Abstract

This study utilizes the FDIC’s Historical Statistics on Banking from 1966 to 2013 to analyze the long-run relationship between federal funds rate policy, bank capital, and lending at U.S. commercial banks. The empirical analysis uses an autoregressive model to examine loan activity between two different groups of banks with different bank capital structures (high and low capital banks). The results of the study show that commercial loans at high capital banks have a stronger relationship to changes in the federal funds rates than low capital banks. Real estate loans show a slightly stronger negative correlation with federal funds for high capital banks than banks with low capital levels. The change in the portfolio ratio between real estate to commercial loans is negatively related to monetary policy changes.

Similar content being viewed by others

Notes

However, asset quality and bank capital adequacy were always a concern of bank regulators (see Mitchell (1909)) and the National Banking Act of 1863 mandated bank solvency.

See Friedman and Schwartz (1963) for detail history on banking runs and crises.

The pooled GLS regression approach used in this study should be appropriate. Panel regression for fixed effects or random effects may be inappropriate since testing by F-Test (or Wald tests on the significance of the alternative intercepts) and the Hausman test indicate that pooled approach is more appropriate.

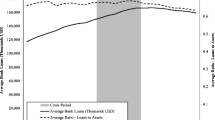

Specifically, the ratio of total equity capital to total assets (or BKTA ratio).

The FFR is obtained from the Federal Reserve Bank’s website listed within the H.15 data series.

The study did experiment with using the Livingston Survey’s forecast of GDP provided by the Philadelphia Federal Reserve, but this variable offered no improvement over the actual GDP and may have introduced higher order serial correlation.

The study was not able to use the Federal Reserve’s Survey of Senior Loan Officers because of a gap between 1984 and 1990. This survey would be useful in controlling for changing credit standards at banks. The study also tested the first difference between the 3-month U.S. Treasury Bill rate and the Moody’s BAA corporate bond yield as a proxy for credit risk, but the variable was insignificant and not used.

The autoregressive technique transforms the baseline linear model into a nonlinear model. The transformed nonlinear model’s coefficients are then estimated using a Marquardt nonlinear least squares algorithm. This autoregressive approach seeks to minimize the direct usage of the lagged dependent variable. See: Davison and MacKinnon (Davidson and MacKinnon 2004, pp. 214–215).

It is not possible to separate domestic loan activity from loans after 1978 and no separate foreign loan activity is available prior to 1978.

A time trend dummy was test and subsequently dropped since it was insignificant. National Bureau of Economic Research (NBER) recession dummy years were test, but were insignificant and not included.

Full results for all the independent variables like GDP are available upon request and were left out to save space. GDP was highly significant and used as a control variable.

References

Aikman D, Vlieghe G (2004). How much does bank capital matter? Bank of England Quarterly Bulletin. Bank of England, (Spring): 48–58

Bernanke BS, Blinder AS (1992) The federal funds rate and the channels of monetary transmission. Am Econ Rev 82(4):901–921

Bernanke BS, Gertler M (1987) Banking in General Equilibrium. In: Barnett W, Singleton K (eds) New approaches to monetary economics. Cambridge University Press, Cambridge

Bernanke BS, Lown CS (1991) The credit crunch. Brook Pap Econ Act 2:205–239

Black, L. K., and R. J. Rosen (2007) How the credit channel works: differentiating the bank lending channel and the balance sheet channel. Working Paper Series 2007–13, Federal Reserve Bank of Chicago.

Bolton P, Freixas X (2006) Corporate finance and monetary transmission mechanism. Rev Financ Stud 19(3):829–870

Busch CM, Prieto E (2014) Do better capitalized banks lend less? long-run panel evidence from Germany. International Finance 17(1):1–23

Cornett MM, Tehranian H (1994) An examination of voluntary versus involuntary security issuances by commercial banks: the impact of capital regulations on common stock returns. J Financ Econ 35(1):99–122

Davidson R, MacKinnon J (2004) Econometric theory and methods. Oxford University Press, Oxford

Den Haan WJ, Sumner SW, Yamashiro GM (2007) Banks’ loan portfolio and the monetary transmission mechanism. J Monet Econ 54(3):904–924

Driscoll JC (2004) Does bank lending affect output? evidence from the U.S. states. J Monet Econ 51(3):451–471

Estella A, Park S, Peristiani S (2000). Capital ratios as predictors of bank failure. Economic Policy Review, Federal Reserve Bank of New York, (6): 33–52.

Friedman M, Schwartz A (1963) A Monetary History of the United States. Princeton Press, Princeton, NJ, p 1867–1960

Gambacorta L, Mistrulli PE (2004) Does bank capital affect lending behavior? J Financ Intermed 13:436–457

Hancock D, Wilcox J (1997) Bank capital, nonbank finance, and real estate activity. J Hous Res (Fannie Mae Foundation) 8(1):75–105

Holmstrom B, Tirole J (1997) Financial intermediation, loanable funds, and the real sector. Q J Econ 112(3):663–691

Kashyap AK, Stein JC (1995) The impact of monetary policy and bank balance sheets. Carn-Roch Conf Ser Public Policy 42:151–195

Kashyap AK, Stein JC (2000) What do a million observations on banks say about the transmission of monetary policy? Am Econ Rev 90(3):407–428

Kishan RP, Opiela TP (2006) Bank capital and loan asymmetry in the transmission of monetary policy. J Bank Financ 30(1):260–284

Kuttner KN, Mosser PC (2002) The monetary transmission mechanism: some answers and further questions. Federal Reserve Bank of New York Economic Review. Federal Reserve Bank Of New York 8(1):15–24

Laidler DEW (1985) The Demand for Money: Theories, Evidence, and Problems. Harper & Row, New York, NY

Mankiw G (1986) The allocation of credit and financial collapse. Q J Econ 101(3):455–470

Meh C, Moran K (2004). Bank capital, agency costs, and monetary policy. Bank of Canada, Working Paper # 2004–6

Miller MH (1995) Do the m&m propositions apply to banks? J Bank Financ 19:483–489

Mishkin FS (1995) Symposium on the monetary transmission mechanism. J Econ Perspect 9(4):3–10

Mitchell W (1909) The decline in the ratio of banking capital to liabilities. Q J Econ 23(4):697–713

Nier E, Ziccchino L (2006) Bank weakness, loan supply, and monetary policy. Bank of England, Work in Progress

Peek J, Rosengren E (1995) The capital crunch: neither a borrower nor a lender be. J Money Credit Bank 27(3):626–638

Sharpe SA (1995) Bank capitalization, regulation, and the credit crunch: a critical review of the research findings, vol 95(20). Papers in the Finance and Economics Discussion Series, Federal Reserve Board, Washington, DC

Stein JC (1998) An adverse selection model of bank asset and liability management with implication for the transmission of monetary policy. RAND J Econ 29(3):466–486

Wall LD, Peterson PP (1996) Banks responses to binding regulatory capital requirements. Economic Review. Federal Reserve Bank Of Atlanta 81:1–17

Author information

Authors and Affiliations

Corresponding author

Additional information

This paper was part of my dissertation work at the New School for Social Research.

Data Appendix

Data Appendix

1.1 U.S. Bank Capital Groups

This appendix provides details on the construction of the two capital banking groups. Data was obtained from the FDIC’s Historical Statistics on Banking (FDIC HS) from 1966 to 2013. The capital to asset ratio is the total equity capital divided into total assets (or BKTA ratio). The U.S. banking industry average for the capital to asset ratio for all U.S. FDIC commercial banks over this time period was 8.39 %. Each state is calculated to determine its own capital to asset ratio that is then placed into one of two groups (or high and low capital banks) that is either above or below the U.S. banking industry historical average BKTA ratio. U.S. states plus the District of Columbia are given below by their common U.S. Postal abbreviation followed by their respective historical capital to asset ratio average stated as a percentage.

1.2 Capital to asset ratio

States in the ‘high capital’ bank group (states above the U.S. capital to asset ratio) are: AK 11.05 %, DE 10.94 %, NV 10.41 %, NH 9.46 %, WV 9.18 %, SD 9.16 %, AL 9.06 %, GA 9.02 %, KS 8.94 %, AR 8.78 %, IA 8.68 %, ME 8.67 %, NE 8.60 %, RI 8.57 %, ND 8.55 %, LA 8.54 %, WY 8.53 %, MS 8.50 %, TN 8.45 %, KY 8.43 %, UT 8.43 %.

States in the ‘low capital’ bank group (states below the U.S. capital to asset ratio) are: VA 8.38 %, OR 8.37 %, HI 8.37 %, OK 8.29 %, MT 8.28 %, SC 8.25 %, DC 8.24 %, IN 8.15 %, MD 8.13 %, ID 8.13 %, CT 8.12 %, MO 8.11 %, WI 8.11 %, FL 8.08 %, WA 8.02 %, NM 7.98 %, PA 7.92 %, TX 7.91 %, MI 7.83 %, OH 7.82 %, CO 7.82 %, CA 7.75 %, MN 7.68 %, IL 7.57 %, NC 7.56 %, VT 7.53 %, AZ 7.49 %, NJ 7.42 %, NY 7.31 %, MA 7.09 %.

Rights and permissions

About this article

Cite this article

Orzechowski, P.E. Bank capital, loan activity, and monetary policy: evidence from the FDIC’s Historical Statistics on Banking. J Econ Finan 41, 392–407 (2017). https://doi.org/10.1007/s12197-016-9359-5

Published:

Issue Date:

DOI: https://doi.org/10.1007/s12197-016-9359-5