Abstract

Tropical forests are rapidly disappearing due to the expansion of cash crops to meet demands from distant markets. Pressing concerns on deforestation impacts resulting from the global trade of tropical commodities have led some high-income countries’ governments to consider diverse regulatory and trade levers to tackle the problem. These include proposals for new supply chain due diligence legislation concerning imports of forest-risk products and the inclusion of environmental measures in trade deals. To contribute to this debate, we conducted a comprehensive analysis of existing data on global trade and consumption patterns of tropical commodities, attribution of commodity production to deforestation, trade agreements, and progress in the implementation of crop sustainability standards. We used global data on key tropical commodities of oil palm, cocoa, and coffee. Our study shows that high-income countries have the highest per capita consumption for the three commodities evaluated and that consumption rates have dramatically increased in the last two decades. We discuss a range of measures that can potentially be required to tackle deforestation in global supply chains, which are currently being considered by policymakers, before discussing the kinds of post-growth, convivial approaches that are often excluded by the framing. Given the inherent expansionary nature of global market dynamics, we show that market-based initiatives are inadequate to tackle continuing deforestation and socio-ecological degradation. More transformative solutions amplify commoning and post-growth approaches are required to lead to some uncoupling of trade and territorialising of economic activity to fit within planetary boundaries and allow for plural values.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Tropical forests presently cover about 1.84 billion hectares and account for 45% of the tropical region (FAO 2020). These forests cover more land area than forests in other biomes (i.e. 11, 16, and 27% in subtropical, temperate, and boreal regions) (FAO 2020) and store the highest carbon density (Pan et al. 2013; Harris et al. 2021). They are vital in capturing carbon and serve as a natural buffer to climate change (Brinck et al. 2017; Mitchard 2018). They harbour high biological diversity and various endemic species and are important in maintaining ecosystem functions and services essential to support local livelihoods, food security, and human well-being in developing countries (Davis et al. 2020; Pillay et al. 2022). However, tropical forests have been subjected to rapid deforestation and forest degradation and escalated carbon emissions from land-use change in recent decades (Taubert et al. 2018; Brando et al. 2019; Hansen et al. 2020). About 60% of total forest losses were associated with the expansion of cropland, pasture, and industrial tree plantations (Pendrill et al. 2019). This expansion is driven by increased demand for tropical commodities such as oil palm, soybeans, cocoa, coffee, beef, and rubber from consumers in the international market (Hoang and Kanemoto 2021; Sun et al. 2022) and growing affluent populations in the commodities’ producing countries (Munroe et al. 2019; Xiong et al. 2021).

High-income countries (HICs), including members of the Organisation for Economic Cooperation and Development (OECD), are recognised as among the leading international consumers of tropical deforestation embodied in trade (Pendrill et al. 2019). Between 2015 and 2017, the OECD HICs' imports of key forest-risk commodities were associated with an estimated total deforestation risk of 358,235 ha per year (equivalent to 3.08 ha per 10,000 people per year) (Pendrill et al. 2022). This is primarily due to limited production, overall high consumption rates per capita, and the presence of large food and feed industries in these countries (Bager and Lambin 2020; Fuchs et al. 2020). Besides OECD countries, Asian emerging economies such as China and India are also among the leading consumers of forest-risk commodities over the same period, although their trade-associated deforestation risk is significantly lower compared to the OECD HICs (i.e. 166,850 and 46,302 ha per year, or equivalent to 1.15 and 0.33 ha per 10,000 people per year) (Pendrill et al. 2022). Estimation of the extent of deforestation associated with crop production has so far been carried out using rudimentary data on the country or sub-national-level crop production and forest cover change, raising uncertainties in their accuracy (Pendrill et al. 2019, 2022). Given the recent availability of spatiotemporally explicit data on the change in crop distribution in major producing countries, such as oil palm (Xu et al. 2020; Descals et al. 2021), soybeans (Song et al. 2021), and cocoa (Abu et al. 2021), there is room to evaluate more accurately the actual extent of deforestation attributed to the production of tropical crops.

Environmental provision has generally been lacking in trade policies (Brandi et al. 2020; Abman et al. 2021). The relationship between the environment and trade, and the legal and economic implications, have been much debated over the last thirty years, especially since the creation of the World Trade Organization (WTO) in 1995 (Brack 2013; Bigdeli 2014). The relatively small number of WTO disputes involving policies aimed overtly at protecting the environment have been scrutinised extensively without generating consensus on any way forward (Brack 2013; WTO 2022a). However, pressing concerns on deforestation risk embodied in tropical commodity imports, perpetuated by problems of global inequality (Sun et al. 2022), have recently led some HIC governments, including the EU and UK, to propose new legislation that mandates companies and businesses involved in forest-risk commodity imports to comply with the supply chain due diligence and reporting requirements (Environment Act 2021; European Commission 2021). These proposals marked the beginning of a formal legislative process aimed at reducing deforestation associated with trade (Brandi et al. 2020; Abman et al. 2021), although many details are yet to be addressed in the secondary regulations before they come into force by 2024.

One of the challenges in formulating secondary regulations in deforestation-free trade legislation is to devise an appropriate due diligence mechanism for each regulated crop without breaching the countries’ commitment under existing international trade agreements. Sustainability standards are one of the relevant mechanisms that have long been discussed within the WTO. Sustainability standards seek to ensure that commodities are cultivated, sourced, and processed through a predefined set of sustainability threshold indicators, covering environmental and social dimensions. Private standards are not generally used in national-wide trade policy, i.e. in determining a country’s levels of import or export duty, or regulatory requirements governing imports and exports. However, they have recently been used by the Switzerland authorities to verify compliance with the sustainability criteria included in the EFTA–Indonesia CEPA (European Free Trade Association–Indonesia Comprehensive Economic Partnership Agreement), thereby rendering compliant products eligible for reductions in import duty (Larrea et al. 2021; Limenta 2022).

Here, we assess the potential route toward a more environmentally responsible trade of tropical crops drawing from existing data on global trade and consumption patterns of tropical commodities, attribution of commodity production to deforestation, incorporation of environmental elements in trade agreements, and progress in the implementation of crop sustainability standards. More specifically, we seek to answer four related research questions: (1) What is the current global trade of tropical commodities, and what are the commodity consumption patterns across countries with different development statuses? (2) How is the production of tropical crops associated with deforestation and how does the estimation of crop-induced deforestation vary by approach? (3) How have environmental clauses been incorporated into trade agreements and how robust are they in reflecting environmental goals? (4) What is the evidence of sustainability standards’ effectiveness and impact? By addressing these questions and carrying out a comprehensive analysis of relevant data, we discuss potential leverage points pertaining to global trade which can potentially be enhanced to reduce environmental damage to the biodiverse tropical landscape and what additional measures or more transformative approaches might be required to achieve environmental goals with respect to tackling deforestation in supply chains.

Materials and methods

We analysed data on three key forest-risk commodities: oil palm, cocoa, and coffee. These commodities were chosen to represent various geographical foci (with differing socio-environmental conditions) and crop production models (large-scale plantations and small- and medium-scale farms). Oil palm is produced largely in tropical Asia (Indonesia and Malaysia) (Descals et al. 2021), cocoa in tropical Africa (Côte d'Ivoire and Ghana) (Abu et al. 2021), and coffee in tropical Latin America (Brazil and Colombia) (Ovalle-Rivera et al. 2015). Large-scale plantations are recognised as the primary actors in oil palm production and supply chain (Descals et al. 2021), whereas small- and medium-scale farms are prevalent in the cocoa and coffee sectors (Somarriba and López Sampson 2018; World Cocoa Foundation 2019). In the following subsections, we outline the approach and data used for analysing each of the four-pronged questions that we intend to address. Detailed methodologies are provided in the Supplementary Methods.

Global trade and consumption patterns of tropical crops

We used the UN Comtrade database (UN Statistics Division 2022) to estimate the annual quantity of imports and exports of oil palm, cocoa, and coffee for the period of 2011–2015 and 2016–2020. We focused on raw products, i.e. commodities in their raw form that undergo minimal processing. To give an estimate of the net demand for the production of a specific crop, the equivalent weight is used rather than the actual weight of the imported commodities recorded in the UN Comtrade database (see Table S1). For each crop, each country involved in the trade was classified based on their primary role as: (i) exporting country; (ii) trading country; and (iii) importing country. An exporting country is defined as a country whereby the quantities of commodity being exported far exceeds imports. A trading country is defined as a country whereby the quantities of commodities being exported account for more than 30% of the quantities being imported into the country; therefore, a large proportion of the commodity undergoes limited processing and then is exported elsewhere (Jones et al. 2020; Verschuur et al. 2022) An importing country is defined as a country where the quantities of imports far exceed exports. We evaluated patterns of consumption or utilisation of commodities across countries with differing economic statuses, i.e. high-income (HICs), upper-middle-income (UMICs), and low- and lower-middle-income countries (LMICs). Consumption rates per capita were estimated as the cumulative quantity of raw commodities imported and the quantity produced in that country subtracted by the quantity exported, divided by the country’s population.

Deforestation risk attributed to crop production

Deforestation risks attributed to crop production were estimated using three approaches: (A) forest cover change datasets in combination with data on the spatiotemporally explicit crop expansion data; (B) the latest spatial data on crop distribution; and (C) existing crude deforestation risks estimated from the sub-national data (Pendrill et al. 2022). The spatiotemporally explicit crop expansion data is considered to provide the most accurate direct attribution of the crop to deforestation, i.e. identification of forest clearance that was immediately replaced by the crop (Song et al. 2021). The latest spatial data on crop distribution provides an indirect attribution of the crop to deforestation, i.e. identification of forest clearance that eventually led to crop cultivation; such data is therefore considered more accurate than the crude estimates.

For oil palm, we evaluated the deforestation risk in Indonesia and Malaysia. For cocoa, we focused on Côte d’Ivoire and Ghana, and for coffee on Brazil, Colombia, and Vietnam. Data types A, B, and C are available for oil palm; therefore, we used these three data types to generate and compare the embodied deforestation risk estimates. Data type A was unavailable for cocoa, so only data types B and C were used. For coffee, only data type C was available and therefore used in the analysis. We focused on the expansion of crops and deforestation occurring between 2011 and 2019, which reflects the period in which our different datasets overlap.

Trade agreements and the environmental sustainability elements

We collected data on trade agreements from the WTO RTA database (WTO 2022b) and focused on bilateral and multilateral (regional) trade agreements made between 1980 and 2022. For each trade agreement, we collected information on the RTA name, signatory countries, date of notification, date of entry into force, specific section(s) referencing the environment, environmental criteria relating to the traded products, and provision to withdraw trade preferences if the criteria are not met. The level of environmental commitments for each trade agreement was then assessed using an evaluative scale classified as very weak, weak, medium, and strong. These scales were generated based on four key criteria: (1) description of commitments to sustainable development and/or environmental protection; (2) specific chapter dedicated to the environment, forest-based products, and/or biodiversity; (3) review of the environmental impact of the trade agreement; and (4) measures and support to address environmental issues. The charactersation of each criterion into different scales is summarised in Table 1.

Sustainability certification schemes’ implementation and evidence of impact

For each commodity, we carried out a systematic review of past empirical studies evaluating the impact of sustainability certification schemes. Impact evidence was evaluated on five dimensions: (i) deforestation, biodiversity, or wildlife; (ii) greenhouse gas (GHG) emissions or fire; (iii) management of water, soil, or waste; (iv) poverty, income, or food security; and (v) human rights, tenure security, and conflicts. For each study, we collected information on:

-

the approach used to derive evidence, including: (i) case report or case–control study (either before–after or with–without), whether or not there was consideration of confounding factors, and (ii) rigorous quasi-experimental method, i.e. comparing treated and control before and after certification, and accounting for baseline conditions at the pre-treatment stage (Ferraro 2009; Sills et al. 2017);

-

whether or not the study considers the spatial spillover effects of certification schemes to the broader landscapes (within and surrounding certified farms) (Heilmayr et al. 2020; Schleicher et al. 2020);

-

the type of producer evaluated, including large-scale plantations, scheme smallholders (normally tied to plantations), or independent smallholders; and

-

indicators of sustainability evaluated on the five above-mentioned dimensions and summary of their impact: positive, neutral (no impact), or negative.

Results

What is the current global trade of tropical commodities and what are the commodity consumption patterns across countries with different development statuses?

Oil palm

Between 2016 and 2020, the largest exporting countries of raw oil palm were Indonesia, Malaysia, Colombia, and Guatemala (Fig. 1a). Indonesia and Malaysia exported 32.8 and 17.4 Mt per year, and Colombia and Guatemala exported 0.65 and 0.82 Mt per year, respectively. These countries are also the major producers of oil palm globally. The Netherlands was the major trading country importing 4.2 Mt per year of oil palm and 41.4% of these imports were then exported or distributed elsewhere. Middle-income Asian countries of India, China, and Pakistan, and high-income OECD countries of Germany, Spain, Italy, USA, and New Zealand were the largest importers of the commodity. Similar patterns of countries were obtained from 2011 to 2015 (Fig. S1a).

Global trade flow in raw oil palm (a), cocoa (b), and coffee (c) between 2016 and 2020. Raw is defined as a commodity in its raw form or with minimal processing, and thus it mostly contains the commodity. An exporting country is a country whereby exports of the commodity substantially exceed imports; an importing country is a country whereby imports substantially exceed exports; and a trading country is a country whereby exports of the commodity account for more than 35% of the imports (i.e. a large proportion of the commodity is transiting through the country and distributed elsewhere)

The consumption rates per capita of oil palm in each country (accounting for the country’s import, export, and crop production quantities), based on the 2016–2020 datasets, systematically vary by the country’s economic status (Fig. 2a). HICs were the largest consumers of oil palm, with the median annual consumption rate of 4.44 kg per person. Comparatively, the median annual consumption of UMICs and LMICs was 3.54 and 2.96 kg per person, respectively. Consumption rates of New Zealand, the Netherlands, and Malaysia far exceeded those of other countries within the same economic status (Fig. 2a). New Zealand was estimated to consume 389 kg of oil palm per person per year, and the country’s oil palm use had increased 126 times over the last two decades (Fig. S2a). New Zealand’s oil palm consumption is primarily in the form of palm kernel meals to support the dairy and meat industries, which have grown rapidly in the last two decades (Stringer et al. 2016) and now account for 20% of the country’s economy (Ballingall and Pambudi 2017). The Netherlands and Malaysia annually consume 141 and 158 kg of oil palm per person, on average, and consumption rates increased 3.6 and 1.7 times since the period of 1996–2000.

Country ranking in the per capita consumption of raw a oil palm (for food and non-food use), b cocoa, c and coffee between 2016 and 2020, by country economic status (i.e. HICs, UMICs, and LMICs). Per capita consumption in each country was estimated as the cumulative total quantity imported and total quantity produced in that country per year subtracted by the total quantity exported, divided by the country’s population number

Cocoa

The largest exporting countries of cocoa between 2016 and 2020 were Côte d’Ivoire, Ghana, Indonesia, and Ecuador (Figs. 1b and S1b). Côte d'Ivoire exported nearly 2 Mt per year, whereas Ghana, Indonesia, and Ecuador exported 1.31, 0.97, and 0.33 Mt per year, respectively. EU countries of the Netherlands, Germany, France, and Spain, and Southeast Asian countries of Malaysia and Singapore were the major trading countries during this period. The Netherlands’ imports of cocoa were 1.57 Mt per year and 47.5% of these imports were exported elsewhere. Germany’s imports of cocoa were 1.33 Mt per year and 56.1% of these imports were exported elsewhere. High-income OECD countries of the USA, Belgium, UK, Italy, Canada, and Poland, and the middle-income country of Russia were the largest importers of the commodity. We obtained similar patterns from 2011 to 2015 (Fig. S1b).

The consumption rates per capita of cocoa in each country, based on the 2016–2020 data, markedly vary by the country’s economic status (Fig. 2b). HICs were the largest consumers of cocoa, with a median annual consumption rate of 1.06 kg per person. Comparatively, the median annual consumption of UMICs and LMICs were 0.23 and 0.02 kg per person, respectively. Cocoa consumption of high-income European countries of Belgium, the Netherlands, Switzerland, and Iceland far surpassed that of other countries (Fig. 2a). Belgium was estimated to consume 64 kg of cocoa per person annually, on average, and the country’s cocoa consumption had increased 5.3 times since the period of 1996–2000 (Fig. S21b). The Netherlands and Switzerland annually consume 48 and 24 kg per person, and cocoa consumption increased by a factor of 27 and 3.9 since the 1996–2000 period. Belgium and Switzerland are well known for their major chocolate production, and the Netherlands is the largest trade hub of cocoa beans in Europe (Alberts and Cidell 2006; Garrone et al. 2016).

Coffee

Between 2016 and 2020, the largest exporting countries of coffee were Brazil, Vietnam, Colombia, Indonesia, and Honduras (Figs. 1c and S1c). Brazil and Vietnam exported nearly 1.86 and 1.47 Mt per year, whereas Colombia, Indonesia, and Honduras exported 0.71, 0.36, and 0.34 Mt per year, respectively. Belgium was the largest trading country during this period, importing 0.3 Mt per year of coffee, and 62.9% of these imports were then exported elsewhere. High-income OECD countries of the USA, France, Germany, Italy, Canada, the UK, the Netherlands, Spain, Japan, and Austria were the largest importers of the commodity. Similar patterns were observed for the 2011–2015 period (Fig. S1c). Unlike oil palm and cocoa commodities whereby some countries play an important role as intermediaries or re-export hubs, coffee tends to be sourced directly from the producing countries (Figs. 1 and S1).

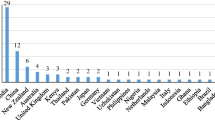

Data from the 2016–2020 period show that HICs were the largest coffee consumers, with median consumption rates of 6.69 kg per person per year (Fig. 2c). The median consumption of UMICs and LMICs was significantly lower (0.97 and 0.01 kg per person per year, respectively). Coffee per capita consumption of high-income European countries of Luxembourg, Andorra, Iceland, Austria, Finland, Estonia, Norway, and France, and tropical tourist destination countries of Bermuda, Aruba, and Palau were far above that of other countries (Fig. 2c). Luxembourg and Andorra were estimated to annually consume 93 and 78 kg of coffee per person, on average, and the consumption rates had increased 77.5 and 3.8 times since the period of 1996–2000 (Fig. S2c). Iceland and Austria annually consume 47 and 35 kg of coffee per person, and consumption rates increased 2.5 and 5.9 times over the last two decades. Tropical tourist countries of Bermuda and Palau annually consume 37 and 29 kg of coffee per person, and the consumption rates have increased tremendously by a factor of 184 and 294 in the last two decades.

How is the production of tropical crops associated with deforestation, and how does the estimation of crop-induced deforestation vary by approach?

For oil palm, deforestation risk attributed to the crop was estimated based on three approaches with decreasing order of accuracy: (i) direct attribution of the crop to deforestation (based on spatiotemporal distribution of the crop), (ii) indirect attribution of the crop to deforestation (based on current spatial distribution of the crop), and (iii) crude deforestation estimates (based on country-level crop data; Pendrill et al. 2022). For Indonesia, the deforestation risk estimate based on the direct attribution approach (330,102 ha per year) was higher than those based on the indirect attribution (164,470 ha per year), but lower than those based on the crude estimate (424,757 ha per year) (Fig. 3a). For Malaysia, the deforestation risk estimate based on the direct attribution approach (157,117 ha per year) was higher than that based on the indirect attribution (79,190 ha per year) and the crude estimate (46,015 ha per year) (Fig. 3a). For cocoa, spatiotemporal explicit data were not available for the crop, and deforestation risks were estimated based on indirect attribution and crude approaches. Similar to Malaysian oil palm, deforestation risks based on the indirect attribution approach for cocoa were higher than those based on the crude estimates (Fig. 3b). The deforestation risk associated with the development of cocoa in Cote d'Ivoire was 37,250 ha per year based on the indirect attribution approach, whereas the crude approach estimated deforestation of 14,541 ha per year. For Ghana, the indirect attribution approach estimated a deforestation risk of 18,837 ha per year, whereas the crude approach estimated zero deforestation. For coffee, a detailed distribution map derived from satellite images is not available; therefore, deforestation risk can only be based on crude estimates. Based on this approach, the deforestation risk associated with the development of coffee in Colombia was 13,747 ha per year, and in Brazil and Vietnam approximately 1,300 ha per year (Fig. 3c).

a–c Deforestation risk associated with the cultivation of oil palm, cocoa, and coffee, and d–f percent forest loss attributed to these commodities between 2011 and 2019 accounting for the extent of forest in 2011. Deforestation risk or percent forest loss is broken down by the approach used to derive the estimates with decreasing order of accuracy: (i) direct attribution, (ii) indirect attribution, and (iii) crude estimation approach. Major producing countries included in the assessment are Indonesia (IDN) and Malaysia (MYS) for oil palm; Côte d’Ivoire (CIV) and Ghana (GHA) for cocoa; and Brazil (BRA), Colombia (COL), and Vietnam (VNM) for coffee

Direct attribution and indirect attribution methods generally yielded a higher deforestation risk than the crude estimation approach twofold (Fig. 3a for oil palm in Malaysia and Fig. 3b for cocoa in Côte d’Ivoire and Ghana). An exception to this is oil palm in Indonesia, whereby the crude estimates were markedly higher than the direct attribution and indirect attribution methods (Fig. 3a). The underestimation of actual crop contribution to deforestation derived from the crude sub-country-level datasets for Côte d’Ivoire and Ghanaian cocoa is likely due to the predominance of smallholders in the production of these crop in these countries (Somarriba and López Sampson 2018; World Cocoa Foundation 2019), which makes the attribution of the crops to deforestation difficult to be accurately captured from the sub-national administrative data. On the other hand, the overestimation of actual crop contribution to deforestation derived from the crude sub-national-level datasets for Indonesian oil palm is likely due to the presence of multiple extractive industries (logging, timber plantations, and mining) in major oil palm-producing areas in Indonesia (Abood et al. 2015; Gaveau et al. 2019), potentially overlooking the contribution of other sectors to deforestation in the sub-national data.

Although oil palm has the highest deforestation risk in terms of the absolute deforestation extent (in ha per year), the percentage of forest loss attributed to the crop is smaller compared to cocoa (Fig. 3d, e). Based on the indirect attribution method, oil palm is associated with 1.5% forest loss in Indonesia between 2011 and 2019 (given forest extent of 99.7 million ha in 2011) and 3.8% forest loss in Malaysia (forest extent of 18.9 million ha in 2011) (Fig. 3d). Comparatively based on the same method, cocoa is associated with 8.5% forest loss in Cote d'Ivoire (given forest extent of 4 million ha in 2011) and 2.1% forest loss in Ghana over the same period (forest extent of 8 million ha in 2011) (Fig. 3e).

How have environmental clauses been incorporated into trade agreements and how effective are they in achieving the environmental goals?

Trade agreements aim to boost investments and commercial ties between participating countries by reducing or eliminating certain barriers to trade, such as reducing tariffs on products imported to a country. Import tariffs of goods across different countries had drastically reduced from an average of 14% before 1995 to 5% prior to 2020 (World Bank 2022), allowing easy movement of materials and goods over distant places. However, sending and receiving goods from one place to another also has implications for the redistribution of environmental costs along the production chain, and these costs are often unaccounted for in trade (Meng et al. 2018; Chen et al. 2021). The RTA database shows that more regional and bilateral trade agreements are being made, especially in the last three decades (Fig. 4a). Before 1990, there were three trade agreements signed per year on average globally, but the number increased to 15 per year in the period of 1991–2022.

Trends in a the likelihood of trade agreements signed per year between 1960 and 2021, and b the strength of environmental elements in trade agreements between 1980 and 2021. See Table 1 for the definition of the strength

Of all 512 trade agreements signed between 1980 and 2022, 195 agreements contain environmental clauses or references to environmental protection and/or sustainability (Table S2). These environmental elements can be classified as: (i) very weak: these agreements contain only a brief reference to the environment or sustainable development; (ii) weak: these agreements contain more texts on a commitment to sustainable development and environment than the ‘very weak’ category, but still lack the details of the reviewing processes; (iii) medium: these agreements include a more substantial review of the impact of the agreement on sustainability, including the role of public participation in the review; (iv) strong: these agreements include a set of environmental criteria for defining the sustainability of the traded goods (Tables 1, S3).

We classified 94 of the 195 agreements as ‘very weak’ in terms of environmental commitments, 79 as ‘weak’, 20 as ‘medium’, and two as ‘strong’. The inclusion of environmental clauses in such agreements has become more common (Fig. 4b). After a decade since the period 2000–2009, ‘weak’ agreements displaced ‘very weak’ agreements as the most common category. ‘Medium’ and ‘strong”’ agreements increased from only 9.5% in the period of 2010–2019 to 28.9% only in the last few years. Of those agreements classified as ‘medium’ or ‘strong’ between 2000 and 2022 (a total of 22), the majority (18) featured the EU and/or the UK as a party and the remaining four included the US, EFTA (European Free Trade Association), and Nicaragua–Taiwan.

What is the evidence of sustainability standards’ effectiveness and impact?

Geographical and certification scheme coverage of past evaluations

A total of 51 studies of sufficient quality were found that evaluate the impact of sustainability certification for oil palm (Table S3; Fig. 5a). The majority of studies were carried out on the voluntary certification scheme RSPO (Roundtable on Sustainable Oil palm) (40 studies), and the remaining were on the national certification ISPO (Indonesian Sustainable Oil palm) and MSPO (Malaysian Sustainable Oil palm). Of these 51 studies, 41 were conducted in Indonesia and Malaysia and 8 in other countries (Thailand, Colombia, Ecuador, and Ghana). There was no study on other voluntary certification schemes supposedly important for oil palm, such as ISCC + (International Sustainability and Carbon Certification Plus) and RSB (Roundtable on Sustainable Biomaterials). This is probably because these schemes are not specific to oil palm and they are widely applied to other commodities and biofuel production and supply chains.

Environmental and social impacts of sustainability certification for a oil palm, b cocoa, and c coffee, estimated from past studies. Studies are categorised based on: (i) the methodology used to derive evidence of impact: rigorous counterfactual versus case report or case–control approach; and (ii) the crop production model evaluated: large-scale plantations versus independent smallholders or medium-scale farms

A total of 25 studies were found for cocoa certification schemes, mostly focused on Côte d’Ivoire and Ghana (Table S4; Fig. 5b). These studies were carried out on farms certified by Rainforest Alliance Sustainable Agriculture (RA-SA), UTZ, or Fairtrade Cocoa schemes. For coffee certification schemes, we found significantly more studies than in cocoa (47 studies) (Table S4; Fig. 5c). A total of 27 studies were from countries in Latin America, 17 from countries in Africa, and 3 from Asia. Studies were carried out on farms certified by RA-SA, UTZ, Fairtrade, or 4C (The Common Code for the Coffee Community) schemes.

Agriculture production models and sustainability indicators evaluated

For oil palm sustainability certification, the evaluation studies found vary by producer type, i.e. plantations (including scheme smallholders) and independent smallholders (Fig. 5a). A large proportion of studies from Indonesia and Malaysia were derived from company plantations (32 out of 51 in total) and 19 were from independent smallholders. This could reflect the fact that key oil palm players in this region are large producers (Varkkey et al. 2018; Santika et al. 2021). On the other hand, studies on cocoa and coffee certification were all carried out on independent smallholders (typically under cooperative schemes) and medium-scale farms (Fig. 5b, c). This could reflect the majority of agricultural production models for these two crops globally (Somarriba and López Sampson 2018; World Cocoa Foundation 2019).

In terms of the sustainability indicators, studies for the oil palm certification schemes evaluated a wide range of sustainability dimensions, including deforestation and biodiversity, GHG emission, water and soil management, poverty, and human rights and land tenure conflicts (Fig. 5a). Studies appraising human rights or land tenure outcomes, as well as GHG emissions or fire, are more common in oil palm compared to cocoa and coffee (Fig. 5). The absence of human rights, land tenure, and conflicts appraisal for cocoa and coffee certification may be partly because the production model of these crops is dominated by small-scale or medium-scale holders (Somarriba and López Sampson 2018; World Cocoa Foundation 2019). This is quite different from many oil palm production contexts, whereby large-scale plantations are key actors in major oil palm-producing countries, and the countries’ weak land tenure systems often allow large-scale land acquisitions to occur leading to long-standing conflicts between agroindustry and local communities (Castellanos-Navarrete et al. 2021; Yang and He 2021), thus making land tenure topics especially relevant for the crop. Nonetheless, human rights issues especially regarding child labour (i.e. workloads and deprived opportunities for health and education development as defined by ILO) and trafficking are recognised as pervasive issues in oil palm (Pasaribu and Vanclay 2021), cocoa (Perkiss et al. 2021), and coffee (Bager and Lambin 2020), regardless of the crop production model. The lack of GHG emission appraisal in cocoa and coffee is likely because cocoa and coffee are generally cultivated on mineral soil, unlike oil palm which has been extensively developed on peatland in the major producing countries of Indonesia and Malaysia (as part of government legacy in the utilisation of perceived “unproductive” land) (Dohong et al. 2017) and therefore making GHG emissions a highly relevant issue. Thus, the sustainability indicators covered by existing evaluations likely reflect specific challenges faced by each crop and the associated biophysical and socio-political contexts of the cultivated region.

Evidence of impact of sustainability certifications

Available evidence on the environmental and social impact of certification was largely drawn from case report or case–control approaches (comparing before and after, or with and without intervention, whether or not they address confounding factors). Of the total 51 studies we evaluated for oil palm, only a third (16 studies) applied a rigorous counterfactual approach (Fig. 5a), and nearly all of these were conducted on RSPO-certified plantations. For cocoa, a third of the studies (8 of 25) applied a counterfactual approach (Fig. 5b). For coffee, the proportion of studies applying a counterfactual approach was higher than for cocoa (51%) (Fig. 5c).

The impact of sustainability certification for oil palm appears to be mixed across different dimensions of sustainability (Fig. 5). The environmental impact of certification (deforestation and biodiversity, GHG emission, and water and soil management) was neutral or negligible, but the social impact (poverty, human rights, and land tenure) tends to be negative. For cocoa and coffee, the impact of certification tends to be positive on the environmental sustainability indicators. Certification impact on poverty and income appears positive for cocoa, but mixed (positive and neutral) for coffee.

Discussion and conclusions

A range of policy levers exist to achieve a reduction in the consumption and demand of tropical commodities. A broad distinction can be drawn between reform-oriented policy levers, which work through market-based mechanisms, and more transformative pathways (Acosta 2013; Martin et al. 2020). The likely effectiveness of different reform-oriented policy levers and the shift in political will required to achieve them vary. Broad normative economic proposals relating to degrowth in wealthy nations and enhanced sharing of wealth are put forward in ecological economics (Hickel 2020; Lenzen et al. 2022). These include practical proposals, such as cutting advertising industries to tackle consumption (Niinimäki et al. 2020; Sina et al. 2022), banning high environmental impact industries that have little value to society (e.g. private jets, large mansions) (Lynch et al. 2019), and eliminating planned obsolescence (Satyro et al. 2018; Bisschop et al. 2022). Degrowth scholars argue, however, that for poorer nations, growth is still necessary (Hickel 2021). Convivial conservation proposals call for more radical levers (Büscher et al. 2022). Below, we discuss some measures that fit within the deeper end of the reform-oriented spectrum and some that potentially could be classified as transformative in nature for tackling deforestation in supply chains, and more holistic visions of future pathways toward sustainability.

Reducing consumption of tropical commodities

Extractivism and neo-extractivism have long-standing roots in colonial and post-colonial development processes, in which tropical regions have been exploited for their natural resources and labour. Reformist proposals have focused on enhanced natural resource governance through conventional economic policies, which present environmental damage largely as a given (Acosta 2013). From this point of view, problems and conflicts that arise from extractivism can be solved with “proper governance” of how natural resources are used. The ways to achieve this are orthodox economic policies, such as increasing responsibilisation and participation of civil society in the oversight of extractive industry projects, more social investment in the areas where extractivism takes place to reduce social protests, and transparent information about the income obtained by the extractive enterprises, local governments, and central government. Environmental destruction is accepted as the inevitable cost of achieving development. Development paths that are inherently based on natural resource exploitation have critical implications for politics, social relations, and territorial orders, although these vary depending upon the willingness, for example, of political elites to support rent redistributions (Burchardt and Dietz 2014).

The sustainability of land and raw material use is increasingly challenged by over-exploitation, an increase in high-consumption lifestyles, and the unwillingness to target rich asset owners with taxes, and to deliver land reforms that tackle land inequalities (Burchardt and Dietz 2014). The extraction of raw materials has high environmental impacts, but their monetary value is significantly lower than that of processed goods (Frey et al. 2018; Givens et al. 2019). In the global system where places have unequal economic positions perpetuated by colonial histories (Ziai 2016), centres of consumption allow the exchange of values of materials through trade while undermining the productive potential of places where the raw materials are extracted. The accumulation of these value exchange activities allows centres of consumption to further extract raw materials and low-cost labour from the producing areas (Mair et al. 2016) and shift the environmental and social burden to the latter (Essandoh et al. 2020; Chen et al. 2021), consequently widening the social and economic disparities between places along the supply route (Mossay and Tabuchi 2015; Backhouse et al. 2021). It also distances economic agencies from territorial actors (Bonnedahl et al. 2022).

The relationship between centres of consumption and producing areas can reflect the interconnection between high- and low/middle-income countries at the global scale under the current market system (Cai et al. 2018; Duan et al. 2021), as well as urban and rural areas (Sethi and Puppim de Oliveira 2015; Zhang et al. 2018), and general public and elite wealth within countries (Mirza et al. 2019; Beckert 2022). As our analysis shows, per capita consumption of forest-risk commodities for oil palm, cocoa, and coffee generally follows the country's socioeconomic status; countries with higher income are associated with higher consumption rates overall than countries with lower economic status (Fig. 2). Similar conclusions were found in other studies (Pendrill et al. 2019; Sun et al. 2022). Per capita consumption rates have increased over time for all country types, but they tend to race to the level where the highest consumption can be attained in a given period, in this case by HICs (Fig. S1). The level of consumption by HICs can influence other countries by providing legitimation to emulate a similar consumption trajectory, a behaviour analogue to the debate on historical greenhouse gas emission (GHG) expenditure (Wei et al. 2012; Jakob et al. 2021). Furthermore, HICs continue to make up the largest proportion of importing and trading countries in raw oil palm, cocoa, and coffee, whereas LMICs make up the largest proportion of exporting tropical countries (Fig. 1) where most of the environmental costs are incurred (Fig. 3) (Dupas et al. 2022).

Existing patterns of ever-growing consumption, deterioration of tropical environments driven by trade, and the widening of socioeconomic inequality will continue unless appropriate measures are implemented. HICs have the largest responsibility and capabilities to reduce their per capita consumption of forest-risk commodities (Tukker et al. 2020; Hickel et al. 2022). In the short term, one potential option to reduce the consumption of forest-risk raw commodities and their derivative products is to apply consumption taxes, whether they are produced domestically or imported (Afionis et al. 2017; Rocco et al. 2020). Raising commodity prices is likely not a popular approach for consumers, especially when the products have already been subjected to other taxes, such as the sugar tax on chocolate (Shahid and Bishop 2019). However, public acceptance may be higher if the revenue collected were recycled to support smallholder farmers and programmes in crop-producing countries to reduce environmental degradation due to crop cultivation. Several studies have shown that richer nations’ consumers are willing to support activities linked to sustainable food production and consumption (Tait et al. 2016; Li and Kallas 2021). Alternatively, importing countries can apply import duties to forest-risk commodities and the revenue generated can be recycled to support producing countries’ sustainable agricultural programmes and environmental monitoring and mitigation. Some HICs may have already been obliged to set zero or limited tariff rates for certain commodities due to bilateral or multilateral trade agreements (e.g. EU imports of cocoa from most African countries receive zero tariff), and increasing import duties would place them in violation of their commitment under the WTO. However, it may be unlikely that their exporting partners would initiate a dispute if they were receiving the revenue.

More ambitious transformative shifts in the food system and dietary behaviour towards more locally adapted food consumption patterns and minimising food waste are also required to reduce consumption rates in HICs (Green et al. 2015; Alexander et al. 2016; Hickel 2020) and urban areas in countries of emerging economies (da Costa Louzada et al. 2018; He et al. 2018). Public procurement is another key tool for incentivising more sustainable production (Martin-Ortega and Treviño-Lozano 2023). There are also movements seeking to territorialise food and agricultural production as a whole, such as those supporting small-scale agriculture, agroecology principles, and reduced use of transgenic crops (Chaifetz and Jagger 2014). Such movements could receive more support from governments, e.g. through grant funding for food hubs or commoning institutions, such as Chambers of the Commons and Commons Assemblies, alongside land reform processes, which would represent deeper leverage points in richer nations with potential multi-dimensional benefits (Srnicek and Williams 2015).

Strengthening sustainability criteria in trade and a process of reform of environmental policy and land governance, and supporting improvement in producer country’s own certification system

Meeting certain environmental criteria can be used to render a reduction in import duties described above. In general, WTO regulations, including the Technical Barriers to Trade Agreement, require criteria to be expressed based on performance rather than descriptive characteristics. Trade preference given to ‘sustainable oil palm’, for example, is permissible, but specifying ‘sustainable oil palm’ as only those products certified by RSPO, or other voluntary schemes, would not. HICs’ government applying the measure would need to draw up a list of criteria for each forest-risk commodity which any supplier could potentially meet regardless of its membership in a certification scheme. These criteria can be informed by those listed in the existing voluntary standards. The use of voluntary certification schemes solely for trade preference is highly problematic due to several reasons. First, the existence and coverage of certification schemes vary widely, and some forest-risk commodities are either not covered or not to a great extent (Tayleur et al. 2017; van der Ven et al. 2018). Second, different certification schemes can cover different sets of criteria with different strengths in verification and auditing, and unintended consequences of ‘standards shopping’ may occur among suppliers (Schmeichel 2017). Third, past evaluations of the social and environmental impacts of voluntary certification schemes tend to show mixed results which put into question their effectiveness (Fig. 5) (Oya et al. 2018; Meemken et al. 2021) and numerous complexities exist due to a mismatch in the implementation across different sectors and institutional levels (Lambin and Thorlakson 2018; Pacheco et al. 2020; Katic et al. 2023). Fourth, certification systems are often time-consuming and costly to introduce and implement and this can be particularly challenging for smallholder farmers (Dompreh et al. 2021; Watts et al. 2021).

Some voluntary standards organisations have made efforts to address the above-mentioned issues, e.g. through the development of specific smallholder standards with the provision of support for audits and streamlined processes for group certification (Latynskiy and Berger 2017; Watts et al. 2021) and jurisdictional or landscape approaches to demonstrating compliance with criteria such as zero deforestation across a wider area than individual farms (Seymour et al. 2020; Watts et al. 2021). However, there seems to be little progress in certification for providing traceability systems and verifying compliance with criteria throughout the supply chain (Pacheco et al. 2020; Meemken et al. 2021). Additionally, low/middle-income country governments have often been unenthusiastic or unreceptive to voluntary standards, as these are often perceived to be Western-dominated systems imposed on commodity supply chains without considering the development priorities of the countries that produce the commodities (Schouten and Bitzer 2015; Tyson and Meganingtyas 2022). This sentiment also partly lies behind the development of national schemes, such as ISPO and MSPO for oil palm (Astari and Lovett 2019; Choiruzzad et al. 2021).

Although the use of environmental criteria in trade is feasible, it should not be regarded as an ideal method in isolation, especially under the broader aim of life-enhancing economies. Trade agreements are not intrinsically well suited to pursuing socio-environmental outcomes, as they focus necessarily on the mutual removal of restrictions (such as import duties, quotas, and administrative requirements) rather than incentivising different modes of production, consumption, or investment, which is generally what environmental policy seeks to do (Gammage 2018; Kolcava et al. 2019; Bastiaens and Postnikov 2020). A combination of different forms of measures, including trade restrictions (e.g. discrimination in trade between products produced sustainably or unsustainably, either legally or illegally) coupled with a process of reform of environmental policy and land governance in the producing country partner, as well as a reward system for sustainably produced products in the consumer markets, all supported by capacity-building assistance from donor countries, is likely to be more effective than the current status quo. Where low/middle-income country governments have interest and can mobilise political will to achieve ambitious environmental goals, using trade restrictions could provide a valuable reinforcement, especially where the sustainability criteria can be met by certification or similar systems that have been developed by the producer country itself, rather than those of external voluntary sustainability standards. The provision of support from high-income consumer countries would be vital and could include assistance to improve the producer country’s own certification system to ensure that it can credibly verify compliance with the criteria included in the agreement. In these circumstances, the inclusion of environmental criteria in trade agreements could play a valuable role. Nevertheless, regular and robust monitoring and evaluation will be required to assess both the direct and indirect impacts of these initiatives so that timely and adequate action can be taken to minimise the unintended effects (Sellare et al. 2022; Zhunusova et al. 2022).

Enhancing monitoring of crop environmental footprints through detailed spatiotemporal data

Efforts to monitor deforestation associated with commodity production have so far focused on industrial-scale plantations (e.g. oil palm and soybean), and this is mainly due to their social and environmental consequences (Fehlenberg et al. 2017; Phélinas and Choumert 2017; Santika et al. 2019) and the ease of capturing large-scale land cover change from satellite images. The impact of crop expansion by small-scale farmers has received less attention, although there have been growing calls for more rigorous monitoring (Ashiagbor et al. 2022; Ramírez-Mejía et al. 2022; Zhao et al. 2022). Elevated demands for tropical crops from the global market can incentivise lucrative practices and maximisation of production in the short term, and this likely has an impact on the exacerbation of agricultural expansion by both large-scale and small-scale producers following numerous mechanisms and pathways. Studies from Indonesia indicate that large-scale plantations were the primary actor in the expansion of oil palm in remote forest lands in the early stage of oil palm development; however, following the establishment of oil palm mills in the new development areas, the number of smallholders began to grow at rapid rates emulating the earlier expansion patterns of the large-scale producers, creating an extremely complex supply chain network (Prabowo et al. 2017; Heilmayr et al. 2020; Santika et al. 2021). Studies from the coffee sector in Ghana and Côte d’Ivoire show that lack of agricultural input and management due to limited capital in smallholders poses challenges to poor soil fertility and high pest and disease pressures, and this aggravates the abandonment of farms that are no longer productive on the seeking of new fertile lands and forest areas for agriculture (Ameyaw et al. 2018; Ashiagbor et al. 2022).

Our study shows that the widely used approach based on rudimentary data on crop distribution at the national or sub-national level tends to underestimate the crop deforestation risk attributed to both large-scale plantations and smallholder farms (Fig. 3). Detailed spatiotemporal change in land cover derived from satellite images that enable the detection and differentiation between large-scale plantations and small-scale farms can offer more accurate monitoring (Bey et al. 2020; Xu et al. 2020). Coupled with the trade datasets, they can be used to inform environmental policy measures. Nonetheless, while revealing the impact of deforestation on global supply chains is key for all actors, the availability of more information and traceability should not distract from the aim to catalyse change in the basic features of capitalist relations towards identifying and pursuing more transformative leverage points.

Potential transformative leverage points in achieving socio-ecological goals in supply chains

Current work on transformative change levers seeks to identify leverage points as possible entry points to a system to make far-reaching changes (Meadows 1999). In food and agricultural systems, transformations are increasingly called for in policy circles, including tackling deforestation, but the primary question is how to achieve such shifts given the power inequalities and concentrations of wealth within agrifood systems (Dupas et al. 2022; Slater et al. 2022). Neoliberal economic globalisation has given rise to multi-national corporate power, expansion of global value chains, and polycentric trade patterns, rendering communities and national governments less power than before to hold multi-national companies to account (Sikor and Lund 2009; Clegg et al. 2018). Actors who hold such power are increasingly able to influence the rules governing the global economy in their interests, leading to a thinning of democracy and a shrinking of civic space (Standing 2018). A recent intergovernmental assessment from IPBES urgently calls for a moderation of market fundamentalism, privatisation, accumulation, and extraction, and amplification of solidarity and ethics of care (IPBES 2019).

Measures such as import duties, environmental due diligence, and sustainability standards may be easier for governments to contemplate in the short to medium term, but this is fundamentally because such measures are relatively unchallenging to incumbent actors and relations in the global political economy. Evidence of the impact of sustainability standards is mixed (Oya et al. 2018; Schleifer and Sun 2020; Garrett et al. 2021) and trade agreements are rarely the best option to achieve socio-environmental goals (Rodrik 2018; Kehoe et al. 2020), and to some extent, they can be seen as a distraction from more transformative approaches (Martin et al. 2020). Given the fundamental limitations of market-based mechanisms, it is valuable to ask what a wider range of responses might entail that can facilitate meaningful transformative change to tackle deforestation and all other supply chain sustainability challenges, given that such challenges essentially share the same root cause.

Huge distances created between local dwellers in a landscape and those with control over it, by commodity trade relations, are problematic in terms of creating accountability and an ethics of care. Values, mindsets, attitudes, and feelings of connectedness to nature fundamentally shape the goals that determine land uses, and conversely, a sense of detachment has causally contributed to the deforestation affected by actors locally and extra-territorially (Brown et al. 2019; Bonnedahl et al. 2022). Uncoupling global value chains is needed to lessen the social and environmental costs (Akizu-Gardoki et al. 2018; Lenzen et al. 2022), although some trade will still be needed for food security reasons. Some commodities consumed in the Global North, such as horticultural crops, may be grown locally (López Cifuentes and Gugerell 2021; Li et al. 2022), while for other commodities, especially those with highly negative effects, there may be potential for substitutions (Green et al. 2015; Blay-Palmer et al. 2018). Understanding the potential pathways for uncoupling requires not only detailed scientific analyses of trade-offs, but also a broader exploration of potential value shifts and pathways to greater sustainability through post-growth scenarios (Hickel 2020; Lenzen et al. 2022).

There is a need to move beyond approaches that present sustainable supply chain issues, including deforestation, as fundamentally an issue relating to production zones, and instead, focus on the root causes of the problem. Attentiveness to different classes in society is needed, addressing their relative levels of responsibility and accountability for biodiversity losses, environmental degradation, and climate change (Büscher et al. 2022; Green and Healy 2022). Some actors have greater power in the broader structures of capitalist accumulation. Conservation initiatives not only need to give local people a central role as decision-makers in planning (Friedman et al. 2020; Carmenta et al. 2023), but also focus on behavioural change efforts to create greater democracy in larger structures of power which ultimately shape the success of local-scale initiatives (Büscher et al. 2022; Corson and Campell 2023). Attention has been focused on sourcing localities for far too long, and ultimately this lens depoliticises analytic diagnoses of sustainability challenges (Brockhaus et al. 2021; Kumeh and Ramcilovic-Suominen 2023). Refocusing attention on higher-scale concentrations of power and wealth and how to disrupt and overcome these is therefore key. This could be attained through radical policy prescriptions, such as debt cancellation for poorer nations that were colonised, taxing agro-commodity companies to internalise their social and environmental impacts, increased regulation, monitoring, and accountability of corporate impacts in deforestation-risk countries, as well as support for locally designed approaches which strengthen autonomy.

Data availability

All data used in this study were obtained from public repositories and are described in the cited references. Data on the systematic review and the strength of environmental provisions in trade agreements are included in the Supplementary Information of this article.

References

Abman R, Lundberg C, Ruta M (2021) The effectiveness of environmental provisions in regional trade agreements. Washington DC. No. 9601

Abood SA, Lee JSH, Burivalova Z, Garcia-Ulloa J, Koh LP (2015) Relative contributions of the logging, fiber, oil palm, and mining Industries to forest loss in Indonesia. Conserv Lett 8:58–67

Abu IO, Szantoi Z, Brink A, Robuchon M, Thiel M (2021) Detecting cocoa plantations in Côte d’Ivoire and Ghana and their implications on protected areas. Ecol Ind 129:107863

Acosta A (2013) Extractivism and neoextractivism: two sides of the same curse. In: Lang M, Mokrani D (eds) Beyond development: alternative visions from Latin America. Transnational Institute, Amsterdam, pp 61–86

Afionis S, Sakai M, Scott K, Barrett J, Gouldson A (2017) Consumption-based carbon accounting: does it have a future? Wiley Interdiscipl Rev Clim Change 8:e438

Akizu-Gardoki O, Bueno G, Wiedmann T, Lopez-Guede JM, Arto I, Hernandez P, Moran D (2018) Decoupling between human development and energy consumption within footprint accounts. J Clean Prod 202:1145–1157

Alberts HC, Cidell JI (2006) Chocolate consumption, manufacturing and quality in western Europe and the United States. Geography 91:218–226

Alexander P, Brown C, Arneth A, Finnigan J, Rounsevell MDA (2016) Human appropriation of land for food: the role of diet. Glob Environ Change 41:88–98

Ameyaw LK, Ettl GJ, Leissle K, Anim-Kwapong GJ (2018) Cocoa and climate change: insights from smallholder cocoa producers in Ghana regarding challenges in implementing climate change mitigation strategies. Forests 9:742

Ashiagbor G, Asante WA, Forkuo EK, Acheampong E, Foli E (2022) Monitoring cocoa-driven deforestation: the contexts of encroachment and land use policy implications for deforestation free cocoa supply chains in Ghana. Appl Geogr 147:102788

Astari AJ, Lovett JC (2019) Does the rise of transnational governance ‘hollow-out’ the state? Discourse analysis of the mandatory Indonesian sustainable palm oil policy. World Dev 117:1–12

Backhouse M, Lehmann R, Lorenzen K, Puder J, Rodríguez F, Tittor A (2021) Contextualizing the bioeconomy in an unequal world: Biomass sourcing and global socio-ecological inequalities. In: Backhouse M, Lehmann R, Lorenzen K, Lühmann M, Puder J, Rodríguez F, Tittor A (eds) Bioeconomy and global inequalities. Macmillan, Palgrave, pp 3–21

Bager SL, Lambin EF (2020) Sustainability strategies by companies in the global coffee sector. Bus Strateg Environ 29:3555–3570

Ballingall J, Pambudi D (2017) Dairy trade’s economic contribution to New Zealand. [online]. Available from: http://hdl.handle.net/11540/7268. Accessed 21 May 2022

Bastiaens I, Postnikov E (2020) Social standards in trade agreements and free trade preferences: an empirical investigation. Rev Int Organ 15:793–816

Beckert J (2022) Durable wealth: institutions, mechanisms, and practices of wealth perpetuation. Annu Rev Sociol 48:233–255

Bey A, Jetimane J, Lisboa SN, Ribeiro N, Sitoe A, Meyfroidt P (2020) Mapping smallholder and large-scale cropland dynamics with a flexible classification system and pixel-based composites in an emerging frontier of Mozambique. Remote Sens Environ 239:111611

Bigdeli SZ (2014) Clash of rationalities: revisiting the trade and environment debate in light of WTO disputes over green industrial policy. Trade Law Dev 6:177

Bisschop L, Hendlin Y, Jaspers J (2022) Designed to break: planned obsolescence as corporate environmental crime. Crime Law Soc Change 78:271–293

Blay-Palmer A, Santini G, Dubbeling M, Renting H, Taguchi M, Giordano T (2018) Validating the city region food system approach: enacting inclusive, transformational city region food systems. Sustainability (switzerland) 10:1680

Bonnedahl KJ, Heikkurinen P, Paavola J (2022) Strongly sustainable development goals: overcoming distances constraining responsible action. Environ Sci Policy 129:150–158

Brack D (2013) Trade and environment: conflict or compatibility. Routledge, London

Brandi C, Schwab J, Berger A, Morin JF (2020) Do environmental provisions in trade agreements make exports from developing countries greener? World Dev 129:104899

Brando PM, Paolucci L, Ummenhofer CC, Ordway EM, Hartmann H, Cattau ME, Rattis L, Medjibe V, Coe MT, Balch J (2019) Droughts, wildfires, and forest carbon cycling: a pantropical synthesis. Annu Rev Earth Planet Sci 47:555–581

Brinck K, Fischer R, Groeneveld J, Lehmann S, Dantas De Paula M, Pütz S, Sexton JO, Song D, Huth A (2017) High resolution analysis of tropical forest fragmentation and its impact on the global carbon cycle. Nat Commun 8:14855

Brockhaus M, Di Gregorio M, Djoudi H, Moeliono M, Pham TT, Wong GY (2021) The forest frontier in the Global South: climate change policies and the promise of development and equity. Ambio 50:2238–2255

Brown K, Adger WN, Devine-Wright P, Anderies JM, Barr S, Bousquet F, Butler C, Evans L, Marshall N, Quinn T (2019) Empathy, place and identity interactions for sustainability. Glob Environ Change 56:11–17

Burchardt HJ, Dietz K (2014) (Neo-)extractivism—a new challenge for development theory from Latin America. Third World Q 35:468–486

Büscher B, Massarella K, Coates R, Deutsch S, Dressler W, Fletcher R, Immovilli M, Koot S (2022) The convivial conservation imperative: exploring “biodiversity impact chains” to support structural transformation. In: Visseren-Hamakers IJ, Kok, Marcel TJ (eds) Transforming biodiversity governance. Cambridge University Press, Cambridge, pp 244–263

Cai X, Che X, Zhu B, Zhao J, Xie R (2018) Will developing countries become pollution havens for developed countries? An empirical investigation in the Belt and Road. J Clean Prod 198:624–632

Carmenta R, Barlow J, Lima MGB, Berenguer E, Choiruzzad S, Estrada-Carmona N, França F, Kallis G, Killick E, Lees A et al (2023) Connected conservation: rethinking conservation for a telecoupled world. Biol Conserv 282:110047

Castellanos-Navarrete A, de Castro F, Pacheco P (2021) The impact of oil palm on rural livelihoods and tropical forest landscapes in Latin America. J Rural Stud 81:294–304

Chaifetz A, Jagger P (2014) 40 years of dialogue on food sovereignty: a review and a look ahead. Glob Food Sec 3:85–91

Chen W, Kang JN, Han MS (2021) Global environmental inequality: evidence from embodied land and virtual water trade. Sci Total Environ 783:146992

Choiruzzad SAB, Tyson A, Varkkey H (2021) The ambiguities of Indonesian Sustainable Palm Oil certification: internal incoherence, governance rescaling and state transformation. Asia Europe J 19:189–208

Clegg S, Geppert M, Hollinshead G (2018) Politicization and political contests in and around contemporary multinational corporations: an introduction. Hum Relat 71:745–765

Corson C, Campell LM (2023) Conservation at a crossroads: governing by global targets, innovative financing, and techno-optimism or radical reform? Ecol Soc 28:3

da Costa Louzada ML, Ricardo CZ, Steele EM, Levy RB, Cannon G, Monteiro CA (2018) The share of ultra-processed foods determines the overall nutritional quality of diets in Brazil. Public Health Nutr 21:94–102

Davis KF, Koo HI, Dellangelo J, Dodorico P, Estes L, Kehoe LJ, Kharratzadeh M, Kuemmerle T, Machava D, Pais ADJR, Ribeiro N, Rulli MC, Tatlhego M (2020) Tropical forest loss enhanced by large-scale land acquisitions. Nat Geosci 13:482–488

Descals A, Wich S, Meijaard E, Gaveau DLA, Peedell S, Szantoi Z (2021) High-resolution global map of smallholder and industrial closed-canopy oil palm plantations. Earth Syst Sci Data 13:1211–1231

Dohong A, Aziz AA, Dargusch P (2017) A review of the drivers of tropical peatland degradation in South-East Asia. Land Use Policy 69:349–360

Dompreh EB, Asare R, Gasparatos A (2021) Stakeholder perceptions about the drivers, impacts and barriers of certification in the Ghanaian cocoa and oil palm sectors. Sustain Sci 16:2101–2122

Duan Y, Ji T, Yu T (2021) Reassessing pollution haven effect in global value chains. J Clean Prod 284:124705

Dupas MC, Halloy J, Chatzimpiros P (2022) Power law scaling and country-level centralization of global agricultural production and trade. Environ Res Lett 17:034022

Environment Act (2021) Environment Act 2021 [online]. Available from: https://www.legislation.gov.uk/ukpga/2021/30/contents/enacted. Accessed 5 June 2022

Essandoh OK, Islam M, Kakinaka M (2020) Linking international trade and foreign direct investment to CO2 emissions: any differences between developed and developing countries? Sci Total Environ 712:136437

European Commission (2021) Proposal for a regulation on deforestation-free products

FAO (2020) Global forest resources assessment 2020—key findings [online]. Rome. Available from: https://doi.org/10.4060/ca8753en. Accessed 4 May 2022

Fehlenberg V, Baumann M, Gasparri NI, Piquer-Rodriguez M, Gavier-Pizarro G, Kuemmerle T (2017) The role of soybean production as an underlying driver of deforestation in the South American Chaco. Glob Environ Change 45:24–34

Ferraro PJ (2009) Counterfactual thinking and impact evaluation in environmental policy. New Dir Eval 2009:75–84

Frey RS, Gellert PK, Dahms HF (2018) Ecologically unequal exchange: environmental injustice in comparative and historical perspective. Springer

Friedman RS, Rhodes JR, Dean AJ, Law EA, Santika T, Budiharta S, Hutabarat JA, Indrawan TP, Kusworo A, Meijaard E, St. John FAV, Struebig MJ, Wilson KA (2020) Analyzing procedural equity in government-led community-based forest management. Ecol Soc 25:16

Fuchs R, Brown C, Rounsevell M (2020) Europe’s Green Deal offshores environmental damage to other nations. Nature 586:671–673

Gammage C (2018) A critique of the extraterritorial obligations of the EU in relation to human rights clauses and social norms in EU free trade agreements. Europe World Law Rev 2:1–20

Garrett RD, Levy SA, Gollnow F, Hodel L, Rueda X (2021) Have food supply chain policies improved forest conservation and rural livelihoods? A systematic review. Environ Res Lett 16:033002

Garrone M, Pieters H, Swinnen JFM (2016) From pralines to multinationals: the economic history of Belgian chocolate. LICOS Discussion Paper No. 369, pp 1–40

Gaveau DLA, Locatelli B, Salim MA, Yaen H, Pacheco P, Sheil D (2019) Rise and fall of forest loss and industrial plantations in Borneo (2000–2017). Conserv Lett 12:e12622

Givens JE, Huang X, Jorgenson AK (2019) Ecologically unequal exchange: a theory of global environmental injustice. Sociol Compass 13:e12693

Green F, Healy N (2022) How inequality fuels climate change: the climate case for a Green New Deal. One Earth 5:635–649

Green R, Milner J, Dangour AD, Haines A, Chalabi Z, Markandya A, Spadaro J, Wilkinson P (2015) The potential to reduce greenhouse gas emissions in the UK through healthy and realistic dietary change. Clim Change 129:253–265

Hansen MC, Wang L, Song XP, Tyukavina A, Turubanova S, Potapov PV, Stehman SV (2020) The fate of tropical forest fragments. Sci Adv 6:eaax8574

Harris NL, Gibbs DA, Baccini A, Birdsey RA, de Bruin S, Farina M, Fatoyinbo L, Hansen MC, Herold M, Houghton RA, Potapov PV, Suarez DR, Roman-Cuesta RM, Saatchi SS, Slay CM, Turubanova SA, Tyukavina A (2021) Global maps of twenty-first century forest carbon fluxes. Nat Clim Change 11:234–240

He P, Baiocchi G, Hubacek K, Feng K, Yu Y (2018) The environmental impacts of rapidly changing diets and their nutritional quality in China. Nat Sustain 1:122–127

Heilmayr R, Heilmayr R, Carlson KM, Carlson KM, Benedict JJ (2020) Deforestation spillovers from oil palm sustainability certification. Environ Res Lett 15:075002

Hickel J (2020) Less is more: how degrowth will save the world. Penguin Random House, New York

Hickel J (2021) What does degrowth mean? A few points of clarification. Globalizations 18:1105–1111

Hickel J, O’Neill DW, Fanning AL, Zoomkawala H (2022) National responsibility for ecological breakdown: a fair-shares assessment of resource use, 1970–2017. Lancet Planet Health 6:e342–e349

Hoang NT, Kanemoto K (2021) Mapping the deforestation footprint of nations reveals growing threat to tropical forests. Nat Ecol Evol 5:845–853

IPBES (2022) Methodological assessment report on the diverse values and valuation of nature of the intergovernmental science-policy platform on biodiversity and ecosystem services. Balvanera P, Pascual U, Christie M, Baptiste B, González-Jiménez D (eds). IPBES Secretariat, Bonn, Germany

Jakob M, Ward H, Steckel JC (2021) Sharing responsibility for trade-related emissions based on economic benefits. Glob Environ Change 66:102207

Jones L, Kobza C, Lowery F, Peters C (2020) The rising role of re-exporting hubs in global value chains. J Int Commer Econ 1–42

Katic PG, Cerretelli S, Haggar J, Santika T, Walsh C (2023) Mainstreaming biodiversity in business decisions: taking stock of tools and gaps. Biol Conserv 277:109831

Kehoe L, dos Reis TNP, Meyfroidt P, Bager S, Seppelt R, Kuemmerle T, Berenguer E, Clark M, Davis KF, zu Ermgassen EKHJ, Farrell KN, Friis C, Haberl H, Kastner T, Murtough KL, Persson UM, Romero-Muñoz A, O’Connell C, Schäfer VV, Virah-Sawmy M, le Polain de Waroux Y, Kiesecker J (2020) Inclusion, transparency, and enforcement: how the EU-Mercosur trade agreement fails the sustainability test. One Earth 3:268–272

Kolcava D, Nguyen Q, Bernauer T (2019) Does trade liberalization lead to environmental burden shifting in the global economy? Ecol Econ 163:98–112

Kumeh EM, Ramcilovic-Suominen S (2023) Is the EU shirking responsibility for its deforestation footprint in tropical countries? Power, material, and epistemic inequalities in the EU’s global environmental governance. Sustain Sci 18:599–616

Lambin EF, Thorlakson T (2018) Sustainability standards: interactions between private actors, civil society, and governments. Annu Rev Environ Resour 43:369–393

Larrea C, Campos SL, Voora V (2021) Voluntary sustainability standards, forest conservation, and environmental provisions in International Trade Policy. International Institute for Sustainable Development

Latynskiy E, Berger T (2017) Assessing the income effects of group certification for smallholder coffee farmers: agent-based simulation in Uganda. J Agric Econ 68:727–748

Lenzen M, Keyβer L, Hickel J (2022) Degrowth scenarios for emissions neutrality. Nat Food 3:308–309

Li S, Kallas Z (2021) Meta-analysis of consumers’ willingness to pay for sustainable food products. Appetite 163:105239

Li M, Jia N, Lenzen M, Malik A, Wei L, Jin Y, Raubenheimer D (2022) Global food-miles account for nearly 20% of total food-systems emissions. Nat Food 3:445–453

Limenta M (2022) Toward an ASEAN-EU FTA: examining the trade and sustainable development chapter in the prospective Indonesia-EU CEPA. Leg Issues Econ Integr 49:191–216

López Cifuentes M, Gugerell C (2021) Food democracy: possibilities under the frame of the current food system. Agric Hum Values 38:1061–1078

Lynch MJ, Long MA, Stretesky PB, Barrett KL (2019) Measuring the ecological impact of the wealthy: excessive consumption, ecological disorganization, green crime, and justice. Soc Curr 6:377–395

Mair S, Druckman A, Jackson T (2016) Global inequities and emissions in Western European textiles and clothing consumption. J Clean Prod 132:57–69

Martin A, Armijos MT, Coolsaet B, Dawson N, Edwards GAS, Few R, Gross-Camp N, Rodriguez I, Schroeder H, Tebboth MGL, White CS (2020) Environmental justice and transformations to sustainability. Environ Sci Policy Sustain Dev 62:19–30

Martin-Ortega O, Treviño-Lozano L (2023) Sustainable public procurement of infrastructure and human rights. Edward Elgar Publishing

Meadows DH (1999) Leverage points: places to intervene in a system. The Sustainability Institute, Hartland

Meemken EM, Barrett CB, Michelson HC, Qaim M, Reardon T, Sellare J (2021) Sustainability standards in global agrifood supply chains. Nat Food 2:758–765

Meng B, Peters GP, Wang Z, Li M (2018) Tracing CO2 emissions in global value chains. Energy Econ 73:24–42

Mirza MU, Richter A, van Nes EH, Scheffer M (2019) Technology driven inequality leads to poverty and resource depletion. Ecol Econ 160:215–226

Mitchard ETA (2018) The tropical forest carbon cycle and climate change. Nature 559:527–534

Mossay P, Tabuchi T (2015) Preferential trade agreements harm third countries. Econ J 125:1964–1985

Munroe DK, Batistella M, Friis C, Gasparri NI, Lambin EF, Liu J, Meyfroidt P, Moran E, Nielsen JØ (2019) Governing flows in telecoupled land systems. Curr Opin Environ Sustain 38:53–59

Niinimäki K, Peters G, Dahlbo H, Perry P, Rissanen T, Gwilt A (2020) The environmental price of fast fashion. Nat Rev Earth Environ 1:189–200

Ovalle-Rivera O, Läderach P, Bunn C, Obersteiner M, Schroth G (2015) Projected shifts in Coffea arabica suitability among major global producing regions due to climate change. PLoS ONE 10:e0124155

Oya C, Schaefer F, Skalidou D (2018) The effectiveness of agricultural certification in developing countries: a systematic review. World Dev 112:282–312

Pacheco P, Schoneveld G, Dermawan A, Komarudin H, Djama M (2020) Governing sustainable palm oil supply: disconnects, complementarities, and antagonisms between state regulations and private standards. Regul Govern 14:568–598

Pan Y, Birdsey RA, Phillips OL, Jackson RB (2013) The structure, distribution, and biomass of the world’s forests. Annu Rev Ecol Evol Syst 44:593–622

Pasaribu SI, Vanclay F (2021) Children’s rights in the Indonesian Oil Palm Industry: improving company respect for the rights of the child. Land 10:500

Pendrill F, Persson UM, Godar J, Kastner T (2019) Deforestation displaced: trade in forest-risk commodities and the prospects for a global forest transition. Environ Res Lett 14:055003

Pendrill F, Persson UM, Kastner T, Wood R (2022) Deforestation risk embodied in production and consumption of agricultural and forestry commodities 2005–2018. [online]. Available from: https://doi.org/10.5281/zenodo.5886600. Accessed 21 Sept 2023

Perkiss S, Bernardi C, Dumay J, Haslam J (2021) A sticky chocolate problem: impression management and counter accounts in the shaping of corporate image. Crit Perspect Account 81:102229

Phélinas P, Choumert J (2017) Is GM soybean cultivation in Argentina sustainable? World Dev 99:452–462

Pillay R, Venter M, Aragon-Osejo J, González-del-Pliego P, Hansen AJ, Watson JEM, Venter O (2022) Tropical forests are home to over half of the world’s vertebrate species. Front Ecol Environ 20:10–15

Prabowo D, Maryudi A, Senawi D, Imron MA (2017) Conversion of forests into oil palm plantations in West Kalimantan, Indonesia: insights from actors’ power and its dynamics. For Policy Econ 78:32–39

Ramírez-Mejía D, Levers C, Mas JF (2022) Spatial patterns and determinants of avocado frontier dynamics in Mexico. Reg Environ Change 22:28

Rocco MV, Golinucci N, Ronco SM, Colombo E (2020) Fighting carbon leakage through consumption-based carbon emissions policies: empirical analysis based on the World Trade Model with bilateral trades. Appl Energy 274:115301

Rodrik D (2018) What do trade agreements really do? J Econ Perspect 32:73–90

Santika T, Wilson KA, Budiharta S, Law EA, Poh TM, Ancrenaz M, Struebig MJ, Meijaard E (2019) Does oil palm agriculture help alleviate poverty? A multidimensional counterfactual assessment of oil palm development in Indonesia. World Dev 120:105–117