Abstract

Regulators conduct regulatory impact analyses (RIA) to evaluate whether regulatory actions fulfill the desired goals. Although there are different frameworks for conducting RIA, they are only applicable to regulations whose impact can be measured with structured data. Yet, a significant and increasing number of regulations require firms to comply by specifying and communicating textual data to consumers and supervisors. Therefore, we develop a methodological framework for RIA in case of unstructured data following the design science research paradigm. The framework enables the application of textual analysis and natural language processing to assess the impact of regulatory actions that result in unstructured data and offers guidance on how to map suitable methods to the dimensions impacted by the regulation. We evaluate the framework by applying it to the European financial market regulation MiFID II, specifically the recent regulatory changes regarding best execution. Thereby, we show that MiFID II failed to improve informativeness and comprehensibility of best execution policies.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Regulation of the financial industry and of financial markets is a fundamental tool of governments and policy makers to ensure customer and investor protection as well as market efficiency and market integrity. In order for these tools to be effective and to achieve high regulatory quality, it is critical to ensure that regulatory adjustments and new regulations in the financial industry actually meet their desired objectives and result in the intended changes. The growing pace of technological progress and the increasing interdependencies between different financial regulations pose substantial challenges to policy makers and regulatory quality since the exact effects of a regulation are hard to assess. Therefore, analyzing the impact of regulatory actions is a crucial step for evidence-based policy making.

For this purpose, policy makers and regulators around the globe conduct regulatory impact analysis (RIA) to evaluate whether regulatory actions meet the desired goals. Although there exist different guidelines and frameworks for conducting RIA (e.g., OECD 1997; Radaelli 2004), they are only applicable to regulations whose impact can be measured with structured and quantifiable data. Yet, an increasing and significant number of regulatory actions aim at or result in vast amounts of documents representing textual data that is hard to evaluate manually. In the financial industry, regulatory actions aimed at unstructured data mainly result from increasing disclosure requirements such as additional prospectus requirements for mutual funds in the US (U.S. Securities and Exchange Commission 2009) or new requirements for key information documents for retail investment products in the European Union (European Parliament and Council 2014b).

Regulators become increasingly aware that they need process guidelines and information technology (IT) based solutions to deal with and analyze the masses of reports and textual data. Such innovative IT-solutions are also known under the term RegTech, and are already used by firms to manage their regulatory requirements, e.g., by automating regulatory reporting (Butler and O’Brien 2019). However, RegTech and RegTech literature comes short concerning the supply of appropriate IT-enabled solutions and methodologies for regulators. Yet, such solutions are necessary to assess the impact and effectiveness of regulations that result in massive amounts of unstructured data. They can also serve to assess the compliance of firms to those regulations. Systems and methodologies are needed to appropriately monitor and analyze regulatory documents that firms have to deliver. The analysis of these documents enables regulators to assess the effectiveness of their efforts to ensure economic stability, fair competition, and market integrity (Arner et al. 2017).

To enable researchers and regulators to assess the impact of regulatory actions aimed at unstructured data and to improve future evidence-based policy making with the help of regulatory intelligence and RegTech-solutions, this paper develops a methodological framework for RIA in case of unstructured data (also referred to as RIA-framework hereafter), which builds on methods from textual analysis (TA) and natural language processing (NLP)Footnote 1 (e.g., Loughran and McDonald 2016). Those methods as well as improvements in data processing and aggregation help to make unstructured data quantifiable and, thus, provide the methodological foundation for our framework.

For the development of the RIA-framework, we follow the design science research paradigm, which aims to create methods, tools, and other artificial objects that meet pre-defined goals and provide utility to their users (Simon 1996). Specifically, we adhere to the guidelines for design science research by Hevner et al. (2004) and follow the methodology by Peffers et al. (2007), which builds on these guidelines. The RIA-framework provides an innovative and effective solution for an important practical problem, which are the crucial characteristics of a design science artifact to be a relevant contribution (Geerts 2011; Hevner et al. 2004). The RIA-framework details the necessary steps for the application of TA and NLP to assess both (i) the achievement of regulatory objectives and (ii) compliance of firms with the regulation in case firms have to comply by setting up textual data. It also offers clear guidance on how to map suitable TA and NLP methods to the dimensions impacted by the regulation.

Following Peffers et al. (2007), we evaluate the RIA-framework based on a demonstration of its applicability in a use case of a recent financial market regulation where investment firms, i.e., banks and brokers, have to generate huge amounts of unstructured textual data. Specifically, we use the RIA-framework to assess the impact of the recently enforced changes in best execution requirements of the Markets in Financial Instruments Directive II (MiFID II) in Europe (European Parliament and Council 2014a) that has to be applied since January 2018. These rule changes demand investment firms to provide more informative best execution policies, which also should be easier to understand. In best execution policies, investment firms have to describe their processes of order handling and routing to achieve the best possible order execution for their clients. Thus, these policies should enhance transparency for investors and protect them from potential downsides of the stock market fragmentation in Europe.

The use case confirms that our RIA-framework serves to effectively evaluate the impact of a financial market regulation resulting in unstructured data. Moreover, it shows that the analyzed best execution requirements in MiFID II did not achieve the desired goals. By comparing textual similarity, specificity, and boilerplate information of policies from German institutions before and after MiFID II, we find that the informational value of these policies actually decreased rather than increased as intended by the regulation. Also, we find that these policies became harder to read and are more difficult to understand after the regulatory change. Based on a second and broader sample of European best execution policies, we apply the benchmarking approach proposed in the developed framework and compare the readability of European best execution policies with texts from different contexts and with varying levels of readability (e.g., European legislative documents, companies’ annual financial statements, Wikipedia articles, spoken language). The analysis shows that—although intended to be understood by retail investors—best execution policies are among the most difficult and complex documents and that they are as hard to read as companies’ annual financial statements or legislative documents. Consequently, the analysis of the new regulatory requirements on best execution policies in MiFID II shows that they did not reach the desired goals of increased investor protection and competition between brokers by providing more informative and easily understandable best execution policies.

Although the RIA-framework is developed against the background of the financial industry and demonstrated based on a use case from financial regulation, it can be applied to regulatory initiatives of other economic sectors as no step of the framework is unique to the financial industry. Rather, the RIA-framework represents a general principle to solve a class of real-world problems, i.e., conducting RIA in case of unstructured data.

This paper contributes to the literature streams of RegTech and RIA by equipping regulators and researchers with a new framework for conducting RIA in case of unstructured data based on methods from the fields of TA and NLP. The RIA-framework provides the necessary process steps, decisions, and data requirements, as well as the suitable methodologies to assess the impact of a regulation aimed at or resulting in unstructured data in an organized, largely automated, and objective manner. This research is one of the first studies that aims at using information systems (IS) research methodologies to support regulators to achieve their goal of assessing the effectiveness of regulations and to increase regulatory intelligence based on IT. It extends prevailing RegTech literature that, up to now, mainly focuses on RegTech for compliance by firms and for supervision by authorities (e.g., Butler and O’Brien 2019; Arner et al. 2016). Thereby, this paper also helps to close the gap between the relatively high usage of RegTech in the private sector and the still relatively low adoption of RegTech by regulators themselves (Arner et al. 2017).

The paper is organized as follows: Sect. 2 discusses literature regarding RegTech, outlines the research gap concerning RegTech for regulators and law-makers, and discusses the concept of RIA. Against this background and based on existing guidelines for RIA and methods from TA and NLP, we develop the framework for RIA in case of unstructured data in Sect. 3. Section 4 demonstrates the usability of our RIA-framework by applying it to assess the impact of regulatory changes for European best execution policies. Sect. 5 evaluates the proposed RIA-framework. We discuss our RIA-framework and findings in Sect. 6 and conclude in Sect. 7.

2 Literature review on RegTech and RIA

The RIA-framework contributes to the literature stream RegTech. Therefore, this section provides a short overview of relevant studies related to RegTech and outlines the lack of research on RegTech solutions supporting regulators and policy makers to improve regulatory intelligence. As a basis for the framework development, this section also discusses the concept of RIA, existing guidelines for RIA, and related research.

2.1 Regulatory technology

Regulatory Technology or RegTech refers to IT deployed in the context of regulatory compliance, reporting, and supervision. RegTech helps firms to manage their regulatory obligations (Butler and O’Brien 2019) and supports supervisory authorities by enabling them to effectively monitor whether the economic activities of firms are compliant (Arner et al. 2017; Williams 2013).

RegTech supports firms to set up compliant business systems, to control risks, and to perform or automate regulatory reporting (Butler and O’Brien 2019). This advancement in IT adoption is strongly connected to the general technological change in the industry (Arner et al. 2017). Specifically for compliance management, the literature proposes many different use cases based on IT: For instance, Gozman et al. (2020) explore the potential of applying blockchain technology for regulatory reporting of mortgages or Moyano and Ross (2017) propose a new approach for the know-your-customer (KYC) due diligence process.

Besides helping firms to be compliant, RegTech and related research also support supervisory institutions. Thereby, RegTech enables supervisors to conduct more granular and effective supervision (Arner et al. 2016). This especially holds for financial markets, where supervisors have successfully used IT to monitor and analyze markets and market participants preventing insider trading, market manipulations, and fraud (Arner et al. 2016; Williams 2013; Siering et al. 2017). Furthermore, the literature proposes several applications of advanced methodologies such as predictive analytics and machine learning for supervisory institutions in the context of corporate fraud (Dong et al. 2018), credit card fraud (Bhattacharyya et al. 2011), accounting fraud (Kirkos et al. 2007; Glancy and Yadav 2011; Humpherys et al. 2011), and financial misconduct (Lausen et al. 2020).

However, while RegTech is quite advanced in supporting the compliance of firms and the respective investigations by supervisors, literature comes short concerning the supply of appropriate IT systems and methodologies for regulators, who need to assess and review whether their regulatory actions actually fulfill the desired goals. While there is a call for increasing the efforts regarding the evaluation of regulations’ effectiveness by conducting RIA (Gai et al. 2019), regulators become increasingly aware that they need appropriate process guidelines and IT-solutions to automate the assessment of the masses of data provided in response to the reporting and disclosure requirements of firms (Arner et al. 2016, 2017). Thereby, IT and RegTech may unleash significant benefits for regulators to improve regulatory intelligence and to achieve their goal of facilitating a safe and resilient economic system based on RIA and evidence-based policy making.

2.2 Regulatory impact analysis

The primary goal of RIA is the optimization of policy making by ensuring that benefits to society from regulatory actions are maximized while costs, i.e., potential negative consequences, are minimized (OECD 1997). The (OECD 1997, p. 7) defines RIA as an approach for “systematically assessing the negative and positive impacts of proposed and existing regulations”. All OECD member states (38 countries as of 2022) as well as the European Commission have adopted some form of RIA for their legislative processes, both concerning primary laws and subordinate regulations, to increase regulatory quality (OECD 2018). In particular, ex-post RIA improves the monitoring of existing regulations and builds the basis for potential revisions or even complete cancellations of a regulation depending on the actual regulatory impact (Kirkpatrick and Parker 2004). Therefore, RIA is an analytical and systematic research and policy tool to assist decision makers in evidence-based policy making (OECD 2008).

Academic literature analyzes the impact of policy decisions based on RIA in various domains, however, it mostly aims at regulation that can be assessed by structured and quantifiable data (Radaelli 2004). The limitation to structured data also holds for existing frameworks for RIA such as the general guidelines for systematic impact assessment for OECD member states (OECD 1995), the more specific framework of the European Commission (2005), and the various improvements of OECD frameworks and guidelines (OECD 2008, 2018, 2020). These improved as well as newly developed guidelines and frameworks entirely consider the assessment of regulatory actions based on the analysis of structured and quantifiable data. Yet, research and existing frameworks come short in providing solutions for analyzing the regulatory impact of policies that aim at or result in unstructured data. However, as more and more policies target the creation and provision of unstructured data such as firms’ disclosure requirements to customers or supervisors, the assessment of such regulations becomes increasingly relevant so that regulators and researchers need to be equipped with the necessary tools and frameworks. Data science methods like TA and NLP (e.g., different sentiment (Salton and Buckley 1988; Pierrehumbert 2001) and readability measures (Gunning 1969; Tan et al. 2002)) as well as improvements in data processing and aggregation (e.g., information content (Blei et al. 2003) and textual similarity (Jiang and Conrath 1997; Bag et al. 2019; Lau and Baldwin 2016) analyses) can help to make unstructured data quantifiable and, thus, serve as methodological foundation for RIA in case of unstructured data. Al-Ubaydli and McLaughlin (2017) provide first steps in this direction by developing a measure to quantify regulatory demands in published documents based on methods from TA. We go further and develop and evaluate a framework for RIA using IS research methods.

3 A framework for analyzing regulatory impact based on unstructured data

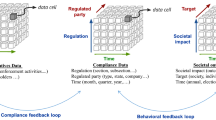

Following the design science research paradigm, we develop a framework for the analysis and evaluation of regulatory actions that result in unstructured data such as text documents. To create the artifact, we build on existing RIA guidelines and on methods from TA and NLP. The RIA-framework provides detailed guidance and the required steps and tools to analyze the impact of a regulation targeting at or leading to unstructured data in a systematic and largely automated manner. Figure 1 presents the proposed framework and the six steps that are necessary for RIA in case of unstructured data.

3.1 Step 1: problem and goal identification

The first step of the regulatory impact analysis is the identification of the economic, social, or environmental problems initiating a regulatory action to put the goals of the new regulations or regulatory adjustments into perspective and to enable their precise evaluation. To receive a profound knowledge base of the issue at stake, it is crucial to identify the key aspects of the problem, reduce conceptual uncertainty, and estimate the potential impact of the problem (European Commission 2005). Once the problem is precisely described, the reasons leading to the problem and its magnitude have to be examined by also taking into account the different entities being affected and their connections to the problem (OECD 2008). This critical in-depth-analysis of the problem addressed by the regulatory action should be based on political statements at the origin of a policy initiative, legal discussions, and academic studies. If the problem is identified and defined well, a sound understanding shall exist regarding the problem itself as well as regarding the reasons requiring regulatory actions to correct the identified problem (OECD 1997), which provides the foundation for a clear identification of the actual objectives of the regulatory action (OECD 2020).

RIA framework in case of unstructured data

A clear identification and formal definition of the regulatory objectives is essential in order to assess the accomplishments of regulatory actions since they are evaluated according to the initial goals of a regulation in light of the identified problem. Valuable information for the identification and description of regulatory objectives can often be directly derived from legal documents themselves. For instance, legislative documents in the European Union provide the reasons for the provisions at the start of every regulatory act in so-called recitals. Furthermore, other related legal documents such as regulatory consultations can be used to identify the objectives of a regulation. A detailed and explicit description of the regulatory objectives builds the basis for the evaluation of a regulatory action to verify whether it actually achieved its goals and objectives (European Commission 2005).

Step 1

Clearly describe the problem that the regulatory action wants to solve and identify the intended goals of the regulation.

3.2 Step 2: identification of affected dimensions

After the identification of the regulatory objectives, the specific dimensions that are affected by the regulatory action need to be determined. Dimensions in this context refer to the means (e.g., informativeness or objectivity) that are targeted by the regulation in order to achieve the identified regulatory goal. They refer to objects (e.g., regulatory disclosures) and subjects (e.g., companies). Thereby, it is crucial to derive the full set of affected dimensions taking into account all stakeholders (European Commission 2005) and to identify all relevant direct as well as indirect dimensions affected by the regulatory change (OECD 2020). The specific dimensions, objects, and subjects targeted by the regulatory action and the explanation of the corresponding operational changes can be extracted from the respective regulatory text, from related legal opinions, comments, and corresponding guidelines. Taking into account the perspective of different stakeholders and how they are affected by a regulation can support the identification of relevant dimensions (European Commission 2005). The identification of the targeted dimensions by a regulatory action is a crucial step in the RIA process since they build the basis according to which the impact of a regulation and thus its success or failure is evaluated.

Step 2

Identify the specific dimensions that are affected by the regulatory action.

3.3 Step 3: data acquisition

The third step of the RIA-framework outlines the data acquisition process and specifies the necessary data to assess the regulatory actions based on the derived dimensions determined in Step 2. To acquire an extensive data set for the assessment of regulatory impact, it is important to involve all relevant data holders and potential sources of unbiased data to guarantee that the RIA is conducted based on the most complete set of information (OECD 2020). The analysis and data acquisition approach for RIA in case of unstructured data differs dependent on whether a regulatory change or a new regulation is to be analyzed.

In case of the revision of an already existing regulation, the affected objects before as well as after the introduction of the regulatory change have to be collected. The inclusion of data from the pre-regulatory environment is important and necessary to establish a baseline and reference against which potential changes are evaluated to ensure a sound assessment of the regulatory impact (OECD 2004). The collection of the affected objects before and after the regulatory action enables the assessment of the regulatory impact based on a pre-post analysis design. Thus, the impact and effects of the regulatory change can directly be derived from the changes in the dimensions targeted by the regulatory change. If possible, a control group should be used to exclude unobserved effects that might change over time independent of the regulatory change. An appropriate control group should not be affected by the regulatory action, however, jurisdictions should still be comparable.

In case of the introduction of a new regulation, the collection of any data before the regulatory change is mostly impossible for regulatory actions aimed at unstructured data since they often require firms to publish new textual documents which did not exist before. However, suitable references are necessary to assess the impact of new regulations aimed at unstructured data. Therefore, we propose a benchmark approach to assess the impact of such new regulations. To collect appropriate benchmarks (e.g., textual data generated in comparable regulatory areas), it is important to ensure comparability between affected objects and chosen benchmarks. The benchmarks should be selected considering the identified objectives and dimensions in Step 1 and Step 2. Furthermore, the background and area of the benchmarks should be matched to the affected objects as well as to the specific dimensions. Several benchmarks should be included in the data set to cover a wide range of different but comparable documents and to ensure an extensive analysis of the impacted aspects. In addition, each benchmark should contain sufficient data providing enough information to compare it with the objects targeted by the regulation.

Step 3

Acquire the necessary data for RIA dependent on whether a change in regulation (pre-post data set) or a new regulation (benchmark data set) is analyzed.

3.4 Step 4: map research method(s) to affected dimensions

In the fourth step, the affected dimensions identified in Step 2 need to be mapped with appropriate scientific research method(s) from TA and NLP that meet the requirements needed to examine the specific regulatory action.

The mapping of TA and NLP methodologies to affected regulatory dimensions is a major component for an effective RIA in case of unstructured data and needs to be adapted for each specific use case. However, the schematic sequence of the mapping process is similar. Starting with the mapping process, it is important to identify relevant methodologies suitable for the TA of the dimensions identified in Step 2. TA covers a wide range of different methodologies enabling the extraction of various information from textual data (Lacity and Janson 1994) and a variety of methods have been used in many different research areas. Focusing on techniques enabling an effective assessment of regulatory impact in case of unstructured data, we provide a set of common TA and NLP methodologies. Table 1 presents an overview of these methodologies for RIA in case of unstructured data. This collection of potential methodologies provides a guidance for RIA application, but can be extended with additional methodologies as necessary for the specific use case.

We group the TA and NLP methodologies in Table 1 into the categories Readability, Complexity, Sentiment & Targeted Phrases, Textual Similarity, Numerical Conversion of Documents, and Information Content & Topic Modeling: First, the category Readability summarizes methodologies that can be used to measure textual difficulty and the required ability of a reader to understand the content of documents. Second, the category Complexity contains measures that reflect the complexity and diversity of language in a text. Third, the category Sentiment & Targeted Phrases represents methodologies targeting certain words or phrases through word lists or dictionaries, which can be connected to specific contexts or common sentiments. Fourth, the category Textual Similarity includes methodologies providing insights on the similarity/distance of terms and documents. Fifth, the category Numerical Conversion of Documents describes methods to convert a text to a numerical representation, which is a crucial step especially for the analysis of topics and textual similarity. And last, the category Information Content & Topic Modeling contains methodologies allowing the identification and extraction of topics within a collection of documents. For further methodological overviews in specific contexts, we refer to the literature (Aggarwal and Zhai 2012; Reshamwala et al. 2013; Loughran and McDonald 2016; Kang et al. 2020).

Once suitable TA methods are extracted from scientific research, it is important to select the appropriate measures for the regulatory assessment and to ensure that the selected methods actually measure the impact on the affected dimensions. Based on the overview of TA and NLP methodologies for RIA in case of unstructured data, we provide a first mapping of TA methods to corresponding regulatory dimensions in Table 2. While these mapped research methods already cover many potential regulatory dimensions, the application of the research methods still needs to be checked for each regulatory action individually and the mapping as well as the methodologies can be further extended based on the required needs of specific use cases. We propose to trigger an academic debate on further suitable mappings as a future research step. Within the RIA-framework, the assignment of TA techniques to specific regulatory dimensions provides the methodological basis for the evaluation of textual data and enables the assessment of regulatory actions concerning specific affected objects.

Step 4

Select appropriate TA and NLP methods and map them to the dimensions affected by the regulation.

3.5 Step 5: analyze and evaluate the impact of the regulatory change

This step of the RIA-framework comprises the actual analysis and evaluation of the regulation’s impact. Depending on the structure of the respective data (e.g., simple text files, documents in PDF format, textual information from web pages, XML, JSON), several preprocessing steps need to be performed to make the data machine-readable. Thereby, relevant textual information needs to be extracted and the handling of textual information from figures, tables, and lists needs to be determined. In addition, and depending on the methodology used for the analysis, further text cleaning steps such as removing stopwords and numerical characters or stemming need to be performed. Because preprocessing depends strongly on the data, goal, and methodology of the analysis, we do not provide a technical overview of different preprocessing techniques but refer to the literature (e.g., Kannan et al. 2014; Vijayarani et al. 2015; Kathuria et al. 2021).

Once preprocessing is completed, the assessment of the regulatory action can be started. At first, the TA and NLP methods determined and mapped to the affected regulatory dimensions in Step 4 are applied. In case the goal of the RIA is to assess a change in regulation, pre-post analysis is conducted and textual data affected by the regulatory change is analyzed using the selected methods on samples both before and after the regulatory change went into force. In case the analysis is conducted to evaluate the regulatory impact of a new regulation, benchmark analysis is performed and textual data resulting from the regulation is compared to suitable benchmarks using the selected TA and NLP methods.

Once these analyses are conducted, the results need to be compared, e.g., by using data visualization and statistical tests. In doing so, researchers and regulators should evaluate whether changes in the analyzed measures can be observed and whether these changes correspond to the regulatory objectives (defined in Step 1). Moreover, they should evaluate whether any undesired effects can be detected. The evaluation of the results should indicate whether the regulator has achieved the objectives of the regulatory action and whether further regulatory requirements might be necessary if the objectives are not met.

Step 5

Conduct necessary data preprocessing steps and analyze the regulatory impact based on the obtained data and the selected TA and NLP methods.

3.6 Step 6: communication to stakeholders

The final step of the framework represents the communication of the results of the RIA to relevant stakeholders, e.g., policy makers, regulators, reporting standards providers, industry and consumer protection associations, and the scientific community, by publishing a policy white paper or a research report. The report should briefly address each step of the framework, describe the TA and NLP methods used to analyze the impact of the regulation, summarize the key findings of the analysis, and elaborate on whether the regulation achieved the desired goals. Moreover, the results of the RIA can be used to discuss potential improvements of the analyzed regulation and the report can elaborate on potential further regulatory actions. The steps of our RIA-framework can be used to structure the report.

Step 6

Communicate the results of the RIA to relevant stakeholders.

4 Framework application: assessment of the change in best execution requirements in MiFID II

To demonstrate its applicability, we make use of the RIA-framework and perform an ex-post regulatory impact analysis of the best execution requirements outlined in MiFID II (European Parliament and Council 2014a). According to Peffers et al. (2007), demonstrating the applicability of an artifact is an important step in design science research to evaluate how well the developed artifact provides a solution to the problem.

4.1 Problem and goal identification (Step 1)

With more than 300 trading venues as of September 2022,Footnote 2 the European securities market is highly fragmented. Consequently, there is a large choice of venues to which an order to buy or sell a stock or other financial instruments could be sent to. The selection of the appropriate trading venue to execute a specific order is one of the key tasks of investment firms to obtain the best possible result for their clients taking into account a range of factors such as price, costs, speed, likelihood of execution (“best execution”). Already in MiFID I that went live in November 2007, the European regulator defined principles for investment firms concerning best execution and required investment firms to publish so-called best execution policies,Footnote 3 which describe their processes to achieve best execution (European Parliament and Council 2014a). The best execution regime allows investment firms to implement individual approaches and strategies (execution arrangements) to achieve best execution in compliance with the statutory minimum requirements (Gomber et al. 2012). These execution arrangements are summarized in best execution policies. Yet, the actual implementation of execution policies revealed significant shortcomings since most policies are limited to minimum information, do not comprehensively describe the whole best execution process, and, most importantly, are difficult to understand (Gomber et al. 2012, MiFID II, Recital 97). With MiFID II, that went live in January 2018, European authorities intended to address these shortcomings. One crucial amendment of this revision is that execution policies are required to become more informative and comprehensible in order to provide value to clients (European Parliament and Council 2014a).

Specifically, MiFID II Recital 97 states that “In order to enhance investor protection it is appropriate to specify the principles concerning the information given by investment firms to their clients on the execution policy [...]”. To achieve this goal, MiFID II Art. 27(5) includes a new paragraph requiring investment firms to specify their execution policies so that the provided “information shall explain clearly, in sufficient detail and in a way that can be easily understood by clients, how orders will be executed by the investment firm for the client” (European Parliament and Council 2014a).Footnote 4 Consequently, the primary desired goal of the regulatory change is to foster investor protection by increasing the informational value and ease of understanding of best execution requirements for clients. Moreover, the regulatory change also aims at increasing the competitive aspect of best execution policies (Committee of European Securities Regulators 2007; Laruelle and Lehalle 2018). Because the new requirements for best execution policies should provide investors a better understanding of how banks and brokers handle their orders, the policies can serve investors as a basis to select the investment firm that best suits their needs and preferences. In summary, the analyzed regulatory change in MiFID II aims to solve the problem of best execution policies being not informative and difficult to understand in order to achieve the desired goals of investor protection and competition between brokers.

4.2 Identification of affected dimensions (Step 2)

The crucial amendment with respect to best execution policies in MiFID II is that they are required to become more informative and comprehensible in order to reach the desired goals, i.e., strengthen investor protection and foster competition between brokers.Footnote 5 Consequently, two dimensions need to be analyzed in order to assess the impact of changed best execution requirements:

-

Informativeness of execution policies (Dimension 1): Derived from the legal text, which states that execution policies need to “explain clearly, in sufficient detail” (MiFID II Art. 27(5)) how the broker handles clients’ orders to achieve best execution.

-

Comprehensibility of execution policies (Dimension 2): Again derived from the legal text, which says that the policies should be “easily understood by clients” (MiFID II Art. 27(5)).

4.3 Data acquisition (Step 3)

According to the RIA-framework, data acquisition depends on whether a new regulation or whether a change in regulation has to be analyzed. Because the amendments to best execution requirements in MiFID II represent a change in regulation, we need to obtain data on the affected dimensions both before as well as after the regulatory change (see Case 1 below). Nevertheless, and as the benchmark approach is a major contribution of the paper, we also evaluate the impact of MiFID II on best execution policies as if it was a new regulation (see Case 2 below). Moreover, this alternative approach can also be used in case data before the regulatory change cannot be obtained, which, however, should regularly not be the case since regulators as the main potential users of the framework can request the necessary documents from the regulated entities (here: investment firms).

Case 1: change in regulation (MiFID I to MiFID II)

Because the amendments to best execution requirements in MiFID II represent a change in regulation, we need to obtain data on the affected dimensions both before and after the regulatory change. Consequently, best execution policies of banks and brokers before as well as after the application of MiFID II need to be obtained. Specifically, we build upon the execution policy examination of Gomber et al. (2012)Footnote 6 analyzing 75 execution policies of the largest German financial institutions and online brokers written in German from 2009. These policies are then matched with the corresponding firm’s execution policies post-MiFID II from 2020. Mergers and acquisitions as well as insolvencies within the time from 2009 to 2020 reduce the sample of the analysis to 50 firms. Thus, the final data set includes a total of 100 execution policies aimed at retail clients (50 from 2009 and 50 from 2020).Footnote 7

Case 2: MiFID II as new regulation

For this second part of the analysis, we collect execution policies from trading members (i.e., banks and brokers) of the largest European stock exchanges.Footnote 8 The execution policies valid as of May 2020 are downloaded from the investment firms’ websites provided that an English version is available to ensure comparability across the different countries. Because MiFID II requires banks and brokers to account for the different characteristics and needs of retail and professional investors (MiFID II Art. 27(9a)), we follow this differentiation and sort the policies in these two groups, i.e., retail and professional clients. This results in a total of 124 execution policies addressing retail investors and 167 execution policies applying to professional investors.Footnote 9

For the benchmark analysis, we choose five different benchmarks from different contexts with varying textual complexity to be able to evaluate the readability and complexity of best execution policies against these benchmarks. Specifically, we (i) use the textual content of the Management Discussion and Analysis (MD&A) section of US Form 10-K filings. 10-K filings represent a standardized form of listed US companies’ annual reports regulated by the Securities and Exchange Commission (SEC). The MD&A section has widely been used in the finance and accounting literature (e.g., Lundholm et al. 2014; Loughran and McDonald 2016). In our context, using 10-K filings is particularly interesting because similar to best execution policies, they represent reporting obligations of companies. We choose a random sample of 10-K filings for the year 2019 of 100 constituents of the S&P 500. Furthermore, we (ii) use the textual content of EU regulatory documents. Regulatory documents not only contain the rules for companies, especially regarding their reporting obligations, but also serve a as benchmark for high complexity texts due to their legal language and conditional statements. The textual content of regulations has been analyzed in various academic studies (e.g., Bommarito and Katz 2010; Katz and Bommarito 2014 for the United States Code). We concentrate on the key EU financial services legislation in the context of financial markets and market infrastructures (European Parliament 2020) and separate the text according to the chapters of the respective documents.Footnote 10 In addition, we follow Hassan et al. (2019) and (iii) include readability and complexity measures of spoken language based on the Santa Barbara Corpus of Spoken American English from Du Bois et al. (2000). We further follow Hassan et al. (2019) and (iv) use chapters of a standard financial accounting textbook (Libby et al. 2004) to cover general financial terms and financial jargon. And last, for general language we (v) use a random sample of 1000 Wikipedia articles.

4.4 Map research methods to affected dimensions (Step 4)

Mapping research methods from the fields of TA and NLP to the affected dimensions (identified in Step 2 of the framework) is one of the central steps in the assessment of regulatory actions aimed at or resulting in unstructured data. The first dimension to be analyzed is the impact of the regulation on the informativeness of best execution policies. In order to assess the informational content of the policies, we rely on three different measures: textual similarity, the percentage of boilerplate information, and specificity. Textual similarity analysis is an appropriate method which has already been applied in other studies analyzing the informational content and the amount of new information in documents (Hoberg and Phillips 2016; Kelly et al. 2018). If the policies only copy the legal text or copy from each other, the policies do not provide informational value to investors. The similarity analysis can reveal such a relation. To measure textual similarity, we follow Hanley and Hoberg (2010) as well as Cohen et al. (2020) and compute the cosine similarity of two documents based on the frequency of terms within each document. When counting the terms in each document, we use stemmingFootnote 11 and adjust the term frequencies by the inverse document frequencies to give more weight to terms that occur less often, i.e., we apply the term frequency-inverse document frequency (tf-idf) approach to compute cosine similarities. Since this word weight approach does not account for the structure of a sentence, we also calculate the cosine similarity based on the doc2vec model developed by Le and Mikolov (2014), which accounts for semantics and was already applied to the financial context by Reichmann et al. (2022).Footnote 12,Footnote 13 The use of similarity analysis as a measure of informativeness is further justified by the regulator’s intention to foster competition between brokers based on their execution policies (Committee of European Securities Regulators 2007; Laruelle and Lehalle 2018). Again, if policies are meant to provide a meaningful basis for broker selection to clients, the policies should contain the specific differences between the brokers and, hence, need to be heterogeneous. To account for the drivers of similarity and to measure informativeness based on the standardization of best execution policies (whereas highly standardized policies would account as less informative), we compute a boilerplate measure following Dyer et al. (2017) and Lang and Stice-Lawrence (2015). Boilerplate information is defined as standard text that is prevalent in many documents and thus is unlikely to be informative. Specifically, we measure boilerplate information by counting all tetragrams, i.e., groups of four words within a single sentence, for each policy. We aggregate the tetragram-counts of each policy and then create a list with tetragrams which occur in at least 30% of the policies. Thereby, the assumption is that the use of common phrases in at least 30% of the policies is boilerplate information since disclosure of such common information is unlikely to be firm-specific. The boilerplate measure is then calculated as the number of words in sentences that include at least one boilerplate tetragram divided by the total number of words of the document. In addition to textual similarity and boilerplate information, we analyze the specificity of all policies following Hope et al. (2016) and Dyer et al. (2017), where more specific information indicates a higher level of informativeness. We calculate the specificity measure as the number of entities (locations, people, organizations, currency amounts, percentages, dates, or times) representing specific information within a policy using the Stanford Named Entity Recognizer (NER)Footnote 14 divided by the total number of words in each policy.

The second dimension that needs to be analyzed in order to assess the new requirements in MiFID II is the comprehensibility of best execution policies. According to the literature (e.g., Loughran and McDonald 2016) and Step 4 of our framework, the ease to understand written text can be investigated by analyzing readability and textual complexity measures. Consequently, the comprehensibility of texts is determined by a multitude of different text-inherent features, which need to be analyzed. Since these features cannot be easily summarized in a single readability or complexity measure, we investigate different features separately when analyzing the comprehensibility of best execution policies.Footnote 15 In order to measure the policies’ readability, we rely on the average word length, the average number of words per sentence, and the modified Fog index. While the original Fog index has proven to work well in previous research, Loughran and McDonald (2014) argue that the Fog Index is incorrectly specified in some cases because a large number of multi-syllabic words in a given context, such as company in a finance context, can be well understood and are not a signal of textual difficulty. Therefore, we follow Kim et al. (2019) and calculate a modified Fog measure. Since their list of context-specific multi-syllable words from companies’ annual reports (10-K filings) does not fit to our context, we create our own word list for the modification of the Fog index. First, we construct a list of common complex words that are not difficult to understand in the context of securities trading and best execution by using securities trading and best execution related documents provided by the regulator.Footnote 16 We extract all complex words of these documents and count the occurrence of each word. When the word occurs at least twice, we consider it as a context specific common word. Then, we calculated the modified Fog index by labeling the context specific common words as non-complex words. As an additional readability measure that does not rely on the identification of complex words, we calculate the Flesch reading ease score, which is another popular readability index (e.g., Li 2008; Kim et al. 2019).Footnote 17

With respect to textual complexity, we analyze document lengthFootnote 18 as a proxy for the effort necessary to process the content of a policy. We also investigate the file size of the unprocessed text documents as proposed by Loughran and McDonald (2014). Further, we follow Li et al. (2015) and apply the concept of cyclomatic complexity, i.e., the frequency of using conditional statements in a document.Footnote 19 Additionally, we analyze the entropy of words (Bommarito and Katz 2010; Katz and Bommarito 2014) and the number of unique bigrams to capture the extent of used terms and variations in vocabulary within a document.Footnote 20 To calculate the number of unique bigrams in a document, we use the set of all bigrams that appear at least once in a document. For normalization, we divide the measures cyclomatic terms and unique bigrams by document length.

4.5 Analyze and evaluate MiFID II’s impact on best execution policies (Step 5)

Before generating quantitative linguistic features from the textual content of the execution policies, we perform several common text preprocessing steps. First, as execution policies are mostly in PDF format, we extract the textual content from the documents and delete lists and tables. We further remove stop words from the derived text. For documents in English language, we use stop words from the Natural Language Processing Toolkit (NLTK) (Bird et al. 2009). For German policies, we use the stop words list of the German BPW Dictionary (Bannier et al. 2019). Because execution policies typically include a large number of execution venues and the respective location of the venues’ operators, we additionally exclude text that includes the name and location of these venues. We derive country and city names from an exhaustive list of “major cities of the world”Footnote 21 and all common forms of the respective exchange names from the execution policies themselves.Footnote 22 We also remove parts of the text that did not contain any relevant information, such as email addresses, website URLs, numbers, non-text characters, and single-character words. And last, we convert the text into lower case letters and split it into individual words.

Case 1: Longitudinal analysis based on pre-post comparison

Since we investigate a change in regulation, we perform a longitudinal analysis considering best execution policies before and after the introduction of MiFID II to gain insights on how new regulatory requirements concerning the investment firms’ (subjects) information provision to their clients improved informativeness and comprehensibility (dimensions) of the execution policies (objects). For the analysis, we use the data set consisting of 100 execution policies (50 from 2009 and 50 from 2020) of the largest German banks and brokers obtained in Step 3.

Informativeness—case 1

First, we analyze the textual similarity of best execution policies by calculating the cosine similarity of the German policies in 2009 and 2020 respectively to investigate whether the regulation led to a change in similarity and thus informativeness of the policies. Table 3 provides the descriptive statistics for this analysis. The results clearly show that the regulatory action indeed led to a change of the policies’ similarity. However, the change is contrary to the desired goals of the regulation. While the policies pre-MiFID II show an average tf-idf (doc2vec) cosine similarity of 0.60 (0.86), this score increases to 0.72 (0.89) post-MiFID II, which is also statistically significant as shown by the Wilcoxon Rank Sum (WRS) test. Furthermore, the results show that the best execution policies have a large portion of boilerplate information both pre- and post MiFID II with an average of 0.47 in 2009 and 0.44 in 2020. Also, specificity of the best execution policies remains low with an average of 0.04 in 2009 and 2020.

Similarities (based on tf-idf) of German best execution policies of 2009 and 2020

The increase in textual similarity is further demonstrated by Fig. 2, which visualizes the similarity of execution policies based on the tf-idf approach. Similar results are obtained when computing cosine similarities based on doc2vec (see Fig. 4 in the Appendix). Again, we see a substantial increase in similarity over the whole sample as all squares get darker, which is particularly true for the German savings banks (dark red part in the right corner). Specifically, all saving banks within the sample report the same content in their execution policy in 2020 in contrast to the disclosure of individual execution policies in 2009. Consequently, our results show that the regulatory change in MiFID II did not reach the desired goal of increasing informativeness of best execution policies and, therefore, this prevents that they can serve clients as a sound basis for broker selection. Instead, the policies became more homogeneous, remain relatively unspecific, and still include a large share of boilerplate information, mainly by reciting parts of the regulation,Footnote 23 which is not informative for clients and does not foster competition between brokers based on how they handle client orders to achieve best execution.

Additionally, we also examine the extent to which banks actually adjusted their best execution policies after MiFID II. Therefore, we measure the cosine similarity of the institutions’ matched policies from 2009 and 2020 and compute the difference in the share of boilerplate and specific information. The results are reported in Table 4 together with differences in readability and complexity between the same institutions’ policies. The high tf-idf (doc2vec) similarity scores of on average 0.84 (0.90) as well as the insignificant boilerplate and minor specificity score changes show that banks and brokers obviously did not substantially change their policies after the regulation, providing further indication that MiFID II failed to increase the informativeness of best execution policies.

Comprehensibility—case 1

Second, we investigate changes in the policies’ comprehensibility due to MiFID II based on readability and textual complexity measures. Table 4 provides the differences in readability and complexity measures between matched polices of the years 2020 and 2009, i.e., we compare each bank’s and broker’s post-MiFID II policy with its pre-MiFID II policy. Descriptive statistics for pooled pre- and post-MiFID II best execution policies are provided in Table 8 in the Appendix. Also, Figs. 5 and 6 in the Appendix illustrates the distribution of the readability and complexity measures for the German policies pre- and post-MiFID II.

The readability and complexity analysis provides evidence that the comprehensibility of best execution policies did not improve after the regulatory change in MiFID II. The average number of words per sentence significantly increased by 1.11 words in 2020 suggesting that the policies are harder to read. This is further supported by a significant increase of the modified Fog by 0.60 in 2020. Also, the two readability measures average word length and the Flesch reading ease score did not change significantly indicating that MiFID II did not improve readability of best execution policies. The absence of improvements in readability becomes even more critical in light of the finding that best execution policies post-MiFID II have an average modified Fog index of 17.17 (see Table 8 in the Appendix), which classifies the majority of policies as unreadable and above the reading level of a college graduate (Li 2008). Generally, texts aiming at a wide audienceFootnote 24 should have a Fog index less than 12 (Burke and Fry 2019). With respect to textual complexity, we observe a similar picture with no changes in the measures document length, file size, and relative bigrams, while entropy, and thus the diversity of language, significantly increases. Consequently, the analysis of readability and textual complexity shows that MiFID II also failed to improve readability and understandability of best execution policies.

With our sample of German best execution policies, we cover different bank types. Specifically, our sample consists of 20 savings banks (40% of the sample), eight state-owned banks (German “Landesbanken”, 16%), five cooperative banks (10%), and 17 private universal banks (34%). Table 9 in the Appendix provides descriptive statistics per bank type for the years 2009 and 2020. The descriptive statistics show that the policies of the different bank types are on average highly comparable across almost all measures in both years. One exception is the document length of policies issued by cooperative banks, which—in 2009—is significantly shorter compared to the policies issued by other banks. However, the document length of cooperative banks’ policies adjusts to similar values as the other banks’ policies in 2020.

To validate the descriptive findings, we conduct the following pooled regression analysis to identify the impact of MiFID II on informativeness and comprehensibility of best execution policies:

Thereby, \(Y_{i,t}\) accounts for each readability, complexity, and informativenessFootnote 25 measure of bank i’s best execution policy in year t (2009 and 2020). MiFID II, our main variable of interest, is a dummy variable that equals one if the respective policy is from the year 2020, i.e., after MiFID II had to be applied. Further, we control for bank specific characteristics by taking the natural logarithm of the number of employees (\(log\_Employees\)) and the natural logarithm of total assets (\(log\_TotalAssets\)) into account. We also investigate whether the type of the bank that issued a specific policy has an effect on changes in readability, complexity, and informativeness. In Eq. (1), BankType represents dummy variables for the different bank types.Footnote 26

Table 5 reports the results of this analysis. The regression analysis strongly supports the descriptive findings, i.e., all analyzed measures did not change or even worsened after MiFID II. Specifically, we observe a significant increase in the number of words per sentence (plus 1.39 words) and the modified Fog index (plus 0.64) of the best execution policies that were issued after MiFID II, which indicates that these documents are harder to read. We also find a significant increase of the policies’ complexity according to file size (plus 5.51 kilobyte) and entropy (plus 0.15). Furthermore, the regression analysis confirms that banks’ best execution policies became more similar after MiFID II with an increase in the tf-idf (doc2vec) cosine similarity of 0.10 (0.03) due to MiFID II relative to a pre-MiFID II average of 0.60 (0.86), while the share of boilerplate and specific information remained unchanged. Concerning a potential influence of the bank type, we see hardly any difference in changes of the policies’ complexity between the different bank types. Regarding informativeness, we find evidence that particularly policies issued by savings banks lost informativeness relative to the policies of other bank types as three of the four informativeness measures are positive and significant indicating higher similarity and more boilerplate content. Concerning readability, our results show that policies issued by cooperative banks and to a lesser extent policies issued by savings banks are even harder to read after MiFID II relative to private universal banks and state-owned banks (German Landesbanken). In summary, the results of the regression analyses show that best execution policies became harder to read, more complex, and more similar after MiFID II.

Case 2: cross-sectional analysis based on benchmark approach

In order to comprehensively demonstrate the applicability of the RIA-framework, we also perform a benchmark analysis to evaluate the impact of the best execution requirements in MiFID II as if it was a new regulation (see Section “Data Acquisition (Step 3)”). For this purpose, we make use of the 124 European best execution policies addressing retail investors and the 167 European best execution policies addressing professional investors (all in English). We differentiate between policies addressing retail and professional investors because the regulation explicitly requires investment firms to differentiate between these two types of clients (MiFID II Art. 27(9a)).

Informativeness—case 2

We investigate the informativeness of European best execution policies based on their textual similarity, and the share of boilerplate and specific information. Table 6 shows the descriptive statistics of the similarity, boilerplate, and specificity scores for all analyzed European best execution policies as well as for policies separated by type, i.e., retail and professional clients. Overall, we find that also the sample of European best execution policies shows relatively high similarity scores although being lower than in the German sample. Specifically, the cosine similarity based on doc2vec on average amounts to 0.71 indicating a considerable homogeneity between banks’ best execution policies while the similarity based on tf-idf is slightly lower with an average of 0.42. These results also hold when differentiating between policies aimed at retail and professional clients although policies addressing retail clients are slightly more similar as suggested by the WRS-test. The best execution policies do have a large amount of boilerplate information with an overall average of 0.41, while their specificity is relatively low (overall average of 0.07). As the WRS-test indicates, there is no significant difference between the boilerplate information and the specificity between best execution policies addressed to retail and professional clients. Consequently, the relatively high similarity of the documents together with the high share of boilerplate information and the low specificity show that European best execution policies valid after MiFID II are not very informative.

In order to derive substantive conclusions on the similarity of best execution policies, however, we need to compare the level of similarity with a suitable reference. Therefore, we cluster the execution policies according to context-specific characteristics. These characteristics are derived from the regulation itself as it requires banks and brokers to differentiate between asset classes (MiFID II Art. 27(5)) in their best execution policies. If banks and brokers provide relevant information for clients in their policies, the similarity of policies within the same asset class cluster should increase because similar information should be included. Put differently, policies with the same context-specific focus and which address the same client group (e.g., retail clients with the intention to trade equities) should be more similar than policies of brokers with a different focus if the policies provide informational value as requested by the new regulation. To investigate this, we perform a cluster analysis, whose results based on the tf-idf similarity are reported in Table 7.

To derive clusters according to covered asset classes, we first determine asset class weightings for each policy based on a TA approach, which are then used to cluster the policies using a K-Means algorithm (MacQueen et al. 1967).Footnote 27 This results in four asset class clusters for retail policies (labels: generalists, equity & debt focus, commodity focus, and foreign exchange (FX) focus) and three clusters for professional policies (labels: generalists, commodity focus, and FX focus). The results show that the similarity within five of the six clusters indeed slightly but significantly rises compared to the similarity of all retail (professional) policies, which is confirmed by a WRS-test. For the cluster “equity & debt focus” aimed at retail clients, the similarity of the policies and thus their informativeness slightly decreases while we observe no change for the cluster “generalists” aimed at professional clients. Yet, these two clusters represent the largest number of policies and corresponding firms. Similar results are obtained when calculating the similarity within clusters based on doc2vec (see Table 11 in the Appendix). Consequently, this analysis provides mixed results on the informational value of European best execution policies. In order to rule out that our results are driven by country-specific differences concerning the implementation of the European legislation into national law and its interpretation, we conduct a robustness test by dividing the sample according to brokers’ geographical orientation (i.e., those being active in only one member state and those being active in multiple countries, who thus need to comply with potentially different national laws). The analysis shows that our results are not driven by such an effect since the similarity within these clusters only marginally changes compared to the full retail and professional samples (see Tables 12 and 13 in the Appendix).

Comprehensibility—case 2

We now analyze whether the regulation achieved its goal to increase the ease of understanding of best execution policies after the introduction of MiFID II. As derived in Step 4 of the framework, we apply different readability and textual complexity measures in order to assess the comprehensibility of policies and benchmark these to other documents which cover different ranges of readability and textual complexity.Footnote 28 Figure 3 shows the distributions of the different textual complexity measures for the retail and professional best execution policies as well as the benchmarks as described in Step 3.

Comparison of the distribution of the readability and textual complexity measures with benchmarks

Although investment firms are obliged to differentiate between retail and professional clients in their policies, the distributions across the different readability and complexity measures almost completely overlap. Policies aimed at retail clients are as hard to read as policies aimed at professional clients. Consequently, we do not find any significant difference in ease of understanding of these policies, which—as a first finding—casts doubt on whether the regulation’s goal of comprehensible best execution policies for both retail and professional clients is achieved. This result is also confirmed by the descriptive statistics and the corresponding WRS-tests provided in Table 10 in the Appendix.Footnote 29

Yet, comparing the readability of retail and professional best execution policies does not allow to draw conclusions how difficult these policies are actually to read. For this purpose, the benchmark analysis is conducted. Considering the distributions of the benchmarks, we observe that the value range of readability and complexity of best execution policies is limited and can be clearly differentiated from the benchmarks. According to the readability measures (average word length, wps, (modified) Fog index,Footnote 30 and Flesch reading ease score), best execution polices are as difficult to read as companies’ annual reports in 10-K filings and almost as difficult to read as European regulatory documents themselves. Spoken language, Wikipedia articles, and textbook chapters are noticeably easier to read than best execution policies. Similar observations can be made concerning textual complexity. Based on the relative number of cyclomatic statements, the execution policies again belong to the most complex documents which are in this case spoken language and regulatory documents. Most of the other benchmarks reveal noticeable smaller amounts of cyclomatic statements. This can be explained by the character of these documents. While regulatory documents and spoken language use many conditional terms (Li et al. 2015; Auer 2009), e.g., to explain under what circumstances a certain regulation is applicable or under what conditions a statement holds, the nature of textbook chapters, Wikipedia articles, and 10-K filings is descriptive and explanatory and, thus, conditional statements are avoided to not confuse the reader. Best execution policies also include a high share of cyclomatic statements, which are for example used to state under which condition an order is routed to a specific trading venue. Also regarding complexity measured by the number of unique bigrams, best execution policies belong to the most complex documents and are comparable to the MD&A section of 10-K filings. Yet, best execution policies use a slightly smaller, i.e., more limited, vocabulary than most of the benchmarks as shown by the distribution of entropy. Best execution policies show an overall lower entropy with the distribution mainly ranging from 6.5 to 8 centered at approximately 7.5, while the entropy of spoken language, textbook chapters, and 10-K filings is higher with the center of the distribution being close to or larger than 8. Only regulatory texts and Wikipedia use an even smaller variation of different terms. Yet, the meaningfulness of entropy as a measure for comprehensibility is less convincing than the other readability and complexity measures when comparing texts from different contexts. Due to the topical focus and the regular repetition of certain terms and definitions, words in legal texts and also best execution policies are more predictable than in other documents.

In summary, the analysis shows that best execution policies are not easy to understand as intended by the regulatory requirements in MiFID II but are highly complex documents which are difficult to read. According to the analysis, comprehensibility of best execution policies is similar to regulatory documents and companies’ annual reports, which is way above what can be expected from retail clients.

4.6 Communication to stakeholders (Step 6)

The results of the analysis show that the regulatory change in MiFID II regarding best execution policies did not achieve the desired results. The informativeness of the policies did not increase as intended but rather decreased as shown by the pre-post analysis of German best execution policies. Also for the cross-sectional analysis of best execution policies, we find that these documents are relatively homogeneous and contain high levels of boilerplate information and few specifics. Concerning the second dimension, which is the comprehensibility of best execution policies, the analysis shows that MiFID II did not lead to easier understandable policies but to policies that are actually more complex and harder to read (longitudinal pre-post analysis). Also, it shows that policies are still too difficult to read compared with the applied benchmarks. Consequently, the analysis of the new regulatory requirements for best execution in MiFID II suggests that the goals of increased investor protection and competition between brokers due to more informative and easily understandable best execution policies were not achieved. This finding is important for regulators, investment firms, and investors alike and calls for further regulatory action.

5 Evaluation of the framework

We now evaluate our proposed RIA-framework in case of unstructured data based on its application to the changed best execution requirements in MiFID II. Rigorous evaluation of the developed artifact is an essential step in design science research (Hevner et al. 2004). With the application of the RIA-framework to a real-world setting, we follow Peffers et al. (2007) to demonstrate the applicability and usefulness of the developed artifact. Case studies are frequently used to evaluate conceptual, actionable instructions such as our framework in design science research (Peffers et al. 2012).

The objective of the framework is to evaluate the quality and effectiveness of regulatory actions that result in unstructured data by providing the necessary process steps, decisions, and data requirements, as well as the suitable methodologies. The developed framework enables regulatory authorities and researchers to assess the impact of regulatory actions aimed at or resulting in unstructured data in a clear and structured manner, and thus provides a solution for this class of real-world problems. The application of the framework to the best execution requirements in MiFID II shows that it fulfills these objectives. The impact of the change in regulation could clearly and objectively be identified. As the demonstration in the previous section shows, each step of the proposed framework was successfully applied to the regulatory change in best execution requirements in MiFID II. In particular, the two most important steps for RIA in case of unstructured data, i.e., the selection of appropriate data and methodology, provided clear guidance for the assessment of the regulatory impact. Specifically, with the help of the benchmark approach, the framework does not only enable to assess changes in regulation by comparing documents before and after the regulatory change, but also enables to analyze new regulations resulting in new documents based on appropriate benchmarks. The RIA-framework also provides the necessary guidance to map TA and NLP methods to the dimensions affected by a regulation. After completion of all six steps of the proposed framework, we were able to show how the regulatory action impacted the dimensions targeted by the regulatory change, whether the regulation achieved the desired goals, and whether further regulatory action might be necessary.

6 Discussion

More and more regulations aim at or result in huge numbers of textual documents. In order to assess whether regulatory actions have met the desired goals, RIA needs to be conducted. Yet, and in contrast to regulatory actions that can be measured with structured data, no framework or guideline exist as to conduct RIA in case of unstructured data. To solve this problem and to contribute to research on RegTech supporting regulators in improving regulatory intelligence, we develop a framework for RIA in case of unstructured data that is based on existing RIA guidelines for structured data and methods from TA and NLP. The framework is mainly intended as a methodology for researchers and regulatory authorities, but can also be applied by different stakeholders affected by a regulatory action. With this study, we pave the way for a largely untapped field of research within the RegTech literature, i.e., RegTech and decision support for regulators and policy makers in addition to the current main fields: compliance by firms and supervision by competent authorities.

Our research approach is based on the design science paradigm (Hevner et al. 2004) and follows the established design science research methodology by Peffers et al. (2007). Most relevant contributions in design science research represent either an improvement of an existing process or the extension of existing methods to a yet unsolved problem in another field (Gregor and Hevner 2013). Our framework belongs to the second group because it applies established TA and NLP methods in the context of RIA so that also the impact of regulations that result in or aim at unstructured data can be assessed. This process is nontrivial as one crucial step is the mapping of appropriate methods to the dimensions affected by the regulation in light of the regulation’s overall goals. Our framework provides guidance in this respect and is extensible based on the investigation of further use cases.

The evaluation of the artifact via the case study of best execution requirements in MiFID II shows that the RIA-framework is valid, useful, and provides a solution to a previously unsolved problem. The framework gives guidance to regulatory authorities and researchers to assess both the effects of regulatory actions resulting in unstructured data and the compliance of firms that have to provide such textual data. Thereby, the developed RIA-framework can support evidence-based policy making and improve the quality of regulatory actions aimed at or resulting in unstructured data.

Existing approaches to evaluate such regulatory actions are based on manual inspection of the relevant documents and qualitative assessments of interviews and peer review procedures, which is highly burdensome, resource-intensive, and often does not lead to objective and clear results (European Securities and Markets Authority 2015, 2017). In contrast, our proposed approach is largely automated, follows established research methods, and leads to objective results. Based on TA, NLP and associated research methods, the affected documents are parsed, preprocessed, and automatically analyzed so that no or few manual inspection of the documents is necessary.

Our framework is not unique to the finance discipline or the financial industry—neither the problem at hand (improving informativeness and comprehensibility of texts for customers) nor any step within our proposed framework. Researchers, regulators, policy makers, and other stakeholders can, therefore, use our method to assess the impact of regulations aimed at unstructured data in different contexts and different domains. Examples for application areas in other domains are quality requirements for patient information leaflets in the pharmaceutical sectorFootnote 31, companies’ corporate social responsibility (CSR) reportingsFootnote 32, or cybersecurity-related disclosure requirementsFootnote 33. We believe that the framework is universally applicable and that it represents a general principle to solve a class of real-world problems (i.e., RIA in case of unstructured data), rather than describing a unique set of steps and methods to solve a unique problem (i.e., impact of best execution requirements in MiFID II) consistent with design theory (Gregor and Hevner 2013). Future research can apply the framework to other domains to confirm this assumption.

There are some limitations to our study: Although the proposed framework uses research methods from TA and NLP and, thus, facilitates the resource-efficient analysis of documents, not every step of the framework can be automated. In particular, the identification of the impacted dimensions and the mapping of appropriate analysis methods is of high importance and requires human intervention and substantial background knowledge in the respective field. Also, the dimensions impacted by a regulation and corresponding suitable research methods are case specific to a certain degree. Yet, our RIA-framework provides guidance on generally applicable mappings of frequently occurring regulatory dimensions and corresponding research methods, which can be extended in future research. Moreover, the framework supports researchers and regulators to select appropriate TA and NLP methods for their specific dimensions and cases. Finally, the application of the framework can be challenging in case of data limitations as it is the case with the analysis of German best execution policies where, due to data availability, the time span between the pre- and post-MiFID II documents is relatively long. Yet, such data problems regularly do not exist for the most important potential users of the framework, i.e., regulators and supervisory authorities, who can request the relevant documents for the analysis from investment firms or other impacted entities.