Abstract

This article argues that maintaining the status quo is not an option for the euro area. The euro has functional and existential weaknesses that force us to take drastic action if we want to become resilient enough to withstand the next banking crisis. The article argues that the existential weaknesses of the euro stem from the D/Y ratio (debt-to-GDP). Euro-area members have only limited scope for using traditional mechanisms to deal with D/Y problems. What makes this especially worrying for the overall stability of the euro area is the ownership of the debt issued by the euro-area member states. It is absolutely vital to separate banks and sovereigns and to slash debt-to-GDP levels. The question is whether the political decision-making processes in the member states can deliver these structural changes.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The future of the Economic and Monetary Union (EMU) is currently a hot topic. The success of the EMU will to a considerable extent determine whether the EU succeeds in fulfilling two of its core promises: prosperity and stability. This article argues that without considerable changes to the EMU, its functional and existential weaknesses will impair the EU’s ability to deliver prosperity and stability. This would ultimately jeopardise the very existence of the EMU. I will start by singling out the most notable functional weakness, which results in the suboptimal functioning of the EMU. The argument is made that while this weakness does not per se endanger the existence of the EMU, it creates severe challenges for certain member states and political friction between its members. Next, I will explain the EMU’s existential weakness, which stems from the D/Y ratio. I will also explain why—unless changes are made to the EMU and to the economies of the member states—the next banking crisis could be fatal. The article concludes by arguing that the euro-area member states must adopt and implement a policy programme (a) to reduce their public debt, so as to cushion the impact of the next crisis, and (b) to separate banks from their sovereigns.

Functional weakness

According to the optimal currency area theory, the euro area suffers from many weaknesses which impair its proper functioning (Mundell 1961). However, we must distinguish between functional and existential weaknesses. The two cannot be completely separated, of course. Still, functional weaknesses constantly hamper the functioning of the EMU, whereas existential weaknesses come to the fore only in crisis situations. Broad academic agreement exists on the euro area’s functional weaknesses, the most important of which is the linkage between the real interest rate and real inflation, a dynamic which boosts upturns and deepens downturns. Other weaknesses, such as low labour mobility and the slow adjustment of prices, are of secondary importance.

The real-interest-rate–real-inflation dynamic was highly evident before the crisis in the euro area erupted. The countries of Southern Europe, also known as the periphery, which had traditionally had higher inflation and interest rates than the core countries, suddenly saw a remarkable drop in both. The low interest rates led to rapid private-sector credit accumulation in countries such as Spain and Ireland. In contrast, the only country with serious public-sector indebtedness prior to the crisis in the euro area was Greece. Low or negative interest rates in the peripheral countries boosted the cycle by discouraging saving and incentivising investments and expenditure, much of which went into real estate and created a bubble in Ireland and Spain. At the same time, however, the exact opposite was happening in the core countries. In Germany, very low inflation encouraged saving, with these savings being channelled by the financial markets to the Southern peripheral countries, which offered higher financial returns (but with low real interest rates for households and companies in those countries) (Storm and Naastepad 2015, 15–20). This dynamic led to a rapid increase in price and wage levels in the peripheral countries. When less developed countries or areas are catching up with more developed ones, it is normal for price and wage levels to increase, due to the Balassa–Samuelson effect.Footnote 1 But in the peripheral countries, a considerable proportion of the price and wage increases was not the result of increased productivity.

It is important to understand that the euro area is not the only monetary union suffering from this dynamic. However, the rigidity of the labour markets in the euro area caused the adjustments to price and wage levels to take longer and be more painful in the aftermath of the euro crisis. In both policy and political terms, the dynamic is difficult to mitigate, especially because it builds up primarily through the private sector. Politically it is challenging, to say the least, to try to slow down credit accumulation in the private sector when the economy is growing and new jobs are being created. This is the very same problem that has always weakened the effectiveness of, and the scope for, Keynesian demand management. At a technical level, countering the problem requires high-quality real-time data and a highly capable administration able to use regulatory and fiscal policy to rein in the real-interest-rate dynamics (Odendahl 2014). Moreover, even with those measures in place, it is difficult to establish whether growth is sustainable. Prior to the crisis, potential output calculations were grossly wide of the mark. For example, Irish potential output prior to the crisis in 2007 was estimated at around -1 percentage point, whereas when it was recalculated in 2014 the output gap proved to be more than +5 percentage points (Anderton et al. 2014).

As requested by the Eurogroup in April 2016, some work on this is being carried out by the European Commission. However, it remains doubtful whether, using the current methodology, potential output can be calculated in real-time accurately enough to base controversial and politically costly fiscal-policy decisions on it. Time lags make it difficult to rein in real interest rates, since slow data collection and analysis mean that policy decisions will always be taken many quarters later. With the further development of economic models and data collection, there is hope that it will become technically easier to counteract the real-interest-rate dynamic. Unfortunately, this does not lessen the political challenge of trying to cool down an economy which is growing too quickly. Moreover, the EMU still has to rely on political decisions instead of letting the economy automatically restabilise itself. Political decisions on highly complex, uncertain and politically costly issues are a major source of political friction among the member states.

Another related problem is that overall labour mobility in the euro area remains low, although new research indicates that it has increased (Ehmer 2017, 2). Mobility is crucial to providing flexibility when asymmetric shocks hit. Optimal currency area theory suggests that symmetry and flexibility are strongly connected: if the economies sharing the same currency are not synchronised in terms of business cycle fluctuations, there must be additional mechanisms in place that offer the flexibility to adjust (Natarajan 2010). In theory, labour mobility is one of the key ‘pressure valves’, yet in the euro area only about 5% of the working-age population (20–64 years old) works in a member state different from the one in which they were born (European People’s Party 2017, 10; Ehmer 2017, 2–3). Political reasons and structural constraints such as language, culture, recognition of qualifications and rigid national social security systems make it difficult to increase labour mobility sufficiently in the short term to have a major impact.

In a monetary union, adjustment of competiveness vis-à-vis other parts of the union requires price adjustment, in which wage adjustment plays an important role (Ehmer 2017, 1–2). We must acknowledge that some very welcome reforms have been introduced during the last five years. In the context of real-interest-rate dynamics, the most important reform in many eurozone countries has been decentralising wage setting and inserting crisis clauses into collective bargaining agreements, so as to introduce more flexibility and thus regain price competitiveness if necessary. The importance of this is highlighted by the Spanish experience, since the rigidity of Spain’s labour markets and wage-setting procedures meant that wages continued to rise until unemployment hit 21.4% (European People’s Party 2017, 10; Villanueva 2015, 2).

The real-interest-rate dynamic is a tangible problem for the EMU because it deepens busts and boosts booms, as well as causing friction among members. Yet it is not an existential weakness. The most potent ways to address and mitigate its effects are through measures to increase labour-market flexibility, encourage equity investments rather than credit investments and remove structural obstacles to labour mobility. Although all three are worthwhile goals, they are difficult to achieve and not without their political drawbacks.

Existential weaknesses of the euro

The most severe threat to the long-term success of the EMU and the euro stems from the interconnectedness in Europe of banks and their sovereigns,Footnote 2 combined with very high D/Y ratios. As argued above, the euro crisis was not caused by public debt. Nevertheless, the high level of public debt arising from the recession and the crisis puts in doubt our ability to handle the next banking crisis. Carmen Reinhart and Kenneth Rogoff have argued that national public-debt crises and banking crises have been a common problem throughout history, and that well-established policy options exist for dealing with them (Reinhart and Rogoff 2009). According to their research, the financial crisis of 2008 was not a unique event in economic history, and we should not assume that it will not happen again.

The interconnectedness of banks and states allows a crisis to spread from the former to the latter, and the other way around. If states had low debt levels, however, this interconnectedness, while still perilous, would not be potentially fatal. That may sound overly dramatic, but if we look at some figures, the alarmism becomes understandable. According to research by Reinhart and Rogoff (2009, 170), when a country experiences a severe banking crisis, its real debt stock increases by about 86% on average. In relation to GDP, moreover, the increases are even higher, because GDP normally falls during banking crises. Naturally, it can be argued that their research is only partially applicable to euro-area countries since these are all advanced economies. However, if we look at the recent financial crisis, a crisis originating in and concerning advanced economies, together with public debt trends in European crisis countries, the figures are sobering. In general the results seem to be very close to Reinhart and Rogoff’s findings.

A country can try to solve its debt issues by reducing the amount of debt (D), or by increasing GDP (Y). To raise its GDP, a country has two main options: implementing structural reforms to increase the growth rate or increasing inflation. To reduce debt, by contrast, a country can repay or restructure debt, make the central bank absorb the debt or try to limit interest costs (Buttiglione et al. 2014, 77–81). Throughout world history, there is scant evidence of countries having grown out of debt (Reinhart and Rogoff 2009, 289). This does not diminish the importance of implementing structural reforms, since boosting growth and job creation, or increasing government efficiency, can hardly be negative outcomes under any circumstances. However, we must recognise that we should not rely solely on structural reforms, which also tend to take time to take effect.

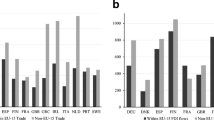

The ownership of sovereign bonds in the EU is a huge obstacle to using any means other than structural changes to lower the D/Y ratio. Sovereign bonds in Europe are largely owned by each country’s own domestic banking sector. There are dramatic differences between countries, but on average the domestic banking sector owns 57% of sovereign bonds. This is considerably higher than the US equivalent of 45%, but what is especially worrying is that in all the big euro-area countries this percentage is above that of the US (European Political Strategy Centre 2015, 2–3). What makes this so concerning is that it limits the options available for countries to deal with their debt levels. For example, forcing losses on creditors through write-downs is not a realistic policy option because it would jeopardise the domestic banking system (Figures 1, 2, 3).

Government-debt-to-GDP ratio, 2007 and 2015, euro crisis countries

Sovereign debt held by domestic banks at the end of 2013 (as a percentage of total government debt)

Exposure of banking system to domestic government debt at the end of 2013 (as a percentage of own funds)

What turns this problem into an existential weakness is the already high debt levels shown in Figure 4, together with the limited scope for lowering debt-to-GDP ratios. If we assume that Reinhart and Rogoff’s research and the experience we have of the recent crisis in the euro area are indicative of the effect the next crisis will have on public debt levels, we can expect the next crisis to raise countries’ debt-to-GDP ratios by more than 50% compared to the pre-crisis level. It remains questionable whether the markets would be willing to fund such an increase in public debt. For example, compared to the current levels, Italy’s debt-to-GDP ratio would be well beyond 200% and France would find its ratio above 150%. Naturally, these are only back-of-the-envelope calculations. However, the dangers associated with the situation should prompt member states to adopt a strategic long-term plan to reduce their debt levels and separate banks from sovereigns, so as to have the room to cushion the next crisis, which is inevitable. The question is whether our democracies are capable of adopting and implementing strategic policy initiatives, which are politically costly and divisive, to create space to cushion the next banking crisis, since this approach will require years of considerable primary surpluses.

Debt-to-GDP ratios in the euro area, 2007 and 2015

Conclusion

This article argues that maintaining the status quo is not an option for the euro area due to functional weaknesses which lead to the suboptimal functioning of the EMU and in turn to political friction among members. Furthermore, far-reaching reforms are needed due to the high D/Y ratios. These result in there being only limited room to cushion the next banking crisis, which, history tells us, is inevitable. If debt-to-GDP ratios are not lowered and banks are not separated from their sovereigns, the next banking crisis may prove to be an existential threat to the EMU. Nevertheless, it is absolutely clear that, rather than dismantling the euro, action should be taken to correct these weaknesses.

Notes

‘Countries with high productivity growth also experience high wage growth, which leads to higher real exchange rates. The Balassa–Samuelson effect suggests that an increase in wages in the tradable goods sector of an emerging economy will also lead to higher wages in the non-tradable (service) sector of the economy. The accompanying increase in inflation makes inflation rates higher in faster-growing economies than it is in slow growing, developed economies.’ (Investopedia n.d.)

‘The sovereign–bank nexus was one of the main amplifying factors of financial distress during the euro area crisis. Banks’ difficulties affected sovereigns directly, through the bailout of troubled intermediaries, and indirectly, through the impact of the disruption of lending on the economy. Sovereigns’ difficulties affected banks’ ratings, funding costs, and balance sheets, while the recession worsened their lending portfolios.’ (Visco 2016)

References

Anderton, R., Aranki, T., Dieppe, A., Elding, C., Haroutunian, S., Jacquinot, P., Jarvis, V., Labhard, V., Rusinova, D., & Szörfi, B. (2014). Potential output from a euro area perspective. European Central Bank Occasional Paper Series no. 156. Frankfurt am Main. https://www.ecb.europa.eu/pub/pdf/scpops/ecbop156.en.pdf?12f64165c5623d34b98b978cbe614ed9. Accessed 1 May 2017.

Buttiglione, L., Lane, P., Reichlin, L., & Reinhart, V. (2014). Deleveraging? What deleveraging? International Center for Monetary and Banking Studies. Geneva Reports on the World Economy. Geneva, Switzerland. http://voxeu.org/system/files/epublication/Geneva16.pdf. Accessed 1 May 2017.

Ehmer, P. (2017). Labour mobility in Europe does little to mitigate economic shocks: National labour markets absorb adjustment pressure. KfW Research no. 156. 18 January. https://www.kfw.de/PDF/Download-Center/Konzernthemen/Research/PDF-Dokumente-Fokus-Volkswirtschaft/Fokus-englische-Dateien/Fokus-2017-EN/Fokus-Nr.-156-January-2017-Labour-mobility-in-Europe_EN.pdf. Accessed 1 May 2017.

European People’s Party. (2017). A safer and more prosperous economic and monetary union. Brussels. http://www.epp.eu/papers/a-safer-and-more-prosperous-economic-and-monetary-union/. Accessed 1 May 2017.

European Political Strategy Centre. (2015). Severing the ‘doom loop’: Further risk reduction in the banking union. Five Presidents’ Report Series 3/2015. https://ec.europa.eu/epsc/sites/epsc/files/5p_note_bankexposure.pdf. Accessed 1 May 2017.

Eurostat. (2017a). General government gross debt (EDP concept), consolidated—annual data. http://ec.europa.eu/eurostat/web/products-datasets/-/tipsgo10. Accessed 30 May 2017.

Eurostat. (2017b). General government gross debt (EDP concept), consolidated—annual data. http://ec.europa.eu/eurostat/web/products-datasets/-/tipsgo10. Accessed 30 May 2017.

Investopedia. (n. d.). Balassa–Samuelson effect. http://www.investopedia.com/terms/b/balassasamuelson-effect.asp. Accessed 1 May 2017.

Mundell, R. (1961). A theory of optimum currency areas. American Economic Review, 51(4), 657–65.

Natarajan, G. (2010). Euroland and optimal currency areas. Urbanomics, 10 May. http://gulzar05.blogspot.com/2010/05/euroland-and-optimal-currency-areas.html. Accessed 1 May 2017.

Odendahl, C. (2014). The eurozone’s real interest rate problem. Centre for European Reform. 8 July. https://www.cer.org.uk/insights/eurozones-real-interest-rate-problem. Accessed 1 May 2017.

Reinhart, C., & Rogoff, K. (2009). This time is different: Eight centuries of financial folly. Princeton, NJ: Princeton University Press.

Storm, S., & Naastepad, C. (2015). Myths, mix-ups and mishandlings: What caused the eurozone crisis? Institute for New Economic Thinking. https://www.ineteconomics.org/uploads/papers/The-Eurozone-Crisis.pdf. Accessed 1 May 2017.

Villanueva, E. (2015). Collective bargaining, wage rigidities and employment: An analysis using microeconomic data. Banco De Espana, Economic Bulletin. April. http://www.bde.es/f/webbde/SES/Secciones/Publicaciones/InformesBoletinesRevistas/BoletinEconomico/15/Abr/Files/be1504-art2e.pdf. Accessed 1 May 2017.

Visco, I. (2016). Banks’ sovereign exposures and the feedback loop between banks and their sovereigns. Concluding remarks, Euro50 Group, The Future of European Government Bonds Markets. https://www.bancaditalia.it/pubblicazioni/interventi-governatore/integov2016/Visco_Euro50_Bank_Sovereign_Exposure_02052016.pdf. Accessed 1 May 2017.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

This article is published under an open access license. Please check the 'Copyright Information' section either on this page or in the PDF for details of this license and what re-use is permitted. If your intended use exceeds what is permitted by the license or if you are unable to locate the licence and re-use information, please contact the Rights and Permissions team.

About this article

Cite this article

Nurvala, JP. The status quo is not an option: functional and existential weaknesses of the EMU. European View 16, 75–84 (2017). https://doi.org/10.1007/s12290-017-0441-y

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12290-017-0441-y