of family member characteristics and involvement: Effects on entrepreneurial behavior in the family firm. Family Business Review, 21(1), 1–14.

Kieschnick, R., & Moussawi, R. (2018). Firm age, corporate governance, and capital structure choices. Journal of Corporate Finance, 48, 597–614.

King, D. R., Dalton, D. R., Daily, C. M., & Covin, J. G. (2004). Meta-analyses of post‐acquisition performance: Indications of unidentified moderators. Strategic Management Journal, 25(2), 187–200.

Kraiczy, N. D., Hack, A., & Kellermanns, F. W. (2015). What makes a family firm innovative? CEO risk-taking propensity and the organizational context of family firms. Journal of Product Innovation Management, 32(3), 334–348.

Le Breton-Miller, I., & Miller, D. (2013). Socioemotional wealth across the family firm life cycle: A commentary on family business survival and the role of boards. Entrepreneurship Theory and Practice, 37(6), 1391–1397.

Lotti, F., Santarelli, E., & Vivarelli, M. (2009). Defending Gibrat’s law as a long- run regularity. Small Business Economics, 32, 31–44.

Lufkin, B. (2020). 12th February Why so many of the world’s oldest companies are in Japan. BBC.com. https://www.bbc.com/worklife/article/20200211-why-are-so-many-old-companies-in-japan

Lumpkin, G. T., & Brigham, K. H. (2011). Long-term orientation and intertemporal choice in family firms. Entrepreneurhip Theory and Practice, 35(6), 1149–1169.

Maksimovic, V., Phillips, G., & Yang, L. (2013). Private and public merger waves. Journal of Finance, 68(5), 2177–2217.

Martínez-Alonso, R., Martínez-Romero, M. J., & Rojo-Ramírez, A. A. (2022). Refining the influence of family involvement in management on firm performance: The mediating role of technological innovation efficiency. BRQ Business Research Quarterly, 25(4), 337–351.

Martínez-Alonso, R., Martínez-Romero, M. J., Rojo-Ramírez, A. A., Lazzarotti, V., & Sciascia, S. (2023). Process innovation in family firms: Family involvement in management, R&D collaboration with suppliers, and technology protection. Journal of Business Research, 157, 113581.

Martínez-Romero, M. J., & Rojo-Ramírez, A. A. (2016). SEW: Looking for a definition and controversial issues. European Journal of Family Business, 6(1), 1–9.

Martínez-Romero, M. J., & Rojo-Ramírez, A. A. (2017). Socioemotional wealth’s implications in the calculus of the minimum rate of return required by family businesses’ owners. Review of Managerial Science, 11(1), 95–118.

Mazelli, A., Kotlar, J., & De Massis, A. (2016). Blending in while standing out: Selective conformity and new product introduction in family firms. Entrepreneurhip Theory and Practice, 42(2), 206–230.

McConaughy, D. L., & Phillips, G. M. (1999). Founders versus descendants: The profitability, efficiency, growth characteristics and financing in large, public, founding-family-controlled firms. Family Business Review, 12(2), 123–131.

McKelvie, A., & Wiklund, J. (2010). Advancing firm growth research: A focus on growth mode instead of growth rate. Entrepreneurship Theory and Practice, 34, 261–288.

Mehrotra, V., Morck, R., Shim, J., & Wiwattanakantang, Y. (2013). Adoptive expectations: Rising sons in Japanese family firms. Journal of Financial Economics, 108(3), 840–854.

Menéndez-Requejo, S., & Feito-Ruiz, I. (2008). Family firm mergers and acquisition in different legal environments. Family Business Review, 23(1), 60–75.

Miller, D., Breton-Miller, L., I., & Lester, R. (2010). Family ownership and acquisition behaviour in publicy -traded companies. Strategic Management Journal, 31(2), 201–223.

Miller, D., Le Breton-Miller, I., Minichilli, A., Corbetta, G., & Pittino, D. (2014). When do non-family CEOs outperform in family firms? Agency and behavioural agency perspectives. Journal of Management Studies, 51(4), 547–572.

Muñoz-Bullon, F., Sanchez-Bueno, M. J., & Suárez-González, I. (2018). Diversification decisions among family firms: The role of family involvement and generational stage. BRQ Business Research Quarterly, 21(1), 39–52.

Murphy, L., Huybrechts, J., & Lambrechts, F. (2019). The origins and development of socioemotional wealth within next-generation family members: An interpretive grounded theory study. Family Business Review, 32(4), 396–424.

Naldi, L., & Davidsson, P. (2014). Entrepreneurial growth: The role of international knowledge acquisition as moderated by firm age. Journal of Business Venturing, 29(5), 687–703.

Nason, R., Mazzelli, A., & Carney, M. (2019). The ties that unbind: Socialization and business-owning family reference point shift. Academy of Management Review. Academy of Management.

Ortiz García de las Bayonas, J. M., Parra Meroño, M. C., & Wandosell Fernández de Bobadilla, G. (2023). What business model factors make SMEs more profitable? Small Business International Review, 7(1), e542.

Pellegrino, G. (2018). Barriers to innovation in young and mature firms. Journal of Evolutionary Economics, 28(1), 181–206.

Pierce, J. R., & Aguinis, H. (2013). The too-much-of-a-good-thing effect in management. Journal of Management, 39(2), 313–338.

Pinelli, M., Chirico, F., De Massis, A., & Zattoni, A. (2023). Acquisition relatedness in family firms: Do the environment and the institutional context matter? Journal of Management Studies, 1–28. https://doi.org/10.1111/joms.12932

Pittino, D., Chirico, F., Henssen, B., & Broekaert, W. (2019). Does increased generational involvement foster business growth? The moderating roles of family involvement in ownership and management. European Management Review, 17(3), 785–801.

Porter, M. E. (1985). Competitive advantage. Free Press.

PwC (2017). 20th CEO survey. Retrieved from https://www.pwc.com/gx/en/ceo-survey/2017/pwc-ceo-survey-report-2017.pdf

Requejo, I., Reyes-Reina, F., Sanchez-Bueno, M. J., & Suárez-González, I. (2018). European family firms and acquisition propensity: A comprehensive analysis of the legal system’s role. Journal of Family Business Strategy, 9(1), 44–58.

Sanders, W. M. G. (2001). Behavioral responses of CEOs to stock ownership and stock option pay. The Academy of Management Journal, 44(3), 477–492.

Schulze, W. S., Lubatkin, M. H., Dino, R. N., & Buchholtz, A. K. (2001). Agency relationships in family firms: Theory and evidence. Organization Science, 12(2), 99–116.

Schulze, W. S., Lubatkin, M. H., & Dino, R. N. (2003). Toward a theory of agency and altruism in family firms. Journal of Business Venturing, 18(4), 473–490.

Sciascia, S., Mazzola, P., & Kellermanns, F. W. (2014). Family management and profitability in private family-owned firms: Introducing generational stage and the socioemotional wealth perspective. Journal of Family Business Strategy, 5(2), 131–137.

Shanmugam, K., & Bhaduri, S. (2002). Size, age and firm growth in the Indian manufacturing sector. Applied Economics Letters, 9, 607–613.

Shi, W., Hoskisson, R. E., & Zhang, Y. A. (2017a). Independent director death and CEO acquisitiveness: Build an empire or pursue a quiet life? Strategic Management Journal, 38(3), 780–792.

Shi, W., Zhang, Y., & Hoskisson, R. E. (2017b). Ripple effects of CEO awards: Investigating the acquisition activities of superstar CEOs’ competitors. Strategic Management Journal, 38(10), 2080–2102.

Shim, J., & Okamuro, H. (2011). Does ownership matter in mergers? A comparative study of the causes and consequences of mergers by family and non-family firms. Journal of Banking and Finance, 35(1), 193–203.

Strike, V. M., Berrone, P., Sapp, S. G., & Congiu, L. (2015). A socioemotional wealth approach to CEO career horizons in family firms. Journal of Management Studies, 52(4), 555–583.

Swab, R. G., Sherlock, C., Markin, E., & Dibrell, C. (2020). SEW what do we know and where do we go ? A review of socioemotional wealth and a way forward. Family Business Review, 33(4), 424–445.

Szulanski, G. (1996). Exploring internal stickiness: Impediments to the transfer of best practice within the firm. Strategic Management Journal, 17(S2), 27–43.

Verbeek, M. (2004). A guide to modern economcetrics. Wiley.

Westhead, P. (2003). Company performance and objectives reported by first and multi-generation family companies: A research note. Journal of Small Business and Enterprise Development, 10(1), 93–105.

Worek, M. (2017). Mergers and acquisitions in family businesses: Current literature and future insights. Journal of Family Business Management, 7(2), 177–206.

Yang, X., Li, J., Stanley, L. J., Kellermanns, F. W., & Li, X. (2020). How family firm characteristics affect internationalization of Chinese family SMEs. Asia Pacific Journal of Management, 37, 417–448.

Zellweger, T. M., & Nason, R. S. (2008). A stakeholder perspective on family firm performance. Family Business Review, 21(3), 203–216.

Zozaya-González, N. (2007). Las fusiones y adquisiciones como fórmula de crecimiento empresarial. Dirección General de Política de la PYME. Ministerio de Industria, Turismo y Comercio

Funding

Funding for open access charge: Universidad de Málaga/CBUA.

Funding for open access publishing: Universidad Málaga/CBUA

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing interests

The authors have no relevant financial or non-financial interests to disclose.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

López-Delgado, P., Diéguez-Soto, J., Martínez-Romero, M.J. et al. Acquisition activity: do firm age and family control matter?. Eurasian Bus Rev (2024). https://doi.org/10.1007/s40821-024-00255-w

Received:

Revised:

Accepted:

Published:

DOI: https://doi.org/10.1007/s40821-024-00255-w