Abstract

This paper reviews findings on how different dimensions of national culture influence management control systems (MCS). It is based on a comprehensive sample of 43 peer-reviewed journal articles that were identified in a systematic literature search. For the categorization of the results, we refer to Malmi and Brown’s (Manag Account Res;19:287–300, 2008. https://doi.org/10.1016/j.mar.2008.09.003) frequently quoted framework. Our systematic literature review offers a detailed analysis of the sample’s bibliographical characteristics, including the chronological order of publications, journal metrics, article type, and country focus. Our results reveal that the research field is dominated by Hofstede's cultural dimensions theory and that the majority of the sample articles explicitly mention or confirm the influence of national culture on MCS. We demonstrate that the cultural influences on a wide range of different MCS practices, tools and methods are examined, and show that a holistic and comprehensive analysis of the interplay of national culture and the elements of the MCS is mostly missing. Moreover, diverging research designs and contextual factors, different understandings of national culture and especially the often too superficial classification of national culture complicates and inhibits the comparability of the different results. Findings show that the underlying motivations and effectiveness of MCSs differ across national cultures, suggesting that MCSs require adaptation to different national cultures.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

When going international, companies engage in global sourcing, international production and sales markets and thus heterogeneous environments as manifestations of external contingency factors. One such external contingency factor is national culture (Otley 1980; Waterhouse and Tiessen 1978). According to contingency theory, firms have to adapt to contingency factors to be effective (Lawrence and Lorsch 1967; Waterhouse and Tiessen 1978), which suggests that organizations need to embrace cultural aspects to thrive. This applies as well to management control systems (MCS), which—in line with other organizational structures—need to match specific cultural contingencies.

Previous studies that address national culture as relevant contingency factor encompass a broad range of different themes, perspectives, and research questions under diverse theoretical lenses. While scholars largely agree that national culture impacts MCS (e.g., Azadegan et al. 2018; Brandau et al. 2014; Douglas et al. 2007; Granlund and Lukka 1998), results often exhibit a high degree of fragmentation and lack comparability due to the varying thematic foci, countries investigated, research designs, modes of data collection, or selected samples (Endenich et al. 2011). Consequently, while prior research shows diverging MCS across countries, insignificant and inconsistent results concerning the impact of national culture on these indicate that research is still at an early stage in explaining how culture influences MCS (Malmi et al. 2020) For instance, individual studies demonstrate mixed results concerning the reliance on certain performance measures in countries characterized by a comparable cultural background (Carmona et al. 2011 vs. Peterson et al. 2002). Similarly, results on the preference of certain reward systems in resembling cultures are different (Murphy 2003 vs. Awasthi et al. 1998 and Chow et al. 1994). Additionally, findings are sometimes in contrast to theory predictions (e.g., Chow et al. 1994; Merchant et al. 1995; Van der Stede 2003). This inconsistency and fragmentation of the research field clearly illustrates a research gap and thus calls for further research and a structured synthesis of extant literature.

To this date, there is no review that structurally and systematically analyzes findings on the interplay of national culture and MCS. Previous related reviews from Endenich et al. (2011) and Harrison and McKinnon (1999) only partially address national culture and MCS. Harrison and McKinnon (1999) emphasize cross-cultural research regarding MCS in the period from the 1980s to 1996 (20 studies in total) to identify methodological weaknesses within the research field. A later review by Endenich et al. (2011) covers 44 studies published between 1990 and 2010 identified in a systematic search of leading accounting journals (e.g., “Management Accounting Research,” “Accounting, Organizations, and Society”). None of the previous reviews used a database-driven approach but rather relied on a journal-based approach, which is prone to delimit the number of articles analyzed (Hiebl 2021). In contrast to the previous reviews, we draw on the holistic framework of MCS of Malmi and Brown (2008) for structuring extant research to enable a more integrated perspective on the impact of national culture on MCS. This way, our review aims to capture the complexity of the topic and contributes to a more comprehensive understanding of whether and how MCS are impacted by culture. Furthermore, by structuring extant empirical findings along this framework, we address the fragmentation of existing literature and offer an updated and evidence-guided synthesis on what we know and do not know about the impact of culture on MCS.

This review draws on a sample emerging from a systematic literature search in six different databases. It focuses on studies comparing MCS in two or more countries that illustrate cultural differences, with the aim to highlight past and current trends as well as to identify gaps in this research field. In this context, a systematic literature review offers several advantages over other review types (e.g., narrative reviews) due to observing certain principles, such as transparency, coverage, saturation, connectedness, universalism, and coherence, and therefore results in higher richness, reproducibility, trustworthiness, and utility (Simsek et al. 2021).

This literature review provides an aggregated overview of the impact of national culture on MCS and aims to identify and expose contradictions by highlighting current gaps, categorizing existing findings, and challenging underlying assumptions and theoretical foundations (Breslin and Gatrell 2020). Findings indicate that the number of publications has risen since the 1980s and suggest a positive trend for the future development of this research field. We provide detailed descriptive information about all sample articles, for instance about the article types, the underlying theoretical paradigms, and the country focus. Our paper demonstrates that national culture is highly relevant for MCS as a contingency factor, especially for internationally operating companies. Consequently, this systematic literature review fosters the understanding of a national culture’s influence on MCS, contributes to the structuring of the research field, promotes the comparability of findings and identifies a broad range of future research implications. In particular, the results show that effective and efficient MCS require embracing the conditions of the prevailing national culture.

The remainder of our paper is organized as follows: After the introduction, concepts of national culture and MCS are defined. This is followed by an explanation of the review methods applied for conducting a systematic literature review. The next two sections of our paper detail and explain the findings from the sample beginning with a descriptive analysis of the sample including an analysis of the publishing journal’s characteristics and chronological order of publications. The content analysis presents our findings along the framework of Malmi and Brown (2008). Finally, our review discusses the results and derives potential implications for future research to facilitate and promote scientific discourse in the research field.

2 Theoretical background

2.1 National culture

The concept of culture comes with various definitions: Kroeber and Kluckhohn (1952), for instance, analyzed more than 150 different culture definitions in 1952 and criticized the definitional complexity and multiplicity of the term culture which has not changed so far (Chen et al. 2012; Jahoda 2012; McSweeney 2002; Tian et al. 2018). “Definitions refer to various forms of culture, such as ideologies (beliefs, basic assumptions, and shared core values) and observable cultural artifacts (norms and practices)” (Chen et al. 2012, p. 52). Underlying reasons for the great variety of definitions include, for instance, the different uses of the term culture (e.g., consumer culture) (Jahoda 2012) and the intensive discussion in several research fields (e.g., business and management, anthropology, psychology) (Chen et al. 2012; Groseschl and Doherty 2000). One of the most cited definitions of national culture stems from Hofstede (1980, p. 25), who defines national culture as “the collective programming of the mind which distinguishes the members of one human group from another.” Following Hofstede (1980), culture refers to whole societies and/or nations and influences so-called subcultures (e.g., organizational culture, family culture).

Hofstede’s cultural taxonomy (Hofstede 1980) is among the most cited ones in the research fields of business and management (Fellner et al. 2015). Cultural differences are categorized along developed cultural dimensions: for example, Hofstede (1980) initially identified four dimensions (power distance, individualism, uncertainty avoidance, masculinity), added a fifth one (short-term vs. long-term orientation) (Hofstede 1991) and subsequently a sixth one (indulgence) (Hofstede et al. 2010). Furthermore, the so-called “Global Leadership and Organizational Behavior Effectiveness (GLOBE) study” by House, Hanges, Javidan, Dorfman, and Gupta (House et al. 2004) complemented Hofstede’s dimensions and presents nine different dimensions to explain cultural differences (House et al. 2004). GLOBE’s nine cultural dimensions, unlike those of Hofstede, are based on a practice score and a value score, which differ noticeably from each other (Grove 2005). For instance, gender egalitarianism was valued or desired by business people at a higher level than it was actually encountered in practice. The first dimension, power distance, used by Hofstede (1980, 1991) and House et al. (2004), describes how well members of a society accept the unequal distribution of power, meaning that in high power distance cultures, such as the Chinese or Latin American cultures, authorities are more readily accepted and less challenged. The second dimension, individualism vs. collectivism identifies the extent of interdependence, resulting in a range from highly individualistic cultures, in which individuals predominantly take care for themselves, compared to highly collectivist cultures, that focus on the wellbeing of society as a whole (Hofstede 1980, 1991). The Globe Study distinguishes this dimension into institutional collectivism and in-group collectivism. The former describes “the degree to which organizational and societal institutional practices encourage and reward collective distribution of resources and collective action” (House et al. 2004, p. 30), whereas the latter shows the extent of expression of pride, loyalty, and cohesiveness towards organizations or families by its members (House et al. 2004). “Although the concept of ‘face’ and ‘sense of shame’ is a human universal, it is particularly salient for more collectivist societies” (Chang et al. 2016, p. 180), and plays an important role in explaining the behavior of collectivist cultures such as China or Taiwan (Chang et al. 2016; Chow et al. 1997; Hofstede and Bond 1988). “Face” is based on the perception of others and is connected to one’s status. Losing “face” refers to a situation in which an individual fails to meet certain requirements, creating a feeling of shame (Ho 1976). The dimension uncertainty avoidance describes the degree to which society fears unknown and ambiguous situations and its coping strategies to avoid those (Hofstede 1980, 1991; House et al. 2004). Hofstede’s dimension, masculinity vs. femininity indicates what is motivational to a society. According to Hofstede, societies that clearly show a score on the masculine side of the scale value competition, achievements, and success, whereas societies on the feminine side of the range strive for quality of life and caring for others (Hofstede 1980, 1991). The Globe Study, on the other hand, uses the concept of gender egalitarianism to describe how societies create opportunities for all genders as well as the dimension of humane orientation to explain how much societies value altruistic behavior (House et al. 2004). With the dimension of assertiveness, the Globe Study also looks at the level of aggressiveness, in terms of how competitive and confrontational members of a society are and uses the dimension of performance orientation to describe how performance improvements are encouraged and rewarded (House et al. 2004). The dimension, long-term vs. short-term orientation or Confucian dynamism (Hofstede 1991; Hofstede and Bond 1998) or future orientation (House et al. 2004) defines how goals of the present and future are seen and evaluated. Long-term-oriented societies are prepared to dismiss short-term gains for long-term success. Short-term orientation focuses on the present or past. The last of the Hofstede dimensions that is not covered by the GLOBE study, indulgence vs. restraint is the degree to which people try to regulate their impulses and desires. Indulgent societies express relatively low control, whereas in restraint societies children are raised rulebound (Hofstede et al. 2010). Furthermore, interdependencies between the dimensions are seen. For example, power distance and individualism appear to be negatively correlated in many countries (Lau and Tan 1998), “i.e., a country low (high) on PD [power distance] would be expected to be high (low) on Individualism” (Douglas and Wier 2005, p. 163). Table 1 compares the mentioned cultural taxonomies briefly.

Measuring culture along taxonomies has long been criticized, especially Hofstede’s attempts to do so (Banai 2010; Baskerville 2003; McSweeney 2002). Both, methodology and measurements of cultural diversity are questionable, as nations are not deemed suitable to demarcate investigations from which to derive conclusions about homogeneous cultures (Baskerville 2003; McSweeney 2002). Furthermore, Hofstede’s (1980) approach of explaining cultural differences by merely investigating one internationally operating company and its subsidiaries is condemned (Banai 2010; McSweeney 2002). Even Hofstede’s cultural understanding is criticized: a classification and quantification of culture are, in general, questionable (Baskerville 2003) and Hofstede’s dimensions are insufficient and even outdated to demonstrate cultural differences (McSweeney 2002). Although Hofstede counters McSweeney’s critique by referring to the temporal stability of cultures (Hofstede 2002), cultural diffusion and dynamism cannot be denied (Baskerville 2003).

Despite all this criticism, the taxonomy of Hofstede appeared to be used by far the most in the investigated studies, and other cultural taxonomies used often complement Hofstede’s framework (see Sect. 4.2). Moreover, a recent study (Akaliyski et al. 2021) demonstrates that nations—although not the only factor that should be considered—are still meaningful units of analysis and can explain the bulk of variations in values once random and arbitrary variation at the individual level are eliminated through aggregation. For these reasons and because the GLOBE study complements Hofstede’s taxonomy, we draw on these two taxonomies to structure our findings.

2.2 Management control systems

Due to the varying definitions and conceptualizations (Anthony and Govindarajan 2007; Merchant and Van der Stede 2012; Simons 1995), there is no common understanding of MCS and this research field has a heterogeneous and fragmented nature (Berry et al. 2009; Günther et al. 2016; Strauss and Zecher 2013). In an attempt to enhance clarity and consistency in conceptualization, Malmi and Brown (2008) developed their framework by drawing on an intensive analysis of previous MCS literature (e.g., Chenhall 2003; Flamholtz et al. 1985; Simons 1995) and argue that “management controls include all the devices and systems managers use to ensure that the behaviours and decisions of their employees are consistent with the organisation’s objectives and strategies, but exclude pure decision-support systems” (Malmi and Brown 2008, p. 290–291). By conceptualizing MCS as a package, viewing controls in their entirety, not as isolated systems is emphasized. Their framework is categorized within five groups of controls: cultural controls, planning, cybernetic controls, reward and compensation, and administrative control.

Within the first category, cultural controls, Malmi and Brown (2008) refer to clan controls (Ouchi 1979), value-based controls (Simons 1995) and symbol-based controls (Schein 1997). Regarding clan controls, Ouchi (1979) emphasizes the importance of values and beliefs through rituals and ceremonies that individuals are exposed to as part of the socialization process within a social group (clan). Value-based controls refer to the values communicated by managers, which are considered fundamental within an organization (Simons 1995) and represent “values and direction that senior managers want subordinates to adopt” (Simons 1994, p. 34). Finally, symbol-based controls can be seen as an expression of visible controls of organizations (e.g., through dress codes or workspace design) (Schein 1997).

The second category, planning is regarded as a future form of control (Flamholtz et al. 1985) and involves setting goals and developing standards to meet them (Malmi and Brown 2008). While action planning usually refers to a period of up to twelve months and includes goals and actions that concern the immediate future, long-term planning mainly determines strategic goals and actions (Malmi and Brown 2008).

For explaining cybernetic controls, Malmi and Brown (2008) refer to Green and Wels (1988, p. 289), who define cybernetic controls as “a process in which a feedback loop is represented by using standards of performance, measuring system performance, comparing that performance to standards, feeding back information about unwanted variances in the systems and modifying the system’s comportment.” Following Malmi and Brown (2008) there are four types of cybernetic controls, namely budgets as well as financial (e.g., return on investment, economic value added), non-financial (e.g., information about product quality), and hybrid measurement systems (e.g., balanced scorecard). Reward and compensation controls compromise “motivating and increasing performance of individuals and groups within organisations by achieving congruence between their goals and activities and those of the organisation” (Malmi and Brown 2008, p. 293). In particular, extrinsic rewards possess a high relevance (Ittner and Larcker 2001) and can increase the individual’s effort invested and performance achieved (Bonner and Sprinkle 2002). Within administrative controls, Malmi and Brown (2008) point out governance structure (e.g., board composition, lines of authority and accountability) and organizational design (e.g., functional specialization) as well as policies and procedures (e.g., standardized procedures).

As this framework should improve the comparability of results as it draws on a very broad and encompassing understanding of MCS (Günther et al. 2016) and comprehensively maps the tools, systems and practices of MC and their potential linkages (Malmi and Brown 2008), we follow this framework in our study in line with other current systematic literature reviews (e.g., Günther et al. 2016; Traxler et al. 2020). In our systematic literature review, we consider only some subcategories of Malmi and Brown's (2008) MCS framework in correspondence with other literature reviews that draw on this framework (Günther et al. 2016; Traxler et al. 2020) as it is impossible to incorporate all sub-categories, because often the papers themselves do not clearly distinguish between these (Günther et al. 2016). Figure 1 presents the modified framework that is used for categorizing the findings of the analyzed studies.

Management control systems framework (adapted from Malmi and Brown 2008, p. 291)

3 Review methods

For conducting this systematic literature review we follow the methodology suggested by Tranfield et al. (2003). A systematic literature review follows a predetermined methodology or, in other words, observes rules that ensure “less bias and more transparency, accountability of execution and measures and techniques of validation and reliability” (Massaro et al. 2016, p. 792). According to Tranfield et al. (2003) a systematic literature review can be divided into three phases: (1) planning the review, (2) conducting the review, and (3) reporting and disseminating the review.

The first phase of a systematic literature review mainly involves the presentation of the underlying motivation (see Introduction) and the preparation of the review protocol, which documents all relevant steps (e.g., the in- and exclusion criteria). The second phase starts with defining the search strategy. We decided to rely on a keyword-based search process of several scientific databases in line with other literature reviews within the management accounting domain (e.g., Ndemewah et al. 2019; Pelz 2019; Sageder and Feldbauer-Durstmüller 2019; Wolf et al. 2020). Moreover, the in- and exclusion criteria were determined (see Table 2). We focused on empirical, English-language, peer-reviewed articles published in scientific journals including all articles published until December 2020 (the literature search was conducted in January 2021). Most importantly, in line with Endenich et al. (2011) only studies investigating national culture and MCS in two or more countries were considered as relevant for our systematic literature review. Moreover, we excluded conceptual-theoretical and literature-based conributions about national culture and MCS, articles investigating other cultural aspects, for instance, organizational culture, related topics such as financial accounting, finance, and auditing, contributions about non-profit-oriented ventures like municipalities, studies about joint ventures, and papers without a direct or indirect reference to cultural dimensions.

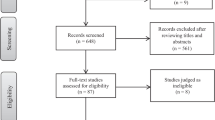

Afterwards, two key-word groups were defined that represented the selected definitions of national culture and MCS within our study and, most essentially, guaranteed identification of a broad range of articles eligible for our sample. Whereas the first keyword group (referring to national culture) only consisted of the term “culture”, the search for the second keyword group (MCS) was more complex. To include MCS and related terms (e.g., managerial accounting, budgeting) in our search process, we referred to the keywords used and identified by Ndemewah et al. (2019) in a current literature review. The two keyword groups were combined with the conjunction “AND”. Adding asterisks allowed us to search for different endings, like “culture” and “cultural,” resulting in the following search query: ("cultur*") AND ("management account*" OR "managerial account*" OR "management control*" OR "managerial control*" OR "control* system*" OR "budget*" OR "performance measure*" OR "performance evalua*" OR "cost account*" OR "cost manage*" OR "activity based manage*" OR "activity based cost*" OR "balanced scorecard*"). The selection of relevant databases was determined by the focus of our review (national culture and MCS), the in- and exclusion criteria (e.g., English-language studies), the possibility to apply the search query, and most essentially, the accessibility of the databases through our academic institutions. Finally, we searched titles, abstracts, and keywords (where applicable) for relevant studies in six scientific databases (EBSCO, Emerald Insight, ProQuest, Science Direct, Scopus and Web of Science). The search from January 2021 (see Table 3) resulted in 4449 matches. In the next step, we excluded duplicates (along the alphabetical order of the databases) and scanned the abstracts whenever the article fit the focus of our systematic literature review. Moreover, we read the full text of all articles whose content did not become clear in the abstract analysis. In total 4406 contributions were excluded, resulting in a final sample of 43 peer-reviewed articles that fit the scope of our review. The search process was accompanied by extensive deliberations by the authors; for inclusion or exclusion at least two authors had to examine the identified studies. However, final decisions were made by all four authors. Moreover, all steps and decisions were recorded in the review protocol. All included sample articles are marked with an asterisk in the references.

Following Kubíček and Machek (2018, p. 967) we “did not limit the results to any particular preselected class of journals” to capture innovative and unorthodox thoughts that might not be published in ranked journals. The descriptive information of the sample of our systematic literature review provides details on the journal metrics (according to the Academic Journal Guide (AJG) 2021 by the Chartered Association of Business Schools, JOURQUAL3 (JQ3) ranking from the German Academic Association for Business Research (VHB), and the Journal Impact Factors (JIF) from Thomson Reuters).

For the purpose of the content analysis, we used a coding scheme based on the MCS framework by Malmi and Brown (2008) and extracted relevant data through repeated reading. By determining analyzers and paraphrasing content passages, data was successively reduced and brought to a general level of abstraction, which formed the basis for the categorization of the findings. Findings were categorized along MCS clusters by at least two authors in order to enhance replicability. To ensure inter-rater reliability, every disagreement triggered a discussion for consensus. We refrained from calculating inter-coder reliability measures (e.g., Nili et al. 2017) as all measures are based on independent coders. Since all authors are working in the same scientific surrounding with the same scientific background/scientific school, they could not be regarded as independent coders. Moreover, we followed a structured process for analyzing the sample articles to avoid research bias. For the descriptive categorization of the studies (cross-sectional vs. longitudinal, quantitative vs. qualitative etc.) as well as the clustering of the findings of the investigated papers in terms of contents, we drew on a codebook to increase objectivity and replicability. For instance, we relied on codes for sub-clusters of the different control categories of the Malmi and Brown (2008) framework, deducted from literature. As suggested by Massaro et al. (2016), we strove for research validity following numerous steps. For the purpose of internal data validity, we analyzed the development of the research field over time (time series analysis) and used “pattern matching” (after every article analysis, findings were matched with comparable previous findings). To ensure external validity, we explained extracted and synthesized findings with theory (especially with the before mentioned cultural taxonomies and the MCS framework of Malmi and Brown 2008). Despite all these efforts, it has to be noted that subjectivity remains in a literature review, as all processes involved, starting from the selection of databases and keywords, the inclusion of papers and their coding to the presentation of findings are influenced by authors (see also the limitations in Sect. 6.3).

The third phase includes the actual report and its dissemination. We provide critical insights into the research field of culture and MCS. The synthesis, illustration and discussion of the findings from the identified, extensive literature sample based on our research framework offers a detailed overview of previous research and indicates future research avenues. Implications for future research are stated along the research framework to encourage scholars to engage in culture-related MCS research, as well as to facilitate and promote scientific discourse within this research field.

4 Descriptive analysis

4.1 Journal characteristics and publications timeline

Our sample of 43 articles spreads across 25 different peer-reviewed journals, which we categorized along their main theme, into three different categories: (1) accounting, (2) management and business, and (3) psychology journals. The vast majority of the articles (31) were published in 13 accounting journals, followed by the research fields of management and business (11 articles in 11 journals), and psychology (one in one). Regarding the scope of our review, we identified the journal “Accounting, Organizations and Society” with nine articles to be most influential, followed by “Management Accounting Research” (five articles), “International Journal of Accounting” (four) and “Advances in Accounting” (three). Most of the remaining journals merely contributed one article to our sample. Concerning journal rankings, only one journal (“IUP Journal of Management Research”) is not listed in the AJG 2021 or VHB JQ3 and does not possess a JIF 2020, whereas 19 of the journals feature in every ranking, two in two, and three in one. The quality of the included journals and articles indicates that culture-related research on MCS is highly relevant, especially when considering the journal rankings (see Table 4).

The first article (and the only one from the period 1986–1990) of our sample was published in 1988 (Birnberg and Snodgrass 1988). Until December 2020 there is an increasing trend in the number of publications (albeit inconsistently and irregularly). 19 articles were published before the turn of the millennium and 24 afterwards. The positive trend in the chronological order of publications may be another indicator of the high relevance of the research field. However, this positive trend has to be interpreted against the background that publications generally increase over time. Figure 2 and Table 4 provide detailed information about the journal characteristics and timeline of publications.

Chronology of publications

4.2 Article characteristics

Tables 5 and 6 summarize the results of the bibliographical analysis (e.g., article type, data collection, sample information). Most of the sample articles (38) are empirical-quantitative, whereas 7 articles are empirical-qualitative. Two studies apply both, empirical-qualitative and quantitative, research designs. 29 cases choose surveys as their data collection mode, followed by other modes (19) (e.g., experiments) and interviews (7). In total, 41 papers feature cross-sectional and only two longitudinal findings. The sample articles, moreover, show great variation in sample number, participants and investigated industry. Included data stem from varying numbers of countries, ranging from two (e.g., Murphy 2003) to 39 countries (Kitching et al. 2016). In total, 50 countries are investigated. Among the most closely examined countries are the USA (26), Australia (13), Singapore (nine), Taiwan (seven), Germany (six), Japan (six), and Mexico (five). The number of investigations of other countries lies between four and one. However, in most cases developed countries are explored, for instance the USA, Australia and Japan, as well as Western European nations. Studies about or including developing countries are in the minority; only 19 studies deal with developing countries.Footnote 1

Regarding cultural studies, 40 articles apply Hofstede’s definition of culture or refer to his cultural dimensions (see Table 5). The usage of other cultural taxonomies, for instance the GLOBE study (Malmi et al. 2020), Trompenaars (Tallaki and Bracci 2015) or the concept of “face” (Chang et al. 2016; Chow et al. 1997, 1999; Douglas and Wier 2005) are sparse within the sample, and often complement Hofstede’s taxonomy. Birnberg and Snodgrass (1988) do not make a clear reference to a cultural dimension, they explicitly refer to a set of norms and values for their underlying national cultural understanding. In addition, their statements often refer to a collectivist orientation of Japanese culture, even if no direct reference is made to the cultural dimension of collectivism, for instance “Japanese worker comes to the job prepared to consider the implications of his actions for the welfare of other members of the organization” (Birnberg and Snodgrass 1988, p. 450). Additional theoretical paradigms (besides culture) are often missing. Exceptions are for example agency theory, contingency theory, prospect theory, and upper echelon theory.

5 Review findings and analysis

5.1 Cultural impact on MCS and assignment of findings

In total, the vast majority of investigated contributions (40) explicitly state and confirm that MCS are influenced by national culture. Only the remaining three articles (Lau and Tan 1998; Lau et al. 1997; Leach-López et al. 2008b) cannot confirm the influence of national culture on MCS. However, all of these last three papers do not explicitly negate the impact of culture on MCS but rather explain the missing significant influence of national culture with the particularity of their sample (Leach-López et al. 2008b) or argue that opposing effects of certain cultural dimensions neutralize the impact of national culture on the investigated management control practices in the analyzed countries (Lau and Tan 1998; Lau et al. 1997). Consequently, the vast majority of studies point to the importance of considering national culture in the design and adaption of MCS.

Figure 3 illustrates the attribution of the sample articles to the management control clusters of the framework. It is noticeable that the cultural controls cluster contains the fewest with two and the budgets cluster with 20 studies by far the most attributions. The other clusters contain results from 14 (administrative controls), ten (financial, non-financial and hybrid measurement systems as well as reward and compensation) and nine studies (planning). Moreover, the vast majority (29) only considers one management control cluster in their analysis, followed by seven papers that cover two elements, six papers that cover three clusters, and only one case study (Tallaki and Bracci 2015) that addresses four different elements of the framework. No analyzed paper covers all different management control clusters of the framework of Malmi and Brown (2008). Furthermore, the examination of the 43 papers revealed that on average 1.5 MCS elements are used in the studies to explain the effect of culture on MCS.

Journal articles attributed to management control clusters

5.2 Cultural controls

Concerning cultural controls, the content analysis reveals that cultural dimensions have an influence on the design and type of value-based controls.

-

According to the Globe Study (see Sect. 2.1) the Nordic cluster of Scandinavian countries is characterized by lower scores on assertiveness and performance orientation, compared to the Anglo or Germanic cluster, which results in the preference of feminine values and relational employment (Malmi et al. 2020). When selecting employees, firms of the Nordic cluster, therefore, search for individuals whose values are closely aligned to those of the organization. Hence, value-based employee selection is expected to be particularly effective when paired with authority delegation in such a cultural environment. While delegation is thus complemented by employee selection in Nordic firms, the correlation between delegation and employee selection as a value-based input control is insignificant in the Anglo and Germanic cultural regions.

-

One qualitative analysis of German headquarters and their Chinese subsidiaries (Kornacker et al. 2018) indicates that values and corporate culture may be transferred through expatriates to socialize host country employees in the headquarters’ culture in order to ensure the application of certain MCS. The study demonstrates that German headquarters send expatriates to China to solve the tension between the high German emphasis on budget control structures and the absence of corresponding budget control practices at the subsidiaries. The delegated expatriates that serve as “mediators”, “instructors” or “link to the HQ [headquarters]” (Kornacker et al. 2018, p. 37) should broaden the understanding of the German practices among Chinese employees. This way, the expatriates serve as a form of cultural control and should ensure that the Chinese managers eventually socialize with the headquarters’ values in order to reproduce the imposed budget control structures in alignment with the overall strategy.

5.3 Planning

The content analysis of the papers reveals several aspects of how culture impacts the design of planning. First, cultural traits influence the time horizon of planning.

-

Individualistic cultures appear to put more emphasis on short-term planning and favor short-term financial outcomes while collectivist cultures favor long-term, balanced success (Harrison et al. 1994; Carmona et al. 2011). Often, long-term-oriented decisions involve the sacrifice of short-term profits in order to gain long-term benefits. It appears that such situations are more readily accepted by individuals from collectivist societies (Harrison et al. 1994). Moreover, collectivist cultures promote one’s interdependence with others and therefore tend to adopt a long-term and pluralistic perspective, which is reflected in the preference for projects aligned with long-term, balanced success (Carmona et al. 2011). However, a comparison of planning practices between Japan and the USA (Ueno and Sekaran 1992) was unable to confirm longer planning horizons for the collectivist, high uncertainty avoiding Japan.

-

High Confucian dynamism involves greater orientation towards the future. Hence, countries, such as Singapore or Hong Kong, scoring high on Confucian dynamism are more willing to sacrifice short-term performance for long-term benefits (Harrison et al. 1994).

Cultural differences also impact the type of planning firms use. Eastern cultures that score high on Confucian dynamism draw on synthetic thinking while Western cultures with their analytical thinking emphasize the use of quantitative techniques in planning. One quantitative study finds evidence for a greater usage of quantitative planning techniques in Australia and the USA, in contrast to Singapore and Hong Kong (Harrison et al. 1994).

Participation in planning appears to be another area that is determined by cultural preferences.

-

Low power distance and high individualism seem to promote participation in planning. Findings from a case study of two Italian companies with subsidiaries in Morocco (Tallaki and Bracci 2015) show that in both investigated parent companies goal setting is consultative, with all subordinates participating in the process (explained by the low power distance and high individualism of Italy). In the Moroccan subsidiaries, which are characterized by high power distance and collectivism, either an authoritarian approach is taken with the subordinates executing orders, or a consultative approach that is imported from the Italian parent company is adopted. The latter includes aspects of collaboration and consultation (elements transferred from the parental approach) as well as a pronounced hierarchy with a powerful CEO who has the final say (elements of local MCS). In a comparable scenario, an experiment among Mexican and US students (Murphy 2003), Mexican participants are expected to prefer top-down planning as a result of their higher power distance culture. Findings, however, do not provide support for this hypothesis, revealing that both groups have a slight preference for participative planning.

-

Culture may influence the interdependence between participation in planning and other elements of MCS. Given that planning is of great importance in uncertainty avoidance cultures as structuring activities, standardizing rules and procedures as well as detailed and well-defined plans reduce uncertainty and help cope with the inconvenience caused by the unknown, the participation in planning should increase the benefits of delegation in societies characterized by high uncertainty avoidance (Malmi et al. 2020). First, participation strengthens the alignment between subordinate decision-making and company objectives. Second, delegating responsibility to subordinates makes them more willing to share information. Both effects result in greater consensus and clarity on the goals. In a culture with lower uncertainty avoidance, it is not necessary to involve subordinates in planning to offset the increased uncertainty placed upon employees by delegation. In an empirical survey (Malmi et al. 2020) comparing MCS in Germanic and Nordic regions (both characterized by high uncertainty avoidance) and Anglo cultures (with low uncertainty avoidance) the complementary nature of delegation and planning participation in Germanic and Nordic cultural regions is confirmed. However, while there is no significant correlation between delegation and strategic planning in the Anglo countries, there is a positive and significant correlation between delegation and action planning participation. This indicates that delegation and action planning are complements in all investigated Western cultural regions and may form a set of “best practices” applicable in all these cultural regions.

Planning does not only involve setting goals but monitoring them as well. Therefore, actions that ensure the achievement of set goals are an important element of planning. In this regard, culture appears to determine the reaction to deviations from the goals set. This is confirmed in a survey involving data from 39 countries that investigates cultural influence on managerial reactions to declining sales (Kitching et al. 2016). Managers from countries with a high degree of uncertainty avoidance are mostly loss averse and therefore react to sales downturns by cutting costs more aggressively, resulting in less cost stickiness. Generally, and when receiving favorable information, Taiwanese managers (characterized by a higher level of uncertainty avoidance) are expected to be more anxious when facing the uncertainty of the future and are thus more risk-averse and less willing to continue projects than their US counterparts (Chang et al. 2016).

The dominating characteristic of the long-term orientation is the thriftiness of managers. Thrifty managers are more likely to cut costs when sales decline, resulting in less cost stickiness (Kitching et al. 2016). Firms in more masculine societies seem to be less reluctant to terminate employees compared to more feminine societies. Hence, they display a greater willingness to cut costs during periods of sales declines, which results in less cost stickiness.

In high power distance cultures, empire-building behavior is expected to be more prevalent inducing powerful managers to hold excess resources and thus increasing cost stickiness. While the relation between power distance and cost stickiness is as expected in the empirical tests in 39 countries, the effect of power distance on cost stickiness is not significant (Kitching et al. 2016). Similarly, individualism does not affect cost stickiness. This might be explained by the fact that the two channels through which cost stickiness is impacted cancel each other out: On the one hand, individualistic managers are less concerned about terminating employees, but on the other hand, they are more inclined to build empires.

An emphasis on “face” is typical for the Chinese, Taiwanese and other collectivist cultures (Chang et al. 2016; Chow et al. 1997). As a result of the higher collectivism of Chinese/Taiwanese, decision-makers are more willing to continue certain courses of action, even if adverse signals are apparent in order not to admit failure that goes along with a damage of “face” (Chang et al. 2016; Chow et al. 1997). Hence, relative to US managers, Taiwanese are more willing to continue projects despite receiving unfavorable information, especially when the project nears completion, as they are more concerned about “saving face” than avoiding uncertainty in such a situation (Chang et al. 2016). The concept of “face” also influences resource allocation decisions after a project has started. Collectivist Taiwanese managers allocate more funds to complete an ongoing project than do their individualist US counterparts as they are more concerned about the adverse effects the non-completion of a project could have on their reputation (Chang et al. 2016). Similarly, another study confirms that Chinese as opposed to their US counterparts are more likely to continue an unprofitable project by investing additional resources (Chow et al. 1997).

5.4 Cybernetic controls

5.4.1 Budgets

Concerning budgets, several cultural dimensions impact the preference, prevalence and effects of participation in the budgeting process.

-

Low power distance seems to foster participation in the budgeting process (Brandau et al. 2014; Douglas and Wier 2005). In contrast to higher power distance cultures, participation is expected to be met with positive reactions in low power distance countries (Douglas and Wier 2005). Consequently, several studies observe a higher degree of participation in the investigated low power distance cultures compared to high power distance countries (Brandau et al. 2014; Douglas and Wier 2005; Tallaki and Bracci 2015).

-

Given that power distance and individualism appear to be negatively correlated in many countries (see Sect. 2.1), it is found that the effect of participation coincides in low power distance, high individualism cultures as well as high power distance, low individualism societies (Harrison 1992; 1995; Lau and Tan 1998) as the positive impact of participation that goes along with low power distance or low individualism on the one hand, is neutralized or offset by its negative effects resulting from high power distance or high individualism on the other hand (Harrison 1992; Lau and Tan 1998; Lau et al. 1997). When increasing levels of budget emphasis are matched with increasing levels of participation, it is concomitant with lower job-related tension in both investigated societies and not associated with job satisfaction in either culture (Harrison 1992, 1995). Consequently, budget participation appears to level out cultural differences: in individualistic cultures participation helps compensate negative reactions associated with budget emphasis, while in collectivist countries participation and budget emphasis act synergistically (Harrison 1995). The same applies to the impact of the interaction between budget emphasis, budgetary participation and task difficulty on managerial performance, which is found to be unaffected by the investigated combinations of cultural dimensions (low power distance, high individualism vs. high power distance, low individualism) (Lau and Tan 1998).

-

More recent quantitative studies (Leach-López et al. 2007, 2008a; 2008b) comparing US managers working in the US and Mexican managers working for US-controlled maquiladoras in Mexico reach inconclusive results concerning the cultural effect of budgetary participation on performance. Two studies (Leach-López et al. 2007, 2008b) find budgetary participation to improve performance for both US managers and Mexican managers and thus no cultural effect. Sample particularities are expected to account for this missing cultural effect as the participating Mexican managers work for US-controlled companies and may therefore exhibit cultural traits more similar to the USA (Leach-López et al. 2008b). Moreover, the causal mechanisms that link budget participation to performance are different between the US and Mexican managers, partly because of the Mexicans’ higher uncertainty avoidance and preference for group decisions (Leach-López et al. 2007). Similarly, the third study (Leach-López et al. 2008a) identifies no significant differences in the levels of participation, the desired participation and the level of budgetary participation conflicts that stem from deviations of the experienced participation level from the desired level between US and Mexican managers. However, budgetary participation conflicts appear to impair performance much stronger in Mexico. This finding is explained by Mexican managers’ higher score on uncertainty avoidance and long-term orientation and their lower individualism.

-

Comparing Chinese and Western managers, another quantitative study verifies that the interaction effect of management accounting systems and budgetary participation diverges as a result of the different cultural backgrounds. While for the collectivist, large power distance and long-term oriented Chinese managers the relationship between management accounting systems information and performance is negative for high levels of participation, the relationship is positive for high levels of budgetary participation among Western managers (Tsui 2001).

Budget emphasis, “the extent to which the evaluation of managerial performance is primarily based upon the business-unit managers’ ability to continually meet the budget on a short-term basis” (Van der Stede 2003, p. 266) appears also to be impacted by the cultural background of the actors involved. While only one study is unable to confirm a significant influence of national culture on the importance of budgets in performance evaluation (Van der Stede 2003), others find support for the notion that national culture predicts the importance of budgeting (Graham and Sathye 2018) and that budgeting is particularly entrenched in certain cultures such as the US or Germany (Collins et al. 1999; Kornacker et al. 2018). Higher budget emphasis appears to be related to lower job-related tension and higher job satisfaction in high power distance, low individualism cultures, while low reliance on budgets in evaluation is associated with lower tension and higher job satisfaction in low power distance, high individualism countries (Harrison 1992, 1993, 1995). While it seems more important in low power distance countries to balance budget emphasis with other, also individual performance indication criteria and providing the opportunity for subordinates to be consulted, which goes along with a low budget evaluative style, subordinates from high power distance societies are not going to be, nor expect to be consulted in performance evaluation. Instead, the superior evaluates unilaterally and autocratically. Therefore, subordinates prefer and react favorably to an objective performance measurement such as budgets (Harrison 1993, 1995). The preference for higher budget emphasis also results from collectivism. The concern of collectivist subordinates to be compared with others is accommodated by relying on standardized and quantified measures such as budgets, while individualistic subordinates prefer individual evaluations (Harrison 1993). Regarding the interaction between budget emphasis, budgetary participation and performance, two quantitative studies (Lau and Tan 1998; Lau et al. 1997) cannot identify a significant effect of national culture. Instead, managers seem “to perform better under high budget emphasis regardless of culture” (Lau et al. 1997, p. 192).

Incentives for and the behavior to create budgetary slack also vary among different cultures. High uncertainty avoidance countries should be more prone to create slack in order to protect themselves against future uncertainties (Douglas and Wier 2005; Mohanna and Sponem 2020). In individualistic cultures managers feel the urge to create slack to ensure that extra resources become available, and the budget is easily achievable (Ueno and Sekaran 1992). On the other hand, the “concept of face” would discourage budgetary slack creation as it is seen as shirking and misrepresentation (Douglas and Wier 2005). A comparison of US and Chinese managers identifies higher slack creation incentives for US managers but no difference in actual slack creation behavior (Douglas and Wier 2005). Comparing slack creation behavior between the individualistic USA and highly uncertainty avoiding Japan, US managers show a more pronounced tendency to embrace budgetary slack, which is explained by the greater influence of individualism on slack creation behavior (Ueno and Sekaran 1992). Moreover, different rationales appear to impact slack creation behavior. While the investigated US managers’ slack creation behavior increases as incentives increase and decreases as idealism increases, only the incentives affect Chinese managers’ slack creation behavior (Douglas and Wier 2005). Another quantitative study in France and Morocco confirms that the cultural dimensions of individualism and uncertainty avoidance influence the propensity to create slack and therefore the effectiveness of certain budget design mechanisms to counteract slack creation (Mohanna and Sponem 2020). In the collectivist, low uncertainty avoidance culture of Morocco, budget formalization decreases the propensity to create slack as it helps managers to understand budget rules and procedures and thus provides additional information on how to achieve the set organizational goals. However, formalization has no effect in the individualistic, high uncertainty avoidance society of France. Instead, controllability that requires the selection of performance measures that only contain elements that can be influenced to a certain degree by managers, decreases the propensity to create slack in France but has no effect in Morocco. Controllability reduces risk as only controllable factors are considered in performance evaluation, which is important for uncertainty avoiding managers and it also assures that managers are not held accountable for their colleagues’ actions, which is important for individualistic managers.

Investigating the difference in applied tactics (budget game repertoires) to obtain one’s desired budgets between the USA and Latin America, a quantitative study demonstrates that US Americans are more likely to enact devious games that are characterized by a non-straightforward, politicized approach to further their own interests and explains this finding with the pronounced individualism of the USA (Collins et al. 1999).

Relying on the concept of machism, “a sense of ‘masculine pride’ evidenced by an exaggerated awareness of assertion of masculinity” (Collins et al. 2005, p. 142), the impact of different macho stereotypes (chauvinistic, classic, and aggressive) on budgeting procedures is investigated between the USA and Latin America in a quantitative study. US respondents demonstrate a significantly higher, risk-seeking behavior in budgeting explained by the more widespread aggressive machos (dominant, penetrating, strong-voiced, agressively imposing his will on others) in the USA. In contrast, Latin Americans who are more likely chauvinistic (fearless, aggressive with women) or classic machos (personal responsible, self-reliant, upholding the integrity of their group) appear to follow budget procedures more likely and in the case of classic machos accept budget responsibility more likely.

Cultural traits also influence the detail of information required for budget reviews. A quantitative study of Belgian headquarters with subsidiaries in Western countries (Van der Stede 2003) finds business unit managers of high power distance countries to tolerate or even honor more budgeting information detail out of respect for corporate management as a reflection of their high power distance culture. Similarly, more budgeting information is preferred to avoid uncertainty. Contrary, business units in countries with high individualism rely on less detailed budgeting processes. Similarly, a multiple case study of the budgeting processes of German headquarters and their Chinese subsidiaries (Kornacker et al. 2018) shows that some German headquarters compromise on budget accuracy and level of detail in order to increase the utility of the global budget control structure in the more volatile Chinese contexts and in correspondence with China’s low uncertainty avoidance.

In addition, national culture also impacts budget-related communication and coordination. Business-unit managers in high power distance or high uncertainty avoidance cultures accept or even seek more interference by corporate management in business-unit affairs. In contrast, budgeting processes appear to be more hands off when dealing with managers in individualistic cultures (Van der Stede 2003). However, given that individualistic managers are more likely to be self-interested trying to maximize their individual gains, organizations need to resort more to extensive communication and coordination mechanisms in order to ensure the achievement of the organization's goals. This higher reliance on extensive formal communication and coordination in the budget planning process in individualistic societies is confirmed in a quantitative study comparing the individualistic USA and the collectivist Japan (Ueno and Sekaran 1992).

More risk-averse cultures (as a consequence of their Muslim background) such as Indonesia are found to adopt more sophisticated capital budgeting systems (in comparison to Australia) to moderate uncertainty (Graham and Sathye 2017, 2018).

5.4.2 Measurement systems

Regarding the preference for measurement systems, individualistic cultures seem to assign more importance to financial measures (Carmona et al. 2011, 2014). Findings from quantitative experiments between US and Spanish students testing the response to a balanced scorecard initiative (Carmona et al. 2011) and investigating differences in performance appraisals (Carmona et al. 2014) demonstrate that financial dimensions are more important to the individualistic US participants compared to the more collectivist Spanish students. Similar findings from another quantitative study conducted in Indonesia, a Muslim country with high collectivism, indicate that non-financial information (e.g., product quality, synergies, suppliers) possesses a higher relevance compared to Australia (Graham and Sathye 2018).

The different cultural dimensions also influence the design of cybernetic controls.

-

A higher degree of individualism seems to be associated with a greater supply of traditional financial information (e.g., cost control information). The results of a quantitative comparison of Australia and Korea (Choe 2004) show that in countries with a high degree of individualism (here Australia) a higher amount of financial information is provided as these financial measures are regarded as individualism-oriented information and maximize organizational success through individual performance achievements.

-

The qualitative results of Brandau et al. (2014) indicate that a higher degree of Confucian dynamism and uncertainty avoidance within the Brazilian culture (compared to the German culture) implies a stronger long-term orientation of performance measures.

-

Similar results are obtained from a quantitative comparison between Japan and the USA (Ueno and Sekaran 1992), which proves a significantly higher reliance on long-term evaluation time horizons of Japanese as a manifestation of the preference for collectivist outcomes that provide shared benefits but require a longer time span to become noticeable. In line with this, a more recent comparison between the USA and Spain (Carmona et al. 2011) shows that in the more collectivist culture of Spain projects are chosen that promise long-term benefits. However, a further quantitative study is unable to confirm these results (Peterson et al. 2002): Comparing Eastern (here Japan) and Western national cultures (i.e., USA, Western European countries) there are no significant differences between Japanese and US companies regarding the short- and long-term orientation of performance measures although the Japanese culture has a higher degree of Confucian dynamism.

-

Contrary to predictions, one qualitative study (Merchant et al. 1995) is unable to confirm that greater power distance and uncertainty avoidance influence the subjectivity of performance measures. Findings do not prove that within companies of the Taiwanese culture (which is higher on power distance and uncertainty avoidance) the subjectivity of performance measures is greater than within their US counterparts.

National culture also influences the effectiveness of cybernetic controls.

-

In a strong uncertainty avoidance culture financial performance measures seem to be more effective. This is highlighted in a comparison between Korea and Australia (Choe 2004) that demonstrates positive impacts of financial information on the production performance of Korean companies due to their strong uncertainty avoiding culture, which in turn leads to a greater information demand for financial information to cope with this uncertainty. No such positive effect on manufacturing performance is found for the Australian companies.

-

Further, quantitative results from Australia and Singapore indicate that power distance and individualism influence subordinates’ response to objective performance measures such as accounting performance measures and budgets (Harrison 1993). In detail, a high reliance on financial accounting performance measures and budgets in evaluation is associated with lower tension in a high power distance and low individualism society (Singapore) as these objective performance measures attenuate the unilateral and autocratic evaluation of the superior, while low reliance, that also allows individual performance indication criteria, is associated with lower tension in the low power distance and high individualism society of Australia (see also Sect. 5.4.1).

-

Moreover, a quantitative study between US and Australian managers (Chan 1998) on the impact of accountability and performance measurement on the outcome of negotiations confirms the influence of the cultural dimension of long- versus short-term orientation. While Australian respondents exhibit a culturally determined increased long-term orientation (compared to their US counterparts) and therefore interpret their accountability to superiors as a request for more integrative outcomes leading to more concern about accommodating their negotiating partner, the short-term orientation of the US culture results in higher accountability being understood as a request for better individual outcomes in the form of higher profits.

5.5 Reward and compensation

National culture influences the preference for, the determination of, and the effects of reward and compensation controls. Quantitative experiments among students provide mixed results concerning the preference for rewards. While one experiment (Murphy 2003) shows that the individualistic US students prefer individual to group rewards and that collectivist Mexican students have a higher preference for group rewards, this could be neither confirmed in a comparison between Japan and the USA (Chow et al. 1994), where the less individualistic Japanese have no significantly higher preference for group rewards, nor among US and Taiwanese students (Awasthi et al. 1998), where the individualistic US students demonstrate a higher preference for team-oriented payment, which may be explained by US students’ greater concern about the dysfunctional effects of individualism on teamwork that made them choose countermeasures to limit its influence.

Moreover, national culture influences the determination of incentives:

-

In national cultures with a higher degree of Confucian dynamism and collectivism, short-term and individual incentives are of subordinate importance. Nevertheless, a qualitative study (Merchant et al. 1995) shows that Taiwanese managers, unlike their US counterparts, are less frequently using incentives based on long-term performance measures (i.e., longer than one year), which may be interpreted as less need for promoting a long-term perspective due to the higher degree of Confucian dynamism in Taiwan. Higher collectivism leads Taiwanese managers to reject a focus on individual short-term goals for the good of the company's success.

-

Power distance and collectivism influence the amount of discretion in determining incentives. In high power distance cultures bonuses are increasingly based on discretionary in contrast to formula-based factors. The higher the power distance of a country (e.g., the respect shown to superiors), the greater is the discretionary determination of incentives (Van der Stede 2003). This is also reflected in two case studies of Italian companies with subsidiaries in Morocco (Tallaki and Bracci 2015). While one case firm transfers the results-based bonus system (originating from the Italian culture of low power distance and high individualism) to Morocco without considering the Moroccan cultural characteristics, in the other case firm the bonus system of the parent company in Italy is based on the company’s performance but the bonus system of the Moroccan subsidiary, on the other hand, is very subjective and based on the discretion of the Moroccan CEO, because of the high power distance and the strong collectivism of the Moroccan national culture.

Several studies highlight the impact of national culture on the effectiveness of reward and compensation:

-

A case study on the MCS of German headquarters and their Chinese subsidiaries (Kornacker et al. 2018) shows that the cultural dimension of masculinity impacts the linkage between budgets and incentives. Chinese subsidiaries that dedicate themselves to budget control have several common features, such as the linkage between budget targets and financial incentives. Such linkage could be interpreted as “an additional driver of abstract trust in light of the high masculinity in China” (Kornacker et al. 2018, p. 40). In this context, the low level of identification of Chinese employees with the company and the high willingness to change employers in the case of financially more attractive offers are particularly worth mentioning. The effect of this linkage is to increase both, employee loyalty and budget adherence (Kornacker et al. 2018).

-

Several experiments among students investigate the effectiveness of individual vs. group rewards in individualistic vs. collectivist countries. When short-term success builds the basis for the reward system, individualistic US students have a greater preference for short-term profitable projects than their more collectivist Spanish counterparts (Carmona et al. 2011). Comparing Taiwanese and US students (Awasthi et al. 2001) the adoption of a more team-based pay structure does not lead to a more collectivist orientation among the collectivist Taiwanese respondents, while the adoption of a more individualistic pay structure leads to a shift away from collective interest among the individualistic US respondents. Furthermore, US students (high individualism and low power distance culture) working under imposed pay structures show higher levels of dissatisfaction than compatriots working under self-selected pay structures, while no negative effects could be observed with Taiwanese students in this case due to their low individualism and high power distance culture. Investigating the influence of MCS and national culture on manufacturing performance (Chow et al. 1991), no increased performance within the low individualistic culture of Singapore could be found when interdependencies between a group of workers exist. However, when there is no pay dependency between a group of workers, those from the low individualistic culture of Singapore perform better than those from the highly individualistic US culture. On the contrary, workers from the highly individualistic USA do not perform better with either independent workflow or pay. The results suggest that MCS vary in effect in different cultures (although this is neither confirmed nor refuted).

5.6 Administrative controls

In terms of administrative controls, national culture influences organizational structure and design.

-

High power distance cultures appear to put more emphasis on the cognizance of the status of the superior by their subordinates (Chong 2008; Chow et al. 1999). Hence, subordinates in such cultures are more open to receiving directives from their superiors (Chow et al. 1996). As a result, top-down implementations of new MCS in a high power distance culture, such as Malaysia, are more accepted and therefore generate less resistance and defensiveness (Brewer 1998).

-

National culture also influences how successful the implementation of a new MCS, such as activity-based costing (ABC), is. ABC focuses on cross-functional teamwork. Its implementation is found to be less successful in the highly individualistic US – compared to collectivist Malaysia – in a quantitative study (Brewer 1998) as the implementation of a team-based work arrangement is considered a threat to individual accountability and autonomy preferred by individualistic employees. As a consequence, they meet the implementation of ABC with more defensiveness, which in turn diminishes implementation success.

-

Tight controls appear to be less related to dysfunctional behavior in collectivist cultures, such as Japan, as managers are less short-term oriented or prone to manipulations (Chow et al. 1996).

Additionally, national culture influences how decisions are made and where responsibilities are centered.

-

Countries scoring high on individualism tend to emphasize individual decision-making, as well as autonomy (Brewer 1998; Graham and Sathye 2017; Harrison et al. 1994), whereas, collectivist cultures, such as Singapore or Hong Kong, favor group-centered decision-making (Harrison et al. 1994). Collectivist cultures also try to make decisions unanimously through discussion with all members to maintain social harmony, as accommodating everybody’s point of view is important (Graham and Sathye 2017).

-

Low power distance and individualistic cultures are also found to put more emphasis on decentralization, while high power distance and collectivist cultures favor centralization (Harrison et al. 1994; Tallaki and Bracci 2015). Responsibility centers are therefore more widespread in high individualism, low power distance cultures as this “reflects the choice to devolve decision autonomy” (Harrison et al. 1994, p. 249). Furthermore, decentralization is an organizational mechanism that promotes discretion, and individual autonomy goes along with an equal distribution of power. Low power distance cultures, such as the US or Australia, reject unequal distribution of power and therefore, favor decentralized decision-making (Harrison et al. 1994). On the contrary, high power distance cultures, such as Morocco, are characterized by a greater respect for people who hold authority. Paired with ties of respect and obedience as a reflection of collectivism, centralization appears to be the appropriate organizational structure as decentralization is considered as a loss of power (Tallaki and Bracci 2015).

-

Similarly, cultural differences affect the way authority delegation interacts with other elements of the MCS. In the Anglo cultural region, characterized by its individualism, authority delegation and incentive contracting are complements, as members of this cultural region prefer greater autonomy and discretion in their decision-making. Furthermore, combined with incentive compensation, authority delegation is considered an opportunity for individual initiative and achievement. For the more future-oriented Germanic and Nordic regions delegation and incentive contracting act as independent practices, as individuals are more risk-averse and less motivated by extrinsic rewards (Malmi et al. 2020).

Other administrative controls, that are impacted by cultural differences, are policies and procedures.

-

Highly collectivist cultures are believed to place collective interest over personal interest, which suggests less formal control would be needed (Birnberg and Snodgrass 1988; Chow et al. 1996). While one study, analyzing Japanese and US companies, concludes that less bureaucratic procedures are required in Japanese firms due to their hierarchical structure and more informal way of enforcing MCS (Birnberg and Snodgrass 1988), another confirms the contrary, namely significantly tighter controls among the Japanese (Chow et al. 1996).

-

Furthermore, higher uncertainty avoidance fosters the reliance on procedural controls, as they are perceived as more desirable (Chow et al. 1996).

-

National culture is also shown to influence the degree of formalization in an organization. High power distance and uncertainty avoidance cultures seem to prefer a higher degree of formalization (Brandau et al. 2014; Chow et al. 1994; Harrison et al. 1994; Murphy 2003; Tallaki and Bracci 2015), although differences between investigated countries show no significance in several quantitative studies (Harrison et al. 1994; Murphy 2003). A comparison between Brazilian and German companies demonstrates that the high power distance culture of Brazil relies heavily on formal information, as formalization provides rules for information flows and guidelines for the behavior of employees (Brandau et al. 2014). Furthermore, a case study of Italian companies and their Moroccan subsidiaries (both countries scoring high on uncertainty avoidance) finds that formalization helps risk-averse individuals to better cope with uncertainty (Tallaki and Bracci 2015).

-

A quantitative study (de Waal and de Boer 2017) in four different cultures (Austria, Finland, India, and Russia) examines the influence of national culture on the design of MCS for project management. High uncertainty avoidance leads employees to expect the standardization of processes, whereas the collectivist orientation of a culture results in an increased expectation of equality, which in turn is promoted by standardization. Although national culture influences organizational elements of MCS such as standardization, the organizational culture of multinational companies neutralizes its influence in this study.

National culture also influences the way how information is shared, communication is structured, and collaboration is organized.

-

Communication tends to be less open in high power distance and low individualistic cultures, such as Singapore, compared to low power distance and highly individualistic cultures, such as the USA (Chong 2008). Furthermore, US managers are shown to use more people-oriented communication, in terms of setting goals, listening and organizing, as well as giving clear information. While managers from individualistic, low power distance countries such as the USA are expected to communicate unbiased information to influence others’ thoughts and actions, managers from collectivist, high power distance societies, such as Singapore, are expected to provide unbiased information so that subordinates can proceed with their predetermined jobs (Chong 2008). Hence, in such cultures, greater emphasis is placed “on communicating across organizational levels and directing information to the proper individual or work group” (Birnberg and Snodgrass 1988, p. 460).

-

Similarly, in another quantitative study (Chow et al. 1999) Taiwanese, compared to Australian managers, are more likely to ask clarifying questions, whereas the Australians are more likely to speak up and express a contrary or challenging opinion. Taiwanese tend to ask more clarifying questions, as they are more focused on the greater good of the company, whereas they hesitate to challenge their superiors due to the fear of “losing face.”

-

Drawing on interviews with Taiwanese and Australian middle managers to investigate their information-sharing behavior reveals further differences (Chow et al. 1999). Australian managers’ preparedness to share informal information depends on individual differences (personality, style, and skills) and corporate culture. Among the Taiwanese, consistent with their collectivist culture, interviews reveal a sense of collective responsibility that urges organizational members to share information for the good of the company, even if this is disadvantageous for the reporting person. The presence of the superior constrains the sharing of potentially damaging information in Taiwan and Australia, which is explained by the concern with “losing face” that is intensified in the presence of the superior. However, consistent with high power distance, sensitivity to the hierarchy in Taiwan is greater and the superior is perceived as the greater authority, and the legitimate and obliged decision-maker, relative to subordinates.

-

Cultural traits also impact the truthfulness with which subordinates communicate with their superiors. A quantitative study between Chinese and US nationals (Chow et al. 1998) demonstrates that Chinese misrepresent their private information to a lower degree than their US counterparts as Chinese higher collectivism makes them more reluctant to profit individually from misrepresentations at the expense of the organization. Moreover, their higher long-term orientation retards their misrepresentation tendency since they fear long-run consequences more once these misrepresentations may be detected over time.

-

Culture also influences the collaboration among employees. A case study, comparing Italian companies and its Moroccan subsidiaries shows that Moroccans have a habit of forming personal relationships and collaborating more with each other, as it is an expression of their collectivist culture (Tallaki and Bracci 2015).

6 Conclusion, research implications and limitations

6.1 Concluding remarks