Abstract

Using a data set of German stocks that includes the financial crisis, this paper identifies market liquidity as the main driver of return seasonality. In comparison, the economic significance of order flow imbalance is markedly weaker. Applying panel regressions and controlling for unobserved effects, we investigate the effects of both variables simultaneously, together with dummies for calendar effects. US macroeconomic news announcements, which have been identified as one driver of return seasonality in previous studies using non-US data, are of little importance for our data set of German stocks.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

More than four decades ago, Fama (1970) published his seminal paper on efficient capital markets. Many empirical papers that appeared in the 40+ years since then described systematic deviations from the Efficient Markets Hypothesis, often referred to as anomalies. Whereas many such anomalies vanished shortly after their publication, others still persist (for an overview, see Zacks 2011). In particular, seasonal patterns with stock returns on specific days being systematically higher/lower than those on other days (e.g., the so-called turn-of-the-month effect) show remarkable persistence over time. This type of seasonality in returns is well-documented for several countries, and it has been existing for more than 20 years (Liu 2013). The literature considered three main potential reasons for return seasonality: order flow (or order imbalance), market liquidity, and announcements of macroeconomic news (see, e.g., Zwergel 2010).

The present paper documents seasonalities in returns on German stocks and tests these three potential drivers. Using a fixed-effects panel regression methodology, we investigate order imbalance and market liquidity simultaneously, controlling for unobserved effects. Previous studies have focused on only one of these explanations at a time. In addition, our focus on German stocks yields insights into a market which is relevant at the international level, but which has not yet been investigated to the same extent as, e.g., US markets. The paper contributes to the empirical literature in several ways: First, we document a relation between daily liquidity and return patterns of individual stocks, which provides evidence for market liquidity to play an important role for return seasonality. Second, in contrast to other studies, which analyze liquidity considerations of select groups of market participants, we find a link between aggregate order (flow) imbalance and return seasonality. However, despite its statistical significance, the effect of order imbalance on return seasonality is found to be negligible in economic terms. Third, whereas US macroeconomic news announcements have been documented to be an important driver of return seasonality in stock indices also outside the US (Nikkinen et al. 2007a, 2009), we find no significant effects of these announcements on return seasonality in individual German stocks.

The remainder of the paper is organized as follows: Sect. 2 gives an overview of empirical research on return seasonality and its main potential explanations discussed in the literature. Sect. 3 defines the variables and the regression models used. Sect. 4 describes our data together with the sample selection criteria applied. Sect. 5 presents our results, and Sect. 6 concludes.

2 Relation to the literature

Ariel (1987) first documents turn-of-the-month (TOM) effects for a US stock index. Lakonishok and Smidt (1988) confirm the effect for a wider sample period and drill the window of abnormal returns down to 1 day before and 3 days after the end of the month. Several other papers have since documented TOM effects for single stocks, other markets, and other asset classes (for an overview, see Liu 2013; Zwergel 2010). Analyzing S&P 500 ETFs, Liu (2013) shows that the TOM effect is still significant in the recent past and could have been exploited by a trading strategy from 2001 to 2011. However, the effect has shifted to 4 days before and 2 days after the end of the month, which is referred to as the Early TOM effect.

Despite this strong empirical evidence, the causes of the TOM effect are still unclear (Zwergel 2010). The most frequently investigated potential drivers are order (flow) imbalance, market liquidity, and macroeconomic news. The first goes back to Ogden (1990), who suggests that clustering in (US) payments around the month end causes an increase in stock returns. This idea has been taken up by several other researchers (see, e.g., Ziemba 1991; McConnell and Xu 2008; Etula et al. 2015). The general impact of order flow imbalance on returns is well-founded in theory, and there is also solid empirical evidence: Based on the notions of Stoll (1978) and Huang and Stoll (1997), a number of market microstructure models predict a positive relationship between order imbalances and subsequent price changes after excluding bid-ask bounce (e.g., Huang and Stoll 1994, 1997; Stoll 2000; Llorente et al. 2002; Chordia and Subrahmanyam 2004, 2008). Inventory and adverse selection concerns of market makers as well as serially correlated trading are the cornerstones of that link. For an overview of the empirical literature documenting the impact of order imbalance on returns for different assets and geographical regions, see Hanke and Weigerding (2015). The empirical observation that order imbalance itself shows a TOM effect (see Sect. 4) suggests its consideration as a potential driver of TOM effects in returns. Despite the sizeable literature on the link between order imbalance and asset returns, previous empirical evidence on seasonal imbalance patterns is scarce: Chang and Shie (2011) document that buying pressure in the Taiwanese futures market clusters in the last 30 minutes of a trading day. Su and Huang (2008) find that imbalance-related trading strategies for specific NASDAQ stocks are more profitable in the afternoon. Beyond the intra-day horizon, Lee et al. (2004) show that selling activity in the Taiwanese stock market is focused on Tuesday. Likewise, results from Visaltanachoti and Luo (2009) suggest that negative order imbalances on the Thai stock exchange bundle on Monday. By contrast, Chordia et al. (2002) analyze S&P 500 stocks and document that order imbalance is significantly higher on Tuesdays and Wednesdays. We are unaware of any papers documenting seasonality in order imbalance beyond those intra-day or weekday effects. The present paper closes this gap and documents that order imbalance in daily data shows seasonal effects. Although there is seasonality in order flow, the exact mechanism behind the impact of order imbalance on return seasonality is still not clear-cut. Several studies investigate flows of particular market participants, such as asset managers (e.g., McConnell and Xu 2008; Etula et al. 2015). McConnell and Xu (2008) apply a number of fundamental and stock-specific factors to US stock returns, and while TOM effects are somewhat more pronounced for small (and low-priced) stocks and stronger on year ends, McConnell and Xu (2008) cannot explain the seasonality by either size, price, volatility, the risk-free rate, US peculiarities, trading volume or flows to mutual funds. Results for the latter two variables in particular suggest that order flow may not be the main driver of end-of-period effects. The present paper goes one step further and investigates order flow imbalance directly and for the market aggregate (as opposed to focusing only on select market participants). We document that whereas the impact of order flow on return seasonality is statistically significant, it is negligible in economic terms.

The second explanation is somehow related to the payment considerations in Ogden (1990), but it covers a different aspect: applying mainly volume-related liquidity measures, Booth et al. (2001) find that vivid trading activity spurs stock returns around month ends of their Finnish stock market sample. Van den Tempel (2009) extends the analysis to stock indices of other developed countries. TOM effects tend to wane for two consecutive liquid months, where liquidity is measured by the Amihud (2002) ratio. Hong and Yu (2009) analyze the relationship between liquidity and monthly return seasonality. They show for a sample of 51 stock markets over several decades that lower returns during the summer months are related to lower trading volume and higher monthly closing bid-ask spreads. By contrast, Chang et al. (2010) concentrate on Japan and document only weak evidence of turnover-induced (monthly) return patterns. For our data set of German stocks, we find that liquidity (proxied by the bid-ask spread, the Amihud (2002) ratio and relative turnover) explains a sizeable part of return seasonality.

The third major explanation for seasonality is provided by Gerlach (2007) and Nikkinen et al. (2007b). They claim that seasonal clustering of US macroeconomic news announcements causes return seasonality in S&P 500 and S&P 100 index returns. Nikkinen et al. (2007a, 2009) extend the evidence to stock market indices from Finland, France, Germany, and the UK. For the German DAX they find a TOM effect 1 day after the end of the month. The effect becomes insignificant after controlling for announcements regarding employment, employment cost, industrial production and ISM indices. However, it remains unclear whether this macroeconomic news hypothesis holds true on other markets. Jalonen et al. (2010), e.g., do not find any supporting evidence on US and German government bond markets. The present paper analyzes effects on German stocks at the stock level (as opposed to the DAX aggregate). We find that macroeconomic news are no plausible explanation for the Early TOM or other seasonal patterns in this context, as they cluster in the first third of a month.

3 Methodology

3.1 Variables

3.1.1 Return

We compute daily log returns from the last mid-quotes before the closing auction:

where \(\text{ask}_{i,t}\) is the last ask quote for stock i before the closing auction of day t and \(\text{bid}_{i,t}\) the corresponding bid quote. Using mid-quotes instead of traded prices avoids any bid-ask bounce effects, which would induce negative first-order autocorrelation in returns (see, e.g., Roll 1984; Kaul and Nimalendran 1990; Jegadeesh 1990).

3.1.2 Liquidity measures

Market liquidity has several different aspects (see, e.g., Kyle 1985). Although our analysis is confined to daily data, the number of available liquidity proxies is still large. Fong et al. (2017) give an overview about daily and monthly liquidity measures on the stock market and compare their performance to high-frequency measures. The analysis reveals the closing percentage quoted spread and the Amihud (2002) ratio as the best daily liquidity proxies.

We therefore apply both measures in our study. In addition, we use daily relative turnover as a third proxy for liquidity, as it brings trading activity aspects to the analysis. The bid-ask spread is calculated as follows:

Following Amihud (2002), we calculate a second proxy for liquidity as

where any observations with a denominator of zero on a specific day are treated as missing. Whereas Amihud (2002) uses euro volume in the denominator, we proxy this data point by the product of the number of shares traded and the closing price (whereas the original definition of the measure uses the corresponding intra-day price for each trade). This minor adaptation is due to a large number of missing values for the euro volume in our data set.

Daily relative turnover, our third proxy for liquidity, is calculated as

3.1.3 Order imbalance

Our sample of microstructural trading data from Xetra allows for the identification of every single transaction as either buyer- or seller-initiated. Xetra is characterized by auctions and continuous trading. The latter is order-driven, but supplemented by designated liquidity providers, and it features an open order book (Deutsche Börse 2004). The Lee and Ready (1991) trade classification algorithm used in many previous quote-driven studies involving order imbalance is therefore not needed. By including both market orders and marketable limit orders, all traders demanding immediacy in execution are included in our order imbalance measure. However, the data do not contain canceled limit orders, which might have further increased the explanatory power of the imbalance measure (see Li et al. 2010).

Our approach in calculating order imbalance follows that of most previous studies. It is based on the number of buy or sell orders, as this measure tends to have the strongest link to return (see Chordia and Subrahmanyam 2004). Additionally, we scale order imbalance by the total number of trades to compare the data across stocks of different liquidity. Hence, we define the order (flow) imbalance as

3.1.4 News announcements

Nikkinen et al. (2007a) find that the announcements of data on US employment, the Employment Cost Index, industrial production, the ISM Manufacturing and the ISM Non-Manufacturing index significantly affect the return seasonality on the German stock market (at the index level). For this reason, we consider US macroeconomic news announcements as a further potential driver of return seasonality also at the level of individual German stocks. We take the dates of these news announcements as explanatory variables and create a dummy \(A_{a,t}\) (a = 1,\(\ldots\),5) for each of the five economic variables. It takes the value 1 on the days when the respective data are announced, and 0 otherwise.

3.2 Regression models and hypotheses

3.2.1 General remarks

Most papers on return seasonality compare average daily returns across stocks and time points. This methodology cannot fully control for stock-specific peculiarities or for several different effects simultaneously, which may distort the results. By contrast, we stack all observations across stocks in our sample and perform panel regressions. To capture seasonality in returns, we use dummy variables, partially interacted with order imbalance (see Sect. 3.2.2).

Unobserved effects such as market capitalization, which may be correlated with seasonal effects, might be present in our data. To assess whether the data correspond rather to a fixed or a random effects model, we perform Hausman (1978) tests. Estimators for the fixed and random effects model differ significantly (at the 1% level), which leads us to use a fixed-effects model.

We therefore account for stock-specific effects by applying the within transformation (see Wooldridge 2010, p. 302). For a generic variable X, unit-specific effects are removed using

where \(\bar{X_i}\) is the time-average of the observations on \(X_i\). When applied to return data, this transformation is equivalent to applying the constant-mean-return correction (see Brown and Warner 1985, pp. 4–5).

Preliminary data analyses reveal that the error terms are subject to heteroskedasticity. Robust standard errors are therefore calculated using the (diagonal) method suggested by White (1980).

While these statistical modifications enhance the analysis and increase the explanatory power of the results, it may be difficult to quantify the economic effects. To ease the comparison among calendar effects and their potential drivers we calculate the average economic effect by multiplying the coefficient by the average value of the respective independent variable. Since the independent variables focused in our study contain dummy components or are dummies themselves, we calculate the average across the non-zero observations of the dummy only, i.e.

for an interacted variable and

for a dummy variable, where \(\hat{\gamma _\bullet }\) are economic effects and \(\hat{\beta _\bullet }\) the corresponding coefficients. \(\mathbb {I}\) (\(\mathbb {T}\)) is the total number of stocks (time points) analyzed. \(Y_{i,t}\) is a non-dummy variable, \(Z_{i,t}\) is a dummy variable, and the wide tilde in \(\widetilde{Y_{i,t} \cdot Z _{i,t}}\) indicates that the interaction term is subjected to the within transformation described in Eq. (6).

3.2.2 Seasonality in returns

We investigate seasonal patterns for return, liquidity and order imbalance: Dummy variables for 14 days around the month, quarter and year end, denoted by \(M_{d,t},\) \(Q_{d,t}\) and \(Y_{d,t}\) respectively, are used to detect TOM effects. They take the value 1 on a specific day d around a month end and 0 on other days. Formally,

where \(d \in \mathbb {D} = \{ -\,7,\ldots, -\,1,1,\ldots, 7 \}.\)

Furthermore, we apply weekday dummies denoted by \(W_{w,t}\) for the first and last 2 days of a trading week:

where \(w \in \mathbb {W} = \{ 1, 2, 4, 5 \}\) and \(w = 1\) for Monday.

Finally, 11 month dummies, excluding August and denoted by \(N_{n,t}\), account for month effects:

where \(n \in \mathbb {M}\,=\,\{ 1,\,\ldots 7, 9,\ldots ,12 \}\) and \(n\,=\,1\) for January.

The fixed-effects regression model for seasonal return effects is specified as

where \(\epsilon _{i,t}^{r}\) is the error term for stock i at time t. We apply the within transformation defined in Eq. (6) and test the null hypotheses of \(\beta _d^r = 0\), \(\gamma _d^r = 0\), \(\delta _d^r = 0\), \(\zeta _w^r = 0\) and \(\eta _n^r = 0\) separately by means of two-tailed t-tests. The model comprises a total of 57 parameters (without fixed effects).

3.2.3 Effects of liquidity and order imbalance on returns

The impact of liquidity and order imbalance on return seasonality is captured by interacting the variables \(L^{\bullet }\) and I with seasonality dummies. As preliminary data analyses suggest that the liquidity-return and imbalance-return links last for several lags, we add (non-interacted) contemporaneous liquidity and order imbalance together with one of their respective lags as control variables. The fixed-effects regression model is specified as

where the within-transformation defined in Eq. (6) is used. We test the null hypotheses of \(\beta _d^{b} = 0\), \(\beta _{d,\cdot }^{c,\cdot } = 0\), \(\gamma _d^{b} = 0\), \(\gamma _{d,\cdot }^{c,\cdot } = 0\), \(\delta _d^{b} = 0\), \(\delta _{d,\cdot }^{c,\cdot } = 0\), \(\zeta _w^{b} = 0\), \(\zeta _{w,\cdot }^{c,\cdot } = 0\), \(\eta _n^{b} = 0\), \(\eta _{n,\cdot }^{c,\cdot } = 0\) and \(\theta _{p,\cdot }^{b,\cdot } = 0\), separately by means of two-tailed t-tests. The model comprises a total of 293 parameters (without fixed effects).

3.2.4 News announcement effects

In Sect. 3.1.4, we defined dummy variables indicating the announcement of certain macroeconomic news on a given trading day. Return is regressed on these dummy variables by means of the following model:

where we apply the within-transformation defined in Eq. (6).

The aim of this paper is to jointly test a number of explanations for return patterns given by previous papers, in particular, Nikkinen et al. (2007a). For this reason, we closely follow their approach, which is why we do not consider, e.g., German news announcements or sentiment data. Also similar to Nikkinen et al. (2007a), we use the residuals from Eq. (16) as dependent variable for Eq. (14) to investigate whether there are any seasonal return effects left after controlling for US macroeconomic news announcements.

4 Data

4.1 Initial data set

Our data set includes stocks traded on the German Xetra trading system starting from February 1, 2002, until September 30, 2009 (1950 trading days). For all stocks, prices, turnover, and the last available quotes before the closing auction together with order imbalances are available on a daily basis. Trading data are retrieved from Thomson Reuters Datastream, and the order imbalances are computed from data provided by the Karlsruher Kapitalmarktdatenbank. Quotes are adjusted backwards for capital measures such as dividend payouts, stock splits, reverse splits or repurchases. The macroeconomic news announcement dates are taken from the websites of the Bureau of Labor Statistics, the Federal Reserve and the Institute for Supply Management.

The sample selection described in Sect. 4.2 will result in one sample of daily data. To this end, a number of filtering or exclusion criteria are applied to eight subperiods: the calendar years from 2003 to 2008 and two somewhat shorter periods, from February 2002 to year-end and from the beginning of 2009 to the end of September.

4.2 Sample selection and validity checks

Three filtering criteria are applied to the initial data set. First, stocks with insufficient liquidity are excluded to avoid distorting the results (e.g., Chan and Fong 2000; Lo and Coggins 2006). We consider a stock to be sufficiently liquid if order imbalance can be computed. A stock is excluded from the sample in years for which order imbalance could not be calculated on each trading day. Second, ex-dividend days and days with capital changes (e.g., stock splits) are dropped. The corresponding dates are obtained from Thomson Reuters Datastream. Third, days with missing data are excluded. This affects 116 observations with missing quote data, 243 observations with missing Amihud (2002) ratios and all observations on August 24, 2009, which is a day that seems to have a data integrity issue. Another five stocks are excluded from specific subperiods or dropped completely because of incomplete data.

The sample is then checked for data errors and invalid observations. Four observations are dropped because of negative bid-ask spreads, one because of a negative number of shares traded. The remainder of the sample is checked for validity. First, one observation is excluded as order imbalance differs from the cross-sectional daily average by more than 1.0, and other market variables around that date do not support the extreme value. Second, six observations from two stocks are excluded due to bid-ask spreads larger than 20% of the bid quote. Another stock is dropped from the 2008 subperiod, since a share price slump leads to extraordinarily high bid-ask spreads for several weeks. Third, several stocks exhibit extreme returns on May 25 and May 26, 2005 although there are no unusual economic news, index returns or trading volumes on either of these days. To ensure data validity, we exclude May 25, 2005 for all stocks.

4.3 Final data set

The selection criteria and validity checks described in Sect. 4.2 reduce the initial data set of 1,225 stocks (624,236 data points) to 211 stocks [207,696 data points for Eq. (14) and 203,938 for Eq. (15)]. Table 1 provides the number of stocks in the various subperiods. The shorter subperiods 2002 and 2009 and a concentration of liquid stocks around 2007 bias our sample towards the financial crisis: 99,903 observations or 48% fall within the period from July 1, 2007 to September 30, 2009. We therefore run a robustness check for Eq. (14) focusing on this crisis period.

Despite this bias, the descriptive statistics in Table 2 document that buying and selling pressure as well as average daily returns are almost exactly balanced throughout our sample period. There is slightly stronger buying pressure and a somewhat negative stock return. The standard deviations point towards considerable variation, though. 1.6% of all order imbalances are \(\le -\,0.5,\) and 1.6% are \(\ge 0.5.\) The correlation analysis shows that while correlation is typically low between most variables (with the exception of the return/order imbalance and the bid-ask spread/Amihud (2002) ratio relation), there is a tendency towards strong autocorrelation in the liquidity measures. Order imbalance exhibits a marked degree of autocorrelation, as well.

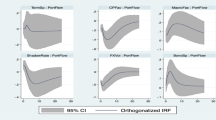

Figure 1 depicts the average variables around the month end. The top panel shows that bid-ask spreads are wider before the end of the month, and Amihud (2002) illiquidity spikes on day 1 after the month end (second panel). While turnover seems relatively stable in this illustration, these patterns support the idea that liquidity may be related to seasonal return effects. The case is even stronger for order imbalance (bottom panel): Imbalances are higher than usual between days − 3 to + 2 around the turn of the month. This finding substantiates the idea in Ogden (1990) that buying pressure clusters around month ends. Combining this observation with the general imbalance-return relation discussed in Sect. 2 suggests to consider order imbalance as a potential driver of TOM effects in returns. For German stocks, Hanke and Weigerding (2015) document a statistically significant relation between order imbalance and returns. However, they do not address the economic significance of this relation.

Turn-of-the-month effect in order imbalance and liquidity levels

Bid-ask spread (top panel), Amihud (2002) illiquidity (second panel), turnover (third panel) and order imbalance (bottom panel) around the turn-of-the-month

5 Results

5.1 Seasonality in returns

Table 3 reports the regression results for the seasonal return effects estimated using Eq. (14). Consistent with other markets, there is pronounced seasonality in German stock returns, and it remains remarkably stable when controlling for stock-specific effects and for several seasonal effects simultaneously: Coefficients are positive and significant 5 days before the end of a month (see parameter \(M_{-\,5, t}\) in Table 3), and then from 3 days before to 2 days after the end of a month (\(M_{-\,3, t}\) to \(M_{+\,2, t}\)). The average daily return is appr. 20–50 bp higher during that period. This is in contrast to previous papers, where positive returns were found to be concentrated on days after the month end. However, it confirms the Early TOM effect recently documented by Liu (2013), which stretches from days − 4 to + 2: The TOM effect seems to have shifted to earlier days. Days more distant from the TOM exhibit no clear pattern, with days + 4 to + 7 showing statistically significant returns with changing sign, but markedly smaller magnitude of around 10–20 bp per day (see \(M_{+\,4, t}\) to \(M_{+\,7, t}\)). The turn-of-the-year effect is M-shaped (see parameters \(Y_{-\,3, t}\) to \(Y_{+\,1, t}\)), with daily returns deviating by 40–110 bp from normal, but with varying signs. The insignificant coefficient on the very last day of a year (\(Y_{-\,1, t}\)) reflects that trading on this day is rather thin in Germany.

By contrast, quarter-end effects seem to counterbalance TOM and year-end effects: While the positive quarter effect is limited to 1 day after the turn of the quarter and amounts to 44 bp on average (see \(Q_{+\,1,t}\) in Table 3), the return during the week before a quarter end is significantly lower: Returns on those days are in total more than one percentage point smaller than on other days, ceteris paribus (see parameters \(Q_{-\,3, t}\) to \(Q_{-\,1, t}\)).

In addition, our sample reveals small, but statistically significant effects on Mondays, Tuesdays, and Fridays (all relative to Wednesdays). Moreover, returns in March/April are significantly positive. The significant negative returns from September to November are influenced by the financial crisis, where the year-end pattern is several times stronger compared to the non-crisis period and lasts until February. The economic impact of the month effects does not exceed 22 bp on average.

5.2 Impact of liquidity and order imbalance on return seasonality

Due to the large number of coefficients, the results from Eq. (15) are split across five tables: Table 4 shows the dummy variables (interacted and non-interacted) for the TOM effect only. For ease of comparison among the independent variables, it is focused on the average effect of each coefficient, which has been calculated by multiplying each coefficient by the average value of the respective independent variable. Average effects have been multiplied by \(10^{4}\). The significance of the coefficients is given, as well. For comparison purposes, the second column gives the original TOM effect from Eq. (14), where explanatory variables such as liquidity or order imbalances have not been considered. Tables 5, 6, 7 and 8 are structured similarly, but they focus on effects around the quarter end (Table 5), the year end (Table 6), across weekdays (Table 7) or months (Table 8).

Comparing columns 2 and 3 in Table 4 shows that the TOM effect shrinks markedly when including explanatory variables. Significance and average effects for the coefficients on days − 3 to + 2 are markedly lower with the coefficients on days − 1 to + 2 turning insignificant (see parameters \(M_{-\,3, t}\) to \(M_{+\, 2, t}\) in columns 2 and 3 of Table 4). Thus, a large part of the TOM effect is explained by liquidity and order imbalance (compared to the low explanatory power of US news shown in Sect. 5.3). The interacted variables in columns 4 to 7 show that liquidity variables are the more important driver for the TOM effect when compared to the economic effects of order imbalance (see parameters \(M_{- \,2, t}\) to \(M_{+\, 2, t}\) in columns 4 to 6 compared to column 7). The general relation between order imbalance and returns described by Hanke and Weigerding (2015) is statistically significant in our study as well, particularly around the month end, but its economic impact is small with average effects around 1 bp (see column 7). By contrast, liquidity variables explain return seasonality by up to appr. 15 bp (see columns 4 and 6). For instance, the TOM effect is significant when interacted with the Amihud (2002) ratio on days − 2 and + 1 (interacted parameters \(M_{- 2, t}\) and \(M_{+\,1, t}\) in column 5) or with bid-ask spreads on days − 1 and + 1 (interactions with \(M_{-\,1, t}\) and \(M_{+\,1, t}\) in column 4). Turnover seems to have significant explanatory power for the TOM effect on day + 1 (see \(M_{+\,1, t}\) in column 5).

The effects around the quarter end are also mostly picked up by liquidity variables. The negative seasonal effects on days − 3 to − 1 are markedly reduced (see \(Q_{-\,3, t}\) to \(Q_{-\,1, t}\) in columns 2 and 3 of Table 5). Instead, interacted variables with bid-ask spreads (see interaction with \(Q_{-\,2, t}\) in column 4), the Amihud (2002) illiquidity (day − 2 in column 5) and turnover (days − 3 and − 2 in column 6) have significantly negative coefficients. Their economic effects range from − 10 to − 90 bp. By contrast, most interactions with order imbalance are insignificant and their economic effects are small (see column 7). The positive quarter-end effect on day + 1 is not explained by any of the variables used in our setting (see interactions with \(Q_{+\,1, t}\) in columns 4 to 7).

Also the M-shaped positive year-end effect is markedly reduced when adding liquidity as explanatory variable. The positive non-interacted coefficients on days − 3, − 2 and + 1 turn insignificant or become negative (see parameters \(Y_{-\,3, t}\), \(Y_{-\,2, t}\) and \(Y_{+\,1, t}\) in column 3 in Table 6), while the coefficients interacted with liquidity are significantly positive. Their economic effects range from 20 to 160 bp and stretch across all 3 days in question and all three liquidity variables (see interacted effects for \(Y_{-\,3, t}\), \(Y_{-\,2, t}\) and \(Y_{+\,1, t}\) in columns 4 to 6). Economic effects from order imbalance are small in relation to these numbers (see column 7).

Weekday effects are affected by liquidity and order imbalance, too, but the direction of their influence is mixed. While the inclusion of additional variables amplifies the negative Tuesday effect (see column 3 in Table 7), the positive Friday effect is picked up by bid-ask spread (see columns 3 and 4).

The first half of the month effects, i.e., the positive coefficients in March and April seem to be related to liquidity. Adding interacted variables markedly shrinks both coefficients, the March coefficients becomes even negative (see March and April effects in columns 2 and 3 of Table 8). Likewise, there are significant positive interacted liquidity coefficients for March (bid-ask spread and turnover in columns 4 and 6) and April (Amihud (2002) ratio and turnover in columns 5 and 6). Order imbalance exhibits significant coefficients for February, April and October to December, but the effects are relatively small (see column 7), whereas the average liquidity effects are within the same range as the original month effects (compare columns 4, 5 and 6 to column 2).

Despite its strong influence, liquidity cannot explain seasonal effects completely in our setup, neither qualitatively nor quantitatively: Regarding qualitative explanations, the positive effect on the first day of a quarter is remarkably robust against inclusion of the interaction terms (see day + 1 in Table 5) and shows an economic effect of 44 bp (63 bp) without (with) interaction terms included. Liquidity does not explain anything of this phenomenon, and order imbalance accounts (only) for a small part. Hence, almost the entire effect remains unexplained by our economic variables, and therefore still a “calendar anomaly”. The same is true for the second half of the month effects (negative returns from September to November, see Table 8), which are reduced after including liquidity and order imbalance variables, but most of the interacted coefficients remain insignificant. Regarding quantitative explanations, consider the TOM effect in the interval \(-\, 3\le d\le -\, 2\): Table 4 shows that without liquidity or order imbalance as potential drivers, the effect is positive for all days with an economic impact between 33 and 52 bp (see parameters \(M_{-\, 3, t}\) and \(M_{-\, 2, t}\) in column 2). The interaction terms with liquidity pick up appr. half, which reduces the economic impact of the corresponding dummies to between 18 and 35 bp (see column 3). For these days, roughly half of the total effect can be explained by liquidity, with the other half still being absorbed by the calendar dummy.

Since explanatory and dependent variables are partly calculated from the same basic variables, there could be endogeneity problems in the regression results. For instance, bid-ask spreads and returns are both derived from bid and ask prices. The error terms from Eq. (15) and the explanatory variables could be related. To allow an assessment of the potential impact, Table 9 provides correlations between the basic explanatory variables and the errors. Given that all correlations are close to zero, we consider the risk of endogeneity problems in our setting to be low.

5.3 Impact of US news announcements on return seasonality

Simple frequency calculations show that the US macroeconomic news announcements that may be significant for the German market cluster on days 1, 3, and 5 after a month end, when data on employment and ISM indices are due. This pattern holds in the correlation between the news announcement dates and the seasonality dummy variables: Table 10 shows that there are positive, double-digit correlations on days 1, 3, and 5 after a month end (see parameters \(M_{+ 1, t}\), \(M_{+ 3, t}\) and \(M_{+ 5, t}\)). Correlations are also higher on days 1 and 3 after a quarter end (\(Q_{+ 1, t}\) and \(Q_{+ 3, t}\)) and on Fridays (\(W_{5, t}\)).

By contrast, while a number of seasonal effects in our analysis are piled up before the month end, very few news announcements fall into that period. Hence, the residuals from Eq. (16) still have pronounced seasonal effects after removing the influence of US macroeconomic news announcement dates (see Table 11 compared to Table 3): The TOM coefficient on day + 1 turns insignificant after controlling for news dates (see parameter \(M_{+ 1, t}\) in column 2). The same is true for the turn of the quarter effect on day − 1 (\(Q_{- 1, t}\) in column 4). Additionally, the TOM effects on days − 2 and − 1 are somewhat weaker (\(M_{- 2, t}\) and \(M_{- 1, t}\)). However, other seasonal effects are similar in size and significance both with and without US macroeconomic news announcement dates. Thus, the explanatory power of macroeconomic news announcements for return seasonality of single German stocks is confined to only very few days.

6 Conclusions and directions for further research

This paper sheds light on the drivers behind seasonality in German stock returns. Using a fixed-effects panel regression methodology, we analyzed liquidity and order imbalance simultaneously as potential explanatory factors. We found that market liquidity has the strongest influence on return patterns: Although we use daily data (as opposed to intra-day data), we find that the variation in bid-ask spreads and the Amihud (2002) ratio accounts for a sizeable proportion of return seasonality. Thus, liquidity seems to be a major driver behind calendar effects at the level of individual stocks. Future research should look more deeply into this relationship for intra-day data as the link may be even more pronounced there. Market liquidity considerations could also be the reason why the TOM effect recently has moved to earlier days, a finding from the recent literature that was confirmed in this paper. By contrast, a shift in return patterns cannot be explained by fixed-date macroeconomic news, which cluster in the first third of a month. Accordingly, we do not find evidence that US macroeconomic news announcements drive return patterns on a broader scale.

Its relation to liquidity dynamics may also explain why order flow is considered a seasonality driver. While most previous studies have focused on flow considerations of select investor groups, this paper analyzes order flow imbalances in aggregate, taking into account orders from all investors active in the market. This setup allows to verify that the variation in order imbalance is indeed related to return patterns. However, the impact of a change in order imbalance is small in economic terms. Besides, this study documents that order flow imbalance is subject to recurring patterns. This suggests that the general imbalance-return links found by previous studies may be partly related to calendar effects.

Limitations of our study could be seen in the news announcement variable indicating the announcement dates of US (instead of German) data. Similar to the approach in Nikkinen et al. (2007a), which we follow here, our study neglects news outside the US and the news direction (positive vs. negative). Moreover, we do not apply instrumental variable estimation, which might be another limitation in case there were endogeneity in the data set.

Our study focuses on the channels through which return patterns are affected, and it reveals liquidity as the main channel. To better understand the mechanisms behind this effect, future research should investigate the causes of fluctuations in liquidity. Kamstra et al. (2017), e.g., argue that mood changes may influence risk aversion during a year. While they suggest that mood changes influence stock return through fund flows, we could imagine that behavioral patterns can also explain fluctuations in liquidity. In addition, liquidity patterns around the month, quarter or year end may be driven by regulatory considerations or behavioral drivers. It therefore seems interesting to analyze whether there are common drivers affecting both return and liquidity.

References

Amihud, Y. 2002. Illiquidity and stock returns: Cross-section and time-series effects. Journal of Financial Markets 5: 31–56.

Ariel, R.A. 1987. A monthly effect in stock returns. Journal of Financial Economics 18: 161–174.

Booth, G., J.P. Kallunki, and T. Martikainen. 2001. Liquidity and the turn-of-the-month effect—evidence from Finland. Journal of International Financial Markets, Institutions and Money 11: 137–146.

Börse, Deutsche. 2004. Marktmodell Aktien. Xetra Release 7: 1.

Brown, S.J., and J.B. Warner. 1985. Using daily stock returns—the case of event studies. Journal of Financial Economics 14: 3–31.

Chan, K., and W.M. Fong. 2000. Trade size, order imbalance and the volatility–volume relation. Journal of Financial Economics 57: 247–273.

Chang, C.Y., and F.S. Shie. 2011. The relation between relative order imbalance and intraday futures returns: An application of the quantile regression model to taiwan. Emerging Markets Finance and Trade 47: 69–87.

Chang, Y., R. Faff, and C.Y. Hwang. 2010. Testing seasonality in the liquidity return relation—Japanese evidence. Applied Economics Letters 17: 951–954.

Chordia, T., and A. Subrahmanyam. 2004. Order imbalance and individual stock returns: Theory and evidence. Journal of Financial Economics 72: 485–518.

Chordia, T., R. Roll, and A. Subrahmanyam. 2002. Order imbalance, liquidity, and market returns. Journal of Financial Economics 65: 111–130.

Etula, E., Rinne, K., Suominen, M., and Vaittinen, L. 2015. Dash for cash: Month-end liquidity needs and the predictability of stock returns, SSRN working paper no. 2528692.

Fama, E. 1970. Efficient capital markets: A review of theory and empirical work. Journal of Finance 25 (2): 383–417.

Fong, K.Y.L., C.W. Holden, and C.A. Trzcinka. 2017. What are the best liquidity proxies for global research? Review of Finance 21 (4): 1355–1401.

Gerlach, J.R. 2007. Macroeconomic news and stock market calendar and weather anomalies. Journal of Financial Research 30: 283–300.

Hanke, M., and M. Weigerding. 2015. Order flow imbalance effects on the German stock market. Business Research 8: 213–238.

Hausman, J.A. 1978. Specification tests in econometrics. Econometrica 46: 1251–1271.

Hong, H., and J. Yu. 2009. Gone fishin’: Seasonality in trading activity and asset prices. Journal of Financial Markets 12: 672–702.

Huang, R.D., and H.R. Stoll. 1994. Market microstructure and stock return predictions. Review of Financial Studies 7 (1): 179–213.

Huang, R.D., and H.R. Stoll. 1997. The components of the bid-ask spread. Review of Financial Studies 10 (4): 995–1034.

Jalonen, E., S. Vähämaa, and J. Äijö. 2010. Turn-of-the-month and intramonth effects in government bond markets: Is there a role for macroeconomic news? Research in International Business and Finance 24: 75–81.

Jegadeesh, N. 1990. Evidence of predictable behavior of security returns. The Journal of Finance 45: 881–898.

Kamstra, M.J., L.A. Kramer, M.D. Levi, and R. Wermers. 2017. Seasonal asset allocation: Evidence from mutual fund flows. Journal of Financial and Quantitative Analysis 52: 71–109.

Kaul, G., and M. Nimalendran. 1990. Price reversals: Bid-ask errors or market overreaction? Journal of Financial Economics 28: 67–93.

Kyle, A. 1985. Continuous auctions and insider trading. Econometrica 53 (6): 1315–1335.

Lakonishok, J., and S. Smidt. 1988. Are seasonal anomalies real? A ninety-year perspective. The Review of Financial Studies 1: 403–425.

Lee, C., and M. Ready. 1991. Inferring trade direction from intradaily data. Journal of Finance 46: 733–746.

Lee, Y.T., Y.J. Liu, R. Roll, and A. Subrahmanyam. 2004. Order imbalances and market efficiency: Evidence from the Taiwan stock exchange. Journal of Financial and Quantitative Analysis 39: 327–341.

Li, M., M. Endo, S. Zuo, and K. Kishimoto. 2010. Order imbalances explain 90% of returns of Nikkei 225 futures. Applied Economic Letters 17 (13): 1241–1245.

Liu, L. 2013. The turn-of-the-month effect in the S&P 500 (2001–2011). Journal of Business and Economics Research 11: 269–275.

Llorente, G., R. Michaely, G. Saar, and J. Wang. 2002. Dynamic volume–return relation of individual stocks. Review of Financial Studies 15 (4): 1005–1047.

Lo, K., and R. Coggins. 2006. Effects of order flow imbalance on short-horizon contrarian strategies in the Australian equity market. Pacific-Basin Finance Journal 14: 291–310.

McConnell, J.J., and W. Xu. 2008. Equity returns at the turn of the month. Financial Analysts Journal 64: 49–64.

Nikkinen, J., P. Sahlström, and J. Äijö. 2007a. Do the US macroeconomic news announcements explain turn-of-the-month and intramonth anomalies on European stock markets? Journal of Applied Business and Economics 7: 48–62.

Nikkinen, J., P. Sahlström, and J. Äijö. 2007b. Turn-of-the-month and intramonth effects: Explanation from the important macroeconomic news announcements. Journal of Futures Markets 27: 105–126.

Nikkinen, P.J., K.T. Sahlström, and J. Äijö. 2009. Turn-of-the-month and intramonth anomalies and U.S. macroeconomic news announcements on the thinly traded Finnish stock market. International Journal of Economics and Finance 1: 3–11.

Ogden, J.P. 1990. Turn-of-month evaluations of liquid profits and stock returns: A common explanation for the monthly and January effects. Journal of Finance 45: 1259–1272.

Roll, R. 1984. A simple implicit measure of the effective bid-ask spread in an efficient market. The Journal of Finance 39 (4): 1127–1139.

Stoll, H.R. 1978. The supply of dealer services in securities markets. The Journal of Finance 78 (4): 1133–1151.

Stoll, H.R. 2000. Friction. The Journal of Finance 55 (4): 1479–1514.

Su, Y.C., and H.C. Huang. 2008. Dynamic causality between intraday return and order imbalance in NASDAQ speculative top gainers. Applied Financial Economics 18: 1489–1499.

Subrahmanyam, A. 2008. Lagged order flows and returns—a longer-term perspective. The Quarterly Review of Economics & Finance 48: 623–640.

Van den Tempel, C. 2009. The turn-of-the-month effect in stock returns investigated during crisis times and (il)liquid periods. Master’s thesis, University of Amsterdam.

Visaltanachoti, N., and R. Luo. 2009. Order imbalance, market returns and volatility: Evidence from Thailand during the Asian crisis. Applied Financial Economics 19 (17): 1391–1399.

White, H. 1980. A heteroskedasticity-consistent covariance matrix estimator and a direct test for heteroskedasticity. Econometrica 48: 817–838.

Wooldridge, J.M. 2010. Econometric analysis of cross-section and panel data. Cambridge: The MIT Press.

Zacks, L. 2011. The handbook of equity market anomalies—translating market inefficiencies into effective investment strategies. New York: Wiley.

Ziemba, W.T. 1991. Japanese security market regularities: Monthly, turn-of-the-month and year, holiday and golden week effects. Japan and the World Economy 3: 119–146.

Zwergel, B. 2010. On the exploitability of the turn-of-the-month effect—an international perspective. Applied Financial Economics 20: 911–922.

Author information

Authors and Affiliations

Contributions

MW carried out the statistical analyses. Both MW and MH drafted the manuscript. All authors read and approved the final manuscript.

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no competing interests.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Informed consent

For this type of study formal consent is not required.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Weigerding, M., Hanke, M. Drivers of seasonal return patterns in German stocks. Bus Res 11, 173–196 (2018). https://doi.org/10.1007/s40685-017-0060-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40685-017-0060-0