Abstract

This article analyzes the effects of the American Taxpayer Relief Act of 2012 (Obama Tax Increase) and the Jobs and Growth Tax Relief Reconciliation Act of 2003 (Bush Tax Cut) on corporate payout decision and stock returns. Logit and fixed-effect panel data analyses are conducted on all firms listed in NYSE, Amex and NASDAQ in the announcement windows of two, three and four quarters before and after the tax reforms. The results show that the implementation of these tax reforms more persistently affects dividend payments than stock repurchases. It also has a boosting effect on stock returns in the Bush Tax Cut that is 75 % greater than their reducing effect in the Obama Tax Increase, in absolute terms, controlling for dividend payment and stocks repurchase. These effects are robust to different market capitalization sizes. Less solvent firms persistently spend larger dollar amounts in stock repurchases, especially in the announcement of the Bush Tax Cut (+1.11 % per solvency ratio percentage in the [−2Q, +2Q] window). Insolvency is more often significant and with positive impacts on stock returns in the Obama Tax Increase, suggesting that some investors decide to migrate to leveraged-high-growth firms once they realize that some dividend-paying firms could change their dividend policies.

Similar content being viewed by others

Notes

Chahyadi and Salas (2012) assert that 100% of the decline in the proportion of dividend payers can be explained by changes in firm characteristics only.

See Hausman (1978).

For example, a firm with good investment opportunities (high Tobin’s Q) could decide to start paying dividends after a dividend tax cut, but the payment dollar amounts from those high-Tobin’s-Q firms will not necessarily be higher than other firms’ amounts.

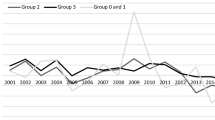

On section 5, a robustness check from Table 9 compares the variables for dividend payers and non-payers in the periods from 1990 to 1999 and from 2000 to 2014.

The top-income stockholders are the majority of investors. As noted by Huang and Marr (2012), the top 20% of taxpayers received around 94% percent of all capital gains in 2012.

References

Allen F, Bernardo A, Welch I (2000) A theory of dividends based on tax clienteles. J Financ 55(6):2499–2536

Alli K, Khan A, Ramirez G (1993) Determinants of corporate dividend policy: a factorial analysis. Financial Review 28(4):523–547

Bali R (2003) An empirical analysis of stock returns around dividend changes. Appl Econ 35(1):51–61

Barclay M (1987) Dividends, taxes, and common stock prices: The ex-dividend day behavior of common stock prices before the income tax. J Financ Econ 19(1):31–44

Ben-Rephael A, Oded J, Wohl A (2013) Do Firms Buy Their Stock at Bargain Prices? Evidence from Actual Stock Repurchase Disclosures*. Review of Finance. doi:10.1093/rof/rft028

Bhattacharya S (1979) Imperfect information, dividend policy, and" the bird in the hand" fallacy. Bell J Econ:259–270

Blouin J, Raedy J, Shackelford D (2004) Did dividends increase immediately after the 2003 reduction in tax rates? (No. In: w10301). Research, National Bureau of Economic

Bradley M, Wakeman LM (1983) The wealth effects of targeted share repurchases. J Financ Econ 11(1):301–328

Cebula R, Boylan R, Foley M, Isard D (2014) Implications of Recent Federal Personal Income Tax Increases for Income Tax Evasion, Tax Revenues, and Budget Deficits. Unpublished working paper, Jacksonville University

Chahyadi CS, Salas JM (2012) Not paying dividends? A decomposition of the decline in dividend payers. J Econ Financ 36(2):443–462

Dann LY (1981) Common stock repurchases: An analysis of returns to bondholders and stockholders. J Financ Econ 9(2):113–138

Dann LY, DeAngelo H (1983) Standstill agreements, privately negotiated stock repurchases, and the market for corporate control. J Financ Econ 11(1):275–300

Dittmar A, Field LC (2015) Can managers time the market? Evidence using repurchase price data. J Financ Econ 115(2):261–282

Dubay, C., 2013. The Bush Tax Cuts Explained: Where Are They Now? The Heritage Foundation. Retrieved from http://www.heritage.org/research/reports/2013/02/bush-tax-cuts-explained-facts-costs-tax-rates-charts. Last access on October 26, 2014

Easterbrook F (1984) Two agency-cost explanations of dividends. Am Econ Rev:650–659

Fama E, French K (2001) Disappearing dividends: changing firm characteristics or lower propensity to pay? J Financ Econ 60(1):3–43

Hanlon M, Hoopes J (2014) What do firms do when dividend tax rates change? An examination of alternative payout responses. J Financ Econ 114:105–124

Hausman J (1978) Specification tests in econometrics. Econometrica 46:1251–1271

Huang, C., Marr, C., 2012. Raising today’s low capital gains tax rates could promote economic efficiency and fairness, while helping reduce deficits. Center on Budget and Policy Priorities. Washington, DC. Retrieved from http://www.cbpp.org/files/9-19-12tax.pdf. Last access on October 26, 2014

Hungerford TL (2013) Changes in income inequality among U.S. tax filers between 1991 and 2006: The role of wages, capital income, and taxes. doi:10.2139/ssrn.2207372

Jagannathan M, Stephens CP, Weisbach MS (2000) Financial flexibility and the choice between dividends and stock repurchases. J Financ Econ 57(3):355–384

Jensen M (1986) Agency costs of free cash flow, corporate finance, and takeovers. Am Econ Rev:323–329

Julio B, Ikenberry D (2004) Reappearing dividends. Journal of Applied Corporate Finance 16(4):89–100

Klein A, Rosenfeld J (1988) Targeted share repurchases and top management changes. J Financ Econ 20:493–506

Litzenberger R, Ramaswamy K (1979) The effect of personal taxes and dividends on capital asset prices: Theory and empirical evidence. J Financ Econ 7(2):163–195

Martínez-Zarzoso I (2013) The log of gravity revisited. Appl Econ 45(3):311–327

Masulis RW (1980) Stock repurchase by tender offer: An analysis of the causes of common stock price changes. J Financ 35(2):305–319

Miller M, Modigliani F (1961) Dividend policy, growth, and the valuation of shares. J Bus 34(4):411–433

Miller M, Rock K (1985) Dividend policy under asymmetric information. J Financ 40(4):1031–1051

Pérez-Cavazos G, Silva A (2014) Tax-minded executives and corporate tax strategies: evidence from the 2013 tax hikes. Unpublished working paper, University of Chicago and University of Miami

Pettit R (1977) Taxes, transactions costs and the clientele effect of dividends. J Financ Econ 5(3):419–436

Poterba J, Summers L (1984) New evidence that taxes affect the valuation of dividends. J Financ 39(5):1397–1415

Rozeff M (1982) Growth, beta and agency costs as determinants of dividend payout ratios. J Financ Res 5(3):249–259

Scholz J (1992) A direct examination of the dividend clientele hypothesis. J Public Econ 49(3):261–285

Tsetsekos GP, Kaufman DJ Jr, Gitman LJ (2011) A survey of stock repurchase motivations and practices of major US corporations. Journal of Applied Business Research (JABR) 7(3):15–21

Vermaelen T (1981) Common stock repurchases and market signalling: An empirical study. J Financ Econ 9(2):139–183

Vermaelen T (1984) Repurchase tender offers, signaling, and managerial incentives. J Financ Quant Anal 19(02):163–181

Wooldridge, J. (2012). Introductory econometrics: A modern approach. Cengage Learning.

Yousuf, H., 2013. Dividend tax hike ‘could have been worse’. CNN Money. Retrieved from http://money.cnn.com/2013/01/02/investing/fiscal-cliff-dividend-tax-rate. Last access on November 3, 2014

Author information

Authors and Affiliations

Corresponding author

Additional information

Andre C Vianna is a Financial analyst from the Ministry of Finance of Brazil under a doctoral research grant at The University of Texas Rio Grande Valley provided by CAPES-Brazil.

The opinions in this publication are the author’s responsibility, not necessarily expressing the viewpoint of the Ministry of Finance of Brazil.

Rights and permissions

About this article

Cite this article

Vianna, A. Effects of Bush Tax Cut and Obama Tax Increase on corporate payout policy and stock returns. J Econ Finan 41, 441–462 (2017). https://doi.org/10.1007/s12197-016-9362-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12197-016-9362-x