Abstract

Counterparty risk remains an issue in over-the-counter derivative transactions following the 2008 financial crisis. While the margin for a derivative transaction can only be transferred until just before the counterparty’s default, the exposure of the derivative transaction can vary stochastically during the margin period of risk, that is, the period from the counterparty’s default to the actual closing-out of the transaction. Thus, the anticipated positive exposure may not be recognized, resulting in counterparty risk. Considering it is difficult to calculate the initial margin (IM) according to the regulations, IM has been calculated in practice using a simplified method proposed by the International Swaps and Derivatives Association (ISDA), which is called the ISDA Standard Initial Margin Model (“ISDA SIMM”). In this study, we derive an approximate formula for some counterparty risk indicators for a stochastic volatility model and illustrate numerical analyses for a call option in the SABR model as an example to examine the effect of the discrepancy between regulations and practices in margin calculation. Our results imply that the IM calculated in practice may be insufficient for counterparty risk management, particularly when the market is volatile.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In derivative transactions (contracts to transfer future funds), it is possible to calculate the present value of the amount to be transferred in the future at each point in time.

Let us assume that you have an OTC derivatives contract with a certain counterparty. The transaction is usually closed by paying (or receiving) the present value of the derivative. However, if the counterparty defaults within the contract period, you must pay an amount equivalent to the counterparty’s present value as contracted when the present value is negative from your side, but you may not be able to receive the full amount of the present value when it is positive from your side. The possibility of incurring losses in derivative transactions due to the counterparty’s default is recognized as counterparty risk.

Counterparty risk has traditionally been considered in the context of financial institutions’ risk management. After the collapse of long-term capital management in 1998 and the 2008 global financial crisis, it became mandatory for standard derivative transactions to be cleared by a central counterparty (CCP). For centrally cleared trade, various margins are exchanged according to the CCP’s rules. However, even for over-the-counter (OTC) derivative transactions not subject to central clearing, reporting requirements on major transactions to trade repositories and the exchange of margins between the parties involved are mandatory. Consequently, most transactions between major financial institutions are now subject to margin exchanges, and their counterparty risks have been significantly reduced.

Generally, derivative transactions are based on the International Swaps and Derivatives Association(ISDA) Master Agreement. Accordingly, it is common to include an additional clause, the Credit Support Annex (CSA), in the ISDA Master Agreement for Margining.

Margin requirements include the variation margin (VM), which preserves the counterparty’s exposure at each point in time, and the initial margin (IM), which preserves the variation in the exposure from the counterparty’s default to closing out.

As such, it is natural to assume that the required VM equals the value of the derivative transaction immediately before the counterparty’s default, which is the last date of margin delivery. However, the required IM cannot be determined at the counterparty’s default time because the value of derivative transactions can vary stochastically during the margin period of risk (MPoR), which is the period from the last date of margin delivery to the transaction’s closed-out timeFootnote 1.

Naively it seems better to require as large a margin amount as possible. However, increasing IM, which in principle does not allow reuse of collateral, means paying collateral procurement costs. In recent years, Green [5] has advocated that funding costs be included in the value adjustment of derivative transactions as MVA (margin valuation adjustment). Huge margins are therefore impractical because they increase transaction costs. Hence, the regulation mandates that 99% of the variation in positive exposure during the MPoR be preserved by the required IM.

However, because IM calculations in line with the regulations depend on the inputted parameters, such as volatility and the valuation model, the required IM is not always consistent among the parties. This is likely to lead to a practical problem of disagreement regarding the amount to be transferred among the parties. So, the ISDA (2021) [10] developed the ISDA Standard Initial Margin Model (SIMM) as an easy-to-use IM calculation model as an industry standard.

The ISDA SIMM is intended to be simply tractable; therefore, it does not elaborate on the features of complicated valuation models or changes in market conditions. Thus, it is possible that the IM requirement calculated using the SIMM may be insufficient in preserving 99% of the variation in positive exposure during the MPoR, which is required by the regulations. Therefore, in this study, we examine the effect on counterparty risk management of discrepancy between regulations and practice in margin calculation. More specifically, our purpose was to formulate and numerically analyze the discrepancy between the level of counterpart risk reduction during the MPoR targeted by the margin regulations and the IM requirement based on the ISDA SIMM used in practice.

First, we set a general model to discuss the margins of an OTC derivative transaction mathematically and define potential future exposure (PFE) and expected positive exposure (EPE), often referred to as counterparty risk indicators. We then introduce the margin conservation ratio (Mratio) as an original indicator to determine the extent to which the SIMM based IM meets the regulation requirements.

Then, for a generalized stochastic volatility model which assumes that the value of a derivative transaction is given by the underlying asset and “pseudo volatility," we approximately derived changes in the derivative value over the MPoR to obtain the explicit approximation formulas of PFE, EPE, and Mratio for the numerical analyses.

Furthermore, we illustrate some numerical analyses for a call option in the SABR model as an example to see if SIMM based IM in practice is sufficient for counterparty risk management.

2 Counterparty risk and margin regulation

In this section, we introduce a general mathematical model to argue for the counterparty risk of derivatives trading. First, we introduce PFE and EPE, which are risk indicators for MPoR commonly used in counterparty risk management. Both are formulated with the difference between the margin to be posted in the event of the counterparty’s default and the value of the derivative at the time when the derivative is actually closed out. Next, we focus on the difference in the calculation method of the IM between regulations and practice, because such a difference indicates that the IM calculated by a simplified method used in practice may be insufficient in achieving the regulations’ expected risk reduction.

2.1 General model for counterparty risk measurement

In this study, we first introduce a probability space \((\Omega , \mathcal {F}, \textbf{P})\); every random variable and process representing derivatives, counterparty credit risk, and so on shall be defined on this probability space. We assume that the probability measure \(\textbf{P}\) is physical.

We consider an OTC derivative contracted at time 0 with maturity T in the continuous period [0, T]. We also introduce the filtration \((\mathcal {F}_t)_{t \in [0, T]}\), which corresponds to the information time-flow available in the market.

We denote by \(\{V(t)\}\) the \((\mathcal {F}_t)_{t \in [0, T]}\)-adapted process that represents the derivative’s market value dynamics. In this study, we assume that the process \(\{V(t)\}\) is almost surely continuous. In short, if the derivative transaction is closed at time t, you can receive V(t) from the counterparty when \(V(t) > 0\) (you are in a profitable position), whereas you must pay \(-V(t)\) to the counterparty when \(V(t) < 0\) (you are in a lossy position).

An important problem is that when \(V(t) > 0\) and the counterparty falls into default, it may not fully receive the expected profit V(t) and may incur some loss. This possibility of incurring losses due to counterparty failure is the so-called “counterparty risk.”

Following the 2009 Pittsburgh Summit and the 2008 financial crisis, some regulations on derivative transactions were introduced to avoid the emergence of counterparty risk. Many derivatives traded among major financial institutions must now be cleared through the CCP system. In such cases, the CCP calculates the margin requirement based on its model and charges the necessary margins to each financial institution. CCP also settles and manages the marginal requirements.

However, exotic derivative transactions which require complex systems despite relatively low demand, and options products for which there is no model to evaluate, are commonly accepted by all market participants.

In the case of OTC derivative transactions between major financial institutions that do not involve CCPs, margin regulations require the exchange of margins to deal with counterparty risk. The margin is repaid to the counterparty if no problems occur when the derivative transaction closes. However, the posted margin can be used to compensate for losses due to counterparty’s default if one is in a profitable position and the counterparty fails, and cannot fully recover its exposure at time t. This is the basic principle of margin regulation in the trading of OTC derivatives.

Given that there is no common system, such as CCP for OTC transactions, the method of exchanging margins is determined for each contract between the parties. Generally, derivative transactions are executed on the "ISDA Master Agreement ([9])," which is the fundamental agreement established by the ISDA. Accordingly, the Credit Support Annex (CSA) is usually concluded for margin transfers as an annex to the ISDA Master Agreement.

As described above, it seems that the counterparty risk problem may be solved if the margin delivery is properly executed. However, in reality, the derivatives are not liquidated immediately when the counterparty falls into default, but after the MPoR has passed.

Thus, the following question arises: “Will the margin received at the time of the counterparty’s default be able to cover the derivative’s profitable position at the actual closed-out time?”, that is, when MPoR is given by a constant \(\delta ^{*} (> 0)\)Footnote 2 If the difference \(V(t + \delta ^{*}) - M(t)\) is positive, the margins are not sufficient; that is, counterparty risk may not be completely avoided.

In general, the required margin is divided into VM and IM. The VM directly preserves the derivative’s present value, whereas the IM is introduced to cover the variability of exposure during the MPoR, which is the period between the time of the counterparty’s default and the transaction’s actual closed-out time.

Given that both VM and IM can vary randomly depending on the derivative’s market value, they can be modeled by \((\mathcal {F}_t)\)- predictable stochastic processes \(\{ \text {VM}(t) \}\) and \(\{ \text {IM}(t) \}\), respectively. Then, the total necessary margin denoted by \(\{M(t)\}\) can be expressed as \(M(t) = \text {VM}(t)+\text {IM}(t)\).

As for the VM, the CSA usually stipulates that the required VM amount is always equal to the value of the derivative; therefore, we suppose \(\text {VM}(t) = V(t)\).

Consequently, we have

Andersen et al. [1] mention three kinds of exposure modeling during MPoR:Classical\(+\), Classical−, and Advanced. Our model corresponds to classical \(+\), which is the simplest.

The IM is intended to cover the variation in the derivative value during the MPoR; however, the required IM cannot be determined because of the variation uncertainty \(V(t + \delta ^{*}) - V(t)\) at the time of the counterparty’s default when the final margin is transferred.

Regarding the problem, the regulations specify the required IM as the (conditional) 99 % point of \(V(t + \delta ^{*}) - V(t)\) so that it can be evaluated at time t of the counterparty’s default.

Therefore, the IM required by the regulations, denoted by \(\text {IM}^{\textrm{Reg}}(t, \delta ^{*})\), is defined as

where \(a^+:= \max \{a, 0\}\) for \(a \in \mathbb {R}\).

To specifically calculate the required IM using (1), it is necessary to identify the conditional probability distribution of the variation \(V(t + \delta ^{*}) - V(t)\), a specific model that describes the dynamics of the process \(\{V(t)\}\). However, derivative valuation models are selected depending on the market environment, financial institutions’ management policies, and academic research progress; the specification of models for calculating IM is not mentioned by the regulations, so the same model is not necessarily used among financial institutions.Footnote 3

Therefore, because it is necessary to calculate the required IM and transfer it smoothly without referring to the specific model of \(\{V(t)\}\), a simplified IM calculation method was developed primarily by the ISDA and has become the industry standard, as discussed in the next subsection.

2.2 IM calculation used in practice: ISDA SIMM

Financial institutions usually have their own valuation models for each derivative transaction and calculate sensitivities, such as delta and vega for risk management. The ISDA proposed a simplified method to calculate IM using sensitivities calculated by financial institutions and a common estimate of market volatility. This is a feature of the industry standard IM calculation method, called the ISDA SIMM. For simplicity, we focus on an interest rate option, such as swaption, excluding margins due to analysis concentration risks.

Suppose the market value of the derivative is given as a function of time t, the value of the underlying asset or variable is denoted by X, and the volatility of the underlying asset is denoted by \(\sigma\).

Then, the ISDA SIMM defines the IM requirement \(\text {IM}^\textrm{CSA}(t)\) for interest rate derivatives and credit derivatives as the sum of the Delta, Vega, and Curvature margins (Refer to ISDA [10] for details).Footnote 4

where the three IM terms on the right-hand side are defined as followsautoedited.:Footnote 5

Note that 1bp stands for 1 basis point, \(= 0.01\%\).

Here, by abuse of notation, we regard the derivative value as \(V(t) = V(t, X(t), \sigma (t))\) with a function \(V(t, x, \sigma )\) obtained from a specified valuation model. We also suppose that we calculate the variations of \(V(t, X(t), \sigma (t))\) for 1bp changes of the underlying asset X(t) and the volatility \(\sigma (t)\) as approximations of the Delta \(\dfrac{\partial V}{\partial x}(t, X(t), \sigma (t))\) and the Vega \(\dfrac{\partial V}{\partial \sigma }(t, X(t), \sigma (t))\).

Furthermore, \(\text {RW}\) and \(\text {VRW}\) are positive constants called SIMM coefficients, which are supposed to correspond to the 99 % of the small variations for a small change of the underlying asset and the volatility, respectively. The ISDA updates the SIMM coefficients annually by estimating them with the market data for the last three years and for stressed years of increasing volatility, such as 2008, to keep the values conservative.Footnote 6

We note that the MPoR is not explicitly included in the ISDA SIMM formula for calculating the required IM because the SIMM coefficients are estimated under the assumption that MPoR is set to 10 days.

2.3 Indicators of counterparty risk: PFE and EPE

We focus on the Positive Exposure (PE) \(\left( V(t + \delta ^{*}) - M(t) \right) ^{+}\) because the excess liquidated amount after MPoR of the derivative over the margin preserved is at issue. Gregory [7] defines PFE as an indicator of counterparty risk given the level at which the probability that the positive risk exposure exceeds the counterparty risk by no more than 1% under a real probability measure. He also performs the EPE using the expected value of positive risk exposure. As you notice, the PFE corresponds to the VaR with a 99% confidence level, which is often used as a market risk measure.

Thus, we specify the PFE and EPE for MPoR \(\delta ^{*}\) at time t as \(\mathcal {F}_{t}\)-conditional random variables as follows:

It follows that the theoretical PFE for regulation-based \(\text {IM}^{\textrm{Reg}}(t, \delta ^{*})\) given by (1) becomes zero.

However, if we calculate the PE in practice based on the ISDA SIMM, we see that the practical PFE denoted by \(\text {PFE}^{\textrm{CSA}}\) does not vanish unless \(\text {IM}^{\textrm{Reg}}(t, \delta ^{*}) \le \text {IM}^{\textrm{CSA}}(t)\), as below.

Given that counterparty risk is often used to visualize the impact on a financial institution’s capital and the value of derivative transactions, it is generally measured in terms of monetary amounts, such as PFE and EPE. In contrast, this study focuses on the extent to which the IM requirement in practice meets that of the regulations, which is specified as a conservation ratio of 99 % of the exposure variation during MPoR. Hence, to determine the extent, we define the Mratio at time t, which is an original indicator in this study, by the \(\mathcal {F}_t\)-conditional probability that positive exposure in practice equals zero as

It follows from the definition of \(\text {IM}^{\textrm{Reg}}(t; \delta ^{*})\) in (1) that the Mratio is 99% when \(\text {IM}^{\textrm{CSA}}(t) = \text {IM}^{\textrm{Reg}}(t; \delta ^{*})\).

Thus, the discrepancy between regulations and practices in IM calculations can be a problem in counterparty risk management in OTC derivative transactions, even with an IM.

In the next section, we present specific formulas for PFE, EPE and Mratio for a general stochastic volatility model. Specifically, we conduct a numerical analysis of the SABR model with a European call option.

3 Counterparty risk measurement specified for a stochastic volatility model

In the previous section, we discussed the possibility that the IM requirements calculated using the ISDA SIMM used in practice may not have reached required regulation levels. In this section, we first introduce a generalized stochastic volatility model and theoretically derive an approximate evaluation formula for the PE using Ito’s formula. Based on the PE approximation, we demonstrate how to calculate PFE, EPE, and Mratio presented in the previous section. As an illustrative example, we demonstrate how to obtain the PFE and EPE of a payer swaption, a type of interest rate derivative that can be regarded as a European call option, with a forward swap rate as the underlying asset under the SABR model (a stochastic volatility model often used in practice).

3.1 Derivation of approximate counterparty risk indicators

Hereafter, we suppose that the value process \(\{V(t)\}\) of a derivative transaction can be expressed by \(V(t) = V(t, X(t), \sigma (t))\) as a function of time t, the underlying asset X(t) and the volatility of the underlying asset (or something that plays a similar role) \(\sigma (t)\) to be consistent with the ISDA SIMM that uses Vega, the sensitivity of V(t) to volatility.

We assume that the underlying asset process \(\{X(t)\}\) and pseudo-volatility process \(\{\sigma (t)\}\) satisfy the following stochastic differential equations (SDEs), called the generalized stochastic volatility model: We note that \(\sigma (t)\) itself is not the true volatility of the underlying asset, but in most specific models, it essentially plays a role in driving the volatility; thus, we call it pseudo-volatility.

where \(\mu _{X}(t, x, \sigma ), \mu _{\sigma }(t, x, \sigma ), \sigma _{X}(t, x, \sigma )\) and \(\sigma _{\sigma }(t, x, \sigma )\) are “good” functions satisfying some regularity conditions that guarantee the existence and uniqueness of strong solutions for the above SDEs, and \(W_{X }^{\textbf{P}}(t)\) and \(W_{\sigma }^{\textbf{P}}(t)\) are correlated standard Brownian motions under the physical measure \(\textbf{P}\) with constant correlation \(\rho \in [-1,1]\), that is, \(dW_{X}^{\textbf{P}}(t) dW_{\sigma }^{\textbf{P}}(t) = \rho dt\).

From Ito’s formula, it follows that if the function \(V(t, x, \sigma )\) is a \(C^{1,2,2}\)-function, we have (for simplicity, write \({\partial _x}V(t)\) and \({\partial _{xx}^2}V(t)\) instead of \(\dfrac{\partial V}{\partial x}(t, X(t), \sigma (t))\) and \(\dfrac{\partial ^2 V}{\partial x^2}(t, X(t), \sigma (t))\) respectively, and so on)

We fix time t for the remainder of this subsection.

Given that MPoR \(\delta ^{*}\) can be regarded as a sufficiently short period, from a few days to a maximum of two weeks (\(\dfrac{\textrm{14 Days}}{\textrm{365 Days}}\) is used in the numerical illustration later), it is possible to apply the discrete approximation of (8) by considering \(dt \approx \delta ^{*}\). Accordingly, \(dW_{X}(t)\) and \(dW_{\sigma }(t)\) can be approximately replaced with \(\sqrt{\delta ^{*}} Z_{X}\) and \(\sqrt{\delta ^{*}} Z_{\sigma }\), where \(Z_{X}\) and \(Z_{\sigma }\) are two standard normally distributed random variables with correlation \(\rho\).

Subsequently, the PE based on ISDA SIMM is approximately represented as follows:

where we define \(\mathcal {F}_{t}\)-measurable random variables \(A_{X}, A_{\sigma }\), and \(A_{C}\) as

Given that \(Z_{X}\) and \(Z_{\sigma }\) are independent of \(\mathcal {F}_{t}\) and each follows a standard normal distribution, the conditional expectation and variance of \(A_{X}(t) Z_{X} + A_{\sigma }(t) Z_{\sigma } + A_{C}(t)\) are represented as follows:

Moreover, letting \(A_{z}(t):= \sqrt{A_{X}(t)^{2} + 2 \rho A_{X}(t) A_{\sigma }(t) + A_{\sigma }(t)^{2}}\), we can obtain another standard normal variable Z independent of \(\mathcal {F}_{t}\) specified by

Thus, we have

Finally, it follows from (3) and (4) that \(\text {PFE}^{\textrm{CSA}}(t; \delta ^{*})\) and \(\text {EPE}^{\textrm{CSA}}(t; \delta ^{*})\) can be obtained as follows:

where \(\textbf{1}_{A}\) is the indicator variable of event \(A \in \mathcal {F}\) and \(\Phi ( \cdot )\) is the standard normal distribution function.

Moreover, the Mratio, defined in (5), can be calculated as

3.2 Example: payer swaption with SABR model

For the numerical analysis of counterparty risk indicators in the next section, we set up a derivative transaction and its valuation model as examples.

As mentioned above, many derivative transactions have become subject to centralized clearing, but exotic derivatives with small trading volumes and some products for which valuation models are difficult to construct are still traded over the counter. In this study, we will use a “payer swaption” (an interest rate derivative that is commonly traded over the counter despite its relatively high trading volume) as an example for numerical analysis from a practical viewpoint.

This option uses the forward swap rate as the underlying asset and can be exercised only on the expiration date. When the option is exercised at maturity, a swap transaction in which the swaption holder pays the fixed rate and receives the floating rate can be initiated (or cleared by exchanging cash, depending on the contract) at strike rate K. For simplicity, the current annuity value is assumed to be one. Therefore, if X(t) represents the forward swap rate at time t, the option payoff V(T) at maturity T is given by the European call option as follows:

Next, we adopt the SABR model as the valuation model, a type of stochastic volatility model proposed by Hagan et al. [8]. The SABR model is often used in interest rate derivative transactions since it considers the volatility skew. In general, the SABR model is formulated as follows. The underlying forward swap rate \(\{X(t)\}\) and the pseudo-volatility \(\{\sigma (t)\}\) follows the SDEs under a swap measure,Footnote 7 denoted by \(\textbf{Q}\).

where \(\{W_{X}^{\textbf{Q}}(t)\}\) and \(\{W_{\sigma }^{\textbf{Q}}(t)\}\) are standard Brownian motions under the measure \(\textbf{Q}\) with \(dW_{X}^{\textbf{Q}}(t) dW_{\sigma }^{\textbf{Q}}(t) = \rho dt\), and the parameters \(\sigma (0)> 0, \beta \in [0,1], \nu > 0\) and \(\rho \in [-1,1]\) are constants.

Note that we can view the SABR model as an example of the generalized stochastic volatility model specified by (6) and (7) by setting \(\mu _{X}(t, x, \sigma ) = \mu _{\sigma }(t, x, \sigma ) = 0, \sigma _{X}(t, x, \sigma ) = \sigma x^{\beta }\) and \(\sigma _{\sigma }(t, x, \sigma ) = \nu \sigma\), though the underlying probability measures are different.

To manage counterparty risk in PFE and so on, it is necessary to transform the dynamics under the swap measure \(\textbf{Q}\) to those under the physical measure \(\textbf{P}\), which will be discussed later.

Hagan et al. [8] derive two types of approximations for pricing European call options using the SABR model. One is consistent with the case of \(\beta =1\) or the Black model (where the forward rateX(t) is log-normal), and the other is consistent with \(\beta =0\) or the Bachelier model (where X(t) is normal). Although negative interest rates have been observed in developed countries since the beginning of the 2010s, the Black (lognormal) model cannot allow for negative interest rates. This study uses the approximation pricing formula consistent with the Bachelier (normal) model. We let \(\sigma _N\) be pseudo-volatility in terms of Bachelier’s model, with \(dX(t) = \sigma _N dW_{X}^{\textbf{Q}}(t)\).

We denote this by \(V(t) = V(T-t, X(t), \sigma _N(t), K)\) the price at time \(t \in [0,T]\) of the European call option with strike K and maturity T. Here, we assume that \(\sigma _N(t)\) is the implied pseudo-volatility at time t, which is consistent with the Bachelier model where \(dX(t) = \sigma _N dW_{X}^{\textbf{Q}}(t)\).

Following Appendix B.2. in Hagan et al. [8], we can approximate \(V(T-t, X(t), \sigma _N(t), K)\) for \(\beta \in (0, 1)\) as:

where

Using the approximate analytical solution for the option price, we can calculate partial derivatives, such as \(\dfrac{\partial V}{\partial x}(t)\) and \(\dfrac{\partial V}{\partial \sigma }(t)\) to obtain counterparty risk indicators.

We suppose that the risk premiums \(\theta _{X}(t)\) and \(\theta _{\sigma }(t)\) are given as \((\mathcal {F}_t)\)-adapted processes that satisfy

Thus, it follows from the Girsanov-Maruyama theorem that Brownian motions \(W_{X}^{\textbf{Q}}(t)\) and \(W_{\sigma }^{\textbf{Q}}(t)\) under the swap measure \(\textbf{Q}\) are converted into Brownian motions \(W_{X}^{\textbf{P}}(t)\) and \(W_{\sigma }^{\textbf{P}}(t)\) under the physical measure \(\textbf{P}\); we can then obtain the dynamics of X(t) and \(\sigma (t)\) with \(W_{X}^{\textbf{P}}(t)\) and \(W_{\sigma }^{\textbf{P}}(t)\) under the measure \(\textbf{P}\).

Given that we have

we can obtain the \(\mathcal {F}_t\)-measurable components \(A_{X}(t), A_{\sigma }(t)\), and \(A_{C}(t)\) (given in (10), (11), and (12)) needed to calculate the risk indicators PFE, EPE, and Mratio for MPoR \(\theta\) (given in (13), (14), together with \(A_{z}(t):= \sqrt{A_{X}(t)^{2} + 2 \rho A_{X}(t) A{\sigma }(t) + A_{\sigma }(t)^{2}}\)).

where \(\text {RW}\) and \(\text {VRW}\) are the SIMM coefficients and \(\text {SF}:= 0.5 \cdot \min \left\{ 1, \dfrac{14 \text {Days}}{T-t} \right\}\) is introduced in subsection 2.2.

In Section A of Appendix A, we demonstrate how to derive the Greeks for the pricing formula (19) of the European call option under the SABR model.

We can further obtain specific expressions for partial derivatives of \(\sigma _N\) with respect to the underlying and pseudo-volatility; however, because they are very complicated expressions, the partial derivatives are numerically computed by taking the central difference.

4 Numerical illustration

In this section, as prepared in the previous subsection, we numerically calculate the counterparty risk indicators (such as PFE) under some conditions for the payer swaption for the SABR model to see how different parameters (such as pseudo-volatility) affect the indicators. We also attempt to determine the source of PFE by decomposing the exposure into three components: Delta, Vega, and Curvature.

4.1 Assumptions for numerical calculations for counterparty risk indicators

First, we assume that the payer swaption used in the numerical analysis has a strike price of \(K = 3.00\%\) and a time to maturity of \(T - t = 1 \text { (Year)}\); that is, the payoff at maturity is given by

For the coefficients of the SABR model, we assume \(\beta = 0.75\) so that we can account for the situation where the volatility increases as interest rates rise, and thus the forward rate approaches a log-normal model with \(\beta = 1\). In addition, we suppose \(\nu = 0.30\) for the volatility of the pseudo-volatility and \(\rho = 0.5\) for the correlation between the underlying asset and its pseudo-volatility. In short, we assume

The ISDA SIMM based IM, denoted by \(\text {IM}^{\textrm{CSA}}\), depends on SIMM coefficients RW and VRW published by the ISDA. The SIMM coefficients for the interest rate derivatives in 2021, published by the ISDA [10] are shown in Table 1.

The RWs for regular currenciesFootnote 8 generally remains between 50 and 60, except for periods of less than one year. The VRW is 0.18 for all currencies. In this study, we assume RW\(= 60\) and VRW\(= 0.20\) for all periods to simplify the calculations.

The MPoR is set to 10 business days.

according to BCBS [2].

Finally, in order to calculate the risk indicators such as PFE, it is necessary to determine the risk premiums \(\theta _{X}(t)\) and \(\theta _{\sigma }(t)\) between the physical measure \(\textbf{P}\) and the swap measure \(\textbf{Q}\). In this example of the call option, we can see that the larger these values are, the higher the PFE and EPE via the argument in subsection 3.1. However, it is difficult to specify and estimate \(\theta _{X}(t)\) and \(\theta _{\sigma }(t)\) although the actual risk premiums seem rather likely to be positive. Taking these into account, we set both \(\theta _{X}(t)\) and \(\theta _{\sigma }(t)\) (equivalently \(\mu _{X}(t)\) and \(\mu _{\sigma }(t)\)) to zeroFootnote 9 so that we can find the lower limit of the risk indicators in a sense. Hence, the actual risk indicators, if the risk premiums are likely to positive, are expected to be worse than those with the zero risk premiums.

The parameters and other factors assumed in the numerical calculations are listed in Table 2.

4.2 Numerical results of counterparty risk indicators

In the following, we numerically calculate counterparty risk indicators PFE, EPE, and Mratio based on the ISDA SIMM method.

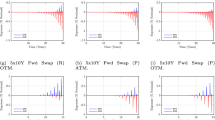

First, for each of the three pseudo-volatility cases of \(\sigma (t)=\) 10, 15, and 20%, we compute the counterparty risk indicators with values of X(t) ranging from 1% to 7%. The weekly data for the 10-year U.S. interest rate from 1990 to the end of 2023 show that it has ranged between 0.5% and 9.0%, with rate of 1% and 7% corresponding to about the second and the 90th percentile point of the whole sample, respectively. Although the pseudo-volatility cannot be directly observed, a naive calculation, assuming volatility to be a constant at each point in time, implies that the pseudo-volatility can be regarded as roughly between 5% and 30% within the above data period. Especially around 20% during the 2008 financial crisis and the upper 20% range during the 2020 coronavirus pandemic. Thus, we believe that the ranges of X(t) and \(\sigma (t)\) used for our numerical experiments are reasonable from a risk management perspective.

The results are presented in Fig. 1. We can easily check whether the IM meets regulation requirements by observing the Mratio in the graphs. Specifically, we can see that in low pseudo-volatility with \(\sigma (t) =\)10%, \(\text {IM}^{\textrm{CSA}}\) is sufficient even for deep in-the-money or high underlying forward rates. It is particularly noticeable that, especially for the high pseudo-volatility case of \(\sigma (t) =\)20%, the PFE (red line) increases rapidly, whereas Mratio (blue line) decreases rapidly when the underlying forward rate X(t) is in-the-money or greater than the strike price \(K=3.00 \%\).

The counterparty risk indicators of PFE, EPE, and Mratio based on the ISDA SIMM method for the values of X(t) ranging from 1% to 7% for three pseudo volatility values: 10% (left), 15% (middle), and 20% (right), respectively. The scale of PFE and EPE is on the left-hand side, while that of Mratio is on the right-hand side (displayed in %)

Next, we calculate the counterparty risk indicators with \(\sigma (t)\) values ranging from 5% to 25% for the out-of-the-money case with \(X(t) = 2\%\) and for the in-the-money case with \(X(t) = 4\%\) and 6%.

The results are presented in Fig. 2. We can see that in the out-of-the money case, \(\text {IM}^{\textrm{CSA}}\) is sufficient even when the volatility is high; however, as the degree of in-the-money increases, the decrease in Mratio becomes steeper with an increase in pseudo-volatility. This numerical illustration assumes \(\mu _X = \mu _\sigma = 0\), so PFE and EPE can increase (Mratio can decrease) for in-the-money trades if \(\mu _X>0\) or \(\mu _\sigma >0\).

The counterparty risk indicators PFE, EPE, and Mratio are based on the ISDA SIMM method for \(\sigma (t)\) values ranging from 5% to 25%, for three values of the underlying forward rate \(X(t) =\) 2% (left), 4% (middle), and 6% (right), respectively. The scale of PFE and EPE is on the left-hand side, while that of Mratio is on the right-hand side (displayed in %)

4.3 Factor decomposition of risk

In ISDA SIMM, as shown in (2), the total \(\text {IM}^\textrm{CSA}\) is calculated by adding \(\text {IM}^{\textrm{Delta}}\), \(\text {IM}^{\textrm{Vega}}\) and \(\text {IM}^{\textrm{Cvtr}}\). If it is possible to determine the extent to which the PFE is related to Delta, Vega, and Curvature factors, this will be useful for counterparty risk management.

Remember that we have

where \(Z_{X}\) and \(Z_{\sigma }\) are standard normal random variables.

In light of this, it follows from (9)–(12) that the exposure during the MPoR over the SIMM based IM, \(V(t+\delta ^{*}) - V(t) - \text {IM}^{\textrm{CSA}}(t)\), can be approximately captured by decomposing it into three factors related to Delta, Vega, and Curvature as seen below.

where

We now discuss 99 % of the future exposure (FE), which can be negative, for each factor \(L^{\mathrm{*}}(t, \delta ^{*})\) in terms of the factorial risk decomposition. However \(L^{\textrm{Cvtr}}(t, \delta ^{*})\) does not include any random variable, so it is considered to contribute as a constant for fixed t.

For that purpose, we denote by \(99\%\text {-FE}^{\textrm{Delta}}(t; \delta ^{*})\) (resp. \(99\%\text {-FE}^{\textrm{Vega}}(t; \delta ^{*})\)) 99 % of the PFE for the factor related to Delta (resp. Vega) given as

However, we should remark

Under the same conditions as in Sect. 4.1, we compute 99 % of FE of each factor for values of X(t) ranging from 1% to 7% for three pseudo-volatility cases: for the case of a normal period with \(\sigma (t) =\)10% or 15% and for the shock period with \(\sigma (t) =\)20%. Factor decomposition results are shown in Fig. 3.

The 99 % of FE of each factor related to Delta, Vega, and Curvature for X(t) values ranging from 1% to 7%, for three pseudo volatility values \(\sigma (t) =\)10% (left), 15% (middle), and 20% (right), respectively

In addition, we compute 99 % of FE of each factor for the values of \(\sigma (t)\) ranging from 5% to 25% for the out-of-the-money case with \(X(t) = 2\%\) and for the in-the-money case with \(X(t) = 4\%\) and 6%. Results are displayed in Fig. 4.

The 99 % of FE of each factor related to Delta, Vega, and Curvature for the \(\sigma (t)\) values ranging from 5% to 25% for the out-of-the money case with \(X(t) = 2\%\) and for the in-the-money case with \(X(t) = 4\%\) and 6%, respectively

Both figures indicate that the delta-related factor contributes most significantly to the increase in PFE when the pseudo-volatility is relatively high.

In an actual interest rate market environment, a sudden rise in inflation may force the central bank to reduce quantitative easing (tapering) or sharply raise interest rates. Considering that volatility and forward rates are likely to increase simultaneously under such fluctuations in the financial environment, the rapid manifestation of counterparty risk, which is not preserved by IM in practice, cannot be ruled out; this is implied by our numerical analysis.

5 Another application of the model to credit valuation adjustments

If the counterparty to a derivative transaction cannot be asked to provide margin or collateral, it is common to calculate the “Credit Valuation Adjustment (CVA)” as “the difference between the value of the derivative transaction with and without considering the possibility of the counterparty’s default under the risk neutral probability measure,” and to see the CVA as a counterparty risk indicator, as mentioned in Green [5] and so forth.Footnote 10

In this section, we do not discuss the CVA evaluation issue in earnest, but after reviewing the equation of CVA for positive exposure \(\left( V(t + \delta ^{*}) - M(t) \right) ^{+}\) considering the MPoR \(\delta ^{*}\) under some naive assumptions. Subsequently, under a setting similar to that in the previous section, we perform a simple analysis by numerically computing CVA for the payer swaptions under the SABR model.Footnote 11

5.1 CVA considering MPoR

To calculate CVA, we consider the uncertainty of derivative transactions and counterparty’s defaults in the probability space \((\Omega , \mathcal {F}, \tilde{\textbf{P}})\), where the probability measure \(\tilde{\textbf{P}}\) is a risk-neutral probability measure. Here, we consider bilateral CVA under simple assumptions and a close-out condition with MPoR.

Next, we model the default-free interest rate, the risk-neutral hazard rate (default intensity) for each of itself and its counterparty, and the recovery rate given counterparty default. Although it is preferable to model them using stochastic processes to obtain CVA precisely, we assign them as constants for simplicity because we do not consider credit risk itself in this study. Note that implicit in this assumption is that the interest rate, default risks of the parties, and derivative market values are all independent.

We let r be the default-free interest rate, and \(\lambda _B\) and \(\lambda _C\) be the risk-neutral hazard rates of yourself (B) and the counterparty (C), respectively. We regard the hazard rate as satisfying the following \(\lambda _{*} \ ({*} = B \text { or } C)\) as satisfying \(\tilde{\textbf{P}} \left( \tau _{*} > t \right) = e^{ -\lambda _{*} t}\), where \(\tau _B\) (resp. \(\tau _C\)) is the user’s default time (resp. the counterparty).

With a slight modification to the bilateral CVA standard expression shown in subsection 3.3 of Green [5], we find that under the above conditions, the expression for bilateral CVA, denoted by \(\text {CVA}(t; \delta ^{*})\), at time t considering MPoR \(\delta ^{*}\) is given by

where \(R_C\) is a constant recovery rate, given counterparty default, and \(\text {DF}(t, u) \ (u \in [t,T])\) denotes the default risk-adjusted discount factor, given by

The closed-out amount must be discounted at the default-free interest rate from the closed-out time, whereas the counterparty’s default is supposed to occur at time u.

As we observe, the conditional expectation term in the integrand of (23) can be transformed into

where the EPE given in (4) is calculated here under the risk-neutral measure \(\tilde{\textbf{P}}\) instead of \(\textbf{P}\).

Hence, we can approximately calculate this conditional expectation term as an example of payer swaption in the SABR model using (14) and (20)-(22) with \(\theta _{X}(t) = \theta _{\sigma }(t) = 0\).

5.2 Numerical analysis for CVA

The parameters for CVA’s numerical calculation are assumed to be \(r = 0.03, \lambda _{B} = 0.005, \lambda _{C} = 0.01\), and \(R_{C} = 0.4\). The integral part is discretized by the time step \(\Delta = 1 / 365\); thus, we calculate the CVA at time t with the time to maturity \(T -t = 1\) as follows:

Our CVA numerical calculations are performed using the following algorithm based on a Monte Carlo simulation with 1,000 trials. Given that the objective is not to obtain the exact CVA value, but to roughly observe the CVA trend for different values of X(t) and \(\sigma (t)\), the number of trials is limited to 1,000 for computational efficiency.

-

1.

Give the initial values X(t) and \(\sigma (t)\) at initial time t.

-

2.

For n-th trial (\(n=1,2,\ldots ,1000\)), we set \(X^{(n)}(t) = X(t), \sigma ^{(n)}(t) = \sigma (t)\) and then generate pseudo-random numbers for correlated normal variables \(Z_X\) and \(Z_{\sigma }\). We then inductively obtain discretized paths of the underlying forward rate \(\{X^{(n)}(t + k \Delta )\}\) and the pseudo volatility \(\{\sigma ^{(n)}(t + k \Delta )\}\) \((k = 1,2, \ldots , 365)\) with the following formulas:

$$\begin{aligned} X^{(n)}(t + k\Delta )&= X^{(n)}(t + (k-1) \Delta ) \\&\qquad + \sigma ^{(n)}(t + (k-1) \Delta ) \left( X^{(n)}(t + (k-1) \Delta ) \right) ^{\beta } \sqrt{\Delta } z_x^{(n,k)}, \\ \sigma ^{(n)}(t + k\Delta )&= \sigma ^{(n)}(t + (k-1) \Delta ) + \nu \sigma ^{(n)}(t + (k-1) \Delta ) \sqrt{\Delta } z_{\sigma }^{(n,k)}, \end{aligned}$$where \(\{(z_{X}^{(n,k)}, z_{\sigma }^{(n,k)})\}_{k=1,2,\ldots ,365}\) are a series of pairs of generated pseudo-random numbers of correlated normal variables \((Z_X, Z_{\sigma })\).

-

3.

Calculate n-the conditional expectation samples in (24) given by

$$\begin{aligned} \text {EPE}^{(n), \textrm{CSA}, \tilde{\textbf{P}}}\left( t+k \Delta ; \delta ^{*}\right) \ (k = 1,2, \ldots , 365), \end{aligned}$$by substituting, at each time \(t + k\Delta\), the randomly generated values \(X^{(n)}(t + k\Delta )\) and \(\sigma ^{(n)}(t + k\Delta )\) into the approximate EPE formula (14) with the components (20)–(22) obtained in the SABR model.

-

4.

We finally achieve the CVA approximately from the following formula.

$$\begin{aligned} \text {CVA} (t; \delta ^{*})&\approx \left( 1 - 0.40 \right) \times 0.01 \times \frac{1}{365} \sum ^{365}_{k=1} e^{-0.03 \times \frac{k+14}{365} - \left( 0.005 + 0.01 \right) \times \frac{k}{365} }\\&\qquad \qquad \qquad \qquad \times \frac{1}{1000}\sum _{n=1}^{1000} \text {EPE}^{(n), \textrm{CSA}, \tilde{\textbf{P}} }\left( t + \frac{k}{365}; \delta ^{*} \right) . \end{aligned}$$

The results are presented in Table 3. It can be seen that CVA is likely to increase as the underlying forward rate X(t) or pseudo-volatility \(\sigma (t)\) increases. In addition, we suggest that the magnitude of the increase depends on the level of \(\nu\). This is because the parameter \(\nu\) affects X(t) and \(\sigma (t)\) over time, thereby affecting exposure throughout the option period.

6 Concluding remarks

Regulations for OTC derivatives trading, initiated after the G20 Pittsburgh Summit (2009) and triggered by the financial crisis, have been completed with the full enforcement of the OTC derivatives trade reporting system (2010), central clearing obligation (2012), electronic trading platform usage obligation (2015), VM requirements (2017) and IM requirements (2022). Their implementation has resulted in the significant reduction of counterparty risks among major financial institutions. In particular, the impact of defaults by individual financial institutions on the financial system has been reduced because the majority of derivative transactions are underwritten by CCPs through central clearing. In addition, counterparty risks for OTC derivative transactions that are not underwritten by CCPs have decreased since the VM and the IM were mandated by the regulations.

However, the IM, which protects against the positive exposure of derivative transactions during the MPoR, can only be transferred immediately before the counterparty’s default. Therefore, the regulation requires that 99% of PE fluctuations be maintained. On the other hand, in practice, the IM requirement has been calculated using a simple calculation method based on the ISDA SIMM. Consequently, there may be a discrepancy between regulation and practice in some cases, with concerns raised that practical SIMM-based IM may not meet required regulation levels.

In fact, ISDA constantly validates its models through back-testing. In 2023, the SIMM coefficients were revised on a quarterly basis instead of once a year as usual, taking into account the rapid fluctuations in the interest rate market. In addition, the frequency of revision of the SIMM coefficients will be changed to twice a year in principle from 2025.Footnote 12

In this study, we first provide a framework to quantitatively evaluate the discrepancy between the 99% PE required by the regulation and the simplified method based on the ISDA SIMM used in practice, with respect to the IM calculation method considering MPoR. Under a general stochastic volatility model, we then derive the approximate formula for PFE and EPE, which are common counterparty risk indicators as well as Mratio, which is newly introduced as a conservation ratio of IM to the variation of derivative transactions’ exposure during the MPoR.

Moreover, we perform numerical analyses of the counterparty risk indicators for payer swaptions (European call options) using the SABR model, which is a stochastic volatility model. It is suggested that if the position is in-the-money and volatility increases, SIMM based IM may not be sufficient to avoid counterparty risk, though it performs well under normal conditions with low volatility.

In addition, we attempt to decompose the PFE calculated by ISDA SIMM into three factors related to Delta, Vega, and Curvature. We also show that the prepared framework could be applied to CVA calculations.

In a real market environment, interest rates and volatility can rise simultaneously due to the monetary policy of sharply raising interest rates. In such cases, the counterparty risk becomes apparent. Even if the counterparty does not default, a CVA may result in accounting losses. Therefore, this study reaffirms the importance of counterparty risk management, even in fully margined derivatives transactions.

Data availability

Data sharing is not applicable to this paper since no real data is analyzed in this study.

Notes

According to the Basel Committee on Banking Supervision (BCBS) (2019) [3], the MPoR is defined as the period from the last exchange of collateral covering a netting set of transactions with a defaulting counterparty until the counterparty is closed and the resulting market risk is re-hedged.

As MPoR is undetermined at the time of the counterparty’s default, it seems natural to regard it as a random variable. However, closed-out derivative transactions are often completed within a few days to two weeks after the counterparty’s default. Therefore, MPoR \(\delta ^{*}\) is treated as a given positive constant in this study for ease of handling.

For example, LCH, a British clearing house group, announced that it calculates its IM requirements for the swap-clearing market using Value at Risk (VaR) or Expected Shortfall, which is derived from historical simulations of five-day fluctuations over the past 10 years. (See the LCH website [13].)

For derivatives other than interest rate and credit derivatives, the basic concept of calculating IM requirements remains the same, although the formulas differ.

Delta and Vega are common option risk indicators. As for Curvature, it is not clear why ISDA uses this term, but a possible explanation is that Curvature is attributed to the second partial derivative of the option value with respect to the underlying asset, that is, so-called “Gamma.” In the Black-Scholes model, Vega and Gamma are known to be proportional; therefore, the Curvature Margin may be considered to correct the effect of Ga:mma on Vega.

Such a parameter estimation is often called the “3+1 method.”

A swap measure, equivalent to the risk-neutral measure, is a pricing measure whose numeraire is an annuity or a portfolio of zero coupon bonds with different maturities. The forward swap rate process becomes a martingale under the associated swap measure. (Refer to Jamshidian [12] for details.)

The regular currencies are USD, EUR, GBP, CHF, AUD, NZD, CAD, SEK, NOK, DKK, HKD, KRW, SGD, and TWD, whereas the only low-vol currency designated is the JPY. Other currencies are classified as high-vol currencies.

We do not assume the risk premiums of the model are actually zero here. It seems indeed unreasonable to assume that the actual risk premium that emerges by measure change from the physical probability measure to the swap measure are zero.

In addition to counterparty risk (CVA), costs or benefits associated with own credit risk (DVA), funding (FVA), margin (MVA), regulatory capital (KVA), and so forth, are now considered in valuation adjustments. Collectively, these are referred to as XVA, which is important for financial institutions to calculate and manage accurately because it is often recognized for accounting purposes. See Gregory [7] for the detail of XVA.

Although not considered in this paper, it has become common in practice to consider Initial Margin Valuation Adjustment (IMVA) when IM is taken into account in CVA calculation. See Green and Kenyonz [6] for the detail of IMVA.

Refer to a website of ISDA [11].

References

Andersen, L., Pykhtin, M., Sokol, A.: Credit exposure in the presence of initial margin. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=2806156 (2017). Accessed 17 Jan 2024

Basel Committee on Banking Supervision (BCBS) Minimum capital requirements for market risk. https://www.bis.org/bcbs/publ/d457.htm (2016). Accessed 17 Jan 2024

Basel Committee on Banking Supervision (BCBS) CRE, Calculation of RWA for credit risk: CRE50, Counterparty credit risk definitions and terminology. https://www.bis.org/basel_framework/chapter/CRE/50.htm (2019). Accessed 17 Jan 2024

Burgard, C., Kjaer, M.: Funding costs, funding strategies. Risk 26, 82–87 (2013)

Green, A.: XVA: Credit, Funding and Capital Valuation Adjustments. Wiley, Amsterdam (2016)

Green, A., Kenyonz, C.: MVA: initial margin valuation adjustment by replication and regression. Working paper (2015)

Gregory, J.: The XVA Challenge: Counterparty Risk, Funding, Capital and Initial Margin. Wiley, Collateral (2020)

Hagan, P.S., Kumar, D., Lesniewski, A.S., Woodward, D.E.: Managing smile risk. Wilmott Magazine, pp. 84–108 (2002)

International Swaps and Derivatives Association (ISDA) 2002 ISDA master agreement. (2002)

International Swaps and Derivatives Association (ISDA) ISDA SIMM methodology version 2.4. https://www.isda.org/a/CeggE/ISDA-SIMM-v2.4-PUBLIC.pdf (2021). Accessed 17 Jan 2024

ISDA website, derivatiViews News ‘ISDA SIMM to Move to Semiannual Calibration.’ https://www.isda.org/2023/09/07/isda-simm-to-move-to-semiannual-calibration/. Accessed 17 Jan 2024

Jamshidian, F.: LIBOR and swap market models and measures. Financ Stochast. 1, 293–330 (1997)

The LCH group website, Risk Management - LTD. https://www.lch.com/risk-management/risk-management-ltd. Accessed 17 Jan 2024

Acknowledgements

This study was supported by JSPS KAKENHI Grant Number JP20K04960 and JP23K04285. We are also deeply grateful to the anonymous reviewers for their helpful comments and to Editage for English language editing.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Derivation of Greeks for the price of European call option price under the SABR model

Derivation of Greeks for the price of European call option price under the SABR model

Here, we discuss how to derive the above Greeks for the pricing formula (19) of the European call option under the SABR model to calculate counterparty risk indicators such as PFE, EPE, and Mratio.

First we notice

Then the first-order partial derivatives, “Delta” \(\left( \dfrac{\partial V}{\partial x} \right)\), “Vega” \(\left( \dfrac{\partial V}{\partial \sigma } \right)\) and “Theta” \(\left( \dfrac{\partial V}{\partial t} \right)\), can be obtained as follows.

Before discussing the second-order partial derivatives, note that

Thus the second-order partial derivatives “Gamma” \(\left( \dfrac{\partial ^{2} V}{\partial x^{2}} \right)\), “Volga” \(\left( \dfrac{\partial ^{2} V}{\partial x \partial \sigma } \right)\), and “Vanna” \(\left( \dfrac{\partial ^{2} V}{\partial \sigma ^{2}} \right)\), are also obtained as follows.

Rights and permissions

This article is published under an open access license. Please check the 'Copyright Information' section either on this page or in the PDF for details of this license and what re-use is permitted. If your intended use exceeds what is permitted by the license or if you are unable to locate the licence and re-use information, please contact the Rights and Permissions team.

About this article

Cite this article

Kitani, R., Nakagawa, H. Discrepancy between regulations and practice in initial margin calculation. Japan J. Indust. Appl. Math. (2024). https://doi.org/10.1007/s13160-024-00660-8

Received:

Revised:

Accepted:

Published:

DOI: https://doi.org/10.1007/s13160-024-00660-8