Abstract

This study examines the asymmetric impact of climate policy uncertainty (CPU) under heterogeneous stock market conditions in the Chinese stock market. The study adopted two econometrics techniques of panel generalized autoregressive condition heteroscedasticity and panel quantiles via moment models. The results show that the markets’ response to CPU is homogeneous and varies across bearish, normal, and bullish conditions. The findings established that CPU is a risk factor, and its pricing is asymmetric as it depends on market conditions. The results also suggest that CPU is one of the predictors of future returns, but the forecast may be largely driven by market conditions. The study further shows how market’s response to CPU varies which often complicates prediction as the direction of response is determined by the market’s condition.

Similar content being viewed by others

Data availability

The data used in this study were obtained from open-source repositories (investing.com and climate policy uncertainty) and its freely available. However, they could be provided upon request.

Notes

Al-Thaqeb and Algharabali (2019) defined policy uncertainty as “the economic risk associated with undefined future government policies and regulatory frameworks” and show that it raises the risk of businesses and individuals delaying spending and investments due to market uncertainty.

The choice of panel generalized autoregressive condition heteroscedasticity is to model the stock returns and volatility in a panel framework while the panel quantiles via moment model (MMQR) was adopted to determine the tail-dependence of the stock market returns to climate uncertainty and other determinants.

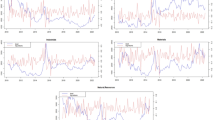

This study controls for CSD given the integration (i.e. the stock markets are moving in together suggesting the possibility of comparable asset returns for a given risk factor (see Fig. 3 in appendix)) of the Chinese stock markets which could lead to possible potential statistical biases in the estimates. Furthermore, the homogeneity test enables this study to test for the commonality of the markets’ response to the CPU.

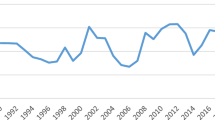

Data on Chinex composite stock in particular started from September 2010 while the climate policy uncertainty data is available till August 2022.

Gavriilidis, K. (2021). Measuring Climate Policy Uncertainty. Available at SSRN: https://ssrn.com/abstract=3847388.

References

Al-Thaqeb, S.A., Algharabali, B.G.: Economic policy uncertainty: a literature review. J. Econ. Asymmetries 20(2019), e00133 (2019). https://doi.org/10.1016/j.jeca.2019.e00133

Bollerslev, T.: Generalized autoregressive conditional heteroskedasticity. J. Econom. (1986). https://doi.org/10.1016/0304-4076(86)90063-1

Bollerslev, T.: Modelling the coherence in short-run nominal exchange rates: a multivariate generalized ARCH model. Rev. Econ. Stat. 72(3), 498–505 (1990)

Bouri, E., Iqbal, N., Klein, T.: Climate policy uncertainty and the price dynamics of green and brown energy stocks. Finance Res. Lett. 47, 102740 (2022). https://doi.org/10.1016/j.frl.2022.102740

Bouri, E., Rognone, L., Sokhanvar, A., Wang, Z.: From climate risk to the returns and volatility of energy assets and green bonds: a predictability analysis under various conditions. Technol. Forecast. Soc. Change 194, 122682 (2023)

Cermeño, R., Grier, K.B.: Conditional heteroskedasticity and cross-sectional dependence in panel data: an empirical study of inflation uncertainty in the G7 countries. Contrib. Econ. Anal. 274, 259–277 (2006)

Chen, X., Chiang, T.C.: Empirical investigation of changes in policy uncertainty on stock returns: evidence from China’s market. Res. Int. Bus. Finance 53(2020), 101183 (2020)

Chen, J., Jiang, F., Tong, G.: Economic policy uncertainty in China and stock market expected returns. Account. Finance 57(2017), 1265–1286 (2017). https://doi.org/10.1111/acfi.12338

Chiang, T.C.: Economic policy uncertainty, risk and stock returns: evidence from G7 stock markets. Finance Res. Lett. 29(2019), 41–49 (2019). https://doi.org/10.1016/j.frl.2019.03.018

Chiang, T.C.: Geopolitical risk, economic policy uncertainty and asset returns in Chinese financial markets. Chin. Finance Rev. Int. 11(4), 474–501 (2021)

Chiang, T.C.: Real stock market returns and inflation: evidence from uncertainty hypotheses. Finance Res. Lett. 53, 103606 (2023)

Chiang, T.C., Li, J.: Stock returns and risk: evidence from quantile regression analysis. J. Risk Finan. Manag. 5(1), 1–130 (2012)

Dai, Z., & Zhang, X. (2023). Climate policy uncertainty and risks taken by the bank: Evidence from China. International Review of Financial Analysis, 87(May 2023), 102579, https://doi.org/10.1016/j.irfa.2023.102579.

Dutta, A., Bouri, E., Rothovius, T., Uddin, G.S.: Climate risk and green investments: new evidence. Energy 265, 126376 (2023)

Engle, R.F., Bollerslev, T.: Modelling the persistence of conditional variances. Econom. Rev. 5(1), 1–50 (1986)

Fuss, S., Szolgayova, J., Obersteiner, M., Gusti, M.: Investment under market and climate policy uncertainty. Appl. Energy 85(2008), 708–721 (2008). https://doi.org/10.1016/j.apenergy.2008.01.005

Hoque, M.E., Zaidi, M.A.S.: Impacts of global economic policy uncertainty on emerging stock markets: evidence from linear and non-linear models. Prague Econ. Pap. (2020). https://doi.org/10.18267/j.pep.725

Huang, W.-Q., Liu, P.: Asymmetric effects of economic policy uncertainty on stock returns under different market conditions: evidence from G7 stock markets. Appl. Econ. Lett. (2021). https://doi.org/10.1080/13504851.2021.1885606

Koenker, R.: Quantile regression. Cambridge University Press, Cambridge (2005)

Koenker, R., Bassett, G., Jr.: Regression quantiles. Econom. J. Econom. Soc. 46(1), 33–50 (1978)

Kundu, S., Paul, A.: Effect of economic policy uncertainty on stock market return and volatility under heterogeneous market characteristics. Int. Rev. Econ. Finance 80, 597–612 (2022). https://doi.org/10.1016/j.iref.2022.02.047

Lamperti, F., Bosetti, V., Roventini, A., Tavoni, M., Treibich, T.: Three green financial policies to address climate risks. J. Financ. Stab. 54, 100875 (2021)

Lei, A.C., Song, C.: Economic policy uncertainty and stock market activity: evidence from China. Glob. Finance J. (2020). https://doi.org/10.1016/j.gfj.2020.100581

Li, T., Ma, F., Zhang, X., Zhang, Y.: Economic policy uncertainty and the Chinese stock market volatility: novel evidence. Econ. Model. (2019). https://doi.org/10.1016/j.econmod.2019.07.002

Li, H., Bouri, E., Gupta, R., Fang, L.: Return volatility, correlation, and hedging of green and brown stocks: is there a role for climate risk factors? J. Clean. Prod. 414, 137594 (2023)

Lv, W., Li, B.: Climate policy uncertainty and stock market volatility: evidence from different sectors. Finance Res. Lett. 51, 103506 (2023). https://doi.org/10.1016/j.frl.2022.103506

Machado, J.A., Silva, J.S.: Quantiles via moments. J. Econom. 213(2019), 145–173 (2019)

Mamman, S.O., Wang, Z., Iliyasu, J.: Commonality in BRICS stock markets’ reaction to global economic policy uncertainty: evidence from a panel GARCH model with cross sectional dependence. Finance Res. Lett. (2023). https://doi.org/10.1016/j.frl.2023.103877

Mei, D., Zeng, Q., Zhang, Y., Hou, W.: Does US economic policy uncertainty matters for European stock markets volatility? Phys. A (2018). https://doi.org/10.1016/j.physa.2018.08.019

Pastor, L., Veronesi, P.: Political uncertainty and risk premia. In: NBER Working Paper, pp. 17464 (2011). http://www.nber.org/papers/w17464

Pastor, L., Veronesi, P.: Uncertainty about government policy and stock prices. J. Finance 67(4), 1219–1264 (2012)

Peng, G., Huiming, Z., Wanhai, Y.: Asymmetric dependence between economic policy uncertainty and stock market returns in G7 and BRIC: a quantile regression approach. Finance Res. Lett. (2017). https://doi.org/10.1016/j.frl.2017.11.001

Pesaran, M.H., Yamagata, T.: Testing slope homogeneity in large panels. J. Econom. 142(1), 50–93 (2008)

Pesaran, M.H.: General diagnostic tests for cross section dependence in panels (IZA Discussion Paper No. 1240). Institute for the Study of Labor (IZA) (2004)

Ren, X., Shi, Y., Jin, C.: Climate policy uncertainty and corporate investment: evidence from the Chinese energy industry. Carbon Neutr. 1(14), 1–11 (2022a). https://doi.org/10.1007/s43979-022-00008-6

Ren, X., Zhang, X., Yan, C., Gozgor, G.: Climate policy uncertainty and firm-level total factor productivity: evidence from China. Energy Econ. 113(2022), 106209 (2022b)

Tian, H., Long, S., Li, Z.: Asymmetric effects of climate policy uncertainty, infectious diseases-related uncertainty, crude oil volatility, and geopolitical risks on green. Finance Res. Lett. 48, 103008 (2022). https://doi.org/10.1016/j.frl.2022.103008

Xu, Y., Wang, J., Chen, Z., Liang, C.: Economic policy uncertainty and stock market returns: new evidence. North Am. J. Econ. Finance 58(2021), 101525 (2021). https://doi.org/10.1016/j.najef.2021.101525

Xu, X., Huang, S., Lucey, B.M., An, H.: The impacts of climate policy uncertainty on stock markets: comparison between China and the US. Int. Rev. Financ. Anal. 88, 102671 (2023). https://doi.org/10.1016/j.irfa.2023.102671

Yuan, D., Li, S., Li, R., Zhang, F.: Economic policy uncertainty, oil and stock markets in BRIC: evidence from quantiles analysis. Energy Econ. 110, 105972 (2022). https://doi.org/10.1016/j.eneco.2022.105972

Zeng, Q., Ma, F., Lu, X., Xu, W.: Policy uncertainty and carbon neutrality: evidence from China. Finance Res. Lett. 47, 102771 (2022). https://doi.org/10.1016/j.frl.2022.102771

Acknowledgements

The article has been prepared with the support of the Ministry of Science and Higher Education of the Russian Federation (Ural Federal University Program of Development within the Priority-2030 Program).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

All authors have no conflict of interest.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Shuaibu, M.I., Mamman, S.O., Iliyasu, J. et al. Asymmetric pricing of climate policy uncertainty under heterogeneous stocks market conditions in China: evidence from GARCH and quantile models. Lett Spat Resour Sci 17, 10 (2024). https://doi.org/10.1007/s12076-024-00372-0

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s12076-024-00372-0