Abstract

This paper examines the relative importance of key variables for the prediction of international sugar prices. Understanding movements in world sugar prices helps policy-makers and participants in the sugar value chain to formulate effective investment strategies and forecast the effects of market shocks more accurately. We combine a Bayesian model averaging (BMA) technique to address specification uncertainty with an out-of-sample analysis to evaluate price predictability. Results show that world sugar quotations are mostly influenced by their own dynamics, changes in international staple food prices, sugar production costs, and macroeconomic variables. The predictability of the BMA is found to be generally high, compared with a sample of benchmark time series approaches.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

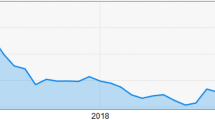

International sugar prices are commonly recognized for being highly volatile (FAO 2016). This volatility stems from the economic and physical characteristics of the sugar market. On the supply side, sugar production is inelastic as a result of the perennial nature of sugarcane, the dominant sugar crop (Elobeid and Beghin 2006; Gemraill 1978; Hammig et al. 1982). Sugarcane represents 80% of the world sugar output compared to 20% from sugar beet. This means that a price decline is not likely to trigger a large supply response, at least in the short run. Likewise, sugar demand is relatively irresponsive to price changes in the short run. The net effect of inelastic supply and demand is the dominance of relatively volatile sugar pricesFootnote 1 (FAO 2004) (Fig. 1).

Monthly international sugar prices

The volatile nature of the sugar market is further exacerbated by the effects of various support measures that benefit the subsector (Mensbrugghe and Mitchell 2003). Sugar is known for being one of the most protected commodities, as governments seek to safeguard producers from low prices through the implementation of various policy instruments such as border measures, minimum price level, and subsidies (FAO 2016). For years, however, there have been calls to reduce, or eliminate, the level of these interventions, particularly those that are market distortive. Dispute cases over sugar subsidies were brought before the World Trade Organization (WTO) in several instances (Burrell et al. 2014; WTO 2019). A number of major sugar producers, noticeably the European Union (EU), have introduced important legislative changes to their domestic sugar market, with the objective of reducing the level of public support (OECD/FAO 2017).

The literature on modeling international sugar markets and projecting their prices tends to use structural specifications, such as general equilibrium models (e.g., Mensbrugghe and Mitchell 2003) or partial equilibrium models (e.g., OECD/FAO 2017; Adenäuer and Witzke 2004; Nolte et al. 2010). These are generally recursive models that provide yearly market equilibriums for production, consumption, trade, and world sugar prices over a projection period. The strength of these trade models is their ability to incorporate a wide range of policy variables and thus measure the effect of specific policies on international sugar market. The other approach to sugar price analysis relies on time series techniques as in Stephen (2013, 2015), Chang et al. (2018), RaboBank (2018), World Bank (2018), and Rumánková et al. (2019). With time series, policy simulation possibilities are relatively narrow, but the technique allows the use of data at a much higher frequency level (e.g., daily) than partial or general equilibrium models, enabling to take advantage of more information. Often the case, a lot of the sugar prediction work, particularly short-term forecasts, is available from the private sector (e.g., investment banks) and is, therefore, not freely accessible to the general public.

In this paper, we identify key drivers of international sugar market and examine their relative importance for short-term predictions of world sugar prices. We use a Bayesian model averaging (BMA) approach to address model uncertainty stemming from many possible combinations between explanatory variables, followed by an out-of-sample prediction analysis to assess price predictability. Since its development by Leamer (1978), the BMA method has been used extensively in statistics and econometrics.

The use of BMA covers a wide range of topics, including economic development (Koop and Potter 2003), cross-country growth comparison (Fernández et al. 2001a; Sala-I-Martin et al. 2004; Man 2015), inflation rate forecasting (Wright 2009), portfolio analysis (Cremers 2002; Maltritz and Molchanov 2013), and energy forecasting (Zhang and Yang 2015; Drachal 2016). In a recent study using BMA, Arin and Braunfels (2018) examine the impact of oil rents on economic growth in the medium and long run using panel data and 54 growth determinants. They found no evidence of resource curse but, instead, some positive effects of oil rent on growth in the long run. Likewise, Zhang and Yang (2015) study natural gas consumption in China using BMA and found that it has a better prediction ability than alternative models, including gray prediction model and artificial neural networks. Application of BMA to agricultural commodity markets remains limited. One study by Crespo and Obersteine (2016) combines BMA and key explanatory variables to decompose price movements of coffee, wheat, and soybeans. Their results show that macroeconomic indicators and market fundamentals explain most of the price changes, while financial developments play a much weaker role.

The use of BMA is quite prolific in the study of economic development. For example, Eris and Ulasan (2013) investigate the relationship between trade openness and economic growth utilizing a BMA approach and conclude that economic institutions and macroeconomics uncertainty contribute to economic growth more so than trade openness. Other studies using BMA include Man (2015), Horvath (2011), Ley and Steel (2009), Eicher et al. (2011), and Ley and Steel (2012).

Our analysis contributes to the existing studies in several aspects. First, a lot of the work on short-term sugar price forecasts is not freely accessible to the general public. We contribute to filling this gap by characterizing the drivers of international sugar prices, measuring their relative importance, and providing a framework for short-term forecasts that can be used by policy-makers. Second, the analysis covers the period from 1990 to 2016, which allows taking into consideration the effect of the last decade surge in food prices in 2007/2008 and 2011, as well as the implication of the global financial crisis of 2007/2008. We also take into account the period of end-1990 and beginning 2000 when several agricultural commodity prices recorded historical lows in real terms (e.g., sugar). Third, we combine a BMA method to address specification uncertainty with an out-of-sample analysis to evaluate price predictability against a sample of time series models.

The remainder of the paper is structured as follows: The next section discusses the main drivers of international sugar prices, followed by a review of the methodology and data employed in the empirical section. We then outline and discuss the main results. The final section gives a summary of the main conclusions and some suggestions for future research.

The Determinants of Sugar Price Dynamics

World Sugar Production Surplus/Deficit and Stock-to-Use Ratio

World sugar production has been for most of the last decades in excess of global sugar consumption. For example, there were five consecutive production surpluses between 2010/2011 and 2014/2015, resulting in large stock buildups and a downward pressure on sugar prices. Production surpluses were quite sizeable in 2012/2013, 2013/2014, and 2017/2018 with production exceeding consumption by 8.2 million tons, 8.8 million tons, and 7.2 million tons, respectively (ISO 2018). Another related driver of sugar prices is the stock-to-use ratio. Often, it is the interaction between the world production surplus/deficit and the level of the stock-to-use ratio that determines the extent of a price movement (Elobeid and Beghin 2006).

Sugar Cost of Production in Brazil

The global sugar market is dominated by Brazil, the world’s largest sugar producer and exporter. Between 2010 and 2014, Brazil accounted for 26% of world sugar production, up from 16.3% in 2000–2004. The expansion in sugar production was driven by a number of factors, including government supports, increasing demand for ethanol-based sugarcane production, and vast and suitable natural resources (OECD/FAO 2017). Also, between 2010 and 2014, Brazil accounted for about 58% of the world’s raw sugar export, while it was responsible for 23% of the world’s total export of refined sugar (FAO 2015). The dominant position of Brazil means that supply shocks in that country have significant impacts on international sugar prices and trade flows. It also implies that world sugar prices tend to follow changes in marginal cost of production in Brazil (Fig. 2) (Stephen 2013).

Source: Authors’ calculations and FAO

World sugar prices versus Brazil sugar cost of production (2000 = 1)

Energy Prices

Sugarcane and sugar beet can also be used as feedstocks for the production of ethanol. However, it is in Brazil where the interaction between sugar and ethanol is most evident with both products competing for sugarcane (Fig. 3). The higher the sugar–ethanol price ratio, the larger the share of sugarcane going into sugar. Sugar mills in Brazil generally have the infrastructure to switch between both products depending on the relative price returns. Given the dominant position of Brazil in the world sugar market, the relative profitability of sugar vs ethanol has a direct effect on Brazil’s sugar export availability and consequently on international sugar prices (Stephen 2015). Given that ethanol competes with gasoline in the fuel transportation subsector, changes in the ratio of gasoline to ethanol, on an equivalent energy content, determine demand for ethanol and consequently the demand for sugarcane. However, the relationship between ethanol and gasoline prices is not linear because of tax policies and various subsidy programs that support the Brazilian biofuel subsector.

Source: Authors’ calculations

International sugar prices versus domestic ethanol prices in Brazil, in raw sugar equivalent

Macroeconomic and Financial Factors

The main macroeconomic variables that have an influence on the sugar market are population growth and per capita GDP growth, with their effects running through various channels (Mitchell 2004; Carman 1982; ISO 2010). Their impact is particularly visible through changes on the demand side of the market. In the case of GDP, during recession periods, for example, demand for beverages and food manufacturing tends to fall, exerting downward pressure on sugar quotations. This is because the bulk of demand for sugar stems from the beverages and food manufacturing sectors, with both sectors highly influenced by the overall economic performance (ISO 2016). The influence of population growth is mostly important in developing countries, as increases in population continue to remain relatively important. On the supply side, changes in GDP, labor market, and inflation rates affect investment decisions at the farm and sugar processing level.

Another set of variables driving international sugar prices relates to financial markets. Most important is the movement in the value of the Brazilian currency (Real) with respect to the value of the US Dollar (USD) (Stephen 2013). A depreciation of the Real against the US dollar tends to lower dollar-denominated sugar production costs in Brazil, which boosts sugar exports and affects world sugar prices, ceteris paribus. Also, because world sugar prices are denominated in US dollar, a depreciation of the Real incentivizes sugar exporters in Brazil to ship greater volumes in order to lock in higher return in local currency.

Empirical Approach

Bayesian Model Averaging

Given the large number of variables that can potentially explain changes in sugar prices, the question becomes which variables should then be included in a model. Making inferences by selecting one particular model specification over a number of possible alternatives can lead to biased estimates, as discussed in Eicher et al. (2011). Also including many variables in a model can result in losing degrees of freedom, particularly when the number of observations is limited. One alternative to address specification uncertainty is to estimate a model for each possible variable combination and to use these models as weights for any statistics. This is in essence what the BMA approach does. The weights are the posterior model probabilities associated with each of the model specifications, assuming that among all the possible specifications, there is one true model (Chua et al. 2013). Specifically, assume there are n possible models, \(M_{1} , \ldots M_{n}\)., that depict the behavior of international sugar prices, with the ith model indexed by a vector of parameters \(\theta_{i}\); the BMA posterior distribution of any statistic \(\Delta\) can be expressed as

while the posterior model probability that model i is the true model can be elaborated following Wright (2009) as

where D represents data, \(P\left( {M_{i} } \right)\), the prior for model i, \(P\left( {D |M_{i} } \right)\), the marginal likelihood, or integrated likelihood, for model i. Because the denominator of the equation is constant over all models, PMP becomes proportional to the marginal likelihood times the model prior. The marginal likelihood can be described as

where \(P(D|\theta_{i} ,M_{i} )\) is the joint likelihood of model \(M_{i}\) and its parameters \(\theta_{i}\) and \(P\left( {\theta_{i} |M_{i} } \right)\) are the prior density of the parameter vector associated with model \(M_{i}\). A typically used point estimate of a model coefficient is an average of the coefficient posterior means across alternative model specifications weighted by the posterior model probabilities. Generally, PMPs are not tractable in closed form and therefore need to be approximated. One popular application is to use sampling techniques, such as the Markov chain Monte Carlo (MCMC), to simulate random draws from the probability distributions (Baldwin and Larson 2017). We assume that various models describing world sugar prices follow a linear regression. Following Wright (2009), the ith model can be described as

where \(y\) is a vector representing observations of international sugar prices, \(\alpha_{i}\) is the constant vector, \(\varvec{X}_{\varvec{i}}\) stands for the matrix of explanatory variables, \(\beta_{i}\) is the parameter vector, and \(\varepsilon_{t}\) represents a vector of normally distributed random shocks, assuming that shocks are i.i.d with mean 0 and variance \(\sigma^{2}\). As it is done in similar studies, we assume improper priors for the constant and the error variance, that is, \(P\left( {\alpha_{i} } \right) \propto 1\) and \(P\left( \sigma \right) \propto \sigma^{ - 1}\). The key prior is on the regression coefficients \(\beta_{i}\). We derive the priors based on Zellner’s \(g\) (Zellner 1971), so that the priors are assumed to be normally distributed with mean zero and a variance structure expressed as \((g\sigma^{2} \left( {X_{l}^{'} X_{l} )^{ - 1} } \right)\). This structure implies that the variance of the coefficients depends on the variance–covariance emanating from the data. The hyperparameter g captures how confident the research is about the value assumed for the prior mean. The larger the value of g, the less certain the researcher is about the assumed prior. This prior framework results in a posterior distribution for the coefficients that follows a t-distribution, with an expected value equal to \(\left( {g/\left( {g + 1} \right)} \right) \beta_{i}^{ols}\), with \(\beta_{i}^{ols}\) representing the OLS estimate of \(\beta_{i}\). Note that as \(g\) tends to infinity, the coefficient estimator approaches OLS estimator. The use of a \(g\)-prior structure of \(\beta_{i}\) leads to an analytically tractable marginal likelihood \(P\left( {D |M_{i} } \right)\) that is linked to R-squared and includes a size penalty parameter associated with model size \(k_{i}\), as illustrated in Zeugner and Feldkircher (2015):

Given the often large number of explanatory variables involved in the BMA analysis, elicitation of posterior distributions becomes a tedious exercise. To reduce the computational efforts, MCMC samplers are often used to approximate posterior distributions as closely as possible. Often, the technique relies on the Metropolis–Hastings algorithm (Tierney 1994; Chib and Greenberg 1995). The algorithm requires a decision to be made on whether to accept or reject a certain drawn model proposal. In the end, the number of times a proposal is selected will converge to the posterior model probability \(P\left( {M_{i} |D} \right)\).

A key decision that has a critical importance on the posterior distributions is the value of the hyperparameter \(g\). The standard literature often assumes unit information prior (UIP), that is, \(g\) = N for all models, literally assigning to the prior the same information that is available in one observation (Zeugner and Feldkircher 2015). Another possibility is to assign a large value to reduce the effect of the prior on the posterior distribution. Fernández et al. (2001b) recommend the use of a large \(g\)-prior, while others recommend intermediate values (Eicher et al. 2011). Another popular alternative is the use of model-specific g-priors, which can be implemented via several approaches. For example, the empirical Bayes \(g\)-local (EBL) involves using the information contained in the data and assigning \(g\) priors to specific models, while the hyper-g-prior (Hyper) assigns a beta prior to the hyperparameter \(g\) (Ley and Steel 2009).

With respect to model priors, the standard procedure is to assume a uniform prior across models, implying that the researcher believes that each of the models is likely to be the true model. Other popular model prior specifications include the binomial prior and the beta-binomial prior. The latter results in a distribution that is less tight around the prior expected model size (Ley and Steel 2009).

Data and Model Selection

From the discussion on the determinants of sugar prices, a total of 18 potential explanatory variables are selected. These can be grouped into three broad categories: (1) fundamental variables (e.g., world sugar stock-to-use ratio, world sugar production), (2) economic variables (e.g., sugar cost of production, index of manufacture production in the USA), and (3) financial variables (e.g., Brazil exchange rate, trade-weighted US dollar index). The impact of some of these variables may take some time to reach the producers; however, the effects on sugar futures prices can be immediate as market participants adjust their price expectations. Table 1 shows a description of the variable series. The data are monthly series spanning from January 1990 to December 2016, with a pseudo-out-of-sample period running from January 2017 to December 2017.

Considering the number of regressors included in this study, a total of 262144 models (that is \(2^{18}\)) are evaluated by the BMA approach. An MCMC method with the Metropolis–Hastings algorithm is implemented to approximate posterior model distributions in view of the relatively large number of predictors. The pseudo-out-of-sample prediction is used to assess the performance of the BMA against alternative methods. We also use sensitivity analysis on key parameters of the BMA to evaluate its predictive power. We use the R package BMS (Zeugner and Feldkircher 2015) to implement and estimate the BMA models, supplemented by our own R scripts for simulation analysis and forecasting.

Results

BMA Estimation

Table 2 shows the outcome of the BMA analysis resulting from assuming uniform model priors and the hyperparameter \(g\) set to UIP, which we subsequently refer to as the baseline BMA model. The first column shows various explanatory variables ranked by their relative importance. The ranking is based on the posterior inclusion probability (PIP) shown in the second column. The PIP is the sum of PMPs for each model where the explanatory variable is present. The higher the value, the more weight a variable carries in explaining movements in sugar prices. The first five predictors with the largest PIPs are: world sugar prices lagged 1 year, the food price index, Brazil sugar cost of production, Brazil exchange rate, and world sugar production lagged 1 year. Results also show that the posterior model mass is mostly concentrated around models that include the lagged sugar price as a variable. With a PIP of 100%, the lagged sugar price variable is included in all possible combinations of models, highlighting the importance of dynamics in sugar price movements. Likewise, the world food price index has a PIP of 82%, a result in line with previous research, which singles out the influence of staple food prices on cash crop prices, and sugar in particular (see Amrouk et al. 2019). The third column of the table shows the resulting posterior means, while the fourth column lists the posterior standard deviations. Finally, the last column represents the sign certainty statistics and illustrates how likely it is for the posterior mean of an explanatory variable to be positive.

Overall, the posterior means of the parameters have the expected signs. In particular, parameters on the lagged sugar prices, the world food price index, and Brazil sugar cost of production all have positive signs. An increase in the value of sugar in the previous period is positively associated with a rise in sugar quotation in the current period, a result that tends to illustrate the dynamics typically characterizing commodity markets. Likewise, the estimated parameter that captures the effect of Brazil sugar cost of production is found positive. As previously discussed, because Brazil is the world’s largest sugar exporter, world sugar prices are influenced by changes in the marginal cost of sugar production in Brazil. An increase in marginal cost will shift the cost curves upward and drive world sugar values higher. The impact of an increase in marginal cost on sugar futures prices can be instantaneous through changes in price expectations.

Similarly, the positive sign of the coefficient capturing the food price index illustrates the relationship between overall price movements in food and sugar markets. A general rise in staple food world prices tends to be associated with an increase in sugar quotations. This co-movement may reflect common macroeconomic, financial, and fundamental factors at play, but could also illustrate the financialization of commodity markets in general, and cash crops and staple foods in particular (Basak and Pavlova 2016; Grosche and Heckelei 2016). As expected, the estimated coefficient associated with the Real/USD exchange is negative, meaning that a depreciation of the currency against the US Dollar lowers international sugar prices. The PIP for the world ethanol prices is estimated at 9.5%, with relatively smaller posterior mean. Likewise, world oil prices and the variable capturing net sugar exports for India, the world’s second largest sugar producers, have PIPs estimated at 9.2 and 9.1%, respectively. Their relatively weak influence is due to smaller marginal likelihood values, as their inclusion does not have as much effect on sugar prices over the sample period.

Predictive Performance of the Estimated BMA

In addition to using the BMA approach to conduct inferences on the parameters, the method can also be used for forecasting purposes. We should note that a model that performs well in explaining the data may not necessary do well in forecasting. This is because inferences on parameters require certain assumptions that may not be met in a model used for predictions. In our case, the focus is on the forecasting capacity of the BMA.

The ability of the BMA to produce good predictive performances can be evaluated by looking at out-of-sample forecasts. In this section, we look at the performance of the estimated BMA model by considering pseudo-out-of-sample forecasting of international sugar quotations and compare the results with a selection of benchmark forecasting models. Root square prediction errors (RSPEs) and root mean square prediction errors (RMSPEs) are then used as loss measures to assess the performance of the BMA model. The root square prediction errors measure the difference between predictions and actual observations, thus informing about how well a model is performing.

Alternative forecasts based on a selection of benchmark models are also developed and their respective loss measures computed and compared with those obtained with the BMA. The selected benchmark models include: (1) vector autoregression (VAR) process, (2) autoregressive (AR) process, (3) random walk (RW), (4) ordinary least squares (OLS), (5) FAO-OECD price forecasts made in 2016 for the year 2017 based on Aglink-COSIMO model, (6) Food and Agricultural Policy Research Institute (FAPRI) price forecasts made in 2016 for the year 2017, and (7) the World Bank price forecasts made in 2016 for the year 2017. We consider ARIMA-based auxiliary equations to construct the iterated multistep forecasts for the explanatory variables. For the lag structure of the autoregressive processes, the use of the Akaike information criterion (AIC) and the Bayesian information criterion (BIC) selects AR(1) and VAR(2) as the most appropriate specification.

Table 3 shows the RSPEs at different horizons up to 12 months and for each of the selected models. RMSPE values are also shown in the bottom panel. We refer in the text to the longer horizon, as a period spanning from 6 to 12 months, while a shorter horizon corresponds to a period between 1 and 5 months.

Over the 12-month period, results indicate that, among the time series-based methods, both the BMA and the AR(1) approaches have the lowest root mean square prediction error, followed by values for OLS, VAR(2), and RW. In contrast, RMSPEs for the FAO-OECD, FAPRI, and the World Bank approaches are comparatively lower. However, the BMA and the other time series benchmarks do well at shorter horizons than at longer horizons, relative to the forecasts provided by the three institutions (FAO-OECD, FAPRI, and the World Bank). For the time series models, AR(1) and BMA have very comparable performances and have consistently superior predictive power than the RW, OLS, and VAR(2), both at shorter and longer horizons. For instance, using BMA instead of an OLS model enables an average reduction in the RSPE of about 5%. Forecasts produced by FAO-OECD, FAPRI, and the World Bank outperform those generated by the time series approach mostly at longer horizons.

Results derived by the BMA approach can be sensitive to the assumptions on the shrinkage parameter as well as model priors. A large \(g\)-prior value indicates the researcher willingness to accept that the density of the prior is less tight around zero, giving more weights to the information contained in the data. To assess the sensitivity of the results to the value taken by the \(g\)-prior, a series of simulations are carried out. These consist of assigning specific values to the hyperparameter \(g\) and computing the resulting RSPEs and RMSPEs. As can be seen in Fig. 4, when the shrinkage value increases, the predictive performance of the BMA model improves, as RMSPE declines consistently, but only up to a certain point where it starts to rise again. The increase in RMSPEs reflects a stronger size penalty imposed by selecting large \(g\) values (Wright 2009). This is because as \(g\) increases, more weights are given to the likelihood than the prior, and as shown in the methodology, the marginal likelihood contains a size penalty parameter that controls for overfitting. The results show that the lowest RMSPE is obtained by considering a shrinkage value equal to 10, which yields a 2% average reduction in prediction errors over the 12-month pseudo-out-of-sample period, in comparison with the case where \(g\) is assumed to equal the unit information prior. Relative to other forecasting approaches, the BMA performs better than the AR(1), VAR(2), OLS, RW, but does not outperform FAO-OECD, FAPRI, and the World Bank.

Root mean square prediction errors (RMSPEs) for various g-prior values

The BMA corresponding to \(g\) = 10 performs particularly well in the longer horizon, when compared with the results under the assumption that \(g\) follows a unit information prior. Setting the prior for \(g\) equal to EBL and Hyper does not alter significantly the pattern of the overall results. We test for these results using a bootstrapped t-Distribution, where the null hypothesis is that the ratio of RMSPE for the baseline BMA relative to RMSPEs of other methods/assumptions is equal to 1, in favor of the alternative hypothesis that it is less than one. The null is rejected for VAR(2), RW, and OLS, while the test fails to reject the null in the case of the other benchmark models, implying that these models have better predictive power.

One of the key assumptions made for the baseline BMA model is that of uniform model priors. Two simulations are carried out to evaluate the effect of relaxing this assumption. First, it is assumed that model priors follow a binomial distribution, where the prior of a model of specific size is the product of the inclusion and exclusion probabilities assigned to each potential explanatory variable. It is shown that within this framework, selecting a prior expected model size comes down to choosing to put more, or less, emphasis on large models (Ley and Steel 2009). Running the model with \(g\) = UIP and with binomial model prior shows that the calculated RMSPE is below that obtained for the baseline BMA model. Also, the mean number of regressors is now 1.63, in contrast to 3.2 obtained for the baseline model, reflecting the fact that binomial model priors put more emphasis on parsimonious models. Results under the assumption of beta-binomial model priors are also similar to those of the binomial, although the estimated PIPs and the posterior means of the parameters display relatively smaller levels.

Discussion on Various Sensitivity Analyses

Various simulations carried out so far on the effects of the underlying assumptions of the baseline BMA suggest that the predictive power of the BMA model is influenced by the values of the shrinkage parameter and the shape of the model prior distribution. As the shrinkage parameter increases, the forecast performance of the BMA model seems to improve, but only up to a certain level when it starts to worsen. Also, changing the assumptions on model priors does seem to improve the forecasting accuracy of simulated models with respect to the baseline BMA model.

Various simulations involving changing the value of the hyperparameter \(g\) and the assumptions on the model priors did not generally result in the selection of values for the PIPs that are fundamentally different from those generated under the baseline BMA model and reported in Table 3. There are, however, some noticeable cases. First, when model priors are assumed to follow a binomial or a beta-binomial distribution, the PIP of the variable capturing changes in crude oil prices increases and is retained among the top six determinants of sugar price movements. As previously stated, oil prices can influence sugar prices through factor input costs, including transportation cost, and most importantly, through higher demand from the ethanol subsector. Likewise, the variable accounting for the net sugar exports of India, the world’s second largest producer, gains in importance for certain values of the hyperparameter \(g\), but its coefficient remains low, as in the baseline BMA model. We note also that the PIP for the variable capturing the introduction of the 2006 sugar reforms in the EU increases from 6% to 43%, when the hyperparameter \(g\) is set to 1, albeit with a small coefficient value. Recently, the EU has introduced drastic modifications to its legislative sugar policy framework. A key element of the reform is the removal of domestic sugar production quotas and isoglucose production quotas as of the 2017/2018 marketing season. It is still to be seen to what extent these reforms will impact the world sugar prices, but the results of this analysis could serve as an indication of their potential effect. Finally, the covariate capturing changes in HFCS prices gains more importance when \(g\) is set between 1 and 8, although the coefficient remains small. HFCS is particularly important as a sugar substitute in the USA, still its share in the market has been declining in recent years.

One of the advantages of a Bayesian approach to forecasting is that it produces a joint posterior distribution for the predictors. Using the joint posterior distribution of the top six explanatory variables generated by the baseline BMA model, we sample 10,000 possible values from the marginal posterior distribution associated with the parameter of each predictor. These coefficient values, along with forecasted values of the regressors, are combined to yield a time-varying distribution of forecasted sugar prices.Footnote 2 For illustrative purposes, price distributions obtained for the months 3, 5, 7, and 12 of the pseudo-out of sample are shown in Fig. 5, with the forecasted sample mean portrayed with a vertical dashed line. These price distributions can be quite useful, especially for sugar analysts and policy-makers, as they provide probabilistic information about price levels and variations not only for the whole forecasting period but also for specific times within that period.

Time-varying distributions of forecasted world sugar prices

Conclusion

Generating robust projections for sugar prices can support sectoral planning and investment, in addition to providing evidence-based assessment of the nature, level, and duration of market interventions, such as those that involve domestic sugar stock purchases and open market sales. Results of this analysis show that changes in sugar-related market fundamentals, in addition to key financial and macroeconomic factors, influence the most sugar price movements at the global level.

Future research could examine whether improved BMA forecasts can be obtained by considering nonlinear models, in addition to the linear specifications explored in this paper. There is also a need to explore the predictive power of the BMA when the forecasting period is relatively long. One option could be to enhance the BMA with a training ability, by splitting the sample or doing a cross-validation, as it produces forecasts for a certain time horizon. Finally, the BMA offers an alternative approach to the more traditional framework that relies on partial or general equilibrium models for conducting commodity projections, particularly when these models are costly to operate and maintain because of data requirements.

Change history

20 August 2021

A Correction to this paper has been published: https://doi.org/10.1007/s12355-021-01034-x

Notes

The world reference quotation for sugar is the International Sugar Agreement (ISA) Daily Prices, which is based on the first three futures positions of the New York ICE, Contract No. 11.

The forecasts of the predictors are obtained with the assumption that they follow an ARIMA-based process.

References

Adenäuer, M., Louhichi, K., Frahan, B.H.D., and H.P Witzke. 2004. Impact of the “everything but arms” initiative on the EU sugar sub-sector. In International Conference on Policy Modelling, No. 330600001. EcoMod2004, Paris, Vol. 30.

Amrouk, E.M., S.C. Grosche, and T. Heckelei. 2019. Interdependence between cash crop and staple food international prices across periods of varying financial market stress. Applied Economics. https://doi.org/10.1080/00036846.2019.1645281.

Arin, K.P., and E. Braunfels. 2018. The resource curse revisited: A Bayesian model averaging approach. Energy Economics 70: 170–178.

Baldwin, S.A., and M.J. Larson. 2017. An introduction to using Bayesian linear regression with clinical data. Behaviour Research Therapy 98: 58–75.

Basak, S., and A. Pavlova. 2016. A model of financialization of commodities. The Journal of Finance 71 (4): 1511–1556.

Burrell, A., Himics, M., Van Doorslaer, B., Ciaian, P., and S. Shrestha. 2014. EU sugar policy: a sweet transition after 2015? Publications Office of the European Union.

Carman, H.F. 1982. A trend projection of high fructose corn syrup substitution for sugar. American Journal of Agricultural Economics 64: 625–633.

Chang, C.-L., M. McAleer, and Y.-A. Wang. 2018. Modelling volatility spillovers for bio-ethanol, sugarcane and corn spot and futures prices. Renewable and Sustainable Energy Reviews 81: 1002–1018.

Chib, S., and E. Greenberg. 1995. Understanding the metropolis-hastings algorithm. The American Statistician 49 (4): 327–335.

Chua, C.L., S. Suardi, and S. Tsiaplias. 2013. Predicting short-term interest rates using Bayesian model averaging: Evidence from weekly and high frequency data. International Journal of Forecasting 29 (3): 442–455.

Cremers, K.J.M. 2002. Stock return predictability: A Bayesian model selection perspective. Review of Financial Studies 15 (4): 1223–1249.

Crespo, C.J., Hlouskova, J., and M. Obersteine. 2016. Forecasting Commodity Prices: A Comprehensive Approach. SUSFANS Project, mimeo.

Drachal, K. 2016. Forecasting spot oil price in a dynamic model averaging framework: Have the determinants changed over time? Energy Economics 60: 35–46.

Eicher, T.S., C. Papageorgiou, and A.E. Raftery. 2011. Default priors and predictive performance in Bayesian model averaging, with application to growth determinants. Journal of Applied Econometrics 26 (1): 30–55.

Elobeid, A., and J. Beghin. 2006. Multilateral trade and agricultural policy reforms in sugar markets. Journal of Agricultural Economics 57: 23–48.

Eris, M.N., and B. Ulasan. 2013. Trade openness and economic growth: Bayesian model averaging estimate of cross-country growth regressions. Economic Modelling 33: 867–883.

Food and Agriculture Organization (FAO). 2004. Commodity market review 2003–2004. Trade and Markets Division. Rome: FAO.

Food and Agriculture Organization (FAO). 2015. Food Outlook May 2015. Trade and Markets Division. Rome: FAO.

Food and Agriculture Organization (FAO). 2016. Medium-term prospects for RAMHOT products. Trade and Markets Division. Rome: FAO.

Fernández, C., E. Ley, and M.F.J. Steel. 2001a. Model uncertainty in cross-country growth regressions. Journal of applied economics 16 (5): 563–576.

Fernández, C., E. Ley, and M.F.J. Steel. 2001b. Benchmark priors for Bayesian model averaging. Journal of Econometrics 100 (2): 381–427.

Gemraill, G. 1978. Asymmetric cobwebs and the international supply of cane-sugar. Journal of Agricultural Economics 29: 9–21.

Grosche, S.-C., and T. Heckelei. 2016. Directional volatility spillovers between agricultural, crude oil, real estate, and other financial markets. In Food Price Volatility and its Implications for Food Security and Policy, ed. M. Kalkuhl, J. von Braun, and M. Torero, 183–205. Cham: Springer.

Hammig, M.D., R. Conway, H. Shapouri, and J. Yanagida. 1982. The effects of shifts in supply on the world sugar market. Agricultural Economics Research. United States Department of Agriculture, Economic Research Service 34 (1): 1–7.

Horvath, R. 2011. Research and development and growth: A Bayesian model averaging analysis. Economic Modelling 28 (1): 2669–2673.

International Sugar Organization (ISO). 2010. World sugar demand: Outlook to 2020. London: ISO.

International Sugar Organization (ISO). 2016. Industrial and direct sugar consumption: an international survey. London: ISO.

International Sugar Organization (ISO). 2018. World sugar balances, November 2018. London: ISO.

Koop, G. and S. Potter. 2003. Forecasting in large macroeconomic panels using bayesian model averaging. SSRN Scholarly Paper No. ID 892860. Social Science Research Network. Rochester, New York.

Leamer, E.E. 1978. Specification Searches. New York: Wiley.

Ley, E., and M.F.J. Steel. 2009. On the effect of prior assumptions in Bayesian model averaging with applications to growth regression. Journal of Applied Econometrics 24 (4): 651–674.

Ley, E., and M.F.J. Steel. 2012. Mixtures of g-priors for Bayesian model averaging with economic applications. Journal of Econometrics 171 (2): 251–266.

Maltritz, D., and A. Molchanov. 2013. Analyzing determinants of bond yield spreads with Bayesian Model Averaging. Journal of Banking & Finance 37 (12): 5275–5284.

Man, G. 2015. Competition and the growth of nations: International evidence from Bayesian model averaging. Economic Modelling 51: 491–501.

Mensbrugghe, D. van der., Beghin, J.C., and D. Mitchell. 2003. Modeling tariff rate quotas in a global context: The case of sugar markets in OECD countries. No. 03-wp343. Center for Agricultural and Rural Development (CARD) Publications. Iowa State University.

Mitchell, D. 2004. Sugar policies opportunity for change. Policy, Research working paper, WPS 3222. Washington, DC: World Bank.

Nolte, S., Buysse, J., Van der Straeten, B., Claeys, D., Lauwers, L.H., and G. Van Huylenbroeck. 2010. Modelling the effects of an abolition of the EU sugar quota on internal prices, production and imports. No. 61346. 114th Seminar, April 15–16, 2010, Berlin, Germany. European Association of Agricultural Economists

OECD. 2017. OECD-FAO agricultural outlook 2017–2026. Paris: OECD Publishing.

Rabobank. 2018. Sugar quarterly Q2 2018, June 2018. London: RaboResearch.

Rumánková, L., L. Smutka, M. Maitah, and I. Benešová. 2019. The interrelationship between sugar prices at the main world sugar commodities markets. Sugar Tech. https://doi.org/10.1007/s12355-019-00739-4.

Sala-I-Martin, X., G. Doppelhofer, and R.I. Miller. 2004. Determinants of long-term growth: A Bayesian averaging of classical estimates (BACE) approach. American Economic Review 94 (4): 813–835.

Stephen, H. 2013. World raw sugar prices: The influence of Brazilian costs of production and world surplus/deficit measures. Sugar and Sweeteners SSS-M-297-01. United States Department of Agriculture, Economic Research Service, Washington, DC.

Stephen, H. 2015. Projecting world raw sugar prices. Sugar and Sweeteners SSS-M-317-01. United States Department of Agriculture, Economic Research Service, Washington, DC.

Tierney, L. 1994. Markov chains for exploring posterior distributions. The Annals of Statistics 22 (4): 1701–1728.

World Bank. 2018. World Bank commodities price data (The Pink Sheet), September 2018. Washington, DC: World Bank.

Wright, J.H. 2009. Forecasting US inflation by Bayesian model averaging. Journal of Forecasting 28 (2): 131–144.

WTO. 2019. India-measures concerning sugar and sugarcane—request for consultations by Brazil. WTO report number 19-1250. WTO, Geneva.

Zellner, A. 1971. An introduction to Bayesian inference in econometrics. Hoboken: Wiley.

Zeugner, S., and M. Feldkircher. 2015. Bayesian model averaging employing fixed and flexible priors: The BMS package for R. Journal of Statistical Software 68 (4): 1.

Zhang, W., and J. Yang. 2015. Forecasting natural gas consumption in China by Bayesian model averaging. Energy Reports 1: 216–220.

Acknowledgements

This research was partially funded by European Union’s Horizon 2020 Research Project SUSFANS under Grant Agreement No. 633692.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The original online version of this article was revised: The funding note has been updated

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Amrouk, E.M., Heckelei, T. Forecasting International Sugar Prices: A Bayesian Model Average Analysis. Sugar Tech 22, 552–562 (2020). https://doi.org/10.1007/s12355-020-00815-0

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12355-020-00815-0