Abstract

This article investigates silver price as a fluctuating commodity price since the financial crisis of 2007–2009. In this regard, a structural vector autoregression (VAR) was applied to observe the sensitivity of the silver price and future pricing due to changes in macroeconomic variables and to review changes in macroeconomic variables due to changes in the silver price. The main results show that the silver price is susceptible to changes in the gold price, increasing sideways. A shock to OECD GDP caused the silver price to increase which makes logical sense, thus showing a positive correlation between output and the silver price. A shock to the oil price caused the silver price to spike over the short term, then move sideways over the long term. A shock to the US Federal funds rate caused the silver price to dip over the short term, then increase slightly over the medium and move sideways over the long term, while a shock to the real effective exchange rate of the USA caused the silver price to increase sideways. The article sheds some light on the reactive status of the silver price to macroeconomic variables and its influence as a safe haven commodity.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The investment demand for silver as a safe haven and world events such as a financial crisis or worldwide pandemic could have significant influence on the current silver price.

Figure 1 shows the $ silver price from 2000 to 2022, reaching its highest point after 2009 at $46 per ounce. It came down to less than $20 per ounce and then shot up to $28 after 2019 with the COVID-19 pandemic, remaining high also with geopolitical tension with the war between Ukraine and Russia. The SVAR model in this paper uses the silver price to estimate the impulse response function and variance decomposition.

$ silver price from 2000 to 2022

One of the earliest price models for silver investigates the determinants of precious metals including demand and supply and industry production (Radetzki 1989). Various other studies have since appeared describing silver price behaviour including monthly time series analysis of single countries such as Thailand (Jongadsayakul, 2015) and Ethiopia (Ayele et al., 2020). Further, authors argue about the volatility between gold and silver prices and that changes in the silver price could be susceptible to changes in the gold price (Bouri and Jalkh 2019; Koulis and Kyriakopoulos 2023). This study contributes in that it involves a macroeconomic viewpoint, building a structural VAR to describe recent, annual silver price behaviour including the gold price but no other commodity prices such as platinum and palladium as used by Batten et al. (2010).

The first part of this article provides the problem statement followed by a literature review, research methodology and ends with policy implications and conclusions.

The problem statement addressed in this paper pertains to a fluctuating silver price. The problem is addressed through:

-

A structural vector autoregression (VAR) to observe the sensitivity of the silver price and future pricing due to changes in macroeconomic variables

-

Changes in macroeconomic variables due to changes in the silver price

The variables used for decomposition were the silver price, gold price, oil price, real effective exchange rate of the USA, the US Federal funds rate and total combined gross domestic product (GDP) of the Organisation for Economic Co-operation and Development (OECD) countries.

Data trends in terms of silver

Looking at Table 1., the demand and supply have changed from 2011 to 2020 with demand decreasing and supply increasing, although mine production declined led by Peru, Mexico and Indonesia.

Although the silver price has declined, the 2021 aftermath of the COVID-19 pandemic and geopolitical tension because of the war between Ukraine and Russia would ensure that the safe-haven status of silver is pronounced with higher prices recorded.

Literature review

One of the earliest works investigates the need for empirical models to explore demand, the uncertainty of price behaviour and production in resources such as silver (Pindyck 1981). Further, theoretical work is done in terms of determinants, such as demand and supply as well as industrial production, also for silver (Radetzki 1989). Much later, the relationship between macroeconomic variables (business cycle, monetary environment and financial market sentiment) and price returns of precious metal markets are investigated (Batten et al., 2010). They found that the volatility of the gold price is determined by monetary variables but this does not hold for the silver price. Another stream of research looks at the relationship between silver and gold, especially co-integration and error correction models (Escribano and Granger 1998; Zhu et al. 2016). Further, authors argue about the volatility between gold and silver prices and that changes in the silver price could be susceptible to changes in the gold price (Bouri and Jalkh 2019; Koulis and Kyriakopoulos 2023). Bouri and Jalkh (2019) find evidence of predictability of the probability of gold implied volatility based on the lagged silver implied volatility across different quantiles. Koulis and Kyriakopoulos (2023) find that the volatility transmission from gold to silver is unidirectional. The latter authors focus on the volatility between gold and silver prices. In the current article, a macroeconomic approach or viewpoint is followed with a structural VAR model where various macroeconomic variables are implemented and not a stock market or volatility approach. In a recent article, some short-term negative effects run from solar energy capacity to the silver price (Apergis et al. 2020).

Possible variables explored here include the silver price (in USD), gold price (in USD), real effective exchange rate of the USA, the Federal funds rate, the oil price (in USD) and the total combined OECD GDP at constant prices. This research follows up on recent research started by Joëts et al. (2017) that concluded that macroeconomic uncertainty such as the financial crisis of 2007–2009 generated price uncertainty in raw material linked to especially macroeconomic activity. The chosen model was adjusted to fit previous studies as pointed out earlier, e.g. the interest rate was also included as an indicator of inflation.

Research methodology

The vector autoregression (VAR) is an econometric model used to capture the linear interdependencies among multiple time series. The empirical analysis in the present research was based on structural VAR models. VAR models, after an appropriate identification of shocks, allow examination of the response of the commodity price (the gold price in this case) to unanticipated shocks, particularly to interest rates and the dollar exchange rate, while taking into account the dynamic interaction between commodity prices (again gold in this case) and macroeconomic variables. To identify shocks, the standard Cholesky scheme has been used. The following variables were considered endogenous variables: the gold price; the real effective exchange rate of the USA; the Federal funds rate; the oil price (in USD) and the total combined OECD GDP at constant prices. The applicable period considered is from 1980 to 2019.

Empirical model specification

A structural economic model (SEM) is chosen above all other models (Vines and Wills 2020).

A structural VAR is formulated for the seasonally adjusted annual time series for the following aggregate variables in logs: the gold price; the real effective US exchange rate; the Federal funds rate; the oil price (in USD) and total combined OECD GDP at constant prices. The SVAR is in log levels of the variables to allow implicitly for possible co-integration between variables. A VAR model for the first differences of variables may lead to biased estimates if co-integrating variables in the different levels are omitted. Two lags of the variables besides intercepts have been found to adequately characterise annual VAR modelling (Wooldridge, 2013). See Appendix for the SVAR estimations.

Annual data variables

The variable Silver price (SilverP) is the silver price in dollar terms and is given by LOG(SILVER_PRICE).

The variable Gold price (GoldP) is the gold price in dollar terms and is given by LOG(GOLD_PRICE).

The real effective exchange rate (REER) is defined as the index of bilateral trade-weighted exchange rate adjusted by the differences in price levels between the USA and its major trading partners and given by LOG(REER).

The Federal funds rate (FEDR) was selected as the interest rate to benchmark data against. It is given as (FEDERAL).

The variable oil price (OILP) is the oil price in dollar terms LOG(OILP).

The aggregate OECD output series is measured as a real gross domestic product in dollar terms LOG(OECD_GDP).

Data was sourced from Quantec (2021) which supplies all the data. The intention was to investigate the effect of exchange rates, interest rates, oil price and output on the silver price.

Impulse response analysis

Impulse responses based on VAR modelling were analysed. Ninety-five per cent confidence intervals obtained by bootstrapping together with the impulse responses to different shocks are presented here. The results are consistent with the theory of Akram (2009) suggesting a negative relationship between interest rates and commodity prices, and theories suggesting a negative relationship between the real value of the dollar and commodity prices. The results of shocks to global output, proxied by OECD GDP and oil prices, are consistent with several studies based on VECM models (Hodge 2015). High economic activity can lead to higher gold prices and ultimately higher oil prices.

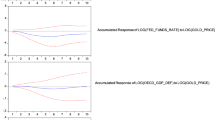

The necessary residual tests were conducted to ensure that the VAR modelling was stable and could be used in a meaningful way. The variables that were used for decomposition were the gold price, the oil price, the real effective exchange rate of the USA, the US Federal funds rate and the total combined OECD GDP. Impulse response functions are shown in Fig. 2 and shocks to each system were investigated and the forecast error variance decomposition over 10 years was examined. As already mentioned, the changes in the silver price are susceptible to changes in the gold price, increasing sideways (Escribano and Granger 1998; Zhu et al. 2016). Further, the main results show that a shock to OECD GDP caused the silver price to increase which makes logical sense, thus showing a positive correlation between output and the silver price. A shock to the oil price caused the silver price to spike over the short term, then move sideways over the long term. A shock to the US Federal funds rate caused the silver price to dip over the short term, then increase slightly over the medium and moving sideways over the long term, while a shock to the real effective exchange rate of the USA caused the silver price to increase sideways.

Impulse response function

Variance decomposition

Contributions of different variables are then investigated according to years over different forecasting horizons (Issler et al., 2014). The percentages of the variance of the error made in forecasting a variable are then displayed at a given horizon due to the shocks. The variance decomposition is shown in Fig. 3. Most of the variance in commodity prices such as oil prices and gold prices occur due to the silver price. These prices declined over the longer term. The silver price increased to about 20% due to the output.

Variance decomposition

Policy implications and conclusion

Silver is used in electrical switches, solar panels, computers, appliance equipment and medicine. However, the safe-haven status of silver is like gold always relevant especially during natural disasters or pandemics such as COVID-19. Price cyclicality and forecasting then become crucial for traders, hedge fund managers and policymakers. Various sources of price and production data exist worldwide. In this regard, a structural vector autoregression (VAR) was designed to check the sensitivity of the silver price and future pricing due to changes in macroeconomic variables and also changes in macroeconomic variables due to changes in the silver (commodity) price. The variables that were used for decomposition were the gold price, the oil price, the real effective exchange rate of the USA, the US Federal funds rate and the total OECD GDP deflator. Impulse response functions with shocks to each system were investigated and the forecast error variance decomposition was examined.

The main results show that the silver price is susceptible to changes in the gold price, increasing sideways. A shock to OECD GDP caused the silver price to increase which makes logical sense, thus showing a positive correlation between output and the silver price. A shock to the oil price caused the silver price to spike over the short term, then move sideways over the long term. A shock to the US Federal funds rate caused the silver price to dip over the short term, then increase slightly over the medium and move sideways over the long term, while a shock to the real effective exchange rate of the USA caused the silver price to increase sideways. The article sheds some light on the silver price and its influence as a safe haven commodity. The oil price, OECD output, interest rate and real effective exchange rate of the US are taken into account in terms of the silver price and the impact of shocks will assist with forecasting, also in terms of geopolitical tensions and financial concerns. This research could serve as a guide for possible early interventions, especially concerning the reactive status of the silver price to macroeconomic variables which would serve the interests of all affected stakeholders such as policymakers.

Data availability

Data is available on request.

References

Akram QF (2009) Commodity prices, interest rates and the dollar. Energy Econ 31(6):838–851. https://doi.org/10.1016/j.eneco.2009.05.016

Apergis N, Carmona-González N, Gil-Alana LA (2020) Persistence in silver prices and the influence of solar energy. Resour Policy 69(September):101857. https://doi.org/10.1016/j.resourpol.2020.101857

Ayele AW, Gabreyohannes E, Edmealem H (2020) Generalized autoregressive conditional heteroskedastic model to examine silver price volatility and its macroeconomic determinant in Ethiopia market. J Probab Stat 2020:5095181. https://doi.org/10.1155/2020/5095181

Batten JA, Ciner C, Lucey BM (2010) The macroeconomic determinants of volatility in precious metals markets. Resour Policy 35(2):65–71. https://doi.org/10.1016/j.resourpol.2009.12.002

Bouri E, Jalkh N (2019) Conditional quantiles and tail dependence in the volatilities of gold and silver. Int Econ 157:117–133

Escribano A, Granger CW (1998) Investigating the relationship between gold and silver prices. J Forecast 17(2):81–107. https://doi.org/10.1002/(SICI)1099-131X(199803)17:2<81::AID-FOR680>3.0.CO;2-B

Hodge D (2015) Commodity prices, the exchange rate and manufacturing in South Africa: what do the data say? Afr J Econ Manag 6(4):356–379

Issler JV, Rodrigues C, Burjack R (2014) Using common features to understand the behavior of metal-commodity prices and forecast them at different horizons. J Int Money Finance 42:310–335. https://doi.org/10.1016/j.jimonfin.2013.08.017

Joëts M, Mignon V, Razafindrabe T (2017) Does the volatility of commodity prices reflect macroeconomic uncertainty? Energy Econ 68:313–326. https://doi.org/10.1016/j.eneco.2017.09.017

Jongadsayakul W (2015) Determinants of silver futures price volatility: evidence from the Thailand Futures Exchange. Int J Bus Soc 9(4):81–87. https://ssrn.com/abstract=2655734

Koulis A, Kyriakopoulos C (2023) On volatility transmission between gold and silver markets: evidence from a long-term historical period. Comput 11(2):25

Pindyck RS (1981) Models of resource markets and the explanation of resource price behaviour. Energy Econ 3(3):130–139. https://doi.org/10.1016/0140-9883(81)90034-7

Quantec (2021) OECD data. http://www.easydata.co.za. Accessed 19 Feb 21

Radetzki M (1989) Precious metals: The fundamental determinants of their price behaviour. Resour Policy 15(3):194–208

Robinson Z (2017) Sustainability of platinum production in South Africa and the dynamics of commodity pricing. Resour Policy 51(July 2016):107–114. https://doi.org/10.1016/j.resourpol.2016.12.001

Robinson Z (2019) Revisiting gold price behaviour: a structural VAR. Miner Econ 32(3):365–372. https://doi.org/10.1007/s13563-019-00204-4

Silver Institute (2021) Silver supply and demand. https://www.silverinstitute.org/silver-supply-demand/. Accessed 09 Mar 21

Vines D, Wills S (2020) The rebuilding macroeconomic theory project part II: multiple equilibria, toy models, and policy models in a new macroeconomic paradigm. Oxford Rev Econ Policy 36(3):427–497. https://doi.org/10.1093/oxrep/graa066

Wooldridge J (2013) Introductory econometrics: a modern approach. Cengage Learning, South-Western

Zhu H, Peng C, You W (2016) Quantile behaviour of cointegration between silver and gold prices. Finance Res Lett 19:119–125. https://doi.org/10.1016/j.frl.2016.07.002

Funding

Open access funding provided by University of South Africa.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Ethics approval

Ethics approval has been granted by the College of Economic and Management Sciences Ethics Committee of Unisa. No human involvement confirmed.

Competing interests

The author declares no competing interests.

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Standard errors in ( ) and t-statistics in [ ]

LOG(SIVER_P) | LOG(GOLD_PRICE) | LOG(OIL_PRICE) | LOG(FED_FUNDS_RATE) | LOG(OECD_GDP_DEFLATOR) | LOG(REER_US) | |

|---|---|---|---|---|---|---|

LOG(SIVER_P(−1)) | 0.646216 | −0.098321 | 0.700326 | 1.057959 | −0.009293 | 0.106264 |

(0.34241) | (0.19478) | (0.45560) | (0.71754) | (0.01200) | (0.08334) | |

[1.88725] | [−0.50478] | [1.53715] | [1.47443] | [−0.77415] | [1.27508] | |

LOG(SIVER_P(−2)) | −0.216223 | −0.151913 | 0.253972 | −1.665056 | 0.022463 | 0.000280 |

(0.35559) | (0.20228) | (0.47314) | (0.74515) | (0.01247) | (0.08655) | |

[−0.60807] | [−0.75101] | [0.53678] | [−2.23451] | [1.80184] | [0.00323] | |

LOG(GOLD_PRICE(−1)) | 0.665090 | 1.286417 | 0.108439 | −1.338141 | 0.038017 | −0.240106 |

(0.67983) | (0.38672) | (0.90455) | (1.42460) | (0.02383) | (0.16546) | |

[0.97832] | [3.32648] | [0.11988] | [−0.93931] | [1.59510] | [−1.45113] | |

LOG(GOLD_PRICE(−2)) | −0.474244 | −0.191916 | −1.143170 | 1.971711 | −0.051027 | 0.135751 |

(0.68477) | (0.38953) | (0.91114) | (1.43497) | (0.02401) | (0.16667) | |

[−0.69256] | [−0.49268] | [−1.25466] | [1.37405] | [−2.12548] | [0.81451] | |

LOG(OIL_PRICE(−1)) | 0.010434 | −0.013024 | 0.104882 | −0.706379 | −0.004223 | −0.008607 |

(0.18128) | (0.10312) | (0.24121) | (0.37988) | (0.00636) | (0.04412) | |

[0.05756] | [−0.12630] | [0.43482] | [−1.85947] | [−0.66447] | [−0.19507] | |

LOG(OIL_PRICE(−2)) | 0.314522 | 0.153724 | 0.201302 | 0.079406 | −0.000126 | −0.019540 |

(0.16286) | (0.09264) | (0.21670) | (0.34129) | (0.00571) | (0.03964) | |

[1.93120] | [1.65928] | [0.92894] | [0.23267] | [−0.02201] | [−0.49296] | |

LOG(FED_FUNDS_RATE(−1)) | 0.025048 | −0.013512 | −0.019832 | 1.011703 | 0.006108 | 0.004061 |

(0.07923) | (0.04507) | (0.10542) | (0.16603) | (0.00278) | (0.01928) | |

[0.31614] | [−0.29981] | [−0.18813] | [6.09351] | [2.19894] | [0.21061] | |

LOG(FED_FUNDS_RATE(−2)) | −0.058765 | 0.017145 | −0.048286 | −0.474145 | −0.007367 | −0.002034 |

(0.07762) | (0.04415) | (0.10328) | (0.16265) | (0.00272) | (0.01889) | |

[−0.75709] | [0.38832] | [−0.46754] | [−2.91508] | [−2.70743] | [−0.10765] | |

LOG(OECD_GDP_DEFLATOR(−1)) | 0.492669 | 2.347661 | 13.79353 | 16.36264 | 1.373924 | 0.937923 |

(4.74845) | (2.70116) | (6.31812) | (9.95054) | (0.16647) | (1.15571) | |

[0.10375] | [0.86913] | [2.18317] | [1.64440] | [8.25312] | [0.81155] | |

LOG(OECD_GDP_DEFLATOR(−2)) | −0.640608 | −2.090763 | −12.33265 | −16.58067 | −0.385717 | −0.865469 |

(4.52655) | (2.57493) | (6.02286) | (9.48553) | (0.15869) | (1.10170) | |

[−0.14152] | [−0.81197] | [−2.04764] | [−1.74800] | [−2.43058] | [−0.78557] | |

LOG(REER_US(−1)) | 0.404845 | 0.136485 | −0.902034 | 1.365237 | −0.000192 | 0.919952 |

(0.96723) | (0.55021) | (1.28696) | (2.02686) | (0.03391) | (0.23541) | |

[0.41856] | [0.24806] | [−0.70090] | [0.67357] | [−0.00565] | [3.90786] | |

LOG(REER_US(−2)) | −0.329614 | 0.407695 | 0.492675 | 0.816841 | −0.011723 | −0.210882 |

(0.96916) | (0.55131) | (1.28953) | (2.03091) | (0.03398) | (0.23588) | |

[−0.34010] | [0.73950] | [0.38206] | [0.40220] | [−0.34501] | [−0.89402] | |

C | 0.597995 | −3.621035 | −0.069559 | −8.370729 | 0.157132 | 1.300732 |

(3.24271) | (1.84462) | (4.31464) | (6.79522) | (0.11368) | (0.78924) | |

[0.18441] | [−1.96303] | [−0.01612] | [−1.23186] | [1.38217] | [1.64809] | |

R-squared | 0.932213 | 0.975751 | 0.891074 | 0.948839 | 0.999476 | 0.861901 |

Adj. R-squared | 0.899675 | 0.964111 | 0.838790 | 0.924282 | 0.999225 | 0.795613 |

Sum sq. resids | 1.000419 | 0.323726 | 1.771143 | 4.393104 | 0.001230 | 0.059262 |

S.E. equation | 0.200042 | 0.113794 | 0.266169 | 0.419195 | 0.007013 | 0.048688 |

F-statistic | 28.64998 | 83.82963 | 17.04282 | 38.63796 | 3977.308 | 13.00245 |

Log likelihood | 15.18652 | 36.62377 | 4.333593 | −12.92621 | 142.5146 | 68.88436 |

Akaike AIC | −0.115080 | −1.243357 | 0.456127 | 1.364537 | −6.816557 | −2.941282 |

Schwarz SC | 0.445147 | −0.683130 | 1.016354 | 1.924764 | −6.256331 | −2.381055 |

Mean dependent | 4.642019 | 6.306815 | 3.528267 | 0.750499 | 4.294960 | 4.717145 |

S.D. dependent | 0.631561 | 0.600673 | 0.662919 | 1.523408 | 0.251948 | 0.107694 |

Determinant resid covariance (dof adj.) | 7.31E−14 | |||||

Determinant resid covariance | 5.92E−15 | |||||

Log likelihood | 298.9150 | |||||

Akaike information criterion | −11.62710 | |||||

Schwarz criterion | −8.265743 | |||||

R-squared | 0.989952 | 0.989988 | 0.993614 | 0.924065 | 0.996794 | 0.980692 |

Adj. R-squared | 0.972727 | 0.972825 | 0.982667 | 0.793890 | 0.991298 | 0.947593 |

Sum sq. resids | 0.081233 | 0.062252 | 0.062724 | 4.291447 | 0.000908 | 0.002479 |

S.E. equation | 0.107725 | 0.094304 | 0.094660 | 0.782984 | 0.011388 | 0.018818 |

F-statistic | 57.47081 | 57.68191 | 90.76645 | 7.098639 | 181.3599 | 29.62888 |

Log likelihood | 26.68291 | 29.34418 | 29.26870 | −12.98769 | 71.62420 | 61.57814 |

Akaike AIC | −1.368291 | −1.634418 | −1.626870 | 2.598769 | −5.862420 | −4.857814 |

Schwarz SC | −0.721065 | −0.987192 | −0.979644 | 3.245995 | −5.215194 | −4.210588 |

Mean dependent | 6.344649 | 6.708798 | 3.750258 | 0.078160 | 4.508368 | 4.671777 |

S.D. dependent | 0.652300 | 0.572067 | 0.719009 | 1.724658 | 0.122071 | 0.082202 |

Determinant resid covariance (dof adj.) | 3.98 E−17 | |||||

Determinant resid covariance | 7.32E−20 | |||||

Log likelihood | 270.3417 | |||||

Akaike information criterion | −19.23417 | |||||

Schwarz criterion | −15.35082 | |||||

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Robinson, Z. A macroeconomic viewpoint using a structural VAR analysis of silver price behaviour. Miner Econ 37, 15–23 (2024). https://doi.org/10.1007/s13563-023-00386-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13563-023-00386-y