Abstract

This paper analyzes the moderation effect of government responses on the impact of the COVID-19 pandemic, proxied by the daily growth in COVID-19 cases and deaths, on the capital market, i.e., the S&P 500 firm’s daily returns. Using the Oxford COVID-19 Government Response Tracker, we monitor 16 daily indicators for government actions across the fields of containment and closure, economic support, and health for 180 countries in the period from January 1, 2020 to March 15, 2021. We find that government responses mitigate the negative stock market impact and that investors’ sentiment is sensitive to a firm’s country-specific revenue exposure to COVID-19. Our findings indicate that the mitigation effect is stronger for firms that are highly exposed to COVID-19 on the sales side. In more detail, containment and closure policies and economic support mitigate negative stock market impacts, while health system policies support further declines. For firms with high revenue exposure to COVID-19, the mitigation effect is stronger for government economic support and health system initiatives. Containment and closure policies do not mitigate stock price declines due to growing COVID-19 case numbers. Our results hold even after estimating the spread of the pandemic with an epidemiological standard model, namely, the susceptible-infectious-recovered model.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The COVID-19 pandemic infected stock markets worldwide. Recent studies show negative investor reactions to be the strongest since the Spanish Flu of 1918 (Zhang et al. 2020). For instance, the S&P 500 index dropped by more than 30% compared to its all-time high on January 16, 2020. Several economic and social lockdowns caused unexpected, exogenous shocks that provoked a high level of uncertainty in the world’s capital markets (Baker et al. 2020; Zhang et al. 2020). A large amount of unfiltered negative news shaped investors’ sentiment and expectations about the pandemic’s economic impact, reinforced market pessimism and triggered investor overreactions (Alexakis et al. 2021; Liu et al. 2021; Salisu and Vo 2020). In a recent study, Erdem (2020) reveals that the pandemic has a significant negative impact on a country's stock market index, with the growth in COVID-19 cases causing a three times larger decline in index prices than fatalities.

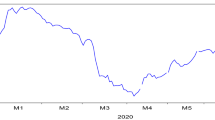

However, after the World Health Organization (WHO) pronounced COVID-19 a pandemic on March 13, 2020, it took only 26 days for the S&P 500 index to recover to its preannouncement value. Remarkably, another 158 days later, on August 18, 2020, the index again surpassed its all-time high from January 16, 2020. Figure 1 illustrates an overlay of the S&P 500 stock market index and the logarithmic growth of global confirmed COVID-19 cases and deaths for an observation period from January 1, 2020 to March 15, 2021.

S&P 500 Index and globally confirmed COVID-19 cases and deaths (logarithmic). This figure shows the S&P 500 stock market index and logarithmic global confirmed COVID-19 cases and deaths for our observation period from January 1, 2020 to March 15, 2021. S&P 500 index data are derived from Thomson Reuters Datastream, and case and death data are obtained from the European Centre for Disease Prevention and Control (ECDC)

What triggered investors to regain optimism rapidly, with the number of cases and deaths still rising? Recent studies on the capital market effects caused by the pandemic argue that government responses to contain the spread of the disease may play an important role in shaping investor sentiment during the pandemic (Alexakis et al. 2021; Hale et al. 2021; Salisu and Vo 2020). However, there is a lack of research on the relevance of government responses to COVID-19 for investor sentiment and capital markets. Only a few studies exist that, at an early stage, either discuss country-level macroeconomic impacts of government initiatives to contain the spread of the disease (e.g., Alexakis et al. 2021; Zaremba et al. 2020) or the impact of COVID-19 on investor sentiment (e.g., Jiang et al. 2021; Sun et al. 2021).

Research calls for studies that investigate the impact of government responses to COVID-19, differentiating government responses by their aim and scope to reveal diverse impacts on investor behavior and capital markets (e.g., Goodell 2020; Hale et al. 2021). Undoubtedly, firms have a deep interest in how to react to a pandemic crisis depending on government policies, leading to the development of communication strategies by all groups of stakeholders. Existing research does not consider that investors of multinational companies (MNCs) are forced to incorporate the policies of multiple governments into their trading decisions. Research thus far does not consider that trust in governments impacts investor sentiment and trading behavior during the pandemic. As the literature provides evidence that external shocks (e.g., terrorist attacks) significantly reduce investors’ trust (Lesmeister et al. 2018), government countermeasures to COVID-19 that reduce investors’ uncertainty can be assumed to positively affect trust and mitigate stock price declines. In addition, recent studies show that firm-specific characteristics may serve as moderators of COVID-19-associated declines in stock prices. For example, Ding et al. (2021) find that firms that are highly exposed to supply chain disruptions exhibit greater declines in returns. However, no study exists that analyzes associations with a firm’s sales side, i.e., sales revenues, by considering that investors can potentially evaluate the COVID-19 situation in other countries, where a large portion of a firm’s revenue is realized.

Our paper addresses this research gap. We argue that government responses influence investor sentiment, leading to diverse moderating effects on the association between the growth rates of COVID-19 cases, the number of deaths and stock market reactions. While restrictive policies may negatively influence investors’ sentiment, increase pessimism, and trigger market overreactions, investors may also appreciate supportive efforts by governments, adjust their perceptions about market development, and, in consequence, positively adjust their investment decisions. Hence, governments may be able to actively reduce uncertainty, increase trust among investors and indirectly affect the stock market. We expect this two-sided effect to be an important driver of rapid stock market recovery during the pandemic.

We build on the research of investor sentiment to explore the impact of the responses of 180 governments on the relationship between the stock prices of S&P 500 firms and the growth rates of COVID-19 cases and deaths in the period from January 1, 2020 to March 15, 2021. Specifically, we analyze 16 indicators covering three major fields of government policies, i.e., containment and closure, health system, and economic support, tracked by Oxford University’s Government Response Tracker (OxCGRT). We use country-specific revenues of each S&P 500 firm to solely assign government responses of firm-relevant countries to a firm and, in a second model, to reveal whether investors are aware of and react differently to a firm’s direct revenue exposure to COVID-19. Please see Fig. 2 for an illustration of our sample structure and our research design.

A Illustration of our sample structure. This graphic illustrates the structure of our sample. We use the S&P 500 firm-specific daily abnormal stock returns to proxy for U.S. capital market effects. Each firm realizes sales revenues at different levels in various countries, symbolized by the money bag. At the same time, these countries are exposed to the COVID-19 pandemic with different severeness over time, symbolized by the virus pictogram. To contain the spread of the disease and to mitigate the economic and social impacts of the pandemic, the countries’ governments respond with country-specific actions and policies, symbolized by the government house pictogram. B Research Design. This figure represents the design of our main regression model: COVID-19 cases and deaths of firm-relevant countries serve as the independent variables. Abnormal returns, measured as adjusted abnormal logarithmic returns using a market model, where expected returns are estimated with market betas using the firm’s daily stock returns, and the S&P 500 index returns of the respective period, is the dependent variable. We employ two moderators to test for interactions with our COVID-19 proxies. First, a set of three government response indices, calculated from 16 indicators covering three major fields of government policies, i.e., containment and closure, health system, and economic support, tracked by the Oxford University’s Government Response Tracker (OxCGRT), including a summarizing index to reflect the entirety of government responses. Second, a firm’s specific revenue exposure to COVID-19 was calculated by weighting the country-specific sales revenues of our sample firms with the country’s growth rates of COVID-19 cases and deaths per million

Results reveal that aggregated government responses mitigate the decline of stock returns due to both rising COVID-19 cases and deaths. Governments’ actions in the fields of containment and closure as well as economic support are most likely appreciated by investors and mitigate negative stock market impacts caused by the pandemic. In contrast, government actions concerning a country’s health system provoke further declines in abnormal stock returns. One reason could be the absence of initiatives that support health systems, e.g., widespread testing or vaccination campaigns, in the initial period of the pandemic. In general, health system initiatives are delayed compared to other government responses, causing uncertainty among investors. The mitigating effect of government responses in the field of economic support is stronger for firms that are highly exposed to COVID-19 on the sales side. We fail to find such effect for containment and closure policies, indicating that they are not strong enough for investors to adjust their pessimistic views on market development. Our results are relevant for firms in anticipating and strategically managing investor relations and in actively demanding government interventions. They are further valuable for governments in discussing the economic costs and benefits of their responses to pandemics. Moreover, our study contributes and expands the knowledge about investor sentiment during crisis situations caused by external shocks.

2 Literature review and research questions

2.1 Investor sentiment and capital markets

The literature on behavioral finance has extensively explored whether investor sentiment affects trading decisions, leads to irrational trading behavior, and affects stock prices (e.g., Baker and Wurgler 2006; Beer and Zouaoui 2012; Chau et al. 2016; Cormier et al. 2010; Fang and Peress 2009; He et al. 2020; Hong and Stein 2007, 1999; Kaniel et al. 2008; Long et al. 1990; Palomino 1996; Shleifer and Vishny 1997). Bollen et al. (2011) find that investors’ trading behavior is directly shaped by their perceptions about future market development. Anxiety increases investors’ risk avoidance and contributes to pessimism (Baker and Wurgler 2006; Cen and Liyan 2013).

One relevant driver of investor perceptions and expectations is news. Tetlock (2007) shows that news media pessimism predicts downward pressure on market prices, even leading to a revision of fundamentals. Subsequent studies find that bad news leads to more intense or even panic-driven, long-term stock market effects (Cohen et al. 2018; Jung et al. 2018; Miller and Skinner 2015). A subordinate literature stream covers the formation and consequences of investor overreactions. In a fundamental study, de Bondt and Thaler (1985) investigate whether, and following which rules, the stock market overreacts. They present experimental evidence that in probability revision problems, people show a tendency to overreact, i.e., they overweight recent information and underweight base rate data. Barberis et al. (1998) link investor overreactions to news. They analyze the impact of good and bad market-relevant news announcements as a moderator of investor overreaction and stock return developments. Results show that investors overreact to consistent patterns of good (bad) news with a correlation to the length of good (bad) news series. Michayluk and Neuhauser (2006) analyze the role of investor overreaction during the market decline following the 1997 Asian financial crisis. They conclude that overreaction is sensitive to news announcements and is traceable for 1 week after the announcement. On a different note, Gennaioli et al. (2015) argue that a single piece of bad news in a series of good news items will not lead to a change in the underlying beliefs of investors regarding certain stocks. Nevertheless, a continuous series of bad news results in investor overreaction because previously ignored bad news is remembered, 'leading to a sharp rise in the perceived probability of a crisis and a collapse of prices' (Gennaioli et al. 2015, p.312).

Another influencing factor on investor sentiment is trust. Georgarakos and Pasini (2011) find an association between trust in financial markets and investors’ trading behavior. Based on a portfolio model using survey data, they show that in countries where investors exhibit a high level of trust toward the capital market, the stockholding share is significantly higher than in low-trust countries. Lesmeister et al. (2018) analyze whether shareholders extend or reduce their monitoring activity (e.g., by shareholder votes) relative to the general trust that they experience. The study reveals that trust reduces the amount of shareholder monitoring activity. Moreover, when exposed to external shocks, such as terrorist attacks, investors’ trust decreases by an increase in announced fatalities.

2.2 Investor sentiment during epidemics/pandemics

As financial crises caused by epidemics or pandemics are not without precedent, few studies have taken the occasion of previous health crises to expand the knowledge of their power to impact investor sentiment. Funck and Gutierrez (2018) examine the impact of Ebola headline news on media-highlighted stocks. They employ the VIX-Investor Fear Gauge (VIX), introduced by Whaley (2009), to proxy for investor pessimism during Ebola outbreak announcements. They reveal that stock prices tend to reverse themselves within one day after the announcement, supporting the traditional theory of investor overreaction. Avian influenza (bird flu), initially reported in China in March 2013, caused a loss in the agriculture sector by $6.5 billion due to changes in prices, consumer confidence and trade volumes. Jiang et al. (2017) explored the impact of daily avian influenza case announcements on stock prices. They find peaks in investors’ overreacting behavior within the initial outbreak announcements; that is, investors seem to act more reasonably in time when the shock of the first outbreak news has been overcome.

Ichev and Marinč (2018) focus on the 2014–2016 Ebola outbreak. They analyze the effect of mass media news announcements about Ebola outbreak events on firms’ stock returns. They find that investors act irrationally to the news on the Ebola outbreak and that Ebola outbreak events unequally affect investors’ sentiment about stock returns, depending on the distance of the outbreak event from the markets. Negative effects on financial markets are stronger for firms that operate in countries with a larger Ebola exposure. They conclude that a firm’s geographic proximity to the Ebola outbreak event increases the impact on its stock returns.

In a recent study, Engelhardt et al. (2020) find that COVID-19-induced stock market declines in 64 countries are mainly associated with greater news attention and less with rational expectations. Following this research, we expect the growth rates of COVID-19 cases and deaths in firm revenue-relevant countries to depress investor sentiment by provoking panic and pessimism, resulting in temporary market overreactions and leading to a decline in stock returns during the pandemic.

2.3 Government responses to the COVID-19 pandemic and investor sentiment

With rising COVID-19 cases and deaths, several governments worldwide took action to mitigate the repercussions of the disease and introduced diverse sets of countermeasures, i.e., government responses. In addition to restrictive policies to contain the spread of the disease (e.g., travel restrictions, stay-at-home requirements, school closings, public transport closings), stimulus packages were implemented to mitigate the economic impact of the pandemic (e.g., income support, debt relief, fiscal measures). Moreover, proactive measures were set in motion to reduce infection rates (e.g., testing policies, vaccination policies, contract tracing) (Hale et al. 2021). Following the literature on investor sentiment, we argue that government responses to COVID-19 can reinforce or mitigate the negative impact of the COVID-19 pandemic on stock prices. Governments may reduce uncertainty among investors, regain investors’ trust and lead to a less severe decline, or even rise, of firms’ stock returns, depending on the aim and scope of the policy. Moreover, we expect investors to rate government responses differently depending on a firm’s exposure to COVID-19; this is how severely those firm-relevant countries are affected, which directly contribute to the firm’s revenues.

3 Data and research design

3.1 COVID-19 data

We obtain daily data on worldwide confirmed COVID-19 cases and deaths per country from January 1, 2020 to March 15, 2021 from the European Centre for Disease Prevention and Control (ECDC). We calculate the daily growth rates of both cases and deaths in each country, relative to a country’s population, by dividing the number of daily cases and deaths per million in country i on day t by the same measure of the previous day t−1. We receive a subsample of 180 countries and 563 observation days per country. Our sample is unbalanced since, for some sample countries, no cases or deaths were reported until April 2020.

3.2 Capital market data

To measure firm-level stock market reactions to the COVID-19 pandemic, we obtain daily stock prices for 511 firms that make up the S&P 500 index during our observation period from January 1, 2020 to March 15, 2021. To solely assign COVID-19 cases and deaths and government responses of firm-relevant countries to a firm, we obtain country-specific sales revenues [REVENUEi,c,t] for the compounding S&P 500 firms for 2019 from the FactSet Geographic Revenue (GeoRev) Database. We assign all countries to a firm that contributed to the firm’s revenues, leading to a combination of multiple countries for each firm per observation day. We only include values with a certainty score of 70 or above, as provided by GeoRev. The certainty score is based on source metadata and ranges from 1 (low certainty) to 80 (declared value). This proceeding enables us to isolate information that is assumed to be of decision-relevant significance to each firm’s investors. See Appendix 1 for a list of countries included and the number of firms that realize revenues in the respective country.

3.3 Government response data

We employ data from the OxCGRT, published by Hale et al. (2021), to measure country-specific government responses to the pandemic. Our dataset covers 16 individual ordinal scaled indicators that represent the strictness of various government policies in response to the COVID-19 pandemic. It should be noted that these values do not reflect the effectiveness of each policy. All indicators can be classified into three groups, representing the scope of the policy, i.e., containment and closure policies, health system policies, and economic policies. We include the following indicators:

Containment and closure policies

School closings; workplace closings; cancelations of public events; restrictions on gatherings; closing of public transport; stay-at-home requirements; restrictions on international movement; international travel controls

Health system policies

Public information campaigns; testing policy; contact tracing; facial covering policy; vaccination policy; protection of elderly people

Economic policies

Income support; debt and contract relief

Please see Appendix 2 for a full list of indicators, including detailed descriptions and scale coding. To reflect the extent of each government’s efforts, we calculate an index for each of the three policy groups.Footnote 1 Since all indicators are ordinally scaled and ranked with different values set as maximums, we calculate subindices to normalize each indicator to an equally spaced scale between 0 and 100. The three indices, i.e., containment and closure index, health system index, and economic support index, are then calculated as simple averages of the normalized individual subindices. Moreover, we aggregate all three indices to create a summarized government response index. We merge our government response data with the firm-country dataset, including growth rates in the number of cases and deaths. Our final sample consists of 10,060,911 daily firm-country-specific observations.

3.4 Empirical model

To test whether government responses to the COVID-19 pandemic moderate the impact of confirmed and announced COVID-19 cases and deaths on firms’ daily stock returns, we estimate the following regression model using firm- (Firm FE) and day-fixed (Day FE) effects*:

where i, c, and t index firm, country, and day, respectively.

Our dependent variable [ARi,t+1] is measured as adjusted abnormal logarithmic returns using a single-index market model, where expected returns are estimated with market betas using the firm’s daily stock returns and the S&P 500 index returns of the respective period (e.g., Brown and Barry 1984; Dai and Zhu 2020; Jain 1986; Sharpe 1963). Specifically, we define abnormal returns as \(AR_{t}^{i} = R_{t}^{i} - E\left( {R_{t}^{i} } \right)\), where \(R_{t}^{i}\) represents the daily return for firm i on day t. We estimate the firm’s expected return as \(E(R_{t}^{i} ) = \alpha_{i} + b_{i} E(R_{t}^{market} )\), with \(R_{t}^{market} = (P_{t}^{market} - P_{t - 1}^{market} )/P_{t - 1}^{market}\), where \(P_{t}^{market}\) represents the S&P 500 index closing price on day t.Footnote 2 Following prior research on the stock market impact of infectious diseases, our model parameters are estimated over a 90-trading-day estimation period, starting one day prior to day t to prevent unusual effects on the measurement day from interfering the estimation (e.g., Liu et al. 2020; Wang et al. 2013).

COVID-19c,t represents either the growth rate of the announced cumulative number of confirmed COVID-19-positive cases [CASESc,t] or deaths [DEATHSc,t] associated with or caused by the disease per million in country c for day t. RESPONSEc,t corresponds to each of our four daily government response indices, i.e., containment and closure index [CONTAINMENT_CLOSUREc,t], health system index [HEALTH_SYSTEMc,t], economic support index [ECON_SUPPORTc,t], and the summarized government response index [GOV_RESPONSEc,t]. We use a set of control variables based on prior literature. We control for abnormal returns one day prior to the measurement day by using abnormal returns [ARi,t] in autoregression to consider stock return autocorrelation (e.g., Kraft and Kraft 1977; Smirlock and Starks 1988). Zaremba et al. (2020) and Ali et al. (2020) reveal a significant impact of the COVID-19 pandemic on market volatility. Hence, we include a firm’s annualized volatility of logarithmic stock returns during our observation period [VOLATILITYi,t]. We control for the number of analysts following a firm’s share [FOLLOWINGi,t] as well as for the percentage of institutional holdings [INSTITUTIONALi,t], with both variables to be measured annually (e.g., Bartov et al. 2018; Chen et al. 2013; Hong et al. 2000). A broad number of studies investigate the relationship between firm fundamentals and stock market returns. We follow these findings by including firm size as proxied annually by the logarithm of a firm’s total assets [SIZEi,t] and the price-to-book ratio as a firm’s daily market price per share divided by the share’s book value [PTBi,t] (e.g., Fama and Franch 1993; Griffin and Lemmon 2002; Pontiff and Schall 1998). Moreover, corporate governance research finds that the number of a firm’s board members shapes board integrity and effectiveness and, thus, reinforced by the perception of investors, affects returns (Cheng 2008; González et al. 2019). Hence, we include the quarterly board size [BOARDi,t] in our set of controls. Davison (2020, p. 2) finds that 'the stocks returns of firms who are relatively unable to transition their business to comply with social distancing are much more responsive to changes in their level of leverage going into the pandemic'. We, therefore, process a firm’s leverage change during our observation period as the yearly differences in the ratio of a firm’s book value debt and total assets [LEVERAGEi,t]. Hu and Zhang (2021) show that firm performance deteriorates during the COVID-19 pandemic. However, the effect is smaller for firms in countries with better health systems, more advanced financial systems, and better institutions. We address these findings by controlling for the quarterly change in a firm’s return-on-assets [ROAi,t], calculated as operating income before depreciation over total assets. Several studies discuss a firm’s economic, social, and governmental scores (ESG scores) to indicate the resilience of stock prices during the COVID-19 pandemic. However, the results of preliminary studies are controversial. Albuquerque et al. (2020) find that stocks with higher ESG scores have significantly higher returns, lower return volatility, and higher operating profit margins during the first quarter of 2020. Broadstock et al. (2021) add that ESG performance mitigates financial risk during a financial crisis and that high-ESG portfolios generally outperform low-ESG portfolios. In contrast, Demers et al. (2020) conclude that higher ESG scores do not immunize stocks. We control for ESG scores [ESGi,t] using the most prevalent Refinitiv ESG SCOREFootnote 3 that weekly measures a company’s relative ESG performance, commitment and effectiveness across 10 main themes, including emissions, environmental product innovation and human rights (Refinitiv 2020). Since the discussed literature on investor sentiment assigns an important role in affecting investor sentiment to news media, we control for three variables covering the spread, perception, and sentiment of COVID-19 news in each country. Data were obtained from the RavenPack Coronavirus Media Monitor. MEDIA_COVERAGEc,t calculates the daily percentage of all news agencies in country c on day t covering the topic of COVID-19. The index is computed as the daily number of distinct news agencies that mention COVID-19, divided by the total available number of news agencies in the country. MEDIA_HYPEc,t measures the percentage of news that is currently reporting about COVID-19 in country c on day t, regardless the originating news agency. The index is computed as the daily number of reports that mention COVID-19, divided by the total daily number of reports. MEDIA_SENTIMENTc,t measures the level of sentiment that news reports express towards a firm that is mentioned in the report alongside COVID-19. Specifically, it reflects the daily average of the difference between the number of positive and negative news reports. RavenPack determines positive or negative sentiment by 'systematically matching stories usually categorized by financial experts as having a positive or negative financial or economic impact. The algorithm produces a score for more than 6900 categories of business, economic, and geopolitical events, ranging from earnings announcements to natural disasters.' (Hafez et al. 2020). The index ranges between − 100 and 100, where a value of 100 is the most positive sentiment, − 100 is the most negative, and 0 is neutral. All variables are defined in Appendix 3.

4 Empirical results

4.1 Summary statistics

Table 1 reports descriptive statistics for all variables in our main regression model specifications. All variables are winsorized at the 1st and 99th percentiles to mitigate the influence of outliers. The mean value of firm-specific abnormal returns is 0.001 [ARi,t+1]. The mean annualized volatility of stock returns is 31.336 [VOLATILITYi,t], which is remarkable since the S&P 500’s annualized average volatility from 1926 through 2017 is 15.2.Footnote 4 The mean share of revenues that a firm derives from a country is 1.126% [REVENUEi,c,t], with a maximum share of 53.175%. This maximum coincides with the average revenue share that S&P 500 firms realize in the United States, as expected. As the median value is 0.083 and the 75th percentile shows a value of 0.301, the highest revenue firms are allocated to a small number of countries. On average, a firm is followed by 22 analysts [FOLLOWINGi,t], and the mean share of institutional owners [INSTITUTIONALi,t] is 82.829%. Firm size [SIZEi,t], price-to-book-ratio [PTBi,t], and the level of leverage [LEVERAGEi,t] show mean values of 223.730 bn, 5.730, and − 0.973, respectively. A firm’s board comprises approximately 11 members. Unsurprisingly, concerning firm performance, the average return on assets is negative at – 1.656%. Thomson Reuters Refinitiv calculates a mean ESG score [ESGi,t] of 63.582 for our sample firms. Turning to country-specific data, on average, a country is exposed to a daily growth of 5.926% in COVID-19 cases per million people [CASESi,t] and a daily growth in COVID-19-related deaths per million people of 0.129% [DEATHSc,t]. We calculate our index for a country’s containment and closure policies [CONTAINMENT_CLOSUREc,t] to average 49.616. Values for our index covering a country’s efforts to support the health system [HEALTH_SYSTEMc,t] as well as the economy [ECON_SUPPORTc,t] rank closely at 54.449 and 43.965, respectively. Our summarized measure for a government’s effort in all fields [GOV_RESPONSEc,t] exhibits a mean value of 54.940. Our controls for the spread, perception, and sentiment of COVID-19 news in each country reveal the following descriptive insights: On average, 55.511% of all news agencies in a country cover the topic of COVID-19. The percentage of news that reports on COVID-19 each day in a country is 46.118. The mean level of sentiment toward a country mentioned in the news alongside COVID-19 is − 5.930, with an overall sample maximum of 50.950 of 100 index points and a minimum of − 97.210. The median remains negative at − 2.460.

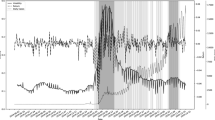

Figure 3 shows the S&P 500 stock market index and the intensity of the global government response index [GOV_RESPONSEc,t] to COVID-19 for our observation period from January 1, 2020 to March 15, 2021. The intensity of global government responses is calculated by accumulating all 16 policy indicators per day over all 180 countries. The scale is normalized on a range of 0–100, where 100 represents the maximum intensity for the observation period. From March 5, 2020 on, worldwide initiatives to contain the spread of the pandemic are increasingly put in place. Hence, the global government response index grows exponentially. The growth accelerates from March 13, 2020, when the WHO declares the COVID-19 outbreak to officially be a pandemic. At the same time, the S&P 500 stock market index experiences a decrease that seemingly mirrors the government response’ s development. After a peak on April 17, 2020, the response index values diminish throughout the summer months, starting from approximately the date when the S&P 500 index recovers to its pandemic pre-announcement value. Towards winter, global government responses increase again slightly despite a continuously bullish stock market.

S&P 500 Index and global government response index. This figure shows the S&P 500 stock market index and the intensity of accumulated global government responses to COVID-19 for our observation period from January 1, 2020 to March 15, 2021. S&P 500 index data are derived from Refinitiv Datastream. Data for the calculation of the global government response intensity are provided by the Oxford COVID-19 Government Response Tracker (OxCGRT) database. The intensity of global government responses is calculated by accumulating all 16 policy indicators per day over all 180 countries. The scale is normalized on a range of 0 to 100, where 100 represents the maximum intensity for the observation period

Figure 4 shows the S&P 500 stock market index and the intensity of accumulated global government responses to COVID-19 for our observation period, split for policies in the fields of containment and closure [CONTAINMENT_CLOSUREc,t], health system [HEALTH_SYSTEMc,t], and economic support [ECON_SUPPORTc,t]. As before, the scale is normalized on a range of 0–100, where 100 represents the maximum intensity for the observation period. All three indices follow the path of the accumulated, global government response index, as illustrated in Fig. 3. However, health system initiatives are implemented later compared to containment and closure policies or economic support. Containment and closure policies experience the strongest decline, with health system initiatives still increasing. In the course of the bullish stock market, economic support and containment and closure policies are reduced, while health system support is still being extended.

S&P 500 Index and global government responses by scope: containment and closure index, health system index and economic support index. This figure shows the S&P 500 stock market index and the intensity of global government responses in the fields of containment and closure, health systems, and economic support for COVID-19 for our observation period from January 1, 2020 to March 15, 2021. S&P 500 index data are derived from Thomson Reuters Datastream. Data for the calculation of the global government response intensity are provided by the Oxford COVID-19 Government Response Tracker (OxCGRT) database. The intensity of each global government response field is calculated by accumulating all field-specific policy indicators per day over all 180 countries. The scale is normalized on a range of 0 to 100, where 100 represents the maximum intensity for the observation period

Table 2 presents the Pearson–Spearman correlations. Both CASESc,t and DEATHSc,t are significantly negatively correlated with ARi,t+1 (Pearson − 0.042; Spearman − 0.029 and Pearson − 0.027; Spearman – 0.022). This is a first indicator of the negative impact that rising COVID-19 cases and deaths cause on stock prices. GOV_RESPONSEc,t shows a significant and positive correlation with AR (Pearson 0.023; Spearman 0.019), as CONTAINMENT_CLOSUREc,t does (Pearson 0.064; Spearman 0.055). In contrast, correlation coefficients for the remaining two indices, HEALTH_SYSTEMc,t and ECON_SUPPORTc,t, are significantly negative regarding ARi,t+1 (Pearson − 0.032; Spearman − 0.041 and Pearson − 0.029; Spearman − 0.018). These findings imply that a split investigation of government responses is imperative since different government policies may provoke different market reactions. All four government response indices are significantly and positively correlated to both CASESc,t and DEATHSc,t, exhibiting high magnitudes (e.g., COV_RESPONSEc,t is correlated to CASESc,t with Pearson 0.0552; Spearman 0.427). This illustrates the sensitivity of government interventions worldwide to rising COVID-19 cases and deaths. Turning to our controls, we find interesting values for our news media measures. As expected, both MEDIA_COVERAGEc,t and MEDIA_HYPEc,t are positively correlated with CASESc,t and DEATHSc,t (e.g., MEDIA COVEERAGEc,t and CASESc,t Pearson 0.192; Spearman 0.140). However, MEDIA_SENTIMENTc,t is negatively correlated with COVID-19 proxies (CASESc,t: Pearson − 0.078; Spearman − 0.110, DEATHSc,t Pearson − 0.124; Spearman − 0.123). This leads to the interpretation that the amount of news that mentions COVID-19 and specific countries increases as COVID-19 cases and deaths grow. At the same time, the sentiment expressed in the news media toward countries becomes negative as COVID-19 numbers grow. Overall, the absence of high correlations among our variables suggests that there are no multicollinearity concerns.

4.2 Government responses and stock returns

First, we examine whether the impact of COVID-19 on firms’ daily abnormal stock returns is moderated by the summarized government responses of countries that contribute to a firm’s revenue. Table 3 presents our main regression results for Eq. (1).

Models I and II examine the raw impact of the growth rate of the announced number of confirmed COVID-19-positive cases [CASESc,t] or deaths [DEATHSc,t] per million associated with or caused by the disease on abnormal returns [ARi,t+1]. As expected, results show that the stock market responds significantly negatively to both COVID-19 proxies. However, the daily growth in the number of country-specific deaths is of greater relevance to investors since the coefficient for DEATHSc,t (− 0.063) is larger in magnitude than the coefficient for CASESc,t (− 0.038). These findings are contrary to previous studies on the impact of COVID-19 cases and deaths on the stock market that expose cases to mainly drive the stock market (e.g., Alexakis et al. 2021; Ali et al. 2020; Erdem 2020). This contrast is most likely explained by the longer observation period that is considered in our study. Specially, when analyzing the consequences of diseases for the first time, a longer observation period allows for incorporating the different stages it passes. More specifically, in the initial period, the spread of the pandemic was mainly measured (and publicly discussed) by the increasing number of cases. In the course of the pandemic, this perspective changed due to worldwide high levels of cases, and deaths became a more important focus of interest for health organizations, governments, and news media. In addition, as is shown in Fig. 1, the increase in the number of deaths was delayed compared to the increase in the number of cases. Hence, due to short observations covering the initial period of the pandemic, most preliminary studies lack enough data to reveal robust and interpretable results concerning deaths.

Our firm specific controls perform as expected and support the findings of the previous studies on stock market reaction we discussed. Turning to our media-related controls, we find MEDIA_COVERAGE and MEDIA_HYPE to show positive effects on stock returns. This is unsurprising since prior research on behavioral finance has well explored that the excessive presence of news, regardless of the expressed sentiment, leads to a higher attention of investors, and thus, gives positive momentum to the stock market development (e.g., Andrei and Halser 2015; Engelhardt et al. 2020). At the same time, MEDIA_SENTIMENT shows a significant and negative impact on stock returns. As this variable incorporates both positive and negative sentiment, and descriptive statistics reveal a mean of − 5.930, and thus, predominantly negative sentiment throughout our observation period, this result follows prior research that finds negative news to negatively influence the stock markets (e.g., Cohen et al. 2018; Jung et al. 2018).

In Models III and IV, we add our summarized government response index [GOV_RESPONSEc,t] to analyze whether the entirety of a country’s responses to the pandemic moderates the association shown in the previous models. Across both models, we find positive and statistically significant coefficients on the moderation of cases and deaths by government responses. This indicates that the entirety of government policies positively influences investor sentiment, retriggers optimism, restores investor trust and eventually mitigates the decline of stock prices. In other words, market participants seem to appreciate governments’ efforts to contain the consequences of the pandemic. Our control variables follow similar patterns as in the previous models. Within each regression, F tests indicate that the coefficients on the CASES/DEATHS and GOV_RESPONSE variables are significantly different from each other in all specifications, suggesting that both variables add explanatory value to our model.

4.3 Government responses split by scope and stock returns

Since we find summarized government responses to play an important role in stock market development during the COVID-19 pandemic, we are now interested in dividing our GOV_RESPONSEc,t index into the different scopes of government responses, measured by our 16 country-specific indicators, to see whether different scopes of responses mitigate or reinforce the negative stock market impact of the pandemic. Table 4 presents the results of our regression models covering the moderating effects of government containment and closure policies [CONTAINMENT_CLOSUREc,t], the support of the country’s health system [HEALTH_SYSTEMc,t], and the support of the economy [ECON_SUPPORTc,t].

In Models I and II, we estimate the additional moderating effect of containment and closure policies in coherence with CASESc,t and DEATHSc,t, respectively. Both interaction coefficients are positive and statistically significant. Hence, governments mitigate negative market impacts of the pandemic by taking actions to contain the spread of the disease, e.g., school closings, workplace closings, closings of public transport or issuing stay-at-home orders.

Government economic support [ECON_SUPPORTc,t] in Models V and VI has similar effects. Investors seem to appreciate the efforts of governments to mitigate the economic consequences of the pandemic by relieving debts and contracts or by supporting incomes. They most likely adjust their perceptions about market development and, in consequence, positively adjust their investment decisions.

Interestingly, government support of a country’s health system [HEALTH_SYSTEMc,t], shown in Models III and IV, causes further declines in abnormal stock returns as the interaction coefficients are negative and significant. For the interpretation of this counterintuitive effect, it is helpful to reinvestigate Fig. 4. The pathway of the index for government efforts globally in supporting health systems [HEALTH_SYSTEMc,t] differs from the remaining two indices. From the date the WHO pronounced COVID-19 a pandemic on March 13, 2020 until the S&P 500 recovered to a preannouncement value on March 30, 2020, the growth of the health system index was significantly smaller, suggesting a smaller contribution to stock market declines. As the situation progressed, with recovering S&P 500 values, the health system index continued growing, while the other two indices showed persistent declines. Analyzing the index composition, one explanation may be the initial weakness and the delay of efforts in strengthening the health system. For example, widespread testing initiatives were implemented late due to the absence of reliable tests. This more obviously holds true for vaccination campaigns. Because health system policies are mainly implemented when the stock market was on a path of recovery and was gaining momentum, investors apparently feared restrictions or policies in the health sector that would interfere with the boom again. This uncertainty most likely provoked pessimism and, in consequence, negative stock market effects. Results from F tests indicate a significant difference in the coefficients on CASES/DEATHS and the government response measures.

The coefficients of our sets of firm and country-specific control variables remain stable in significance, magnitude, and direction with indistinguishable differences from our previous regression covering summarizes government responses.

4.4 Government responses and firm-specific COVID-19 revenue exposure

In contrast to most studies on the economic consequences of the COVID-19 pandemic we discussed, we investigate COVID-19 related impacts on firm-level rather than aggregating an entire economy. This approach allows a detailed investigation of the linkage between the COVID-19 pandemic, worldwide government regulations, and multinational firms’ characteristics.

One major field of interest for both research and practice is whether some firms are more severely affected by the COVID-19 pandemic and by government responses than others. Recent studies show various firm-specific characteristics to moderate the extent of the declines in stock returns associated with the pandemic. For example, Ding et al. (2021) find that firms with high exposure to supply chain disruptions show greater stock price declines.

We aim to analyze whether country-specific sales revenues at the firm level influence the effect of governmental responses to COVID-19-associated stock market effects. Specifically, we are interested in whether investors react differently to a growth in the number of COVID-19 cases and deaths and related government responses when a firm is more severely affected by this growth on the sales side.

We employ the comprehensive FactSet Geographic Revenue Exposure (GeoRev) Database that meters a firm’s annual sales revenue for each of the world's countries it operates in. The data is derived from a broad set of sources, e.g., summarized annual reports. In addition, 'an estimation algorithm based on GDP weighting and accounting logic is then applied to solve for any non-explicit disclosures' (FactSet 2022). The result is a detailed breakdown of a company’s revenues into any geographic country. The database also provides a certainty score that is based on source metadata and ranges from 1 (low certainty) to 80 (declared value). We only include values with a certainty score of 70 or above.

We assume, that for each firm, country-specific revenues reflect the importance of a country to the firm’s economy. The risk of losing revenue in a country may increase when the COVID-19 pandemic’s intensity is high. To combine both the importance of a country for a firm’s revenues and the risk of losses in a country, we calculate an indicator for firm-country-level sales revenue exposure to the pandemic. Thus, EXPOSUREi,t is the country-specific sales revenues of our sample firms [REVENUEi,c,t], weighted by country’s daily growth rates of COVID-19 cases [CASESc,t] and deaths [DEATHSc,t] per million. For instance, a high infection or death rate in a country that does not significantly contribute to a firm’s sales revenues may not be considered as a threat to that firm. The same may holds true for a country that highly contributes to the firm’s sales revenue but shows low infection rates.

The variable is then standardized using z-scores and normalized to a scale from 0 to 100, where higher values indicate a larger firm-specific revenue exposure to COVID-19. For example, a value of 100 would be related to a firm-day observation if the growth in COVID-19 cases or deaths among all firm-relevant countries is the highest in the countries that contribute most to the firm’s revenues. In the same way, a value of 0 would be related to a firm-day observation if there is no growth in COVID-19 cases or deaths among all countries that contribute to a firm’s revenues. We make the following adjustments to our regression model in Eq. (1):

where i, c, and t index firm, country, and day, respectively.

Results are presented in Table 5, where Panels A and B observe CASESc,t and DEATHSc,t, respectively, as proxies for COVID-19c,t.

In Panel A Model I, the three-way interaction reveals that the mitigating effect of summarized government responses [GOV_RESPONSEc,t], as shown previously, is even stronger for firms that are highly exposed to COVID-19 on the sales side. The coefficient is positive and significant but shows a low magnitude.

The same holds true for governmental efforts in economic support [ECON_SUPPORTc,t], presented in Model IV. In contrast, containment and closure policies [CONTAINMENT_CLOSUREc,t] (Model II) seem to be rated differently by investors in the case that a firm’s revenue is highly exposed to COVID-19. While in our main regression model with split government responses by scope, containment and closure policies mitigate stock price declines due to growing COVID-19 case numbers, they seem not strong enough to do so if a firm achieves high sales revenues in countries that are highly affected by the pandemic.

Turning to health system policies [HEALTH_SYSTEMc,t] (Model III), government support seems to be rated more positively when investors are more severely affected by the pandemic. Moreover, the additional positive effect of government health system policies for firms that are highly exposed to the pandemic (coefficient 0.033) even reverses the initial negative effect (coefficient − 0.015), where the moderation of EXPOSUREc,t was unconsidered. Thus, investors of firms with high COVID-19 revenue exposure aim for a fast recovery and positively assess health system policies, regardless of consequential restrictions. In Panel B, COVID-19c,t is represented by DEATHSc,t. For all models, the results are similarly directed. As a sole exception, we fail to find a significant three-way interaction for the economic support index.

4.5 Estimation of COVID-19 growth rates with an epidemiological standard model

In our main regression models, we employ the percentage growth rates for both COVID-19 cases and deaths to proxy for the spread of the COVID-19 pandemic. Specifically, for the increase in COVID-19 cases and deaths, we consider the growth rate of the announced cumulative number of confirmed COVID-19-positive cases per million and country and the growth rate of the announced deaths associated or caused by COVID-19 per million and country, respectively. However, this perspective assumes a linear progression of the pandemic.

In fact, as graphically visible in Fig. 1, the spread of COVID-19 can be separated into two phases: exponential growth of cases and deaths corresponding to initial global outbreaks, followed by logistic progression due to mitigated infection rates as global government responses unfold (De Silva et al. 2012). Epidemiological standard models can be used to address this nonlinearity. Comparing the performance of standard models for fast epidemics, Ma (2020) shows that the susceptible-infectious-recovered model (SIR), first published by Hethcote (1989), provides a robust estimate for the spread of a disease exhibiting a pattern similar to COVID-19. SIR assumes the immunity of recovered individuals and incorporates the number of susceptible individuals. We calculate the SIR growth rate following Ma (2020) and Furtado (2021) as

where S is the share of susceptible individuals, I is the share of infectious individuals, and R is the share of recovered individuals. ß is the transmission rate per infectious individual, and y is the recovery rate. With the total number of individuals kept constant as the sum of S, I, and R, the expected growth rate is calculated as λ = ß – y. Descriptive statistics provide a mean of 4.531%. We recalculate our regression models, substituting our measures for the spread of the disease, i.e., CASESc,t, by the SIR growth rate. Untabulated results remain congruent within all our regression models, indicating no distortion due to an imprecise, exponential fit of our COVID-19 proxies.

5 Robustness tests

5.1 Alternative benchmarks for the measurement of abnormal returns

Clearly, our study covers a worldwide economic crises that, without precedent, can be expected to systematically affect almost all sectors and firms worldwide. Thus, it is particularly important to find a benchmark for a firm’s returns that does not ignore the overarching effects of the crisis and is free of systematic influences. Thus, we employ three alternative approaches for the calculation of abnormal stock returns.

First, we recalculate our models using the daily average market return of the entire US market instead of focusing on the S&P 500. Therefore, we obtain the daily index prices of the Dow Jones U.S. Total Stock Market Index for our observation period. The index measures all US equity issues with available prices and covers 4224 firms and ten sectors. Similar to our main regression, we define the market adjustment of raw returns as \(AR_{t}^{i} = R_{t}^{i} - E\left( {R_{t}^{i} } \right)\), where \(R_{t}^{i}\) represents the daily return for firm i on day t. We estimate the firm’s expected return as \(E(R_{t}^{i} ) = \alpha_{i} + b_{i} E(R_{t}^{market} )\), with \(R_{t}^{market} = (P_{t}^{market} - P_{t - 1}^{market} )/P_{t - 1}^{market}\), where \(P_{t}^{market}\) now represents the Dow Jones US. Total Stock Market Index closing price on day t. As all estimates are statistically indistinguishable from one another, evidence is provided for our main model’s results.

Second, we apply a portfolio-based approach to incorporate firm-specific risk instead of simply observing the daily market average. Specifically, following Fama and French (1995) and Kothari and Warner (2004), we compute a firm’s abnormal returns by adjusting the total returns for factors that have been found to explain cross-sectional differences in stock returns, i.e., a firm’s market capitalization and its price-to-book ratio. Similar to Brav et al. (2000), we form a set of floating portfolios of firms, with each portfolio expressing a distinct range of firm-size, i.e., a firm’s capitalization. Within each portfolio, we rank the firms by their price-to-book ratio. Based on our ranking values, we define a weighting factor \(w_{j}\) for each ranking position. Total returns \(R_{t}^{i}\) are then adjusted by the weighted total returns with varying values for each observation day: \(AR_{t}^{i} = R_{t}^{i} - R_{t}^{i, port}\). Following Sul et al., (2014), we calculate \(R_{t}^{i}\) as the natural logarithm of total returns plus one:\(R_{t}^{i} = ln\left( {R_{t}^{i} + 1} \right)\). \({\varvec{R}}_{{\varvec{t}}}^{{{\varvec{i}},\user2{ port}}}\) therefore, can be defined as \(\frac{1}{n}\sum\nolimits_{j = 1}^{n} {w_{j} \left( {R_{t}^{i} } \right)}\), where the sum of weights in each portfolio equals 1 (\(\sum\nolimits_{j = 1}^{n} {w_{j} = 1}\)). All results remain unchanged in direction and show insignificant divergences in magnitude.

5.2 Aggregation of country-specific data on firm level

Our research design employs daily firm-country specific data. This approach carries important benefits that help to get deeper insights into the role of country-specific government responses when analyzing the pandemic’s impact on firms. Specifically, for each firm, we consider all countries worldwide that contribute to the firm’s revenues within our observation period. As a result, we split each firm into a set of pseudo-subsidiaries, with each subsidiary to solely reflect the effects of government responses of a single, distinct country on the firm’s stock prices over time.

In addition, the approach includes several country-specific control variables, e.g., media-sentiment variables, that continuously measure the spread and tone of pandemic-related news in a country. Following prior research that we discussed beforehand, they may be considered important drivers of investor sentiment.

However, a straightforward way of analyzing our dataset is to aggregate all data at the firm level. Specifically, on firm level, we weight a country’s daily COVID-19 related case and death numbers with its intensity of government responses. The result is a global variable for the overall strength of COVID-19 government policies for each firm. In this approach, again, all countries that contribute to the firm's sales revenues, are included. This calculation is blurred since it averages the country-specific government responses and the COVID-19 measures worldwide. However, it may still reinforce the robustness of our research design. We recalculate our regression models, using the aggregated data on firm level. Results remain unaffected and show similar magnitudes and directions.

5.3 Further robustness tests

We perform further robustness tests to validate the results of our regression models. First, we include country-fixed effects to control for country-level heterogeneity. Again, results remain unchanged in direction and magnitude. Second, to control for cross-effects indicating that abnormal stock returns influence government responses, we repeat all regressions using RESPONSEc,t as the dependent variable. We do not find significant results, supporting our main findings. Third, we conduct an in-time placebo test using placebo time windows to ensure that our regression results are not driven by our research design (e.g., Conley and Taber 2011; Hahn and Shi 2017). We run our main regression model shifting all independent variables back and forth 10, 15 and 30 trading days, respectively, holding our dependent variable, abnormal returns, constant. We fail to find any significant results, suggesting that, assuming no treatment effects, there is no evidence of random or systematic errors due to a weak model design. Forth, the reported results remain stable when conducting random effect regressions. Fifth, we use altering data frequencies to assure that our results are not sensitive to the daily-data approach. We aggregate all variables both weekly and monthly and rerun our main regressions. Results do not reveal divergences. Sixth, we recalculate our analysis substituting our dependent variable, abnormal returns, with raw returns. Results follow similar patterns throughout all models.

6 Conclusion

In this paper, we analyze the role of worldwide government efforts to contain the spread and the economic consequences of the COVID-19 pandemic in shaping investor sentiment and stock market reactions. We explore the impact of government responses in the three fields of containment and closure, health system policies, and economic support of 180 countries on the relationship between growth rates of COVID-19 cases and deaths and firm-specific S&P 500 abnormal stock returns in a period from 1st January 2020 to 15th March 2021. We further investigate weather investor’s behavior is sensitive to a firm’s revenue exposure to COVID-19. We employ both an exponential growth model and an epidemiological standard model to account for the different stages of the pandemic and to address the nonlinear spread of the disease.

In contrast to previous studies, we find that deaths mainly drive stock returns during the COVID-19 pandemic. Undifferentiated, the entirety of government responses mitigates the decline of stock prices as market participants appreciate governments’ efforts to contain the consequences of the pandemic. Split by the different scopes of government responses, governments may mitigate negative market impacts caused by the pandemic by taking actions in the field of containment and closure, e.g., by school closings, workplace closings, closings of public transport or issuing stay-at-home orders. Similar effects stem from government’s economic support. Government support of a country’s health system provokes further declines in abnormal stock returns.

Analyzing the moderation of a firm’s revenue exposure to COVID-19, the mitigating effect of the entirety of government responses is even stronger for firms that are highly exposed to COVID-19 on the sales side. Differentiated by scope, this holds true for the field of government economic support. Containment and closure policies do not seem strong enough for investors to adjust their pessimistic views on market development. Hence, we find no mitigation of stock price declines due to growing COVID-19 case numbers. Contrary to our initial findings, government support of health systems is rated more positively by investors when a firm is more severely affected by the pandemic on the sales side. The additional positive stock market effect for firms that are highly exposed to the pandemic even reverses the initial negative impact. These results remain unchanged when the spread of COVID-19 is estimated using an epidemiological standard model, i.e., the SIR, to account for the pandemic’s nonlinear course.

Our findings contribute to both practice and research. First, firms that become aware of both the pandemic’s impact on investor sentiment and the moderating role of government responses may be able to anticipate and strategically manage investor relations. Regarding investors’ reactions to a firm’s country-specific revenue exposure to COVID-19, firms should aim to redirect and adjust the content and scope of their communications with investors. They may also aim for a dialog with governments to encourage aid in firm-relevant fields. Second, our results are relevant for government regulators debating the economic costs and benefits of government responses to pandemics, since no case of such extent is yet known, and reliable data concerning the consequences of government interventions for medical crises are rare. Third, our study expands the knowledge about investor sentiment as a driver of stock prices during external shocks followed by crisis situations.

As with all studies, our study is limited in several ways and, as such, paves the way for future research. As we derive investor sentiment indirectly by measuring abnormal stock market reactions, qualitative studies will be necessary to more deeply investigate investors’ behavior during the COVID-19 pandemic. Although investor reactions are clearly visible, the psychological motives as well as the strength, composition, and persistence of investor reactions remain unclear and require further investigation. We analyze whether investor’s perceptions of government responses to the COVID-19 pandemic are affected by the share of sales revenues that is threatened by the pandemic in each country. However, this approach compromises several weaknesses since the linkage between the case and death development and sales revenue may not be linear. We encourage further research to build on this bias and seek for more accurate approaches to reflect the risk of losing sales revenues during pandemics. Moreover, we do not analyze whether firm characteristics other than country-specific sales revenues may mitigate or reinforce stock market reactions. For example, the exposure of worldwide supply chains may cause different effects on the stock market and, thus, should be a matter of further research. As our dataset provides firm-country-specific data, further studies may cluster countries and reveal the role of policies and measures among geographic regions or political and economical unions.

Data Availability

Data are available from commercial databases and public sources identified in the paper.

Notes

In the original dataset, Hale et al. (2020) present four indices to give an overall impression of government activity. However, these indices cover a mix of indicators from all three policy groups. To accurately reflect government responses of each policy group, we calculate our own indices, solely including indicators of the assigned group of policies.

* We also control for country-fixed (Country FE) effects as part of our robustness tests. Please see Sect. 5.

Since the COVID-19 pandemic most likely causes widespread systematic effects across firms and sectors worldwide, it is imperative to employ alternative and neutral benchmarks for calculating abnormal returns. Thus, we repeat our analysis using a portfolio-based approach to calculate abnormal returns based on firm-specific risk. In addition, we recalculate our models using the daily average market return of the entire US market instead of focusing the S&P 500. Both analyses are presented in section five (Robustness Tests).

"ESG scores by Refinitiv have been used (or referenced) in more than 1200 academic articles over the past 15 years. Moreover, Refinitiv ESG data are used by major asset managers, such as BlackRock, to manage ESG investment risks. Refinitiv ESG data are also referenced in an ESG white paper featured at the World Economic Forum in 2019 (WEF 2019), and analyzed as one of the three key ratings providers in a recent OECD report." (Boffo and Paralano 2020).

Source: RefinitivDatastream.

References

Albuquerque R, Koskinen Y, Yang S, Zhang C (2020) Resiliency of environmental and social stocks: an analysis of the exogenous COVID-19 market crash. Rev Corp Finance Stud 9(3):593–621

Alexakis C, Eleftheriou K, Patsoulis P (2021) COVID-19 containment measures and stock market returns: an international spatial econometrics investigation. J Behav Exp Finance 29:100428

Ali M, Alam N, Rizvi SAR (2020) Coronavirus (COVID-19)—an epidemic or pandemic for financial markets. J Behav Exp Finance 27:100341

Andrei D, Hasler M (2015) Investor attention and stock market volatility. Rev Finance Stud 28(1):33–72

Baker M, Wurgler J (2006) Investor sentiment and the cross-section of stock returns. J Finance 61(4):1645–1680

Baker SRN, Bloom S, Davis J, Terry SJ (2020) COVID-induced economic uncertainty. NBER Work Pap Ser

Barberis N, Shleifer A, Vishny R (1998) A model of investor sentiment. J Finance Econ 49(3):307–343

Bartov E, Faurel L, Mohanram PS (2018) Can Twitter help predict firm-level earnings and stock returns? Acc Rev 93(3):25–57

Beer F, Zouaoui M (2012) Measuring stock market investor sentiment. J Appl Bus Res 29(1):51

Boffo R, Patalano R (2020) ESG Investing: Practices Progress and Challenges. OECD. https://www.oecd.org/finance/ESG-Investing-Practices-Progress-Challenges.pdf. Accessed 10 Oct 2021

Bollen J, Mao H, Zeng X (2011) Twitter mood predicts the stock market. J Comput Sci 2(1):1–8

Brav A, Geczy C, Gompers PA (2000) Is the abnormal return following equity issuances anomalous? J Finance Econ 56(2):209–249

Broadstock DC, Chan K, Cheng LT, Wang X (2021) The role of ESG performance during times of financial crisis: evidence from COVID-19 in China. Finance Res Lett 38:101716

Brown SJ, Barry CB (1984) Anomalies in security returns and the specification of the market model. J Finance 39(3):807–815

Cen L, Liyan Y (2013) Investor sentiment disagreement and the breadth-return relationship. Manage Sci 59:1076–1091

Chau F, Deesomsak R, Koutmos D (2016) Does investor sentiment really matter? Int Rev Finance Anal 48:221–232

Chen H, De P, Hu YI, Hwang BH (2013) Customers as advisors: the role of social media in financial markets. Working Paper. Purdue University.

Cheng S (2008) Board size and the variability of corporate performance. J Finance Econ 87(1):157–176

Cohen LJ, Marcus AJ, Rezaee Z, Tehranian H (2018) Waiting for guidance: disclosure noise verification delay and the value-relevance of good-news versus bad-news management earnings forecasts. Glob Finance J 37:79–99

Conley TG, Taber CR (2011) Inference with “Difference in Differences” with a small number of policy changes. Rev Econ Stat 93(1):113–125

Cormier D, Aerts W, LeDoux M-J, Magnan M (2010) Web-based disclosure about value creation processes: a monitoring perspective. Abacus 46(3):320–347

Dai Z, Zhu H (2020) Stock return predictability from a mixed model perspective. Pac Basin Finance J 60:101267

Davison C (2020) Stock returns, leverage, and the COVID-19 pandemic. https://ssrn.com/abstract=3627595SSRN (June 15, 2020). Accessed 26 Oct 2021

de Bondt WFM, Thaler R (1985) Does the stock market overreact? J Finance 40(3):793–805

de Long JB, Shleifer A, Summers LH, Waldmann RJ (1990) Positive feedback investment strategies and destabilizing rational speculation. J Finance 45(2):379–395

De Silva E, Ferguson NM, Fraser C (2012) Inferring pandemic growth rates from sequence data. J R Soc Interface 9(73):1797–1808

Demers E, Hendrikse J, Joos P, Lev B (2020) ESG didn’t immunize stocks against the COVID-19 market crash. J Bus Finance Acc 48:433–462

Ding W, Levine R, Lin C, Xie W (2021) Corporate immunity to the COVID-19 pandemic. J Financ Econ 141(2):802–830

Engelhardt N, Krause M, Neukirchen D, Posch P (2020) What drives stocks during the Corona-Crash? News attention vs rational expectation. Sustainability 12(12):5014

Erdem O (2020) Freedom and stock market performance during COVID-19 outbreak. Finance Res Lett 36:101671

FactSet (2022) FactSet geographic revenue exposure. data feed documentation

Fama EF, French KR (1993) Common risk factors in the returns on stocks and bonds. J Finance Econ 33(1):3–56

Fama EF, French KR (1995) Size and book-to-market factors in earnings and returns. J Finance 50(1):131–155

Fang L, Peress J (2009) Media coverage and the cross-section of stock returns. J Finance 64(5):2023–2052

Funck M, Gutierrez JA (2018) Has Ebola infected the market: a contagious reaction to a (Media) Health Care Crisis? J Bus Strateg 35(2):55–75

Furtado P (2021) Epidemiology SIR with regression arima and prophet in forecasting COVID-19. Eng Proceed 5(1):52

Gennaioli N, Shleifer A, Vishny R (2015) Neglected risks: the psychology of financial crises. Am Econ Rev 105(5):310–314

Georgarakos D, Pasini G (2011) Trust sociability and stock market participation. Rev Finance 15(4):693–725

González M, Guzmán A, Téllez D, Trujillo MA (2019) Governance sentiment analysis and initial public offering underpricing. Corp Gov 27(3):226–244

Goodell JW (2020) COVID-19 and finance: agendas for future research. Finance Res Lett 35:101512

Griffin JM, Lemmon ML (2002) Book-to-market equity distress risk and stock returns. J Finance 57(5):2317–2336

Hafez P, Matas R, Grinis I, Gomez F, Kangrga M, Liu A (2020) Factor investing with sentiment: a look at asia-pacific markets. RavenPack Quant Research

Hahn J, Shi R (2017) Synthetic control and inference. Econometrics 5(4):52

Hale T, Angrist N, Goldszmidt R et al (2021) A global Panel database of pandemic policies (Oxford COVID-19 Government Response Tracker). Nat Hum Behav 5:529–538

He W, Hong KH, Wu AE (2020) Does investor sentiment affect the value relevance of accounting information? Abacus 56(4):535–560

Hethcote HW (1989) Three basic epidemiological models. In: Levin S et al (eds) Applied mathematical ecology. Springer, New York, pp 119–144

Hong H, Stein JC (1999) A Unified theory of underreaction momentum trading and overreaction in asset markets. J Finance 54(6):2143–2184

Hong H, Stein JC (2007) Disagreement and the stock market. J Econ Perspect 21(2):109–128

Hong H, Kubik JD, Solomon A (2000) Security analysts’ career concerns and herding of earnings forecasts. Rand J Econ 31(1):121

Hu S, Zhang Y (2021) COVID-19 pandemic and firm performance: cross-country evidence. Int Rev Econ Finance 74:365–372

Ichev R, Marinč M (2018) Stock prices and geographic proximity of information: evidence from the Ebola outbreak. Int Rev Finance Anal 56:153–166

Jain PC (1986) Analyses of the distribution of security market model prediction errors for daily returns data. J Acc Res 24(1):76–96

Jiang Y, Zhang Y, Ma C, Wang Q, Xu C, Donovan C, Ali G, Xu T, Sun W (2017) H7N9 not only endanger human health but also hit stock marketing. Adv Dis Control Prev 2(1):1–7

Jiang B, Zhu H, Zhang J, Yan C, Shen R (2021) Investor sentiment and stock returns during the COVID-19 pandemic. Front Psychol 12:708537

Jung MJ, Naughton JP, Tahoun A, Wang C (2018) Do firms strategically disseminate? Evidence from corporate use of social media. Acc Rev 93(4):225–252

Kaniel R, Saar G, Titman S (2008) Individual investor trading and stock returns. J Finance 63(1):273–310

Kothari S, Warner JB (2004) The econometrics of event studies. SSRN Electron J

Kraft J, Kraft A (1977) Determinants of common stock prices: a time series analysis. J Finance 322:417–425

Lesmeister S, Limbach P, Goergen M (2018) Trust and shareholder voting European Corporate Governance Institute (ECGI)-Finance. CFR Working Paper No. 18-02

Liu H, Manzoor A, Wang C, Zhang L, Manzoor Z (2020) The COVID-19 outbreak and affected countries stock markets response. Int J Environ Res Public Health 17(8):2800

Liu Z, Huynh TLD, Dai PF (2021) The impact of COVID-19 on the stock market crash risk in China. Res Int Bus Finance 57:101419

Ma J (2020) Estimating epidemic exponential growth rate and basic reproduction number. Infect Dis Model 5:129–141

Michayluk D, Neuhauser KL (2006) Investor overreaction during market declines: evidence from the 1997 Asian Financial Crisis. J Financ Res 29(2):217–234

Miller GS, Skinner DJ (2015) The evolving disclosure landscape: how changes in technology the media and capital markets are affecting disclosure. J Acc Res 53(2):221–239

Palomino F (1996) Noise trading in small markets. J Finance 51(4):1537–1550

Pontiff J, Schall LD (1998) Book-to-market ratios as predictors of market returns. J Finance Econ 49(2):141–160

Refinitiv (2020) Environmental social and governance (ESG) Scores from Refinitiv. https://www.refinitiv.com/content/dam/marketing/en_us/documents/methodology/esg-scores-methodology.pdf. Accessed 10 Oct 2021.

Salisu AA, Vo XV (2020) Predicting stock returns in the presence of COVID-19 pandemic: the role of health news. Int Rev Finance Anal 71:101546

Sharpe W (1963) A simplified model for portfolio selection. Manag Sci 9:277–293

Shleifer A, Vishny RW (1997) The limits of arbitrage. J Finance 52(1):35–55

Smirlock M, Starks L (1988) An empirical analysis of the stock price-volume relationship. J Bank Finance 12(1):31–41

Sul H, Dennis AR, Yuan LI (2014) Trading on Twitter: the financial information content of emotion in social media. Decis Sci 454–87

Sun Y, Wu M, Zeng X, Peng Z (2021) The impact of COVID-19 on the Chinese stock market: sentimental or substantial? Finance Res Lett 38:101838

Tetlock PC (2007) Giving content to investor sentiment: the role of media in the stock market. J Finance 62(3):1139–1168

Wang YH, Yang FJ, Chen LJ (2013) An investor’s perspective on infectious diseases and their influence on market behavior. J Bus Econ Manag 14:112–127

Whaley RE (2009) Understanding the VIX. J Portf Manag 35(3):98–105

Zaremba A, Kizys R, Aharon DY, Demir E (2020) Infected markets: novel coronavirus government interventions and stock return volatility around the globe. Finance Res Lett 35:101597

Zhang D, Hu M, Ji Q (2020) Financial markets under the global pandemic of COVID-19. Finance Res Lett 36:101528

Funding

Open Access funding enabled and organized by Projekt DEAL. For this study, no funding has been received.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflicts of interest.

Research involving human participants and/or animals

This article does not contain any studies with human participants or animals performed by any of the authors.

Informed consent

No humans are involved.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1

Country-specific S&P 500 firm allocation

No | Country | Number of Firms | Share of S&P 500 | No | Country | Number of Firms | Share of S&P 500 |

|---|---|---|---|---|---|---|---|

1 | Afghanistan | 154 | 30.14 | 51 | El Salvador | 195 | 38.16 |

2 | Albania | 190 | 37.18 | 52 | Eritrea | 44 | 8.61 |

3 | Algeria | 251 | 49.12 | 53 | Estonia | 249 | 48.73 |

4 | Andorra | 9 | 1.76 | 54 | Ethiopia | 234 | 45.79 |

5 | Angola | 237 | 46.38 | 55 | Faroe Islands | 9 | 1.76 |

6 | Argentina | 289 | 56.56 | 56 | Fiji | 17 | 3.33 |

7 | Aruba | 21 | 4.11 | 57 | Finland | 308 | 60.27 |

8 | Australia | 312 | 61.06 | 58 | France | 331 | 64.77 |

9 | Austria | 316 | 61.84 | 59 | Gabon | 136 | 26.61 |

10 | Azerbaijan | 223 | 43.64 | 60 | Gambia | 2 | 0.39 |

11 | Bahamas | 103 | 20.16 | 61 | Georgia | 198 | 38.75 |

12 | Bahrain | 220 | 43.05 | 62 | Germany | 334 | 65.36 |

13 | Bangladesh | 283 | 55.38 | 63 | Ghana | 226 | 44.23 |

14 | Barbados | 40 | 7.83 | 64 | Greece | 303 | 59.30 |

15 | Belarus | 278 | 54.4 | 65 | Guam | 20 | 3.91 |

16 | Belgium | 320 | 62.62 | 66 | Guatemala | 249 | 48.73 |

17 | Belize | 12 | 2.35 | 67 | Guinea | 114 | 22.31 |

18 | Benin | 123 | 24.07 | 68 | Guyana | 45 | 8.81 |

19 | Bermuda | 47 | 9.2 | 69 | Haiti | 64 | 12.52 |

20 | Bhutan | 13 | 2.54 | 70 | Honduras | 184 | 36.01 |

21 | Bolivia | 232 | 45.4 | 71 | Hungary | 310 | 60.67 |

22 | Bosn. & Herzeg | 206 | 40.31 | 72 | Iceland | 226 | 44.23 |

23 | Botswana | 149 | 29.16 | 73 | India | 310 | 60.67 |

24 | Brazil | 305 | 59.69 | 74 | Indonesia | 279 | 54.60 |

25 | Brunei Darussalam | 102 | 19.96 | 75 | Iran | 269 | 52.64 |

26 | Bulgaria | 284 | 55.58 | 76 | Iraq | 264 | 51.66 |

27 | Burkina Faso | 135 | 26.42 | 77 | Ireland | 322 | 63.01 |

28 | Burundi | 12 | 2.35 | 78 | Israel | 275 | 53.82 |

29 | Cabo Verde | 2 | 0.39 | 79 | Italy | 325 | 63.60 |

30 | Cambodia | 194 | 37.96 | 80 | Jamaica | 131 | 25.64 |

31 | Cameroon | 207 | 40.51 | 81 | Japan | 315 | 61.64 |

32 | Canada | 350 | 68.49 | 82 | Jordan | 222 | 43.44 |

33 | Cent. Afr. Rep | 2 | 0.39 | 83 | Kazakhstan | 262 | 51.27 |

34 | Chad | 98 | 19.18 | 84 | Kenya | 237 | 46.38 |

35 | Chile | 287 | 56.16 | 85 | Kiribati | 1 | 0.20 |

36 | Colombia | 288 | 56.36 | 86 | Kuwait | 258 | 50.49 |

37 | Congo | 92 | 18 | 87 | Kyrgyzstan | 73 | 14.29 |

38 | Costa Rica | 244 | 47.75 | 88 | Laos | 168 | 32.88 |

39 | Cote d'Ivoire | 222 | 43.44 | 89 | Latvia | 260 | 50.88 |

40 | Croatia | 283 | 55.38 | 90 | Lebanon | 232 | 45.40 |

41 | Cuba | 246 | 48.14 | 91 | Lesotho | 5 | 0.98 |

42 | Cyprus | 229 | 44.81 | 92 | Liberia | 7 | 1.37 |

43 | Czech Republic | 315 | 61.64 | 93 | Libya | 218 | 42.66 |

44 | Denmark | 312 | 61.06 | 94 | Liechtenstein | 93 | 18.20 |

45 | Djibouti | 10 | 1.96 | 95 | Lithuania | 280 | 54.79 |

46 | Dominica | 4 | 0.78 | 96 | Luxembourg | 293 | 57.34 |

47 | Dom. Republic | 245 | 47.95 | 97 | Madagascar | 122 | 23.87 |

48 | DR of the Congo | 216 | 42.27 | 98 | Mainland China | 324 | 63.41 |

49 | Ecuador | 262 | 51.27 | 99 | Malawi | 55 | 10.76 |

50 | Egypt | 272 | 53.23 | 100 | Malaysia | 281 | 54.99 |

101 | Mali | 141 | 27.59 | 151 | Sudan | 187 | 36.59 |

102 | Malta | 193 | 37.77 | 152 | Suriname | 27 | 5.28 |