Abstract

This study’s objective is to compare cluster economies and diseconomies for multinational enterprises (MNEs) and uninational enterprises (UNEs) within the London financial services cluster. In contrast to the implicit assumption of the cluster participation literature that the economies and diseconomies of clusters are valued similarly by all firms, we find that economies relating to social capital and labour market pooling are equally important to MNEs and UNEs, economies relating to local competition and diseconomies relating to congestion costs are more important to MNEs than to UNEs, and economies relating to the reputational effects of locating in a world-leading cluster and access to specialised suppliers are more important to UNEs than to MNEs. That MNEs and UNEs do not experience cluster economies and diseconomies in the same way indicates that both cluster participation theory and international business theory need augmentation to recognise that cluster incumbents benefit and suffer from cluster membership differently.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The economies and diseconomies of industrial clustering have long been studied by economists and management scholars (Dunning 1998; Marshall 1890; Porter 1998; Swann et al. 1998). Recently, two special issues on multinational enterprises (MNEs) and location in geographical clusters, one in the Journal of Economic Geography in 2011 and the other in the Journal of International Business Studies in 2013, point to a surge and convergence of interest in the subject by economic geography (EG) and international business (IB) scholars. Within IB, a re-evaluation of the spatial organisation of MNE activities has been underway since Dunning’s (1998) call for more research on location, and in particular, location in clusters. He concluded: “The extent to which MNEs promote, or gravitate to, spatial clusters within a country or region is an under-researched area” (Dunning 1998, p. 58). This is argued to be “[…] partly because scholars have believed that the principles underlying the locational decisions of firms within national boundaries can be easily extended to explain their cross-border locational preferences” (Dunning 1998, p. 49). This belief is explored in this paper and, in particular, we ask: Do MNEs experience different economies and diseconomies of location within a cluster compared to uninational enterprises (UNEs)?

In order to address this question, this paper begins by assessing cluster economies and diseconomies in a highly productive industrial cluster—the City of London financial services cluster. The City of London is an exemplar cluster (Cook et al. 2007), albeit one embedded as a node in an international network of key financial centres (Amin and Thrift 1992). It is one of the few examples of a cluster which stands serious comparison with the iconic status of Silicon Valley. This financial services cluster supports nearly 2.2 million jobs across the UK, paying more in tax than any other sector and contributing 12% of UK GDP (TheCityUK 2016). It is the global leader in fixed income, currencies and commodities (FICC) trading, cross-border lending, and specialty commercial insurance, and consistently occupies a top three position across other major business lines (The City UK 2016).

Following previous research (Nachum and Keeble 2003; Zaheer 1995; Zaheer and Mosakowski 1997), we adopt comparative analysis to investigate and identify those common and distinctive characteristics between MNEs and UNEs. Based on a dataset drawing from a large-scale mail survey, our analysis shows that MNEs and UNEs do experience different economies and diseconomies of location within the financial services cluster in London. Specifically, we find that social capital and labour pooling are equally important to MNEs and UNEs. However, local competition and congestion costs are more important to MNEs, while the reputational benefit of locating in a strong cluster and access to specialised suppliers are more important to UNEs.

Our study’s main contribution is to add sophistication to the extant literature. Scholars of industrial clusters have long studied the economies and diseconomies of cluster participation for firms in general but have not distinguished the effects between MNEs and UNEs (Marshall 1890; Porter 1998; Swann and Prevezer 1996). In contrast to the implicit assumption of this literature, that economies and diseconomies of clusters are valued similarly by all firms, we provide a finer analysis to suggest that the economies and diseconomies of cluster participation are valued differently by MNEs compared to UNEs.

In the next section, based on the established clusters literature and the emerging literature on MNEs in clusters, a set of hypotheses that relate to the research question are generated. Then, the research design of the study is stated describing its unit of analysis and its method of data collection and analysis. Next, we present and discuss the main results and additional results. The final section concludes and states the managerial and policy implications of the study.

2 Literature Review and Hypotheses

Clusters are defined as related firms based in a geographical area (Swann and Prevezer 1996). The geographical concentration of production is not a new phenomenon, and dates back at least to Alfred Marshall who introduced the ‘industrial district’ concept describing the pattern of industrial organisation in late nineteenth century Britain in his Principles of Economics (Marshall 1890). Cluster participation is theorised as incumbents’ desire to access more effectively certain resources in industrial clusters by locating in geographic proximity (Enright 2000; Nachum and Keeble 2003; Porter 1998). A firm is said to participate in a cluster when it is located in geographic proximity to a collection of related firms and maintains various forms of formal and informal linkages with them (Nachum and Keeble 2003).

The economies and diseconomies of cluster participation have attracted much interest among management scholars with notable representatives including Porter (1998), Swann et al. (1998), Dunning (1998), and the two special issues (Journal of Economic Geography in 2011 and Journal of International Business Studies in 2013) on MNEs and location in geographical clusters. Drawing from this stream of literature, the specific economies and diseconomies of locating in a cluster from the perspective of the clustered firm are explained as follows.

Firms may be attracted to a location due to the existence of fixed factors (Swann et al. 1998). These are benefits that exist at a location that are not a function of the co-presence of related firms and institutions and include climate, time zone and language. Beyond these fixed factors, we can distinguish between economies and diseconomies of clustering. The former refer to increased benefits for incumbent firms as each additional firms joins the cluster. The latter refer to decreased benefits for incumbent firms as each additional firm joins the cluster. An additional firm joining the cluster will drive both effects at the same time to differing degrees, which will turn both on the specific identity of the firm and the maturity of the cluster. Net economies give the extent to which economies outweigh diseconomies and so indicate the strength of the cluster. Clusters then vary by strength according to the size of these net economies with rich, strong, high-performing clusters associated with large net economies and shallow, weak, low to average performing clusters associated with small or negative net economies. Economies and diseconomies can arise on both the demand and supply side.

On the demand side, the firm may benefit from customer proximity (Von Hippel 1988) which can be especially important when customers are sophisticated. Such customers can encourage innovation through sophisticated demand and by alerting suppliers of new trends and innovations. The clustered firm may also benefit from reduced customer search costs (Swann et al. 1998). The idea here is that the firm is more likely to be found by customers when it is located in a cluster. This is particularly important when customers have specific requirements. Information externalities on the demand side may also exist, that is, a cluster’s reputation rubs off on the firm that is located in it (Kalnins and Chung 2004).

On the supply side, a major benefit is that knowledge spills over in a cluster and this is particularly important when valuable industry knowledge is tacit rather than codified. In a sense, tacit knowledge becomes a public good (Marshall 1890; McCann and Folta 2009). When this happens, innovation can be more prolific. Mechanisms for knowledge spillovers include labour market churn, social interaction, spin-offs and diffusion via clients and suppliers. A second supply side benefit is access to specialised inputs (Marshall 1890; McCann and Folta 2009). As a result, the firm benefits from lower search costs because it can easily recruit from a pool of specialised labour and can tap into a specialised supplier base. Infrastructure benefits (Porter 1998) go beyond access to a good transport network to include institutions that coordinate activities across companies in order to maximise collective productivity, for example, trade associations which set standards and/or conduct marketing for the cluster as a whole. Better motivation can also exist within a cluster as local rivalry can act as a powerful spur. Also, it can be easier to measure performance (benchmark) against local rivals as they share a similar context leading to lower monitoring costs (Porter 1998). Another important supply side benefit is that it can be easier to try out new ideas in a cluster since it is possible to gain instant feedback and all of the inputs (including sympathetic venture capital) required for experimentation (Swann et al. 1998) are likely to be present in the cluster. Finally, a clustered firm may benefit from informational externalities on the supply side (Swann et al. 1998): The firm enjoys lower risk by observing successful production at a location.

With respect to cluster diseconomies, on the demand side, congestion and competition in output markets (Swann et al. 1998) can lead to lower prices and so profits can fall. Also, a cluster specialised in a particular technology can go into decline if that technology is substituted.

On the supply side, congestion and competition in input markets can lead to higher wages and rents which in turn could lead to movement out of the cluster (Pandit et al. 2002). This is a natural process and can be one whereby the cluster strengthens as those firms which can best take advantage of being in the cluster outbid others for factors of production. Three further decline factors can all tempt behaviour that erodes competitive advantage. Being close to competitors tempts cartel formation and isomorphism (herd behaviour) which can have a detrimental effect on innovation within the cluster (Porter 1990). A large labour pool tempts the formation of powerful trade unions which can stifle the cluster’s flexibility (Porter 1998). Finally, a successful cluster can be taken for granted by local government resulting in stagnant local infrastructure (Swann et al. 1998).

Despite the large literature on the economies and diseconomies of industrial clustering, MNE participation in clusters has not received much attention and has tended to be a by-product when the focus is on other issues (Beugelsdijk et al. 2010). In order to review what is known from empirical research in this emerging area, we systematically trawled the following leading international business and economic geography journals: Journal of International Business Studies, Environment and Planning A, Journal of World Business, Management International Review, and Journal of International Management since 1998 when Dunning published his seminal paper ‘Location and multinational enterprise: a neglected factor?’. We found a total of seven empirical studies of MNE participation in clusters. From these, we located two further relevant studies published in other journals making a total of nine. These studies are summarised in Table 1 and are used to inform the hypotheses that follow.

2.1 Testing the Implicit Assumption of the Cluster Participation Literature

Given the limited literature on MNE participation in clusters, all of the hypotheses that follow are agnostic and derived from arguments in favour of both MNEs and UNEs. Empirical testing will then determine which, if any, are indeed agnostic and which, if any, favour MNEs and which, if any, favour UNEs.

The clusters literature emphasises the importance of social capital that exists in clusters which relies on physical proximity for the building of trust and personal relationships and encourages mutual support (Hendry and Brown 2006). A higher degree of information sharing and cooperation can enhance not only innovation but also productive efficiency. Face-to-face contact is a classic advantage of proximity, which allows not only trust to be built and maintained but also complex, tacit knowledge to be exchanged. The most common finding of the literature summarised in Table 1 on the motivation for MNE location in clusters is that MNEs locate in clusters to source tacit knowledge (Alcacer and Zhao 2012; Hervas-Oliver 2015; Jenkins and Tallman 2010; Mariotti et al. 2010). Three studies attempt to compare and contrast MNE motivation with non MNE motivation. Jenkins and Tallman (2010) and Manning et al. (2010) find that both MNEs and non MNEs (‘isolated firms’ in the case of the former; ‘local firms’ in the latter) benefit from and add to cluster knowledge. Similarly, Nachum and Keeble (2003) find that both ‘foreign’ and ‘indigenous’ firms benefit from social capital. MNEs and UNEs are likely to benefit similarly from a cluster’s social capital because MNEs have increasingly abandoned hierarchical organisational structures in favour of more decentralised organisational structures and have therefore adopted similar operations and organisational processes to UNEs (Nachum and Keeble 2003; Rosenzweig and Singh 1991). This MNE organisational evolution results in greater autonomy for subsidiaries and drives changes in subsidiary activities (Bartlett and Ghoshal 1989; Birkinshaw and Hood 1998; Hennart 2009). Nachum (2003) supports this line of thinking by identifying the increased importance and autonomy of foreign subsidiaries. More autonomous subsidiaries tend to control a larger amount of the value chain and share responsibility for innovation and knowledge creation (Rugman and Verbeke 2001; Rugman et al. 2011). As a result, MNE subsidiaries are likely to be deeply embedded in local clusters and benefit from social capital to the same extent as local UNEs.

Hypothesis 1: In strong clusters, social capital will be equally important to MNEs and UNEs.

The second most common finding of the literature summarised in Table 1 on the motivation for MNE location in clusters is that MNEs locate in clusters because other MNEs have located there. This isomorphic behaviour is most acutely observed by Manning et al. (2010) and Mariotti et al. (2010). Amin and Thrift (1992) suggest that strategic sense-making and strategy formulation with references to peers is a powerful reason why MNEs locate in global cities. Furthermore, Knickerbocker (1973) argues that FDI in oligopolistic industries such as financial services is due to imitative behaviour and that such behaviour is a method of coping with uncertainty. MNEs find that the safest thing to do is to copy rivals and this benchmarking is easier when co-located within a cluster. Hence, a ‘bandwagon effect’ (Sethi et al. 2003) is observed. Supporting this reasoning, Manning et al. (2010) find that MNEs follow other MNEs when making location choices within clusters and Mariotti et al. (2010) find that MNE location in clusters is subject to isomorphic tendencies. What is missing from this literature is a good argument for why UNEs would act differently from MNEs. Giachetti and Torrisi (2017) draw from neo-institutional theory and find that all types of firm imitate the market leader in highly uncertain environments. A cluster is such an environment because therein competition tends to be innovation-based with technologies and practises changing rapidly and a cluster is where the market leader is most likely to reside. This finding holds for all firms in highly uncertain environments with no distinction between MNEs and UNEs or size or market share. Accordingly, we test:

Hypothesis 2: In strong clusters, local competition will be equally important to MNEs and UNEs.

The clusters literature has long recognised that access to a skilled labour pool is a prime attraction to firms and central to the dynamics of clustering (Marshall 1890). Nachum and Keeble (2003) find that both ‘foreign’ and ‘indigenous’ firms benefit from labour pooling. Skilled labour in a cluster is highly valued by MNEs because a MNE can transfer, and so leverage, the knowledge embodied in that labour across different countries (Al Ariss et al. 2014). Also, whilst UNEs interface with their local business environment, MNEs additionally interface with business activities within the overall organisation across numerous locations making their overall environment more complex. It is possible that the more complex nature of MNE business activities mean that MNEs are better able than UNEs to extract potential value from skilled labour. Additional intra-firm knowledge flows places a premium on skilled labour that is better able to understand and absorb knowledge transferred internally within the firm. As MNEs will on average also pay higher wages than UNEs, they are better placed to attract premium skilled labour. Overall, this should mean that MNEs will be able to exploit strategic resources such as skilled labour to a greater extent than UNEs. Tatoglu et al. (2016) provide evidence that supports this line of thinking finding that MNEs employ more complex talent management systems than local firms.

Skilled labour is also highly valued by UNEs because it is one of the main avenues to access new tacit knowledge. Tacit knowledge diffusion occurs via this labour market mobility which increases with pool size. This is a reason why clusters, with their large labour market pools, are associated with high levels of innovation and productivity. This critical resource of skilled labour tends to be highly place-specific and so is a source of abiding competitive advantage to UNEs located in the cluster (Taylor et al. 2003). As the skilled labour pool deepens, so workers are incentivised to invest in higher levels of specialised human capital. The most successful UNEs attract the best talented labour which can subsequently spin-off to create new successful UNEs that attract yet more talented labour.

Overall, we suggest that labour pooling is valued similarly by both MNEs and UNEs although perhaps for different reasons.

Hypothesis 3: In strong clusters, labour pooling will be equally important to MNEs and UNEs.

The reputational advantage of a clustered location is a neglected benefit in the clusters literature generally but is well understood by scholars of the City of London (Allen and Pryke 1994; Clark 2002; Taylor et al. 2003). Being a City firm gives an assurance of quality to the customer, which overcomes an important information asymmetry regarding the true quality of what is essentially a credence good/service, whose quality is very hard to evaluate even after consumption. This is understandably important for UNEs. Equally, it is understandably important for new or less well-known MNEs. However, it may also be important for well-known MNEs that already have a reputation, often stemming from their home country, where a cluster’s reputational effect may complement and so enhance the MNEs country-of-origin effect (Vidaver-Cohen et al. 2015). To contribute to this debate, we test:

Hypothesis 4: In strong clusters, reputation will be equally important to MNEs and UNEs.

Access to specialised suppliers is one of the three classic Marshallian advantages of a cluster location (Marshall 1890). As the cluster deepens, so a greater array of specialised suppliers emerge (Mudambi 2008). That this factor might be more important to UNEs than MNEs is reasonable, given that MNEs are apt to have greater resources, knowledge and capabilities in-house compared to UNEs, an idea going back to Hymer (1976) and a cornerstone of Dunning’s Eclectic Paradigm (Dunning 1979). However, recent research shows declining MNE ownership of value chains with a greater tendency to rely on specialised suppliers rather than wholly-owned affiliates (Narula 2018). Focusing on service sector clustering, Nachum and Keeble (2003) concur, finding that both ‘foreign’ and ‘indigenous’ firms benefit from specialised suppliers. To contribute to this debate, we test:

Hypothesis 5: In strong clusters, access to specialised suppliers will be equally important to MNEs and UNEs.

From Table 1, we see that Manning et al. (2010) is the only empirical study to go beyond economies to consider diseconomies of clustering and find that cluster growth may lead to diseconomies. They find that MNEs are likely to be sensitive to some diseconomies of clusters (such as congestion costs and stagnant local infrastructure). MNEs have comparative information from their dispersed operations because of their different global strategic postures. Also, they make location decisions frequently and are more likely to change location for particular activities if there is a cost advantage. On the other hand, UNEs have all their ‘eggs’ in one locational basket and so will acutely experience diseconomies of clusters and will be less able than MNEs to mitigate negative consequences by, for example, moving some activities out of the cluster (Cook et al. 2007). To inform this controversy, we test:

Hypothesis 6: In strong clusters, congestion will be equally important to MNEs and UNEs.

3 Research Design

The foregoing literature review and theoretical arguments suggest that there are reasons to expect that there is similarity in terms of cluster economies and diseconomies between MNEs and UNEs. However, because of the unique characteristics of MNEs, the impact of cluster participation for MNEs may be different from that for UNEs. We attempt to examine our hypotheses by focusing on one important cluster in this study. This cluster, or unit of analysis, needed to have two characteristics: Firstly, it needed to be a strong cluster. Secondly, it needed to have a substantial MNE component. The unit of analysis chosen, that meets both of these criteria, is the City of London financial services cluster.

3.1 The City of London Financial Services Cluster

The financial services industry plays a vital intermediary role in the world economy, moving funds from entities with savings to those with capital requirements. Swann states “Probably the strongest cluster in the UK is the financial services cluster in the City of London” (Swann 2009, p. 151). Similarly, Dunning states “Perhaps the best illustration of a spatial cluster, or agglomeration, of related activities to minimise distance-related transaction-costs, and to exploit the external economies associated with the close presence of related firms is the Square Mile of the City of London” (Dunning 1998, p. 61). Although the City has historically referred to the ‘Square Mile’ around the Bank of England, developments to the east, west, and north have extended the centre to the extent that the term ‘the City’ is now used to refer to the cluster as a whole and not just the square mile (Kynaston 2001).

The City is best understood as a wholesale financial services centre with core activities in banking, insurance, and fund management supported by a panoply of activities including legal services, accounting, management consultancy, advertising, market research, recruitment, property management, financial printing and publishing, and the provision of electronic information. The City remains strong, despite the financial services downturn beginning in 2007. The cluster has maintained its leading global position in terms of exporting more financial services than any other country and hosting the highest number of FRPS (financial and related professional services) headquarters (The City UK 2016). The financial services cluster in London is the global leader in FICC (Fixed Income, Currencies and Commodities) trading, cross-border lending and specialty commercial insurance, and consistently occupies a top three position across other major business lines (The City UK 2016).

London is also a leading FRPS cluster due to its network of interconnected businesses, suppliers, and associates. This ‘cluster effect’—which encompasses the full range of FRPS—provides the UK’s FRPS businesses with better efficiencies, productivity, access to talent, and more rapid innovation than other international locations (The City UK 2016). The London financial services cluster supports nearly 2.2 million jobs across the UK, paying more in tax than any other sector and contributing 12% of UK GDP (The City UK 2016).

What of the second criterion, the need for the cluster to have a substantial MNE component? The City’s current attractiveness as a centre for FDI and its position as the world’s most important international financial services cluster is the result of a number of significant developments in the post-war period, the most recent of which was deregulation in the 1980s which triggered a substantial rise in FDI in the City (Kynaston 2001). It was the first major deregulation of this type in Europe: “This focus on competitiveness meant that foreign investment was encouraged, resulting in most of the leading wholesale institutions being foreign owned” (HM Treasury 2003, p. 31, emphasis added). Clark states:

“London is an ‘industrial district’ that has attracted and retained firms whose home location could place them elsewhere in the world (in the US and Europe for example). Indeed, for many such firms, locating and developing a significant presence in London has been a conscious locational choice made both in relation to competitors and related firms, and in relation to the preferences and needs of UK and European customers” (2002, p. 438).

The globalisation of finance began to accelerate during the 1970s in terms of the growth of international banking and securities markets, the strengthening of the linkages between domestic banking and securities markets, and the deepening of these same domestic markets (Coleman 2014). In 2015, the UK attracted 94 international projects, accounting for one third of all financial services FDI in Europe, creating 8138 jobs (EY 2016).

3.2 Methods

The hypotheses were tested via a questionnaire (available from the authors on request) consisting of 40 cluster economy and diseconomy items. In almost all cases, respondents were asked to rank the importance of a potential economy (benefit) or diseconomy (cost) from 1 (not important) to 5 (very important) with an option of 0 if not applicable.

In order to ascertain the reach of cluster economies and diseconomies, a focus group study of senior financial services executives was conducted. This revealed that the appropriate area was up to 500 metres beyond the boundaries of the City of London and Canary Wharf. The focus group also advised which lines of activity to include within the questionnaire survey. The sample of financial services companies (engaged in banking, investment banking, insurance, fund management, legal services, accounting, management consultancy, advertising, market research, recruitment, property management, financial printing and publishing, and the provision of electronic information) was drawn from this area from the Market Location database. This UK database contains 2.3 million business records which detail contact names by job title, SIC and Market Sector codes, number of employees and location status (branch, head office or sole office and precise location based on postal address). It was therefore well suited for our purpose. Because of the particular importance of large ‘hub’ or ‘universal’ firms in the City, we over-sampled these by including all of the largest 350 financial services firms within our geographical boundary. A further 1150 financial services firms were then drawn at random from the remaining population of 22,650 firms. Accordingly, a total of 1500 questionnaires were posted, addressed to the chief executive officer, by name when it was known. The study benefited from the support of a very senior and highly regarded public official connected to the UK financial services industry who agreed to add her endorsement in the questionnaire’s covering letter.

A total of 310 usable questionnaires were returned, a response rate of just over 20%. Of these, 140 were UNEs and 170 were MNEs. We tested to see if our sample was representative. A Chi square analysis of the composition of the sample by 3 digit SIC line of activity against the 1500 questionnaires sent showed no statistically significant difference between the two groups. The critical value of Chi square (7) at the 10% level is 12.017, the calculated Chi square for our test for non-response bias is 3.395 for the 1150 stratified random sample, 5.367 for the 350 largest firms, and 5.457 for both groups combined. We are therefore confident that we have a random and representative sample of the population of interest. As a further check of non-response bias, tests were conducted for any significant differences between early and late responders (those who responded before and after a reminder request was sent). Using a Chi square test based on a null hypothesis of no difference in composition by 3 digit SIC, the calculated Chi square was 2.991 compared to the 10% critical value of Chi square (6) of 10.645, showing insufficient evidence to reject the null. Two-sample t tests were conducted using firm size and the score on each of the six main factors used in the analysis. Only one test showed a significant difference, that for the score on the ‘local competition’ factor, which was just significant at the 10% level. In summary, there is scant evidence of non-response bias.

Two related analyses were performed on the data in order to address the study’s objectives. Firstly, an exploratory factor analysis was conducted to organise and reduce the cluster economy and diseconomy variables into factors (or latent variables). Secondly, the derived factors scores were entered into logit and multinomial logit analyses to identify factors which discriminate between MNEs and UNEs, pooling domestic and foreign MNEs into a single MNE category in the logit model and keeping them separate for additional more fine-grained analysis in the multinomial logit. Multinomial logit is the appropriate estimation method, rather than conditional or mixed logit, since none of the variables represents an inherent property of the alternatives, UNE, domestic MNE or foreign MNE. We use the term foreign MNE rather than foreign subsidiary to reflect the fact that many foreign financial services MNEs are headquartered in the City (The City UK 2016). The City is therefore more than a subsidiary location for these MNEs. The use of multinomial logit here differs from the standard case in economics, where the alternatives are choices made by an individual and the variables represent influences on that choice. Instead, the variables here should be thought of as discriminators between different alternatives. This is akin to the use of multinomial logit in medical statistics, where the variables would be symptoms which are possible discriminators between different underlying pathologies (Long and Freese 2006).

Custom control and dummy variables were added to each model. Dummy variables were added for the principal line of activity, with banking being the default category and size was controlled for using numbers of employees, which resulted in the loss of 16 observations, and age, which resulted in a loss of a further 20 observations. Some analysis was performed using total assets as an alternative proxy for size, however this was not particularly informative, as it reduced the effective sample by a further 80 observations because some types of firm are not required to disclose such information. Total assets were never significant as a variable and their inclusion did not make a clear difference to the overall conclusions. Six variables were included in the initial analysis which identified how important a London location was in helping firms innovate through developing respectively: new products, new services, better ways of delivering products or services, developing new markets, improving organisational structure, and re-orienting the company strategically. A set of dummies was also included which indicated whether or not the firm had received important or very important benefits from interaction with personnel in another local company in each of the following ways: meeting at local business events; contact by telephone for short term problem solving; contact by telephone for information; mixing with industry colleagues in social settings; chance meetings where interesting information had been heard. A final set of dummies was included to capture (1) the extent of reliance on the South East as a source of labour (2) the proportion of work derived from contact with other firms in London; and (3) three variables were included to investigate how important informal channels of recruitment were for hiring senior management, senior staff and specialist staff. This reflects the hypothesised importance of personal contacts and reputation networks in recruitment of highly skilled knowledge workers. As explained below, the results presented are based on only a subset of these controls, following diagnostic checking.

The main reason for not estimating full structural equation models is that the purpose of the second analysis was not to test hypothesised relationships between the latent variables that are estimated but rather to examine if there is a significant difference between MNEs and UNEs on certain latent variables. We follow a standard approach of exploratory factor analysis to measure latent variables. We preferred exploratory factor analysis over principal components analysis as our purpose was to use our manifest variables to measure underlying factors, which are consistent with factors favouring and disfavouring clusters identified in the literature. It was not to reduce our data to a smaller set of uncorrelated variables which is the rationale for principal components analysis (Blunch 2008). We did not have sufficiently strong theoretical priors to impose the typical restrictions required for confirmatory factor analysis, namely that each of our manifest variables was related to one and only one factor or that particular parameter values could be imposed on the relationship between a particular factor and its manifest indicator.

Factor extraction was by principal axis factoring (Blunch 2008; Kim and Mueller 1978). Highly similar results (not reported) were obtained using principal components, therefore little hinges on this choice. The main method used to determine the number of factors to use was the scree plot (Cattell 1966), which indicated six factors at the point of inflection. According to Stevens (2002), the scree plot method is reliable provided there are over 200 observations. The scree plot is preferred to Kaiser’s criterion of retaining all factors with an eigenvalue greater than one as neither of the rules for Kaiser’s criterion being accurate are satisfied (Kaiser 1961): The average communality value is less than 0.6, even though there are less than 300 observations.

The method of rotation used was varimax, which has the benefit of producing more interpretable groups of variables on each factor, important because the factors themselves are of independent interest in this analysis (Field 2009). In principle, there is a case for oblique rotation as there are theoretical grounds for suspecting the factors to be correlated with one another. Inspection of the correlation matrix for the factor scores revealed no serious correlation between scores on the factors in each analysis. Nevertheless, Oblimin rotation was run as a robustness check. The substantive interpretation of the factors extracted was the same, although the factors themselves were not quite so distinct. For this reason, the results using Varimax rotation are reported. Nothing important hinges on this choice.

Stevens (2002) suggests that with at least 300 observations the relevant criterion is a factor loading of 0.364 or more. Based on this rule, factor loadings after rotation in excess of 0.37 are reported.

As stated above, initially 40 variables were entered. These sets of variables needed to be reduced as problems of multicollinearity were indicated by a determinant of the R-matrices well below 0.00001. Variables were identified for removal based on an inspection of the anti-image correlation matrix. No items had small correlations, all being above 0.6 and the vast majority being above 0.8, but off-diagonal elements were inspected to identify pairs of variables which had the largest correlations and/or correlation substantially greater than zero with several variables. Robustness analysis was conducted by deleting slightly different sets of variables where alternative borderline judgements were used. This did not materially affect the substantive conclusions regarding factor structures. We ended up with 24 variables.

Regarding the validity of the factor analyses, the Kaiser-Meyer-Olkin measure of sampling adequacy was very good at 0.846, indicating reliable factors would be extracted. The correlations in the anti-image matrix were all between 0.776 and 0.918, indicating good sampling adequacy. Cronbach’s α was generally satisfactory with all values apart from factor 6 lying above the 0.7 threshold. The value of α in each case was not sensitive to deletion of items in each sub-scale. This indicates that the scales are reliably measured.

Our dependent variable was independently obtained, thus reducing the risk of common method bias (Chang et al. 2010). Also, it is highly unlikely that the assessments of respondents would have been influenced by a working model of the relationship between status as MNE or UNE and the importance of particular sources of cluster economy and diseconomy. Furthermore, in many cases the variables loading onto a particular factor were not adjacent to one another in the questionnaire. Finally, our results are not degenerate, as would be indicated if all manifest variable load onto one big factor. We identify many distinct factors which make sense in relation to the existing literature. In summary, the results are unlikely to be seriously affected by common method bias.

We do not control for multiplant enterprises. This is because in many areas in financial services, there are branch offices (think of the major banks) and many of these will be small and of little strategic significance, so separately examining multiplant firms is not very meaningful in this sector in the way that it would be if we were dealing with manufacturing, where even a small production facility is a far bigger commitment than a branch of a bank or an insurance company. Two robustness checks were made. First, a dummy variable was added to indicate a multiplant UNE (MNEs are by definition multiplant). This was always well short of being significant. Second, multiplant UNEs were identified as a separate category in a multinomial logit analysis. In this case, the results were not significant and were uninformative.

Regarding the main results, we report results for MNEs as a whole and do not distinguish between foreign and domestic MNEs because our results show that, except for the composition of the domestic and foreign MNE samples by sub-sector, there are no strong differences between them regarding the clustering variables or the key controls. An auxiliary logit model, modelling the difference between domestic and foreign MNEs (not reported), but excluding the sub-sector dummies, was well short of significance (χ2(16) = 15.59, p = 0.4818). The auxiliary regression including the sub-sector dummies was significant at the 5% level.

4 Main Results

The factor loadings in Table 2 show how strongly each variable correlates with the factor onto which it loads. It is not unusual, nor a problem, if one variable loads onto more than one factor. We organise and reduce the cluster economy and diseconomy variables into six factors, namely social capital, local competition, congestion costs, labour pooling, reputation, and specialised suppliers.

We then enter derived factor scores into a main logit analysis to identify factors which discriminate between MNEs and UNEs and also a multinomial logit analysis for some auxiliary analysis to identify factors which discriminate between UNEs, domestic MNEs and foreign MNEs. The dependent variable in the logit model takes the value 0 for a UNE, and 1 for an MNE and in the multinomial logit model takes the value of 0 for a UNE, 1 for a domestic MNE, and 2 for a foreign MNE. The results do not show how important the factors are in absolute terms. Rather, they show similarities and differences in how they are evaluated by each firm type. In the logit model, a factor with a positive coefficient is more important for MNEs whilst a factor with a negative coefficient is more important UNEs. Statistical insignificance indicates that the factor is equally important for MNEs and UNEs. It does not necessarily indicate that the variable is not important to either type of firm, merely that they rate the importance of the variable in much the same way. Interpretation is not so straightforward in the multinomial logit and will be explained fully below.

Table 3 presents the main findings of the study from our logit analysis and shows the standard coefficients and the marginal effects, which are average marginal effects taken over all observations in the sample. The marginal effects give the change in the probability the firm is an MNE for a small change in the continuous variables and for the presence of a characteristic for the qualitative variables.

The results clearly support hypothesis 1. Social capital is statistically insignificant. This suggests that this cluster factor has similar economies for MNEs and UNEs. The group of variables loading highly onto the social capital factor concern geographical proximity’s promotion of personal relationships, which is important to both MNEs and UNEs because a higher degree of information sharing and cooperation, which can enhance not only innovation but also greater productive efficiency in the finance industry.

Regarding hypothesis 2, the coefficient on local competition is positive and significant at the 5% level. This indicates that this cluster factor is more important to MNEs compared to UNEs, which supports the findings of Manning et al. (2010), Mariotti et al. (2010) and the theoretical reasoning of Amin and Thrift (1992) and Knickerbocker (1973). It is notable that the spur of rivalry and the ability to benchmark load heavily onto local competition, supporting one of Porter’s (1990) leading contentions. The ability to access real time information is also highly important. There is also a link between local competition and the ability to take market share from rivals and this is redolent of Hotelling’s (1929) work which was the first to model the geographical dimension of competition. All of this is not to say that locating close to rivals is unimportant to UNEs. It is likely that they too benefit from the increased ability to imitate rivals and the market leader in particular, benefit from the spur of local rivalry, access real time information and the ability to take market share from rivals. What we find is that MNEs value these abilities significantly more than UNEs.

The results clearly support hypothesis 3. Labour pooling is statistically insignificant. This indicates that this cluster factor has similar economies for MNEs and UNEs. The group of variables loading highly onto the labour pooling factor concern labour pooling’s promotion of innovation, the spread of tacit knowledge and best practise and labour and the facilitation of easier recruitment which are equally important to both MNEs and UNEs in the finance industry. Whilst labour is mobile globally and the London labour market has global reach, the London labour market itself is immobile—people will come to the City, but not other locations even a short distance away.

Regarding hypothesis 4, the coefficient on reputation is negative and significant at the 5% level. This indicates that this cluster factor is more important to UNEs compared to MNEs. Reputation centres on information externalities on the demand side whereby the cluster’s reputation rubs off on firms that are located in it. As we have argued, this is a neglected benefit in the clusters literature generally but is well understood by scholars of the City of London (Allen and Pryke 1994; Clark 2002; Taylor et al. 2003). For example, Allen and Pryke find that “[…] in the case of finance, the abstract space of the City of London has secured its dominance over time through its ability continually to mould the space around it in its own image. The City is finance […]” (Allen and Pryke 1994, p. 459). Similarly, on the basis of extensive interview evidence, Clark finds that “[…] a firm’s reputation may depend upon the reputation of its financial centre as much as its own competence” (Clark 2002, p. 440). UNEs will be less prominent than MNEs and so may benefit disproportionately from a cluster’s reputation as a means for overcoming an important information asymmetry regarding the true quality of their product.

Regarding hypothesis 5, the coefficient on specialised suppliers is negative and significant at the 10% level. This indicates that this cluster factor is more important to UNEs compared to MNEs. Specialised suppliers in the City of London include the professional body The City UK, educational institutions such as London Business School and the Financial Times newspaper. That access to these specialist suppliers is more important to UNEs than MNEs is reasonable as MNEs, with their greater resources, are more likely to produce industry information and offer in-house professional development programmes compared to UNEs.

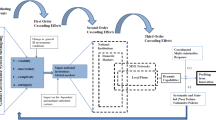

Regarding hypothesis 6, the coefficient on congestion costs is positive and significant at the 10% level. This indicates that this cluster factor is more important to MNEs compared to UNEs, which supports the argument that MNEs are likely to be particularly sensitive to congestion costs compared to UNEs because they have comparative information from their dispersed operations. Also, they make location decisions more frequently than the typical UNE and are, arguably, more likely to change location for particular activities if there is a cost advantage. Figure 1 depicts the main findings of the study.

Cluster economies and diseconomies

Some robustness testing was done by re-estimating the model for firms above median size (20 employees). The results were broadly similar, however the estimates were not precise, due to the high attrition among the UNEs, where only 25 firms remained, confounding the comparison. Two of the cluster variables switched sign, reputation and access to specialised suppliers, but were a long way from being significant. This is unlikely to be due to a pure size effect. A further auxiliary regression was run adding total assets to the model to control for size as well as numbers of employees and the coefficients on reputation and access to specialised suppliers remained negative and significant.

4.1 Additional Results

Table 4 shows factor means and means for age, total assets and employees for UNEs and MNEs, split between domestic and foreign and combined. It also shows the results of a standard t test of equality of means between UNEs and MNEs. A series of Scheffé tests of all pairwise comparison of means between UNEs, domestic MNEs, and foreign MNEs (not reported for brevity) revealed no significant difference between domestic and foreign MNEs on any variable in Table 4. Multinomial logit results, also show that it is data admissible to combine domestic and foreign MNEs, but not to combine either type of MNE with UNEs. It is plausible that liability of foreignness (Zaheer 1995) is less significant in our sample than it is generally. The literature suggests that liability of foreignness is apt to be less serious in a cosmopolitan world city like London (Castells 2000; Friedmann 1986; Hall 1966; Sassen 1991). Also financial services firms are highly globalised and do not suffer the liability of foreign to the extent suggested by the theory (Nachum 2003). To be sure, we ran a multinomial logit with UNE/domestic MNE/foreign MNE as categories and the results were qualitatively similar to the model we report and were very similar between the two types of MNEs. We have also conducted an analysis to make sure that the MNE effect is different from a size effect. Given that MNEs are larger than UNEs on average, we may expect the MNE effect may due to a size effect. This is not the case as we repeated the analysis only for large firms and the basic pattern of difference remained.

Table 4 shows that MNEs are significantly older than UNEs. They are also almost significantly larger than UNEs (the test for total assets is just outside conventional significance, but this test has fewer degrees of freedom, as there were gaps in the data on total assets). MNEs put significantly more emphasis on labour pooling and benchmarking against competition which would be expected given their strategic incentives for choosing to locate in a particular place. They are also significantly more sensitive, as expected, to congestion costs. UNEs place significantly more emphasis on the reputational benefits of locating in the City. As will be seen in the multivariate analysis, the significance of labour pooling disappears, whereas there is evidence that access to specialised suppliers is significantly more important to UNEs.

There were some differences in the preponderance of each type of firm in the various sub-sectors included in the data set. These were Banking, Insurance, Accounting, Legal, Management Consultancy and ‘Other’. Standard Chi square tests of association were carried out, in each case testing the null hypothesis that UNEs, domestic MNEs and Foreign MNEs were equally likely to be present in each sub-sector. In the main, this null was not rejected, however there were some exceptions. Foreign MNEs were significantly over-represented in the Banking sub-sector (χ2(2) = 39.80, p = 0.000). This difference remained highly significant when just comparing foreign and domestic MNEs (χ2(2) = 18.76, p = 0.000). This makes sense as there was a significant wave of entry of foreign banks into the City following deregulation in 1986. In addition, many central banks of foreign countries have outposts in the City. Foreign MNEs are significantly under-represented in Legal (χ2(2) = 9.75, p = 0.008). This difference remained highly significant when comparing domestic and foreign MNEs (χ2(2) = 9.49, p = 0.002). This also makes sense given the very specific characteristics of national legal systems, which creates an institutional barrier to entry. Foreign MNEs were also underrepresented in Fund Management, although this was only weakly significant (χ2(2) = 5.63, p = 0.06). The multinomial results that follow confirm that the principal difference in sub-sector composition is being driven by the foreign MNEs.

A series of Scheffé tests of comparison of means of Age, Total Assets, Employees, Social Capital, Competition, Congestion, Labour Pooling, Reputation and Specialised Suppliers were conducted, comparing across the different sub-sectors. There were no significant differences between any pair of sub-sectors at the 5% level. This is accounted for, in part, by relatively low degrees of freedom when breaking the data set down into its components. This provides some reassurance that the cluster effects reported in Sect. 4 are not being driven by differences in sub-sector composition.

Regarding Table 5, UNEs are the base outcome, against which the other two categories are compared. Unlike the logit model, the coefficients are not of central interest, however it can be noted that a positive coefficient indicates that a firm is more likely to be a domestic MNE than a UNE in the domestic MNE column and likewise, more likely to be a foreign MNE than a UNE in the foreign MNE column. The converse is true for a negative coefficient, which in both cases indicates that the variable is more likely to be associated with a UNE. What the coefficients do not show is whether an increase in a continuous variable, or the presence of a particular characteristic, is more likely to indicate the firm is a UNE, a domestic MNE or a foreign MNE, as they are based only on two-way, not three-way comparisons. The marginal effects, reported in Table 6, show the change in probability that a firm is a UNE, domestic MNE or foreign MNE. Here a negative coefficient indicates a lower probability that the firm will belong to the particular category indicated by the column and vice versa for a positive coefficient.

Tables 5 and 6 reveal some interesting auxiliary results. Starting with Table 5, and taking the domestic MNE category first, labour pooling and social capital are well short of conventional significance and as such do not influence the probability the firm is a domestic MNE, as opposed to being a UNE. Accordingly, these two factors, whilst they are important to both domestic MNEs and UNEs in an absolute sense, do not discriminate between them, so are equally important to each type of firm. Greater concern about congestion costs raises the probability the firm is a domestic MNE rather than a UNE and the effect is significant. Greater importance on the benefit of being able to benchmark against competition also raises the probability the firm is a domestic MNE and this effect is just outside conventional significance (p = 0.11). Greater importance placed on access to specialised suppliers lowers the probability the firm is a domestic MNE, as opposed to being a UNE and the effect is significant. Greater importance placed on reputational effects of locating in the cluster also lowers the probability the firm is a domestic MNE and this effect is just outside conventional significance (p = 0.13). Size, measured by employment, is strongly significant and increases the probability a firm is an MNE, consistent with the strongly significant different in mean size between the two types of firm. Recruiting a smaller percentage of staff from the South East significantly increases the probability the firm is a domestic MNE.

A very similar pattern is evident when foreign MNEs are compared to being a UNE (which remains the base category). Social capital and labour pooling are far from significance. A greater importance placed on benchmarking against competition and on congestion costs raises the probability the firm is a foreign MNE, as opposed to being a UNE (p = 0.11 for the congestion costs). A greater importance placed on gaining reputational effects and access to specialised suppliers lowers the probability the firm is a foreign MNE. Size is strongly significant and positively associated with being a foreign MNE. Recruiting a high proportion of staff from the South East is significant and decreases the probability the firm is a foreign MNE. What stands out in the foreign MNE comparison is that the sub-sector dummies are all strongly significant and being in any sector other than banking decreases the probability the firm is a foreign MNE, whereas sub-sector is not a significant discriminator when comparing UNEs and domestic MNEs. This makes sense. The industrial composition of the UNEs and domestic MNEs will reflect the natural endowments and institutions of the home country. The strongest firms will become MNEs. There is a well know sub-sector bias in which firms become MNEs (Caves 1996) and this shows up more in the composition of the foreign MNEs and is driven by those sub-sectors which (a) are more predisposed to become MNEs and (b) which would find London an especially favourable location at the sub-national scale. This means the make-up of sub-sectors in the foreign MNE sample will be more specific than for the domestic firms. What the results show is that this sub-sector bias is overwhelmingly in banking.

Table 6 shows the average marginal effects of the variables on the probability that a firm will belong to a particular one of the three categories, UNE, domestic MNE or foreign MNE. Thus, belonging to insurance raises the probability that a firm is a UNE by 0.2166, raises the probability that a firm is a domestic MNE by 0.189 and lowers the probability that a firm is a foreign MNE by 0.4056. The sum of these marginal effects is 0, as the firm must belong to one of the three categories. The results are consistent with the two-way comparisons: The industrial composition of the foreign MNEs is significantly different to domestic firms, both UNEs and MNEs. As before, social capital and labour pooling are not significant. Local competition and congestion are negatively and significantly associated with being a UNE. There is no significant difference between the effect of these factors on being either a domestic or a foreign MNE, but, as will be shown below, these factors do have a significant positive effect on the probability of being an MNE when domestic and foreign are pooled. Separating the two simply dilutes the effect on the probability. Access to specialised suppliers makes it significantly more likely the firm is a UNE and the reputation factor is also positively and significantly associated with the probability of being a UNE.

As Table 7 shows, the Wald test of the admissibility of combining categories is not rejected for the categories of domestic and foreign MNEs, which supports our use of the bivariate logit comparing just MNEs as a single category with UNEs. The multinomial logit relies on the assumption that the errors in the underlying model determining which category the firm is most likely to fall into are independent. This is commonly known as the independence of irrelevant alternatives assumption, although we are not in the standard random utility framework in the current case and there is no behavioural assumption in question, as there would be in a choice-theoretic context. The Hausman test is satisfied in this case, with χ2(23) = 21.85, p = 0.530 for the omission of the domestic MNE category and χ2(23) = 20.08, p = 0.637 for the omission of the foreign MNE category.

5 Conclusion

This study has sought to compare the economies and diseconomies of clusters for MNEs and UNEs. We find that some are similarly valued by MNEs and UNEs, some are valued more by MNEs, and some are valued more by UNEs. The results test our hypotheses. Economies relating to social capital and labour market pooling are equally important to MNEs and UNEs. Economies relating to local competition and diseconomies relating to congestion costs are more important to MNEs than to UNEs. Economies relating to the reputational effects of locating in a world-leading cluster and access to specialised suppliers are more important to UNEs than to MNEs.

That MNEs and UNEs do not experience all cluster economies and diseconomies the same way indicates that general cluster participation theory needs augmentation to recognise that cluster incumbents benefit and suffer from cluster membership differently. This chimes with the increasingly influential Resource-Based View (RBV) of the firm which emphasises firm heterogeneity (Barney 1991; Teece et al. 1997; Wernerfelt 1984). From this perspective, we would expect different firms to value cluster economies and experience cluster diseconomies differently depending on how the economy or diseconomy enhances its resource strength, mitigates resource weakness, or is overcome by resource strength. Moreover, they will differ in their ability to take advantages of the cluster externalities which are available.

The results also support Dunning’s (1998) unease with the implicit conjecture on which so much IB research has been based. It seems that the principles underlying the locational decisions of firms within national boundaries are different to the principles underlying the locational decisions of firms across national boundaries. The fact that MNEs and UNEs do not experience all cluster economies and diseconomies the same way therefore suggests that existing IB theory needs augmentation and this study is a step towards that.

Our findings have managerial and policy implications. First, the City of London’s claim to be the world’s leading international financial centre is supported, as both MNEs and UNEs are reported to benefit similarly from cluster participation with respect to social capital and labour pooling. Furthermore, local competition is found to be important for MNEs, and reputation gained from participating in the cluster and access to specialised suppliers are found to be important for UNEs. These are compelling attractors that justify the high cost of a London location and contribute to the cluster’s global recognition as the home for expertise and innovation. Second, our findings show that MNEs are more sensitive to congestion costs even in one of the most developed and globalised cities—London. In our survey, congestion costs such as disadvantages in national and international transportation, poor infrastructure and problematic government regulation in London are more important to MNEs compared to UNEs. With the UK’s planned exit from the EU, getting the response right to meet these challenges is essential to maintain the global strength of the financial services cluster in the City of London. Policymakers and regulators should bring forward policies that promote greater investment in environmental quality, modern buildings, and digital as well as national and international transport infrastructure.

References

Al Ariss, A., Cascio, W. F., & Paauwe, J. (2014). Talent management: Current theories and future research directions. Journal of World Business, 49(2), 173–179.

Alcacer, J., & Zhao, M. (2012). Local R&D strategies and multilocation firms: The role of internal linkages. Management Science, 58(4), 734–753.

Allen, J., & Pryke, M. (1994). The production of service space. Environment and Planning D, 12(4), 453–475.

Amin, A., & Thrift, N. (1992). Neo-Marshallian nodes in global networks. International Journal of Urban and Regional Research, 16(4), 571–587.

Arita, T., & McCann, B. (2002). The spatial and hierarchical organization of Japanese and US multinational semiconductor firms. Journal of International Management, 8(1), 121–139.

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management, 17(1), 99–120.

Bartlett, C. A., & Ghoshal, S. (1989). Managing across borders: The transnational solution. Boston: Harvard Business School Press.

Beugelsdijk, S., McCann, P., & Mudambi, R. (2010). Introduction: Place, space and organization-economic geography and the multinational enterprise. Journal of Economic Geography, 10(4), 485–493.

Birkinshaw, J., & Hood, N. (1998). Multinational subsidiary evolution: Capability and charter change in foreign-owned subsidiary companies. Academy of Management Review, 23(4), 773–795.

Blunch, N. J. (2008). Introduction to structural equation modelling using SPSS and AMOS. London: Sage Publications.

Castells, M. (2000). The Rise of the network society. London: Wiley.

Cattell, R. B. (1966). The scree test for the number of factors. Multivariate Behavioral Research, 1(2), 245–276.

Caves, R. E. (1996). Multinational enterprise and economic analysis. Cambridge: Cambridge University Press.

Chang, S. J., van Witteloostuijn, A., & Eden, L. (2010). From the editors: Common method variance in international business research. Journal of International Business Studies, 41(2), 178–184.

Clark, G. L. (2002). London in the European financial services industry: Locational advantages and product complementarities. Journal of Economic Geography, 2(4), 433–454.

Coleman, W. (2014). Financial services, globalization and domestic policy change. London: Palgrave Macmillan.

Cook, G. A. S., Pandit, N. R., Beaverstock, J. V., Taylor, P. J., & Pain, K. (2007). The role of location in knowledge creation and diffusion: Evidence of centripetal and centrifugal forces in the City of London financial services agglomeration. Environment and Planning A, 39(6), 1325–1345.

Dunning, J. (1979). Toward an eclectic theory of international production: Some empirical tests. Journal of International Business Studies, 11(1), 9–31.

Dunning, J. H. (1998). multinational. Journal of International Business Studies, 29(1), 45–66.

Enright, M. J. (2000). Regional clusters and multinational enterprises. International Studies of Management & Organization, 30(2), 114–138.

EY (2016). Foreign direct investment in UK financial services industry at highest level since 2006. http://www.ey.com/uk/en/newsroom/news-releases/16-06-13—foreign-direct-investment-in-uk-financial-services-industry-at-highest-level-since-2006. Accessed 15 November 2017.

Field, A. P. (2009). Discovering statistics using SPSS. London: Sage Publications.

Friedmann, J. (1986). The world city hypothesis. Development and Change, 17(1), 69–83.

Giachetti, C., & Torrisi, S. (2017). Following or running away from the market leader? The influences of environmental uncertainty and market leadership. European Management Review. https://doi.org/10.1111/emre.12130.

Hall, P. (1966). The world cities. London: Weidenfeld and Nicolson.

Hendry, C., & Brown, J. (2006). Organizational networking in UK biotechnology clusters. British Journal of Management, 17(1), 55–73.

Hennart, J. (2009). Down with MNE-centric theories! Market entry and expansion as the building of MNE and local assets. Journal of International Business Studies, 40(9), 1432–1454.

Hervas-Oliver, J. (2015). How do multinational enterprises co-locate in industrial districts? An introduction to the integration of alternative explanations from international business and economic geography literatures. Journal of Regional Research, 32, 115–132.

Hotelling, H. (1929). Stability in competition. Economic Journal, 39(153), 41–57.

Hymer, S. (1976). The international operations of national firms. Cambridge: MIT Press.

Jenkins, M., & Tallman, S. (2010). The shifting geography of competitive advantage: Clusters, networks and firms. Journal of Economic Geography, 10(4), 599–618.

Kaiser, H. F. (1961). A note on Guttmanʼs lower bound for the number of common factors. British Journal of Psychology, 14(1), 1–2.

Kalnins, A., & Chung, W. (2004). Resource-seeking agglomeration: A study of market entry in the lodging industry. Strategic Management Journal, 25(7), 689–699.

Kim, J., & Mueller, C. E. (1978). Statistical. Beverly Hills: Sage Publications.

Knickerbocker, F. T. (1973). reaction. Cambridge: Harvard University Press.

Kynaston, D. (2001). The City of London: Volume IV: A club no more 1945–2000. London: Chatto & Windus.

Long, J. S., & Freese, J. (2006). Regression models for categorical dependent variables using Stata (3rd ed.). College Station: The Stata Press.

Manning, S., Ricart, J. E., Rique, M., & Lewin, A. Y. (2010). From blind spots to hotspots: How knowledge services clusters develop and attract foreign investment. Journal of International Management, 16(4), 369–382.

Mariotti, S., Piscitello, L., & Elia, S. (2010). Spatial agglomeration of multinational enterprises: The role of information externalities and knowledge spillovers. Journal of Economic Geography, 10(4), 519–538.

Marshall, A. (1890). Principles of economics. London: Macmillan.

McCann, P., Arita, T., & Gordon, I. (2002). transactions. International Business Review, 11(6), 647–663.

McCann, B., & Folta, T. (2009). Demand- and supply-side agglomerations: Distinguishing between fundamentally different manifestations of geographic concentration. Journal of Management Studies, 46(3), 362–392.

Menghinello, S., Propris, L., & Driffield, N. (2010). Industrial districts, inward foreign investment and regional development. Journal of Economic Geography, 10(4), 539–558.

Mudambi, R. (2008). Location, control and innovation in knowledge-intensive industries. Journal of Economic Geography, 8(5), 699–725.

Nachum, L. (2003). Liability of foreignness in global competition? Financial service affiliates in the city of London. Strategic Management Journal, 24(12), 1187–1208.

Nachum, L., & Keeble, D. (2003). MNE linkages and localised clusters: Foreign and indigenous firms in the media cluster of Central London. Journal of International Management, 9(2), 171–192.

Narula, R. (2018). Multinational firms and the extractive sectors in the 21st century: Can they drive development? Journal of World Business, 53(1), 85–91.

Pandit, N. R., Cook, G. A. S., & Swann, G. M. P. (2002). A comparison of clustering dynamics in the British broadcasting and financial services industries. International Journal of the Economics of Business, 9(2), 195–224.

Porter, M. E. (1990). The competitive advantage of nations. New York: Free Press.

Porter, M. E. (1998). Clusters and the new economics of competition. Harvard Business Review, 76(6), 77–90.

Rosenzweig, P., & Singh, J. (1991). Organizational environments and the multinational enterprise. Academy of Management Review, 16(2), 340–361.

Rugman, A. M., & Verbeke, A. (2001). Subsidiary-specific advantages in multinational enterprises. Strategic Management Journal, 22(3), 237–250.

Rugman, A. M., Verbeke, A., & Nguyen, Q. (2011). Fifty years of international business theory and beyond. Management International Review, 51(6), 755–786.

Sassen, S. (1991). The global city: New York, London, Tokyo. Princeton: Princeton University Press.

Sethi, D., Guisinger, S., Phelan, S., & Berg, D. (2003). Trends in foreign direct investment flows: A theoretical and empirical analysis. Journal of International Business Studies, 34(4), 315–326.

Stevens, J. P. (2002). Applied multivariate statistics for the social sciences. Hillside: Erlbaum.

Swann, G. M. P. (2009). The economics of innovation: An introduction. Cheltenham: Edward Elgar.

Swann, G. M. P., & Prevezer, M. (1996). A comparison of the dynamics of industrial clustering in computing and biotechnology. Research Policy, 25(7), 1139–1157.

Swann, G. M. P., Prevezer, M., & Stout, D. (1998). The dynamics of industrial clustering: International comparisons in computing and biotechnology. Oxford: Oxford University Press.

Tatoglu, E., Glaister, A. J., & Demirbag, M. (2016). Talent management motives and practices in an emerging market: A comparison between MNEs and local firms. Journal of World Business, 51(2), 278–293.

Taylor, P., Beaverstock, J., Cook, G., & Pandit, N. (2003). Financial services clustering and its significance for London. London: Corporation of London.

Teece, D. J., Pisano, G., & Shuen, A. (1997). Dynamic capabilities and strategic management. Strategic Management Journal, 18(7), 509–533.

The City UK (2016). Key facts about UK financial and related professional services. London: The City UK.

Treasury, H. M. (2003). The location of financial activity and the euro. London: HM Treasury.

Vidaver-Cohen, D., Gomez, C., & Colwell, S. R. (2015). Country-of-origin effects and corporate reputation in multinational firms: Exploratory research in Latin America. Corporate Reputation Review, 18(3), 131–155.

Von Hippel, E. (1988). The sources of innovation. New York: Oxford University Press.

Wernerfelt, B. (1984). A resource-based view of the firm. Strategic Management Journal, 5(2), 171–180.

Zaheer, S. (1995). Overcoming the liability of foreignness. Academy of Management Journal, 38(2), 341–363.

Zaheer, S., & Mosakowski, E. (1997). The dynamics of the liability of foreignness: A global study of survival in financial services. Strategic Management Journal, 18(6), 439–463.

Acknowledgements

The authors thank the reviewers for their considerable input in shaping the final version of this paper. They are of course not responsible for any remaining errors.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Pandit, N.R., Cook, G.A.S., Wan, F. et al. The Economies and Diseconomies of Industrial Clustering: Multinational Enterprises versus Uninational Enterprises. Manag Int Rev 58, 935–967 (2018). https://doi.org/10.1007/s11575-018-0363-1

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11575-018-0363-1