Abstract

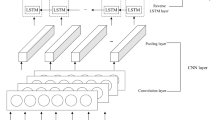

Due to many factors and noise involved in stock market, predicting stock prices is a challenging task. Existing approaches for stock price prediction use only a subset of features and factors that are effective in stock market. In this paper, we present a stock prediction model, which takes into account a diverse and comprehensive set of factors and elements that affect stock market. We accordingly present a comprehensive input model, as a generalization and improvement of existing input models, and feed it into a learning model to predict stock prices. Our learning model is a neural network, consisting of 4 hidden LSTM layers. We evaluate our proposed stock price prediction model over eight real-world datasets, and show its high performance and accuracy.

Similar content being viewed by others

Notes

In our experiments, the exchange rate of Iranian rial with the US dollar is used, as our studied companies are in Iran.

We call it comprehensive because it takes into account a diverse and comprehensive set of features and factors. We call it deep because it exploits a deep neural network for prediction.

References

Abu-Mostafa YS, Atiya AF (1996) Introduction to financial forecasting. Appl Intell 6(3):205–213. https://doi.org/10.1007/BF00126626

Akita R, Yoshihara A, Matsubara T et al (2016) Deep learning for stock prediction using numerical and textual information. In: 15th IEEE/ACIS International Conference on Computer and Information Science, ICIS 2016, Okayama, Japan, June 26-29, 2016. IEEE Computer Society, pp 1–6, https://doi.org/10.1109/ICIS.2016.7550882,

Chehreghani MH (2022) Half a decade of graph convolutional networks. Nat Mach Intell 4(3):192–193. https://doi.org/10.1038/s42256-022-00466-8

Chou J, Nguyen T (2018) Forward forecast of stock price using sliding-window metaheuristic-optimized machine-learning regression. IEEE Trans Ind Inf 14(7):3132–3142. https://doi.org/10.1109/TII.2018.2794389

Coronado S, Jimenez-Rodriguez R, Rojas O (2018) An empirical analysis of the relationships between crude oil, gold and stock markets. Energy J 39:193–208. https://www.jstor.org/stable/26606269

Gao T, Chai Y (2018) Improving stock closing price prediction using recurrent neural network and technical indicators. Neural Comput 30(10). https://doi.org/10.1162/neco_a_01124,

Glorot X, Bengio Y (2010) Understanding the difficulty of training deep feedforward neural networks. In: Teh YW, Titterington DM (eds) Proceedings of the Thirteenth International Conference on Artificial Intelligence and Statistics, AISTATS 2010, Chia Laguna Resort, Sardinia, Italy, May 13-15, 2010, JMLR Proceedings, vol 9. JMLR.org, pp 249–256, http://proceedings.mlr.press/v9/glorot10a.html

Gokmenoglu K, Eren BM, Hesami S (2021) Exchange rates and stock markets in emerging economies: new evidence using the quantile-on-quantile approach. Quant Financ Econ 5(1):94–110

Gokmenoglu KK, Fazlollahi N (2015) The interactions among gold, oil, and stock market: Evidence from s &p500. Procedia Economics and Finance 25(C):478–488. https://doi.org/10.1016/S2212-5671(15)00760-1

Gwilym O, Clare A, Seaton J et al (2011) Gold stocks, the gold price and market timing. J Deriv Hedge Funds 17. https://doi.org/10.1057/jdhf.2011.16

Heaton JB, Polson NG, Witte JH (2017) Deep learning for finance: deep portfolios. Appl Stochas Models Bus Ind 33(1):3–12. https://doi.org/10.1002/asmb.2209

Hegazy O, Soliman OS, Salam MA (2014) A machine learning model for stock market prediction. 1402.7351

Huang C, Yang D, Chuang Y (2008) Application of wrapper approach and composite classifier to the stock trend prediction. Expert Syst Appl 34(4):2870–2878. https://doi.org/10.1016/j.eswa.2007.05.035

Huang W, Nakamori Y, Wang S (2005) Forecasting stock market movement direction with support vector machine. Comput Oper Res 32:2513–2522. https://doi.org/10.1016/j.cor.2004.03.016

Ji X, Wang J, Yan Z (2021) A stock price prediction method based on deep learning technology. Int J Crowd Sci 5:1

Jiang W (2020) Applications of deep learning in stock market prediction: recent progress. CoRR abs/2003.01859. arXiv:2003.01859

Kim R, So CH, Jeong M, et al (2019) Hats: A hierarchical graph attention network for stock movement prediction. arXiv:1908.07999. https://doi.org/10.48550/ARXIV.1908.07999

Kingma DP, Ba J (2015) Adam: A method for stochastic optimization. In: Bengio Y, LeCun Y (eds) 3rd International Conference on Learning Representations, ICLR 2015, San Diego, CA, USA, May 7-9, 2015, Conference Track Proceedings, http://arxiv.org/abs/1412.6980

Lee SW, Kim HY (2020) Stock market forecasting with super-high dimensional time-series data using convlstm, trend sampling, and specialized data augmentation. Expert Syst Appl 161:113704. https://doi.org/10.1016/j.eswa.2020.113704

Lin H, Chen C, Huang G et al (2021) Stock price prediction using generative adversarial networks. J Comput Sci 17(3):188–196. https://doi.org/10.3844/jcssp.2021.188.196

Lin Y, Guo H, Hu J (2013) An svm-based approach for stock market trend prediction. In: The 2013 International Joint Conference on Neural Networks, IJCNN 2013, Dallas, TX, USA, August 4–9, 2013. IEEE, pp 1–7. https://doi.org/10.1109/IJCNN.2013.6706743

Liu J, Wan Y, Qu S et al (2023) Dynamic correlation between the Chinese and the us financial markets: From global financial crisis to covid-19 pandemic. Axioms 12(1):1–14

Marchesi M, Lux T (1999) Scaling and criticality in a stochastic multi-agent model of a financial market. Nat (Lond) 397(6719):498–500

Mikolov T, Chen K, Corrado G, et al (2013a) Efficient estimation of word representations in vector space. In: Bengio Y, LeCun Y (eds) 1st International Conference on Learning Representations, ICLR 2013, Scottsdale, Arizona, USA, May 2-4, 2013, Workshop Track Proceedings arXiv:1301.3781

Mikolov T, Sutskever I, Chen K, et al (2013b) Distributed representations of words and phrases and their compositionality. In: Burges CJC, Bottou L, Ghahramani Z, et al (eds) Advances in Neural Information Processing Systems 26: 27th Annual Conference on Neural Information Processing Systems 2013. Proceedings of a meeting held December 5–8, 2013, Lake Tahoe, Nevada, United States, pp 3111–3119, https://proceedings.neurips.cc/paper/2013/hash/9aa42b31882ec039965f3c4923ce901b-Abstract.html

Pearson K (1901) LIII. On lines and planes of closest fit to systems of points in space. https://doi.org/10.1080/14786440109462720

Preis T, Kenett DY, Stanley HE et al (2012) Quantifying the behavior of stock correlations under market stress. Sci Rep 2(1):752–752

Senol D, Ozturan M (2008) Stock price direction prediction using artificial neural network approach: the case of turkey. J Artif Intell 1(2):70–77

Sharaf M, Hemdan EE, El-Sayed A et al (2021) Stockpred: a framework for stock price prediction. Multim Tools Appl 80(12):17923–17954. https://doi.org/10.1007/s11042-021-10579-8

Suriani S, Kumar MD, Jamil F et al (2015) Impact of exchange rate on stock market. Int J Econ Financ Issues 5:385–388

Thormann ML, Farchmin J, Weisser C, et al (2021) Stock price predictions with lstm neural networks and twitter sentiment. Stat Optim Inf Comput 9(2):268–287. https://doi.org/10.19139/soic-2310-5070-1202, http://www.iapress.org/index.php/soic/article/view/1202

Velickovic P, Cucurull G, Casanova A et al (2018) Graph attention networks. In: 6th International Conference on Learning Representations, ICLR 2018, Vancouver, BC, Canada, April 30–May 3, 2018, Conference Track Proceedings https://openreview.net/forum?id=rJXMpikCZ

Vijh M, Chandola D, Tikkiwal VA, et al (2020) Stock closing price prediction using machine learning techniques. Procedia Comput Sci 167:599–606. https://doi.org/10.1016/j.procs.2020.03.326, https://www.sciencedirect.com/science/article/pii/S1877050920307924, international Conference on Computational Intelligence and Data Science

Wong HT (2022) The impact of real exchange rates on real stock prices. J Econ Financ Admin Sci 27(54):1–15

Zhong X, Enke D (2019) Predicting the daily return direction of the stock market using hybrid machine learning algorithms. Financ Innovat 5(24)

Funding

Not applicable.

Author information

Authors and Affiliations

Contributions

MSM: developed ideas, collected data, implemented algorithms, ran experiments, wrote paper. MHC: developed ideas, wrote paper, supervised work.

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no competing interests as defined by Springer, or other interests that might be perceived to influence the results and/or discussion reported in this paper.

Ethical approval

Not applicable.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Salemi Mottaghi, M., Haghir Chehreghani, M. A deep comprehensive model for stock price prediction. J Ambient Intell Human Comput 14, 11385–11395 (2023). https://doi.org/10.1007/s12652-023-04653-2

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12652-023-04653-2