Abstract

In this paper, we propose an artificial market to model high-frequency trading where fast traders use threshold rules strategically to issue orders based on a signal reflecting the level of stochastic liquidity prevailing on the market. A market maker is in charge of adjusting prices (on a fast scale) and of setting closing prices and transaction costs on a daily basis, controlling for the volatility of returns and market activity. We first show that a baseline version of the model with no frictions is able to generate returns endowed with several stylized facts. This achievement suggests that the two time scales used in the model are one (possibly novel) way to obtain realistic market outcomes and that high-frequency trading can amplify liquidity shocks. We then explore whether transaction costs can be used to control excess volatility and improve market quality. While properly implemented taxation schemes may help in reducing volatility, care is needed to avoid excessively curbing activity in the market and intensifying the occurrence of abnormal peaks in returns.

Similar content being viewed by others

Notes

This terminology, now quite common in the financial literature but possibly less used elsewhere, was actually introduced by the economist Nicholas Kaldor to refer to the most relevant elements requiring explanation. In his words, “The theorist...ought to start off with a summary of the facts which he regards as relevant to his problem [and] concentrate on broad tendencies, ignoring individual detail, and proceed on the ‘as if’ methods, i.e. construct a hypothesis that could account for these ‘stylized facts’...”, see Kaldor (1961).

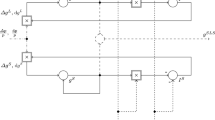

To facilitate the comprehension, we use capital letters to denote all intra-day variables, whereas small letters are used to denote daily variables. Accordingly, intra-day variables are indexed by t, whereas calendar dates are indexed by n.

We assume that the demand is always fulfilled by a market maker, who adjusts taxation in order to limit/entice activity on the market.

\({\mathbb {E}}^i[\cdot ]\) is the expectation with respect to the joint distribution of vector \(\underline{\epsilon ^{-i}}=(\epsilon _j)_{j\ne i}\).

We stress that the market maker also operates on a fast scale: he adjusts prices on the fast intra-day time scale and, eventually, makes the closing daily price available for time series analysis.

The truncation to positive values is just one of the possible positive transformations of the Ornstein–Uhlenbeck process. See, for instance, Almgren (2012) for other specifications of positive transformations for mean-reverting stochastic processes representing liquidity on markets.

The Matlab code used to numerically simulate our returns, including the iteration procedure of the best response map, can be downloaded at https://drive.google.com/open?id=1Gx-UpwslWZPpPvabaARFtj5YSWpw4weg. The simulations produced by this code are exactly the ones that are statistically analyzed in Sect. 3.2.

The level of \({\bar{\tau }}\) is not crucial, provided that it is large enough to reach a stable value for intra-day returns. A value of \({\bar{\tau }}\) that is too low would not let the intra-day market stabilize on an equilibrium value for returns.

We used the EuStockMarkets dataset, which is available in R Core Team (2017) and contains the time series of the DAX, the SMI, the CAC and the FTSE from the beginning of 1991 to the end of 1998 (1860 daily observations for each index) to compute summary statistics of the returns. For instance, standard deviations and kurtosis are 0.010, 0.009, 0.011, 0.008 and 9.28, 8.74, 5.39, 5.64 for the four time series, respectively. Similar figures are reported as examples for stocks and indices in Campbell et al. (1997), even though there is obviously considerable variability among different assets or financial acitvities. In Pagan (1996), the estimate of autocorrelation at lag 1 of squared returns for US stocks is 0.189.

To run the numerical fit, we fix a seed for the generation of the random signals of the Ornstein–Uhlenbeck process. We then use a \(20\times 20\) grid of values for \(\mu \) and \(\sigma \). This calibration operation required about 30 h of machine time on a Core i7-6700 processor. The same methodology was implemented in a second round for the calibration of \(\theta \), where we used a grid of ten values ranging from 0.1 to 1. Note that implementation of a Monte Carlo experiment with \(M=20\) trajectories would require approximately 20 days. A statistical robustness check of this result follows from the analysis of time series produced by the model relying on those values of the parameters.

Figures in Table 5 are computed as the median values extracted from the 19 simulations.

We thank an anonymous referee for his or her useful remarks on tail exponents.

As a proxy for volatility of daily returns, we have used the standard deviation of intra-day returns.

References

Almgren R (2012) Optimal trading with stochastic liquidity and volatility. SIAM J Financ Math 3(1):163–181

Brock WA, Durlauf SN (2001) Discrete choice with social interactions. Rev Econ Stud 68(2):235–260

Budish E, Cramton P, Shim J (2015) The high-frequency trading arms race: frequent batch auctions as a market design response. Q J Econ 130(4):1547–1621

Campbell JY, Lo AW-C, MacKinlay AC (1997) The econometrics of financial markets. Princeton University Press, Princeton

Chiarella C, He X-Z, Shi L, Wei L (2017) A behavioural model of investor sentiment in limit order markets. Quant Finance 17(1):71–86

Chiarella C, Iori G, Perelló J (2009) The impact of heterogeneous trading rules on the limit order book and order flows. J Econ Dyn Control 33(3):525–537

Cont R (2001) Empirical properties of asset returns: stylized facts and statistical issues. Quant Finance 1(2):223–236

Dai Pra P, Sartori E, Tolotti M (2013) Strategic interaction in trend-driven dynamics. J Stat Phys 152(4):724–741

Fontini F, Sartori E, Tolotti M (2016) Are transaction taxes a cause of financial instability? Phys A Stat Mech Appl 450:57–70

Ghoulmie F, Cont R, Nadal J (2005) Heterogeneity and feedback in an agent-based market model. J Phys Condens Matter 17:1259–1268

Gillespie CS (2015) Fitting heavy tailed distributions: the poweRlaw package. J Stat Softw 64(2):1–16

Granovetter M (1978) Threshold models of collective behavior. Am J Sociol 83(6):1420–1443

Hasbrouck J, Saar G (2009) Technology and liquidity provision: the blurring of traditional definitions. J Financ Mark 12(2):143–172

Hasbrouck J, Saar G (2013) Low-latency trading. J Financ Mark 16(4):646–679

Kaldor N (1961) Capital accumulation and economic growth. In: Lutz FA, Hague DC (eds) The theory of capital. St. Martin’s Press, New York

Kirman AP (1992) Whom or what does the representative individual represent? J Econ Perspect 6(2):117–136

LeBaron B, Yamamoto R (2008) The impact of imitation on long memory in an order-driven market. East Econ J 34(4):504–517

Lux T (2009) Stochastic behavioral asset-pricing models and the stylized facts. In: Hens T, Schenk-Hoppe KR (eds) Handbook of financial markets: dynamics and evolution, handbooks in finance. North-Holland, San Diego, pp 161–215

Lux T (2016) Applications of statistical physics methods in economics: current state and perspectives. Eur Phys J Spec Top 225(17):3255–3259

Maslov S (2000) Simple model of a limit order-driven market. Phys A Stat Mech Appl 278(3–4):571–578

Nadal J-P, Phan D, Gordon MB, Vannimenus J (2005) Multiple equilibria in a monopoly market with heterogeneous agents and externalities. Quant Finance 5(6):557–568

Pagan A (1996) The econometrics of financial markets. J Empir Finance 3(1):15–102

Phan D, Pajot S, Nadal J-P (2003) The monopolist’s market with discrete choices and network externality revisited: small-worlds, phase transition and avalanches in an ACE framework. In: Ninth annual meeting of the society of computational economics, University of Washington, Seattle, USA

R Core Team (2017) R: a language and environment for statistical computing. R Foundation for Statistical Computing, Vienna

Spahn B (2002) On the feasibility of a tax on foreign exchange transactions. Technical Report, Federal Ministry for Economic Cooperation and Development, Bonn

Acknowledgements

We are indebted to two anonymous referees for their helpful and constructive comments. The authors acknowledge the financial support of Ca’ Foscari University of Venice under the grant “Interactions in complex economic systems: innovation, contagion and crises”. We are also grateful to Antonella Basso for her support in sharing computer multi-core resources that proved to be invaluable for running our simulations. We received useful remarks from participants in the WEHIA 2017 conference held at Università Cattolica di Milano and seminars held at the University of Technology Sydney, Ca’ Foscari University of Venice and at the Centre d’Economie de la Sorbonne (CES), but are entirely responsible for all remaining errors.

Author information

Authors and Affiliations

Corresponding author

Electronic supplementary material

Below is the link to the electronic supplementary material.

Rights and permissions

About this article

Cite this article

Liuzzi, D., Pellizzari, P. & Tolotti, M. Fast traders and slow price adjustments: an artificial market with strategic interaction and transaction costs. J Econ Interact Coord 14, 643–662 (2019). https://doi.org/10.1007/s11403-018-0233-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11403-018-0233-8