Abstract

French insurance is part of a public–private partnership with the French State to compensate flood-related damages, and there is growing concern among insurers about damaging climatic events. To promote preventive actions as well as to take them into account in flood risk assessment, insurers have recently expressed the need to develop a rating system of preventive actions. This study identified Action Programs for Flood Prevention (Programme d’Action pour la Prévention des Inondations—PAPI) as the key French public policy instrument: they provide an overview of the diversity of actions that are conducted locally at the relevant risk basin scale. A database of all intended actions in the 145 launched PAPIs was constructed and the actions were coded (88 codes). The analysis consisted of two steps: (1) We conducted an expert valuation using the Analytic Network Process and the Analytic Hierarchy Process, aiming at creating an experimental national rating system. The results show the importance of implementing an integrated strategy that particularly emphasizes land use planning and urban planning. This appears even sounder as individual actions show relatively limited effectiveness. (2) The ratings of actions were applied to each PAPI according to their implemented actions. The resulting scores for individual PAPIs, as local risk coping capacity indicators, show great variance ranging from 8 to 324 points. This confirms the need to take prevention into account in flood risk assessment.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The French insurance industry is increasingly concerned about natural hazard-induced disasters. According to the press release of 4 July 2017 by the German reinsurer Munich Re, 2016 was the costliest year since 2012, with 167 billion Euros of damages worldwide related to natural hazard-induced disasters. Insurance companies in France play a central role in the compensation of damages caused by natural hazard-induced disasters. With the upward trend of reported damages and the expected increase in frequency and intensity of extreme events related to climate change (IPCC 2014), French insurance companies are getting increasingly involved in risk assessment and prevention enhancement.

1.1 The French Natural Disaster Compensation Scheme

In 1982, France made the political choice to establish, through the Act No. 82-600 of 13 July 1982, a national risk transfer scheme. It is based on the principle of national solidarity and relies on a public–private partnership between the insurance industry and the French State as its guarantor (Nussbaum 2015). This compensation scheme addresses the direct damages caused by major disasters (floods, droughts, earthquakes, and so on)Footnote 1 and is financed by a compulsory additional premium that is applied to all citizens who buy insurance to cover damage to property (home, car, business). This additional premium is calculated by applying a rate to the basic insurance policy premium, which is fixed by the state and the same for all citizens.Footnote 2

The insurance companies cannot bring the premiums in line with people and their property exposure or sensitivity, but must insure properties against natural hazard-induced disasters in all insurance contracts that cover damage to property. On average 664 million Euros are provided annually by the French insurance industry to compensate flood-related damages to property (AFA 2015). The French Insurance Association (l’Association française de l’assurance—AFA) expects this cost to double by 2040 (AFA 2015). In addition, the potential evolution of the political context, which includes the reform of the French compensation scheme and the new European solvency requirements, puts the question of natural disaster knowledge and prevention, including floods, into the spotlight.

1.2 The Importance of Prevention Knowledge and Assessment

The compensation scheme provides national coverage for damages caused by natural hazard-induced disasters, but also includes a preventive component. The Act of 1982 states that compensation should be provided only if the usual measures to prevent damages were not effective or could not be taken. Incentives for prevention have been reinforced through the 1995 introduction of the Risk Prevention Plan (RPP) that allows insurers to refuse insurance if buildings do not comply with RPP zoning or recommendations (Gérin 2011). The Act also established the Fund for the Prevention of Major Natural Risks (Fonds de Prévention des Risques Naturels Majeurs—FPRNM or “Barnier Fund”) in 1995, which is sustained by a 12% levy on the additional premiums related to natural disasters.Footnote 3 This state fund subsidizes various individual or collective prevention measures under certain conditions, including existence of a RPP (Nussbaum 2015). There is growing interest among French insurance companies to optimize this fund allocation, and the insurance companies have investigated the question of preventive measures, their efficiency, and the role that evaluative results would have in their relations with insured people and public authorities (Gérin 2011).

In 2000, following the severe floods and storms of 1999, the two French insurance trade associations established the Association of French Insurance Undertakings for Natural Risk Knowledge and Reduction (Mission Risques Naturels—MRN).Footnote 4 Part of the MRN’s mission consists of the development of specific tools for professional purposes to assess flood risk. Vulnerability has been identified by many authors and insurers as the core concept in flood risk assessment (Birkmann and Wisner 2006). The AFA expects damages linked to vulnerability factors (number, value, and distribution of assets) to increase 72% in the next 25 years, whereas the impact of climate change or annual climate variability is expected to play a smaller role (AFA 2015). Since its establishment, the MRN has supported Ph.D. research projects in collaboration with universities. This article is the result of one such project, initiated in 2014 between MRN and the urban planning laboratory Lab’urba, to develop an operational tool in order to integrate prevention into vulnerability assessment, as well as to improve prevention effectiveness knowledge in order to contribute to public policies.

2 Conceptual and Methodological Framework

Before assessing the French flood risk prevention actions, this section presents vulnerability and collective prevention actions and their interactions.

2.1 The Central Role of Risk Coping Capacity Within Vulnerability Assessment

Assessing vulnerability has been identified as a key component in developing more effective and efficient flood risk management (Guillier 2016a). Defining the concept of vulnerability appears nevertheless a complicated task because it is characterized by multiple meanings with respect to various disciplines or targeted objectives (Reghezza 2006). Considering that vulnerability refers to the propensity for damaging consequences, one way to assess it is loss measurement (Birkmann and Wisner 2006; Reghezza 2006). To some extent, compensated damages reveal a retrospective measure of potential loss and constitute a concrete and meaningful measure within insurance companies. This research focuses on direct material damages related to floods.

Assessing vulnerability ex ante is a great challenge that requires taking into account factors that contribute to it (Birkmann and Wisner 2006; Guillier 2016a). The identification of these root causes has been center stage in many research projects (Reghezza 2006). Two biophysical factors have long been identified: (1) exposure that refers to the degree or extent to which a system is in contact or subject to a perturbation (Gallopín 2006); and (2) sensitivity, or susceptibility, that defines the extent to which a system can be affected. Two houses, for example, may be exposed in the same way, but will be differently impacted according to their sensitivity—the amount of damage will not be the same (Bourguignon 2014). Research has also shown the influence of social factors, including institutional, economic, and demographic factors, as well as individual response capacity (D’Ercole et al. 1994). The evolution and diversification of flood risk management strategies outline the growing involvement of societies and the recognition of their capacity of action. To take account of this, we introduced a third factor—flood risk coping capacity, defined as “a combination of all strengths and resources available within a community or organization that can reduce the level of risk, or the effects of a disaster” (UNISDR 2002, p. 16). Insurance companies are now considering the importance of prevention in the measure of risk (Guillier 2016a). Flood risk coping capacity has an impact on exposure and sensitivity, and constitutes a central factor to understand vulnerability (Fig. 1). We also introduce an index to vulnerability (V0) as vulnerability is a variable that evolves over time as a function of factors external to the identified area—national policy frameworks, for example—and factors internal to the area, such as local development and prevention actions that are implemented.

Source: Adapted from Guillier (2017)

Vulnerability to flooding—a conceptual framework.

Prevention actions enhance risk coping capacity and contribute to stabilizing or reducing vulnerability. To assess flood risk coping capacity and how prevention actions influence it, we shall investigate at which scale the prevention actions have to be taken into account. Insurers are able to know what prevention actions each insured person has implemented at the individual level. However, knowing the existing actions at the collective level and their impacts still represents a great challenge. This study examined collective flood risk coping capacity.

2.2 The Collective Dimension of Risk Coping Capacity

To address flood risk coping capacity effectively, we have to consider the collective dimension of flood risk. Flood risk is collective with respect to insurance terms because the risk of one insured person to have his/her house flooded is not independent from the risk of his/her neighbor’s house being flooded. Flood risk is expected to impact multiple people at the same time. It is not an isolated and independent risk. Flood risk is also collective in terms of its management. More and more stakeholders are involved in flood risk assessment, decision making, and intervention. The diversification of actors has resulted from the administrative decentralization process during the second half of the twentieth century that gives increasingly more responsibilities to actors at the local level. Three main categories of actors are part of flood risk management in France (Ledoux 2006): the French State and its branches at more local levels (for example, Regional Directorate for Environment, Land Planning and Housing, Départemental Directorate for Territories); local authorities (such as inter-municipal cooperation body, municipalities); civil society and prevention experts, including insurance professionals, nongovernmental associations representing the environmental challenges, flood-damaged people, and so on, and private and public experts.

Implementing actions to enhance risk coping capacity thus calls for a great diversity of actors at different levels. Flood risk basins are considered to be the relevant scale within the French legal framework for flood risk management (FRM) (Guillier 2016b). A risk basin is defined, according to the National Data Reference Center (Service d’administration nationale des données et référentiels sur l’eau—SANDRE), as a homogenous geographical unit that is subject to the same natural phenomenon and cuts across administrative boundaries.Footnote 5 This reinforces the need for multiple actors to be involved in order to implement actions that will impact the whole risk basin. This diversity of actors at different levels implies a great variety of potential actions. We thus need to structure and categorize them to be able to evaluate their difference in impact on risk coping capacity and vulnerability.

2.3 Existing Strategies Towards Prevention

There is a number of ways to act to cope with flood risk. Based on the existing typologies of strategies (French national flood risk management policy, STAR-FLOOD European project, FloodSite European project, and so on), we consider six strategies of actions (Steinführer et al. 2009; Hegger et al. 2013; Guillier 2016a):

-

1.

Risk knowledge;

-

2.

Risk awareness through education and preventive information;

-

3.

Adaptation to risk, including control and mitigation of urbanization;

-

4.

Resistance to floods through hazard-oriented measures;

-

5.

Anticipation of floods through watercourse monitoring, forecasting, and vigilance;

-

6.

Reaction to floods, that is, coping capacity or crisis management.

Recovery and reconstruction are not included in our study. In the case of France, the capacity to recover is partly related to compensation through the French natural disaster compensation scheme settled at the national level (Larrue et al. 2016; Guillier 2016a). In addition, regarding our adopted definition of vulnerability, post-crisis measures have much less impact in reducing direct damages. The above six strategies stand for the collective prevention framework our research project aimed to assess. The texts of the French flood risk management policy and the National Strategy for Flood Risk Management, which was elaborated in 2014 in application of the EU Flood Directive, emphasize the principle of an integrated strategy, but indicate no explicit prioritization between strategies (MEDDE 2014). The absence of explicit prioritization may be interpreted in different ways: (1) all strategies have the same importance, which means that their impact on vulnerability is equal; (2) strategies have different impacts on vulnerability that are commonly shared at the national level, but not reported in the national strategy; and (3) strategies may have different impacts on vulnerability, but the “right” combination depends on the area concerned. To investigate the question of risk coping capacity, we examine to what extent each strategy impacts vulnerability to determine what would be the optimal combination of strategies to promote, whether there might be a national and shared combination of strategies, and whether all strategies have the same value.

2.4 Collecting Information About Collective Risk Coping Capacity

Despite the multiplicity of actors involved, the French State still represents the most important actor in French flood risk management (Larrue et al. 2016). As far as general interest is concerned, the French State is the predominant actor that intervenes (Dourlens 2003). As a consequence, public policies and public actions stand for collective capacities to face public problems.

Considering the relevant risk basin scale for flood risk management, the diversity of actors, and the tools/actions they can mobilize to enhance risk coping capacity, we identified the French Action Programs for Flood Prevention (Programme d’Action pour la Prévention des Inondations—PAPI) as the most relevant public policy instrument to analyze. The objective of the programs is to coordinate actions and actors at the risk basin scale and to develop a multi-year and integrated strategy that relies on the implementation of the other existing public policy tools. It is the only public policy tool that deals with flood risk and implements actions through seven axes that match all the strategies of flood risk coping capacity (Fig. 2) (Guillier 2016a).

PAPIs are a bottom-up public policy tool initiated by local actors on a voluntary basis. Local actors elaborate a project and identify the local authority (municipality, inter-municipal cooperation body, river syndicate, and so on) who will be in charge of carrying out the project. In a simplified way, the PAPI project, which consists of an application form, is then presented by the local authority in charge to the Regional Directorate for Environment, Land Planning and Housing and the National Flood Committee who will decide whether the project is accepted. If accepted, it will receive a subsidy from the Barnier Fund that will provide about 40% of the total PAPI budget.

Since its institution in 2002, 145 PAPIs have been accepted in France. Most PAPIs are a 6-year long program. Among the 145 PAPIs, some are already completed, others are ongoing projects; and some PAPIs will be launched in the next years. As PAPIs are local initiatives, the considered risk basin is also defined at local levels. As a consequence, some PAPIs consider large risk basins whereas others are on small risk basins (Erdlenbruch et al. 2009)—for example, the PAPI on the Dordogne risk basin is 24,000 km2 whereas the one on the Préconil risk basin is 60 km2.

This study is based on the assumption that the total 145 PAPIs—implemented in 112 risk basins that represent more than 40% of the area of France—offer an adequate prism to appreciate and assess risk coping capacity. Few studies are completed in France that address public policy evaluation, and real evaluation of PAPI implementation and published materials on the subject are very limited. Through PAPI, the program that tackles risk coping capacity through the six strategies and a wide range of other public policy instruments and actions, we investigate to what extent the strategies within risk coping capacity impact vulnerability and to what extent actions contribute to strategies.

3 Rating PAPIs: Material and Method

To assess flood risk coping capacity through PAPI, we develop a database of the different actions that can be implemented in PAPIs that will then be rated by using a multicriteria analysis method.

3.1 Construction of a PAPI Action Database

A database gathering the actions that will be or have been implemented in PAPIs was constructed based on the analysis of the 145 PAPI application forms. To be able to compare actions from one PAPI to another, a coding method was used: from a sample of PAPIs and existing recognized types of actions (subsidized actions, research work, and so on), 88 codes were determined to represent the diversity of actions within each PAPI (Guillier 2016a) (Table 1). For instances, hydraulic modeling (for example, flow velocity) and hydrologic modeling (for example, mapping the consequences of extreme events) are coded as “Hazard knowledge.” Each code mainly corresponds to one axis within PAPI’s structure in seven axes.Footnote 6

The identification of 88 codes, representing the diversity of actions that a risk basin may mobilize, offers the opportunity, through the assessment of their effectiveness, to identify and emphasize the most interesting actions. Once a PAPI has been scored, an indicator of the reduction of vulnerability to flooding of the considered risk basin can be obtained. To score PAPIs, we first rate the contribution, by crediting a number of points, of the 88 identified codes that represent all potential actions that can be implemented in PAPIs.

3.2 The Necessary Use of Expert Valuation

Assigning points of contribution to actions according to their effectiveness through quantitative methods is neither appropriate nor feasible—it would require multiple experimental designs with similar flood events as well as loss data that are either unavailable or limited (Hubert and Ledoux 1999; Bourguignon 2014). In this perspective, action rating is based on expert valuation, similar to the US Community Rating System (CRS) that credits points to prevention activities according to their assessed effectiveness (FEMA 2014).

The use of expert valuation raises the question of the relevance of the expert panel (Guillier 2016a). To assess the collective dimension of flood risk management, a panel of stakeholder representatives was constituted through the opportunity of presenting our experimental process at the National Flood Committee and to the local authorities in charge of PAPIs. The constituted panel includes 40 people from 20 organizations involved in flood risk management at different levels and with different responsibilities:

-

1.

Five organizations representing the French State and its services, with representatives from French ministries in charge of environment and civil security, from local state services, and state scientific experts;

-

2.

Eight representatives from local authorities with representatives of river syndicates, inter-municipal cooperation bodies, risk basin water boards, and the European Centre for Flood Prevention, which is a national representative of local authorities;

-

3.

Seven representatives of civil society and private/public experts, including representatives from insurance companies, people who have suffered flood damage, and so on.

The expert valuation part was conducted from March to June 2016 through individual interviews. Each meeting was 3–5 h long and needed additional time for the results to be compiled and validated by each expert. The aggregated results were then presented to the whole panel.

The question that follows the selection of experts is the method of building a relevant and robust rating model by using a qualitative approach.

3.3 Using the Analytic Network and Analytic Hierarchy Processes to Weight the Relative Importance of Strategies and Rate the Contribution of PAPI Actions

Regarding the diversity and complexity of actions within PAPI, as well as the six strategies of risk coping capacity, a multicriteria approach has to be used in order to assign points of contribution or weight to each action or strategy (Guillier 2016a). Multicriteria analysis (MCA) offers a great range of methods that are based on expert valuation (Renard 2010; Saaty and Ergu 2015). This experimental assessment uses the Analytic Network Process (ANP) and Analytic Hierarchy Process (AHP) established by Saaty (2008). It is one of the most used MCA methods (Huang et al. 2011), and was identified as the most adequate method according to our data and objectives because it allows for (Guillier 2016a): (1) a complete ordering of alternatives (Renard 2010); (2) the use of pairwise comparisons to weight the alternatives and criteria, which is considered an easy method to understand; (3) the checking of judgment consistency (Saaty 2008); (4) the addressing of interdependencies between criteria or alternatives within the ANP model (Saaty 2008); and (5) the addressing of an unlimited number of actions to be rated (rating mode of AHP model).

The use of AHP-ANP methods consists of two steps:

-

1.

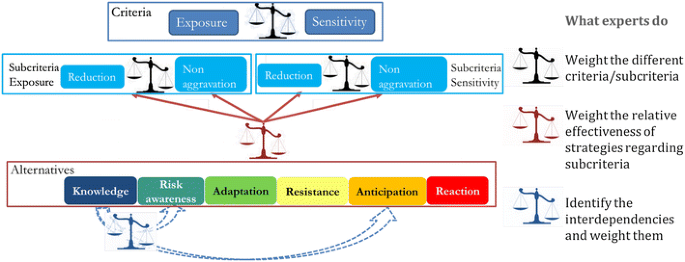

The comparison of the six strategies using an ANP model to determine the relative weight of strategies with regard to their effectiveness. The comparison helps to identify the optimal combination of strategies. The ANP model is required on the assumption that strategies are interdependent. Thus, the choice of the ANP for strategies is consistent with regard to the integrated strategy emphasized by the national policy framework. Using the ANP, the weight is distributed between the six strategies (expressed in percentage). The ANP model is presented in Fig. 3, together with the way the experts contribute; two criteria and four subcriteria were used: exposure and sensitivity; and nonaggravation of asset exposure, reduction of the exposure, reduction of the sensitivity of assets, and nonaggravation of their sensitivity.

Fig. 3

The analytic network process model to weight the six strategies

-

2.

The rating of the contribution of each of the 88 codes to one or several strategies to assess their effectiveness.Footnote 7 This was done through six AHP models (one for each strategy). Also the identified criteria were adapted in each of the six AHP models, the objective was to compare their contribution through the collective dimension of their impact—does it have an impact on the whole risk basin or on a small area—and the effectiveness of their impact. Here, the rating mode is used so that the determined weight is not dependent on the number of contributing codes (Guillier 2016a). The resulting rate is in points between 0 and 100, with 100 meaning the action would be considered most effective.

The two steps allow the calculation of a quantitative score for a PAPI. Rating risk coping capacity through a PAPI thus consists of summing the points of the actions the program has implemented—the score of a PAPI is the sum of the points obtained by each action in each strategy, multiplied by the weight of the strategy:

where Y is the score or total number of points of the PAPI, Y i is the total number of points credited for the action i, n is the number of actions in the PAPI, x ij is the number of points obtained by the action i within the strategy j, X j is the weight of the strategy j.

The different steps of PAPI rating, from expert valuation to application of the results, allow the addressing of our different objectives: the weights and points credited by experts to strategies and codes help to identify the best strategies and actions to implement towards vulnerability reduction. The application of these results to derive the PAPI scores of specific risk basins, based on the implemented actions in the concerned risk basins, offer a risk coping capacity indicator.

4 Rating Flood Risk Coping Capacity Within PAPIs

The experimental assessment allows investigating both theoretical and practical risk coping capacities: on the one hand, the results show the ideal combination of strategies and the contribution of actions to strategies according to the experts and, on the other hand, the rating of PAPIs give an overview of existing flood risk coping capacities regarding each implemented PAPI at the national level.

4.1 The Built Consensus of Strategy Weighting: The Central Role of Land Use Planning and Urban Planning

The relative effectiveness of the six strategies regarding their impact on vulnerability to flooding was weighted through value judgments by each expert of the panel. The built consensus of the experts through geometric mean on the ANP model results gives a weight of:

-

1.

50% for the adaptation strategy (land use planning and urban planning);

-

2.

15% to the resistance strategy (building dikes, maintenance, building upstream retention basins, and so on);

-

3.

13% to reaction (warning and crisis management);

-

4.

12% to knowledge;

-

5.

5% to anticipation (watercourse monitoring); and

-

6.

5% to risk awareness.

The robustness of the built consensus was tested through a sensitivity analysis and the results are not substantially modified by changing criteria weights or by adding new fictive experts. The results show that, according to the experts, adaptation is the most effective strategy to reduce vulnerability to flooding. The assessed weights reveal the change in paradigm from resistance to other strategies and highlight the central role of the spatial organization of people and activities in improving risk coping capacity and managing vulnerability to flooding. Even though land use planning and urban planning are the strategies to encourage, experts have identified and weighted interdependencies between adaptation and other strategies (Fig. 4).

Source: Guillier (2017)

Dependencies identified by the expert panel between adaptation and other strategies to manage vulnerability to flooding.

The interdependencies were identified and weighted for each strategy by the experts. Adaptation is, according to the experts, dependent on four other strategies with a strong dependency on knowledge (Fig. 4). Adaptation was not considered dependent on resistance strategy: according to the experts, resistance actions are not needed to implement or to support the effectiveness of actions that contribute to adaptation. Regarding the other strategies, the same links of dependency to knowledge, anticipation, and risk awareness were identified. The results also show that all strategies have a strong dependency on knowledge (always the highest weight of dependency), showing the high importance of knowledge to guaranty the effectiveness of other actions. These results show that implementing land use planning and urban planning is the biggest challenge to reducing vulnerability; nevertheless, the implementation of all strategies to build risk coping capacity is necessary to insure effectiveness.

According to the experts, the ANP model was useful for translating their opinions on strategies. It is an effective tool to weight strategies and to build robust results. In this study, a shared recognition of the optimal combination of strategies to enhance risk coping capacity was achieved, although the expert panel could be expanded to achieve even more robustness.

4.2 Rating the Different Actions: Limited Effectiveness

The rating of the contribution of the 88 codes of action to each of the six strategies raises the issue of the effectiveness of available tools regarding the strategies. The results of ratings, based on the geometric mean of individual expert judgment, highlight the moderate effectiveness of actions whatever the considered strategy is (Fig. 5). No action reaches 100 points. The points of the actions appear to be low to moderate (between 14 and 69), except for the anticipation strategy. Anticipation is a special strategy as only three codes of action are considered to contribute to it—watercourse monitoring by state services, watercourse monitoring by local authorities, and forecast modeling.

Source: Adapted from Guillier (2017)

Boxplots of the points obtained from the contributing codes for each strategy for managing vulnerability to flooding.

Multiplying the contribution of one code to one strategy by the weight of the strategy (obtained at the first step), the results show that the codes that are credited more points are mostly the land use planning and urban planning contributing codes, with “Risk Prevention Plan” ranking first place. But other actions can also be identified, such as “Crisis management exercise” and “Feedback after flooding.”

The points attributed by each expert are very variable from one expert to the other. In that sense, the results are substantially sensitive. The sensitivity analysis shows that the number of points is not robust, but it appears that the order is more robust. The large differences between the experts indicate the serious difficulties of quantifying the effectiveness of concrete actions. The effectiveness of one single action may be different according to the considered risk basin, as well as in different areas within the same risk basin, or at different times—some actions may be effective in some places, but not in others, some actions may have been effective once, but not the second time, and so forth.

These results also highlight the limits of the rating method used here to assess each tool/action. The method does not consider that the effectiveness of two tools implemented in parallel may be higher than the sum of their respective effectiveness. However, it was necessary to consider actions independently because each PAPI chooses its own combination of actions, and scoring every potential combination of actions is not realistically feasible. The identified limits raise the issue of the capacity of the rating mode of the AHP to compare adequately so many actions. The available tools to enhance strategies and risk coping capacity have shown limited effectiveness. This contributes to the conviction that no individual tool is effective enough to enhance risk coping capacity, but that there is a need for a combination of tools to address any specific area’s issues.

4.3 Enhanced Risk Coping Capacity in PAPIs: The Impact of the French National Public Policy Framework

By applying the credited points to each code of actions, we can assess the PAPIs according to the actions they implemented. The resulting ratings of the 145 PAPIs range from 8 to 324 points, which shows a great difference in risk coping capacity. The distribution of the average points of actual implemented strategies (all PAPIs considered) is significantly different from the “ideal” strategy combination that refers to the strategy weights attributed by the experts during the first step of the analysis. Adaptation as the most prioritized strategy received 39% of all points within the implemented and planned PAPIs, and knowledge represents the second largest part of the strategies with 22% of all points on average (Fig. 6). The Hierarchical Cluster Analysis (HCA) identifies three groups of PAPIs (Fig. 6) with different characteristics:

Source: Adapted from Guillier (2017)

Average prioritization of strategies in the French Action Programs for Flood Prevention PAPIs (Programme d’Action pour la Prévention des Inondations), and the spatial distribution of Hierarchical Cluster Analysis (HCA) groups with significantly different prioritizations.

-

1.

Group 1 implements significantly less the resistance strategy (11%, t test p value = 1.24 × 10−11) and more the knowledge strategy (28%, p value = 4.6 × 10−6);

-

2.

Group 2 implements significantly more the adaptation strategy (50.5%, p value = 2.2 × 10−16) and less the reaction strategy (6%, p value = 3.07 × 10−8);

-

3.

Group 3 implements significantly less the adaptation strategy (24%, p value = 4.6 × 10−10) and more the resistance strategy (34.5%, p value = 1.6 × 10−4).

By examining the influencing factors, we found that the combination of strategies within one PAPI is strongly dependent upon the type of PAPI. There are four types of PAPI:

-

1.

First generation PAPIs: these are the first programs implemented in France following their establishment in 2002;

-

2.

Complete PAPIs: they correspond to the second generation PAPIs that began in 2011. They include actions related to hydraulic works, and their budget is over 3 million Euros;

-

3.

Small PAPIs: they also include actions related to hydraulic works, but the budget is below 3 million Euros;

-

4.

Intended PAPIs: they include several actions, but they can only implement studies related to hydraulic works.

The intended PAPIs cannot implement the ideal strategy combination by construction so they cannot implement most resistance strategy actions. Most of the intended PAPIs belong to Group 1 of the HCA groups. First generation PAPIs are said to have done a lot of hydraulic works, which is confirmed through this analysis. They mostly belong to Group 3. Risk coping capacity is strongly linked to the type of PAPI and thus to the national framework related to this public policy instrument.

No other variable—such as type of hazard, density of population, proportion of urbanized land, and hydrographic basin—has demonstrated a significant influence. This suggests that local specificities do not play a crucial role in strategy combination. Strategy combination seems to be an interesting way to identify the prioritization of strategies. Further application of the risk coping indicator through PAPI rating is needed within insurance companies to translate the results of this study into decisions. The indicator requires special attention because it considers the intended actions that risk basins want to implement during the next 2–6 years. The rating of a PAPI is a theoretical indicator of risk coping capacity that has to be nuanced according to the real implemented actions.

5 Conclusion

This research reflects the French insurance industry’s growing concern about natural risks, especially flood risks. By investigating the question of prevention, they join the more general concern that emphasizes the recognition of societal capacity to move on from a fatalistic view towards prevention and more resilient territories (Guillier 2016a).

The ANP and AHP models represent a great opportunity to overcome the difficulties in assessing the effectiveness of strategies and tools, by using value judgments within a semiquantitative approach. At the strategy level, the study highlights a shared predominance of land use planning and urban planning. Nevertheless, there is a real need for an integrated strategy to enhance risk coping capacity. The advantage of such Multicriteria Analysis (MCA) models is to quantify the relative importance of strategies and not an absolute one. The limited effectiveness of each tool or action taken separately tends to reinforce this need for an integrated and coordinated strategy.

PAPIs, as the key flood risk management public policy instrument in France, are interesting windows of opportunity for assessing expected risk coping capacity. But because PAPIs address only part of the national territory, the possibility to understand risk coping capacity nationwide through such an instrument is limited. In this perspective, only local knowledge of implemented actions can be used on flood risk basins where there is no PAPI. Building a national platform of implemented prevention actions should be emphasized to go further.

Notes

Other natural risks like windstorms, hail, and weight of snow on roofs, are not part of this scheme, but are covered by other insurance contracts.

For example, 12% for the basic insurance policy premium that covers housing property. If we consider the average cost of the basic insurance policy premium that covers housing property, which is 300 Euros, then the premium that will have to be paid is 336 Euros (300 Euros plus 36 Euros related to the additional premium).

We use the example of Footnote 2: 36 Euros are paid that stand for the additional premium. About 4 Euros will be levied with regards to the Fund for the Prevention of Major Natural Risks.

This French dedicated structure mirrors other similar projects abroad, such as, in the United States, the Institute for Business and Home Safety (IBHS); and in Europe, ZURS Geo in Germany, HORA in Austria, and so on. MRN participates in the gathering and sharing of data relative to damages and risk management and has been a partner of the National Observatory of Natural Risks (Observatoire National des Risques Naturels—ONRN) since its establishment in 2012, together with the ministry in charge of the environment and the French State reinsurance company CCR (Caisse Centrale de Réassurance).

According to SANDRE, there are four nested levels of hydrographic basins: the 1st order considers 24 hydrographic regions and the 4th order considers 6188 hydrographic areas. Each of them can be considered a flood risk basin.

Some codes appear difficult to categorize within one or another axis. Some differences can be observed in the different application forms.

In fact, even if one code can be mainly associated with one PAPI axis, we leave the opportunity to the experts to express the different contributions one code may have regarding strategies.

References

AFA (I’Association française de I’assurance/French Insurance Association). 2015. Synthesis of climate change analysis and insurance, climatic risks: What impacts on natural disaster insurance on the 2040 horizon (Synthèse de l’étude changement climatique et assurance, Risques climatiques: quels impacts sur I’assurance contre les aléas naturels à I’horizon 2040?). Paris: AFA (in French).

Birkmann, J., and B. Wisner. 2006. Measuring the unmeasurable: the challenge of vulnerability. UNU-EHS Source. Bonn: UNU-EHS.

Bourguignon, D. 2014. Events and territories: Flooding cost in France—Spatial and temporal analysis of insured loss data (Évènements et territoires—Le coût des inondations en France, Analyse spatio-temporelle des dommages assures). Ph.D. thesis, University Montpellier 3, Montpellier, France (in French).

D’Ercole, R., J.-C. Thouret, O. Dollfus, and J.-P. Asté. 1994. Vulnerabilities of societies and urbanized areas: Concepts, typology, methods (Les vulnérabilités des sociétés et des espaces urbanisés: concepts, typologie, modes d’analyse). Revue de Géographie Alpine 82(4): 87–96 (in French).

Dourlens, C. 2003. The issue of flooding: The social science prism (La question des inondations: le prisme des sciences sociales). Rapport au Ministère de I’équipement, des Transports et du Logement, Direction de la recherche et des affaires scientifiques et techniques (in French).

Erdlenbruch, K., É. Gilbert, F. Grelot, and C. Lescoulier. 2009. A spatialized cost-benefit analysis of protection against flooding: Application of the avoided damages method to Orb lower valley (Une analyse coolyse coe c spatialisse de la protection contre des inondations. Application de la mmages method to Orb lowelle d lobasse vallée de I’Orb). Ingénieries 53: 3–20 (in French).

FEMA (Federal Emergency Management Agency). 2014. National flood insurance program community rating system: CRS coordinator’s manual. Washington, DC: FEMA.

Gallopín, G.C. 2006. Linkages between vulnerability, resilience, and adaptive capacity. Global Environmental Change 16(3): 293–303.

Gérin, S. 2011. An assessment process of Risk Prevention Plans in the context of natural disaster insurance (Une démarche évaluative des Plans de Prévention des Risques dans le contexte de I’assurance des catastrophes naturelles: contribution au changement de I’action publique). Ph.D. thesis, University Paris 7 – Paris Diderot, UMR 8586 PRODIG (in French).

Guillier, F. 2016a. Insurance and risk assessment: How to integrate prevention? In ICUR2016 Proceedings, International Conference on Urban Risks, Lisbon, 35–42, 30 June–2 July 2016.

Guillier, F. 2016b. The PAPI public policy instrument: Developing local capacities through an integrated flood risk management strategy. In ICUR2016 Proceedings, International Conference on Urban Risks, Lisbon, 957–964, 30 June–2 July 2016.

Guillier, F. 2017. Evaluation of vulnerability to flooding: Experimental design implemented on Action Programmes for Flood Prevention (Evaluation de la vulnérabilité aux inondations: Méthode expérimentale appliquée aux Programmes d’Actions de Prévention des Inondations). Ph.D. thesis, University of Eastern Paris, Paris (in French).

Hegger, D.L.T., C. Green, P.P.J. Driessen, M.H. Bakker, C. Dieperink, A. Crabbé, K. Deketelaere, B. Delvaux, et al. 2013. Flood risk management in Europe: Similarities and differences between the STAR-FLOOD consortium countries. Utrecht, The Netherlands: STAR-FLOOD Consortium.

Huang, I.B., J. Keisler, and I. Linkov. 2011. Multi-criteria decision analysis in environmental sciences: Ten years of applications and trends. Science of the Total Environment 409(19): 3578–3594.

Hubert, G., and B. Ledoux. 1999. The cost of risk…: Socioeconomic impact assessment of floods (Le Coût du risque…: I’évaluation des impacts socio-économiques des inondations). Paris: Presses de I’École Nationale des Ponts et Chaussées (in French).

IPCC (Intergovernmental Panel on Climate Change). 2014. Climate change 2014: Synthesis report. In Contribution of Working Groups I, II and III to the fifth assessment report of the Intergovernmental Panel on Climate Change, ed. Core Writing Team, R.K. Pachauri, and L.A. Meyer. Geneva: IPCC.

Larrue, C., S. Bruzzone, L. Lévy, M. Gralepois, T. Schellenberger, J.B. Trémorin, M. Fournier, C. Manson, and T. Thuilier. 2016. Analysing and evaluating flood risk governance in France: From state policy to local strategies. Tours, France: French STAR-FLOOD Team.

Ledoux, B. 2006. Flood risk management (La gestion du risque inondation). London: Éditions Tec & Doc (in French).

MEDDE (Ministry of Environment, Sustainable Development and Energy / Ministère de I’Environnement, du Développement Durable et de I’Énergie). 2014. National strategy of flood risk management: National flood risk management public policy (Stratégie Nationale de Gestion du Risque Inondation—SNGRI: Politique Nationale de Gestion du Risque Inondation). https://www.ecologique-solidaire.gouv.fr/sites/default/files/2014_Strategie_nationale_gestion_risques_inondations.pdf. Accessed 11 Sept 2017 (in French).

Nussbaum, R. 2015. Involving public private partnerships as building blocks for integrated natural catastrophes country risk management—Sharing on the French national experiences of economic instruments integrated with information and knowledge management tools. IDRiM Journal 5(2): 82–100.

Reghezza, M. 2006. Thinking about metropolitan vulnerability: Facing the centennial flood risk in Paris (Réflexions autour de la vulnérabilité métropolitaine: la métropole parisienne face au risque de crue centennale). Ph.D. thesis, Université de Nanterre – Paris X, Paris (in French).

Renard, F. 2010. The surface runoff risk in urban areas: From hazard typology to vulnerability assessment: The Grand Lyon case (Le risque pluvial en milieu urbain: de la caractérisation de I’aléa à I’évaluation de la vulnérabilité: le cas du Grand Lyon). Ph.D. thesis, University Lyon 3, France (in French).

Saaty, T.L. 2008. Decision making with the analytic hierarchy process. International Journal of Services Sciences 1(1): 83–98.

Saaty, T.L., and D. Ergu. 2015. When is a decision-making method trustworthy? Criteria for evaluating multi-criteria decision-making methods. International Journal of Information Technology & Decision Making 14(6): 1–17.

Steinführer, A., B. De Marchi, C. Kuhlicke, A. Scolobig, S. Tapsell, and S. Tunstall. 2009. Local communities at risk from flooding: Social vulnerability, resilience and recommendations for flood risk management in Europe. FLOODsite report T11-07-12, Helmholtz-Zentrum für Umweltforschung, Department Stadt-und Umweltsoziologie, Leipzig. http://www.floodsite.net. Accessed 11 Sept 2017.

UNISDR (United Nations International Strategy for Disaster Reduction). 2002. Living with risk: A global review of disaster reduction initiatives. Geneva: UNISDR.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Guillier, F. French Insurance and Flood Risk: Assessing the Impact of Prevention Through the Rating of Action Programs for Flood Prevention. Int J Disaster Risk Sci 8, 284–295 (2017). https://doi.org/10.1007/s13753-017-0140-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13753-017-0140-y