Abstract

Nowadays, platforms in many industries offer content for a (monthly) flat rate (e.g., music streaming). While flat rates are efficient in reducing transaction costs for administering customers, platforms’ rules for remunerating content right holders are crucial for royalty allocation and, as a result, heavily discussed in several industries. The music industry’s business practices could be on the verge of their next disruption. There is an ongoing heated debate with respect to how the income of flat rates through streaming services should be allocated to right holders (labels and artists). This research investigates aspects of the supply and demand side effects as well as the resulting monetary consequences of changing the currently applied proportional-to-usage remuneration policy (pro rata) to a user-centric policy. Using individual-level data from 3,326 participants and data from Spotify’s API, we empirically quantify the monetary consequences of this change for the music industry. Depending on the remuneration system, we find a substantial reallocation of nearly 170 million € per year at Spotify. We discuss demand and supply-side consequences that may change the way music is currently produced and consumed. We conclude with a research agenda on the impact of business conventions for users, platforms, and artists in the music streaming industry.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

How Many Music Streams Does It Take to Earn a Dollar?

www.visualcapitalist.com/how-many-music-streams-to-earn-a-dollar

Which is the best streaming service for supporting artists?

www.theguardian.com/technology/askjack/2019/oct/31/best-streaming-service-mp3-pays-artists

Subscription-based platform services

Platforms serve as (two-sided) markets in which demand meets supply. They are popular for digital content or services that “are non-rival, have near zero marginal costs of production and distribution, low marginal costs of consumer search, and little transaction costs” (Lambrecht et al., 2014, p. 331). Many global market leaders in the music, motion picture, and gaming industries, such as Spotify, Netflix, and Electronic Arts, provide online access to digital content, which is attractive to consumers because the platforms offer large assortments at reasonable prices (Carroni & Paolini, 2020; Datta et al. 2018).

The introduction of affordable flat rates for customers increased the popularity of online platforms. Many consumers prefer flat rates for large assortments, even if the rate is not the least costly tariff (Lambrecht & Skiera, 2006), for two main reasons: the “insurance effect” (with no variation in consumers’ monthly billing rate) and the “taxi meter effect.” Usage of content paid beforehand can be enjoyed as if it were free instead of watching a running taxi meter (Prelec & Loewenstein, 1998). Thus, flat rates are popular among customers.

Flat rates are also efficient in reducing transaction costs for administering customers (Rindfleisch & Heide, 1997). As the assortments of digital content are often quite large (e.g., 70 million songs for Spotify), platforms prefer to apply the simplest rule for remunerating the content offered by content right holders. Such a rule takes the revenue of the platform, subtracts a certain percentage as a service fee, and distributes the remaining “pot of money,” which we define as total royalty, proportional to the overall usage of the content. Note, these market structures can be found in several completely unrelated industries (outside of digital entertainment services, e.g., music streaming) whenever an aggregator offers product or service bundles at a flat rate. For example, in local public transportation services, an aggregator may bundle various public transportation offers from different suppliers in one integrated service. Then, customers pay a monthly fee while the suppliers are paid by relative usage that is determined via admission controls or surveys (e.g., TranSystems, 2009).

In general, the economic success of platforms in terms of profit is mostly determined by their incoming subscription (and advertising) revenue, but also by the procurement costs for content or services. Therefore, we analyze the consequences of choosing a certain content remuneration model for both the supply side and the demand side.

The rise of music streaming usage has continuously been accompanied by discussions of how much streaming services pay the products’ right holders–our two introductory headline quotes underline this debate. However, the current debate in the industry centers less around how much money will be paid but rather mainly on how the money that is collected by streaming services via flat rates (or advertising) from users is allocated to the right holders. Specifically, the two remuneration models outlined in more detail below are fiercely debated today (e.g., Theurer, 2020):

-

Pro rata: The revenue from all subscriptions is divided by the total number of streams. Thus, the monthly payout per stream is based on its market share across all users.

-

User-centric: The revenue from each single user is divided by the total number of streams generated by this user. Thus, the monthly payout per stream is based on its market share of each individual user and may vary across users.

The heated debates focus on the currently applied pro rata remuneration policy, which is the industry standard, whereas many artists demand a change toward a user-centric model (Theurer, 2020). In fact, the streaming service Deezer started an online campaign promoting a user-centric system (Deezer, 2019). On the contrary, the pro rata system is defended by Spotify’s director of economics, Will Page, as the most efficient payout system due to low administration costs (Page & Safir, 2018). This debate raises the question on the managerial consequences of different remuneration policies for the creation and consumption of media products. Changing remuneration policies may potentially lead to substantial shifts in the competitive landscape of the music industry as these policies would introduce new supply and demand dynamics.

While the question of how streaming affects the industry has been addressed in recent articles (e.g., Wlömert & Papies, 2016, 2019; Aguiar & Waldfogel, 2018), there is hardly any research related to the remuneration model implemented by the platforms. This is surprising given the high economic relevance of platforms and the considerable media attention to the discussion of different content remuneration models (especially in the music industry; e.g., Theurer, 2020). Both the design and outcome of the remuneration of content providers by platforms have received scant attention from marketing scholars (see the analytic work of Amaldoss et al., 2021). Page and Safir (2018) conceptually discuss the problem and argue that the payout system should be balanced between equity and efficiency, and plead for keeping the pro rata model.

We address this research gap and clarify the supply and demand side consequences by calculating the difference in allocation between the pro rata and the user-centric payout policies. We focus on genres as allocation units (Lena & Peterson, 2008) and find substantial monetary consequences with a shift away from a pro rata model to a user-centric model. Our empirical study relies on data at the individual level taken from an online panel survey of the German population in January/February 2019 (n = 3,326 participants) that is enriched with genre-specific song profiles from the Spotify API as well as the analysis of time-related chart positioning.

While a change of the remuneration system does not change the revenue of the streaming service, we find substantial financial consequences for right holders resulting from supply and demand side effects that suggest a substantial reallocation of the revenue contributions from mainstream to niche genres. The financial impact on royalties accumulates to nearly 170 million euros p.a. from Spotify alone (reallocated from mainstream to niche genres). We provide an analysis of the revenue shifts between major labels when switching from a pro rata to a user-centric model and find substantial reallocation effects between them.

In addition to our empirical results, we provide a research agenda that may serve other researchers as inspiration to generate new theoretical, analytical, or empirical insights in this important field. For example, we find initial support for incentives to “optimize” the content in a pro rata model. These are supply and demand side driven. Specifically, we find that overall song length has decreased by 2.5 s. per year (-10% over the last five years) and a 30% increased label share for hip hop in the Billboard Top 100 Charts over the last 10 years. We believe that additional research is needed and therefore provide an overview that focuses on pressing marketing issues from the demand and supply perspective.

Overall, this research may help artists, labels, and streaming platforms discuss the monetary effects of the two debated remuneration models in their ongoing negotiations. The findings are also of interest for policy makers seeking to support local or niche artists since the findings show that massive revenue shifts can be expected when streaming platforms shift the remuneration model from a pro rata to a user-centric model.

Content remuneration by flat-rate platform services

Systems of content remuneration

A review of platform services across industries reveals two general kinds of remuneration systems when offering large content assortments to consumers (Table 1). First, platforms produce or license content from suppliers and offer the content as a bundle to consumers. Second, platforms offer content providers (e.g., artists, labels) an upload interface to provide their content, and the right holders receive a royalty based on the total revenue of all customers (pro rata) or the revenue of individual consumers (user-centric).

A platform’s choice of content remuneration model depends on transaction costs, risk effects, and competition. First, procuring large assortments of content results in high transaction costs (Rindfleisch & Heide, 1997) if each contract is negotiated individually. Recently, the music streaming platform Spotify (2021) noted having more than 70 million songs, so individually negotiating contracts per song is not efficient. Therefore, the platform offers the same conditions for all songs and distributes 70% of its revenue as royalty to the right holders of the content proportional to its consumption. This model facilitates both the procurement and the administration of remuneration. By contrast, the number of movies available in an assortment is much smaller in the movie industry (Netflix has roughly 4,000 movies available online per country; Statista 2021). Thus, platforms such as Netflix individually negotiate the conditions for new movies or movie bundles in a license model.

Second, platforms procuring content also consider risk effects in designing remuneration models. For example, if the supplied content is paid for by the platform according to its consumption, the risk is shifted to the supplier. This shifting of risk worries content providers when fraud generated by “streaming farms” leads to unfair usage—a common issue in the field of music streaming (Carr 2020). However, if the price for content is negotiated individually and independent of consumption, the risk shifts to the platform offering the service (e.g., Avinadav et al., 2021) as observed in the movie industry.

Third, platforms face competition not only in procuring new high-quality content but also in attracting as many (premium) subscribers as possible. When critical mass has been reached, platforms mainly compete against one another based on the contractual setting (e.g., the price for a flat rate, subscription period, number of users per subscription) and the platform assortment (e.g., assortment size, content quality; Kübler et al., 2021). A platform’s market position weakens when there is exclusive content from suppliers, and a competitive threat occurs when other platforms can potentially meet the needs of unsatisfied consumers with exclusive, better, or cheaper content.

The question of how the remuneration of the content providers affects competition has received scant attention in the (analytic) literature. Avinadav et al. (2021) find that distribution platforms selling virtual products can improve profits by implementing a menu of contracts for revenue sharing over unified contracts with suppliers, given the content exceeds a minimum quality level. However, empirical studies that explicitly compare the monetary outcome of content remuneration models and consumers’ fairness perceptions of the models implemented by platforms are missing. We address this research gap and focus on streaming platforms in the music industry that currently apply the pro rata content remuneration model. This model is highly attractive for platforms because of its low transaction costs, minimal risk, and limited competition. These platforms, however, may be challenged by competitors offering user-centric remuneration for consumers who prefer that their payment only goes towards the content they use.

Comparison of pro rata and user-centric content remuneration systems

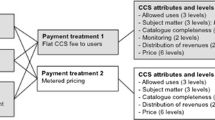

Comparing remuneration models for content providers requires an analysis of the relevant supply- and demand-side factors influencing the allocation of the total royalty generated by a streaming platform across content providers. Figure 1 summarizes the characteristics of the two remuneration policies, pro rata and user-centric, using the streaming platform Deezer (2019) as an example.

Comparison of remuneration models for subscription accounts (visual related to Deezer, 2019)

Figure 1 shows our comparison of a pro rata and a user-centric content remuneration model, focusing on three drivers that may lead to different royalty payouts for content providers (labels and artists). First, streaming services offer their customers different subscription plans, such as a full-priced account, a reduced account (e.g., students, families), and even a free option that is monetized through advertising. Consequently, the revenue contribution per individual subscription varies. Second, the amount of royalties for content providers depends on consumer listening behavior. Consumers differ in their listening behavior, which is depicted in their music choice and the amount of music (number of streams) to which they listen. Additionally, the listened songs vary in their song length, which, assuming constant listening times, affects the number of generated streams. Third, distributed royalties depend on the allocation rule applied by the streaming service.

Our example contains the streaming service Deezer, two artists (content providers), and two customers who differ in their characteristics. Amber subscribed to the reduced price of €5 per month, while Sasha is paying the complete price of €10 per month. The listening behavior of both customers also differs. Amber is a music aficionado and generates 90 streams, while Sasha only generates 10 streams. The total revenue generated is €15 (€5 + €10), while the total number of streams generated is 100 (90 + 10). Amber only listens to Artist 1, while Sasha only listens to Artist 2, so 90% of all streams are generated for Artist 1, while the remaining 10% of streams are generated for Artist 2.

Before we compare the specific royalties of the applied content remuneration model, we note that the share the streaming service withholds as service fee (e.g., Deezer) is €4.50. A common practice across all major streaming services is to keep roughly 30% of the total revenue and distribute the remaining 70% as remuneration to the service providers (Eriksson et al., 2019; Spotify Technology S.A., 2018). In this case, the share of the streaming service does not depend on the applied remuneration model as the service fee is deduced before distribution and just the remaining 70% of revenue is allocated to content providers (70% of €15 = €10.50).

Focusing on the different levels of royalty payments to the content providers, we begin with the pro rata model that is currently used by all major streaming services (Eriksson et al., 2019) and compare it with the outcome of a user-centric model:

-

Pro rata (proportional-to-usage remuneration system) allocation: A pro rata remuneration is based on the total revenue and the market share of the respective song on the streaming service. In this case, the market share of streams for Artist 1 is 90%, resulting in 90% × €10.50 = €9.45, while Artist 2 receives 10%, resulting in 10% × €10.50 = €1.05. This outcome leads to the situation in which Sasha implicitly supports Artist 1 by paying royalties for him, an artist to whom he never actually listened (Flynn, 2015; Marshall, 2015). Furthermore, Artist 1 was listened to by Amber with a reduced subscription price of €5, while Artist 2 was only listened to by Sasha with a full-priced account.

-

User-centric allocation: In the alternative user-centric remuneration model, the revenue contributed by an individual consumer is distributed only according to the individual listening behavior of that customer. In this case, the payments of a customer are only distributed across the artists to whom this customer listened; the distribution is not affected by the listening behavior of other customers using the streaming service. Thus, unlike the pro rata model, this policy cannot result in a situation in which a customer implicitly supports an artist not listened to (see Fig. 1).

The structure of a remuneration model can allow different levels of abuse. For example, the pro rata model allows individual consumers to upload their own songs and to use click generators to create artificial streams that lead to a redistribution of revenue. In addition, some artists have asked their listeners to play their music silently while asleep to generate a larger share of remuneration (Billboard, 2014). Click fraud has no effect in a user-centric model because only the revenue from the respective customer is affected (Dimont, 2017).Footnote 1

Indeed, the streaming service Deezer started an online campaign promoting the user-centric remuneration model as the fairer system, suggesting a respective change (Deezer, 2019). By contrast, Spotify’s director of economics defended the pro rata model as the most efficient payout system due to low administration (transaction) costs (Page & Safir, 2018). Moreover, Page and Safir (2018) argue that it might be considered inequitable that the average payout per stream differs between each customer in the user-centric remuneration model. In the extreme case in which a customer generates only one stream, the entire subscription fees of this customer (after the deduction of the platform's share) are allocated to this one stream. Thus, one stream can generate 5€. However, a stream of the same song could be worth €0.001 if the customer generates, e.g., 5.000 streams that month (5€ / 5.000 streams). In a subsequent report, Page and Safir (2018) discuss the attractiveness of both remuneration models from the artist’s perspective. An artist whose fans have little diversity in their listening behavior and low usage will prefer the user-centric remuneration model as the artist can gather a large share of the subscription fees from the respective users. In a pro rata remuneration model, a customer with low usage would only marginally affect the royalties of this artist. By contrast, an artist whose fans have little diversity but high usage will prefer the pro rata remuneration model as this can increase the artist’s share of total streams on the platform. In their concluding remarks, Page and Safir (2018) propose modifying the pure forms of both remuneration models, factoring in qualitative criteria such as the song’s length and work valuation.

We argue that in a digital transaction system with well-defined interfaces, transaction costs should not differ much between a pro rata and a user-centric remuneration model. Furthermore, risk considerations should also not be of relevance for a platform as the platform claims its revenue share before allocating the remaining revenues across the right holders.

Next, we outline our framework and data that we collected to quantify the financial consequences and their resulting impact on the market players.

Empirical study: Monetary outcomes of content remuneration models

Framework and data

We compare the monetary outcomes of the two content remuneration models in the music streaming market by using the currently applied pro rata model as a benchmark and simulating the outcomes when changing to a user-centric remuneration model. This way we can assess the differences between the two content remuneration models and, thereby, the relevance of choosing between these alternatives. Our empirical study also decomposes the outcome into effects of different drivers coming from both the supply and demand side.

Quantifying the revenue effects of a change to a user-centric content remuneration model requires data on the music consumption of individual people. Due to the lack of data on artist level, we chose the genre as the unit of analysis because genres are the fundamental categorization scheme for both companies and consumers in the music industry (Lena & Peterson, 2008). By analyzing more highly aggregated data, we obtain a generalized picture of the relationships and therefore create direct managerial implications. Additionally, consumers’ music taste can be effectively classified by genres, and information about genres helps consumers in their search for musical acts.

As streaming services’ individual-level subscriber data are not available, we simulate the consequences with the help of a survey we conducted through a professional panel provider (Respondi) with a representative sample, according to age (average of 46.2 years) and gender (49% women), of the German population from January–February 2019 (3,326 respondents). The survey enables us to differentiate between 20 different genres and captures detailed information about music consumption in general, in addition to music streaming behavior (43.6% streamers). To simulate the contribution and reception of artists in a particular genre, we combined the survey data with genre-specific song profiles. Using the Spotify API for each of our 20 genres, we identified 200 artists (= 4,000 artists in total) assigned to that genre by Spotify and collected information on the 10 most successful songs by those artists. The information on 40,000 songsFootnote 2 allowed us to measure the average duration of a song by genre that has a direct impact on the number of streams a person can generate when listening to music for an hour. Using this information, we calculate the influence of potential drivers on the resulting royalties from the supply and demand sides by considering (1) the individuals’ interest in genres, (2) the individuals’ listening time per genre, (3) the individuals’ subscription fee, and (4) the mean song length per genre.

Interest in genres

We applied a two-step approach to gain knowledge on genre interest. We first asked our respondents to indicate which of the presented genres they associate their music taste with. We found a considerable difference in the number of people who are interested in mainstream genres (95% are interested in international pop and 86% in international rock) over all other genres (average interest of 27% per genre). Then, we asked respondents to allocate 100 points between the genres of their interest to gain a more precise picture. Summing up everyone’s interest in a specific genre (a person allocating 20 points to a genre counts as 0.2 people for that specific genre) resulted in the distribution of interest (Fig. 2).

Distribution of genre interest from respondents. Note: HHR = hip-hop rap; EDM = electronic dance music; R&B = rhythm and blues. Two-step question approach: “To which of these genres would you classify your musical taste?” and “How often do you listen to each genre? (Please distribute 100% across all genres).”

Listening time

We asked our respondents how much time they spend streaming music per week (continuously scaled). The histogram of our survey data indicates that the listening time across customers substantially varies (Fig. 3, left panel). While roughly 20% of the respondents did not listen to music within the last seven days, nearly one-third listened to music for more than five hours in the same period. However, most of the respondents (nearly 50%) listened to music for more than zero hours but less than five hours within the last seven days. On average, consumers listened to 5.9 h of music via streaming services per week (3.1 h free streamers and 7.2 h paying streamers). The high variance in listening time in a user-centric remuneration model implies very different royalties per stream across customers.

Distribution of listening time and payment per consumer. Note: Among other types of music consumption, the question was: “How many hours have you listened to music in the last 7 days? g) Free music streaming services (only the free ones with advertising interruptions), h) Paid (subscription) music streaming services incl. free test accesses & vouchers (e.g., Spotify Premium, Deezer Premium, Apple Music, Amazon Music).”

Revenue per customer (payment)

Although all customers have unlimited access to the product via the subscription fee (as a flat rate), price differentiation occurs by granting discounts such as student rates or family packages, which result in varying revenue contributions per customer. Figure 3 (right panel) displays the histogram of paid subscription fees per individual. Note that many individuals use platforms offering free advertising-based content and therefore have paid zero fees. However, they potentially influence the royalty payouts to a great extent.

Song length

We analyzed the average song length per genre by scraping the song length of 40,000 songs (2,000 per genre) via the Spotify API. Figure 4 displays the genre’s percent differences in mean value (216 s) across all genres. For example, 17% for the metal genre reflects a 17% longer song length of 255 s than the mean song length (216 s) across all genres. Some genres, particularly jazz, blues, and metal, have an on-average longer song length and therefore generate fewer streams in a given time, while pop, hip-hop rap (HHR), electronic dance music (EDM), and German folk are favored by a shorter song length. A longer song duration results in less generated streams per period and is consequently disadvantaged when it comes to royalty allocation.

Distribution of song length for genres. Note: R&B = rhythm and blues

As shorter songs generate more streams in a given period, we suspect that artists and labels may have already reacted by shortening the song length. In support of this, we observe that content providers have been continuously reducing the song length across nearly all genres (Hiller & Jason, 2017; Kopf, 2019; Marshall, 2015) in the last 10 years (see Fig. 5). In particular, genres such as HHR, EDM, and rhythm and blues (R&B) have significantly reduced their song length in recent years, which has resulted in a higher generation of streams (and royalties) in comparison to the other genres. We note that this observation does not imply a causal relationship but rather a post hoc hypothesis.

Development of song length by genre over the last 10 years. Note: Linear regression of song length in seconds of all genres: \(-2.52 \times years + 238.59; {R}^{2}= 0.6885\); significant slope parameter (–2.52; p < 0.05)

In the following subsection, we examine the royalty effects when changing from the current pro rata remuneration model to a user-centric model, accounting for the genre-level differences between supply (song level) and demand (customer level).

Results

We calculate the monetary consequences of changing from the current pro rata model to a user-centric model by including not only royalties from paying customers but also the royalty on the streams generated from non-paying customers obtained via companies advertising on Spotify.Footnote 3 We determine the number of streams by dividing the total listening time of all customers for the pro rata model or the listening time of certain customers for the user-centric model by the mean song length either overall (pro rata) or for a certain customer (user-centric). We then calculate the royalty per stream by dividing the total royalty by either the number of streams (pro rata) or, alternatively, for a certain customer (user-centric). We then multiply this number by the number of streams of a certain genre either for all customers (pro rata) or for a certain customer (user-centric). In the case of user-centric, the royalty per customer needs to be aggregated over all customers interested in a certain genre. This way of calculation also allows us to determine the influence of single components, as formulas (1) and (2) show. Finally, we can compare the difference between the two models by aggregating the numbers by genre shares and royalties per genre.

-

$$Royalty\left(Genre\right)=\frac{SubscriptionFee(All Customers)}{\frac{ListeningTime(All Customers)}{MeanSongLength(All Genres)}}* \frac{ListeningTime\left(Genre, All Customers\right)}{MeanSongLength\left(Genre\right)}.$$(1)

-

$$Royalty\left(Genre,Customer\right)=\frac{SubscriptionFee\left(Customer\right)}{\frac{ListeningTime\left(Customer\right)}{MeanSongLength\left(All Genres\right)}}* \frac{ListeningTime\left(Genre, Customer\right)}{MeanSongLength\left(Genre\right)}.$$(2)

To arrive at meaningful numbers that add up to the total royalties that Spotify distributes to its content providers, we extrapolate the numbers from our survey to the Spotify International level. When comparing the resulting royalties of the content remuneration policies, positive values mean that a certain genre will obtain more royalties under a user-centric model than under a pro rata model and vice versa for negative values. Figure 6 displays the results and Appendix 1 provides detailed information about the calculations.

Total royalty reallocation by genre when changing from pro rata to user-centric remuneration. Note: A positive value implies that a certain genre would gain more royalties in a user-centric remuneration model vs. a pro rata remuneration model

Our results show positive values for genres such as rock (German and international €66 million p.a.), metal (€36 million p.a.), and classical (€30 million p.a.), which means that the streams of those genres will receive more royalties under the user-centric model than under the pro rata model. These genres currently “subsidize” genres with negative values, such as HHR (German and international -€109 million p.a.) and EDM (-€37 million p.a.), of up to a total sum of nearly -€170 million per year in a pro rata system..

For several genres such as international pop, indie, jazz, country, international folk, Latin, and punk, we find a relatively small royalty reallocation, which is caused by either opposing effects of the drivers of royalty distribution (e.g., international pop) or by relatively small levels of all drivers (e.g., punk). Figure 7 displays the decomposition of genre-related effects by the drivers of listening time, subscription fee amount, and song length, assuming average values for the other factors.

Drivers of royalty reallocation by genre. Notes: A positive value implies that a certain genre would gain more royalties in a user-centric remuneration model vs. a pro rata remuneration model. Given the multiplicative nature of the relationships between these causes of reallocation, the sum of effects per genre is not equal to the total revenue reallocation shown in Fig. 6

In the example of international pop, the song length is below average (209.5 s vs. an overall average of 216.6 s), thereby generating more streams per listening time. On average, listeners of international pop pay a lower subscription fee (€7.56 vs. an overall average of €8.08). Both of these effects favor the pro rata model. On the other side, the listening time (6.4 h.) is smaller than average (7.1 h.), resulting in fewer streams and thus is valued higher in the user-centric model. In this case, the three opposite royalty effects cancel one another out for a sum of only -€1.5 million favoring the pro rata model (see Table 2 in Appendix 1).

Overall, we find that the genre German HHR is the clear winner of the currently implemented pro rata remuneration model, benefiting from both demand-side effects (high average listening time and subscription fee) and supply-side effects (short average song length). We note that all three drivers of royalty distribution are negative (loosing royalties in case of a change towards a user-centric remuneration model) only for the German HHR and German folk genres.

Regarding the consequences for artists and labels, we can generally state that whether a content provider (artist/label) has advantages or disadvantages from the applied remuneration model depends on its share of genres relative to other artists/labels. An artist focusing purely on German HHR has a market advantage over an international rock artist in a pro rata remuneration system. The same applies to labels; advantages and/or disadvantages arise depending on the genre’s market share relative to other labels.

Discussion

This research provides initial and important insights about the supply and demand side effects of the pro rata and user-centric payout policies.

First, starting with the reallocation of revenue, user-centric remuneration results in a reallocation of revenue shifting it from mainstream to niche genres. Genres like HHR, EDM, and German Folk would lose revenue share while genres like International Rock, Classic, and Metal would win revenue share. The total reallocation would sum up to nearly 170 million € p.a. on Spotify, and is driven by the song length as well as the payments per listening time.

Second, by analyzing the consequences of a change to a user-centric system we see that labels that have a high share in niche genres will directly benefit. Due to the ability to act and earn money locally, local artists would also benefit from a user-centric model and therefore a user-centric remuneration promotes a more diverse and vibrant music scene.

We discussed our findings with top-level executives in the music industry and also with executives from a streaming service. Furthermore, confidential internal studies from the respective streaming service provided external support for our results by supplying a small sample of artists in France.

However, we also wish to note that when streaming services are not willing to change to the user-centric model, and the high media interest on this issue remains, we believe it to be very likely that the awareness of the reallocation effects of customers’ payments will continue to grow. This awareness will eventually provoke reactions which in turn may cause multiple cultural consequences. Particularly, artists and labels may further engage in shortening songs because it generates more streams. In addition, the proportional-to-usage policy can provoke click fraud by generating clicks through robots or asking people to stream even while they are sleeping. Thus, the choice of a remuneration policy has a direct effect on the creation of digital media products, as shown in the case of the music streaming industry.

With regard to strategic implications, we first made reallocation effects transparent. Increasing transparency may result in reconsiderations of remuneration models by the respective market players and thus the competition within this market. The results of our study indicate that content providers who are currently disadvantaged by the pro rata model (e.g., classical music) should reconsider their content-provisioning strategy. Content providers with strong negotiation power could start bundling their content into specific genre channels (e.g., classical music channel) and offer platforms their specific bundles in a license deal. Ultimately, this could lead to platforms offering a base service, with consumers wanting special content needing to subscribe to special channels—a strategy observed by paid television providers that offer access to sport or international language channels only when additional payments are made. For example, the television platform Sky offers packages for movies, international television stations, football and other sports.

In addition to the two mainly strategic implications, we highlight two important operational topics that are also debated in the industry. First, as previously mentioned, Page and Safir (2018) argue that it would not be equitable if the payout per stream is different across songs. “However, … there is no such thing as a global, all-in revenue/content pool. Instead, there are dozens of separate buckets: for every subscription tier, every local market and so on. All the different types of streams create distinct content pools, and that means one simple thing. Not all streams are equally valuable” (Pastukhov, 2019).

Second, the structure of a remuneration policy can allow different levels of abuse. If the overall number of streams is evaluated like in the pro rata model, all kinds of click fraud could be committed to increase the number of streams. Fortunately, click fraud has limited effects in a user-centric model because only the money of the respective consumer is affected (Dimont, 2017).

Finally, a user-centric remuneration system also allows artists with smaller marketing budgets to monetize on their local fan base more effectively. In a user-centric model, local artists can spend their marketing budgets on more specific local target groups so that gaining new individual listeners would directly result in revenue returns (Maasø, 2014). Thus, while in a pro rata model mass marketing is important, the user-centric model introduces a nuanced option to profitably target local customers with local marketing activities.

Along with our empirical findings, we see potential research on how the different interests from several music industry players may impact the supply and demand side and thus the competition in this market, which we outline in the research agenda below.

Research agenda for remuneration of flat rates

Aside of the analytic research by Avinadav et al. (2021), academic research has largely ignored the relevance of remuneration systems. Our initial empirical results serve as a starting point to better understand the outcome of different remuneration mechanisms implemented by flat-rate-based streaming services. However, we note that we only address a few important issues and that the field–which is of high economic relevance–offers many more important research topics. Thus, we provide a research agenda that may serve other researchers as inspiration to generate new theoretical, analytical, and/or empirical insights in this important field.

The established Five Forces model (Porter, 1983) inspires this research agenda (Fig. 8). From it, we offer five major conjectures regarding the impact of the design of remuneration systems on platforms’ value chains and business models.

Research agenda—strategic issues for platforms

Suppliers

Our study on the remuneration policies that platform streaming service providers offer their content suppliers shows that the different remuneration policies have severe financial consequences for content suppliers. This finding is in line with the current music industry debate, shifting from the question of how much a streaming service remunerates to how the allocation is designed. In the past, there had been a few instances where top artists have complained about the rather small amount of remuneration offered by pro rata-based streaming services and therefore have removed their content from platforms (Engel, 2014). The same could happen now as there is this intense debate about the impact of the remuneration model on supply.

The alternative user-centric remuneration policy was favored by the competing platform Deezer but it remains unclear why they have not yet changed to this policy. Amaldoss et al. (2021) argue that artists in the music industry do not have market power to request changes. However, most of these artists are marketed via one of the three major labels, Universal, Warner, or Sony, who could exercise enormous market power. In the neighboring field of movie streaming service providers (e.g., Netflix), we have recently seen that the content provider Disney now offers its content via its own platform Disney + . This poses the question: Is this a path that can also happen in the music industry? We find that there is not much known about the streaming of digital products, the platforms, and the market dynamics. Aside from the discussed music industry, similar questions arise for movie streaming platforms (e.g., Netflix), eBook reading (e.g., Skoobe), and gaming (e.g., ActionGame.com). Therefore, we believe that it would be fruitful to study the supply effects dependent on remuneration systems. A stronger focus on independent labels would be particularly important to generalize our initial findings in a larger setting.

As outlined, platforms’ choice of content remuneration models depends on transaction costs, risk effects, and competition (Hracs & Webster, 2021). However, the choice is not independently made without accounting for suppliers’ (and demanders’) market power. Specifically, when assessing the content supply, researchers should distinguish between artists and labels. Technically, they both belong to the supply side but there may be diverging individual interests (as suggested by the principal-agent theory; e.g., Bergen et al., 1992) and substantial differences in transaction costs for the two parties. This setting is interesting for analytical research but also for empirical researchers that have access to contract details. To the best of our knowledge, contracts between artists and labels are individually negotiated and are therefore very diverse. Some artists even complain that their contracts were created during pre-streaming times when the label received 85% of the income and the artist only 15%, which is no longer suitable as the labels do not have high distribution costs anymore (Bakare, 2021). These contractual changes entail big differences in the allocation of the live, physical, and streaming revenues to the artists. As these contracts are not publicly available, we had to analyze the financial consequences for the content providers without differentiating between label and artist. However, it would be of great interest to assess the direct consequences for artists if streaming platforms would switch to user-centric remuneration. An issue that could also be studied in simulations.

This may be of importance as we see a potential conflict of interest between a single artist and a label. The three major labels held or still hold sufficient shares of Spotify (Ingham, 2020), which enables them to influence developments, including changes in the remuneration system. With this in mind, the majors would benefit from a music landscape where single stars, mostly marketed by one of these majors, dominate the industry; which is great for that particular artist but worse for all other artists. This raises the question of whether the music industry benefits from the current streaming model, or whether a change would be more beneficial. Note that Wlömert and Papies (2016) investigated whether sales in the music industry would suffer from the introduction of streaming services such as Spotify. However, they did not consider the individual artist perspective.

Currently, remuneration models do not directly affect streaming platforms’ profits. The interests of the majors may be the reason for their ambivalent or even negative attitude towards a user-centric system. While Deezer is only demanding but not implementing a user-centric system, small platforms such as SoundCloud have already switched to a user-centric system (Cooke, 2021). It may be of interest to further investigate, e.g., by Conjoint experiments, the possibilities and market potential of platforms that are not heavily influenced by the interests of the majors and what their role in the democratization of the cultural industries could be (Hesmondhalgh et al., 2019).

In general, we suggest that it would be of great value to increase research in the field of margins. The role of the service fee is of utmost importance in a competitive setting. There seems to be a 30% service fee agreement across different industries. It would be very interesting for marketing research to understand the role of the margins better (more on margins in Dolan & Simon, 1996).

Finally, remuneration is currently based on the number of streams. This measure is not the best option for all market players and may lead to artists producing more songs but at a reduced song length with positive effects for the number of streams but maybe negative effects for the preferences for such a song. In addition to the two compensation systems discussed so far, pro rata and user-centered, the distribution parameters (e.g., the unit of distribution) must be investigated further. Up to now, streams have always been the basis. These are generated when a user has listened to a song for at least 30 s. There are many other options available which mix different remuneration models and distribution parameters. For example, (1) remuneration based on per-second usage, (2) remuneration based on quality ratings, or a combination of user-centric and pro rata remuneration (e.g., 50% of the subscription fee is allocated as user-centric and the rest pro rata). Additionally, the disadvantage for long-tail content could be solved by not remunerating proportionally but rather according to a concave function that remunerates very popular content not per stream but with decreasing marginal value. This problem is similar to principal-agent problems and the optimal remuneration may be determined with solving a principal agent problem. It would be very interesting to study financial and cultural outcomes depending on the different remuneration and distribution parameter designs–a field that can be addressed with analytical work or simulations.

Buyers

The demand side is influenced by two aspects. First, customers may change preferences to alternative services that implement a different remuneration model than the standard pro rata model. However, this would require that consumers understand how remuneration is executed and how their subscription fees are used. We are not aware of any empirical research that measures subscribers’ knowledge on remuneration mechanisms.

Many consumers are not currently aware of different allocation mechanisms for content remuneration and their outcomes (Dredge, 2018). However, representatives from independent labels, along with the streaming service Deezer, have initiated a campaign intended to increase consumers’ awareness of “fairness.” Deezer asserts that a user-centric model “would make the industry fairer for artists all over the world” (Legaspi, 2019). This argument is highly relevant to the relationship between artists and their fan base. Artists who can mobilize their fan base may benefit from drawing revenue from other consumers who do not actually listen to them in a pro rata model. As one of many examples, Justin Bieber asked his fans to stream his songs and suggested fans leave his songs on repeat while they slept (Sanghvi, 2020). Other consumers may perceive this as unfair and might switch to other streaming platforms that have adopted a user-centric remuneration model. This would be a starting point for interesting studies in the field of consumer behavior. Although the choice of remuneration policy (pro rata vs. user-centric) mostly affects content providers, it may also have relevance for informed consumers because the user-centric remuneration policy is potentially perceived as fairer. The question is whether consumers really find the current pro rata remuneration to be unfair and would react by switching to another service that offers a fairer remuneration. At the moment, there is no fairness in remuneration awareness among consumers as discussed by industry players. However, referring to the dual entitlement principle and social identification theory (Kahneman et al., 1986; Tajfel & Turner, 1986), it is likely that consumers who experience or observe unfair treatment will react to this by preferring the fair alternative. This opens a new field of research in a society that reacts very sensitive to corporations not treating customers or artists well. This research area is also interesting in terms of gaining a deeper understanding on how subscribers differentiate between the platforms’ allocation of subscription income (“consumers’ money”) versus advertising income (advertisers’ money).

Second, the changes in listening behavior induced by the remuneration model are an interesting research field. For example, in our empirical study, we show that it is essential to generate as many streams as possible in a pro rata system. The number of streams is higher if labels focus on mainstream genres rather than on niche genres. Furthermore, focusing on small niche segments is financially less interesting and could result in a more monotone product landscape. We find indications of this effect by analyzing the genre share in the yearly Billboard Top 100 Charts over time. From 2010 to 2019 genres such as Rock and R&B bisected their market share from approximately 10% to 5% each. Smaller genres such as EDM, International Folk, and Punk (which were present from time to time in the Top 100) are no longer present at all, while the market share of Hip Hop Rap is continuously growing (Gini coefficient 2010 of 0.81 and 2019 of 0.83). Furthermore, we analyzed the label composition of the Billboard Top 100 Charts and registered an increase of 5.3% (from 133 to 140 unique companies) in the number of labels present in the Top 100 Charts, comparing the time periods of 2010 to 2013 with 2017 to 2019. The number of labels in the Hip Hop Rap genre, as the most privileged genre in a pro rata system, increased by 32.4% (from 37 to 49) while the number of labels from all other genres shrunk by 6.6% (from 106 to 99). We also see an increase in the number of labels of the genres with a negative revenue reallocation and thus benefiting from the pro rata remuneration (see Fig. 6) by 3.5% (from 113 to 117) while the number of labels with a positive revenue reallocation gaining from a change to the user-centric model (see Fig. 6) decreased by 44.7% (from 47 to 26). While these findings may point to potential correlations, we suggest additional in-depth analyses of these changes to establish a deeper understanding of the causality.

Demand dynamics may also result from changes in the product and the assortment offered to customers (Morris, 2020). For example, we find initial support for cultural effects due to the incentives to “optimize” the content in a pro rata model. Specifically, we find that song length has declined by 2.5 s. per year (-10% in the last five years) and by a 30% increased label share for hip hop in the Billboard Top 100 Charts over the last 10 years. We believe that additional research is needed on pressing product issues from the demand and supply perspective.

Demand is strongly influenced by playlists and premium offers (Aguiar & Waldfogel, 2021; Wlömert & Papies, 2016). The design of playlists is of high importance to keep consumers in a flow. Ideally, a consumer remains listening to the same artist or label and generates more streams. However, the most successful playlists are managed by the streaming service (Audiohype.io, 2022). Thus, a playlist can be compared to a shelf in the supermarket in which platforms may ask for listing fees. This, in combination with remuneration plans and advertising strategies within the service, is a very interesting new research area.

A more general question of interest would be: What are the consequences of playlists and premium offers (e.g., exclusive pre-releases or live concerts) that are managed by the platforms? As nearly all successful playlists, as well as the algorithms determining the lists, are in the hand of the platforms, they may control the demand in the music market. Multiple newspaper articles accuse Spotify to secretly astroturfing its playlists with undercover in-house artists, saving itself a fortune as those tracks racked up millions of streams (Deahl & Singleton, 2017; Ingham, 2016). This gives a single dominant market player the power to determine supply and to steer demand accordingly (Datta et al. 2018). Comparing the importance of the remuneration policy and the impact on a playlist’s success, we ask whether there is a way to combine both to gain an overall “fair” model?

New entrants

One of the most fundamental questions is whether artists should market their content (e.g., songs) via platforms. Bender et al. (2021) found that the benefit an artist derives from streaming their music depends on the artist catalog on the platform. In addition, as Ferraro et al. (2021) point out, this also depends on how fair artists consider platforms’ activities and remuneration models. Of course, this is dependent on the demand and the potential contract between the platform and the content provider. A content provider has several options as they could distribute their content via (1) multiple platforms, (2) provide exclusive rights to a single platform, or (3) rely on their own distribution channel (e.g., their own streaming service). Referring to (1) and (2), content providers (artists/labels) could restrict content to one or more streaming platforms. Offering exclusivity to a platform can be profitable for the label if the label achieves a higher royalty per stream than in a usual pro rata model or if the platform is promoting this song more intensely through playlists. Due to the fact that platforms do not exactly offer the same assortment of songs, this setting may provide a nice quasi experimental setting to investigate the effect of exclusivity on demand as it has been done in other industries (e.g., in the motion picture industry; Danaher et al., 2010, Mukherjee & Kadiyali, 2011, Hashim et al., 2019or Yu et al., 2021). Based on future empirical analyses, research could focus on developing an analytical model for the optimal decision on exclusivity, or maybe even an exclusive limited time offer which is also known as “windowing” (Hennig-Thurau & Houston, 2019).

Looking at the second aspect in more detail, the platform with exclusive rights could also be a platform from one of the majors. As mentioned in our empirical study, single majors may benefit more than others from the current pro rata model. Therefore, it would also be interesting to investigate (e.g., analytically) what would happen if a major label, analogous to Disney + , withdrew its content from the pro rata streaming platforms and created its own.

If a streaming provider focuses on popular content at the expense of niche (long-tail) content then the question is whether there will be competitors that enter the market with a focus on the long-tail and may even be cheaper. If and how this will happen, can be researched both empirically and analytically.

Focusing on aspect (3), Kanye West, an influential artist, recently launched his own streaming service. Kanye West has not only created his own platform, he is also offering his new album exclusively on that platform: “Donda 2 will only be available on my own platform, the Stem Player. Not on Apple, Amazon, Spotify, or YouTube. Today artists get just 12% of the money the industry makes. It’s time to free music from this oppressive system. It’s time to take control and build our own.” (Minsker, 2022). Similar investigations on the distribution of apps were conducted by Avinadav et al. (2021) who compared the option of distributing an app via one of the popular platforms (e.g., Apple’s App Store) or to market it directly via the webpage. They additionally investigated what kind of revenue sharing is optimal. Thus, choosing a certain remuneration system, and considering the subsequent supply and demand dynamics, may result in a shift away from revenue sharing models and incline towards a licensing deal. For example, in the movie industry, companies like Netflix and Amazon are no longer just licensing content but also creating more and more of their own content. The platform itself became a supplier and reduced its dependence on content suppliers. Until now, Spotify has not acted as a full content supplier but they started a program with weekly in-house recorded songs which are directly marketed on Spotify since 2016 (Gallucci, 2016). It may be of interest to investigate the impact of a platform-based content supply on demand in the music industry when other platforms or formats (e.g., online radio or YouTube) are used.

If we consider current artificial intelligence developments, how would the music industry develop if algorithms are able to produce just as good music as artists? In 2020 Spotify applied for a patent that included a building block for Spotify to create its own AI-generated music and potentially compete with artists without having to pay for content (Fergus, 2020).

Substitutes

Ideally, every policy should be immune against fraud. Unfortunately, the pro rata policy is reported to have led to click fraud where either streams are collected by algorithms or users are asked to let Spotify play certain songs all day and night in a loop (Eriksson et al., 2019). With user-centric remuneration, click fraud would become irrelevant because the money paid by the user is distributed according to the listened songs of this user. Nevertheless, any other remuneration policy must always be checked for incompatibility with user interests.

Previous research found that streaming services played an important role in the music industry which was heavily suffering from piracy (Papies & van Heerde, 2017; Wlömert & Papies, 2019). Instead of using file sharing networks or other ways for illegal downloads, consumers appreciated the new way of music allocation and agreed to pay a flat rate at moderate prices or to accept advertising. We argue that perceived fairness can play an important role for customer behavior and we think that it would be very interesting to study potential shifts towards piracy channels dependent on executed remuneration models. For example, could a remuneration model be perceived as an unfair trigger for more piracy? In line with this, exclusive content offers from one platform may increase the utility of piracy channels for non-subscribers of the respective platform. We currently observe that streaming platforms continuously engage in offering podcasts and audiobooks. In both fields, exclusive offers on one single platform are observed, and the remuneration is not based on a pro rata allocation scheme but often negotiated in a license deal. Thus, it would be interesting to know under which conditions this model is superior compared to the traditional pro rata remuneration model.

Platforms

Finally, Porter (1983) discusses the competition between industry players as a key strategic force. A thorough analysis on the competitive setting would be very economically interesting because entertainment products are marketed as different versions. For example, music can be purchased physically (CD), digitally (download), or consumed on demand via streaming services related to audio (e.g., Spotify), video (e.g., YouTube), or consumed via a (online) radio bundled in a program. The attractiveness of these channels for suppliers highly depends on the margin the right holders can claim. However, streaming became very popular due to the wide selection of content for free (advertising-based), or for a reasonable subscription price (Wlömert & Papies, 2019). The strong dynamics between supply and demand, driven by remuneration systems, will offer many potential research opportunities not only for marketing scientists that aim to understand the impact of marketing instruments across the different channels but also for economists that aim to study market outcomes.

We hope that our initial empirical findings combined with this research agenda will trigger additional research in this interesting field that is not only relevant for the music industry, but also for publishers, movie studios, and game developers–among others.

Notes

This is true, except for the case when accounts are hacked to generate fake streams which would also affect the user-centric model (King 2021).

The analysis is based on two data sources. First, we use data from a survey of 3,326 respondents that is available as an Excel file. Second, we use the Spotify API via an official developer account to (1) search for artists by genre and (2) collect the duration of their songs. We cannot provide all of this data but can provide the R code and a clear description of how we gathered this information from the API to allow others to replicate the findings.

Platforms distribute ad revenues from free users the same way as subscription fees from premium users and keep approximately 30%.

References

Aguiar, L., & Waldfogel, J. (2018). As streaming reaches flood stage, does it stimulate or depress music sales? International Journal of Industrial Organization, 57, 278–307.

Aguiar, L., & Waldfogel, J. (2021). Platforms, power, and promotion: Evidence from spotify playlists. The Journal of Industrial Economics, 69(3), 653–691.

Amaldoss, W., Du, J., & Shin, W. (2021). Media platforms’ content provision strategies and sources of profits. Marketing Science, 40(3), 527–547.

Audiohype.io. (2022). The best spotify playlists in 2022, Retrieved April 3, 2022 from https://audiohype.io/resources/the-best-spotify-playlists

Avinadav, T., Chernonog, T., & Khmelnitsky, E. (2021). Revenue-sharing between developers of virtual products and platform distributors. European Journal of Operational Research, 290(3), 927–945.

Bakare, L. (2021). The music streaming debate: what the artists, songwriters and industry insiders say, The Guardian, Retrieved May 11, 2022 from https://www.theguardian.com/music/2021/apr/10/music-streaming-debate-what-songwriter-artist-and-industry-insider-say-publication-parliamentary-report

Bender, M., Gal-Or, E., & Geylani, T. (2021). Attracting artists to music streaming platforms. European Journal of Operational Research, 290(3), 1083–1097.

Bergen, M., Dutta, S., & Walker, O. C., Jr. (1992). Agency relationships in marketing: A review of the implications and applications of agency and related theories. Journal of Marketing, 56(3), 1–24.

Billboard. (2014). Inside Vulfpeck’s Brilliant Spotify Stunt, Retrieved June 8, 2020 from https://www.billboard.com/articles//5937612/inside-vulfpecks-brilliant-spotify-stunt

Carr, S. (2020). The rise of Spotify streaming farms: How fraudsters are cashing in. Retrieved February 25, 2021 from https://ppcprotect.com/spotify-streaming-farms/

Carroni, E., & Paolini, D. (2020). Business models for streaming platforms: Content acquisition, advertising and users. Information Economics and Policy, 52, 100877.

Cooke, C. (2021). SoundCloud announces shift to user-centric royalty distribution for its 100,000 independent creators, Retrieved March 28, 2022 from https://completemusicupdate.com/article/soundcloud-announces-shift-to-user-centric-royalty-distribution-for-its-100000-independent-creators/

Danaher, B., Dhanasobhon, S., Smith, M. D., & Telang, R. (2010). Converting pirates without cannibalizing purchasers: The impact of digital distribution on physical sales and internet piracy. Marketing Science, 29(6), 1138–1151.

Datta, H., Knox, G., & Bronnenberg, B. (2018). Changing their tune: How consumers’ adoption of online streaming affects music consumption and discovery. Marketing Science, 37(1), 5–21.

Deezer. (2019). Deezer wants artists to be paid fairly - By adopting a User-Centric Payment System (UCPS), Retrieved December 20, 2019 from https://www.deezer.com/ucps

Deahl, D. & Singleton, M. (2017). What’s really going on with Spotify’s fake artist controversy, Retrieved March 28, 2022 from https://www.theverge.com/2017/7/12/15961416/spotify-fake-artist-controversy-mystery-tracks

Dimont, J. (2017). Royalty inequity: Why music streaming services should switch to a per-subscriber model. Hastings LJ, 69, 675.

Dolan, R. J., & Simon, H. (1996). 1996. Power pricing. The Free Press.

Dredge, S. (2018). How would user-centric payouts affect the music-streaming world?, Retrieved June 8, 2020 from https://musically.com/2018/03/02/user-centric-licensing-really-affect-streaming-payouts/

Engel, P. (2014). Taylor swift explains why she left spotify, Retrieved March 28, 2022 from https://www.businessinsider.com/taylor-swift-explains-why-she-left-spotify-2014-11

Eriksson, M., Fleischer, R., Johannson, A., Snickars, P., & Vonderau, P. (2019). Spotify teardown: Inside the black box of streaming music. MIT Press.

Fergus, J. (2020). Spotify could soon replace real artists with AI music, Retrieved March 28, 2022 from https://www.inputmag.com/tech/spotify-could-soon-replace-real-artists-with-ai-music

Ferraro, A., Serra, X. & Bauer, C. (2021). What is fair? Exploring the artists’ perspective on the fairness of music streaming platforms, IFIP Conference on Human-Computer Interaction (pp. 562–584). Springer.

Flynn, M. (2015). You Need Me Man, I Don't Need You: Exploring the debates surrounding the economic viability of on-demand music streaming. KES Transactions on Innovation in Music, Vol. 2: Innovation in Music, 157–173.

Gallucci, N. (2016). Spotify adds weekly in-house recordings with 'Singles', Retrieved March 28, 2022 from https://mashable.com/article/spotify-original-singles-music-streaming

Hashim, M. J., Ram, S., & Tang, Z. (2019). Uncovering the effects of digital movie format availability on physical movie sales. Decision Support Systems, 117, 75–86.

Hennig-Thurau, T., & Houston, M. B. (2019). Entertainment science. Data analytics and practical theory for movies, games, books, and music. Springer.

Hesmondhalgh, D., Jones, E., & Rauh, A. (2019). SoundCloud and Bandcamp as alternative music platforms. Social Media+ Society, 5(4), 2056305119883429.

Hiller, R. S., & Jason, M. W. (2017). The rise of streaming music and implications for music production. Review of Network Economics, 16(4), 351–385.

Hracs, B. J., & Webster, J. (2021). From selling songs to engineering experiences: Exploring the competitive strategies of music streaming platforms. Journal of Cultural Economy, 14(2), 240–257.

Ingham, T. (2016). Spotify is making its own records… and putting them on playlists, Retrieved March 28, 2022 from https://www.musicbusinessworldwide.com/spotify-is-creating-its-own-recordings-and-putting-them-on-playlists

Ingham, T. (2020). Who really owns spotify? , Retrieved March 28, 2022 from https://www.rollingstone.com/pro/news/who-really-owns-spotify-955388

Kahneman, D., Knetsch, J. L., & Thaler, R. (1986). Fairness as a constraint on profit seeking: Entitlements in the market. The American Economic Review, 76(4), 728–741.

Kopf, D. (2019). Pop songs have become significantly shorter over the past 5 years, Retrieved September 2, 2019, https://qz.com/1519823

Kübler, R., Seifert, R., & Kandziora, M. (2021). Content valuation strategies for digital subscription platforms. Journal of Cultural Economics, 45, 295–326.

Lambrecht, A., Goldfarb, A., Bonatti, A., Ghose, A., Goldstein, G., Lewis, R., & Yao, S. (2014). How do firms make money selling digital goods online? Marketing Letters, 25(3), 331–341.

Lambrecht, A., & Skiera, B. (2006). Paying too much and being happy about it: Existence, causes, and consequences of tariff-choice biases. Journal of Marketing Research, 43(2), 212–223.

Legaspi, A. (2019). Deezer launches initiative for ‘User-Centric’ approach to distribute royalties, Rolling Stone. Retrieved June 8, 2020 from https://www.rollingstone.com/pro/news/deezer-launches-initiative-for-user-centric-approach-to-distribute-royalties-883310/

Lena, J. C., & Peterson, R. A. (2008). Classification as culture: Types and trajectories of music genres. American Sociological Review, 73(5), 697–718.

Maasø, A. (2014). User-centric settlement for music streaming, Retrieved January 31, 2020 from http://www.hf.uio.no/imv/forskning/prosjekter/skyogscene/publikasjoner/usercentric-cloudsandconcerts-report.pdf

Marshall, L. (2015). ‘Let’s keep music special. F—Spotify’: on-demand streaming and the controversy over artist royalties. Creative Industries Journal, 8(2), 177–189.

Minsker, E. (2022). Kanye West Says New Album Donda 2 Won’t Stream, Will Be Available Only on His Stem Player, Retrieved March 28, 2022 from https://pitchfork.com/news/kanye-west-says-new-album-donda-2-wont-stream-will-only-be-available-on-his-stem-player

Morris, J. W. (2020). Music platforms and the optimization of culture. Social Media+ Society, 6(3), 2056305120940690.

Mukherjee, A., & Kadiyali, V. (2011). Modeling multichannel home video demand in the U.S. motion picture industry. Journal of Marketing Research, 48(6), 985–995.

Page, W. & Safir, D. (2018). Money in, money out: Lessons from CMOs in allocating and distributing licensing revenue. Music & Copyright Newsletter 29 August 2018.

Papies, D., & van Heerde, H. J. (2017). The dynamic interplay between recorded music and live concerts: The role of piracy, unbundling, and artist characteristics. Journal of Marketing, 81(4), 67–87.

Pastukhov, D. (2019). What music streaming services pay per stream (and why it actually doesn’t matter), Soundcharts blogs. Retrieved September 11, 2021, from https://soundcharts.com/blog/music-streaming-rates-payouts

Prelec, D., & Loewenstein, G. (1998). The red and the black: Mental accounting of savings and debt. Marketing Science, 17(1), 4–28.

Porter, M. E. (1983). Competitive Strategy. The Free Press.

Rindfleisch, A., & Heide, J. B. (1997). Transaction cost analysis: Past, present, and future applications. Journal of Marketing, 61(4), 30–54.

Sanghvi, Y. (2020). Artists begging for streams takes away from quality music. The Daily Targum, Retrieved September 9, 2021, from https://dailytargum.com/article/2020/01/artists-begging-for-streams

Spotify Technology S.A. (2018). Annual Report.

Spotify. (2021). Company info. Retrieved February 25, 2021 from https://newsroom.spotify.com/company-info/

Statista (2021). Netflix: Daten und Fakten zur Erfolgsgeschichte des Streaming-Riesen. Retrieved February 25, 2021 from https://de.statista.com/themen/1840/netflix/

Tajfel, H., & Turner, J. C. (1986). The social identity theory of intergroup behavior. In S. Worchel & W. G. Austin (Eds.), Psychology of intergroup relations (pp. 7–24). Nelson-Hall.

Theurer, M. (2020). Aufstand der Stars, Frankfurter Allgemeine Sonntagszeitung, January 24, 2020.

TranSystems. (2009). Regional transit fare structure and revenue sharing study. San Diego Association of Governments.

Wlömert, N., & Papies, D. (2016). On-demand streaming services and music industry revenues — Insights from Spotify’s market entry. International Journal of Research in Marketing, 33(2), 314–327.

Wlömert, N., & Papies, D. (2019). International heterogeneity in the associations of new business models and broadband internet with music revenue and piracy. International Journal of Research in Marketing, 36(3), 400–419.

Yu, Y., Chen, H., Peng, C. H. & Chau, P. Y. K. (2021). The causal effect of subscription video streaming on DVD sales: Evidence from a natural experiment. Working paper, University of Memphis. https://ssrn.com/abstract=2897950

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Natasha Foutz served as Area Editor for this article.

Appendix

Appendix

Appendix 1 Reallocation of revenue

In Appendix 1 we provide detailed calculations of the reallocation of revenue in case of a change from the current pro rata remuneration model to a user-centric model. We distinguish between free and paid streaming as their revenue allocation is fulfilled in separate “pots.” First, we focus on free users. People adopting a free streaming service generate revenue each time a commercial is streamed. Therefore, listening to music longer automatically increases the revenue on a one-to-one ratio. We assume four ads play per hour. We obtain the Sum of Free Streams (38,190) generated for a genre by considering the sum of hours all survey participants spent listening to a specific genre via free streaming and dividing this number by the average song length of the genre. We obtain the Royaltyg by dividing the total number of streams by genre and then by the total number of streams. Spotify’s 2018 balance report offers insight into the Cost of Revenue (CoR), which is defined as royalty and distribution costs incurring for Spotify. Due to the distribution costs of a digital product being close to zero, we assume that the CoR is equal to the pure royalty payments from Spotify to labels and artists. Therefore, the Share by Model multiplied by the Ad-Supported CoR (€445 million) equals the genre-specific free streaming revenue contributions per genre.

Second, we address paying users by calculating the sum of all streaming payments from our survey participants per genre and dividing them by the total sum of streaming payments over the last 30 days to obtain the Share by Model. When multiplying this share by the Premium CoR (€3,461 million) from the Spotify balance report, we obtain the genre-specific paid streaming revenue contribution. For the revenue receipt of paid streaming, we proceeded analogically towards the free streaming contribution and calculated the Sum of Hours Listened for a specific genre and divided it by the Average Song length of that genre to obtain the Sum of Streams per genre. Multiplying the share by the Total CoR (€3,906 million) from the 2018 Spotify annual report gives us the royalty payment distribution as it is today.

Table 2 summarizes the differences between royalties by genre when changing from a pro rata to a user-centric model:

To quantify the reallocation of revenue, we calculated the difference of genre shares. For International Rock, for example, there is a free streaming delta (upper row) of rounded 0.04 percentage points (share of user centric of 1.52% minus share of pro-rata of 1.49%). This means that International Rock would receive 0.04% less royalties when changing to a user-centric model, which is equal to €1.4 million (column delta in Million Euros) in royalty payments from Spotify per year. For paid streaming (bottom row) International Rock has a delta of 1.46 percentage points (13.19%-11.73%), which would be equal to less royalties of €56.9 million per year in case of a change. In total, International Rock would receive €58.3 million more with a change to a user-centric allocation of royalties. This amount of €58.3 million is 11.3% short of what it currently receives. In addition to International Rock, there are also Classic, Metal, and Blues receiving approximately 15 to 25% less royalties when remaining under the pro rata model, while HHR, EDM, and German Folk receive more and therefore are advantaged with respect to royalties.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Meyn, J., Kandziora, M., Albers, S. et al. Consequences of platforms' remuneration models for digital content: initial evidence and a research agenda for streaming services. J. of the Acad. Mark. Sci. 51, 114–131 (2023). https://doi.org/10.1007/s11747-022-00875-6

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11747-022-00875-6