Abstract

This paper aims to assess the effects of money laundering (ML) and corruption on socioeconomic development in Iran as a case study for developing countries. We also investigate the complex interactions among socioeconomic development, ML, corruption, private expenditure, and dependence of the Iranian economy on oil production. The paper uses the partial least squares approach to structural equation modeling (PLS-SEM) to estimate an index of Iranian ML over the period 1997–2017. The results show that in the short run, there is a positive overall effect of ML on economic development. This effect is due to the multiplicative effect of the reinvestment of criminal proceeds in the national economy. We estimate that, in the last decade, a plausible estimate of Iranian ML is approximately 10% of official GDP. From a methodological perspective, this research applies a new calibration approach to convert the latent scores calculated by PLS-SEM into actual values of ML.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Money laundering (ML) is the process of concealing the illicit origin of the proceeds of crimes. The literature considers ML a growing global issue (e.g., Loayza et al. 2019). Regarding its scope, the International Monetary Fund (IMF 2018) estimates that the amount of money laundered annually ranges between 2 and 5 percent of global GDP (i.e., approximately 1.6 to 4 trillion US dollars). According to the United Nations Organization Office on Drugs and Crime (UNODC 2011), ML equaled approximately 2.7% of world GDP in 2009. According to Global Financial Integrity (2019), during the period from 2005 to 2016, potential illicit flows in and out of the developing world represented between 20 and 30 percent of the total trade in developing countries. These figures, despite being a rough approximation of the size of ML, highlight that the knowledge of the size of ML and its multifaceted effects on market competition and development is not only an econometric task but also an important topic for numerous economic issues.

A vast body of literature reviews the economic and noneconomic consequences of ML (e.g., Unger 2007; Unger et al. 2006; Ferwerda 2013; Savona and Riccardi 2017; Romero 2020; Barone et al. 2022; Slama and Gueddari 2022). According to this literature, there are two antagonistic effects of ML on socioeconomic development. On the one hand, ML hinders the economic performance of a country for at least three main complementary reasons. First, because those who invest illicit proceeds mainly aim to launder dirty money rather than to maximize returns, ML generates unfair market competition between laundering-maximizing criminal actors and profit-maximizing legal actors if they compete in the same market. As a consequence, ML activities reduce the market capacity available to realize efficient resource allocation. Second, ML diverts resources from sectors with low capacity to launder dirty money toward sectors with higher turnover or with a larger use of untraceable transactions (e.g., cash). This second source of misallocation reduces marginal profits in cash-intensive sectors because of excess investment. As a consequence, in these sectors, the equilibrium price may be fixed at a level that yields negative marginal profits; “this makes it difficult, if not impossible, for legitimate business to compete against front companies with subsidized funding, a situation that can result in the crowding out of private sector business by criminal organizations” (McDowell and Novis (2001: 7). According to Unger et al. (2006), these detrimental allocative effects for the economy mainly affect international trade and capital investments, particularly in the real estate sector. Walker (1995) estimated for Australia that one million dollars of laundered money decreases output by 1.2 million dollars because criminals spend and invest the money less productively than the victims would. In general, criminal organizations overinvest illegal earnings in sectors that wash dirty money easily (e.g., because they typically use more cash and/or are difficult to detect by AML authorities because they produce intangible goods or services). For that reason, the excess investments in ML-friendly sectors and the presence of business actors that have a primary aim of laundering money instead of maximizing their profit lead to unfair market competition and the crowding of “normal” profit-maximizing firms. Moreover, ML may hinder economic development in several other ways, e.g., it weakens the financial sector due to the entry of illegal money (Kumar 2012), it increases the risk of bankruptcy and financial crises by threatening the financial market (Bartlett 2002), ML is positively correlated with corruption (Ospina-Velasco 2003; Markovska and Adams 2015).

On the other hand, ML may positively affect economic growth, especially in developing economies, because of the reinvestment of laundered illegal funds in the formal economy (e.g., Masciandaro 1999, 2007). This result has been empirically validated by Stancu and Rece (2009) and Slim (2011). Uger et al. (2006: 9) analyze the multiplier effect of ML in the Dutch economy and conclude that “one billion of additional money laundering leads to about 0.1% more growth”. However, they distinguish between short-term effects, where ML seems to be a smart strategy for rich countries to attract additional capital inflows, increased government revenues, employment and growth, and long-run effects. In the long term, “Criminal money is a ticking bomb” (Uger et al. 2006: 7), as it attracts crime. According to their estimates for the Netherlands, one million laundered illegal proceeds are partly reinvested into further illegal activities, this will increase ML of the related crime by 10% to 20% resulting in Є 1.1 to 1.2 million of money laundering. More recently, Romero (2020) analyzes this effect in Mexican local economies. He observes that ML, by increasing investment of dirty money in legal local businesses, leads to short-term improvements in these economies. However, this windfall attracts additional criminal organizations that endogenously increase violence. As a consequence, Romero (2020: 21) concludes that these “gains are more than overshadowed by the subsequent rise in criminal violence”. Launderers' reinvestments in hotels, villas, apartment buildings, shopping malls, luxury stores, and restaurants, despite raising local revenues and expenses and increasing employment, provide benefits for local governments in the short run while, in the long run, ML increases violence. Henry and Moses (2020) investigate the relationship between ML and economic growth in a developing country (i.e., Trinidad and Tobago) by using the volume of fraud and narcotics offenses as proxies for ML. Different from the previous literature, their results are mixed and highlight the relevance of measurement errors in the economic analysis of ML. Specifically, they find that ML influences economic growth in both the short run and long run and that these effects can be both positive and negative depending on the proxy and time span.Footnote 1 Loayza et al. (2019) present an overlapping-generations growth model with both licit and illicit activities. They analyze the effects of ML by calibrating the theoretical model to the Colombian economy and simulating the estimates of the volume of laundered assets. Similar to Henry and Moses (2020), Loayza et al. (2019) find that the effects of asset laundering on savings and social welfare are ambiguous. In particular, if asset laundering comes mainly from drug trafficking, then it has a positive effect on aggregate savings and social welfare in the economy. In contrast, if asset laundering comes from common crimes, the effect is negative. In conclusion, the basic intuition for this hypothesis is that, in the short run, ML acts as a multiplier for employment and production by reinvesting criminal proceeds. Obviously, these studies do not argue that the overall net effect of ML is advantageous for the economy but that, at least in the short run, ML contributes to reducing the negative externalities generated by criminal activities on growth. To prevent misunderstanding, this hypothesis argues that ML acts as a multiplier not only for GDP but also for crime, corruption and terrorism (e.g., Gnutzmann et al. 2010). The increase in these phenomena undermines democratic institutions, and this comes at a significant cost to society in the long run. The main reason for this incongruity between the short- and long-term effects of ML concerns the role of institutions in economic development. According to Acemoglu and Robinson (2010: 1), “the main determinant of differences in prosperity across countries are differences in economic institutions”, but changing “the rules of the game in a society”Footnote 2 is a complex and slow process that requires several years. In contrast, a decline in ML activities has an immediate negative effect on economic growth via the ML multiplier. For instance, Sabir et al. (2019) argue that corruption and inefficient institutions can be considered the most important determinants of ML in developing countries. Specifically, they note that a weak institutional setting is positively correlated with corruption and that the latter is often essential for the success of an ML process. In this scenario, anti-money laundering (AML) policies, by disincentivizing corruption and illicit activities, enhance political and economic institutions and, in the long run, foster socioeconomic development. However, in the meantime, AML policies reduce the reinvestment of criminal proceeds in the formal economy or push these illicit proceeds abroad by decreasing economic growth rates.

The aim of this article is to analyze the relationships among ML, corruption, and socioeconomic performance in a developing country where the first two phenomena are estimated to be particularly widespread. In particular, according to Transparency International Organization (2022), Iran is in the lowest quartile of countries in terms of institutional quality (147th on 180 countries). It is also considered among the highest-risk countries for ML in the world. Indeed, according to the Basel AML Index (2017),Footnote 3 Iran occupies an unenviable first place in this world ranking. For Salehi and Imeny (2019), the geographical position of Iran explains the high presence of laundering activities. Indeed, Iran’s neighbors—the first (Afghanistan) and sixth (Pakistan) largest world opium producers—often use Iran to launder their dirty money yield by smuggling drugs abroad (e.g., to Europe). For these reasons, we consider Iranian ML a meaningful case study for developing countries.

To sum up, this paper contributes to the literature in different ways. From a methodological perspective, this is the first application of PLS-SEM to investigate relationships among ML, corruption and socioeconomic development. From a positive, we find that the direct effect of ML on socioeconomic development is not statistically significant while the indirect and overall effects are positive in our time frame (1997–2017). Accordingly, the normative implication of this research is that, in the short run, AML policies should be accompanied by an increase in public expenditure to offset the detrimental indirect effects that come through the multiplicative effect of a lower reinvestment of illicit earnings in the economy.

2 Empirical analysis

The aim of this section is to summarize the statistical approach (i.e., PLS-SEM) and model specification used to investigate the complex interactions among Iranian socioeconomic development, ML, corruption, private expenditure, and the dependence of the Iranian economy on oil production. We consider the PLS-SEM approachFootnote 4 suitable for the two complementary aims of this research: to predict an index of Iranian ML over the period 1997–2017 and to investigate the interactions among latent constructs that have intrinsic multidimensional content (e.g., socioeconomic development) and constructs that are not directly observable (e.g., ML, corruption). Assuming that twenty years is a short period to account for the effect of ML on Iranian institutions, we consider our results to be descriptive of the short-term consequences of ML activities on socioeconomic development.Footnote 5

2.1 The PLS-SEM specification

Following the literature on ML and the trade-off between data availability and a parsimonious specification, we selected the potential indicators to define the measurement (or outer) reflective models of the key latent variables used in this research—i.e., Money Laundering (ML), Corruption (Corr) and Socioeconomic Development (Socio-Econ_Dev) and outer formative models for latent composite control variables—i.e., private consumption and investment per capita (Priv. Exp_cap) and dependence of Iranian GDP on oil rents (ResDep). Variable definitions and data sources are provided in Appendix 1.

2.1.1 The measurement (or outer) models

We measure the latent construct ML using a formative model, which includes three indicators. Given that ML is intended to disguise criminal proceeds, we assume that this latent variable is affected by the size of those criminal activities that generate the largest illegal proceeds, i.e., drug trafficking, illegal trade, and fencing of stolen property (fencing). Specifically, the first observable variable accounts for the quantity (in kilograms) of drugs discovered per 100,000 people (Drugs) as reported by the Statistical Center of Iran. The second component variable of ML is an indicator of Iranian illegal trade (Illegaltrade) based on Farzanegan (2009) for the period 1997–2002 and the Iranian Combating Goods and Exchange Smuggling Central Staff (2021) for more recent estimates of smuggling on total trade. The third formative indicator accounts for fencing of stolen goods (Fencing) in ML. We assume that this component of ML is proportional to the sum of thefts from places such as government buildings, industrial and commercial centers, and houses and the theft of motor vehicles.

The Corruption latent construct (Corr) is measured by a reflective outer model including four observable proxies for corruption. The Bayesian Corruption Index (BCI) is a composite index of the perceived overall level of corruption proposed by Standaert (2015). It lies between 0 and 100, with an increase in the index corresponding to a rise in the level of corruption. The Structural Corruption Perception Index (Corr_SEM) proposed by Dell’Anno (2020a) ranges between 0 (no perceived corruption) and 100 (highest perceived corruption).Footnote 6 The third and fourth reflective indicators are the Political Corruption (Corr_Pol) and Public sector corruption (PubS_corr) indices proposed by Coppedge et al. (2019) and Pemstein et al. (2019). The first proxy accounts for the perceived pervasiveness of political corruption. The PubS_corr indicator is based on the question “To what extent do public sector employees grant favors in exchange for bribes, kickbacks, or other material inducements, and how often do they steal, embezzle, or misappropriate public funds or other state resources for personal or family use?” The directionality of the latter two corruption indices runs from the least corrupt to the most corrupt.

The third latent construct in the PLS-SEM measures the multidimensional concept of socioeconomic development. The reflective outer model of this latent variable includes seven manifest variables that account for educational, social, technological and economic development. Specifically, we include two variables related to the education system: (1) the Human Capital Index (HCI) extracted from the Quality of Government database (Teorell et al. 2021), which is based on years of schooling, and (2) the ratio between students enrolled in tertiary education and the population over 10 years of age (tertiEDU). To account for social measures of development, we consider (3) the Human Development Index (HDI) extracted by the United Nations Development Program (2020) as an overall proxy for achievements in three dimensions of human development (i.e., health, education and standard of living); and (4) life expectancy at birth in years (Lifexp). To account for technological development and the standard of living of rural households, we use the percentage of the population with access to electricity (Acc_el_r_p). This index is based on electrification data collected from industry, national surveys and international sources provided by the World Development Indicators. To account for economic development, we consider (6) the gross domestic product per capita in real terms (gdp_cap) and (7) the ratio of the female to male labor force participation rate (LB_Fem_M).

The fourth construct accounts for the theoretical hypothesis (e.g., Unger et al. 2006; Masciandaro 2007; Loayza, 2019) that ML may also have positive effects on economic development by increasing private expenditure in an effort to launder dirty money. We empirically test this hypothesis by defining a latent construct (Priv. ExpGDP) that is fixed equal to the (observed) sum of real aggregate private consumption and investment per capita.Footnote 7

The fifth latent construct accounts for oil resource dependence (ResDep), and it is measured by setting it equal to the (manifest) variable “Oil rents as a percentage of GDP” published in the World Development Indicators database. This construct controls for the effect of natural resource dependence on both Iranian socioeconomic development and corruption. According to the resource curse hypothesis, natural resource-abundant countries tend to underperform economically, and one of the prevalent arguments for this detrimental effect is that more resource rents incentivize corruption (Kolstad and Søreide 2009; Arezki and Brückner 2011).Footnote 8 To conclude, to account for the time-series nature of the variables and prevent spurious correlations among constructs, we include a latent variable equal to the time trend (time) in the structural model.

2.1.2 The structural (or inner) model

The structural model is the “core” of the PLS-SEM because it includes the regressions used to empirically test the theoretical hypotheses of this research. Specifically, PLS-SEM Model 1, in analytical terms, comprises five equations:

A relevant advantage of PLS-SEM, with respect to the standard OLS regression approach or factor model, consists of simultaneously estimating both the direct and the indirect effects among latent variables.

(Structural) Equation 1 is intended to test the hypotheses on the direct effects of ML and corruption on socioeconomic development, controlling for the effects of variations in oil rent dependence and private expenditure. Equation 2 provides an econometric test for the hypothesis that ML, by reinjecting illegal resources into the official market, has positive consequences for socioeconomic development. Equations 3 and 4 estimate the partial marginal effects of corruption on ML and resource dependence on corruption.

2.1.2.1 Hypotheses on the relationships among ML, corruption, and socioeconomic development

According to the ambiguous results of the consequences of ML mentioned in the previous section, in this study, we use PLS-SEM to test the effects of ML on socioeconomic development in the short run:

Hp. 1

Higher ML indirectly increases socioeconomic performance because of the multiplier effect of ML (i.e., higher expenditure comes from illegal earnings in the legal economy), ceteris paribus. In symbols, \({\upbeta}_{1} {\upbeta}_{5} > 0\).

Hp. 2

Higher ML has a direct negative effect on socioeconomic performance in the short run (\({\upbeta }_{2} < 0)\) because it reduces allocative efficiency and attracts criminal activities, ceteris paribus.

To control for confounding factors, we include in the inner model a proxy for corruption, which is considered both a source of illegal income to launder and a detrimental factor for socioeconomic development. Specifically, two rationales may support the hypothesis that corruption is positively correlated with ML. On the one hand, wider perceived corruption increases criminals’ expectation of going unpunished, i.e., if discovered, they have the chance to successfully corrupt authorities and prosecutors to not report their illegal activity. On the other hand, corruption and ML expand under weak institutions, e.g., Henry and Moses (2020) state that inadequate rule of law and regulatory enforcement make crime and ML more attractive activities.

A vast body of literature addresses the relationship between corruption and economic development.Footnote 9 Corruption constitutes a deadweight loss for society, and it slows economic development due to reduced tax revenue and regulatory compliance, the deterioration of social capital, the proliferation of rent-seeking activities, and the creation of obstacles to development due to imperfect market competition. Accordingly, we test the following hypotheses:

Hp. 3

Corruption is positively correlated with ML activities, ceteris paribus (\({\upbeta }_{6} > 0)\).

Hp. 4

Corruption is negatively correlated with socioeconomic development, ceteris paribus (\({\upbeta }_{3} < 0\)).

2.1.2.2 Hypotheses on the relationships among resource dependence, corruption, and socioeconomic development

The fifth latent variable in the inner model is oil dependence (ResDep). It allows us to control for the effect of natural resources (i.e., oil rent as a percentage of GDP) in the Iranian economy through two channels that are related to the academic debate on the resource curse hypothesis. Following Dell’Anno (2020b), we can classify both economic (e.g., “Dutch disease”, the inefficiency of the market economy because natural resources tend to be owned by firms with significant degrees of monopoly and monopsony power) and political arguments (e.g., greater opportunities for rent-seeking activities, wars for ownership of natural resources, weaker democracy) to rationalize a negative correlation between resource abundance and economic growth. In our PLS estimation, we test for both channels by estimating path coefficients \(\beta_{4}\) (direct effect) and \(\beta_{7}\). According to the literature, resource dependence is expected to have a direct positive correlation with corruption (e.g., Sachs and Warner 1997; La Porta et al. 1999; Ades and Di Tella, 1999). There is a lack of consensus in the empirical literature on the direct effect of oil rent on socioeconomic development.Footnote 10 Accordingly, we test the following hypotheses:

Hp. 5

Resource dependence is positively correlated with corruption, ceteris paribus (\({\upbeta }_{7} > 0\)).

Hp. 6

Resource dependence may have an ambiguous relationship with socioeconomic performance, ceteris paribus \(\left( {\beta_{4} \frac{ > }{ < }0} \right)\).

Figure 1 shows the path diagram of PLS-SEM Model 1, i.e., the reference model in this research. We also estimate a PLS-SEM where we omit statistically insignificant path coefficients from the previous inner model specifications (i.e., Model 2).

Path diagrams PLS-SEM for money laundering (model 1)

3 Empirical results

This section reports metrics for evaluating the PLS-SEM findings.Footnote 11 Preliminarily, a single goodness-of-fit criterion is not available in PLS-SEM, unlike covariance-based SEM (Hair et al. 2014). That is, we have to assess the goodness-of-fit in each part of the PLS-SEM specification (i.e., the outer and inner models).Footnote 12

Specifically, according to Henseler et al. (2016), if the outer model does not possess the minimum required properties of acceptable reliability and validity, then the inner model estimates become meaningless. Consequently, the first step in evaluating PLS-SEM results involves examining the measurement models with criteria that differ for reflective and formative constructs.

Following Dell’Anno et al. (2020a), to assess the reflective outer models, we test: (a) the reliability of reflective indicator—outer loadings should be larger than 0.708; (b) the internal consistency reliability—Cronbach’s alpha (Cα) and composite reliability (CR) fall between the thresholds 0.70 and 0.95; (c) Convergent validity—the average variance extracted (AVE) of each construct is 0.50 or higher; Discriminant validity—we test if the heterotrait-monotrait (HTMT) ratio is lower than 0.90.

Four tests are suggested to assess the formative outer models (Hair et al. 2019): (1) convergent validity—the correlation of the formatively measured construct with the single-item construct, measuring a similar concept, should be 0.70 or higher;Footnote 13 (2) indicator of collinearity—Variance inflation factor (VIF) values of 5 or above indicate potential collinearity problems; (3) Statistical significance of weights (p-values should be lower than 0.05 and, (4) relevance of indicators with a nonsignificant weight (by checking if the outer loadings are larger than 0.50). Table 1 reports Cα, CR, AVE, HTMT, loadings and p-values of loadings to assess reflective models, and VIF, the statistical significance of weights and, for nonsignificant weights, outer loadings for formative latent variables.

According to the assessment statistics in Table 1, we conclude that with the exclusion of discriminant validity and composite reliability of the “Socioeconomic Development” construct—which is larger than the upper threshold (0.95)—the reflective latent constructs are satisfactorily measured by their outer models. Regarding the formative model of ML, “Drugs” has the highest loadings and contributes to explaining the variation in the Iranian ML relatively more than “Fencing” and “IllegalTrade”.

The second step of assessing a PLS-SEM consists of evaluating the structural model. Following the PLS-SEM literature, we consider the following statistics: (1) the statistical significance of standardized path coefficients, where due to the standardization, a path coefficient larger than 0.70 indicates a relevant direct marginal effect (Table 2); (2) the Collinearity Assessment—VIF values above five are indicative of probable collinearity issues among the constructs (ideal values of VIF are lower than 3); (3) Adjusted coefficient of determination (\(R_{{{\text{adj}}}}^{2}\))—which represents the amount of explained variance of each endogenous construct which should show a value higher than 0.66 to infer a substantial exogenous effect on the endogenous variable; (4) assessment of a model’s predictive power—which consists to apply an algorithm that splits the full dataset into k equally sized subsets of data. The algorithm then predicts each fold (hold-out sample) with the remaining k-1 subsets, which, in combination, become the training sample—Shmueli et al. (2016) propose as a metric for good prediction performance a \(Q_{{{\text{pred}}}}^{2} > 0\); (5) Model comparison by using the Bayesian (or Schwarz) information criterion (BIC) that penalize over-parameterization of models and try to achieve a trade-off between fit and model parsimony. According to this statistic, the model that minimizes the values of the Money Laundering construct should be preferred. Table 2 shows the statistics assessing the structural model.

From a statistical perspective, Models 1 and 2 have convincing goodness of fit statistics. However, according to the Bayesian information criterion, the Model 2 should be preferred.

Regarding the main hypotheses of this research, our findings based on structural Model 2 validate the first hypothesis, i.e., higher ML indirectly increases socioeconomic performance because of the multiplier effect of ML. Specifically, the (standardized) indirect effect of ML on socioeconomic development is equal to β5β1 = 0.117 with a t-statistic = 4.73. In contrast, the second hypothesis (i.e., higher ML has a direct negative effect on socioeconomic performance, at least in the short run) is not validated in Iran (i.e., the path coefficient is not significantly different from zero (Hp. 2 is not validated, i.e., β2 = − 0.003 with a t-statistic = 0.043).

Regarding Hypotheses 3, 4, 5, and 6 Corruption is positively correlated with ML activities (Hp. 3 is validated, i.e., \(\beta_{6} > 0)\), but there is not a direct effect on Socioeconomic development (Hp. 4 is not validated—\(\beta_{3} = 0\)). This implies that Corruption only has an indirect effect on Socio-econ. Dev is equal to \(\beta_{6} \beta_{5} \beta_{1}\)=0.112 (t-statistic = 4.728).

Finally, we find evidence of the resource curse hypothesis (Hp. 6 is validated, i.e., \(\beta_{4} < 0\)) and that the correlation between Oil dependence (Oil rent in Gdp) and Corruption is not statistically significant (Hp. 5 is not validated, i.e., \(\beta_{7} = 0\)).

The last step of this analysis consists of estimating an index of Iranian ML based on the PLS-SEM scores.

Given that the latent variables are estimated with a mean equal to zero and a unit variance, we need (at least) two exogenous values of this variable to calibrate the latent construct. In particular, following Dell’Anno (2023), we estimate the mean (\(\hat{\mu }_{{{\text{ML}}}}^{{}}\)) and standard deviation (\(\hat{\sigma }_{{{\text{ML}}}}^{{}}\)), which minimize the difference between standardized latent scores obtained by PLS-SEM (\(\overset{\lower0.5em\hbox{$\smash{\scriptscriptstyle\frown}$}}{{\text{M} L}}_{t}^{{\text{z - PLS - SEM}}}\)) and exogenous estimates of the ML \(({\text{ML}}_{{t^{*} }}^{{{\text{exog}}}}\)) by applying OLS.Footnote 14

To calibrate the latent scores obtained by PLS-SEM, due to the lack of official estimates, we use two alternative proxies for Iranian ML in Eq. 7.

The first source is based on Iranian President Hassan Rouhani’s claim in his speech to the Iranian Parliament in August 2018. He stated that his government had succeeded in reducing the total value of illicit trade from $22 billion since the beginning of his term (i.e., 2013) to $12.5 billion (Batmanghelidj 2018). Although it is unclear how these numbers were calculated, to the best of our knowledge, these are the only estimates that come from official sources of the size of one of the most important components of Iranian ML, i.e., smuggling of goods and services.

The second exogenous estimate of Iranian ML is based on Arabmazar Yazdi and Khodkari's (2008) estimation of “dirty money” based on the currency demand approach.

Having estimated \(\hat{\mu }_{LM}^{ } \equiv {\hat{\alpha }}_{0}\) and \(\hat{\sigma }_{ML}^{ } \equiv {\hat{\alpha }}_{1}\), we can unstandardize the (standardized) latent scores \(\widehat{{{\text{M}}L}}_{t}^{{{\text{z - PLS - SEM}}}}\) to compute a time series in a real metric (\(\widehat{{{\text{M}}L}}_{t}^{{{\text{PLS - SEM}}}}\)) using the following equation:

Figures 2 and 3 show the estimates of ML as a share of GDP and in millions of US dollars based on two exogenous estimates.Footnote 15

Money laundering in Iran calibrated by Rouhani’s (2018) claim

Money laundering in Iran calibrated by Arabmazar Yazdi and Khodkari (2008)

According to our estimates, Rouhani’s claim of a reduction from 22 billion to 12.5 billion (in US dollars) during the period 2013 to 2018 is excessively optimistic. Specifically, if we calibrate the latent construct by the exogenous values of illicit trade declared for \(t_{0} =\) 2013 and \(t_{1} =\) 2017,Footnote 16 we obtain (unreliable) negative estimates of ML over the period 1997 to 2005 (see Fig. 2). In contrast, ML estimates calibrated following Arabmazar Yazdi and Khodkari (2008) have more reasonable values (see Fig. 3).

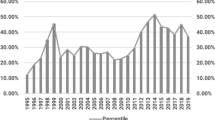

In terms of trend analysis, the ML activities, after a steady growth between 2003 and 2008 (average annual growth rate is about 12%) have fluctuated between 9 and 11% of GDP up to 2017. To provide a graphical causal interpretation of estimated ML, we compare the dynamics of the “causes” of the Iranian ML in Fig. 4.

Analysis of the determinants of money laundering

Figure 4 points out a substantial co-movement of ML activities with the level of corruption (0.956), drug traffic (0.676) and illegal trade (0.356) while the relationship between ML and fencing crime is weak (0.153). Looking at the reasons behind the two estimated peaks in ML activities, the first peak (2008–2009) is due to the (temporary) upturn in drug trafficking observed in the period 2006–2012, while the second one has been caused by the exceptional level of illegal trade observed in 2013.

4 Conclusions

This research examines ML in Iran using a PLS-SEM. From a methodological perspective, this is the first application of PLS-SEM to estimate this phenomenon and to investigate relationships among ML, corruption and socioeconomic development. This statistical method has two main advantages over previous econometric approaches applied in this strand of the literature. PLS-SEM can cope with unobservable variables (i.e., ML and Corruption) and multidimensional concepts (i.e., Socioeconomic development) simultaneously. Moreover, in contrast to multiple regression, it is possible to include both latent and observed variables in the structural model to account for confounding factors.

In particular, we include the resource dependence of the Iranian economy based on oil production and the deterministic trend to account for potential spurious correlation. Furthermore, by including the private expenditure per capita, we test the overall effect of ML on the Iranian economy by disentangling direct and indirect marginal effects.

From an empirical perspective, we find that while the direct effect of ML on socioeconomic development is not statistically significant, the indirect and overall effects are positive. This result validates the strand of the literature that hypothesizes that ML activities reduce, in the short run, the negative cost of crime due to the reinvestment of illegal earnings in the formal economy (e.g., Masciandaro 2007; Unger et al. 2016; Romero 2020).

According to our estimates of ML, the Iranian Government's estimates of ML over the period 2013–2018 (approximately 3% of GDP with a reduction of 43% over six years, from 22 billion to 12.5 billion dollars) are excessively optimistic. Indeed, if we use these “official” estimates to calibrate our PLS-SEM index, they produce negative values of ML over the period 1997 to 2005. In contrast, by calibrating latent scores with Arabmazar Yazdi and Khodkari's (2008) estimates based on the currency demand approach, we estimate that ML in 2017 is approximately 10% of official Iranian GDP. These results reveal that the exercise to estimate something, whose nature is not observable, is very complicated, and estimates of latent variables in the actual metric should always be considered as a rough approximation of the phenomenon. Indeed, even if the PLS-SEM model provides a satisfactory representation of the ML construct (i.e., goodness-of-fit statistics are adequate), the reliability of the ML estimates is significantly affected by the consistency of the exogenous estimates used to calibrate the latent scores.

In terms of policy implications, our results show that, in the short run, AML policies should be accompanied by an increase in public expenditure to offset the detrimental indirect effects that come through the multiplicative effect of a lower reinvestment of illicit earnings in the economy. Failure to do so is likely to lead to a serious misunderstanding of how ML can affect development due to the insignificant positive direct effect in the short run. This result does not mean that combatting ML is detrimental to a country’s development but that the positive effects of AML policies occur later than the negative indirect effects. This incongruity between the short- and long-term effects supports the view that AML legislation should be defined by international standards rather than national regulations due to the lack of government incentives to approve effective AML policies because the benefits due to better institutions and market efficiency do not offset the decline in economic performance in the short run (i.e., the political mandate of the government has approved them).

Notes

Specifically, if ML is measured by statistics on fraud crimes, it has a negative effect on economic growth in the short run and a positive effect in the long run. If ML is measured by drug crimes, it has no statistically significant effect in the short run and negative effects on growth in the long run.

“ …or, more formally, […] the constraints that shape human interaction” (North 1990: 3).

The Basel AML Index is a composite index whose overall score is calculated based on a weighted average of 14 indicators. These indicators are classified into five categories of ML/terrorist financing risk, corruption risk, financial transparency and standards, public transparency and accountability and political risk. The Basel AML index ranges between 0 (lowest risk) and 10 (highest risk). According to the Basel AML report (2017: 2), the top 10 high-risk countries are Iran, Afghanistan, Guinea-Bissau, Tajikistan, Laos, Mozambique, Mali, Uganda, Cambodia, and Tanzania.

SEM is a multivariate statistical approach used to measure and analyze the relationships between latent (unobserved) and manifest (observed) variables. The SEM may estimate unknown parameters by two alternative approaches: the covariance-based approach (CB-SEM) and the PLS method (PLS-SEM). In comparative terms with the CB-SEM, the PLS-SEM should be primarily used as a technique for predictive analysis in the presence of component-based proxies for latent variables. For details on PLS-SEM, see Dell’Anno and Maddah (2022). AlQudah et al. (2021) have applied PLS-SEM to investigate the role of public governance in mediating the impact of culture on money laundering.

This hypothesis is based on the inclusion of indexes of corruption and socioeconomic development—that are related directly or indirectly to the quality of political institutions—in the econometric model. The literature that analyzes the effect of political institutions on economic development suggests to measure institutional determinants using time period significantly larger than twenty years, e.g. Acemoglu et al. (2005) and Tabellini (2010) use 40 year window around five dates: 1600, 1700, 1750, 1800 and 1850.

This index is estimated by a SEM model where, corruption is the latent variable, the causes and the indicators are observable variables. Given that the indicators of the unobservable construct are proxies of corruption, then Corr_SEM can be considered as a meta-index of corruption.

This specification of the outer model allows including an observed variable in the inner model.

For example, according to Havranek et al.’s (2016) meta-analysis, 40% of empirical studies estimate a negative effect, 40% find no effect, and 20% of the analyzed studies showed that natural resources abundance positively affects economic growth.

Estimates are based on SmartPLS® (version 4.0.9) by Ringle et al. (2022), t-statistics and p-values are computed by applying 10,000 bootstrap samples. As a consequence of the limited time dimension (t = 21), we replace 21 missing values in the original dataset (see Appendix 1) with linear interpolations. The results are qualitatively robust to alternative methods for replacing missing values such as mean replacement (see Appendix 2).

These statistics are available from the corresponding author.

Due to the macroeconomic nature of dataset we cannot perform convergent validity of formative constructs. Basically, this assessment consists in testing whether the formatively measured construct is highly correlated with a reflective measure of the same construct. However, to execute this test, the reflective latent variable must be specified in the research design phase and included in data collection for the research. Unfortunately, the nature of the dataset makes unfeasible both collecting alternative manifest indicators to measure by reflective model the ML or using a single-item construct of the Iranian ML.

This specification derives from inverting the formula of standardization, i.e., from \(z_{t} = \left( {x_{t} - \hat{\mu }} \right)/\hat{\sigma }\) to \(x_{t} = \hat{\mu } + \hat{\sigma }z_{t}\).

See Appendix 3 for exogenous values and estimated values of ML.

The 2017 value is calculated by linear interpolation between the 2013 and 2018 values.

References

Acemoglu D, Robinson J (2010) The role of institutions in growth and development. Rev Econ Inst 1(2):1–33

Acemoglu D, Johnson S, Robinson J (2005) The rise of europe: Atlantic trade, institutional change, and economic growth. Am Econ Rev 95(3):546–579

Ades A, Di Tella R (1999) Rents, Competition, and Corruption. American Econ Rev 89(4):982–993

AlQudah A, Bani-Mustafa A, Nimer K, Alqudah AD, AboElsoud ME (2021) The effects of public governance and national culture on money laundering: a structured equation modeling approach. J Public Aff. https://doi.org/10.1002/pa.2796

Arabmazar Yazdi A, Khodkari L (2008) The estimation of volume of dirty money in Iran. Econ Res 7(27):119–142 (in Persian)

Arezki R, Brückner M (2011) Oil rents, corruption, and state stability: evidence from panel data regressions. Eur Econ Rev 55(7):955–963

Barone R, Masciandaro D, Schneider F (2022) Corruption and money laundering: you scratch my back, I’ll scratch yours. Metroeconomica 73:318–342

Bartlett LB (2002) The negative effects of money laundering on economic development. The Asian Development Bank, Regional, Assistance Project No. 5967. Countering Money Laundering in the Asian and Pacific Region. International Economics Groupm Dewey Ballantine LLP

Basel Institute on Governance. (2017). Basel AML index 2017 report. (https://baselgovernance.org/publications/basel-aml-index-2017)

Batmanghelidj E (2018) Tougher U.S. sanctions will enrich Iran’s Revolutionary Guards, Foreign Policy, 4 October 2018, (https://foreignpolicy.com/2018/10/04/irans-revolutionaryguard-corps-wont-suffer-from-stronger-u-s-sanctions-theyllbenefit-irgc-trump-sanctions/.)

Central Bank of Iran. (2020). Economic time series database. https://www.cbi.ir/page/8020.aspx

Coppedge MJ, Gerring CH, Knutsen SI, Lindberg J, Teorell D, Altman D, Ziblatt 2019. V-dem [country-year/country-date] dataset v9. Varieties of Democracy (V-Dem) Project. doi: https://doi.org/10.23696/vdemcy19.

Dell’Anno R (2020a) Corruption around the world: an analysis by partial least squares—structural equation modeling. Public Choice 184(3):327–350

Dell’Anno R, Maddah M (2022) Natural resources, rent seeking and economic development an analysis of the resource curse hypothesis for Iran. Macroecon Financ Emerg Mark Economies 15(1):47–65

Dell’Anno R (2023) Measuring the unobservable. Estimating informal economy by a structural equation modeling approach. Int Tax Public Financ 30(1):247–277

Dell’Anno R, Pergolizzi A, Pittiglio R, Reganati F (2020) Waste crime in Italian regions: a structural equation approach. Socioecon Plann Sci 71:100751

DellAnno R (2020b) Reconciling empirics on the political economy of the resource curse hypothesis. Evidence from long run relationships between resource dependence, democracy and economic growth in Iran. Resour Policy 68:101807

Farzanegan MR (2009) Illegal trade in the Iranian economy: evidence from a structural model. Eur J Polit Econ 25(4):489–507

Ferwerda J (2013) The effects of money laundering. In: Unger B, van der Linde D (eds) Research Handbook on Money Laundering. Edward Elgar Publishing, Cheltenham, pp 35–46

Global Financial Integrity (2019). Illicit financial flows to and from 148 developing countries: 2006–2015. Global Financial Integrity, Washington, DC (USA)

Gnutzmann H, McCarthy KJ, Unger B (2010) Dancing with the devil: country size and the incentive to tolerate money laundering. Int Rev Law Econ 30(3):244–252

Gründler K, Potrafke N (2019) Corruption and economic growth: New empirical evidence. Eur J Polit Econ 60:101810

Hair JF Jr, Hult GTM, Ringle CM, Sarstedt M (2014) A primer on partial least squares structural equation modeling (PLS-SEM). Sage Publications, USA

Havranek T, Horvath R, Zeynalov A (2016) Natural resources and economic growth: a meta-analysis. World Dev 88:134–151

Henry L, Moses S (2020) The impact of money laundering in beautiful places: the case of Trinidad and Tobago. Journal of Economics and International Finance 12(1):39–47

Henseler J, Hubona G, Ray PA (2016) Using PLS path modeling in new technology research: updated guidelines. Indus Manag Data Syst 116(1):2–20

International Monetary Fund (2018). Finance and Development. https://www.imf.org/external/pubs/ft/fandd/2018/12/imf-anti-money-laundering-and-economic-stability-straight.htm

Iranian Combating Goods and Exchange Smuggling Central Staff (2021). Research and Statistics. [https://epe.ir/News/18618/%D8%A8%D8%B1%D8%A2%D9%88%D8%B1%D8%AF-%D8%AD%D8%AC%D9%85-%D9%82%D8%A7%DA%86%D8%A7%D9%82-%DA%A9%D8%A7%D9%84%D8%A7-%D8%AF%D8%B1-%D8%B3%D8%A7%D9%84-1396]

Kolios B (2017) The resource curse hypothesis and welfare: a panel data analysis. J Empir Econ 5(3):163–168

Kolstad I, Søreide T (2009) Corruption in natural resource management: implications for policy makers. Resour Policy 34(4):214–226

Kumar VA (2012) Money laundering: concept, significance and its impact. Eur J Bus Manag 4(2):113–119

La Porta RL, de Silanes FL, Shleifer A, Vishny R (1999) The quality of government. J Law Econ Organ 15(1):222–279

Lashitew AA, Werker E (2020) Do natural resources help or hinder development? Resource abundance, dependence, and the role of institutions. Resour Energy Econ 61:101183

Loayza N, Villa E, Misas M (2019) Illicit activity and money laundering from an economic growth perspective: a model and an application to Colombia. J Econ Behav Organ 159:442–487

Markovska A, Adams N (2015) Political corruption and money laundering: lessons from Nigeria. J Money Laund Control 18(2):169–181

Masciandaro D (1999) Money laundering: the economics of regulation. Eur J Law Econ 7(3):225–240

Masciandaro D (2007) Economics of Money Laundering: A Primer. Working Paper. Paolo Baffi Centre Bocconi University

Mauro P (1995) Corruption and growth. Q J Econ 110(3):681–712

McDowell J, Novis G (2001) The consequences of money laundering and financial crime. Econ Perspect 6(2):6–8

North DC (1990) Institutional Change, and Economic Performance. Cambridge University Press, New York

Ospina-Velasco J (2003) Combating money laundering and smuggling in Colombia. Journal of Financial Crime 10(2):153–156

Pemstein D, Marquardt KL, Tzelgov E, Ting Wang Y, Medzihorsky J, Krusell J, von Romer J (2019) The V-Dem measurement model: Latent variable analysis for cross-national and cross-temporal expert-coded data. Working Paper No. 21, 4th edition, University of Gothenburg, Varieties of Democracy Institute.

Ringle, C. M., Wende, S., and Becker, J.-M. (2022). SmartPLS 4. Oststeinbek: SmartPLS GmbH, https://www.smartpls.com/

Romero V (2020) Bloody investment: misaligned incentives, money laundering and violence. Trends in Organized Crime, 1–29

Sabir S, Rafique A, Abbas K (2019) Institutions and FDI: evidence from developed and developing countries. Financ Innov 5(8):1–20

Sachs JD, Warner AM (1997) Sources of slow growth in African economies. J Afr Econ 6(3):335–376

Salehi M, Imeny VM (2019) Anti-money laundering developments in Iran. Qual Res Financ Mark 11(4):387–410

Savona, E.U., Riccardi, M. (eds) (2017). Assessing the risk of money laundering in Europe. Final Report of Project IARM (www.transcrime.it/iarm). Milano: Transcrime – Università Cattolica del Sacro Cuore (Italy)

Slama MB, Gueddari A (2022) The Relationship Between Money Laundering and Economic Growth in the MENA Region—A Simultaneous Equation Model. In: Ben Ali MS (ed) Key Challenges and Policy Reforms in the MENA Region Perspectives on Development in the Middle East and North Africa (MENA) Region. Springer, Cham

Slim, S., (2011). Macroeconomic Effects of Money Laundering, MPRA. Universidad de Quintana Roo. Paper No. 37031http.

Shmueli G, Ray S, Velasquez Estrada JM, Chatla SB (2016) The elephant in the room: Predictiveperformance of PLS models. J Business Res 69(10):4552–4564

Stancu I, Rece D (2009) The relationship between economic growth and money laundering - a linear regression model. Theor Appl Econ 16(9):3–8

Standaert S (2015) Divining the level of corruption: a bayesian state-space approach. J Comp Econ 43(3):782–803

Statistical Center of Iran. (2018). Statistical Yearbook. https://www.amar.org.ir/english.

Tabellini G (2010) Culture and Institutions: economic development in the regions of Europe. J Eur Econ Assoc 8(4):677–716

Teorell J, Sundström A, Holmberg S, Rothstein B, Alvarado Pachon N, Dalli CM (2021) The Quality of Government Standard Dataset, version Jan21. University of Gothenburg: The Quality of Government Institute, http://www.qog.pol.gu.se doi:https://doi.org/10.18157/qogstdjan21

Transparency International Organization (2022). Corruption Perception Index. Available at: https://www.transparency.org/en/cpi/2022

Unger B (2007) The Scale and Impacts of Money Laundering. Edward Elgar Publishing, UK

Unger B, Siegel M, Ferwerda J, de Kruijf W, Busuioic M, Wokke K, Rawlings G (2006) The amounts and the effects of money laundering. Report for the Ministry of Finance, 16. Utrecht School of Economics, Netherlands

United Nations Development Programme. (2020). Human Development Reports 1990–2020. http://hdr.undp.org/en/global-reports

United Nations Office on Drugs and Crimes (UNODC) (2011). UNODC report: Estimating illicit financial flows resulting from drug trafficking and other transnational organized crimes. United Nations Office on Drugs and Crime, Vienna (Austria)

Walker J (1995). Estimates of the Extent of Money Laundering in and through Australia. Paper prepared for Australian Transaction Reports and Analysis Centre (ATRAC), September by John Walker Consulting Services.

World Bank (2020). World Bank Indicators. https://data.worldbank.org/indicator

Funding

Open access funding provided by Università degli Studi di Salerno within the CRUI-CARE Agreement.

Author information

Authors and Affiliations

Contributions

Roberto Dell'Anno contributed to conceptualization, methodology, econometric analysis; writing—original draft preparation of sections 2, 3; and writing—review and editing. Majid Maddah contributed to data curation and writing—original draft preparation of sections 1, 4.

Corresponding author

Ethics declarations

Conflict of interest

The authors did not receive support from any organization for the submitted work. The authors have no relevant financial or non-financial interests to disclose.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1: Dataset

Label | Definition | Sources [variable code] | Mean | Min | Max | Obs |

|---|---|---|---|---|---|---|

oil_r_gdp | Oil rents (% of GDP) | WDI [NY.GDP.PETR.RT.ZS] | 21.85 | 11.84 | 32.37 | 21 |

Acc_el_r_p | Access to electricity, rural (% of rural population) | WDI [EG.ELC.ACCS.RU.ZS] | 97.50 | 94.16 | 100.00 | 18 |

HCI | Human Capital Index | Quality of Government Dataset [pwt_hci] | 2.00 | 1.61 | 2.42 | 21 |

HDI | Human Development Index | Quality of Government Dataset [undp_hdi] | 0.72 | 0.64 | 0.79 | 21 |

LB_Fem_M | Ratio of female to male labor force participation rate (%) (modeled ILO estimate) | WDI [SL.TLF.CACT.FM.ZS] | 21.52 | 15.38 | 26.09 | 21 |

Lifexp | Life expectancy at birth, total (years) | WDI [SP.DYN.LE00.IN] | 72.76 | 69.14 | 76.27 | 21 |

Tert_edu | School enrollment, tertiary (% gross) | WDI [SE.TER.ENRR] | 38.37 | 18.31 | 69.64 | 18 |

gdp_cap | GDP per capita (constant LCU) | WDI [NY.GDP.PCAP.KN] | 74,215,733 | 58,676,435 | 88,948,153 | 21 |

Priv.Exp_cap | Final consumption expenditure + private investment expenditure (constant 2004 million rials) divided by total population | Central Bank of Iran/ WDI [SP.POP.TOTL] | 18.27 | 12.94 | 22.65 | 19 |

BCI | Bayesian corruption index | Quality of Government Dataset [bci_bci] | 49.96 | 48.98 | 53.57 | 21 |

Corr_SEM | Structural corruption perception index | Dell'Anno (2020a, Appendix 2, Table A2) | 69.99 | 65.00 | 73.97 | 20 |

Pol_Corr | Political corruption index (Question: How pervasive is political corruption?) | Quality of Government Dataset [vdem_corr] | 0.70 | 0.53 | 0.83 | 21 |

PubS_corr | Public sector corruption index (Question: Question: To what extent do public sector employees grant favors in exchange for bribes, kickbacks, or other material inducements, and how often do they steal, embezzle, or misappropriate public funds or other state resources for personal or family use?) | Quality of Government Dataset [vdem_pubcorr] | 0.61 | 0.45 | 0.73 | 21 |

Drugs | Drug discoveries (kg per 100,000 people) | Statistical Center of Iran | 573.93 | 196.28 | 1005.66 | 21 |

Fencing | The sum of thefts from places such as government buildings, industrial and commercial centers, houses and theft of motor vehicles (per 100,000 people) | Statistical Center of Iran | 323.50 | 138.93 | 688.24 | 18 |

Illegaltrade | Smuggling on total trade (%) | For 1997–2002, we calculate the annual average of the minimum and maximum values of ten estimated series reported in Farzanegan (2009, Table 4). For 2008 and 2013–17: we calculate the ratio between “Smuggling” (estimated by Iranian Combating Goods and Exchange Smuggling Central Staff (2021) and “Total trade”(source Central bank of Iran) | 9.73 | 7.30 | 15.90 | 12 |

Appendix 2: Robustness check for replacement method of missing values

Figures

Model 1 (p-values in parentheses)

5 and

Model 2 (p-values in parentheses)

6 report estimated coefficients based on the replacement of missing values by using variable mean.

Appendix 3: PLS-SEM Estimates of Money Laundering and Exogenous estimates

Year | ML AK (2008) (% GDP) | ML index CurrDem (% GDP) | ML index CurrDem (millions US$) | ML AK (2008) (millions US$) | ML Rouhani (% GDP) | ML Rouhani Index_PLS − SEM (% GDP) | ML Rouhani Index_PLS − SEM (millions US$) | ML Rouhani (millions US$) |

|---|---|---|---|---|---|---|---|---|

Exogenous | Calibrated | Calibrated | Exogenous | Exogenous | Calibrated | Calibrated | Exogenous | |

1997 | 5.063 | 5.149 | 5910.84 | 5768.09 | − 2.460 | − 13,587.94 | ||

1998 | 5.784 | 5.081 | 5899.34 | 6378.79 | − 2.548 | − 14,019.15 | ||

1999 | 5.474 | 5.427 | 5957.95 | 6231.93 | − 2.101 | − 11,822.70 | ||

2000 | 4.761 | 5.185 | 5916.96 | 5217.87 | − 2.414 | − 13,358.87 | ||

2001 | 4.701 | 4.941 | 5875.60 | 5964.01 | − 2.729 | − 14,908.51 | ||

2002 | 5.056 | 5895.02 | − 2.581 | − 14,180.85 | ||||

2003 | 5.351 | 5945.00 | − 2.200 | − 12,307.80 | ||||

2004 | 6.348 | 6114.01 | − 0.911 | − 5,974.47 | ||||

2005 | 6.963 | 6218.29 | − 0.116 | − 2,066.67 | ||||

2006 | 7.706 | 6344.14 | 0.843 | 2,649.65 | ||||

2007 | 9.121 | 6583.98 | 2.671 | 11,637.59 | ||||

2008 | 9.964 | 6726.74 | 3.760 | 16,987.23 | ||||

2009 | 10.004 | 6733.57 | 3.812 | 17,243.26 | ||||

2010 | 8.892 | 6545.15 | 2.375 | 10,182.27 | ||||

2011 | 9.576 | 6660.93 | 3.258 | 14,521.28 | ||||

2012 | 10.040 | 6739.68 | 3.858 | 17,472.34 | ||||

2013 | 10.753 | 6860.50 | 4.780 | 4.780 | 22,000.00 | 22,000 | ||

2014 | 9.527 | 6652.66 | 3.195 | 14,211.35 | ||||

2015 | 10.110 | 6751.55 | 3.949 | 17,917.02 | ||||

2016 | 9.349 | 6622.46 | 2.965 | 13,079.43 | ||||

2017 | 9.556 | 6657.70 | 3.233 | 3.233 | 14,400.00 | 14,400 |

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Dell’Anno, R., Maddah, M. Money laundering, corruption and socioeconomic development in Iran: an analysis by structural equation modeling. Int Rev Econ 70, 395–417 (2023). https://doi.org/10.1007/s12232-023-00424-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12232-023-00424-9