Abstract

In this research paper we used prospect theory (PT) to analysis the association between risk and dividend changes. We used global index (24 countries index data) data from 2000 to 2021. To improve PT, we suggest a novel alternative to the traditional reference point. Reference was established by tracking dividend growth or declines across sectors. The assumption is that before the end of the period, all the firms’ industrial dividend changes have to be known. In this research we calculated our reference point separately for individual years because the mean of industry dividend changes in the previous year. We utilised GMM estimation for the robustness test and split our sample up by business size, and we used 3 empirical methods (pooled regression, industry regression, and cross-sectional regressions analysis). Using the aforementioned empirical methods, we determined that dividend fluctuations are significantly correlated with a decrease in a company's risk. These findings imply that companies whose dividend changes are more than (less than) their benchmark will take on more (less) risk.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

It is common knowledge that dividends are frequently subjected to high rates of taxation, particularly in the United Kingdom, where the capital gains tax is lower than the dividend tax. Despite this common knowledge, researchers have spent the better part of the last few decades attempting to unravel the reasons why organizations pay dividends or why stockholders are interested in receiving dividends (Bozos et al., 2011). Miller and Modigliani (1961) were the first to argue that even in the most ideal circumstances for the capital markets, dividend policy has little or no impact on a company's value. Despite this, they came to the realisation that investment plans do in fact have an effect on the value of the company. Following in the footsteps of Miller and Modigliani, a number of researchers have investigated the question of whether or not announcements of changes to dividends communicate any information to the stock market and whether or not such announcements have any impact on the returns of the stock market (Aharony & Swary, 1980; Bozos et al., 2011; Das et al., 2023; Dasilas & Leventis, 2011; Hasan, 2021a, b; Hasan, 2022; Lonie et al., 1996; Nissim and Ziv, 2001; Petit, 1972).

Some studies feel that dividend increases (or cuts) transmit good (or negative) information about the worth of a company when they are announced (Al-Yahyaee, 2014; Ho & Wu, 2001; Kato & Loewentein, 1995; Nguyen, 2014). The bulk of research shows that dividend announcements have a substantial impact on stock performance (Dasilas & Leventis, 2011; Kumar, 2017; Pan et al., 2014; Yilmaz & Gulay, 2006).

Why companies pay dividends is a mystery to conventional finance, but this is a subject that behavioural finance seeks to answer. According to Shefrin and Statman (1984), one of the main reasons businesses embrace the behavioural dividend policy is because shareholders are more disciplined in their spending decisions. For this reason, when investors see a dividend uptick, they often incorrectly assume that the mean dividend growth rate has also risen.

Behavioural finance suggests a direct association between risk and dividend changes. Expected Utility Theory (EUT) (Von Neumann & Morgenstern, 1944) provides the theoretical foundation for the decision-making models in question, which typically include rational actors (Bernoulli, 1954). EUT is widely acknowledged as the primary instrument for investigating choice under uncertainty. Risk and dividend fluctuations are positively correlated, according to EUT. Despite the fact that EUT is the primary resource for making decisions, the data so far suggests that decision-makers often disregard its basic principles.

Based on EUT, Kahneman and Tversky developed a decision-making model under risk known as Prospect Theory (PT) (Kahneman & Tversky, 1979). Although PT is based on EUT, it violates the latter’s basic beliefs. Later, in 1992, Kahneman and Tversky extended PT and developed a new theory called Cumulative Prospect Theory (CPT) (Kahneman & Tversky, 1992). CPT helps decision-makers to take decisions on risky prospects with any predetermined number of results.

According to prior studies, the financial markets have a habit of responding more strongly to announcements of dividend cuts than announcements of dividend increases (Gebka, 2019; Hasan, 2021a, b). While this bimodal response to pricing did not entice many academics, (Gebka, 2019): Veronesi's (1999) model attributes this to the short-term uncertainty generated by the announcement of unexpected dividend reductions, while Allen and Michaely's (2003) model attributes it to the greater amplitude and lower frequency of dividend cuts than dividend increases. Baker et al. (2016) argue that the shift from conventional to PT attitudes among contemporary investors explains the asymmetry in price responses. On the other hand, Gebka (2019) argued that investors maintain their traditional beliefs. Gebka (2019) also mentioned that it is true that dividend increasing firms are high quality ones, but if dividend distribution costs go down, then low-quality firms can also increase their dividends. This means there is always an uncertainty between gains and losses.

According to the behavioural theory of firms, proposed by Bromiley (1991), firms take more risks when their dividends increases and low risks when dividends decrease. PT argues further that companies with dividend changes that are higher than the reference point are taking greater risks, while companies with dividend changes that are lower than the reference point are taking less risks. In this study, we established our hypothesis based on this realisation, which states that companies whose dividend changes are greater than (less than) their reference point are exposed to a greater level of risk, and that this level of risk will be reflected by a greater (smaller) dividend change distance.

Whilst PT's inception was tied to the process of decision-making at the human level, it has now found widespread use in corporate settings (e.g., Chang & Thomas, 1989; Fiegenbaum, 1990; Fiegenbaum & Thomas, 1988; Gooding et al., 1996; Johnson, 1994; Lee, 1997; Lehner, 2000; Miller & Bromiley, 1990). Keeping in view the importance of PT, we decided to study this filed in context of dividends growth. On this basis, we hypothesised that managers of companies with dividend growth below (above) their benchmark would be more inclined to take risks than managers of companies with higher dividend growth.

Managers determine the reference point for dividend payouts based on factors such as past dividend levels, market expectations, and other relevant considerations. The reference point plays a significant role in influencing dividend policy as managers aim to avoid negative outcomes or losses. By maintaining or increasing the current dividend level, managers align their decisions with the reference point. Future research can explore the specific factors and mechanisms involved in determining the reference point and its implications for dividend policy. Furthermore, Loss aversion can influence dividend policy during economic downturns. Managers may hesitate to reduce dividends due to loss aversion, even when it is financially advisable. This reluctance stems from a desire to avoid negative perceptions and maintain firm valuation. Further research can explore the impact of loss aversion on dividend reductions and investor perception.

Mental accounting also plays a role in dividend payout decisions. Managers may consider the impact of dividend payments on investors' mental accounting and the perceived utility of their investments. Behavioral biases related to mental accounting can influence dividend policy, as individuals tend to assign different levels of risk and utility to different accounts. Understanding these influences and biases can contribute to a deeper understanding of how mental accounting affects dividend decisions.

In this research paper we use 24 different countries stock market index data from 2000 to 2021. In here we use three types of Ordinary-Least-Squares method to estimate in equation form our hypothesis. After running all three types of Ordinary-Least-Squares method regressions, according to our findings, businesses that have dividend changes that are larger (or lower) than their reference point are prepared to take on a higher (or lower) amount of risk, which is in line with the predictions we made.

The index data often exhibit nonstationary behavior and volatility clustering, which can violate the assumptions of the GMM framework. We have taken steps to address this concern by applying appropriate transformations and robust standard errors to account for potential issues arising from nonstationarity and volatility clustering. However, we acknowledge that capturing these dynamics comprehensively is challenging. In our revised manuscript, we will provide a more thorough discussion of the limitations associated with these issues and their potential impact on the interpretation of our findings (Bollerslev, 2008; Hamilton, 2020).

The following are some ways that this study advances the body of literature: (a) According to the findings of this research, there is a link between exposure to risk and varying levels of dividends; (b) our research suggests a new alternative reference point which will resolve the problems sketched above. Finally, (c) Our results provide a unique addition to the existing research on the topic of the relationship among risk and dividend fluctuations.

The following is the structure of the paper: In the second portion, we established our hypothesis while also doing a literature study on the history of research pertaining to PT and dividends. The third portion covers topics such as determining the reference point, discussing our database, and doing empirical research. In part 4, we provide the outcomes of our research, and in Sect. "Robustness and endogeneity test", we detail our robustness testing. The sixth section of our article serves as our conclusion.

Literature Review and Development of Hypothesis

Prospect Theory

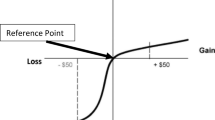

The PT model, which was created by Kahneman and Tversky (1979), is both one of the most well-known and significant models of decision making in situations where there is a degree of uncertainty (Evans & Bahrami, 2020; Wakker, 2010). It is one of the most effective theories in the subject of behavioural finance, and it has been applied to decision-making in the domains of finance, consumer choice, and political affairs. Behavioral finance is a discipline that studies human behaviour in relation to financial markets. The idea that people make decisions based on losses and gains in reference to a reference point rather than as final stages of wealth or welfare is the most important and significant invention that PT has brought into the world. This idea is known as reference dependence. There are three basic indications of reference dependency in PT: sign dependence is defined as an attitude towards risk or uncertainty that is reflected in a person's decision weights and how those weights change dependent on the result of the sign; diminishing sensitivity to results, which means that individuals are more sensitive to changes in results that are close to the reference point than to changes that are farther away from it; and A negative departure from the reference point has a greater effect than a positive deviation of the same magnitude, as a result of loss aversion and the utility unfolding, convexity for losses and concavity for gains. Individuals, in PT, seek to maximise the weighted sum of value rather than utility, where weights are not equivalent to probability (Kahneman & Tversky, 1979; Shiller, 2001).

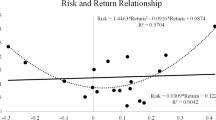

PT has the ability to capture a wide range of experimental evidence on attitudes to risk (Barberis et al., 2021; Kedarya et al., 2023). Most academics agree that prospect theory is the best currently available descriptive framework for decisions made in the face of uncertainty (Barberis, 2013; Starmer, 2000; Wakker, 2010). There are some crucial components of PT theory that have been ignored in the past when it comes to strategic applications. For the most part, decision makers utilise PT to analyse a risk in isolation, during which time they don't factor in their present wealth while doing so. The results of a company's risk-taking are affected by the way its leaders feel. The implications of PT for mixed bets are especially important since, if gambles are examined in isolation, both positive and negative outcomes are possible. When there is a negative link among risk and return above the reference point, higher-performing organisations have to be more risk-averse than lower-performing ones in order to remain competitive, and vice versa when the connection is positive below the reference point.

Prospect Theory and Dividend Policy

In recent years, dividend policy has emerged as one of the areas of behavioural finance that has received the greatest amount of academic attention. Throughout the research that has been done before on the topic of corporate payout policy, the choice to pay dividends or not has been analysed (for example, Al-Shattarat et al, 2017; Baker & Wurgler, 2004a, b; DeAngelo et al., 2004; Fama & French, 2001; Hasan, 2021a, 2022; Hasan & Islam, 2022 Kumar, 2017; Tsai & Wu, 2015), how much and how to pay-repurchases versus dividends (Jagannathan et al., 2000; Miller & Rock, 1985; Rozeff, 1982; Stephens & Weisbach, 1998). There have been studies that compare the dividend practises of common law and civil law nations, such as the one conducted by Ferris et al. (2009). The effect of corporate governance on payout policy has been studied by a number of academics (Chang et al., 2012; Jiraporn et al., 2011; Mitton, 2004; O'Connor, 2013, to name a few). Several forms of theory, including as catering theory, life cycle theory, and signalling theory, have been employed by researchers to undertake the aforementioned studies. Shefrin and Statmen (1986) and Ferris et al. (2010) examined dividend pay-out policy, but only Ferris et al. (2010) examined how often corporations should pay dividends when making the choice to pay dividends.

You may think of PT as a mathematically structured theory that replaces the probabilities with weights and the utility function with a value function in the context of anticipated utility theory. In PT, people prioritise outcomes based on their weighted sum of value rather than their utility (Kahneman & Tversky, 1979; Shiller, 2001). Kahneman and Tversky (1979) proposed a function of actual probabilities to derive the weights, which gave no weight to very low probability and gave one to extremely high probabilities. Alternatively, individuals tend to think very unlikely things won't happen and highly likely things will (Kahneman & Tversky, 1979). So, (in the preceding example provided by Allais (1953)) individuals would attribute a very high weight to occurrences which are extremely evident and minimal weight to events which are not very definite even though the price/constant is the same. Changing the probabilities in anticipated utility theory to weights allows for the study of "human behaviour towards risk."

Risk perception has a significant impact on a firm's dividend policy, as outlined by Prospect Theory (Kahneman & Tversky, 1979). Managers' perception of risk, influenced by the gain or loss domain, can shape their decisions regarding dividend payouts. In the loss domain, managers may exhibit risk-seeking behavior and opt for higher dividend payouts to offset perceived losses (Odean, 1998). Conversely, in the gain domain, managers may adopt a more conservative approach to dividend payouts, prioritizing retention of earnings for future investments or stability (Baker & Wurgler, 2004; Barberis et al., 2021). Additionally, behavioural biases that affect judgements about dividends based on gains or losses include the disposition effect.

The framing of dividend announcements or changes can influence investor reactions and subsequent dividend policy decisions. Prospect Theory suggests that investors may exhibit different responses to dividend increases compared to dividend decreases due to the framing effect (Kahneman & Tversky, 1979). When a dividend increase is framed as a gain or positive outcome, investors may respond positively. Conversely, when a dividend decrease is framed as a loss or negative outcome, investors may respond negatively. Future research can explore the framing effects of dividend announcements and changes to gain a deeper understanding of how different frames and reference points impact investor reactions and subsequent dividend policy decisions.

Cash dividend agreements that highlight the difference between 'problems of form' and 'issues of substance' are more attractive to investors. In conventional financial theory, a dividend payment in cash is equivalent to a stock dividend payment in terms of purchasing power. There's a growing body of research suggesting 'shape' is critical. Arrow (1982) discusses this body of work and uses a dramatic example from McNeill et al.'s (1981) research to highlight the significance of form. Decision-makers who are confronted with uncertain outcomes, according to Kahneman and Tversky (1979, 1981), tend to conflate matters of form with those of content.

After the dividend payment is set, some would argue that dividend frequency is irrelevant. In contrast, the increased utility obtained by investors from getting more frequent payouts is suggested by Kahneman and Tversky's (1979) PT and Thaler's (1980) mental accounting, which are both ignored by this reasoning. Together, these theoretical advances indicate significant forecasts about the payouts investors wish to receive. Investment utility is said to be concave across the domain of profits, according to PT. An investor's assessment of a dividend stream is affected by the way in which they evaluate gains over a concave utility function. Moreover, it implies that an investor's value of a total dividend payout will increase as dividend payment frequency increases. The concave utility function of PT, as stated by Barberis and Thaler (2003), provides the investor with a higher return.

Since investors always desire to obtain cash dividends, Kahneman and Tversky's (1979) theory predicts that people would prioritise firms based on the likelihood of receiving dividends from such companies before investing. Additionally, they hypothesise that people are risk-averse when it comes to investments that involve only gains, risk-seeking when it comes to investments that involve only losses, and fearful of losses more than gains when it comes to investments that allow for the possibility of either a gain or loss of equal magnitude. As a result, a typical Kahneman and Tversky value function is somewhat asymmetric in the single-variable scenario, being concave in gains and convex in losses.

PT has applications in economics, consumer behaviour, and policymaking. The most ground-breaking aspect of PT is the concept of reference dependency, which states that choices are made in light of gains and losses in comparison to some baseline, instead of as ultimate states of income or welfare. Sign dependency, decreased outcome sensitivity, and risk aversion are the three most prominent signs of benchmark reliance in PT. Individuals in PT want to maximise the weighted sum of value rather than utility, with weights not necessarily correlating to probability. PT is a formalised theory that replaces the probability and utility function of anticipated utility theory with weights and a value function, respectively. Individuals rate firms based on the likelihood of earning profits from that business prior to investment, as suggested by PT (Kahneman & Tversky, 1979).

Companies often evaluate their dividend growth or decline from year t-1 in relation to the dividend growth or decline of other companies in the respective industry, using their frame of reference as a benchmark. Based on our research, we know that companies have to decide their desired degree of risk for the next year t at the start of the preceding year t-1 when the average payout for the industry shifts. Under this hypothesis, the degree of risk associated with a company is quantified as the gap between its realised dividend yield and the industrial average payout fluctuates at year t.

One of the core ideas in finance is the trade-off between risk and reward, suggesting that investors require higher returns for assuming higher levels of risk. Dividend changes can be seen as indicators of a company's risk profile. In line with this tradeoff, companies that increase dividends beyond market expectations might be perceived as assuming lower levels of risk, as they commit to sharing profits with shareholders. On the other hand, companies that reduce dividends significantly might be viewed as taking on higher levels of risk, such as pursuing growth opportunities or addressing financial challenges. The risk-return trade off framework helps explain the relationship between dividend changes and risk and its implications for investors' risk perception (e.g., Black, 1972; Sharpe, 1964; Yao et al., 2020).

Our premise is that companies whose dividend changes fall below (or rise above) their benchmark will be more (or less) risky. The underlying idea behind this concept is that riskier businesses pay out larger dividends than safer ones. On the basis of these new considerations, we propose the following hypothesis:

H1: A negative association exits between a firm’s dividend changes within the industry and subsequent risk level.

According to signaling theory, dividend changes can act as a signal to investors regarding a company's financial health and future prospects (Bhattacharya, 1979; Ross, 1977). When a company increases its dividends, it may be viewed as a positive signal, indicating strong financial performance and confidence in future earnings. Conversely, a decrease in dividends might signal financial difficulties or a cautious outlook. Investors interpret these signals and adjust their risk perceptions accordingly. Signaling theory has been widely used to explain the relationship between dividend changes and risk (Baker & Wurgler, 2004; Lang & Litzenberger, 1989).

Furthermore, Agency theory suggests that the relationship between dividend changes and risk can be influenced by the agency problems inherent in the separation of ownership and control in corporations (Jensen, 1986) Dividend changes can serve as a mechanism for aligning the interests of shareholders and managers. For instance, managers might increase dividends to demonstrate their commitment to shareholder value and mitigate agency conflicts. Alternatively, managers may reduce dividends to retain earnings for investment opportunities, potentially increasing the risk profile of the firm. Agency theory provides insights into the dynamic between dividend changes, managerial decisions, and risk-taking behavior (e.g., (Fama & Jensen, 1983; Jensen, 1986).

Data and Empirical Analysis

Determination of the Reference Point

Identifying or establishing the PT reference point is a crucial step at the organisational level. It was stated by Kahneman and Tversky (1979) that there is no hard and fast criterion for establishing a PT benchmark. Nevertheless, they did note that the decision maker's goal may influence where the reference point was placed and how the result was coded as profits and losses. So far as we are aware, there has been no prior research on the relationship between risk and dividend payments under PT; hence, our research is the first in this field. However, if we look at the previous work related to risk-returns association under PT, we can observe that past studies have adopted a standard reference point at the sectoral level, which is often quantified by the average or median profits across all industries (Fiegenbaum, 1990; Fiegenbaum & Thomas, 1988; Johnson, 1994; Kliger & Tsur, 2011; Miller & Bromiley, 1990). Based on that assumption this research paper also uses industry the mean value of dividend changes as the reference point.

The limited control does pose challenges in precisely defining and measuring variables of interest, which can impact the establishment of causality or isolation of specific effects However, it is important to note that despite these challenges, index data still provides valuable insights and serves as a useful proxy for market-level analysis In our study, we have taken several steps to address these concerns and ensure the validity and reliability of our empirical findings.

Firstly, we have employed robust statistical methods, such as the Generalized Method of Moments (GMM) estimation, to account for potential endogeneity and mitigate biases arising from using index data (Arellano & Bond, 1991; Hansen, 1982). GMM estimation allows us to address endogeneity concerns by utilizing instrumental variables to strengthen the identification strategy (Blundell & Bond, 1998). Secondly, we have split our sample by business size and conducted various empirical analyses, including pooled regression, industry regression, and cross-sectional regression analysis. This approach helps us examine the relationship between dividend fluctuations and risk from different perspectives, enhancing the robustness and generalizability of our findings.

Furthermore, Regarding the selection of an unbalanced number of indices from different markets, we provide a robust justification based on the unique characteristics and dynamics of these markets. Our study aims to capture a diverse range of market conditions and variations in dividend changes by including indices from regions such as Asia, North America, and others. This approach enhances the robustness and applicability of our findings by incorporating different market perspectives and ensuring a comprehensive analysis of the association between risk and dividend changes.

Moreover, it is important to recognize that our study focuses on examining this association within the specific context of the selected indices. While the results derived from this dataset offer valuable insights, we acknowledge the potential limitations in generalizing these findings to other markets or time periods. The characteristics of the selected indices and the specific time frame analyzed may influence the observed relationships. To address these concerns, we will thoroughly discuss the implications and limitations of our dataset on the generalizability of our findings. We will provide a comprehensive analysis of the strengths and weaknesses associated with our sample selection and emphasize the need for cautious interpretation when extending the results to other market segments or time periods. By providing this justification and discussing the limitations, we aim to enhance the transparency and interpretation of our research outcomes.

In this work, we analyse two of Kliger and Tsur's (2011) findings and recommendations for a different kind of degermation for businesses. In the first method, we employ the average of dividend yield by industry to determine a reference point for the whole year, whereas in the second method, we utilise it only for businesses' choices in the succeeding period. In this research, we include the variable of time in our description of the connection between risk and dividend fluctuations, and we do so by using a weaker functional structure.

Data

Our study focuses on the association between risk and dividend changes using global index data, it is important to consider the influence of firm-level characteristics on the findings. Research has shown that firm-level characteristics and idiosyncratic factors can significantly impact the relationship between risk and dividend changes (Baker et al., 2002; Zhang & Semmler, 2009). We recognize that firm-specific factors, such as financial health, industry dynamics, and management decisions, can have an impact on both dividend policies and risk-taking behavior. While firm-level characteristics and idiosyncratic factors could indeed have an impact on the results, our research design and data scope necessitate a market-level perspective. By using index data, we capture the overall behavior of the market and investigate how dividend changes at the market level relate to risk preferences. Our aim is to provide insights into the general relationship between risk and dividend changes, which can have implications for understanding risk management strategies of companies as a whole. We believe that our approach of analyzing market-level data across multiple countries and over a long time period provides a broader perspective and enhances the generalizability of the findings. While firm-level analysis would undoubtedly be valuable, it falls outside the scope of our current study (Table 1).

The sample for this data collection is comprised of firms that are publicly traded on a range of stock exchanges located in twenty-four different countries. In our data set we have 19 countries from Europe, 2 from North America, 1 from Asia and 2 from Australia (See Table 2 for stock market list). The sample period is from 2000 to 2021. We only considered statements of the total dividend and did not include any announcements of the equity dividend or any other interim dividends for the timeframe in question. We used NAICS industry classification. The total sample covers 18 industries and 1952 firms. Win is our main independent variable and two other independent variables and interaction variables, first one is interacting between dividend changes and dividend increase dummy (DPI) and second, one is interactions between dividend changes and divided decrease dummy (DPD). Risk is our dependent variable.

Firm size, which was one of our control variables, was calculated by taking the natural logarithm of a company's market value. Larger organisations are acknowledged to perform better than smaller ones due to their extensive capabilities, which include their ability to conduct efficient operations and scale- and scope-related cost savings (Majumder, 1997; Penrose, 1995). Therefore, it should be clear how business size, firm returns, and market volatility are related. Increased debt can result in agency issues and underinvestment, according to Lazar (2016), who notes that leverage is a major determinant of a firm's profits (Ibhagui & Olokoyo, 2018). Table 1 contains the relevant traditional control variables.

The given dataset provides us with data for 24 countries, including 19 countries from Europe, 2 from North America, 1 from Asia and 2 from Australia. The number of observations broken down by country are shown in Table 3 below. 25,120 observations in total were made for this study. The country with the most observations (9420) is the USA, and the country with the fewest observations is Latvia (27). Based on the data shown in Table 4, we can determine that there were 1300 occurrences in the year 2021 and only 100 in the year 2000 (939). Traditionally, businesses have been categorised using the NAICS (North American Industrial Classification System) (see Table 5). The most observations are in NAICS 31–33, with 10,752; the fewest are in NAICS 55, with only 4.

Measures

Calculating the average of the business's dividend changes relative to its industry the year before yields the reference point for company I in industry j in year t, denoted by Ref (i,j,t).

where Mean (j,t−1) is the average rate of change (RDIV) in dividends for Business Sector j in Year t−1. We update our baseline yearly to account for the most recent information available on the true value of dividends in each individual sector.

From the literature we can see that some previous research has used the mean–variance approach to analyse this type of association. This method is valid only if the dividend change distribution stays the same during the research period. Let RDIV (i,j,t) represent the RDIV of company I operating in sector j in the year t. The following formula was used to determine RDIV:

where DIV0 is the dividend distributed in the first, or base, year and DIV-1 is the dividend distributed in the year before. Here we measure uncertainty annually for each company by summing the standard deviations of their dividend fluctuations.

We illustrate risk as a function of how the firm's yearly dividend change is distributed around the median dividend change for the industry as a whole. When a company has a good understanding of the causes of the exogenous elements that influence the entire industry but are beyond its control, it may better mitigate the negative consequences of those forces. To make it simpler, we can assume that in a similar way these factors can influence all our firms in a given industry.

Empirical Analysis

To put the central hypothesis to the test, we developed an empirical setup. This approach establishes a connection between the dividend change stance of a company and the associated amount of risk. There is a declared variable that indicates whether or not our company's dividend change is within or higher than the reference point, indicating where our company stands in terms of dividend changes. Below we provide a basic model to test the hypothesis:

In this case, I[RDIV (i,j,t-1) > Ref (I,j,t)] = I (win (i,j,t)]. If the given condition is true, the indicator function I[.] will keep returning the value 1, and else it will return 0. The phrase ε (i,j,t) is an unintended one. Risk as a result of the specified variable (ranking of dividend changes within the industry) is represented by the coefficient. Our hypothesis predicts that businesses with larger absolute dividend increases (those that are more than the reference point) would be more willing to take on risk than those with smaller absolute dividend changes (those that are less than the reference point).

To calculate Eq. 3, we use three variations of the Ordinary-Least-Squares technique: (a) a pooled regression, (b) individual regressions for 18 industries, and (c) yearly cross-sectional regressions for each year from 2000 to 2021 as a sensitivity check. Time, sector, and company-specific effects were filtered out by means of the inclusion of control variables.

Pooled Regression

Pooled regression was done based on Eq. 4. With Eq. 4 we included a dummy variable to control industry and time-specific effect (Year). We ran pooled regression using four different model specifications (we indicate the model as i, i = 1,…0.4):

\(i=1,\ldots {n}_{j}\); \(j=1,\ldots 18\); \(t=2001,\ldots 2021\);\(k=1, \ldots 17\);

\(\iota =2001,\ldots 2020\)where \({n}_{j}\) is the number of firms in industry j. \({I}_{{ind}_{i,j,t}}\) = I[k = j]; and \({I}_{{year}_{i,j,t}}\) = I[\(\iota\) = t]. \({\varepsilon }_{i,j,t}\) is error term. \({Risk}_{i,j,t}\) is our dependent variable. \({I}_{{win}_{i,j,t}}\) is independent variable. \(R\Delta DIV\) is the dividend changes in percentage. DPI is the dummy variables, where if dividend changes increase it takes value 1, otherwise 0. DPD is the dummy variables, where if dividend changes decrease it takes value 1, otherwise 0. Many firm-specific variables, such as return, log size, Leverage, ROE, Invest/A, log PPE, volatility, and shock, are included in the vector of controls because of their predictive power. We group the standard error by company.

Industry Regressions

To reduce the impact of both temporal and firm-specific characteristics in our industry regressions, we employed two dummy variables. Here we performed individual regression for each of the 13 industries (as we excluded utility and financial institutions; also, for two industries we did not have any observations in our final data set). The model we used to do the industry regressions is given as:

For, \({n}_{j} =1,\ldots 18\);\(i=1, \ldots {n}_{j}\); \(t=2001, \ldots 2021\);\(\iota =2001, \ldots 2020\)

\(m=1,\ldots {n}_{j-1}\)where, \({n}_{j}\) is the number of firms in industry j. \({I}_{{firm}_{m,j,t}}\)= I[m = i], and \({I}_{{year}_{i,j,t}}\)= I[\(\iota\) = t].

Summary of Statistics

Table 6 provides descriptive statistics for the variables. From Table 6 we can see that Risk mean value is 0.809 and minimum and maximum values are respectively 0 and 1.596. Mean value of our Win variable is 0.353. We can see that volatility and shock variables has very low mean values compared to other variables.

Table 7 provides the cross-correlation of our paper. From Table 7 we can see that risk has a positive correlation with reference point but has negative correlation with win variable, in both situations results are statically significant at 5% level. Reference point also negatively correlated with win and statistically 5% level significant.

Results

Baseline Model Specification

Table 8 displays the results of a regression analysis conducted on the baseline model. Four distinct model specifications, including industries and years, were employed in the baseline model regression study. The findings indicate a considerable negative relationship between the risk levels of the corporation and its dividend positions. Win is evidently statistically significant and negative in all four mode specifications. Our research shows that this notion is correct, and that firms that increase (decrease) their dividends by more than the benchmark are taking on greater risk.

Pooled Regression Analysis

The compiled regression results are shown in Table 9. We employed four distinct model parameters across sectors and time periods in our pooled regression analysis. The positions of the firm's dividend yield are significantly correlated negatively with their risk levels. In all four mode definitions, victory is negative and statistically significant. Our findings verify that businesses that experience a dividend adjustment above (below) the reference point do, in fact, take on more (less) risk than those that do not. From Table 9 we can also see that as expectedly when dividend changes interacted with dividend increase dummy all the results in all four models are statistically significant and positive, similarly when dividend changes interacted with dividend decrease dummy results in all four models are negative and statistically significant. These results are indicating that when dividend increases firms’ risks are increased and when dividend decrease then firms have less risk.

Industry Regressions Analysis

In the second specification, we ran regressions separately for each of the 18 industries. Table 10 shows that win is statistically significant for 14 industries out of 17 and win is negative in all 17 industries. On the other hand, constant is positive in all 17 industries. These findings are comparable to those obtained using pooled regression analysis, and they support our hypothesis that businesses that experience a dividend change that is more than or less than the reference point are more likely to be exposed to risk.

Robustness and Endogeneity Test

Cross-Sectional Regressions

We performed a different cross-sectional regression for every year between the years 2000 and 2021 so that we could examine the robustness of the results. In this cross-sectional regression we also included dummy variables to control industry specific effects:

for, \(i=1, \ldots {n}_{j}\); \(j=1,\ldots 18\); \(t=2000,\ldots 2021\);\(k=1,\ldots 17\);

where \({n}_{j}\) is the number of firms in industry j. \({I}_{{ind}_{i,j,t}}\) = I[k = j]; and \({\varepsilon }_{i,j,t}\) is error term.

Descriptive data for the yearly cross-sectional regression analysis are shown in Table 11. There is a comparative analysis of the pooled regression analysis outcomes in the rightmost column. The table shows that the mean value of win is similar to the pooled regression value. The coefficient δ mean value is (0.489) and the pooled regression value is (− 0.660). Our findings from a cross-sectional regression analysis performed annually reveal that victory is statistically significant at the 1% level every single year. This research corroborate the pooled regression findings indicating businesses that experience a dividend shift above (below) the baseline are taking on more (less) risk.

GMM Estimation

The robustness test based on GMM estimation using Eq. 4 is presented in Table 12. In this study, we use system GMM estimation instead of difference GMM estimation due to the former's superior performance and the latter's problematically weak instruments (Blundell & Bond, 1998). According to (Alonso-Borrego & Arellan, 1999). In comparison to one-step estimate, we found that two-step estimation was more accurate, therefore that's why we went with it (Alam et al., 2020). Many problems, including measurement errors, unobserved heterogeneity, endogeneity, and omitted variable bias, may be caused by reverse causality. These concerns are dealt with using the GMM estimating approach (Alam et al., 2019; Hasan et al., 2022; Mthanti & Ojah, 2017).

Table 12 results are consistent with our Tables 8 and 9, and consistent with our hypothesis. The data shows that companies with dividend changes above (below) the benchmark are more (less) risky.

Alternative Test

Here we provide the results of the further tests we conducted to back up our initial conclusions. In the first step, we separated the sample into two groups, one for small businesses and one for larger ones. The company is deemed tiny if its mean size is less than three dollars, and it is considered big if its mean size is six or seven dollars (Hasan et al., 2022). Results based on coefficients that account for the size of the firm are more robust. More cash dividends paid by a bigger company, for instance, mean less money available for investment in low- or no-payback ventures. In contrast, it is typical for small firms to invest more in positive investments and to pay no or little cash dividend, which will lower risk.

Firm size-based pooled regression estimate results are shown in Table 13. Column (1)–(4) shows that win value is negative which is consistent with our expectation, but the results are not statistically significant. This means that small size firms have less risk. On the other hand, from column (5)–(8) win value is statistically significant and shows negative sign. Our hypothesised greater (lower) degree of risk for companies with a dividend shift above (below) the reference point is supported by these findings, which are congruent with our benchmark simulated data.

Conclusion

This research paper employed PT to analyze the association between risk and dividend changes. We put forth an alternate starting point, which is a cornerstone of PT. In this research, we estimated risk by taking into account a company's current status, its planned actions, and the potential outcomes of those choices. This study's methodology rests on the central tenet that company behaviour and context remain static across time. The fundamental argument against this method is that the metric used is only valid if dividend changes are stable across the time period under consideration.

In addition, this study measured the reference point by industry dividend changes, the assumption being that before the end of the period all of a firm’s industrial dividend changes have to be known. Due to the fact that the median of the industry dividend varies from year to year, we determined our reference point on an annual basis individually.

We can observe that there is a substantial negative correlation between a company's dividend changes and its eventual risk level using all three empirical methodologies. These ways include pooled regression analyses, industry regression analyses, and cross-sectional regression studies. These findings provide credence to and provide evidence in support of our hypothesis, which states that companies whose dividend movements are more than (less than) their reference point take a greater amount of risk. Because of this, the dividend change distance will be greater (or lower), respectively.

Implications

The findings of this study have several implications for both researchers and practitioners in the field of finance. By utilizing Prospect Theory and examining the association between risk and dividend changes, this research sheds light on the complex relationship between these two variables. The significant correlation between dividend fluctuations and a company's risk suggests that dividend decisions can be indicative of a firm's risk management strategies. Understanding this association can help investors, financial analysts, and managers in making informed decisions regarding risk assessment and dividend policies.

Furthermore, the introduction of a novel alternative to the traditional reference point by tracking dividend growth or declines across sectors provides a valuable contribution to the literature. This approach allows for a more nuanced analysis of dividend changes and their impact on risk, considering industry-specific dynamics and benchmarks. Researchers can build upon this alternative reference point methodology to explore other dimensions of risk and dividend behavior in future studies.

Limitations and Future Directions

While this study provides important insights into the association between risk and dividend changes, there are several avenues for further research. Some potential future directions include: It would be beneficial to delve deeper into the mechanisms through which dividend changes are associated with risk. Exploring theoretical explanations, such as signaling theory, agency theory, and the risk-return trade-off, can provide a theoretical foundation for the observed relationship. Further investigation into these mechanisms can enhance our understanding of the underlying dynamics between risk and dividend changes.

This study focused on global index data from 24 countries, which provides a broad perspective. However, conducting a more detailed cross-country analysis can reveal potential variations in the relationship between risk and dividend changes across different markets, regulatory environments, and economic conditions. This can help identify country-specific factors that influence this association.

The current study analyzed data from 2000 to 2021, covering a substantial time period. However, extending the analysis further back in time or conducting a longitudinal analysis can provide insights into how the relationship between risk and dividend changes has evolved over different economic cycles and market conditions. The impact of dividend changes on investor behavior, market reactions, and stock prices can provide a comprehensive understanding of the implications of dividend fluctuations. This can include investigating the role of dividend changes in investor sentiment, market efficiency, and stock market volatility.

References

Aharony, J., & Swary, I. (1980). Quarterly dividend and earnings announcements and stockholders’ returns: An empirical analysis. Journal of Finance, 35, 1–12.

Alam, A., Uddin, M., & Yazdifar, H. (2019). Institutional determinants of R&D investment: Evidence from emerging markets. Technology Forecasting and Social Changes, 138, 34–44.

Alam, A., Uddin, M., Yazdifar, H., Shafique, S., & Lartey, T. (2020). R&D investment, firm performance and moderating role of system and safeguard: Evidence from emerging markets. Journal of Business Research, 106, 94–105.

Allais, M. (1953). Le Comportement de l’Homme rationnel devant le risque, critique des postulats et axiomes de l’Ecole Americaine. Econimetrica, 21, 441–451.

Allen, F., & Michaely, R. (2003). Payout policy. In G. M. Constantinides, M. Harris, & R. M. Stulz (Eds.), Handbook of the economics of finance (Vol. 1, pp. 337–429). North-Holland.

Alonso-Borrego, C., & Arellano, M. (1999). Symmetrically normalized instrumental-variable estimation using panel data. Journal of Business and Economic Statistics, 17(1), 36–49.

Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. The Review of Economic Studies, 58(2), 277–297.

Arrow, K. J. (1982). Risk perception in psychology and economics. Economic Inquiry, 2(1), 1–9.

Al-Yahyaee, K. H. (2014). Shareholders wealth effects of stock dividends in a unique environment. Journal of International Financial Markets, Institutions and Money, 28, 66–81.

Baker, H. K., Powell, G. E., & Veit, E. T. (2002). Revisiting managerial perspectives on dividend policy. Journal of Economics and Finance, 26, 267–283.

Baker, M., Mendel, B., & Wurgler, J. (2016). Dividend as reference point: A behaviour signalling approach. Review of Financial Studies, 29(3), 697–738.

Baker, M., & Wurgler, J. (2004). A catering theory of dividends. The Journal of Finance, 59(3), 1125–1165.

Baker, M., & Wurgler, J. (2004a). A catering theory of dividends. Journal of Finance, 59, 1125–1165.

Baker, M., & Wurgler, J. (2004b). Appearing and disappearing dividends: The link to catering incentives. Journal of Financial Economics, 73, 271–288.

Barberis, N. C. (2013). Thirty Years of Prospect Theory in Economics: A Review and Assessment. Journal of Economic Perspectives, 27(1), 173–196.

Barberis, N., & Thaler, R. H. (2003). A survey of behavioral finance. In Handbook of the economics of finance (pp. 1052–1121).

Barberis, N., Jin, L. J., & Wang, B. (2021). Prospect theory and stock market anomalies. The Journal of Finance, 76, 2639–2687.

Bernoulli, D. (1954). Exposition of a new theory on the measurement of risk. Econometrica, 22(1), 23–36.

Black, F. (1972). Capital market equilibrium with restricted borrowing. The Journal of Business, 45(3), 444–455.

Bhattacharya, S. (1979). Imperfect information, dividend policy, and the bird in the hand’’ fallacy. The Bell Journal of Economics, 259–270.

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143.

Bollerslev, T. (2008). Glossary to arch (garch). CREATES Research paper, 49.

Bozos, K., Nikolopoulos, K., & Ramgandhi, G. (2011). Dividend signaling under economic adversity: evidence from the London Stock Exchange. International Review of Financial Analysis, 20, 364–374.

Bromiley, P. (1991). Testing a causal model of corporate risk taking and performance. Academy of Management Journal, 34, 37–59.

Chang, B., & Dutta, S. (2012). Dividends and corporate governance: Canadian evidence. Journal of Applied Finance, 18(4), 5–30.

Chang, Y., & Thomas, H. (1989). The impact of diversification strategy on risk-return performance. Strategic Management Journal, 10, 271–284.

Das, B. C., Hasan, F., Sutradhar, S. R., & Shafique, S. (2023). Ukraine–Russia Conflict and Stock Markets Reactions in Europe. Global Journal of Flexible Systems Management, 24(3), 395–407.

Dasilas, A., & Leventis, S. (2011). Stock market reaction to dividend announcements: evidence from the Greek Stock Market. International Review of Economics and Finance, 20(2), 302–311.

DeAngelo, H., DeAngelo, L., & Skinner, D. (2004). Are dividends disappearing? Dividend concentration and the consolidation of earnings. Journal of Financial Economics, 72, 425–456.

Evans, S., & Bahrami, H. (2020). Super-Flexibility in Practice: Insights from a Crisis. Global Journal of Flexible Systems Management, 21(3), 207–214.

Fama, E. F., & French, K. R. (2001). Disappearing dividends: Changing firm characteristics or lower propensity to pay? Journal of Financial Economics, 60, 3–43.

Fama, E. F., & Jensen, M. C. (1983). Separation of ownership and control. The Journal of Law and Economics, 26(2), 301–325.

Ferris, S. P., Noronha, G., & Unlu, E. (2010). The more, the merrier: An international analysis of the frequency of dividend payment. Journal of Business Finance & Accounting, 37(1–2), 148–170.

Ferris, S. P., Sen, N., & Unlu, E. (2009). An international analysis of dividend payment behaviour. Journal of Business Finance & Accounting, 36(3–4), 496–522.

Fiegenbaum, A. (1990). Prospect theory and the risk-return association: An empirical examination of 85 industries. Journal of Economic Behavior and Organization, 14, 187–203.

Fiegenbaum, A., & Thomas, H. (1988). Attitudes toward risk and the risk-return paradox: Prospect theory explanations. Academy of Management Journal, 31, 85–106.

Gebka, B. (2019). Asymmetric price reactions to dividend announcements: Always irrational. Economics Letters, 185, 1–4.

Gooding, R. Z., Goel, S., & Wiseman, R. M. (1996). Fixed versus variable reference points in the risk-return relationship. Journal of Economic Behavior and Organization, 29, 331–350.

Hamilton, J. D. (2020). Time series analysis. Princeton University Press.

Hansen, L. P. (1982). Large sample properties of generalized method of moments estimators. Econometrica: Journal of the Econometric Society, 50(4),1029–1054.

Hasan, F. (2021a). Relationship between orthodox finance and dividend policy: A literature review. Indian-Pacific Journal of Accounting and Finance., 5(1), 13–40.

Hasan, F. (2021b). Dividend changes as predictors of future profitability. The Journal of Prediction Markets, 15(1), 37–66.

Hasan, F. (2022). Using UK data to study the effects of dividends announcements on stock market returns. The Journal of Prediction Markets, 16(2), 47–75.

Hasan, F., & Islam, M. R. (2022). The relationship between behavioural finance and dividend policy: A literature review. Academy of Accounting and Financial Studies Journal, 26(5), 1–11.

Hasan, F., Shafique, S., Das, B. C., & Shome, R. (2022). R&D intensity and firms dividend policy: Evidence from BRICS countries. Journal of Applied Accounting Research, 23(4), 846–862.

Ho, K. S., & Wu, C. (2001). The earnings information content of dividend initiations and omissions. Journal of Business Finance and Accounting, 28(7–8), 963–977.

Ibhagui, O. W., & Olokoyo, F. O. (2018). Leverage and firm performance: New evidence on the role of firm size. The North American Journal of Economics and Finance, 45, 57–82.

Jagannathan, M., Stephens, E. P., & Weisbach, M. S. (2000). Financial flexibility and the choice between dividends and stock repurchases. Journal of Financial Economics, 57(3), 355–384.

Jensen, M. C. (1986). Agency costs of free cash flow, corporate finance, and takeovers. The American Economic Review, 76(2), 323–329.

Jirporn, P., Kim, J., & Kim, Y. (2011). Dividend payouts and corporate governance quality: An empirical investigation. The Financial Review, 46, 251–279.

Johnson, H. J. (1994). Prospect theory in the commercial banking industry. Journal of Financial and Strategic Decisions, 7, 73–89.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47, 263–291.

Kato, K. and Loewentein, U. (1995). The ex-dividend-day bahevior of stock prices: the case of Japan. The Review of Financial Studies, 8(3), 817–847.

Kedarya, T., Elalouf, A., & Cohen, R. S. (2023). Calculating Strategic Risk in Financial Institutions. Global Journal of Flexible Systems Management, 24(3), 361–372.

Kliger, D., & Tsur, I. (2011). Prospect theory and risk-seeking behavior by troubled firms. The Journal of Behavioral Finance, 12, 29–40.

Kumar, S. (2017). New evidence on stock market reaction to dividend announcements in India. Research in International Business and Finance, 39, 327–337.

Lang, L. H., & Litzenberger, R. H. (1989). Dividend announcements: Cash flow signalling vs. free cash flow hypothesis? Journal of Financial Economics, 24(1), 181–191.

Lazar, S. (2016). Determinants of firm performance: Evidence from Romanian listed companies. Review of Economic and Business Studies, 17, 53–69.

Lee, D. Y. (1997). The impact of poor performance on risk-taking attitudes: A longitudinal study with a PLS causal modeling approach. Decision Sciences, 28, 59–80.

Lehner, J. M. (2000). Shifts of reference points for framing of strategic decisions and changing risk-return associations. Management Science, 46, 63–76.

Lonie, A. A., Abeyratna, G., Power, D. M., & Sinclair, C. D. (1996). The stock market reaction to dividend announcements: A UK study of complex market signals. Journal of Economic Studies, 23(1), 32–52.

Majumdar, S. K. (1997). The impact of size and age on firm-level performance: Some evidence from India. Review of Industrial Organization, 12, 231–241.

McNeill, B., Pauker, S. J., Sox, H. C., & Tversky, A. (1981). Patient preferences for alternative therapies, unpublished.

Miller, K., & Bromiley, P. (1990). Strategic risk and corporate performance: An analysis of alternative risk measures. Academy of Management Journal, 33, 756–779.

Miller, M., & Rock, K. (1985). Dividend policy under asymmetric information. Journal of Finance, 40, 1031–1052.

Miller, M., & Modigliani, F. (1961). Dividend policy, growth, and the valuation of shares. Journal of Business, 34, 411–433.

Mitton, T. (2004). Corporate governance and dividend policy in emerging markets. Emerging Markets Review, 5, 409–426.

Mthanti, T., & Ojah, P. (2017). Entrepreneurial orientation (EO): Measurement and policy implications of entrepreneurship at the macroeconomic level. Research Policy, 46(4), 724–739.

Nguyen, k. H. (2014). Impact of a dividend initiation wave on shareholder wealth. Applied Financial Economics, 24(8), 573–586.

Nissim, D., & Ziv, A. (2001). Dividend changes and future profitability. The Journal of Finance, 56(6), 2111–2133.

O’Connor, T. (2013). Dividend payout, corporate governance, and the enforcement of creditor rights in the emerging markets. Journal of Corporate Governance, 12(1), 7–34.

Odean, T. (1998). Volume, volatility, price, and profit when all traders are above average. The Journal of Finance, 53(6), 1887–1934.

Pan, R., Tang, X., Tan, Y. and Zhu, Q. (2014). The Chinese stock dividend puzzle. Emerging Markets Finance and Trade, 50(3), 178–195.

Penrose, E. (1995). The theory of the growth of the firm. Oxford University Press.

Petit, R. R. (1972). Dividend announcements, security performance, and capital market efficiency. Journal of Finance, 27, 993–1007.

Ross, S. A. (1977). The determination of financial structure: The incentive-signalling approach. The Bell Journal of Economics, 8(1), 23–40.

Rozeff, M. (1982). Growth, beta and agency costs as determinants of dividend payout ratios. Journal of Financial Research, 5, 249–259.

Sharpe, W. F. (1964). Capital asset prices: A theory of market equilibrium under conditions of risk. The Journal of Finance, 19(3), 425–442.

Shefrin, H. M. and Stateman, M. (1984). Explaining investor preference for cash dividends. Journal of Financial Economics, 13(2), 253–282.

Shefrin, H. M., & Stateman, M. (1986). Explaining investor preference for cash dividends. Journal of Financial Economics, 13, 253–282.

Shiller, R. J. (2001). Bubbles, human judgment, and expert opinion. Cowles Foundation for Research in Economics. Discussion Paper No. 1303.

Starmer, C. (2000). Developments in Non-expected Utility Theory: The Hunt for a Descriptive Theory of Choice under Risk. Journal of Economic Literature, 38(2), 332–382.

Stephens, C. P., & Weisbach, M. S. (1998). Actual share reacquisitions in open market repurchase programs. The Journal of Finance, 53(1), 313–333.

Thaler, R. H. (1980). Toward a positive theory of consumer choice. Journal of Economic Behavior and Organizations, 1, 39–60.

Tsai, H. J. and Wu, Y. (2015). Bond and stock market response to unexpected dividend changes. Journal of Empirical Finance, 30, pp. 1–15.

Tversky, A., & Kahneman, D. (1981). The framing of decisions and the psychology of choice. Science, 211, 453–458.

Tversky, A., & Kahneman, D. (1992). Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk and Uncertainty, 5, 297–323.

Veronesi, P. (1999). Stock market overreactions to bad news in good time: A rational expectations equilibrium model. Review of Financial Studies, 12, 975–1007.

Von Neumann, J., & Morgenstern, O. (1944). Theory of game and economic behavior. Princeton University Press.

Wakker, P. P. (2010). Prospect theory: For risk and ambiguity. Cambridge University Press.

Yao, W., Zhang, L., & Hu, J. (2020). Does having a semimandatory dividend policy enhance investor confidence? Research on dividend-financing behaviour? Economic Systems, 44, 100812.

Yilmaz, A. K. and Gulay, G. (2006). Dividend policies and price-volume reactions to cash dividend on the stock market: evidence from the Istanbul Stock Exchange. Emerging Markets Finance and Trade, 42(4), 19–49.

Zhang, W., & Semmler, W. (2009). Prospect theory for stock markets: Empirical evidence with time-series data. Journal of Economic Behavior & Organization, 72(3), 835–849.

Funding

No funding is associate with this research work.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no financial conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Hasan, F., Kayani, U.N. & Choudhury, T. Behavioral Risk Preferences and Dividend Changes: Exploring the Linkages with Prospect Theory Through Empirical Analysis. Glob J Flex Syst Manag 24, 517–535 (2023). https://doi.org/10.1007/s40171-023-00350-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40171-023-00350-3