Abstract

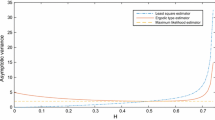

We discuss some inference problems associated with the fractional Ornstein–Uhlenbeck (fO–U) process driven by the fractional Brownian motion (fBm). In particular, we are concerned with the estimation of the drift parameter, assuming that the Hurst parameter \(H\) is known and is in \([1/2, 1)\). Under this setting we compute the distributions of the maximum likelihood estimator (MLE) and the minimum contrast estimator (MCE) for the drift parameter, and explore their distributional properties by paying attention to the influence of \(H\) and the sampling span \(M\). We also deal with the ordinary least squares estimator (OLSE) and examine the asymptotic relative efficiency. It is shown that the MCE is asymptotically efficient, while the OLSE is inefficient. We also consider the unit root testing problem in the fO–U process and compute the power of the tests based on the MLE and MCE.

Similar content being viewed by others

References

Bercu B, Coutin L, Savy N (2011) Sharp large deviations for the fractional Ornstein-Uhlenbeck process. SIAM Theory Probab Appl 55:575–610

Bishwal JPN (2008) Parameter estimation in stochastic differential equations. Springer, Berlin

Bishwal JPN (2011) Minimum contrast estimation in fractional Ornstein-Uhlenbeck process: continuous and discrete sampling. Fract Calc Appl Anal 14:375–410

Brouste A, Kleptsyna M (2010) Asymptotic properties of MLE for partially observed fractional diffusion system. Stat Inference Stoch Process 13:1–13

Cheridito P, Kawaguchi H, Maejima M (2003) Fractional Ornstein-Uhlenbeck processes. Electron J Probab 8:1–14

Duncan TE, Hu Y, Pasik-Duncan B (2000) Stochastic calculus for fractional Brownian motion I. Theory SIAM J Control Optim 38:582–612

Gripenberg G, Norros I (1996) On the prediction of fractional Brownian motion. J Appl Probab 33:400–410

Hu Y, Nualart D (2010) Parameter estimation for fractional Ornstein-Uhlenbeck processes. Stat Probab Lett 80:1030–1038

Kleptsyna ML, Le Breton A, Roubaud MC (2000) Parameter estimation and optimal filtering for fractional type stochastic systems. Stat Inference Stoch Process 3:173–182

Kleptsyna ML, Le Breton A (2002) Statistical analysis of the fractional Ornstein-Uhlenbeck type process. Stat Inference Stoch Process 5:229–248

Kolmogorov AN (1940) Wienersche Spiralen und einige andere interessante Kurven im Hilbertschen Raum. Dokl Acad Nauk SSSR 26:115–118

Liptser RS, Shiryaev AN (1977) Statistics of random processes I: general theory. Springer, New York

Mandelbrot BB, Van Ness JW (1968) Fractional Brownian motions, fractional noises and applications. SIAM Rev 10:422–437

Norros I, Valkeila E, Virtamo J (1999) An elementary approach to a Girsanov formula and other analytical results on fractional Brownian motions. Bernoulli 5:571–587

Tanaka K (1996) Time series analysis: nonstationary and noninvertible distribution theory. Wiley, New York

Watson GN (1958) A treatise on the theory of Bessel functions, 2nd edn. Cambridge University Press, London

Acknowledgments

The author would like to thank the editor, Professor Denis Bosq, and an anonymous referee for valuable comments and suggestions.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Proof of Theorem 1

It follows from the fractional version of Girsanov’s theorem that

where \(\kappa =(\theta _1+\alpha -\beta )\eta _H/(4(1-H))\) and we have put \(\beta =\sqrt{\alpha ^2-2 \theta _2}\). Then it follows from Kleptsyna and Le Breton (2002) that this last quantity yields

where \(z=\beta M/2\). Then, using the relation

it can be verified that \(m(\theta _1,\theta _2)\) is given by (35), which establishes Theorem 1.

Proof of Theorem 2

When \(\alpha =0\), the distibution function of \(\tilde{\alpha }_{MLE}\) is defined by

where

Then, it follows from the form of the integrand that \(x\) is always coupled with \(M\) as \(M \times x\). Thus we can confirm the statement in the theorem.

As for the MCE, we have

where

The same reasoning as before applies here, which establishes Theorem 2.

Proof of Theorem 3

Let \(x_\gamma (H,M)\) be the \(100 \gamma \%\) point of the distribution of \(\tilde{\alpha }_{MLE}\) for \(\alpha =0\) under \(H\) and \(M\). Then the power of the test at the level \(\gamma \) is computed as

where

Noting that \(M x_\gamma (H,M)\) is independent of \(M\) because of Theorem 2, it is seen from the form of the c.f. that the power depends only on \(\alpha M\). We can also prove this fact for the power of the test based on \(\hat{\alpha }_{MCE}\), which establishes Theorem 3.

Rights and permissions

About this article

Cite this article

Tanaka, K. Distributions of the maximum likelihood and minimum contrast estimators associated with the fractional Ornstein–Uhlenbeck process. Stat Inference Stoch Process 16, 173–192 (2013). https://doi.org/10.1007/s11203-013-9085-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11203-013-9085-y

Keywords

- Fractional Ornstein–Uhlenbeck process

- Maximum likelihood estimator

- Minimum contrast estimator

- Characteristic function

- Unit root test