Abstract

We assess whether and how VC investors’ education and experience influence their screening decisions of potential investee candidates. Empirically, we perform an experimental choice-based-conjoint (CBC) analysis with 564 individual VC investors. Our results highlight that the level and field of education, as well as the decision maker’s investment and entrepreneurial experience, moderate the relative importance of different screening criteria. More specifically, we find that international scalability seems to become more important for decision makers with higher education and those with entrepreneurial experience. Whereas decision makers with a background in natural science focus on the value-added of the product or service, engineers seem to value a break even profitability and focus less on the management team. Investment experience, on the other hand, leads to a stronger focus on the management team. Our study contributes to the literature investigating the influence of human capital characteristics of the decision maker in venture financing. Practical implications exist for entrepreneurial ventures seeking financing and for risk capital investors making investments in such ventures.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Management research comprehensively documents that strategic decisions of companies are affected by the human capital of the individuals in charge (e.g., Datta and Iskandar-Datta 2014; Hambrick et al. 1996; Hambrick and Mason 1984; Wang et al. 2016). Extending these arguments to the context of venture capital (VC), prior studies argue that VC investors’ experience and expertise influence their venture evaluation processes (e.g., Dimov et al. 2007; Dimov and Shepherd 2005; Franke et al. 2008; Shepherd et al. 2003).

A large number of studies identify important screening criteria of VC investors when assessing entrepreneurial ventures such as management team characteristics, product characteristics, as well as market and industry factors (e.g., Block et al. 2021; Franke et al. 2008; Gompers et al. 2020; Hoenig and Henkel 2015; Hsu et al. 2014; Shepherd et al. 2003; Warnick et al. 2018). However, little is known about how the importance of these criteria varies due to the individual characteristics of the decision maker, such as education and experience. Since the vast majority of venture proposals are rejected in the screening phase where a single decision maker typically screens the venture (e.g., Block et al. 2019; Gompers et al. 2020), an understanding of the importance of different screening criteria used, and, in particular, how and whether the importance is influenced by the decision maker’s individual characteristics is crucial (e.g., Dimov and Shepherd 2005).

We tap into this research gap by exploring how VC investor’s education and experience influence the importance of different screening criteria. While prior research argues that education provides the knowledge base as well as analytical and problem-solving skills, experience enables decision makers to focus on key dimensions and ignore less important variables (Shepherd et al. 2003; Watson et al. 2003). For example, an education in business has been associated with risk-averse behavior and a stronger focus on financials (Carpenter et al. 2004; Slater and Dixon-Fowler 2010). Besides, experience affects the ability to identify promising startups and detect opportunistic behavior (Dimov and Shepherd 2005; Scarlata et al. 2016; Walske and Zacharakis 2009; Zarutskie, 2010). However, it is an open question of how the education and experience of the individual VC decision maker affect the screening criteria to identify potential portfolio companies. Therefore, the following research question is at the core of our study: How does the decision maker’s level and field of education as well as his/her investment and entrepreneurial experience influence the relative importance of different screening criteria while identifying potential portfolio ventures?

Our study is exploratory because the effects of education and experience on the relative importance of different screening criteria are not easy to predict. We develop and conduct an experimental choice-based-conjoint (CBC) analysis that uses seven screening criteria that are important in the screening phase of a potential VC investment (e.g., Block et al. 2019). Our sample comprises 564 individual VC investors. The results identify revenue growth, value-added of the product or services, track record of the management team, and international scalability as the most important screening criteria. Profitability, the business model, and the current investors of the firm seem to be of lower importance. However, our results highlight that the relative importance attributed to the different screening criteria is moderated by the decision maker’s education and experience. Whereas the importance of international scalability seems to increase with an increased level of education, the importance of current profitability decreases. Regarding the field of education, our findings indicate that decision makers with an engineering background prefer startups with break even profitability and focus less on the management team. In contrast, those with a natural science background are particularly interested in the value-added of the product or service and those with a business education seem to value the ease of international scalability less. Decision makers with a high degree of investment experience value the track record of the management team particularly high while decision makers with entrepreneurial experience seem to put more weight on the international scalability of the business.

With these results, we contribute to the literature on how decision makers differ in their assessment of ventures (e.g., Franke et al. 2008; Shepherd et al. 2003). We show that the two individual human capital characteristics education and experience of the decision maker can help to explain some of these differences. More specifically, we add to prior research on experience in the VC context by showing that the prior investment and entrepreneurial experience of the decision maker affect the importance of different screening criteria (Franke et al. 2008; Scarlata et al. 2016; Shepherd et al. 2003; Walske and Zacharakis 2009; Zarutskie 2010). Furthermore, we connect the literature on the consequences of the field of education (Ghoshal 2005; Hambrick and Mason 1984; Slater and Dixon-Fowler 2010) with the venture screening context. And third, we contribute to the literature on the screening criteria of risk capital investors (for recent studies see Block et al. 2021; Gompers et al. 2020; Hoenig and Henkel 2015; Hsu et al. 2014; Warnick et al. 2018) by investigating ventures in their growth and expansion stage where additional criteria become available.

Our study is also of practical relevance. Our results inform entrepreneurial ventures about which criteria matter for obtaining VC financing. In particular, revenue growth, value-added of the product, and the management team seem to play an important role in this regard. VC investors can use these results to benchmark their screening criteria against the market. This study can also help them to identify potential biases regarding the screening criteria resulting from the education and experience of their decision makers.

2 Theoretical background

2.1 Venture evaluation process and investor’s screening criteria

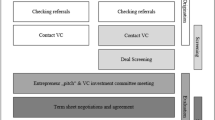

VC investors typically assess new venture proposals in a multistage evaluation process (Gompers et al. 2020; Tyebjee and Bruno 1984). In the initial screening phase, investors [who could be a senior partner, a junior partner, an associate, or a junior analyst, depending on the size of the VC (Gompers et al. 2020)] aim to drastically reduce the number of proposals and focus only on those proposals which match the VC’s broad screening criteria and preferences (Dimov et al. 2007; Franke et al. 2008). After overcoming this crucial hurdle, the investor typically invites the venture’s management team for a personal meeting to present the investment opportunity to other members of the VC firm. If the members of the VC team are convinced after this meeting, the investment proposal will typically be evaluated by (other) partners of the VC firm before a formal process of due diligence is initiated (Petty and Gruber 2011). If the venture passes this due diligence process, a decision to invest is made (Gompers et al. 2020).

While Petty and Gruber (2011) find that around 20% of the venture proposals make it through the screening phase, Gompers et al. (2020) state that around 99% of venture proposals are already rejected in this phase. At this stage, only one individual member of the firm usually screens the venture (Gompers et al. 2020) and relies on a relatively small set of decision criteria (Zacharakis and Meyer 1998). These criteria change as the evaluation process progresses so that the decision criteria and their respective weight differ by evaluation stage (Gompers et al. 2020; Kollmann and Kuckertz 2010; Petty and Gruber 2011).

Numerous studies investigate the screening criteria of risk capital investors. We summarize the main findings of this research in Table 1. In summary, the most important screening criteria include the entrepreneur and the management team (e.g., Franke et al. 2006, 2008; Warnick et al. 2018), product and service offerings (e.g., Hoenig and Henkel 2015; Tyebjee and Bruno 1984), as well as the industry and market environment (e.g., Kollmann and Kuckertz 2010; Bachher and Guild 1996). Financial criteria, including venture performance measures, have been found to only play a minor role in the screening decision (e.g., MacMillan et al. 1987; Muzyka et al. 1996; Tyebjee and Bruno 1984).

2.2 The influence of education and experience on venture capitalists’ decision making

Prior research shows that decision makers’ human capital characteristics, such as education and experience, directly affect their belief structures, attitudes, and, ultimately, their decisions (e.g., Becker 1964; Hambrick and Mason 1984). More specifically, research shows that education and experience are important to develop knowledge structures and rules which help individuals to make decisions and influence how they evaluate opportunities (Shane et al. 2003; Walsh 1995; Wood and Williams 2014). Prior research typically distinguishes between level and field of education as well as the amount and type of experience as determinants for decision making.

2.2.1 Education and venture capital decision making

The level of education typically refers to the attained level of formal education as indicator of an individual’s cognitive abilities (e.g., Hambrick and Mason 1984; Hitt and Tyler 1991; Pelled 1996; Wiersema and Bantel 1992). Individuals are boundedly rational, and their ability to handle multiple and complex decision criteria is constrained by their cognitive abilities (March and Simon 1958). Higher levels of education are also indicative of more abstract ways of thinking and problem-solving skills (Gibbons and Johnston 1974; Wiersema and Bantel 1992). Also, higher levels of education could result in more specialized and focused cognitive models (Hitt and Tyler 1991). For example, individuals with a higher level of formal education have higher awareness and receptiveness for innovation (Bantel and Jackson 1989; Hambrick and Mason 1984; Wiersema and Bantel 1992). Notably, this difference seems to be associated less with the specific knowledge or techniques learned during formal education than with a more general ability to confront complex situations.

Focusing on the field of education, individuals with different educational backgrounds develop different knowledge bases and have different skill sets (Gruber et al. 2013; Unger et al. 2011). Hence, the field of study chosen reflects the personality and shapes the perspectives of an individual (Wiersema and Bantel 1992; Woolnough 1994). The acquired knowledge can either be more general or more specific depending on the chosen subject (Dimov and Shepherd 2005; Zarutskie 2010). For example, specific education in business schools might result in less innovative and less risk-prone behavior (Ghoshal 2005; Slater and Dixon-Fowler 2010). The consequence is that decision makers with such an education try to avoid big losses or mistakes (Hambrick and Mason 1984) and focus more strongly on financials and more specifically on profit maximization (Ghoshal 2005; Slater and Dixon-Fowler 2010). In the context of VC research, having an MBA might harm fund performance (Zarutskie 2010). On the other hand, having an engineering or natural sciences background has been argued to be more product-focused and task-related (Gruber et al. 2013; Hambrick and Mason 1984; Wiersema and Bantel 1992). Furthermore, a more general education, such as an education in humanities, results in a lower ability to detect specific risks but, at the same time, helps to facilitate the integration and accumulation of new knowledge (Dimov and Shepherd 2005; Gimeno et al. 1997; Zarutskie 2010).

In summary, prior literature shows that both the level and field of education influence decision makers’ cognitive abilities and knowledge structures and hence, influence their decision making behavior.

2.2.2 Experience and venture capital decision making

A large amount of prior research investigates the influence of experience on decision making behavior (e.g., Bonner 1990; Gibbons and Waldman 2004; Reuber 1997). This research finds that experience shapes decision makers’ risk-taking behavior by affecting their use of heuristics and mental shortcuts but also triggers biases such as overconfidence (Parhankangas and Hellström 2007; Shepherd et al. 2003; Sitkin and Pablo 1992). In particular, task-specific experience provides tacit knowledge, domain familiarity, and the skill-set to make evaluated decisions and achieve higher performance (Dimov and Shepherd 2005; Gibbons and Waldman 2004; McEnrue 1988; Reuber 1997).

In the context of VCs, investment experience helps investors to develop an accurate perception of risk, return, and investment opportunities (Dimov and Shepherd 2005; Scarlata et al. 2016; Walske and Zacharakis 2009; Zarutskie 2010). With an increased investment experience, they become more secure in their ability to make decisions on portfolio companies (MacMillan et al. 1987; Shepherd et al. 2003). In this context, Franke et al. (2008) show that novice and experienced VC decision makers differ in their evaluation of ventures’ team characteristics.

Task-specific experience in the context of VCs can also be related to a decision maker’s experience as an entrepreneur. Prior research argues that entrepreneurial experience shapes an individual’s cognitive models and opportunity recognition behavior (Baron and Ensley 2006; Delmar and Shane 2006). More specifically, prior entrepreneurial experience affects the evaluation of entrepreneurial opportunities such as newness or profitability (Baron and Ensley 2006; Shane et al. 2003). Hence, VC decision makers with own entrepreneurial experience have been argued to evaluate startups differently than VC decision makers without this specific experience (Zarutskie 2010). Also, prior research shows that entrepreneurial experience affects the ability to identify promising startups (Walske and Zacharakis 2009; Zarutskie 2010) and to detect opportunistic behavior (Scarlata and Alemany 2009; Walske and Zacharakis 2009).

In summary, while education provides the knowledge base as well as analytical and problem-solving skills, task-specific experience enables decision makers to focus on key dimensions and ignore less important variables (Shepherd et al. 2003; Watson et al. 2003). By combining education and experience in their cognitive structure, decision makers create schemata that enable them to form an opinion (Franke et al. 2008; Matlin 2005). Based on these results, we expect that decision makers’ level and field of education as well as their investment and entrepreneurial experience shape their schemata and influence their evaluation of different screening criteria.

3 Method, data, and variables

3.1 Identifying screening criteria through prior literature and expert interviews

To identify a list of screening criteria used by VC investors, we first derived a list of possible criteria from prior research. We then conducted 19 expert interviews with risk capital investors from Europe and North America to identify their most relevant investment criteria. The interviews were transcribed and coded by two researchers to identify the most relevant criteria, which formed the basis of the conjoint study. We triangulated the findings from the interviews with archival data such as the investor’s websites and with informal expert interviews.

Table 2 reports the most frequently mentioned criteria used by risk capital investors in their initial screening of ventures and their operationalization in our conjoint study. These criteria are (1) revenue growth, (2) profitability, (3) track record of management team, (4) current investors, (5) business model, (6) value-added of the product or service, and (7) international scalability.

3.2 Type of conjoint study and experimental design

To evaluate the importance attached to the different screening criteria, we conducted a quantitative conjoint study. Our experimental approach and the main dataset used are the same as described in Block et al. (2019). Yet, the research question, sample, and analysis of this study differ substantially.

We use a choice-based-conjoint (CBC) analysis, in which the participants are presented with two ventures and are asked to select the one venture that better matches their investment preferences. We chose a CBC approach because market participants come to a discrete decision (“yes” or “no”; “go further” or “reject”) within their actual screening activities to decide which ventures to investigate further and which to eliminate (Boocock and Woods 1997; Fried and Hisrich 1994; Tyebjee and Bruno 1984).

To enable a holistic assessment of the proposed ventures by our respondents, our CBC presents all attributes from Table 2. Because the number of possible attribute combinations would create too many choice tasks that could not be handled by the participants, we use a reduced conjoint design (Chrzan and Orme 2000; Kuhfeld et al. 1994). The reduced conjoint design was used to create 800 different experimental designs, from which the participants had to complete 13 random choice tasks. For each task, participants must decide which of the alternative ventures presented they prefer. Additionally, each participant was asked to complete two fixed choice tasks. The two fixed tasks are identical for all participants and do not rely on an experimental design in order to test the retest reliability of participants.

Research indicates that participants in a conjoint experiment should not be exposed to more than 20 choice tasks (Johnson and Orme 1996). A pretest with four researchers and four investors revealed that 13 random and 2 fixed choice tasks constitute an adequate length. The pretesters also confirmed our selection of criteria and the particular scales to be an appropriate portrayal of screening decisions.

To avoid biases through order effects, which may occur in conjoint studies, we randomized the order of the choice tasks and the order of options within each task (i.e., the order of the attributes). Although the order of tasks and options is randomized between participants, it is consistent for each individual.

3.3 Choice tasks and survey on the characteristics of the decision maker

The set of choice tasks presented to each respondent was prefaced by a short description, which clarified that every venture presented is supposed to match the investor’s geographical, industrial, and investment size preferences. The description also clarified that the target ventures are in later stages. That is, the target ventures have passed the start-up stage and are not yet in a maturity or bridge stage. Instead, the ventures are in a stage of early growth or expansion. We further clarified that the ventures already have market traction, a validated business model, multiple paying customers, growth in sales and customers, and multiple employees. Additionally, we described the ventures that participants could choose from as all being active in the same industry and as having the same level of revenues. This keeps the variables constant across participants. The introductory slide is displayed in Fig. 5 (Appendix). Then, participants were told that they would be confronted with two different ventures from which they should choose the one that best matches their investment preferences. The two ventures are described in terms of the identified screening criteria (“attributes”) and only differ from each other in the respective specification of these criteria (“attribute levels”).

We conducted a pretest with four investors and four scientists to check the face validity of the attributes and the attribute levels as well as the complexity of the choice task. Figure 6 (Appendix) shows an example of a choice task that the participants were confronted with.

After completing the choice tasks, participants were asked to complete a survey about the characteristics of the decision maker and the investment company. The survey collected detailed information on the level and field of education, entrepreneurial experience, and investment experience of the decision maker.Footnote 1

3.4 Variables

3.4.1 Conjoint experiment variables

To assess the attributes’ importance, we construct a dummy variable for each attribute level that takes a value of “1” if the respective attribute level is shown as a characteristic of the particular venture. For example, if in a choice task a venture’s profitability is stated to be “break even”, the dummy variable “Profitability: break even” takes a value of “1” while the other variables of this attribute (i.e., “Profitability: profitable” and “Profitability: not profitable”) both take a value of “0”.

Our dependent variable “preference of the decision maker” determines whether a venture was selected by the respondent or not. The variable takes a value of “1” if the investor prefers the venture that is shown and “0” if s/he chooses the alternative venture. This allows us to perform logistic regressions that assess whether certain attribute levels increase or decrease the probability that a venture is selected by an investor.

3.4.2 Education, entrepreneurial experience, and investment experience variables

To measure the level of education, participants indicated their highest formal educational degree. We constructed three dummy variables that represent each level of education: “Bachelor’s degree”, “Master’s degree or MBA”, and “PhD or doctoral degree”. Participants were further asked to indicate their main field of study, which we used to construct dummy variables to distinguish the respondents’ educational background. Hence, the variables “Business”, “Natural science” and “Engineering” take a value of “1” if the respondent has been educated solely in the respective field and a “0” otherwise.

To capture the investors’ entrepreneurial experience, we asked the participants if they have started their own company and, if yes, how many companies they have founded. We created two dummy variables with this information. The variable “Entrepreneur” takes a value of “1” if the investor started at least one company and “0” otherwise. The variable “Serial entrepreneur” takes a value of “1” if the investor stated to have founded more than one company and “0” if she/he has founded only one company or no company at all. Finally, we distinguish between experienced and inexperienced investors by asking how many years they have worked as investors. The variable “Investment experience high” takes a value of “1” if the investor stated to have worked as an investor for eight years or more, and “0” for less than eight years. Eight years is the median experience in our sample.

3.5 Sample

We collected information on potential investors from Pitchbook at the beginning of 2016. Pitchbook is one of the most comprehensive VC databases and provided 15,600 addresses of individual decision makers who had invested in ventures in the growth or expansion stage at least once in the past. The participants were invited via email to participate in our conjoint experiment. We sent three reminders over five months and the data collection concluded at the end of 2016. We used a two-fold approach to ensure the participation of only those decision makers who have experience in growth venture financing. First, Pitchbook offers the ability to filter for investors that have done deals in certain stages. Hence, we only contacted decision makers that were involved in at least one venture financing deal in the last ten years since 2016 that was classified as series A, B, C, D, or expansion. Second, the invitation mail to our conjoint experiment asked decision makers to only participate if they have experience in later-stage venture financing. To make our understanding of the ventures as transparent as possible to respondents, we included an introductory slide outlining our understanding of later-stage ventures (Fig. 5, Appendix).

In total, 749 individuals participated in our conjoint experiment accounting for 19,474 recorded decisions (response rate = 6.24%). Because the respondents were told that the presented ventures in the choice tasks match their usual geographical, industrial, and investment size preferences, the experiment bears the danger that the investors evaluate the ventures differently, based on their industry focus. To decrease this problem, our analyses use a more homogeneous subsample. First, we only include investors that are exclusively active in IT-related industries such as “Software & services”, “IT infrastructure or systems”, or “E-Commerce”. Investors that invest, for example, in “Biotech” or “Consumer products” are excluded (N = 188). In addition, we exclude investors working for corporate venture capital funds, leveraged buyout funds, family offices, business angels, and debt funds (N = 160) because different types of investors follow distinctive investment strategies (Block et al. 2019). Furthermore, because we focus on investors that have experience in later stage investments, all investors that stated to exclusively invest in seed and/or early stages were excluded (N = 157). To ensure that the sample contains only investors with a formal education in a certain field, we excluded those participants whose highest educational degree is below a bachelor’s degree (N = 3). In the last step, we dropped those investors whose field of education could not be identified clearly (N = 12). Our final sample consists of 229 investors and 5954 decisions. On average, each choice task took the participants 21 s to complete.

Table 3 provides a descriptive overview of our sample. The majority of the participants are male (90%) and between 35 and 54 years old (53%). Regarding participants’ level of formal education, 24% have a bachelor’s degree, while 67% have a master’s degree or an MBA. The remaining 8% hold a PhD or a doctoral degree. The majority of respondents have an educational background exclusively in business or economics (62%). 7% have a background exclusively in natural sciences and 9% exclusively in engineering. The remaining 22% received an education in multiple fields (e.g., in business/economics and engineering). The average investment experience is 11 years. Regarding the current position within the investment firm, most respondents in our sample are partners or CEOs (49%). About 17% are currently employed as directors or principals, 19% as analysts, and 15% as investment managers. 49% of the participants are working for independent VCs and 51% are working for growth equity funds. Concerning the geographical distribution of decision makers, the largest group indicated to have their headquarter in Europe (49%), followed by North America (29%). The remaining investors are headquartered in Asia (5%), South America (1%), Oceania or another region (15%).

We find no evidence of a late-response or non-response bias with regard to important descriptive variables (e.g., age, position in the firm). In addition, the two fixed tasks were used to test the retest reliability of participants’ choices in the study. By assessing the ability of the 13 random choice tasks to predict the two fixed choice tasks, a proxy for this retest reliability can be estimated. This leads to a 79% accuracy rate, which is in line with prior studies (Shepherd 1999b).

4 Results

We analyze the importance of the screening criteria by employing a logit model. This approach allows us to initially assess the relative importance of all criteria and of several subsamples that display the importance of the criteria for certain groups such as investors with a bachelor’s degree or with an education solely in engineering.

The screening decision made by participants (1 = chosen; 0 = not chosen) defines the dependent variable. We use different attribute levels as independent variables. Because our observations are hierarchically structured and nested within the individuals (multiple decisions are made by one individual, therefore the observations are not completely independent), we use multilevel regressions (Aguinis et al. 2013).

The results in Table 4 show the main effects in the full sample. The model demonstrates that all attribute levels significantly influence the decision of the investor (p < 0.01) except for the criterion current investor: external investors—unfamiliar to you. The log odds of 1.918 in the full sample model indicate that revenue growth is the most important criterion for the overall sample, followed by the value-added of the product or service (log odds = 1.495), the track record of the management team (log odds = 1.125), the international scalability (log odds = 0.940), the profitability (log odds = 0.876), the business model (log odds = 0.661) and the current investor (log odds = 0.485). To investigate the influence of education and experience, the results of the subsamples are further described in Sects. 4.1 and 4.2.

4.1 Effects of investor education on selection criteria importance

We split our full sample into six subsamples, distinguishing between the level of education (Bachelor, Master, PhD) and field of education (Business, Natural Science, Engineering). The full results for each model are displayed in the Appendix (Table 7). To facilitate interpretation, we calculate the relative importance of the different attributes for each subsample and introduce those in Figs. 1 and 2. Figure 1 shows the relative importance for each attribute separated into subsamples depending on the investors’ level of education. Additionally, we incorporate the attributes’ relative importance of the full sample for reference.

Relative importance of attributes: Level of education. Calculated based on the coefficients of the main models (Tables 4, 7). Reading example: With a relative importance of 27.74%, investors with a bachelor’s degree consider revenue growth to be more than four times as important as the criterion current investors (relative importance: 6.54%). This value also signifies that the criterion revenue growth accounts for 27.74% of the decision maker’s total utility

Relative importance of attributes: Field of education. Calculated based on the coefficients of the main model (Tables 4, 7). Reading example: With a relative importance of 29.95%, engineers consider revenue growth to be more than three times as important as the criterion business model (relative importance: 9.49%). This value also signifies that the criterion revenue growth accounts for 29.95% of the decision maker’s total utility

The graphical illustration unveils certain patterns. First, an increasing level of education seems to decrease the importance of revenue growth and profitability. While investors with a bachelor’s degree attribute more than a quarter of the explained utility to the venture’s revenue growth (27.74%), the importance drops to 25.73% for investors with a master’s degree and 20.22% for investors with a PhD. This effect seems to be even stronger for the venture’s profitability. Investors holding a bachelor’s degree attribute 13.84% of the explained utility to profitability. For investors holding a master’s degree, the importance drops to 11.85%, and investors with a PhD attribute only 4.37% of the explained utility to profitability, making it their least important criterion. The opposite effect is found for the attribute international scalability, where a higher level of education seems to increase the importance. While investors holding a bachelor’s degree attribute 7.48% of the relative importance to the international scalability, the importance almost doubles for investors with a master’s degree (13.67%) and takes a value of 17.33% for investors with a PhD.

Figure 2 shows the relative importance of the attributes while distinguishing between the investors’ field of education. First, Fig. 2 shows that the venture’s revenue growth is the most important criterion for investors solely educated in engineering (29.95%) and investors solely educated in business (24.01%). With a relative importance of 27.72%, the value-added of the product or service is slightly more important than the revenue growth (26.43%) to investors solely educated in natural sciences. Notably, engineers (7.68%) and natural scientists (9.09%) rank the importance of the management team relatively low, compared to investors with a pure business background (15.69%). With a relative importance of 17.47%, engineers attribute more importance to a venture’s capability to scale internationally, whereas the importance of international scalability is lower for natural scientists (13.58%) and investors with a background in business (10.82%). Additionally, we find that investors with a background in engineering attribute a very low importance to the current investors (2.42%), compared to natural scientists (6.59%) and investors with a business background (7.09%). Nevertheless, as shown in Table 4, the current investors do not seem to have a significant effect on the investors’ decision.

To show that the differences we find in the main effects are robust and statistically significant, we then include interaction effects in our models. All attribute level dummies in Table 5 include interactions with the dummy variable indicated on top of the columns, comparing certain investors with the remaining sample.

Model (1) in Table 5 shows the difference between investors that hold a bachelor’s degree and all other investors. In line with our main effects, we find that investors with a comparably low level of education attribute significantly less importance to an easy international scalability. While we cannot find significant differences in Model (2) (investors holding a master’s degree), Model (3) shows that investors holding a PhD attribute significantly less importance to the profitability of the venture. Furthermore, the interaction models show that investors with a PhD attribute significantly more importance to innovation-centered business models compared to investors without a PhD.

With regard to the field of education, we find that investors who have an education solely in business or economics attribute significantly less importance to the ease of the venture’s international scalability. Furthermore, the interaction effects confirm that investors who have an education solely in natural sciences rate the value-added of the product or service significantly higher than all other investors. In addition, we find that investors who have solely been educated in engineering put a significantly lower importance on the track record of the venture’s management team compared to all other investors. Additionally, investors with an engineering background put significantly more importance on the medium level of profitability, which is break even, and not that much importance to the highest level of profitability.

4.2 Effects of investor experience on selection criteria importance

Similar to Sect. 4.1, we calculate the main effects with regard to the investors’ experience for subsamples distinguishing between investors with entrepreneurial and investment experience. The results are shown in the Appendix (Table 8). We illustrate the results in Figs. 3 and 4, which show the relative importance of the different attributes for the different types of experience.

Relative importance of attributes: Entrepreneurial experience. Calculated based on the coefficients of the main model (Tables 4, 8). Reading example: With a relative importance of 23.37%, entrepreneurs consider revenue growth to be more than three times as important as the criterion current investors (relative importance: 7.21%). This value also signifies that the criterion revenue growth accounts for 23.37% of the decision maker’s total utility

Relative importance of attributes: Investment experience. Calculated based on the coefficients of the main model (Tables 4, 8). Reading example: With a relative importance of 24.94%, investors with low investment experience consider revenue growth to be more than four times as important as the criterion current investors (relative importance: 5.31%). This value also signifies that the criterion revenue growth accounts for 24.94% of the decision maker’s total utility

Figure 3 shows the relative importance of the venture’s attributes with regard to the investors’ entrepreneurial experience. While the relative importance for most attributes seems to be relatively similar to the full sample, we find that the value-added of the product or service (entrepreneur = 20.78%; serial entrepreneur = 21.52%) and the venture’s international scalability (entrepreneur = 15.29%; serial entrepreneur = 17.64%) become more important with more entrepreneurial experience. Conversely, the importance of the management team (entrepreneur = 14.82%; serial entrepreneur = 13.54%) and the business model (entrepreneur = 7.10%; serial entrepreneur = 5.18%) decreases with increasing entrepreneurial experience.

Figure 4 illustrates the relative importance and distinguishes investors with low (i.e., less than 8 years) and high (i.e., 8 or more years) levels of investment experience. It is noticeable that less experienced investors attribute more importance to the venture’s value-added of the product or service (21.03%; investment experience high = 18.98%), profitability (12.53%; investment experience high = 10.87%), and business model (12.09%; investment experience high = 6.00%). On the other hand, investors with a high degree of investment experience put more importance on the management team (17.31%; investment experience low = 12.38%), the international scalability (13.42%; investment experience low = 11.71%), and the current investors (7.44%; investment experience low = 5.31%). The importance of revenue growth barely differs between less experienced (24.95%) and more experienced investors (25.98%).

To assess whether the differences we unveiled in the previous paragraphs are robust and statistically significant, we use interaction effects with dummy variables related to investor experience. The results are shown in Table 6. Model (1) focuses on entrepreneurial experience (i.e., whether the investor has founded at least one company or not). The significant positive effect for an easy international scalability highlights that investors with previous entrepreneurial experience put significantly more importance on the venture’s internationalization possibilities than investors without entrepreneurial experience. Model (2) focuses on serial entrepreneurs. Here, we find that investors with more entrepreneurial experience attach even more importance to an easy international scalability of the venture compared to the rest of the sample. Finally, we interact the attribute levels with the dummy variable investment experience. We find that more experienced investors are significantly less interested in innovation-centered and lock-in business models. However, more investment experience leads to a higher attribution of importance to the track record of the venture’s management team.

5 Discussion and implications

We investigate the relative importance of seven different screening criteria of VC investors and how the value attributed to these criteria is influenced by their education and experience. Overall, we find that the most important screening criteria of VCs are revenue growth, value-added of the product or service, the track record of the management team, and international scalability. Criteria such as profitability, the business model, and current investors are of comparably lower importance. However, the value attributed to these different criteria is influenced by the decision makers’ level and field of education as well as their investment and entrepreneurial experience. This finding is in line with prior research which argues that education and experience develop an individual’s knowledge structure and influence how they evaluate opportunities (Walsh 1995; Wood and Williams 2014).

5.1 Education

Our results indicate that the importance attributed to the international scalability of a venture’s business and its current profitability depend on the level of education of a decision maker. Prior research finds that the international expansion for new ventures is an important step to exploit growth opportunities and with that, realize performance advantages and increase profitability (Fernhaber et al. 2007; Lu and Beamish 2001; McDougall and Oviatt 1996; Oviatt and McDougall 2005). Our results suggest, that a higher level of education increases the awareness of decision makers regarding international scalability as an indicator of the potential of a venture’s business idea. Furthermore, the relative importance of profitability decreases with an increased level of education. This result indicates that decision makers with a higher level of education seem to emphasize the future potential of the venture instead of its current financial situation. Besides, decision makers with a higher level of education seem to prefer innovation-centered business models. This is in line with prior research arguing that a higher level of education leads to higher awareness and receptiveness for innovation (Bantel and Jackson 1989; Hambrick and Mason 1984; Wiersema and Bantel 1992).

Regarding the field of education, our results show that VC decision makers with different educational backgrounds seem to have a different perspective on the screening criteria. While our results confirm prior findings that decision makers with a natural science background are more focused on the product (Gruber et al. 2013; Hambrick and Mason 1984), we show that this does not seem to be the case for engineers. Engineers seem to attach a higher value to ventures whose profitability already reached the break even point. This could be understood as an indicator for initial market success, a competitive advantage, effective management, and, eventually, firm survival (Davidsson et al. 2009; Delmar et al. 2013). In contrast to prior research, which argues that a business education results in a stronger focus on profit-maximization (Ghoshal 2005; Slater and Dixon-Fowler 2010), we could not find any evidence supporting this argument. This result might be related to the specifics of the VC industry, where one of the main tasks of a VC is to identify promising ventures which have a high future success potential and that financials at this stage are of lower importance. However, in light of this, it is surprising that decision makers with a business education place comparably less value on the ease of the international scalability of the business model as a potential indicator for future growth opportunities of the venture (Lu and Beamish 2001; McDougall and Oviatt 1996). These results add to prior research investigating the consequences of different fields of education (Gruber et al. 2013; Slater and Dixon-Fowler 2010; Wiersema and Bantel 1992), specifically in the venture financing context (Dimov and Shepherd 2005; Zarutskie 2010).

5.2 Experience

Furthermore, our study indicates that decision makers with prior entrepreneurial experience seem to put more weight on the international scalability of a business model. Prior research argued that experience as an entrepreneur affects the evaluation of entrepreneurial opportunities and increases the ability to detect promising ventures (Baron and Ensley 2006; Dimov and Shepherd 2005; Walske and Zacharakis 2009; Zarutskie 2010). Based on this argument, international scalability seems to indicate the future success potential of a venture (Fernhaber et al. 2007; Lu and Beamish 2001; McDougall and Oviatt 1996; Oviatt and McDougall 2005). This argument is reinforced by our finding that more experienced entrepreneurs put even more weight on this criterion.

Decision makers with prior investment experience seem to focus strongly on the track record of the management team. This finding is particularly interesting in light of the ongoing jockey versus horse debate (Block et al. 2019; Kaplan et al. 2009; Macmillan et al. 1985; Mitteness et al. 2012). Prior research investigates which criteria are more important for private equity investors—the management team (jockey) or product- and market-related aspects (horse)—with conflicting results (Kaplan et al. 2009; Mitteness et al. 2012; Petty and Gruber 2011). Mitteness et al. (2012) argue that these conflicting results may be a function of the stage of the funding process. Our study adds to this debate by showing that some of these differences might also be explained by the prior experience of the decision maker. Since task-specific experience has been found to help investors to develop an accurate perception of risk, return, and investment opportunities (Dimov and Shepherd 2005; Walske and Zacharakis 2009; Zarutskie 2010), it could be argued that experienced investors understand the track record of the management team as a positive indicator of a venture’s success potential.

Overall, our study adds to prior research on the importance of the human capital characteristics education and experience on decision making behavior (Hambrick and Mason 1984; Slater and Dixon-Fowler 2010), particularly in the VC context (Franke et al. 2008; Shepherd et al. 2003; Watson et al. 2003). Furthermore, we contribute to the literature on the screening criteria of risk capital investors (for recent studies see Gompers et al. 2020; Hoenig and Henkel 2015; Hsu et al. 2014; Warnick et al. 2018). This literature has thus far focused primarily on early-stage ventures. We extend this line of research by investigating ventures in their growth and expansion stage where additional criteria such as venture performance measures (i.e., profitability and revenue growth) become available.

5.3 Practical implications

Our empirical insights are of particular importance for entrepreneurs seeking venture capital because they can provide guidance on the most relevant attributes risk capital investors are going to evaluate. Typically, the first screening requires only a few minutes, and only a small number of ventures pass this stage of evaluation (Gompers et al. 2020; Petty and Gruber 2011). We find that investors seem to prefer ventures with high revenue growth, high value-added of the product or service, and those in which team members have a relevant management track record. Hence, ventures seeking financing should highlight these aspects in their investment application. However, ventures should be aware that the importance of different screening criteria is influenced by the decision maker’s education and experience. Our results suggest that ventures should try to obtain information about the background of the VC decision makers before applying. This could help them to highlight the relevant criteria and make the application more target-oriented which could increase their chances of success of entering the next round in the VC process.

Also, risk capital investors can use these results to better understand their own investment decisions and benchmark them to the market. Furthermore, our results demonstrate that the human capital characteristics education and experience, affect their selection decision and hence, the selection of target ventures finally considered for investment. This information provides a deeper understanding of whether those making decisions for the investors act in line with the investors’ overall investment philosophy and their business strategy.

6 Limitations, future research, and conclusion

6.1 Limitations and future research

This study is not without limitations, some of which relate to the conjoint approach used in our study. Early research on the assessment criteria of risk capital investors used mainly qualitative interviews and post hoc questionnaires (MacMillan et al. 1985, 1987; Tyebjee and Bruno 1984). This research was criticized for suffering from post hoc and self-report bias. Moreover, the respondents were typically asked to evaluate the respective criteria in isolation and were not forced to trade-off criteria against each other. The use of conjoint experiments has been advocated to overcome these shortcomings. However, the conjoint method also has its drawbacks. For example, it presents only hypothetical ventures to investors. Many other potential effects, such as the appearance of the business plan and the way the opportunity entered the deal flow of the investor are not measured. Relatedly, the conjoint method implicitly assumes that decision makers possess information on all different criteria assessed. In reality, however, not all of this information may be available for every venture that enters the screening process of investors.

Additionally, the seven criteria used in our conjoint study only represent a selection of criteria that is based on prior literature and interviews. We were not able to test the effects of various other decision criteria named in our interviews (e.g., intellectual property protection, competition in the market, or valuation of the venture). To reduce the risk of omitting important screening criteria, we checked with our interview partners that those criteria in our study were really the most important ones. Also, our conjoint analysis implicitly assumes that decision makers apply a fully compensatory model when evaluating ventures (i.e., they weigh all seven possible criteria in their decision making process). However, research by Maxwell et al. (2011) indicates that this may not always be the case: business angels use a short cut decision heuristic where less criteria are used and are only evaluated as to whether they are above a threshold value and use an “elimination-by-aspects” heuristic to trim the evaluation set to a more manageable size for further analysis. In addition, our CBC approach sometimes made it difficult for participants to choose between two ventures. As an alternative, we could have used a rating-based conjoint approach which allows participants to rate two ventures equally high. Finally, although we reduced our sample to a more homogeneous subsample in our analysis, we cannot completely rule out that different decision makers from different industries interpret one and the same venture description and venture criterion differently. Future research could address this issue by having a stronger industry focus (e.g., Biotech, Cleantech).

Our study also has limitations with regard to the generalizability of the results. As we focus only on the screening phase, no direct conclusions about the criteria for final investment decisions can be made. Future research could investigate, how the influence of education and experience and thus, the focus on specific screening criteria, affects the final investment decision and ultimately the success of the venture. Related to this, prior research finds that decision criteria vary depending on the stage within the VC evaluation process (Gompers et al. 2016; Petty and Gruber 2011). We propose that some of these differences might be explained by the education and experience of the decision maker as different individual profiles are required in these different stages. Hence, future research should investigate the influence of human capital characteristics such as education and experience in the different stages on the VC evaluation process.

Our analyses also showed that investors, depending on their education or experience, differ only in some criteria. This might indicate, that the evaluation of certain criteria, especially the criterion revenue growth, is very stable across all groups, independent from education or experience. However, it needs to be considered, that we only include two types of experience, namely investment and entrepreneurial experience, in our study. Other types of experience such as firm-specific or management experience could also affect the evaluation of different screening criteria. Furthermore, we do not ask about the quality of the decision maker’s experience. It could be argued that failure experience in prior investment decisions or as an entrepreneur can have a very different effect on venture screening than success experience. Hence, we would recommend future studies to include additional types of experience as well as measures regarding the quality of the experience.

Our study also does not allow for conclusions about the quality of risk capital investors’ screening. Making a “good deal” requires that an investor has better or more reliable information on the future than others because otherwise the information might already be reflected in the price of the deal. Hence, decision makers might not always choose already successful ventures but focus more on the current valuation of the company, their expectations for the future but also on their value-added for the venture. Consequently, the criteria used and value-added services offered to the venture must be linked to the success potential of the venture (Guo and Jiang 2013). More knowledge about this relationship would help to shed light on the question of whether performance is mainly driven by the selection process or by the investor’s value-added services (Croce et al. 2013; Hellmann and Puri 2002; Naulin and Moritz 2021) and how this relationship differs by investment and/or venture stage. It could be argued that the effect of the value-added services is higher at early versus later stages of the venture cycle, as the path of the venture is easier to influence when the venture is still young and nascent. This implies that the venture selection process of VCs differs depending on the stage in the venture cycle the financing is provided. In this context, not only the human capital of the decision maker but also his/her social capital might play an important role in the decision making process and the development of the ventures.

6.2 Conclusion

We perform an experimental choice-based-conjoint analysis with 229 individual VC investors to assess whether and how VC investors’ education and experience influence their screening decisions. Our results indicate that the level and field of education, as well as the decision maker’s investment and entrepreneurial experience, indeed moderate the relative importance of different screening criteria. For example, we find that international scalability seems to become more important for decision makers with higher education and those with entrepreneurial experience. Additionally, decision makers with a background in natural science focus on the value-added of the product or service, engineers seem to value a break even profitability and focus less on the management team. Investment experience, on the other hand, leads to a stronger focus on the management team. With these findings, our study contributes to the literature on how decision makers differ in their assessment of ventures, to the literature on the consequences of the field of education, and to the literature on the screening criteria of risk capital investors. Our results have practical implications for entrepreneurial ventures that seek financing and for risk capital investors.

Notes

The survey is available from the corresponding author upon request.

References

Aguinis H, Gottfredson RK, Culpepper SA (2013) Best-practice recommendations for estimating cross-level interaction effects using multilevel modeling. J Manag 39(6):1490–1528

Bachher JS, Guild PD (1996) Financing early stage technology based companies: investment criteria used by investors. Front Entrep Res 996:363–376

Bantel KA, Jackson SE (1989) Top management and innovations in banking: does the composition of the top team make a difference. Strateg Manag J 10(1):107–124

Baron RA, Ensley MD (2006) Opportunity recognition as the detection of meaningful patterns: evidence from comparisons of novice and experienced entrepreneurs. Manage Sci 52(9):133–344

Becker GS (1964) Human capital. Columbia University Press, New York City.https://doi.org/10.1093/nq/s1-IV.92.83-a

Bliss RT (1999) A venture capital model for transitioning economies: the case of Poland. Ventur Cap 1(3):241–257

Block J, Fisch C, Vismara S, Andres R (2019) Private equity investment criteria: an experimental conjoint analysis of venture capital business angels, and family offices. J Corp Finan 58:329–352

Block J, Hirschmann M, Fisch C (2021) Which criteria matter when impact investors screen social enterprises? J Corp Finan 66:101813

Bonner SE (1990) Experience effects in auditing: the role of task-specific knowledge. Account Rev 65(1):72–92

Boocock G, Woods M (1997) The evaluation criteria used by venture capitalists: evidence from a UK Venture Fund. Int Small Bus J 16(1):36–57

Carpenter MA, Geletkancz MA, Sanders WG (2004) Upper echelons research revisited: Antecedents, elements, and consequences of top management team composition. J Manag 30(6):749–778. https://doi.org/10.1016/j.jm.2004.06.001

Carter RB, Van Auken HE (1992) Effect of professional background on venture capital proposal evaluation. J Small Bus Strateg 3(1):45–55

Chan CS, Park HD (2015) How images and color in business plans influence venture investment screening decisions. J Bus Ventur 30(5):732–748

Chrzan K, Orme B (2000) An overview and comparison of design strategies for choice-based conjoint analysis. Sawtooth Software Research Paper Series

Croce A, Martí J, Murtinu S (2013) The impact of venture capital on the productivity growth of European entrepreneurial firms: ‘screening’ or ‘value added’ effect? J Bus Ventur 28(4):489–510

Datta S, Iskandar-Datta M (2014) Upper-echelon executive human capital and compensation: generalist vs specialist skills. Strateg Manag J 35(12):1853–1866

Davidsson P, Steffens P, Fitzsimmons J (2009) Growing profitable or growing from profits: putting the horse in front of the cart? J Bus Ventur 24(4):388–406

Delmar F, Shane S (2006) Does experience matter? The effect of founding team experience on the survival and sales of newly founded ventures. Strateg Organ 4(3):215–247. https://doi.org/10.1177/1476127006066596

Delmar F, McKelvie A, Wennberg K (2013) Untangling the relationships among growth, profitability and survival in new firms. Technovation 33(8–9):276–291

Dimov DP, Shepherd DA (2005) Human capital theory and venture capital firms: exploring “home runs” and “strike outs.” J Bus Ventur 20(1):1–21

Dimov D, Shepherd DA, Sutcliffe KM (2007) Requisite expertise, firm reputation, and status in venture capital investment allocation decisions. J Bus Ventur 22(4):481–502

Elango B, Fried VH, Hisrich RD, Polonchek A (1995) How venture capital firms differ. J Bus Ventur 10(2):157–179

Feeney L, Haines GH, Riding AL (1999) Private investors investment criteria: insights from qualitative data. Venture Cap 1(2):121–145

Fernhaber S, Gilbert BA, McDougall P (2007) International entrepreneurship and geographic location: an empirical examination of new venture internationalization. J Int Bus Stud 39:267–290. https://doi.org/10.1057/palgrave.jibs.8400342

Franke N, Gruber M, Harhoff D, Henkel J (2006) What you are is what you like—similarity biases in venture capitalists evaluations of start-up teams. J Bus Ventur 21(6):802–826

Franke N, Gruber M, Harhoff D, Henkel J (2008) Venture capitalists evaluations of start-up teams: trade-offs, knock-out criteria, and the impact of VC experience. Entrep Theory Pract 32(3):459–483

Fried VH, Hisrich RD (1994) Toward a model of venture capital investment decision-making. Financ Manag 23(3):28–37

Ghoshal S (2005) Destroying good management practices. Acad Manag Learn Educ 4(1):75–91

Gibbons M, Johnston R (1974) The roles of science in technological innovation. Res Policy 3(3):220–242

Gibbons R, Waldman W (2004) Task-specific human capital. Am Econ Rev 94(2):203–207

Gimeno J, Folta TB, Cooper AC, Woo CY (1997) Survival of the fittest? Entrepreneurial human capital and the persistence of underperforming firms. Adm Sci Q 42(4):750–783. https://doi.org/10.2307/2393656

Gompers P, Kaplan SN, Mukharlyamov V (2016) What do private equity firms say they do? J Financ Econ 121(3):449–476

Gompers PA, Gornall W, Kaplan SN, Strebulaev IA (2020) How do venture capitalists make decisions? J Financ Econ 135(1):169–190

Gruber M, Harhoff D, Hoisl K (2013) Knowledge recombination across technological boundaries: scientists vs. engineers. Manage Sci 59(4):837–851

Guo D, Jiang K (2013) Venture capital investment and the performance of entrepreneurial firms: evidence from China. J Corp Finan 22:375–395

Hambrick DC, Mason PA (1984) Upper echelons: the organization as a reflection of its top managers. Acad Manag Rev 9(2):193–206

Hambrick DC, Cho TS, Chen M (1996) The influence of top management team heterogeneity on firms competitive moves. Adm Sci Q 41(4):659–684

Hellmann T, Puri M (2002) Venture capital and the professionalization of start-up firms: empirical evidence. J Financ 57(1):169–197

Hitt MA, Tyler BB (1991) Strategic decision models: integrating different perspectives. Strateg Manag J 12(5):327–351

Hoenig D, Henkel J (2015) Quality signals? The role of patents, alliances, and team experience in venture capital financing. Res Policy 44(5):1049–1064

Hsu DK, Haynie JM, Simmons SA, McKelvie A (2014) What matters, matters differently: a conjoint analysis of the decision policies of angel and venture capital investors. Venture Cap 16(1):1–25

Johnson RM, Orme BK (1996) How many questions should you ask in choice-based conjoint studies? Sawtooth Software Research Paper Series

Kaplan SN, Sensoy BA, Strömberg P (2009) Should investors bet on the jockey or the horse? Evidence from the evolution of firms from early business plans to public companies. J Financ 64(1):75–115. https://doi.org/10.1111/j.1540-6261.2008.01429.x

Karsai J, Wright M, Filatotchev I (1997) Venture capital in transition economics: the case of Hungary. Entrep Theory Pract 21(4):93–110

Khan AM (1987) Assessing venture capital investments with noncompensatory behavioral decision models. J Bus Ventur 2(3):193–205

Kirsch D, Goldfarb B, Gera A (2009) Form or substance: the role of business plans in venture capital decision making. Strateg Manag J 30(5):487–515

Knight RM (1986) Criteria used by venture capitalists. J Small Bus Entrep 3(4):3–9

Knight RM (1994) Criteria used by venture capitalists: a cross cultural analysis. Int Small Bus J 13(1):26–37

Kollmann T, Kuckertz A (2010) Evaluation uncertainty of venture capitalists investment criteria. J Bus Res 63(7):741–747

Kuhfeld WF, Tobias RD, Garratt M (1994) Efficient experimental design with marketing research applications. J Mark Res 31:545–557

Lu JW, Beamish PW (2001) The internationalisation and performance of SMEs. Strateg Manag J 22(6–7):565–586. https://doi.org/10.1002/smj

MacMillan IC, Siegel R, Subbanarasimha PN (1985) Criteria used by venture capitalists to evaluate new venture proposals. J Bus Ventur 1(1):119–128

MacMillan IC, Zemann L, Subbanarasimha PN (1987) Criteria distinguishing successful from unsuccessful ventures in the venture screening process. J Bus Ventur 2(2):123–137

March JG, Simon HA (1958) Organizations. Wiley, New York

Mason C, Stark M (2004) What do investors look for in a business plan? A comparison of the investment criteria of bankers, venture capitalists and business angels. Int Small Bus J 22(3):227–248

Matlin MW (2005) Cognition. Wiley, Hoboken

Maxwell AL, Jeffrey SA, Lévesque M (2011) Business angel early stage decision making. J Bus Ventur 26(2):212–225

McDougall PP, Oviatt BM (1996) New venture internationalization, strategic change, and performance: a follow-up study. J Bus Ventur 11(1):23–40. https://doi.org/10.1016/0883-9026(95)00081-X

McEnrue MP (1988) Length of experience and the performance of managers in the establishment phase of their careers. Acad Manag J 31(1):175–185

Mitteness CR, Baucus MS, Sudek R (2012) Horse vs. Jockey? How stage of funding process and industry experience affect the evaluations of angel investors. Ventur Cap 14(4):241–267. https://doi.org/10.1080/13691066.2012.689474

Murnieks CY, Haynie JM, Wiltbank RE, Harting T (2011) I like how you think: similarity as an interaction bias in the investor-entrepreneur dyad. J Manage Stud 48(7):1533–1561

Muzyka D, Birley S, Leleux B (1996) Trade-offs in the investment decisions of european venture capitalists. J Bus Ventur 11(4):273–287

Naulin T, Moritz A (2021) Value-adding impact of accelerators on startups’ development. Int J Entrep Ventur (in press)

Oviatt BM, McDougall PP (2005) Defining international entrepreneurship and modeling the speed of internationalization. Entrep Theory Pract 29(5):537–553. https://doi.org/10.1111/j.1540-6520.2005.00097.x

Parhankangas A, Hellström T (2007) How experience and perceptions shape risky behaviour: evidence from the venture capital industry. Ventur Cap 9(3):183–205. https://doi.org/10.1080/13691060701324478

Pelled LH (1996) Demographic diversity, conflict, and work group outcomes: an intervening process theory. Organ Sci 7(6):615–631

Petty JS, Gruber M (2011) In pursuit of the real deal: a longitudinal study of VC decision making. J Bus Ventur 26(2):172–188

Reuber R (1997) Management experience and management expertise. Decis Support Syst 21(2):51–60

Riquelme H, Rickards T (1992) Hybrid conjoint analysis: an estimation probe in new venture decisions. J Bus Ventur 7(6):505–518

Sandberg WR, Schweiger DM, Hofer CW (1988) The use of verbal protocols in determining venture capitalists decision processes. Entrep Theory Pract 13(1):8–20

Scarlata M, Alemany L (2009) How do philanthropic venture capitalists choose their portfolio companies? SSRN Working Paper. https://doi.org/10.2139/ssrn.1343563

Scarlata M, Zacharakis A, Walske J (2016) The effect of founder experience on the performance of philanthropic venture capital firms. Int Small Bus J 34(5):618–636. https://doi.org/10.1177/0266242615574588

Shane S, Locke EA, Collins CJ (2003) Entrepreneurial motivation. Hum Resour Manag Rev 13(2):257–279. https://doi.org/10.1016/S1053-4822(03)00017-2

Shepherd DA (1999a) Venture capitalists’ introspection: a comparison of “in use" and “espoused” decision policies. J Small Bus Manag 37(2):76–87

Shepherd DA (1999b) Venture capitalists assessment of new venture survival. Manag Sci 45(5):621–632

Shepherd DA, Ettenson R, Crouch A (2000) New venture strategy and profitability: a venture capitalist’s assessment. J Bus Ventur 15(5–6):449–467

Shepherd DA, Zacharakis A, Baron RA (2003) ‘VCs’ decision processes: evidence suggesting more experience may not always be better. J Bus Ventur 18(3):381–401

Silva J (2004) Venture capitalists decision-making in small equity markets: a case study using participant observation. Venture Cap 6(2–3):125–145

Sitkin SB, Pablo AL (1992) Reconceptualizing the determinants of risk behavior. Acad Manag Rev 17(1):9–38

Slater DJ, Dixon-Fowler HR (2010) The future of the planet in the hands of MBAs: an examination of CEO MBA education and corporate environmental performance. Acad Manag Learn Educ 9(3):429–441

Tyebjee TT, Bruno AV (1984) A model of venture capitalist investment activity. Manage Sci 30(9):1051–1066

Unger JM, Rauch A, Frese M, Rosenbusch N (2011) Human capital and entrepreneurial success: a meta-analytical review. J Bus Ventur 26(3):341–358

Walsh JP (1995) Managerial and organizational cognition: notes from a trip down memory lane. Organ Sci 6(3):280–321

Walske JM, Zacharakis A (2009) Genetically engineered: why some venture capital firms are more successful than others. Entrep Theory Pract 33(1):297–318. https://doi.org/10.1111/j.1540-6520.2008.00290.x

Wang G, Holmes RM, Oh IS, Zhu W (2016) Do CEOs matter to firm strategic actions and firm performance? A meta-analytic investigation based on upper echelons theory. Pers Psychol 69(4):775–862

Warnick BJ, Murnieks CY, McMullen JS, Brooks WT (2018) Passion for entrepreneurship or passion for the product? A conjoint analysis of angel and VC decision-making. J Bus Ventur 33(3):315–332

Watson W, Stewart WH, BarNir A (2003) The effects of human capital, organizational demography, and interpersonal processes on venture partner perceptions of firm profit and growth. J Bus Ventur 18(2):145–164

Wiersema MF, Bantel KA (1992) Top management team demography and corporate strategic change. Acad Manag J 35(1):91–121

Wood MS, Williams DW (2014) opportunity evaluation as rule-based decision making. J Manag Stud 51(4):573–602. https://doi.org/10.1111/joms.12018

Woolnough BE (1994) Factors affecting students’ choice of science and engineering. Int J Sci Educ 16(6):659–679. https://doi.org/10.1080/0950069940160605

Wright M, Robbie K (1996) Venture capitalists, unquoted equity investment appraisal and the role of accounting information. Account Bus Res 26(2):153–168

Zacharakis AL, Meyer GD (1998) A lack of insight: do venture capitalists really understand their own decision process? J Bus Ventur 13(1):57–76

Zarutskie R (2010) The role of top management team human capital in venture capital markets: evidence from first-time funds. J Bus Ventur 25(1):155–172

Acknowledgements

Deutsche Forschungsgemeinschaft (DFG). The title of the grant is Entscheidungskriterien von Risikokapitalgebern in der Spätphasenfinanzierung von Wachstumsunternehmen. The Grant ID is 400567894. The grant was received by Joern Block, who is the corresponding author.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Moritz, A., Diegel, W., Block, J. et al. VC investors’ venture screening: the role of the decision maker’s education and experience. J Bus Econ 92, 27–63 (2022). https://doi.org/10.1007/s11573-021-01042-z

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11573-021-01042-z