Abstract

In this paper we explore the profit-taking tactics employed by informed traders when there are informational asymmetries across investors. Our laboratory is Tradesports, which until 2015 operated a double auction exchange where participants traded binary options contracts. This venue is a close analog to stock markets and, because each contract’s value is unambiguously revealed, the joint hypothesis problem is mitigated. We demonstrate that when the ratio of noise traders to sophisticated traders is highest, shares are most overpriced. Data show that informed traders heavily target noise traders when liquidity is high, and in conducting profit-taking operations they prefer to short sell via small transactions and round lots. Results suggest that, even in the absence of liquidity constraints and certain costs and risks related to short selling, the relative complexity of short selling can itself lead to overpricing.

Similar content being viewed by others

Notes

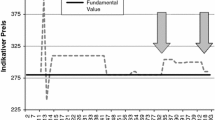

It is noteworthy that contracts are significantly overpriced in each of the first three price quintiles. Theories developed by Kahneman and Tversky (1979) and Prelec (1998) suggest that an s-shaped pattern should emerge with a point of inflection around $37, but here the point of inflection first occurs at around $66 (see Fig. 1).

Prior equity research has examined the informativeness of lot size rounding, and evidence suggests that round-quantity trades have greater price impact than do unrounded trades (Alexander and Peterson 2007).

References

Admati A, Pfleiderer P (1988) A theory of intraday patterns: volume and price variability. Rev Financ Stud 1:3–40

Alexander G, Peterson M (2007) An analysis of trade-size clustering and its relation to stealth trading. J Financ Econ 84:435–471

Avramov D, Chordia T, Jostova G, Philipov A (2013) Anomalies and financial distress J Financ Econ 108:139–159

Baker M, Wurgler J (2006) Investor sentiment and the cross section of stock returns. J Financ 61:1645–1680

Barclay M, Warner J (1993) Stealth trading and volatility. J Financ Econ 34:281–305

Bloomfield R, O’Hara M, Saar G (2009) How noise trading affects markets: an experimental analysis. Rev Financ Stud 22:2275–2302

Borghesi R (2007) Price biases in a prediction market: NFL contracts on Tradesports. Journal of Prediction Markets 1:233–253

D’Avolio G (2002) The market for borrowing stock. J Financ Econ 66:271–306

Engelberg J, Reed A, Riggenberg M (2012) How are shorts informed? Short sellers, news, and information processing. J Financ Econ 105:260–278

Grossman S, Miller M, Kenneth C, Fischel D, Ross D (1997) Clustering and competition in asset markets. J Law Econ 40:23–60

Harris L (1991) Stock price clustering and discreteness. Rev Financ Stud 4:389–415

Hodrick L, Moutlon P (2009) Liquidity: considerations of a portfolio manager. Financ Manag 38:59–74

Kahneman D, Tversky A (1979) Prospect theory: an analysis of decision under risk. Econometrica 47:263–292

Miller E (1977) Risk, uncertainty and divergence of opinion. J Financ 32:1151–1168

O’Connor P, Zhou F (2008) The Tradesports NFL prediction market: an analysis of market efficiency, transaction costs, and bettor preferences, 2008. Journal of Prediction Markets 2:45–71

O’Hara M, Yao C, Mao Y (2014) What is not there: the odd-lot bias of TAQ. J Financ 69:2199–2236

Prelec D (1998) The probability weighting function. Econometrica 66:497–527

Sadka R, Scherbina A (2007) Analyst disagreement, mispricing, and liquidity. J Financ 62:2367–2403

Schmeling M (2009) Investor sentiment and stock returns: some international evidence. J Empir Financ 16:394–408

Stambaugh, R, Yu J, Yuan Y (2012) The short of it: investor sentiment and anomalies. J Financ Econ 104:288–302

Subrahmanyam A (1991) Risk aversion, market liquidity, and price efficiency. Rev Financ Stud 4:417–441

Tetlock P (2008) Liquidity and prediction market efficiency. Columbia University, Working Paper

Wolfers J, Zitzewitz E (2006) Five open questions about prediction markets. University of Michigan and Dartmouth College, Working Paper

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Borghesi, R. Liquidity, overpricing, and the tactics of informed traders. J Econ Finan 41, 701–713 (2017). https://doi.org/10.1007/s12197-016-9375-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12197-016-9375-5