Abstract

In characterizing entrepreneurial behavior, researchers often regard nascent entrepreneurs entering risky markets as overconfident. In this paper, we challenge this prevailing view and show that a more differentiated consideration reveals the effects of overconfidence on market entry to be ambiguous if not irrelevant. In a first step, we emphasize the inconclusiveness of past empirical evidence. With a simple decision model, we show that “observed” overconfidence can also be interpreted as the outcome of fully rational behavior when acknowledging information available to and acquired by the entrepreneur. We criticize that empirical studies, which neglect individually available information, inductively propose overconfidence for observed behavior without substantiating it with appropriate data. Nevertheless, we do not generally deny overconfidence in decision making. Thus, in a second step, we explicitly postulate confidence biases of an intended rational decision maker. This enables us to analyze through which channels they may affect market entry. By considering over- and underconfidence in the entrepreneur’s forecasting ability, we find that market entry may be affected positively, negatively, or not at all, thereby revealing the overall ambiguity of confidence biases in decision behavior. Finally, we show formally that, even if overconfidence increases the probability of market entry, this does not make it a characteristic feature of market entrants. Overall, our objective is to debunk the myth of the overconfident entrepreneur and to promote the more important role of information in entrepreneurial decision making.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In their fundamental agenda for entrepreneurship research, Shane and Venkataraman (2000) raise the question of why some people discover and exploit opportunities for value creation, while others do not. With regard to exploitation, especially self-efficacy (Bandura 1977), i.e., confidence in one’s abilities, is viewed as a major determinant for entrepreneurial action (Boyd and Vozikis 1994; Hmieleski and Baron 2008; Cassar and Friedman 2009). In their survey on the roots of entrepreneurship, Åstebro et al. (2014) identify different risk attitudes, overconfidence, and nonpecuniary benefits from self-employment as possible explanations for empirically observed entry into and persistence in the market. While the first and the third explanations imply that entrepreneurs have specific preferences, in line with the long tradition of subjectivist theories of entrepreneurship (Foss et al. 2008), overconfidence poses a challenge for research, because the entrepreneur’s decisions would be based on misperceptions that lead to possibly harmful errors. With entrepreneurial earnings lower than paid employment (e.g., Hamilton 2000), or the expected utility of entrepreneurial ventures empirically assessed to be negative (see Hall and Woodward 2010 for an analysis of venture-capital-backed firms), individuals entering the market are, indeed, often even regarded as being overconfident (Busenitz and Barney 1997; Bernardo and Welch 2001; Fitzsimmons and Douglas 2006; Koellinger et al. 2007; Thomas 2018). Overconfidence as a psychologically well-investigated (mis)perception plausibly explains why some people do things, which others would not dare. Thus, it also seems to be a good explanation for excessive market entry.

Building on empirical and experimental research, Hayward et al. (2006) develop a “hubris theory of entrepreneurship,” which explains why and how overconfidence induces entrepreneurs to initiate ventures, despite high rates of failure. With such a comprehensible theoretical foundation, empirical studies (e.g., Cassar 2010; Pirinsky 2013) over the past decade have established overconfidence “as a defining trait of entrepreneurs—practically a caricature” (Chen et al. 2018, p. 992; see also Thomas 2018 and Vörös 2020). However, as a solution to the fundamental research question posed by Shane and Venkataraman (2000), this view would imply that entrepreneurship, the widely proclaimed engine of innovation and economic growth, is driven by people who, because of their dispositional biases, make decision errors in their most fundamental decisions. We see here a contradiction to traditional theories that have characterized the entrepreneur as an information manager and market maker (Casson 2005). We also believe that the perception of overconfidence as an entrepreneurial trait has questionable implications, in particular for entrepreneurship practice and policy. How should one encourage the individual entrepreneur? What should one teach prospective entrepreneurs? How should policies address decision makers who persistently make mistakes?

In our paper, we, therefore, contrast this popular notion of entrepreneurial overconfidence with a more rationality-based entrepreneurship paradigm. We analyze market entry from the perspective of the decision-making entrepreneur, thereby complementing previous contributions to subjectivist theory that emphasize the role of entrepreneurial judgment as the driver of entrepreneurial action (see Foss et al. 2008 for an overview and synthesis of the influential subjectivist schools of thought). In our view, to understand the relevance of perceptional biases, they must be studied from the perspective of the entrepreneur rather than the outside observer. We substantiate our claim, first, by demonstrating the inconclusiveness of outside observations of overconfidence, second, by revealing the ambiguous impact of overconfidence on the market-entry decision of the entrepreneur, and third, by resolving the confusion of overconfidence as a driver of market entry with overconfidence as a trait of market entrants.

Previous theoretical studies have shown that rational decision behavior, i.e., Bayesian updating based on the available information (Benoît and Dubra 2011), assumed better information of the decision maker (Gui et al. 2009), or the rational "choice-driven overoptimism" mechanism (Van den Steen 2004) may yield decision patterns which closely resemble overconfident behavior, thereby casting doubt on theories of entrepreneurial overconfidence. The question that remains, though, is how strongly this rational view weighs against the overwhelming empirical evidence of overconfidence. We address this question explicitly and question the conclusiveness of the empirical evidence, by revealing the ambiguous relationship between overconfidence and market entry, and by clarifying when specific behavior classifies as a trait.

In the first part of our analysis, we take the outside perspective of descriptive empirical research that observes what potential market entrants do but does not capture the inside (subjectivist) perspective on why they do it. As a consequence, observed beyond average or aggregated behavior is often classified as biased (Cassar 2010; Pirinsky 2013; Wu and Knott 2006). By describing this setting within a simple decision-theoretical framework, we can view the market entry decision of the entrepreneur formally as a decision under uncertainty, thereby enabling us to understand what individual reasons drive her decision to enter the market. By acknowledging the crucial role of individually available information, we show how the “observed” overoptimistic behavior of a real sample of entrepreneurs can be reproduced within a rational decision framework without any psychological biases. Our formal framework thereby enables us to explain why and how the outside perspective of descriptive research may confuse justified high confidence with overconfidence or overoptimism when (unobserved) available information is neglected. Indeed, the notion of overconfidence appears to be inductively proposed rather than derived from the sample.

Nevertheless, we do not doubt the occurrence of overconfidence but view it, following Kahneman (2011), as a common human feature. Hayward et al. (2006) provide several compelling arguments as to why it may affect the entrepreneur’s behavior, and Koellinger et al. (2007) find empirical evidence for a negative relationship between overconfidence and market survival. However, as Hayward et al. (2006, p. 170) emphasize, “the greater scholarly challenge is not just to link founder overconfidence to venture failure […] but to explain and predict how founders’ overconfidence affects the nature and quality of their judgment. Joining this challenge should yield theory and evidence on how present and prospective founders will produce better ventures.”

In the second part of our analysis, we, therefore, switch from the outside perspective of the analytical observer to the inside perspective of the decision maker in order to study the behavior of an intended rational, but biased entrepreneur. By explicitly postulating and specifying overconfidence as well as underconfidence within our theoretical framework, we consider two decision scenarios: In the first, we assume that the entrepreneur has a biased perception of a given information system, and we show how this may affect market entry positively, negatively, or not at all for both over- as well as underconfidence. In the second scenario, we regard the acquisition of information as a costly activity and assume a confidence bias in the skill of acquiring information. Here we also find that the probability of market entry may increase as well as decrease. The individual ambiguities that we reveal with our simple model provide insights into the overall ambiguity of the relationship between confidence biases and market entry at a more sophisticated level. Our analysis thus emphasizes the necessity of distinguishing between over- and underconfidence as experimentally confirmed behavioral biases and their relevance for entrepreneurial decisions in market situations.

Since we cannot generally dismiss all empirical evidence of overconfidence, we show formally in a third and final step that, even if we postulate that overconfidence unambiguously increases the probability of market entry, this does not imply that entrepreneurs, who are more likely to enter the market, are predominantly driven by overconfidence. This converse causality may, indeed, be an intuitive statistical confusion that nourishes the belief of overconfidence in market entry.

In summary, we find the overconfident entrepreneur to be more or less a popular myth, but one which falls short of the fundamental role of entrepreneurship for society. With our theoretical approach, we contribute to the research agenda on entrepreneurial decision making (Shepherd et al. 2015; Ferreira et al. 2019) three formal arguments against entrepreneurial overconfidence as a driver of market entry—first, the empirical evidence of entrepreneurial overconfidence is inconclusive; second, the effect of assumed overconfidence on market entry is ambiguous; and third, even if overconfidence does induce market entry, it cannot necessarily be regarded as an entrepreneurial trait.

Our analysis begins in Sect. 2 with a review of the literature on different notions of overconfidence. In Sect. 3, we present the decision theoretical framework, which we use throughout the analysis to establish our main results that we present in three separate sections. In Sect. 4, we show why empirical evidence of overconfidence is inconclusive. In Sect. 5, we establish the ambiguity of biased confidence in entrepreneurial decision making. And in Sect. 6, we use basic statistical reasoning to reveal that even an unambiguous effect of overconfidence does not make it a characteristic feature. In the concluding Sect. 7, we emphasize the merits of the rationality paradigm and point out promising implications of our theoretical framework for research, practice, policy, and teaching.

2 Notions of overconfidence

To better understand the effects of overconfidence and the differing observations in empirical and experimental research, Moore and Healy (2008) distinguish three different notions of overconfidence: overestimation, overprecision, and overplacement. Presumably most prevalent in the entrepreneurship literature is the decision maker’s overestimation of her “ability, performance, level of control, or chance of success” (Moore and Healy 2008, p. 502). Also related to the decision maker’s perception of her self-confidence, but empirically distinguishable in a context of uncertainty, is overprecision, i.e., inappropriately narrow estimates of confidence intervals around predictions or rather “excessive certainty regarding the accuracy of one’s beliefs” (Moore and Healy 2008, p. 502). In contrast, the decision maker may assess her relative performance, in which case overconfidence becomes overplacement of oneself as compared to the median or average, which is related to the better-than-average effect (Koellinger et al. 2007).

Although there is no clear-cut distinction between the situations, in which the different types of overconfidence occur, overestimation is often seen as the driving force of excess market entry (e.g., Hayward et al. 2006; Vörös 2020). Overestimation is also used as an explanation for high failure rates of market entries (Cooper et al. 1988). Koellinger et al. (2007) show for a sample based on surveys from 18 countries that self-confidence in the sense of overestimation is a strong determinant for entrepreneurial propensity, and that there is a negative correlation between self-confidence and the chance of survival, which could be seen as evidence for overconfidence. Empirical observations of market entry despite the high rates of market failure, thus, have given strong support to theories of overconfidence, in particular, in the form of overestimation.

Overestimation of one’s entrepreneurial abilities or performance appears to be related to overoptimism concerning one’s market performance (Cassar 2010; Thomas 2018). The latter is often used as a proxy for the former (Invernizzi et al. 2017; Vörös 2020).

The seemingly close relationship between overconfidence and overoptimism in the literature is presumably due to the mutation of terminology over the past decades: Kahneman and Tversky (1995) introduced the concept of “optimistic overconfidence” referring to “the common tendency of people to overestimate their ability to predict and control future outcomes” (Kahneman and Tversky 1995, p. 49). Unfortunately, Griffin and Varey (1996, p. 228) use the same terminology but refer to the tendency to overestimate the likelihood of one’s favored outcome, thereby shifting the focus from confidence (in one’s ability) to optimism (concerning the outcome). Griffin and Varey (1996, p. 228) then contrast their definition of “optimistic overconfidence” with “overconfidence in the validity of one’s judgment,” which, confusingly, resembles Kahneman and Tversky’s (1995) definition of optimistic overconfidence. Hayward et al. (2006) then go even further and combine the two concepts by defining “overconfidence as the extent to which founders overestimate the wealth that they will generate from their ventures,” which, in turn, is closely linked to founders’ perception of their ability to ensure such survival (Hayward et al. 2006, p. 161,162). With this understanding, overoptimism concerning performance becomes causally linked to the overestimation of the ability to ensure this performance. This mix of optimism and confidence is also captured in Moore and Healy’s (2008) widely accepted definition of overestimation, given above, thereby blurring the distinction to overoptimism, e.g., as conceived by Cassar (2010).

Overestimation and overoptimism, however, are not synonymous, as several authors have critically pointed out over the past years (Trevelyan 2008; Hogarth and Karelaia 2012; Zhang and Cueto 2017). While overoptimism may be causally related to overestimation in the case of positive events, overestimation of one’s ability to predict negative events may result in underconfidence, overpessimism, and, thus, “missed opportunities” (Hogarth and Karelaia 2012, p. 1734). As we show in Sect. 5, this ambiguity in the relationship between confidence and optimism is responsible for the ambiguous relationship between overestimation and market entry.

Overprecision was first investigated in psychological research by Fischoff et al. (1977), who discovered a general tendency of decision makers towards extreme confidence in their estimates, typically measured by confidence intervals. In their comparison of decisions made by entrepreneurs and managers, Busenitz and Barney (1997) focus on overprecision and find entrepreneurs to be more overconfident in this respect. Klayman et al. (1999) show in different experiments how overprecision varies with the nature of the decision. Herz et al. (2014) find in experiments that overprecision negatively affects innovation. Applying their result to entrepreneurial activity, Åstebro et al. (2014) conclude that the effects of overprecision on market entry are not clear, which also confirms previous findings of Simon et al. (2000). Hence, it seems to be difficult to find hard evidence or even convincing arguments that overprecision increases the likelihood of market entry.

The experimental work of Camerer and Lovallo (1999) focuses on overplacement, measured by performance in relation to competitors. They find that subjects who consider their performance better than average are more likely to enter a competitive market. In this context, the comparison with potential competitors is what initiates overconfidence. Benoît and Dubra (2011) criticize, however, that the identification of overplacement requires information concerning the strengths of subjects’ beliefs, thereby casting doubt on previous experimental research in this domain. To identify overplacement outside of the laboratory, one needs a panel or survey that contains direct comparisons with competitors.

By making precise distinctions, the relationship between the different notions of overconfidence can be investigated, although it is not fully clear whether all notions should even be related. As experimental research has revealed, one cannot infer that one type of overconfidence necessarily implies another (Moore and Healy 2008). For the decision to enter the market, Cain et al. (2015) find in their experiments that overplacement plays a more significant role than overestimation. Yet, whether this also holds for real market situations, where laboratory conditions are not met and relative performance is difficult to assess, remains unclear (Vörös 2020). Theories of entrepreneurial overconfidence in the literature have been largely nourished by empirical observations, i.e., outside of the laboratory, where overconfidence is typically measured by and therefore inferred from observed deviations from average market behavior, e.g., the so-called “excessive” market entry (Wu and Knott 2006; Cassar 2010; Prinsky 2013). However, without identifying overconfidence at the individual level, as in the laboratory, it remains unclear to what extent the underlying entrepreneurial behavior is justified or, indeed, driven by overconfidence. What is required for a distinctive assessment is a rational benchmark of justified confidence against which overconfidence can be measured.

3 A decision-theoretical framework for entrepreneurial decisions

In this section, we present a simplified version of the “blackboard” decision model of Chwolka and Raith (2012) that we use for two theoretical exercises. First, in Sect. 4, we show how to rationalize empirically observed data of (seemingly overconfident) market entry from the perspective of a decision analyst. In Sect. 5, we then switch to the perspective of the decision-making entrepreneur, to whom we can ascribe specific forms of overconfidence.

In the model, the entrepreneur has the choice of either entering the market or staying out, where staying out yields a normalized payoff of \(V_{0} \equiv 0\). If she enters the market, the venture will be successful with probability s, yielding an estimated net payoff of \(V_{s} > 0\), or it may fail with probability \(1 - s\), resulting in an estimated net payoff of \(V_{f} < 0\). As long as the a-priori expected payoff of market entry is positive, i.e., \(sV_{s} + (1 - s)V_{f} > 0\), a risk-neutral or even slightly risk-averse entrepreneur would enter the market. Let us, therefore, assume in the following that the expected payoff of starting the venture is negative from an outside perspective, i.e., \(sV_{s} + (1 - s)V_{f} < 0\). In this situation, no rational risk-neutral or risk-averse entrepreneur would choose to enter the market.

If we observe market entry nonetheless, one might infer that the entrepreneur is perhaps overconfident in assuming that her personal performance is much better than average, so that she expects a positive payoff. Indeed, if her personal perceptions are unfounded, then the market failure could be driven by what Hayward et al. (2006) refer to as hubris—the “dark side” of overconfidence. However, the problem with the observance of selected entrepreneurial decisions is that we usually have only little background information on the entrepreneur’s motivation for her action choice. In other words, although we may clearly observe what the entrepreneur does, we often do not know why. The answer to the latter question is the motivation behind our theoretical approach.

In order to highlight the relevance of this aspect, assume that, prior to market entry, the entrepreneur can acquire additional information concerning the likelihood of her venture success. The decision tree in Fig. 1 illustrates the modification of the decision problem, where the squares depict the entrepreneur’s decision nodes, the circles characterize random choices by nature, and the triangles denote terminal nodes with corresponding payoffs. The entrepreneur’s decision problem now begins with the choice between proceeding with or without additional information.

The entrepreneur’s decision to use additional information prior to market entry

The upper branch in Fig. 1 reflects the alternative “Information Acquisition” (IA). The entrepreneur may have access to a whole array of information systems to choose from or to draw on repeatedly over time (Choi et al. 2008). For expositional convenience, we assume here that there is only one such source of additional information and that the entrepreneur is only once confronted with the choice of acquiring it.Footnote 1 The purpose of this information is to provide a signal, telling her whether to enter the market (scenario 2). Since the entrepreneur’s market decision involves only two alternatives, entry, and no entry, we restrict our analysis to two distinct signals, ‘positive’ and ‘negative.’Footnote 2 Which signal will be obtained from the information system, is a priori uncertain. For simplicity, the market payoffs, Vs and Vf, are assumed to remain the same across both scenarios. An (intended) rational entrepreneur will enter the market after a positive signal, only if the perceived conditional probabilities of success and failure lead to a positive expected outcome. If she chooses “Null Information,” i.e., not to acquire additional information (in Fig. 1 the lower branch labeled NI), the decision situation, scenario 1, is the same as our initial setting above, and a rational risk-neutral decision maker would not enter the market due to the negative expected payoff.

The problem for empirical researchers observing just the market entry is that they generally cannot distinguish between scenarios 1 and 2. Hence, in order to fully understand the entrepreneur’s decision, one needs to acknowledge the information on which it is based. There are many ways for decision makers to acquire information in order to deal with uncertainty, which vary with the nature of uncertainty and the type of decision maker (Shepherd et al. 2015). Planners may weigh conceptual alternatives based on the calculated benefits of possible outcomes (Gavetti and Levinthal 2000; Chwolka and Raith 2012). Business planning generally involves several steps and employs a variety of analytical techniques (Gruber 2007), where the value of these techniques depends on the information collected during the planning process (Hopp 2012). Based on their meta-analysis of factors influencing the relationship between business planning and venture performance, Brinckmann et al. (2010) propose an approach that combines planning and learning, which may also be conducted after market entry, e.g., as in the lean start-up approach (Shepherd and Gruber 2021). While planning a venture involves market expectations, learning refers more to the evaluation of observed outcomes, which provide imperfect signals in the form of recommendations for further action. In line with behavioral theories of choice (Knudsen and Levinthal 2007), this “complementarity of planning and learning during the entrepreneurial process” is confirmed by the longitudinal study of PSED participants by McCann and Vroom (2015: 632). The acquired information need not be the result of complex analysis, but simply the outcome of a successful heuristic based on experience (Gigerenzer and Brighton 2009; Gigerenzer and Gaissmaier 2011). Effectuators may rely on their network or test market (Dew et al. 2009), where the outcomes of experimentation with new ideas serve as additional information (Gavetti and Levinthal 2000; Manso 2016). In line with Gavetti and Levinthal’s (2000) combination of cognitive and experiential search, Smolka et al. (2018) find empirically that ventures benefit from combining a (causal) planning approach with effectual reasoning. According to Dew et al. (2009), entrepreneurial experts tend more than novices to rely on effectual logic, indicating that entrepreneurial experience itself provides valuable information. In a world of Knightian uncertainty, “[e]ven a mere ‘hunch’ or ‘something tells me’ […] may readily be accepted as valid ground for action […]” (Knight 1921, p. 236). In all of the above formal or less formal approaches, the decisions based on the entrepreneur’s acquired additional information will differ from the prior decisions without the information (Rapp and Olbrich 2020). In this sense, our view here is in line with Casson (2005), who sees the entrepreneur as a specialist in information management, which specifically involves the use of available information.

The important aspect is that information will be acquired if the entrepreneur is confident that it will increase the expected payoff. Otherwise, she would stick with her a-priori beliefs and, as in our example, not enter the market. Accordingly, her market-entry decision will critically depend on her confidence in the reliability of the additional information. The question then arises, to what extent this confidence is justified because the justified confidence of the decision maker is the benchmark against which one should measure overconfidence.

4 Justified confidence in entrepreneurial decisions

Confidence in an information system intuitively depends on the perceived quality of the signals that it produces. Following the literature, we measure this quality by the (perceived) likelihood with which the signals correctly forecast the prospective venture’s performance (Bernardo and Welch 2001; Chwolka and Raith 2012). More formally, the quality of the additional information is assumed to be characterized by the likelihoods P(Positive|Success) and P(Negative|Failure), i.e., the conditional probabilities with which the future venture outcomes (Success or Failure) are correctly signaled (Positive or Negative). In order to keep our model as tractable as possible, we assume in the following that success and failure are forecasted by the signals equally well, i.e., P(Positive|Success) = P(Negative|Failure) = q, where q ∈ [0.5, 1] measures the quality of the information. With q = 1, the information provides a perfect forecast of the future. At the other extreme, with q = 0.5, it corresponds to the toss of a coin, which contains no useful information whatsoever.Footnote 3 Since q measures the forecasting quality of the information used by the entrepreneur, it is a quantitative measure of her forecasting ability. However, for empirical research, the actual measurement of this ability would require data on repeated forecasts, which is available for established investment brokers or venture capitalists (Zacharkis and Shepherd 2001) with a forecasting reputation, but in general, not for entrepreneurs newly entering the market.

The a-posteriori probabilities of success and failure, i.e., after the entrepreneur observes the signal, will depend on q. According to Bayes’ rule, the a-posteriori probabilities are

where the conditional probabilities of failure are simply one minus the conditional probabilities of success. Moreover, the probabilities of the two signals,

are given by the denominators of the conditional probabilities in Eqs. (1). With q < 1, the entrepreneur is faced with noise in her predictive judgments, where the fallibility of the signals may lead to unsuccessful market entry, since P(Failure|Positive) > 0, or premature termination of the venture (no entry) with a missed opportunity, since P(Success|Negative) > 0.Footnote 4

To show how our decision model in Fig. 1 can be related to empirically observed market-entry decisions, we use exemplarily Cassar’s (2010) panel study of entrepreneurial overoptimism with a sample of 386 nascent entrepreneurs taken from the PSED data. In Table 1, we reproduce the status description of the selected panel participants.

If we assume the same general a-priori market information for all entrepreneurs, we can restrict our attention to the upper branch (IA) of Fig. 1, since the lower branch (NI) cannot explain why 214 of the representative panel participants rationally chose “Market Entry,” while 172 chose “No Market Entry.” Moreover, those 172 panel participants who reported to be nascent at their first interview, i.e., when they were taken into the panel, but later on chose “No Market Entry,” must have received some information on which they based their decision to terminate the venture. We can therefore assume that all 386 nascent entrepreneurs in the sample followed the upper branch (IA, scenario 2) at time t0 by acquiring some form of additional information in preparing their startup. Figure 2 shows how the statistics of Table 1 fit into the decision tree of Fig. 1.

The deduced decision tree for the PSED sample of Cassar (2010)

Of the 386 nascent entrepreneurs, 185 reported having been operating 60 months after the first interview. In Fig. 2, we classify these as the group that chose “Market Entry” at time t1 after a positive signal and established a successful business. Only 29 nascent entrepreneurs reported having stopped the venture after startup. If we assume the worst case and classify these as failed startups, we can assert that the ex-post (i.e., actually realized) success rate of all 214 (= 185 + 29) nascent entrepreneurs that entered the market after a positive signal was about 86,45 percent (= 185/214), which is remarkably high, given that the sample was assumed to be representative.Footnote 5 The remaining 172 (= 386–214) nascent entrepreneurs were not operating at the end of the panel study, because they had given up (168) or were still not in the market (4). We classify all of these 172 nascent entrepreneurs in Fig. 2 as having chosen “No Entry” due to a negative signal, even if the last four (not operating) may still be waiting for a signal.

Hence, in the end, nearly 48 percent (\(=\) 185/386) of all nascent entrepreneurs had an operating business (cf. Table 1). If we assume that market entry was induced by a positive signal and no entry by a negative signal, then the statistics of Table 1 translate in Fig. 2 to P(Positive) = 214/386 = 0.5544 and P(Success|Positive) = 185/214 = 0.8645. With the two formal definitions of P(Success|Positive) and P(Positive) given by Eqs. (1) and (2) above and their corresponding empirical values given by the panel, we can calibrate our decision model to reproduce the panel statistics by appropriately choosing the quality of information, q, and the a-priori probability of success, s, as solutions to the following two equations:

Since the effects of q and s in the definitions of the two probabilities are symmetric, the two equations together yield the values s = 0.5853 and q = 0.8188, or vice versa. Note that, in either case, the panel sample features an a-priori probability of success, which our model assumes to be greater than 50 percent, i.e., s > 0.5.Footnote 6 Since the actual success rate of market entrants found in the PSED data of Cassar (2010) is, indeed, quite high, our calibrated value of s = 0.5853 does not seem unrealistic for this particular sample.

Of course, the probabilities of the signals, ‘Positive’ and ‘Negative,’ will only correspond to the actual market entry statistics, if the entrepreneur strictly follows the signals, i.e., market entry after a positive and no entry after a negative signal. Plausibly, this will depend on the quality of the signal that the entrepreneur obtains from her acquired information. Specifically, in a situation with a priori negative expected value, a positive signal will only induce a risk-neutral entrepreneur to enter the market, if the expected payoff of entering the market is greater than the value of staying out:

Thus, the quality of the signal must exceed the minimum level \(q_{\min }^{{{\text{pos}}}}\) to induce the entrepreneur to enter after a positive signal. Analogously, in a situation with a priori positive expected value, a negative signal induces the entrepreneur to stay out of the market, if this leads to a higher expected payoff, i.e.,

The quality of the signal must exceed the minimum quality \(q_{\min }^{{{\text{neg}}}}\) to induce the entrepreneur to stay out of the market after a negative signal. Hence, the entrepreneur will enter the market after a positive signal and stay out of the market after a negative signal, if the quality of information exceeds both minimum qualities, i.e., \(q > q_{\min } \equiv \max \left\{ {q_{\min }^{{{\text{pos}}}} ,q_{\min }^{{{\text{neg}}}} } \right\}\). Since Eqs. (4) and (5) together reveal that \(q_{\min }^{{{\text{pos}}}} + q_{\min }^{{{\text{neg}}}} = 1\), the larger of the two implies qmin ≥ 0.5. If the quality of the signal from information acquisition (IA) lies below the minimum level, i.e., \(0.5 \le q < q_{\min }\), the entrepreneur will choose the same action with or without information. The signal quality of acquired information is then too close to 0.5 (i.e., the toss of a coin) to be of any value for the decision maker.

Reliable information raises the ex-ante expected outcome of information acquisition (i.e., the upper branch of Fig. 1). Formally, from the definitions of the conditional probabilities in Eqs. (1), one can see that \({\text{P(Success|Positive)}} > s > {\text{P(Success|Negative)}}\) for \(q > q_{\min } \ge 0.5\). Hence, with reliable information, the conditional chance of success after a positive signal will be higher than the a-priori chances without the signal. Likewise, since “planning may also reveal negative information” (McCann and Vroom 2015, p. 619), a negative signal will lower the conditional probability of success. In the calibrated model of Fig. 2, one can see that the probability of market success rises from a-priori 0.5853 to a-posteriori 0.8645 after a positive signal and declines to 0.2380 after a negative signal. Hence, for an entrepreneur with reliable information, it is absolutely rational to enter the market after receiving a positive signal—this has nothing to do with overconfidence, and the higher expected outcome has nothing to do with overoptimism. On the contrary, the entrepreneur’s “domain-specific self-efficacy” (Cassar and Friedman 2009, p. 243) is justified by the level (quality) of her forecasting ability. Her optimism, rather than being dispositional (Hmieleski and Baron 2009), simply “reflects [her] interpretation of the privileged information at [her] disposal” (Casson 2005, p. 330). Nevertheless, for an empirical researcher not being able to observe this information, the entrepreneur’s expectations may (incorrectly) appear irrational.

Our calibrated decision model also allows us to replicate the quantitative findings of entrepreneurial overoptimism in the PSED sample given above. Cassar (2010) measures “operational overoptimism” as the difference between entrepreneurs’ self-assessed mean expected probability of operation and the ex-post statistically observed percentage of operation.Footnote 7 In the PSED sample, entrepreneurs’ mean expectation of operation (reported at their first interview when entering the panel) was 81 percent. In contrast, ex post, 185 of the 386 nascent entrepreneurs, i.e., only circa 48 percent (= 185/386), reported having an operating business. With this realized percentage interpreted as the “rational expectation of operation,” Cassar (2010) finds a mean expectation bias of 81–48 = 33 percent, which serves as his measure of operational overoptimism among entrepreneurs.

As our decision model reveals, the rational expectations of the nascent entrepreneurs will depend on the information they consider when they form their expectations. In Fig. 2, if nascent entrepreneurs form their expectation of operation at time t0 in the decision process, where they have not yet received any additional information, they must acknowledge the possibility of termination due to a negative signal. If they receive a positive signal with only a 55 percent chance (P(Positive) = 214/386 = 0.5544), then their rational expectation of operation would, indeed, be 0.5544·0.8645 = 0.48, as stated by Cassar (2010). Thus, implicit in this interpretation of the descriptive statistics is the assumption that all entrepreneurs were first interviewed at time \(t_{0}\) in Fig. 2, i.e., before they had received any information.

One must keep in mind, though, that nascent entrepreneurs in the PSED were at various preparation stages prior to market entry and that they will have acquired different amounts and types of information before they have given their first interview for the panel. According to Cassar (2010), a significant number of nascent entrepreneurs in the PSED sample were reported to have had business plans, financial projections, or industry experience, which are all sources of additional information. Consequently, some nascent entrepreneurs in the PSED will have given their initial interview at a more informed level, say, at time t1 in our simplified two-stage decision process depicted in Fig. 2. Note that, at this stage in the process, nascent entrepreneurs, who had already received a negative signal, would have earlier chosen to terminate their startup and would therefore not be included in the panel anymore.Footnote 8 Only entrepreneurs who had previously received a positive signal would be included in the panel at time t1, where their rational expectation of operation should be over 86 percent (P(Success|Positive) = 185/214 = 0.8645). With a reported mean expectation of operation of 81 percent (Cassar 2010), nascent entrepreneurs interviewed at t1, therefore, cannot be considered to be overoptimistic. Empirical validation of overoptimism or overconfidence thus requires more empirical data on the timing of subjective beliefs, since these are likely to vary (positively or negatively) with the received signals. This is in line with the findings of McCann and Vroom (2015), who examine how information activities by nascent entrepreneurs in the PSED influence their success beliefs as they proceed through the process.

So far, we have shown that valuable additional information always justifies higher performance expectations. All types of entrepreneurial decision makers that have been acknowledged in the literature seem to make use of the information that they have at hand, be it by analogies, heuristics, calculations, etc. Even the effectuation principles (Sarasvathy 2001), such as having a network (building a quilt) or controlling the future (pilot on the plane), only make sense if they spawn signals for entrepreneurial action. Without observations of these signals, we see no convincing evidence that overoptimism is the cause of above-average market expectations or overconfidence a driver of market entry. On the contrary, it appears that the overconfidence or overoptimism in the empirical research of market entry is more an inductive proposition from observed behavior rather than an empirically substantiated hypothesis. However, even if overconfidence is explicitly proposed, the question remains to what extent it is likely to affect market entry. We turn to this q uestion in the next section.

5 Biased confidence in entrepreneurial decision making

None of the previous analyses is supposed to prove that entrepreneurs are not susceptible to overconfidence, or, more generally, biased confidence, since experimental research has also shown distortions due to underconfidence. Yet, rather than assuming it in observed behavior, we explicitly postulate biased confidence in our decision model to show where, how, and why it affects decision making (Hayward et al. 2006). In the following, we extend our analysis by analyzing two plausible occurrences of biased confidence in the market-entry decision that match the characterizations given by Shepherd et al. (2015). The first setting involves biased confidence in a given information system, e.g., experts of a social network or a personal consultant, from whom the entrepreneur may obtain signals that affect her market expectations. The second setting considers biased confidence in the quality of acquiring information in the entrepreneurial process, e.g., the quality of the entrepreneur’s own business planning or test market. For both settings, we change our perspective from the outside analytical observer of entrepreneurial decisions to the subjective perspective of the decision-making entrepreneur.

5.1 Biased confidence in estimating the quality of a given information system

Suppose that the entrepreneur is biased in her assessment of her information system’s quality, i. e., she over- or underestimates her “ability to make correct predictions” (Shepherd et al. 2015: 30). We denote this by \(q^{O} > q^{A}\) and \(q^{U} < q^{A}\), where \(q^{O}\) denotes the overestimated, \(q^{U}\) the underestimated, and \(q^{A}\) the actual forecasting ability of the entrepreneur. This measure of overconfidence corresponds to Kahneman and Tversky’s (1995) definition of “optimistic overconfidence,” but it can be traced back even further to Oskamp’s (1965) measure of overconfidence, which builds on the confidence scale of Adams (1957). Interestingly, since the quality q of the information also characterizes the precision of the signal’s forecast (Bernardo and Welch 2001), over-/underestimation of the quality of the information system technically entails over-/underprecision with respect to the signal that it produces. Our characterization thus captures both biased estimation as well as precision.

Assessing the quality of a given information system is not an easy task, and one can assume that it becomes even more difficult, if the information system does not have a history that one can evaluate statistically. An internal information system may provide less critical signals than an external one (Cooper et al. 1988; Meissner and Wulf 2016). Moreover, the belief in the ‘law of small numbers’ is a cognitive bias that may mislead decision makers to overestimate the quality of their sample (cf. Simon et al. 2000). In addition, one can well imagine that an entrepreneur’s assessment of her information system differs before and after the additional information (in Fig. 2 given by the two points in time t0 and t1). From the definitions in Eqs. (1), we know that a biased assessment of the information system will (rationally) distort the perceived a-posteriori probability of market success, i.e., after receiving a positive or a negative signal, where d P(Success|Positive)/dq > 0 and dP(Success|Negative)/dq < 0. Overestimation of the entrepreneur’s predictive ability, i.e., the goodness of information, thus results in overoptimism after a positive signal and overpessimism after a negative signal. Underestimation has the opposite effects, implying that overoptimism/-pessimism may result from both over- as well as underconfidence. These diverging effects of confidence and optimism reveal that they need to be treated as distinct constructs (Zhang and Cueto 2017). The crucial question, though, is whether or not the entrepreneur’s biased perception of the quality of her information also distorts her decision to enter the market. As we formalize in the following proposition, this depends on whether or not the given information system yields reliable or unreliable signals.

Proposition 1

If an entrepreneur’s given information system yields reliable signals, i.e., \(q^{A} > q_{\min } \) then overestimation will not distort market entry behavior, while underestimation may distort the entrepreneur’s decision to enter the market, if \(q^{U} < q_{\min } < q^{A}\). Conversely, if an entrepreneur’s given information system yields unreliable signals, i.e., \(q^{A} < q_{\min } \), then underestimation will have no relevance for market entry behavior, while overestimation may distort the entrepreneur’s decision to enter the market, if \(q^{O} > q_{\min } > q^{A}\).

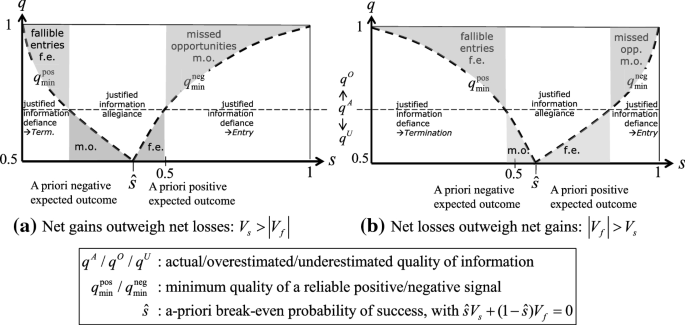

A formal proof is provided in the Appendix along with the proofs of all further propositions. According to Proposition 1, whether or not a biased estimation of information quality is distortionary, depends on the minimum level of information reliability, i.e., qmin, in relation to the actual quality qA and the over- or underestimated qualities of information, qO and qU, respectively. The actual quality qA is by assumption exogenously given, and the biased quality assessments depend on the individual characteristics of the entrepreneur. In contrast, qmin is exogenously determined by the given market situation, as it is the maximum of \(q_{\min }^{{{\text{neg}}}}\) and \(q_{\min }^{{{\text{pos}}}} ,\) which from Eqs. (4) and (5) are both functions of the possible venture outcomes, Vs and Vf, as well as the a-priori probability of success, s.

We illustrate the different relationships in Fig. 3, which characterizes two different market constellations. In panel a) net gains of success outweigh net losses of failure, i.e., Vs >|Vf|. With Vs >|Vf|, the a-priori break-even probability, \(\hat{s}\), at which the a-priori expected payoff of market entry is zero, i.e., \(\hat{s}V_{s} + (1 - \hat{s})V_{f} = 0\), is smaller than 0.5. For a-priori probabilities \(s > \hat{s}\), expected outcomes are positive, and for \(s < \hat{s}\), expected outcomes are negative. Panel a) thus illustrates how \(q_{\min } = \max \left\{ {q_{\min }^{{{\text{pos}}}} ,q_{\min }^{{{\text{neg}}}} } \right\}\) varies across the range of possible a-priori probabilities of success, s, determined by \(q_{\min }^{{{\text{pos}}}} ,\) for \(s < \hat{s},\) and by \(q_{\min }^{{{\text{neg}}}} ,\) for \(s > \hat{s},\) for given values of Vs > Vf. For completeness, panel b) illustrates the constellation when net losses outweigh net gains, |Vf|> Vs, and the a-priori break-even probability, \(\hat{s}\), is greater than 0.5.Footnote 9

For both market constellations in Fig. 3, we can now contrast \(q_{\min }\) with the actual given quality of the information system qA > 0.5, which we depict in both figures by the dashed horizontal line. For values of s, where \(q^{A} > q_{\min }\), the quality of the information system justifies following its signals to enter the market or terminate the venture. In both figures, this range of a-priori probabilities is titled “justified information allegiance.” In contrast, for a-priori probabilities, s, where \(q^{A} < q_{\min }\), it is justified for the entrepreneur to defy the unreliable signals of the information system and act according to the a-priori expected outcome—she should enter the market for \(s > \hat{s}\) and terminate the venture for \(s < \hat{s}\).

To illustrate the two statements of Proposition 1, consider an overestimation of the actual information quality, i.e., qO > qA. In both panels, qO is a value above the horizontal dashed line. Within the range of justified information allegiance, where \(q^{A} > q_{\min }\), an overestimation of the information quality will not affect its given reliability. Thus, according to the definitions of the a-posteriori probabilities, overestimation of the actual information quality, i.e., qO > qA, may lead to overoptimistic or overpessimistic market expectations, depending on the signal, but with qA determining the actual signals, the entrepreneur’s decision to enter the market or terminate the venture will not be affected by her overconfidence. Within this range, information allegiance is justified in the sense that the signals of the information system guide the entrepreneur to a higher expected outcome, regardless of the entrepreneur’s biased perception of these signals.

For values of s to the left and the right of the range of justified information allegiance in both panels of Fig. 3, one can see that qA < qmin, implying that the actual information system is unreliable because the minimum required quality is too high. These are the ranges in which, according to Proposition 1, the entrepreneur’s decisions may be distorted by overconfidence. To the right of the range of justified information allegiance, it is justified for the entrepreneur to enter the market with no additional information due to a positive a-priori expected return. If the entrepreneur is aware of the rising information requirements (increasing qmin) when expected returns increase (as s rises), then small assessment biases, qO > qA, should not induce her to rely on the information system, as long as she believes that qO is still below qmin. We, therefore, denote the whole area above the qA-line and below the \(q_{\min }^{{{\text{neq}}}}\)-curve by “justified information defiance.” The situation is different, though, with overconfidence high enough to erroneously believe in the reliability of the signal, i.e., \(q^{O} > q_{\min } > q_{A}\). In a market, in which entry is a priori justified, the only signal that can distort the decision to enter the market is the signal to terminate the venture. As Fig. 3 illustrates, sufficiently high overconfidence in a market situation of a-priori justified entry may lead to missed opportunities due to fallible termination. It is important to emphasize that this possibility of a missed opportunity is not a consequence of underconfidence. It is overconfidence in an unreliable information system that induces the entrepreneur to become overpessimistic after an incorrect negative signal. In Fig. 3, one can see that missed opportunities are most likely in markets with high a-priori expected gains or where success is more likely than failure. To the left of the range of justified information allegiance, in markets with negative a-priori expected returns, it is justified for the entrepreneur to terminate the venture with no additional information. With the same reasoning as before, we denote the whole area above the qA-line and below the \(q_{\min }^{{{\text{pos}}}}\)-curve by “justified information defiance.” However, if \(q^{O} > q_{\min } > q_{A}\), the only signal that can distort the decision to terminate the venture is the signal to enter the market. As Fig. 3 illustrates, with sufficiently high overconfidence, excess entry is the consequence of overoptimism in a market situation of justified termination. In both panels, one can see that those fallible entries are most likely in markets with high expected losses. This specific scenario could capture the situation characterized by Hayward et al. (2006), where overestimation drives market entry and leads to high rates of failure.

Underestimation, i.e., qU < qA, is characterized in Fig. 3 by a value below the dashed horizontal line. In the ranges of justified information defiance, qA < qmin, underestimation of the actual quality will only confirm the entrepreneur’s neglect of the information system and, therefore, have no distortionary effects on the entry decision. The situation is different, though, within the range of justified information allegiance, where qA > qmin. If underconfidence is strong enough, such that qU < qmin < qA, the entrepreneur’s bias will induce her to ignore reliable signals of the information system. To the left of \(\hat{s},\) the neglect of a reliable positive signal will erroneously induce the entrepreneur to terminate the venture, with overpessimism leading to a missed opportunity (m.o.). To the right of \(\hat{s},\) the neglect of a reliable negative signal will lead to a fallible entry (f.e.) due to overoptimism.

To conclude, for a given market constellation, the ranges of justified information allegiance and defiance are determined by the actual quality of information, where both figures illustrate how the range of information allegiance widens and the ranges of information defiance narrow when the actual quality of information, qA, rises. Since overconfidence distorts market entry only within the ranges of information defiance and underestimation only within the range of information allegiance, our analysis reveals how the relevance of both dispositional confidence biases is situationally determined by the quality of the information in a specific market environment. Confidence biases may occur at all levels of information quality, but, as the actual quality of information rises, our analysis suggests that the distortionary effects of overconfidence become less while those of underconfidence become more relevant for market entry decisions.

Moreover, as Proposition 1 states, overestimation distorts entry or termination decisions only with an unreliable given information system. As Fig. 3 illustrates, this is most likely in extreme market situations, i.e., with very high or very low levels of a-priori success, and, accordingly, high expected gains or losses. Hence, the relevance of overestimation inducing incorrect market-entry decisions appears to be restricted to extreme market situations. In contrast, underestimation distorts entry or termination decisions in market situations where a-priori success and failure are balanced, with low expected gains or losses. If the former market situation corresponds to what Moore and Healy (2008) refer to as a “difficult task” and the latter to a “simple task” then both could induce the biases observed in their experiments.

As a caveat to our analysis, note that our sharp distinction between ranges of justified information allegiance and defiance assumes that the entrepreneur has a bias only in her perception of information quality while knowing precisely all the other parameters of the decision problem and how they are functionally related to each other. This applies, in particular, to \(q_{\min }\), which maps the boundary between reliable and unreliable information in Fig. 3 in a non-trivial way. More realistically, one might assume that the entrepreneur does not know the course of \(q_{\min }\) in Fig. 3, or that she may not know that a critical value \(q_{\min }\) even exists. Could low overconfidence in unreliable information, i.e., \(q_{\min } > q^{O} > q^{A}\), or low underconfidence in reliable information, i.e., \(q_{\min } < q^{U} < q^{A}\), then also lead to fallible entries or missed opportunities? The answer is yes. This, however, applies generally when the entrepreneur erroneously follows an unreliable information system or neglects a reliable information system. What drives the fallible decision here is the entrepreneur’s structural ignorance, which should not be confused with the very specific perceptional bias of over- or underestimation.

5.2 Biased confidence in acquiring an information system

After looking at the biased estimation of a given quality of information, we now go one step further by investigating how over- or underconfidence may affect the actual quality of acquired information. We do this by treating the quality as the endogenous outcome of an investment decision based on a cost–benefit analysis. We thus widen our analysis from the value of having information to the economics of acquiring information (Stigler 1961). The benefit of additional information is given by the information value (IV), i.e., the difference between the expected outcomes with information acquisition (IA) and with null information (NI). In Fig. 1, this is the difference between the expected outcomes of following the upper and the lower branches of the decision tree. As Chwolka and Raith (2012) show for their binary decision problem, the information value rises linearly in the quality of information for \(q \in [q_{\min } ,1].\) This is depicted for our model in Fig. 4 by the linear function IV(q) for some arbitrary value of \(q_{\min } \ge 0.5\).

The decision maker’s optimal (unbiased) quality of acquired information, \(q_{A}^{*}\), and the reduced quality of information \(q_{A}^{O}\) under overconfidence

To acknowledge that acquiring information is costly, we assume specifically that the (actual) cost of additional information is a convex function \(C_{A} (q)\) of the quality q of the information system, beginning at qmin with an arbitrary fixed cost and rising exponentially as q increases (Chwolka and Raith 2012). The net benefit of information is given by the difference between the information value IV(q) and the (actual) cost of the information \(C_{A} (q)\). In Fig. 4, the resulting actual net benefit of the information is shown as the concave function \(NB_{A} (q),\) with a maximum at \(q_{A}^{*}\). This is the optimal quality of information, which will rationally be chosen by an entrepreneur with unbiased beliefs (i.e., who is neither over- nor underconfident). With \(q_{A}^{*} > q_{\min }\)(where \(q_{\min } \equiv \max \left\{ {q_{\min }^{{{\text{pos}}}} ,q_{\min }^{{{\text{neg}}}} } \right\}\)), we know that the optimally chosen quality of information, if it exists, will always be reliable (cf. Fig. 3).

To introduce overconfidence, we follow Hayward et al. (2006, p. 167), who argue that “more overconfident [founders] will underestimate their ventures’ need for initial resources.” Accordingly, we assume for the current setting that overconfident entrepreneurs underestimate the resources required and thus the costs for acquiring information of a given quality, or, conversely, that they overestimate the prediction ability (information quality) that they obtain for the amount of resources invested. According to Meissner and Wulf (2016), this seems more likely for firm-internal than -external acquired information. In Fig. 4, overconfidence would thus shift the entrepreneur’s perceived cost curve downward or outward. Without loss of generality, we assume that the cost curve rotates downward, as shown by the dashed curve CO(q).Footnote 10 With underconfidence, the exact opposite effects would occur. The economic consequences of these perceptional biases are stated in the following proposition.

Proposition 2

If overconfidence induces the entrepreneur to underestimate the costs needed for a certain quality of information q, i.e., CO(q) < CA(q), then the actual quality of the chosen information system under overconfidence, \(q_{O}^{A} \), will be lower than the unbiased optimal information system, i.e., \(q_{O}^{A} < q_{A}^{*}\). As a consequence, overconfidence will lower (raise) the likelihood of market entry for s > 0.5 (s < 0.5). Conversely, if underconfidence induces the entrepreneur to overestimate the costs of information, i.e., CU(q) > CA(q), then the actual quality of the chosen information system, \(q_{U}^{A}\), will be higher than the unbiased optimal information system, i.e., \(q_{U}^{A} > q_{A}^{*} \). As a consequence, underconfidence will raise (lower) the likelihood of market entry for s > 0.5 (s < 0.5).

As Fig. 4 illustrates, overconfidence induces the entrepreneur to choose a (perceived) quality level of \(q_{O}^{*} < q_{A}^{*}\) based on the perceived net benefits NBO(q) (dashed curve). However, with the choice of this perceived optimal quality \(q_{O}^{*}\) determining the costs, \(C_{O} (q_{O}^{*} )\), the actual quality \(q_{O}^{A}\) of additional information, corresponding to this investment, \(C_{A} (q_{O}^{A} ) = C_{O} (q_{O}^{*} )\) will turn out to be lower, i.e., \(q_{O}^{A} < q_{O}^{*}\). Hence, the overconfident entrepreneur’s perceived quality, \(q_{O}^{*}\), is again higher than the actual quality,\(q_{O}^{A}\), of additional information. In addition, with \(q_{O}^{A} < q_{A}^{*} \), the actual quality of the acquired information system is now lower than the chosen quality of the non-overconfident entrepreneur. In contrast to Sect. 5.1, where overconfidence in a given information system did not affect the actual quality of the information, overconfidence in acquiring information now reduces the quality of information.

Nevertheless, with \(q_{O}^{A} > q_{\min }\), the actual information system under overconfidence will remain reliable enough to follow its signals. However, as we have shown in Eqs. (2), the actual quality of information determines the resulting probabilities of positive and negative signals. Consequently, the lower actual quality of information \(q_{O}^{A}\) will affect the entrepreneur’s market entry behavior through the signals that it induces. According to Proposition 2, when market success is a priori more likely than failure (s > 0.5), the lower quality of the information system leads to a higher probability of negative signals that induce nascent entrepreneurs to terminate their projects. Hence, with less reliable signals due to overconfidence, there will be more missed opportunities. As stated before, it is overconfidence rather than underconfidence, which discourages market entry. In contrast to Hogarth and Karelaia (2012), though, the missed opportunities in our setting are not the consequence of a fallible decision to terminate the venture. This decision is fully justified by the reliable negative signal. The likelihood of missed opportunities increases because of the lower actual quality of the chosen information system. It is this choice that is fallible. Interestingly, if we apply our setting here to the PSED sample in Table 1, which we calibrated with a value of s > 0.5, overconfidence should lead to a reduction rather than an increase in market entries. The opposite occurs in markets where success is a priori less likely than failure (s < 0.5). Here overconfidence promotes entries, which seems to correspond more to the view of Hayward et al. (2006). Yet, one must acknowledge here as well that these are not fallible excess entries. The increased entries are fully justified by the reliable signal, but which is based on the fallible choice of a poorer information system. In both cases, since the actual a-posteriori probability of success decreases with the actual quality of information, \(q_{O}^{A} ,\) the actual mean outcome of acquired information will decrease as well. In line with Knight (1921), the likelihood of failure increases for reasons that are now rationally related to the use of informational resources.

In summary, one may very well assume that entrepreneurs are prone to overconfidence, just as other decision makers are in other decision contexts. To understand if and how overconfidence affects market entry, one must understand how and why it affects the entrepreneurial decision process leading to market entry. Due to the ambiguity of the results that we obtained in this simplified decision framework, one can expect even more contradicting effects in a richer setting, which will then also affect empirical analyses. Consider, for example, a rich entrepreneurship panel, such as the PSED, with the data of many entrepreneurs featuring different educational and professional backgrounds, who are at different stages of their venture process targeting different markets. Any behavioral hypothesis of overconfidence that fails to acknowledge the ambiguities that we have revealed in our Propositions 1 and 2 will be highly speculative.Footnote 11 Since there is no reason to assume that the ambiguity will decrease within a more complex decision context, we believe that further theoretical research along this line is required to shed light on the, often, contradictory results in the empirical literature. At this point, we find it difficult to present even a theoretical case for overconfidence as a driver of market entry. Indeed, one may question why this is so important. We address this question in the next section.

6 What makes overconfidence an entrepreneurial trait?

Although the experimental evidence holds mixed results, and our theoretical analysis also reveals ambiguous effects, there seems to be a strong belief among (empirical) entrepreneurship researchers that overconfidence does, indeed, increase the likelihood of market entry. The question remains, though, whether this empirical finding is sufficient to establish overconfidence as a characteristic trait of market entrants and, in particular, as a caricature of entrepreneurs (Chen et al. 2018). Suppose, for example, that the probability of market entry is higher for an overconfident than for a non-overconfident decision maker (Camerer and Lovallo 1999), where the specific notion of overconfidence—overestimation, overplacement, or overprecision—is irrelevant for our argument. In conditional probabilities, one can state this formally as \({\text{P}}(E|O) > {\text{P}}(E|\overline{O})\), where E denotes market entry and O denotes overconfidence. According to Bayes’ rule, this statistical relationship is equivalent to \({\text{P}}(O|E) > {\text{P}}(O|\overline{E})\), stating that one is likely to find a higher share of overconfident people in the market than outside. Hence, if one is on the lookout for overconfidence, the market is a proven area. However, this statistical feature could be a source of confusion in the literature, where captivating stories of popular overconfident entrepreneurs may suggest that this is a general entrepreneurial feature in the sense that most market entrants are overconfident. The following proposition emphasizes that this conclusion is incorrect.

Proposition 3

Even if overconfidence increases the likelihood of market entry, then this does not imply that overconfidence is a characteristic feature among the majority of market entrants.

To illustrate the implications of Proposition 3, suppose that the likelihoods of market entry for overconfident and non-overconfident entrants are given by \({\text{P}}(E|O) = 0.75\) and \({\text{P}}(E|\overline{O}) = 0.4\), respectively, implying that overconfidence has a strong impact on market entry. In addition, let us assume that overconfidence is not a common trait, but characteristic for only a minority of the whole population, say 20%—this is larger than the share of new and established business owners in most countries (Bosma et al. 2020). With \({\text{P}}(O) = 0.20\), we can apply Bayes’ rule to obtain

showing that overconfidence is, indeed, more prevalent among market entrants than among non-entrants. Yet, a share of overconfident market entrants of less than 1/3 makes it difficult to defend overconfidence as a characteristic feature of market entrants or, more specifically, of entrepreneurs, who make up only a small share of the population. Even if overconfidence does spur market entry, it is a misleading exaggeration to conclude that overconfidence is a characteristic feature of market entrants.

7 Discussion, implications, and conclusions

With this paper, we question the established trend of overconfidence (Shepherd et al. 2015; Thomas 2018) in entrepreneurship research both from an empirical as well as theoretical perspective: Is overconfidence an accurate description of entrepreneurs’ beyond-average behavior? Is it necessary or even helpful for entrepreneurship practice, policy, or teaching to view individual entrepreneurial decision making, in particular the decision to enter markets, as driven by perceptional biases?

Within our decision-theoretical framework, we have shown that entrepreneurial behavior, which is often attributed to overconfidence, can just as well be explained with rational decision making if the entrepreneur’s use of information is considered. Our decision-theoretical approach here is in line with the traditional subjectivist view of the entrepreneur as an expert in the use of knowledge (Casson 2003, 2005; Harper 1996). Overconfidence, as a caricature of entrepreneurship (Chen et al. 2018), may contribute to a more mysterious picture of entrepreneurs as economically, socially, and politically relevant actors, but it is difficult to imagine how one should address, promote, or educate entrepreneurs, who are known to systematically make decision errors. If their activities are regarded as crucial for economic prosperity, is this despite or because of their overconfidence? As we argued from several perspectives in this paper, we see no empirical, theoretical, or statistical reason to support the portrayal of the overconfident entrepreneur. It is doubtful whether the understanding of entrepreneurial behavior and the promotion of entrepreneurial action has substantially improved over the past decades through the assumption of entrepreneurial overconfidence.

Yet, if overconfidence is a feature of decision making, in general, then we must also acknowledge its presence in entrepreneurial decisions, and we need to understand more about the influence of this bias on the decision-making process (Thomas 2018). Our theoretical analysis illustrates the importance of understanding (1) where overconfidence enters the decision process and (2) through which channels it may or may not distort the decisions of the entrepreneur. Since the effect of overconfidence depends on the specific decision context, the analysis of the decision must include the information acquired and used by the decision-making entrepreneur, in order to capture not only the dispositional but also the situational component of overconfidence. The power of our decision-theoretical analysis is that it identifies effects that cannot be empirically observed, such as missed opportunities due to fallible terminations. This also reveals the main limitation of our approach, as the propositions that we derive cannot be employed as testable hypotheses, because the relevant data in the field is not available. The quality variable q offers a precise measure for overestimation, which could be well measured in the laboratory with repeated experiments (Adams 1957; Oskamp 1965). It could also be used in practice where past prediction data is available, e.g., in assessing the performance of investment brokers or venture capitalists (Zacharkis and Shepherd 2001). The problem with firm founders is that past data of their predictive ability is, in general, not available. Nevertheless, the quality of their predictions will have a crucial influence on the nature and success of their decisions. Our theoretical analysis enables us to identify the various channels through which overconfidence may affect these decisions.

Our findings and propositions reveal directions for future empirical research. To identify overconfidence, empirical research must capture how information is used by entrepreneurs in their decision process (McCann and Vroom 2015) or, more generally, in the whole process of value creation (Pinelli et al., 2021). As we have shown, the focus on observed deviations from average behavior alone is not sufficient to draw convincing conclusions on what drives entrepreneurs to do things that others find too risky. A closer look at acquired information sources (Meissner and Wulf 2016), and a comparison with regard to the conclusions drawn for specific decisions, e.g., concerning market entry, investments, growth strategies, etc., will help us understand more about the quality of different types of information and thereby also the justified confidence that they entail. From an exchange-based view of entrepreneurship (Pinelli et al., 2021), this should be particularly important for the interaction with other stakeholders, e.g., investors, whose evaluation of a venture depends on the degree to which they discount the optimism of the entrepreneur (Dushnitsky 2010). Moreover, with acquired information often coming from external sources, such as consultants, who themselves may be prone to overconfidence or under pressure to succeed in influencing decision makers, simple misjudgments of externally provided information may have the same distorting effects on entrepreneurs’ decisions as their own biases, although the practical implications of both will be quite different. Future theoretical and empirical research will hopefully address the effects of alternative information sources.

The nature of the information employed by the entrepreneur will also shed light on what type of decision maker she is—planner or effectuator, calculator or gut decision maker, driven by experience or by advice. This may help us understand whether specific types of decision makers are more susceptible to overconfidence than others, thereby addressing the agenda of Shepherd et al. (2015). If business planning and the calculations that it entails helps to curb overconfidence (Hogarth and Karelaia 2012), could it be that causation (Sarasvathy 2001) is less prone to overconfidence than effectuation? Are heuristics based on experience a safeguard against overconfidence? The answers to these questions, of course, must be assessed against the more fundamental question of whether overconfidence is good or bad for innovation and economic development. As Bernardo and Welch (2001) have argued, overconfidence may, indeed, lead to higher benefits for society, albeit at the expense of individual entrepreneurs.

While empirical research can provide valuable insights into the varying specificities of entrepreneurial decision contexts, more decision-theoretical research is required to understand how modifications of the decision context, e.g., through overconfident assessments of the entrepreneur, will affect the decision outcomes. In our analysis, we have taken up only one example related to market entry to show how overconfidence in information acquisition yields lower levels of information quality, which, in turn, may lead to a higher or a lower likelihood of entry, depending on the a-priori probability of success. The channels through which overconfidence operates will differ, though, for strategic decisions in the market or investment decisions. We believe that more elaborate theoretical decision models along the line of our approach may help to provide a better foundation for empirical research.

The important aspect of a theoretical approach is that a clear understanding of how confidence biases affect the decision maker also provides insight into ways of dealing with them, both at the individual as well as the political level. Here a decision theoretical perspective could provide valuable hypotheses, in particular for longitudinal empirical analyses along the lines of Manso (2016) or McCann and Vroom (2015), who relate experimentation, planning, and information acquisition activities to self-efficacy and performance expectations. A decision theoretical foundation could provide sharper hypotheses and point out potential relationships that are worth investigating. For example, self-efficacy could be measured by justified confidence and thereby serve as a benchmark for identifying over- or underconfidence.

Our theoretical results also have important implications for nascent entrepreneurs in practice. As all decision makers, entrepreneurs are probably prone to confidence biases, and it is important to understand psychologically how these situations may arise. The business plan, as a documentation of the rational planning process, may serve as a safeguard against over- or underconfidence. If appropriately done, it reveals the coherence or incoherence of the entrepreneur’s predictions and strategies.

For teachers of entrepreneurship, if they believe that entrepreneurship is driven by overconfidence, it is not clear whether they should teach any systematic approach to venture creation. As we have shown, however, the rational paradigm acknowledges all the crucial aspects of entrepreneurial decision making, regardless of whether they are planners or effectuators. Moreover, it provides a benchmark for identifying deviations due to psychological traps. If valuable information leads to decisions and actions that others would not dare, then teaching entrepreneurial decision making could increase the value and decrease the costs of information.

Finally, for policy makers, who rely on entrepreneurship as the engine of innovation and economic growth, it makes a fundamental difference, whether this process is driven by an underlying logic or mostly by decision errors. Surely, the individual entrepreneur cannot be regarded as being fully rational, but what matters for policy makers is whether behavior, in general, follows some conceivable rationale, because this is the basis for policy measures. For society, in general, and politics, in particular, it is important to know whether or not overconfidence should be promoted. Although overconfidence may spur innovations that are beneficial to society, the investment in an individual entrepreneur is likely to be riskier.

To conclude, we doubt that the view of the overconfident entrepreneur is necessary or even helpful. On the contrary, seeing the entrepreneur as a rational information manager provides sufficient possibilities for venture creation, policy support, or entrepreneurship education. Of course, even a rational information manager may be affected by confidence biases. As we have argued throughout the paper, the relevance of this aspect for entrepreneurial performance is debatable. As a consequence, we advocate (the return to) an entrepreneurship paradigm based on a rational information manager with a focus on the systematic creation and exploitation of opportunities.

Notes

More generally, with multiple signals and a smaller number of alternatives, one would have to specify how the observed signal relates to the alternative actions. The general logic of this specification is best understood with two signals and two alternatives, which, according to Klayman et al. (1999), also appears to be the choice scenario of greatest practical relevance.

We ignore here the case of q ∈ [0, 0.5], which is possible, but characterizes more a technical peculiarity, where the quality of information, again, becomes more reliable, albeit incorrect.