Abstract

There is a significant gender gap in accounting academia that places women at a disadvantage in terms of recruitment, hiring, promotion, tenure, status, high-level areas or positions (both research and administrative), burden distribution of work, and remuneration. Women are disproportionately represented in part-time or non-tenure tracks, such as lecturers, instructors, and assistant professors. They experience a slower rate of advancement and have lower pay and prestige. Given that various authors attribute this situation to the level of research and production of papers in top-tier scientific journals, this article aims to describe women's participation as authors in cost and management accounting to contribute to clarifying possible causes of gender disparity in the accounting case.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

Accounting, since its genesis, historically proclaimed itself male (Haynes, 2017; Haynes & Fearfull, 2008) based on patriarchal beliefs and prejudices (Kirkham, 1992), such as women’s intellectual and physical incapacity (Cooper, 2010). Men also used exclusionary practices (Thane, 1992), making women ineligible and thus guaranteeing and improving access privileges, rewards, and opportunities for men as the dominant community (Cooper, 2010; Lehman, 1992; Roberts & Couts, 1992; Walker, 2011; Wootton & Kemmerer, 1996).

Throughout the twentieth century, technology, improvement in education and legislation, and social and economic changes generated an increase in the labour participation of women (Ciancanelli et al., 1990; Cooper, 2001; Kirkham & Loft, 1993; Lehman, 1992; Loft, 1992; Ruane & Dobson, 1990; Thane, 1992; Walker, 2008). However, the entrance of women into the labor force generally took place in activities that men did not want to carry out, either because they were considered mechanical, servile, operational, or not very challenging; or because men were the main participants in the world wars (Cooper, 2010; Evans & Rumens, 2020; Lehman, 1992; Loft, 1992). Additionally, these tasks had worse compensation and status (Kirkham & Loft, 1993, 2001; Walker, 2003; Wootton & Kemmerer, 1996).

Teaching and the first approaches to accounting research were linked to professional practice for many years (Fogarty & Zimmerman, 2019). The academic field replicated the dominant androcentric view (Baldarelli et al., 2019; Haynes & Fearfull, 2008), where the feminine is viewed pejoratively (Dillard & Reynolds, 2008).

Academia has been characterized as a field dominated by men since its earliest days, with low female representation (Baldarelli et al., 2016; Gaudet et al., 2022; Norgaard, 1989). Women have reduced opportunities to reach high administrative positions or professorial ranks (Tessens et al., 2011), a slower rate of promotion, lower remuneration (Lee & Won, 2014; Sohn, 2015), and prestige (Broadbent, 2016; Haynes & Fearfull, 2008). This is because women are assigned mainly teaching tasks or tutoring sessions and less time and participation in research activities (Davies & Thomas, 2002; Haynes & Fearfull, 2008), meaning less visibility and productivity in high-impact publications (Blättel-Mink et al., 2009; Davies & Thomas, 2002; Gaudet et al., 2022).

A first step to identify gender disparities in accounting academia is to describe the participation of women in top-tier journals since authorship of this type of research outcome is prioritized and highly valued by the academic community for the granting of merits and benefits to researchers. It is suggested that gender discrimination studies be conducted in relatively small homogeneous subgroups (Ruane & Dobson, 1990). We will focus on cost and management accounting. This document is structured as follows: the first section presents a theoretical framework as a foundation for developing the hypotheses. The following section describes the data source, sample, and measurement of variables. The third and fourth sections present the results and the conclusions.

The situation of women in academia: hypotheses development

Women in accounting academia

Parallel to male dominance in the occupational and professional field, science has also been traditionally classified as a masculine construction (Kelly, 1985; Larivière et al., 2013). Great philosophers such as Plato, Aristotle, Aquinas, Locke, and Bacon have left a macho legacy, considering women incapable of participating in science due to their emotional, personal, and subjective character and lack of ‘rational’ thought (Oakes & Hammond, 1995). Consequently, not only has the presence of women in academia been scarce historically (Bay et al., 2001), but themes, research subjects, experimentation, theorization, practices, and applications have been carried out by and for men (Cislak et al., 2018; Rosser, 1989; Walker, 2008).

Likewise, universities can be very hostile places for women (Baldarell et al., 2019; Broadbent, 2016) since they are hierarchically gendered, and patriarchal relationships seem resistant to change (Cooper, 2001; Tessens et al., 2011). This is even more the case in knowledge related to business, which was conceived historically as a “school of manhood” (Gamber, 1998, p. 4).

Regarding accounting, during the nineteenth century and until the middle of the twentieth century, higher education was dominated by men as a reflection of the professional field (Norgaard, 1989; Turner Lomperis, 1990). There was little or null female presence, whose link was limited to first accounting courses and non-professional institutions (Gago & Macías, 2014).

Although women’s presence and status have increased over time (Baldarelli et al., 2016; Jordan et al., 2006; Metz et al., 2016), accounting academia is far from achieving parity of composition (Bay et al., 2001; Broadbent, 2016). Research results have revealed that women are still a minority (Broadbent, 2016; Tessens et al., 2011). Their participation tends to be relegated to institutions emphasizing teaching or service activities and tutoring students, tasks men are freed. Consequently, they have more time to pursue their academic interests and achieve more and better benefits (Davies & Thomas, 2002; Tessens et al., 2011). Access to research grants, participation in high-level activities, areas or positions (both research and administrative), prestige, status, ranks, and compensation continue to be restricted to a low proportion of women. There is also a disproportionate female concentration in part-time or non-tenure positions such as lecturers, instructors, and assistant professors (Baldarelli et al., 2016; Broadbent, 2016; Gago & Macías, 2014; Geisler et al., 2007; Tessens et al., 2011).

Theoretical framework about gender differences

Differences in productivity and efficiency that lead to wage and status gaps between men and women have traditionally been explained by factors such as personal attributes, investment in human capital (Becker, 2009; Sweetland, 1996), institutionalized schemes, discrimination patterns, or a combination of the above (Addis & Villa, 2003; Gago & Macías, 2014). Specifically related to the academic context of accounting, these aspects are as follows.

-

Women’s personal and work-life attributes Although it has been found that female accountants are intelligent, firm, assertive, competitive, and achievement-oriented (Davidson & Dalby, 1993; Maupin, 1993), in the development of research, they are perfectionists, meticulous, cautious, and seek to cover a topic comprehensively without their level of productivity being affected (Mynati et al., 1997). Some studies indicate that women are considered weak, indecisive, uncompetitive, with a low level of self-confidence, and with little capacity to handle pressure (Barker & Monks, 1998; Tessens et al., 2011).

-

Theory of human capital Various studies recognize that women currently negotiate their roles to perform both as "good" academics and "mothers" (Haynes & Fearfull, 2008; Huopalainen & Satama, 2019). However, according to the theory of human capital, enunciated by Smith (1952) in 1776 and developed by labour economists, the type and amount of investment made by women in said capital translate into reduced skills, wages, and productivity; less or slower professional advancement, and an unbalanced distribution of working time between teaching and research (Bellas, 1994; Maranto & Streuly, 1994; Ruane & Dobson, 1990; Schaefer & Zimmer, 1995; Smart, 1991). When talking about human capital, reference is made to aspects such as:

-

Education At the doctoral level, there has historically been a shortage of female PhDs (Baldarelli et al., 2016; Heath & Tuckman, 1989; Norgaard, 1989; Toutkoushian, 1999). Moreover, although the number of female doctors has increased (Baldarelli et al., 2016; Baldwin et al., 2012), additional efforts are still required so that their participation in the academy is considered equal (Brown-Liburd & Joe, 2020; Jordan et al., 2006).

-

Work experience Although already Ferber et al. (1978) revealed that 84.3% of women had worked full time and without maternity leave, it is still considered that they have less work experience due to discontinuous career patterns caused by breaks, leaves and part-time agreements to fulfill maternity and parenting responsibilities (Pyke, 2013; Baldarelli et al., 2016), in addition to being high-cost workers due to their higher levels of absenteeism and turnover (Gago & Macías, 2014; Whiting & Wright, 2001).

-

Work commitment Since the 1990s, professional aspirations have been similar between men and women (Barker & Monks, 1998; Collins, 1993). The patriarchal vision, predominant in academia, considers that women make less effort than men in terms of their professional progress, anticipating their possible job leave, dedicate themselves to motherhood, nurturing, care, and the education of children (Pyke, 2013; Tessens et al., 2011; Whiting & Wright, 2001).

-

-

Time lag In line with human capital attributes, the hypothesis of the pipeline phenomenon postulates that since efforts to reduce discrimination began to bear fruit in the 1970s (Baldarelli et al., 2019; Lehman, 1992; McKeen & Richardson, 1998; Norgaard, 1989; Ried et al., 1987; Walker, 2008), women had a late entry into the academic accounting profession (Broadbent, 2016; Norgaard, 1989). Therefore, they have a younger career age or less professional maturity and have yet to have time to reach the top (Jordan et al., 2006; Metz & Harzing, 2009; Tessens et al., 2011). At the same time, the ‘leaky pipeline’ hypothesis refers to the fact that the desertion rates of women in academic positions are higher than men, and this occurs just when they have the qualifications and experience to access higher levels of academia (Baldarelli et al., 2016; Edwards et al., 2018; Pyke, 2013).

Regarding discrimination and associated phenomena, our patriarchal background gave rise to affirmations like those made by Ferber et al. (1978), who affirmed that “women are treated unequally because they are unequal, not because of discrimination” (p. 2) or by Raymond et al. (1988) who suggest no discrimination against women, being approved and generalized socially, occupationally, and academically. Nevertheless, various studies have recently identified that the differential between men and women in academia with the same qualifications in terms of recruitment, hiring, promotion, tenure, status, teaching load, and remuneration is mainly attributed to the structural and systemic gender discrimination in organizations (Baldarelli et al., 2016; Broadbent, 2016; Gago & Macías, 2014; Lee & Won, 2014; Whiting & Wright, 2001).

Although it was claimed that there is no relationship between academic rank, productivity, and the marital and parental status of academics (Sonnert & Holton, 1996), more recent studies have found that being a woman, being married, and having children makes female researchers be seen as less committed (Cooper, 2001). It is a source of discrimination, hinders her academic career, hinders promotion, and constitutes the foundation of the glass ceiling (Broadbent, 2016; Cooper, 2001; Whiting & Wright, 2001).

One of the women’s first experiences of discrimination occurs during pregnancy (Cooper, 2001). From this moment, they begin to receive derogatory comments; their benefits are cut off, they face obstacles that are difficult to overcome (Dambrin & Lambert, 2008; Tessens et al., 2011) or are fired based on the belief that children and their care are a women’s responsibility: they are forced to give up their careers, reduce their professional aspirations, submit to greater pressure to adjusting to family and professional responsibilities (Haynes & Fearful, 2008), sacrifice their marital and family life to advance professionally (Turner Lomperis, 1990), and to break the glass ceiling and be successful (Whiting & Wright, 2001; Windsor & Auyeung, 2006).

Women and publications as a priority in the current academic system

Ultimately, the different theoretical references reaffirm that the labour market considers the ideal employee focused on work and earning a living without marital, family, or domestic responsibilities (Acker, 2006; Davies & Frink, 2014).

On the other hand, universities have adopted a business, managerial, competitive, and marketing orientation focused on achievement and results for around three decades (Beattie & Goodacre, 2012; Locke & Lowe, 2008). The papers published in top-tier journals are the main criteria used by stakeholders, businessmen, media, research evaluation agencies, government, business agencies, accreditation agencies, and the community in general for the achievement of financing and investment international accreditations, growth, recognition, image, brand, institutional status, recruitment and retention of students (Beattie & Goodacre, 2012; Chan et al., 2006; Edwards et al., 2013; Fogarty & Liao, 2009; Hopwood, 2007, 2008).

Universities have prioritized research and publications in top-level peer-reviewed journals (Carnegie et al., 2003) over teaching, administration, or service (Gaudet et al., 2022). The authorship of papers in top-level journals has become the criterion for granting scholarships and project grants, achieving hiring, promotion, tenure, awards, economic incentives, and salary increases. Likewise, for college and university professors, publishing is an indicator of reputational and cultural capital, research quality, professional recognition, success, experience, productivity, standing, and professional advancement (Beattie & Goodacre, 2004, 2012; Bonner et al., 2006; Edwards et al., 2013; Moizer, 2009).

However, there is a tendency to assign academic and student care tasks to women (Gaudet et al., 2022; Haynes & Fearfull, 2008) instead of activities that allow them to advance in the "commercial" publication scheme that is in force today (Beattie & Goodacre, 2012). Thus, Baldarelli et al. (2016) find that women have different publication opportunities than men.

As Raddon (2002) and Gaudet et al. (2022) point out, academic success is related to the reputation someone achieves through publications that are products of their research more than through teaching, administration, and caring, pastoral activities. It is crucial to understand the participation of women as paper authors in top-tier journals to assess the conditions of gender in accounting academia over time (Williams et al., 2015). Thus, it is worth validating the following hypothesis:

Hypothesis 1a

Women are considered a minority due to their low representation of cost and management accounting papers authors in top-tier journals.

Given that the volume of published papers is considered a critical component of the status, advancement, and remuneration of academics and has been used as the main measure of authors’ productivity and performance (Beattie & Goodacre, 2012; Brown et al., 2007; Chan et al., 2007; Stephens et al., 2011), it is key to observe at the group of most prolific authors and determine their composition by gender.

Hypothesis 1b

Among the most productive authors in cost and management accounting, there is a higher proportion of men.

Previous studies have shown that in the case of papers written by one author, there is no doubt about the contributions’ origin, responsibility, and accreditation (Peidu, 2019). Therefore, in some cases, these types of papers imply greater prestige and importance for professional progression (Williams et al., 2015), and it has been used as a measure of research success previously (Larivière et al., 2013; Metz & Harzing, 2009; Miller et al., 2005). Considering the situation of women in academia over time, we are interested in validating the following hypothesis:

Hypothesis 2a

There is a lower presence of women as sole authors.

However, in recent decades there has been a positive trend toward larger teams of authors in published papers (Gaunt, 2014; Kumar & Ratnavelu, 2016; Wuchty et al., 2007).

Thus, given the focus of the academic world on papers, studies indicate that it is not considered important to be only an author. However, it is strategic to achieve a dominant position (Van Praag & Van Praag, 2008) that accredits the responsibility and relative contribution that each one has made (Haeussler & Sauermann, 2013; Helgesson & Eriksson, 2019; Peidu, 2019; Sauermann & Haeussler, 2017; West et al., 2013), since this plays a vital role as a basis for scientific merit and performance (Helgesson, 2020), allowing the identification of outstanding researchers, and has important academic, social and financial implications (Corrêa et al., 2017; Frandsen & Nicolaisen, 2010; Tscharntke et al., 2007; West et al., 2013). However, there is no consensus or clarity on how authors are presented in scientific publications: this varies between (and within) countries, disciplines, groups of researchers, and institutional settings, and even among informal rules (Costas & Bordons, 2011).

Various strategies are followed to determine the order of authors in publications. According to the literature, the most representative are (i) alphabetical order (using as a criterion the initial of the author’s surname: under this approach, all authors have made the same contribution to the study) (Efthyvoulou, 2008; Laband & Tollison, 2006; Marušić et al., 2011; Van Praag & Van Praag, 2008; Waltman, 2012); (ii) in order of contribution (where the first author makes the most significant contribution) (Frandsen & Nicolaisen, 2010; Peidu, 2019; Van Praag & Van Praag, 2008; Waltman, 2012); and (iii) by seniority (where the first author usually is starting his academic career, is a junior or doctoral student, while the last authors are supervisors, veteran leaders or senior staff, who drive the research both intellectually and financially) (Costas & Bordons, 2011; Tscharntke et al., 2007).

It is shown in various studies that in economics and related subjects, the authors are mainly listed alphabetically (Efthyvoulou, 2008; Einav & Yariv, 2006; Helgesson & Eriksson, 2019; Joseph et al., 2005; Laband & Tollison, 2006; Van Praag & Van Praag, 2008; Waltman, 2012). However, the order of authors’ according to their contribution is the formal policy suggested by APA standards (Efthyvoulou, 2008; Hart, 2000; Joseph et al., 2005). It is the general guideline in most disciplines and the convention used by professional bodies, editors of scientific journals, and a large number of academics, who interpret first place as a greater scientific contribution and, therefore, academic merit (Efthyvoulou, 2008; Frandsen & Nicolaisen, 2010; Peidu, 2019).

Additionally, the position of the first author is important because some search engines give them exclusive visibility. There is a tendency to associate emblematic works with the name of the first author (Kumar & Ratnavelu, 2016). They have greater rememberability due to the alphabetical presentation of the references (Efthyvoulou, 2008) and the fact that often only the first author is mentioned, and the rest are abbreviated as ‘and co,’ ‘and others’ or ‘et al.’ (Einav & Yariv, 2006; Peidu, 2019; Van Praag & Van Praag, 2008). Thus, authors listed in the first place (either due to their higher level of contribution or because their last name begins with a letter before in the alphabet) enjoy advantages such as the increased probability of having papers with greater downloads, readings, and citations. This helps them receive tenure, obtain scholarships and prestigious awards, achieve greater visibility and prestige, achieve professional recognition and a significant salary increase (Costas & Bordons, 2011; Efthyvoulou, 2008; Marušić et al., 2011; Van Praag & Van Praag, 2008).

For its part, the criterion of seniority has also been used traditionally (Tscharntke et al., 2007). It is based on the professional rank and age of the authors as a determinant of their function and, therefore, of the position they are listed (Costas & Bordons, 2011). In this sense, the last position is assigned to the supervisor, who represents experience, seniority, leadership, and success (Costas & Bordons, 2011; Gingras et al., 2008).

In conclusion, those who appear as the first and last authors of a scientific paper make the greatest contribution. Studies indicate that a certain number of first or last positions as an author in peer-reviewed papers is required to qualify for certain positions, promotions, or tenure (Helgesson, 2020; West et al., 2013).

In line with studies such as those by Larivière et al. (2013), Metz and Harzing (2009), and West et al. (2013) that analyse the position, recognition, and advancement of women in different fields of academia and given the disadvantageous situation of women in accounting academia and the relationship with publications and the order of authorship we formulate the following hypotheses:

Hypothesis 2b

There is a lower presence of women as first authors.

Hypothesis 2c

There is a lower presence of women as the last authors.

On the other hand, a variable positively related to the presence of women as authors of papers in top-tier journals is the proportion of women on the editorial board (Metz & Harzing, 2009).

With this, it is not proposed that gender diversity in the composition of the editorial board can lead to a lack of neutrality or objectivity that leads to a biased acceptance that favors (or harms) women (Addis & Villa, 2003). As mentioned by Metz and Harzing (2009), editors usually do not know the gender of the author or authors of the papers they review. However, in the practice of their role as "gatekeepers of knowledge" (Brinn & Jones, 2008; Fogarty & Liao, 2009; Metz & Harzing, 2009), the editorial boards determine which research perspectives are accepted (thematic areas, types of documents, methodologies, among others) (Addis & Villa, 2003; Dhanani & Jones, 2017; Lee, 1997; Parker et al., 1998).

Given that accounting research is primarily male-dominated (Carnegie et al., 2003) and accounting journal editorial boards remain largely male-dominated (Dhanani & Jones, 2017), statements such as those formulated by Oakes & Hammond in 1995 are still valid today. They assert that the "mainstream" research topics with greater acceptance and dissemination appertain to a male interest and approach. At the same time, women are frequently excluded as an object of research and are often ignored regarding other matters that may interest or affect them (Addis & Villa, 2003).

In this sense, greater gender diversity on editorial boards fosters equal opportunities (Dhanani & Jones, 2017). It promotes intellectual openness and innovative thinking (Parker, 2007) by favouring and recognizing alternative values, perceptions, ways of thinking, feeling, and acting (Carnegie et al., 2003). These are reflected in the openness and interest toward other perspectives and fields of research that are addressed mainly by women (Addis & Villa, 2003; Metz & Harzing, 2009; Metz et al., 2016).

Women authors of papers in top-level journals are the ones who can form part of the editorial boards of such journals (Metz & Harzing, 2009). Consequently, they achieve benefits such as establishing, consolidating, and reformulating dominant, legitimate, and accepted research perspectives (Dhanani & Jones, 2017; Fogarty & Zimmerman, 2019); accessing to greater resources for research (time, data, human talent) (Brinn & Jones, 2008; Fogarty & Liao, 2009); being part of renowned academic networks; and achieving more reputation, prestige, influence, power and better economic conditions (Brinn & Jones, 2007; Swanson et al., 2007).

As stated by Metz and Harzing (2012) and Geisler et al. (2007), the participation of women in editorial boards has a direct relationship with the climate and career of women in the academy. Therefore, the relationship between the proportion of women on the editorial board and as authors represents the current state of women in the accounting community and potentially on future editorial boards. It is, therefore, worth validating the following hypothesis:

Hypothesis 3

There is a greater presence of female authors in journals whose editorial board has a greater female presence.

Historically, according to the neoclassical view of salary differences (Bellas, 1994), gaps in terms of remuneration and the general status of women in relation to men are attributed to lower productivity (Addis & Villa, 2003; Larivière et al., 2013).

In this sense, several studies have used citations as a measure of productivity (Larivière et al., 2013; Stock et al., 2022), quality (Lehmann et al., 2006), impact (Lin et al., 2013) and success (Miller et al., 2005), associating that the number of authors’ citations impacts academics’ public relations, recognition, reputation, appointments, promotions and tenures, salaries, and the achievement of awards (Beattie & Goodacre, 2012; Lehmann et al., 2006). It is necessary to analyse another possible factor in the origin of gender disparities in accounting academia. Therefore, we will validate the following hypothesis:

Hypothesis 4

Women have lower numbers of citations.

Methodology

Data and sample for analysis

Given the heterogeneity of the labour market and the academic field (Blättel-Mink et al., 2009), authors such as Ruane and Dobson (1990) suggest that empirical analyses concerning gender discrimination and its implications should focus on relatively small homogeneous subgroups. On the other hand, according to Englebrecht et al. (1994), the degree of difficulty and the potential to publish is different for all areas in the academic field. Therefore, the field of analysis of this work is limited to cost and management accounting.

As a source of information to carry out the analysis, all papers published during the period 1960–2019 from the following journals were manually compiled: Journal of Accounting Research; Accounting Review; Management Accounting Research; Journal of Accounting & Economics; Accounting, Organizations and Society; British Accounting Review; Accounting, Auditing & Accountability; Critical Perspectives on Accounting; European Accounting Review; Journal of Accounting and Public Policy; Contemporary Accounting Research; and Review of Accounting Studies.

These journals were selected following several criteria: (i) They have a clear focus on accounting and publish papers on cost and management accounting (Carmona et al., 1999). (ii) Studies such as that by Chan et al. (2006) that analyse research productivity consider a 12-year period adequate. In our case, the newest journal has been published for 23 years. (iii) According to the perception of academics in the field, these journals are classified as having a higher level of quality and could therefore affect the status and benefits of academics (Beattie, 2005; Beattie & Goodacre, 2004). (iv) These journals correspond to the highest quality refereed publications according to the impact factor in the ISI journal citation report, based on the average number of citations compiled by the Social Sciences Citation Index (SSCI) of Web of Science (WOS). They have remained in the top-quality categories (Q1 or Q2) for five straight years. Journals from this category were chosen as they imply a similar level of demand; therefore, there is no bias between quality and quantity (Toutkoushian, 1994).

From these journals, we obtained all documents classified as research papers, for which we collected the year, volume, number, title, authors' names, pages, keywords, and abstract. We exclude introductions, forewords, editorials, book reviews, notes, reports, conference reports, tributes, obituaries (and documents in memoriam), hall of fame, reflections, or points of view since they usually do not offer the same review processes or require the same scientific criteria (Carnegie et al., 2003; Chan et al., 2006; Swanson et al., 2007).

Based on the available information, each of the authors classified the papers as belonging to the area of cost and management accounting or not. In case of divergence, the paper’s specific content was reviewed until a consensus among the authors was reached, a procedure used in previous works (Chan et al., 2006). In this way, we obtained 1798 cost and management accounting papers.

Thus, we obtained a base of authors whose names we reviewed in detail to unify them since many of them are listed differently in each paper. For example, Smith Robert M., Smith RM, Smith R. M., or Smith Bob; we used institutional affiliation over time as a criterion. We obtained 1916 authors and we determined their gender. In the first instance, we reviewed the biographies (and photos) that appear on the web pages of the universities where the authors are currently linked, detailing if they were referred to as "he" or “she.” We then reviewed the bibliographies in the papers or other academic pages in which the authors were mentioned, detailing in the same way if they were referred to by “he” or “she.” We also determined gender by searching for the name on internet pages, following studies such as those by Dhanani and Jones (2017). If there was still no clarity or no information was available, we coded the gender of these authors as “missing.”

Considering the proposed analyses, in cases where the author’s gender was missing, or the pages of the paper were missing, we eliminated the publications from the initial database (this way, some co-authors also left the database). In summary, we eliminated 49 papers (2,8%) and 115 authors (6%) in total, of which 43 (2.24%) are of unspecified gender, 11 women (0,57%), and 61 men (3,18%). This is a small proportion of the data that is unlikely to distort the results presented here. Finally, our author database comprises 1801 authors (1388 men—77.07% and 413 women—22.93%).

At the same time, we followed a similar process for the editorial boards. We manually compiled each year, volume, issue, and editorial composition; where they were unavailable, we accessed the hard copies. Once we had the list of members, we unified their names and manually determined their gender (following the same path as for the authors). We excluded the Review of Accounting Studies from this analysis because of the lack information during the period studied. For the other journals, we did not find information on the editorial board in 2.6% of cases, and we could not determine the gender of 0.24% of members.

Likewise, for each paper, we consulted the citations it received in Google Scholar and Web of Science and the citations accumulated by each author on our database.

Variable measurement

The variables we determined from our database are presented below, specifying the type of variable it is and its definition (Table 1, 2).

Descriptive statistics

Results and discussion

To test the first hypothesis, to measure the presence of female authors from 1960 to 2019, we observed the female and male presence in authorship (without suppressing the multiplicity of those authors who have written more than one paper) at a general level and by a journal.

According to Fig. 1, we found that, of total authorship, women are considered a minority population, corresponding to only 19.63% of the authors of cost accounting and management accounting.

Author distribution by gender: classification by gender of the general database of authors

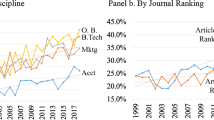

If we evaluate the situation by journal, according to Fig. 2, we find that of all the authors who have written about cost accounting and management, the highest participation of women corresponds to only 27.98% (Contemporary Accounting Research).

Female authorship per journal: proportion of women out of all authors, classified by journal

Considering that women’s professional progress has been dynamic and progressive, it is key to see their evolution. A referential moment is the end of the 70s and the beginning of the 80s when there was a greater representation of women in the profession as university graduates, CPAs (Cooper, 2001; Honeyman, 2007; Ikin et al., 2012; Ried et al., 1987), or PhDs (Heath & Tuckman, 1989; Norgaard, 1989; Toutkoushian, 1999), as well as increased recruitment, participation in the workforce and career progression, and an improvement in salary. At the same time, in the 1980s, the incorporation of women into academia began to be significant, and the gender gap decreased (Lehman, 1992; McKeen & Richardson, 1998; Turner Lomperis, 1990; Walker, 2008). Consequently, we observed the presence of women in the authorship of papers (without considering whether an author had written more than one paper) for different periods.

Table 3 and Fig. 3 show that men’s participation has decreased while women’s is rising. It has gone from female participation of 1.61% from 1960–1980 to 29.34% from 2010 to 2019. Although these data are still far from parity, the evolutionary character that has occurred over time is highlighted.

Author participation by gender: percentage distribution of the gender of authors over time

This minority but evolving participation of women can be confirmed with the analysis presented in Table 4, which shows greater participation in the author teams. It is striking that the teams of exclusively male authors (0% women per paper) went from 97.5% between 1960–1980 to 48.01% in 2011–2019. However, the frequency of teams of authors made up of 33%, 50%, and 100% women, although it has increased over time, even for the years 2010–2019, is very low since it corresponds to only 14.68%, 18.16%, and 11.94% respectively.

According to the previous results, and consistent with parallel studies, there is a clear gender gap between the authors, with a majority male presence (Baldarelli et al., 2019; Carnegie et al., 2003; West et al., 2013; Williams et al., 2015). Thus, over time in the accounting academic community, women are considered a minority due to their low representation as authors, validating hypothesis 1a.

To analyze a more specific niche, in a first analysis, following the works of Brown (1996), Chan et al. (2006), and Lee and Williams (1999), we determined the first quartile of the most productive authors. To do this, we analyze the relative contribution of the authors (distributed among the total number of authors) in terms of papers and pages written.

We find that, whether using the number of papers or pages as productivity criteria, the first quartile of most productive authors is mostly men (83.18% and 74.34%, respectively) (Fig. 4).

Most productive authors: gender of the most productive quartile of authors, measured by the relative contribution (in papers and pages written)

Following Brinn and Jones (2008), Lukka and Kasanen (1996), and Rodgers and Williams (1996), an alternative to analyse the concentration in productivity is to observe the presence of authors in several journals. The results obtained (Table 5) reveal that, in general, the participation of authors (both women and men) in more than one journal (concentration) is low (427 authors, 23,71%). Of this minority of authors who write in more than one journal, only 90 are women, corresponding to 5% of our total sample of authors of 1801. Three women (0.17%) have published in 5 of the 12 journals in our sample. No women published in six out of the twelve journals in our database, while at least six men hold this achievement.

Thus, using three different criteria, we confirm that there is a higher proportion of men among the most productive authors, with which we validate hypothesis 1b.

Moving on to the second group of hypotheses, per previous studies, we find that there is an increasing trend in the average number of authors over the years in the area of cost and management accounting (Fig. 5) (Kumar & Ratnavelu, 2016; Wuchty et al., 2007).

Authors per paper: average number of authors per paper over the years

Previous research attributes this increase in co-authorship to benefits such as the intellectual fusion that allows the integration of various fields of expertise of the authors. That synergy allows the research’s result to be greater than the sum of its parts, an efficient division of work, higher quality, higher probability of being published, higher levels of citation, better redistribution of the risk of failure in the editorial process, higher pay taking into account the opportunity cost of academics’ time, and even higher productivity (Ductor, 2015; Kumar & Ratnavelu, 2016; Laband & Tollison, 2000). However, as seen in Fig. 6 and Table 6, 40.08% of the papers have been written by single authors, of which 86.73% are men.

Composition of author teams: graph of the frequencies of the number and gender of authors per paper

Although studies such as those by Edwards et al. (2018) and McDowell et al. (2006) find that both genders are more likely to collaborate with researchers of the same gender, this is valid only for men, as we have found out in our research. This is supported by previous studies of other disciplines (Lee & Bozeman, 2005; Williams et al., 2015) (Fig. 6, Table 6). For teams of two and three authors (36.13% and 20.24%, respectively), 64.87% and 50.28% are made up only of men, while 5.85% and 3.39% are made up only of women. 29.27% and 46.33% are mixed teams for two and three authors, respectively. Thus, the papers written by three authors have the highest participation of mixed teams.

Specifying the evolution of women as sole, first, and last authors over time, we found that women's participation as sole authors has increased from 0.50% between 1960 and 1980 to 27.63% between 2010 and 2019 (Fig. 7 and Table 7). However, this value is still far from parity, which confirms hypothesis 2a, which indicates a lower presence of women as sole authors.

Gender of sole authors: Percentage composition of unique authors by gender over time

Following previous studies (Larivière et al., 2013; West et al., 2013), we find that this same pattern is followed in the analysis of the first (Fig. 8 and Table 8) and last author (Fig. 9 and Table 9). Although the participation of women is growing, recently, there is still a lower presence of women as first (32.92%) and last authors (21.12%), with which we validate hypotheses 2b and 2c.

Gender of first authors: Percentage composition of first authors by gender over time

Gender of last authors: percentage composition of last authors by gender over time

Although the scope of this work is to describe the participation of women as authors in top-tier journals and not to find the exact causes that generate such gender disparities. We present a bibliographic review of what the previous literature recognizes as aspects that can affect the participation, visibility, and presence of women authors at a general level, specifically as sole, first, and last authors, without intending to link the reasons one by one with the results.

For this, the first thing to consider is that, as we mentioned in the first section, the differences in the status of women, in general, can be due to two causes. The first is associated with less investment in human capital, which leads to reduced productivity. The second is related to discrimination schemes that affect women’s performance in the same way.

In this sense, the first verification is related to the differences in productivity by gender. We calculated a mean difference of the relative contribution in the number of pages and the number of papers written. Our results (Tables 10 and 11, respectively), in line with previous studies such as those by Abramo et al. (2009) and Lee and Bozeman (2005), reveal that there is a significant difference between the number of papers and pages written between men and women, where the female contribution is low.

However, we made a mean difference test between the average time men and women take to publish their next paper to see if it is related to a difference in the women’s capability to generate intellectual production from the authors with more than one paper in our database. We found (Table 12) no significant differences between them in any period. Even (although we do not reveal it in the tables), we observe with the standard deviation that there is less variation in women’s productivity. In other words, women’s productivity is more homogeneous, while the level of productivity of men is much more irregular.

With this, women’s lower presence and visibility as authors have nothing to do with a lower production capacity. Quantitatively, it may be related to the fact that women have yet to achieve a critical mass that balances the amount of intellectual production that men have had over time. Theoretically, we compile some factors the literature recognizes may affect said productive capacity.

-

Work-life balance Considering traditional gender roles, women are responsible for the home, care, and family. There is a clear difference between men’s and women's academic career patterns according to their personal and family situations (Broadbent, 2016; Norgaard, 1989). Marriage has positively affected men's careers, resulting in a higher publishing rate, rank, professional title (Ph.D.), and salary (Sonnert & Holton, 1996). In contrast, the pattern of professional motivation for women is L-shaped, high at the beginning of their career but falling upon entering marriage (Lee Cooke & Xiao, 2014). Regarding pregnancy, women are pressured to align three clocks—the biological, the professional (stage of tenure), and the spouse’s professional (Baldarelli et al., 2016). The time when academic women can be hired (once they have finished their Ph.D. and have some post-doctoral experience) is the same time couples are thinking about having a family, and the woman assumes the negative professional consequences while prioritizing the man’s career (Broadbent, 2016; Sonnert & Holton, 1996). In caring for the home, the marriage, and the family, whether by force or choice, women spend a disproportionately greater amount of time dedicated to such tasks. At the same time, men usually free themselves from these activities (Haynes & Fearfull, 2008) and dedicate their time to achieving salary raises and career advancement. Thus, women are forced to survive or choose between two conflicting roles: on the one hand, being wives, mothers, and housewives, and on the other, their academic progress (Raddon, 2002; Tessens et al., 2011). They face greater time and energy restrictions and experience greater stress levels when applying for leadership positions or focusing on research (Haynes & Fearfull, 2008). This can be translated into different rates of time, dedication, and productivity in research and, consequently, lower participation and visibility of women as authors (Bellas, 1992; Cooper, 2001; Tessens et al., 2011).

-

Non-mainstream research areas, methodologies, and perspectives There is a dominant empirical, positivist, quantitative, and statistical research school (Carnegie et al., 2003; Hopwood, 2008; Lee, 1995; Locke & Lowe, 2008; Panozzo, 1997) that mainly studies Anglo-Saxon contexts (Brinn & Jones, 2008; Jones & Roberts, 2005; Khalifa & Quattrone, 2008; Lee, 1995; Tinker & Fearfull, 2007) and whose approach is consistent with top-tier journals. Men are more inclined towards these topics and methodologies, so they achieve greater publications, acceptance, prestige, status, and reputation. This allows them to have more colleagues willing to be their co-authors, resulting in more publications (Carnegie et al., 2003; Dhanani & Jones, 2017). However, women tend to investigate history, gender, diversity, behavioural accounting, and social accounting (Metz & Harzing, 2012) from different critical, ontological, epistemological and non-positivists perspectives in non-traditional contexts (Carnegie et al., 2003; Oakes & Hammond, 1995). This kind of research is considered suspicious, subjective, or low-level for the mainstream academia and, therefore, ends up marginalized and silenced (Özbilgin, 2004). Thus, women are more likely to fail in the publication process in top-tier journals (Panozzo, 1997; Tinker & Fearfull, 2007).

-

Old boy network or organizational homosociality Such as in business (Barker & Monks, 1998; Windsor & Auyeung, 2006). In academia, there has been an institutionalized male social network (old boy network) (Bellas, 1992; Ferber, 1988; Norgaard, 1989; Tessens et al., 2011) that is select, elitist, and exclusive to successful, high-status, and reputable men with similar university origins, training, hobbies, and lifestyle. They participate in informal social gatherings outside office hours, where they share their affinities in terms of stereotypically masculine sports and leisure activities (for example, Gaelic games, rugby, soccer, and golf) (Dhanani & Jones, 2017; Metz et al., 2016; Khalifa, 2013). This makes them intertwine their professional and personal lives, and thanks to this, they accumulate social capital, exchange information, achieve informality in their relationships, form alliances, and benefit in the work and academic sphere, increasing their productivity (Baldarelli et al., 2019; Haynes, 2017). Not necessarily having the same tastes and affiliations, women are excluded from achieving high-level academic and professional relationships, integration, and success (Anderson Gough et al., 2005). At the authorship level specifically, women have less chance of achieving intellectual collaboration and synergies for co-authorship and less access to high-level academics (with higher productivity). As a result, they faced limited options to collect and disseminate research results, exchange manuscripts, become familiar with the research topics and perspectives from the mainstream academic community, get feedback and disseminate their research interests, projects, and academic achievements, and, ultimately, achieve parity in the publication in top tier journals (Addis & Villa, 2003; Khalifa, 2013; Shearer & Arrington, 1993; Tessens et al., 2011).

-

Assortative matching hypothesis Previous studies have shown that the formation of work teams is not randomly done but in favour of productivity (both in quality and quantity) and the reputation of academics (Ductor, 2015). It has also been determined that gender is a variable that affects co-authors’ selection (Boschini & Sjögren, 2007; Ivanova-Stenzel & Kübler, 2011). In keeping with the old boy network postulate, collaborations are probably between male authors with similar skills and productivity and graduates of schools of the same rank. Consequently, following the postulate of homosociality (Khalifa, 2013), women are usually paired with relatively lower-quality co-authors. They are less likely to associate with higher-level authors, affecting their productivity (measured in quantity and quality), their position as first or last author, and the consequences that this implies for their academic career (Boschini & Sjögren, 2007). This is reflected in the case of cost and management accounting, observing the top 25 percent of most productive authors (measured by relative contribution to papers and pages written). The vast majority have male co-authors (Table 13), reflecting the limitation women have to access academics with higher status and productivity.

-

Matthew effect Taking into account the two previous aspects, it is worth mentioning the Mathew effect, which is related to what is stated in the Gospel according to Saint Matthew “For whosoever hath, to him shall be given, and he shall have more abundance; but whosoever hath not, from him shall be taken away even that he hath” or in other words, it corresponds to the logic that “the rich get richer, and the poor get poorer.” Based on the above, Merton (1968) points out that, in the field of science, certain eminent scientists (according to our figures, men) make contributions such that they achieve rewards (social validation, recognition, prizes, status, honor, or esteem). Due to psychosocial processes, the scientific community and society give them disproportionately large credits and, in a stratification system, place them in a “superior” position. This, in turn, makes available new resources (human talent, information, networks, etc.) and opportunities that allow them to have greater achievements and, thus, more and more recognition, like a snowball. In this stratification, there is another group of scientists (according to our figures, women) with similar talents, merits, and contributions to science than the previous scientists but did not obtain any award or recognition and, therefore, remain anonymous, receiving credit disproportionately low for matching contributions. According to recent research, this phenomenon is still valid in the current academy (Drivas & Kremmydas, 2020; Medoff, 2006; Teixeira da Silva, 2021) and may harm the academic well-being and prosperity of women.

-

Queen bee syndrome This is a phenomenon initially described by Staines et al. (1974), who points to the "queen bees" as women who have been successful in contexts dominated by men (such as science and accounting), behaving with stereotypically masculine characteristics to adhere to the social identity of the context and, thus, entrench themselves in their leadership position and protect their achievements. In addition, they denigrate other women (who try to enter their circle or seek to ascend), appealing to discriminatory arguments against women (for example, low commitment, assertiveness, low qualifications, and professional skills). Recent studies indicate that this is a persistent phenomenon (Derks et al., 2011) in science (Ellemers et al., 2004) and academia (Faniko et al., 2021), and this may affect the intention of high-level women to co-author, as well as indicating a lower propensity to act as supervisor, role models or mentors for other women.

-

Mentoring – Role models Mentoring relationships are between a senior professional who acts as a mentor and provides help to a junior professional to advance professionally. To do this, it carries out career activities (protection, exposure, visibility, coaching, and feedback), psychosocial activities (acceptance and confirmation, friendship, and counseling) and acts as a role model (Blake-Beard et al., 2011) (constituting an example of success or an inspiring model (Lockwood, 2006) that allows a junior professional to see the objectives that can be reached and the path that must be followed to achieve them (Herrmann et al., 2016). According to previous research, people need to feel interpersonal comfort on the one hand (Allen et al., 2005) and that someone like them has been able to succeed (Lockwood, 2006). Therefore, various studies have highlighted the importance of gender coincidence in mentoring relationships and the role model figure (Allen et al., 2005; Lockwood, 2006). Women need to know that another woman has succeeded (Blake-Beard et al., 2011) despite the stereotypes and gender gaps, as well as the masculinized workplaces they face (Lockwood, 2006). When this occurs, their relationships become interdependent, close, or enriching (Cullen, 1993), making junior women professionals integrate their role models' professional skills and personal characteristics into their professional and personal lives (Gilbert, 1985). In this way, they affirm their academic and professional objectives; they feel identified and motivated, and thus, their performance improves their perceived success (Herrmann et al., 2016). They achieve greater promotions, higher income, and greater satisfaction (Ensher & Murphy, 1997).

However, the accounting area has traditionally lacked women to provide mentoring (Adapa et al., 2016; Barker et al., 1999; Collins, 1993; Viator & Scandura, 1991) and to act as role models (Adapa et al., 2016; Barker & Monks, 1998; Collins, 1993; Ogharanduku et al., 2021). This affects the performance and productivity of women accounting scholars and their ability to partner with other women. For example, exclusively female co-author teams represent only 8.18 percent (Table 6).

-

Self-promotion and female modesty One aspect that socially identifies women as more ‘feminine’ is modesty in their achievements (Daubman et al., 1992; Rudman, 1998) and a genuine concern for and commitment to the harmony and wellbeing of others and groups, emphasizing similarities and connections (Hentschel, 2019; Rudman, 1998; Spence & Buckner, 2000). In other words, women are prone to cooperatives and communalism (Hentschel, 2019; Rudman, 1998), while men culturally and traditionally have been focused on agentic values such as individuality, leadership, hierarchy, achievement, and self-promotion (Daubman et al., 1992; Hentschel, 2019; Rudman, 1998; Spence & Buckner, 2000). In this scenario, women, to increase the other's liking for them, to avoid an interpersonally uncomfortable situation, and to protect the other's feelings about themselves, may be limited when it comes to presenting their abilities, achievements, status, and attractiveness (Daubman et al., 1992; Daubman & Sigall, 1997). Ultimately, this represents that women minimize their abilities or achievements and conform more than men in public settings (Daubman et al., 1992; Eagly, 1987), which in our study may suggest a disadvantage for female authors when negotiating the order of authors’ positions.

Continuing with the third hypothesis, first, we observe female participation in editorial boards. Following previous papers (Addis & Villa, 2003; Carnegie et al., 2003) and according to Fig. 10, there is an increase over time in the participation of women as members of editorial boards.

Women in editorial boards: Average participation of women on editorial boards over time

However, looking at the average participation (Fig. 11 and Table 14), the journal with the highest involvement of women in such an instance is Critical Perspectives on Accounting, with a percentage of 25%. The editorial board with the highest female participation has been achieved in the same journal with 40% women. However, looking at the highest numbers, 36% and 32%, accounting journals have yet to take steps towards equality and diversity on their editorial boards.

Women in editorial boards per journal: average participation of women on editorial boards per journal

Table 15 shows the connection between the proportion of female authors and the presence of women on the different journal editorial boards over time. A positive and significant confirmation exists for the studied period (i.e., 1960–2019). However, when separating the sample by decades, this connection weakens and loses its statistical significance as the oldest periods are eliminated from 2000 onwards. Consequently, although there is a positive connection between the number of female authors and the number of women on editorial boards (allowing us to accept Hypothesis 3), it is possible that, over time, this connection will become significant for the entire sample.

To understand and dimension this situation, it is worth noting that the editorial boards are a select group of individuals who have graduated from high-status schools with power, success, recognition, reputation, status, and position as research experts in a particular discipline (Metz et al., 2016). According to the theory of homosociality, groups seek, enjoy, and prefer the company of people with similar backgrounds, inclinations, values, and characteristics (Lipman-Blumen, 1976). Since the composition of the editorial board has historically been homophilic and isomorphic, the access and participation of women in these groups are limited (Brinn & Jones, 2007; Fogarty & Zimmerman, 2019; Metz et al., 2016; Swanson et al., 2007).

Likewise, the interest of women to entrench in their position means that, as described by queen bee syndrome (Staines et al., 1974), they seek to behave according to the masculine social norms stipulated by the context (Derks et al., 2011; Faniko et al., 2021), in this case for example according to the editors.

Thus, although it is expected that the presence of women on the editorial board favours the acceptance of alternative research perspectives (Addis & Villa, 2003), the fact that women do not reach a critical mass (Figs. 10 and 11, Table 14) limits the women’s ability to mobilize the focus of the journals to these new perspectives. Therefore, there is no greater participation of women as authors, and the low correlation can be explained.

To validate the fourth hypothesis related to possible gender gaps in citation patterns, we calculate the mean differences between the citations the papers have received. We took Google Scholar and Web of Science as references, assigned in an absolute and weighted way to the authors according to their gender. We also calculate the mean difference of the citations in the authors' profiles (from Google Scholar).

The results (Table 16) show that, from the point of view of citations of papers (assigned to their authors in absolute and relative terms), there is no significant difference by gender. However, analysing the Google Scholar profiles of the authors (last file of Table 16), we found a significant difference in the number of citations accumulated by men and women. Therefore, we reject the fourth hypothesis taking only our database of papers as a reference, but we validate it for our database of authors.

Previous literature does not show a consensus regarding citation patterns related to gender. Some studies indicate that women are cited more than men (Grossbard et al., 2021; Thelwall, 2018, 2020), and other studies affirm that men are cited more (Addis & Villa, 2003; Ferber & Brün, 2011; Larivière et al., 2011, 2013).

Although the causes for these differences are not clarified with precision, some studies state various aspects that may influence this relationship at a general level and that may be linked to the present results.

Since there is a positive correlation between the level of productivity and citations of authors (Tables 17 and 18), as there is a lower presence of women as authors of papers in top-tier journals, there is also a lower level of citations for them (from the authors’ point of view).

Significant differences exist between the number of publications and citations depending on the area of knowledge. The size of the community of authors is also a determining factor for the accumulation of citations (Dion et al., 2018). It is crucial to locate cost and management accounting, which corresponds only to 11.71 percent of published papers in accounting (Fig. 12). On the one hand, these results may indicate that we are taking a subsample (of both papers and authors) that must reflect the general accounting stage. According to the mainstream approach, men may achieve a greater impact, measured by citations, on topics that generate greater visibility, presence, status, and impact (Gago & Macías, 2014; Gonzalez-Brambila & Veloso, 2007). On the other hand, considering that academic communities as a social system (Beattie, 2005) are stratified (Bourdieu, 1988; Whitley, 1984), there is a group of dominant individuals or institutions (which in the accounting case, as we have seen, is mainly made up of men) (Brinn & Jones, 2008; Edwards et al., 2013; Williams et al., 2006) that can influence discipline’s future (Fogarty & Liao, 2009), defining legitimate accounting knowledge as relevant and of quality, restricting the production and dissemination of knowledge (Dhanani & Jones, 2017), determining what is produced, communicated, unified, reproduced, debated, reformulated, evaluated, archived and rewarded in terms of knowledge and e stipulating what are considered quality criteria (Brinn & Jones, 2007). The paradigms, thematics and methodological interests of an area and its political declarations are represented by a reduced and selected group of (male) academics (Fogarty & Liao, 2009).

Evolution of the number of papers in accounting, cost accounting and management, and the gender of the authors: proportion of cost accounting and management papers over time. Evolution of the percentage of women and men as authors

Along these lines, studies have revealed that once universities or individuals have gained said privileged position, it is relatively easy to maintain (Lee & Williams, 1999). Its generational change involves keeping researchers focused on what they have learned. Self-proclaimed as “the most promising areas” or “methodological ideals” (Lukka & Kasanen, 1996, p. 771), once it becomes apparent that the non-elite (in this case, women authors) can reach this terrain, this elite proclaims new themes in which they can continue to lead (Fogarty & Zimmerman, 2019). As reflected in Fig. 12, when participation in cost and management accounting papers decreases, this is when the proportion of men as authors decrease and women increase.

Given that male authors tend to cite people of the same gender (Ferber & Brün, 2011; Knobloch-Westerwick & Glynn, 2013; Tekles et al., 2022) and that women authors are still considered a minority in the accounting academy (Figs. 1 and 2, Tables 3 and 4), we can see that the gender gap in the number of citations of authors has not been eliminated. Along the same lines, given that the Matthew effect refers to a phenomenon in which eminent and already famous authors and editors receive credit, citations, status, and influence and generate disproportionate recognition for their contributions, strengthening and enhancing their reputation more and more over time (Merton, 1968). Mainly men have achieved that top position in citations and recognition for their work. In contrast, there is the Matilda effect, which refers to ignorance of the work and contributions of women scientists who have been the main authors or have been co-authors of men who, due to the halo generated by the Matthew effect, have been given full credit for scientific achievements and discoveries (Rossiter, 1993). Said ignorance can ultimately translate into lower citations for female authors (Knobloch-Westerwick & Glynn, 2013). Considering men’s inclination for self-promotion (Daubman et al., 1992; Hentschel et al., 2019; Rudman, 1998; Spence & Buckner, 2000), they would be more inclined to create and update their profile for dissemination of academic achievements, such as Google Scholar. Therefore, they have greater visibility, dissemination, and presence. On the other hand, men have a greater inclination for self-citation (King et al., 2017; Wullum Nielsen, 2017). Therefore, by having more publications, they, in turn, achieve increasing numbers of citations (Rudman, 1998). In contrast, women, probably according to queen bee syndrome (Staines et al., 1974), cite authors regardless of gender (Knobloch-Westerwick & Glynn, 2013).

Conclusions

Findings

Despite the importance and recent interest in diversity, the accounting academic community is still predominantly represented by men as a reflection of the professional environment. In contrast, women are in a disadvantageous position in terms of recruitment, hiring, promotion, tenure, status, distribution of workload, and remuneration. Some authors have attributed those differences to the lower productivity of women in research outputs.

Considering the current dynamics of universities and the academic system, where productivity and visibility in research are prioritized and, specifically, in publications in top-level peer-reviewed journals, investigating the authorship of this type of output can be a way of approaching the gender gap that exists in the academy.

Therefore, this study analyzes women’s participation as authors in cost and management accounting. The results validate our first hypothesis, and we confirm that, although women have been gaining presence among the authors in cost and management accounting, they are still considered a minority group (H1a). Classifying these results by journal, the greatest presence of women as authors (27.98%) is in Contemporary Accounting Research. Likewise, we found that taking as a reference the relative contribution of the authors (measured by papers and pages written) as well as by the participation in several journals, the most productive authors are mainly men (H1b).

Regarding the second group of hypotheses, we confirm that although the presence of women as sole/first/last authors has increased over time, their participation is still lower than that of men for 2010–2019. corresponds to 27.63% (H2a)/32.92% (H2b)/21.12% (H2c), respectively.

The presence of women on editorial boards has been increasing over time. However, journals still need to focus on achieving more equitable teams in terms of gender since the highest average participation of women is held by the journal Critical Perspectives on Accounting, with 25.5%. Although it would be expected that a more significant female presence on editorial boards would lead to the opening of alternative research perspectives that would encourage women’s participation as authors, this only occurred from 1990 to 2019 (H3). Subsequently, between 2000 and 2019 we reject hypothesis 3, which postulates that there is a greater presence of women authors in journals whose editorial board has a prominent female presence.

Finally, we found that taking as a reference the citations that the papers from our database have received (in Google Scholar and Web of Science) and assigning them in absolute and relative terms, there are no gender differences. Therefore, we reject hypothesis 4, which suggests that women have fewer appointments for cost accounting and management papers from 1960 to 2019. However, looking at the profiles of the researchers in our database, we found that men have a significantly higher number of citations.

On the other hand, the theory points out two main factors that affect women's status: investment in human capital and its impact on productivity. The second contemplates the discrimination women face that affects their performance.

Although the results show that women have a lower volume of research products (papers and written pages), this does not respond to a lower productive capacity since they have the same publication rate as men. This suggests that numerically it responds to a lower presence of women as authors. Therefore, we present a review of the different phenomena related to differential and discriminatory behaviors, which may have affected women’s performance, such as the conflict they face between personal and work life, participation in non-mainstream areas, methodologies and perspectives, homosociality phenomena, assortative matching, the Matthew effect, the queen bee syndrome, lack of role models, and female modesty.

Implications for the academy

The results of this work are considered a call for institutional attention that we hope will provoke universities to review the gender composition of their academic teams to balance them. Consequently, universities must integrate alternative interests, methodologies, and research perspectives into the mainstream that mainly favor masculine, inbred, and traditional visions of reality. This will ultimately lead to constructing a dynamic, comprehensive, inclusive, pluralistic, diverse, and equitable discipline.

Our results and the factors the literature recognizes as drivers of the gender gap are considered input for universities to investigate their practices and organizational structures to know if priority is given to male performance or if there is systemic discrimination that puts women at a disadvantage. Pointing out those related to the integration between personal and work life helps minimize the impact generated by traditional gender roles on the academic productivity of men and, mainly, of women.

Implications for the profession

The reciprocity and cyclical nature between the professional and academic spheres mean that this work, its results, and its scope are not limited solely to universities but constitute a call for professional bodies and the accounting community. Moreover, many phenomena explained here are transposed from the professional field, where misogynistic and discriminatory practices have been documented.

Therefore, the results presented here motivate the dialogue between the academy and the profession, so there is a paradigm shift in gender roles and the participation of women within the profession from the training process and the academic role models. Consequently, we hope to encourage a generational change (both professional and academic) so that male prioritization and macho dynamics are put aside. Thus, Universities can be real agents of transformation for the new generations.

Limitations and future research

Despite the implications we highlight, we find some limitations in this study. It refers to the productivity measured by papers in a specific group of journals, leaving aside other research results in other journals or other languages that can also be valuable and representative of the advancement of women in academia. We also recognize that this database includes professors from other disciplines, such as sociology, mathematics, statistics, etc., who collaborate with cost and management accounting professors, which can partially influence the present results and analysis. Finally, we point out the descriptive nature of the work that, although it allowed us to visualize the current panorama of the academy to dispel the gender gaps, does not determine the exact causes behind this panorama, nor does it show the aspects that could lead to gender parity in academia.

Considering the results of this work as a starting point, future research should adopt an explanatory approach where the causes of gender differentials in the productivity and visibility of accounting research are determined with the spirit of managing or correcting them. Additionally, new research must focus on the aspects that have had an impact over time on the progressive reduction of this gap to promote and empower them. For this, it would be valuable to inquire directly with the actors involved, both the universities and the scholars.

Likewise, complementing this work by including other areas of accounting would eliminate possible area biases that could arise and, thus, achieve a general and complete overview of the discipline. In addition, new research should identify other areas of accounting knowledge in which there are significant differences in citations between male and female authors.

References

Abramo, G., D’Angelo, C. A., & Caprasecca, A. (2009). Gender differences in research productivity. Scientometrics, 79(3), 517–539. https://doi.org/10.1007/s11192-007-2046-8

Acker, J. (2006). Inequality Regimes: Gender, class, and race in organizations. Gender and Society, 20(4), 441–464. https://doi.org/10.1177/089124320628949

Adapa, S., Rindfleish, J., & Sheridan, A. (2016). ‘Doing gender’ in a regional context: Explaining women’s absence from senior roles in regional accounting firms in Australia. Critical Perspectives on Accounting, 35, 100–110. https://doi.org/10.1016/j.cpa.2015.05.004

Addis, E., & Villa, P. (2003). The Editorial boards of Italian economics journals: Women, gender, and social networking. Feminist Economics, 9(1), 75–91. https://doi.org/10.1080/1354570032000057062

Allen, T. D., Day, R., & Lentz, E. (2005). The role of interpersonal comfort in mentoring relationships. Journal of Career Development, 31(3), 155–169. https://doi.org/10.1007/s10871-004-2224-3

Anderson Gough, F., Grey, C., & Robson, K. (2005). ‘“Helping them to forget…”’: the organizational embedding of gender relations in public audit firms. Accounting, Organizations and Society, 30(5), 469–490. https://doi.org/10.1016/j.aos.2004.05.003

Baldarelli, M. G., Del Baldo, M., & Vignini, S. (2016). Pink accounting in Italy: Cultural perspectives over discrimination and/or lack of interest. Meditari Accountancy Research, 24(2), 269–292.

Baldarelli, M.-G., Del Baldo, M., & Vignini, S. (2019). The first women accounting masters in Italy: Between tradition and innovation. Accounting History Review, 29(1), 39–78. https://doi.org/10.1080/21552851.2019.1610467

Baldwin, A. A., Lightbody, M. G., Brown, C. E., & Trinkle, B. S. (2012). Twenty years of minority PhDs in accounting: Signs of success and segregation. Critical Perspectives on Accounting, 23(4–5), 298–311. https://doi.org/10.1016/j.cpa.2011.11.001

Barker, P. C., & Monks, K. (1998). Irish women accountants and career progression: A research note. Accounting, Organizations and Society, 23(8), 813–823. https://doi.org/10.1016/S0361-3682(98)00009-9

Barker, P., Monks, K., & Buckley, F. (1999). The role of mentoring in the career progression of chartered accountants. British Accounting Review, 31(3), 297–312. https://doi.org/10.1006/bare.1999.0103

Bay, D., Allen, M. F., & Njoroge, J. (2001). Gender orientation, success and job satisfaction in accounting academia. In C. R. Lehman (Ed.), Advances in accountability: Regulation, research, gender and justice (advances in public interest accounting) (Vol. 8, pp. 1–20). Emerald Group Publishing Limited.

Beattie, V. (2005). Moving the financial accounting research front forward: The UK contribution. British Accounting Review, 37(1), 85–114. https://doi.org/10.1016/j.bar.2004.09.004

Beattie, V., & Goodacre, A. (2004). Publishing patterns within the UK accounting and finance academic community. The British Accounting Review, 36(1), 7–44. https://doi.org/10.1016/j.bar.2003.08.003

Beattie, V., & Goodacre, A. (2012). Publication records of accounting and finance faculty promoted to professor: Evidence from the UK. Accounting and Business Research, 42(2), 197–231. https://doi.org/10.1080/00014788.2012.673159

Becker, G. S. (2009). Human capital: A theoretical and empirical analysis, with special reference to education. The University of Chicago Press.

Bellas, M. L. (1992). The effects of marital status and wives’ employment on the salaries of faculty men: The (House) wife bonus. Gender and Society, 6(4), 609–622.

Bellas, M. L. (1994). Comparable worth in academia: The effects on faculty salaries of the sex composition and labor-market conditions of academic disciplines. American Sociological Review, 59(6), 807–821. https://doi.org/10.2307/2096369

Blake-Beard, S., Bayne, M. L., Crosby, F. J., & Muller, C. B. (2011). Matching by race and gender in mentoring relationships: Keeping our eyes on the prize. Journal of Social Issues, 67(3), 622–643. https://doi.org/10.1111/j.1540-4560.2011.01717.x

Blättel-Mink, B., Kramer, C., & Mischau, A. (2009). Disciplinary cultures in higher education: Looking behind the mirror of gender" neutrality". Equal Opportunities International. Equality, diversity and inclusion, 28(1), 5–7.

Bourdieu, P. (1988). Homo Academicus. Stanford University Press.

Bonner, S. E., Hesford, J. W., Van der Stede, W. A., & Young, S. M. (2006). The most influential journals in academic accounting. Accounting, Organizations and Society, 31(7), 663–685. https://doi.org/10.1016/j.aos.2005.06.003

Boschini, A., & Sjögren, A. (2007). Is team formation gender neutral? Evidence from coauthorship patterns. Journal of Labor Economics, 25(2), 325–365. https://doi.org/10.1086/510764

Brinn, T., & Jones, M. J. (2007). Editorial boards in accounting: The power and the glory. Accounting Forum, 31(1), 1–25. https://doi.org/10.1016/j.accfor.2006.08.001

Brinn, T., & Jones, M. J. (2008). The composition of editorial boards in accounting: A UK perspective. Accounting, Auditing & Accountability Journal, 21(1), 5–35. https://doi.org/10.1108/09513570810842304

Broadbent, J. (2016). A gender agenda. Meditari Accountancy Research, 24(2), 169–181. https://doi.org/10.1108/MEDAR-07-2015-0046

Brown, L. D. (1996). Influential accounting articles, individuals, Ph.D. granting institutions and faculties: A citational analysis. Accounting, Organizations and Society, 21(7–8), 723–754. https://doi.org/10.1016/0361-3682(96)00012-8

Brown-Liburd, H., & Joe, J. R. (2020). Research initiatives in accounting education: Toward a more inclusive accounting academy. Issues in Accounting Education, 35(4), 87–110. https://doi.org/10.2308/ISSUES-2020-059

Brown, R., Jones, M., & Steele, T. (2007). Still flickering at the margins of existence? Publishing patterns and themes in accounting and finance research over the last two decades. British Accounting Review, 39(2), 125–151. https://doi.org/10.2308/ISSUES-2020-059

Carmona, S., Gutiérrez, I., & Cámara, M. (1999). A profile of European accounting Research: Evidence from leading research journals. European Accounting Review, 8(3), 463–480. https://doi.org/10.1080/096381899335880

Carnegie, G. D., McWatters, C. S., & Potter, B. N. (2003). The development of the specialist accounting history literature in the English language: An analysis by gender. Accounting, Auditing & Accountability Journal, 16(2), 186–207. https://doi.org/10.1108/09513570310472058

Chan, K. C., Chen, C. R., & Cheng, L. T. (2006). A ranking of accounting research output in the European region. Accounting and Business Research, 36(1), 3–17. https://doi.org/10.1080/00014788.2006.9730003

Chan, K. C., Chen, C. R., & Cheng, L. T. (2007). Global ranking of accounting programmes and the elite effect in accounting research. Accounting and Finance, 47(2), 187–220. https://doi.org/10.1111/j.1467-629X.2007.00234.x

Ciancanelli, P., Gallhofer, S., Humphrey, C., & Kirkham, L. (1990). Gender and accountancy: Some evidence from the UK. Critical Perspectives on Accounting, 1(2), 117–144. https://doi.org/10.1016/1045-2354(90)02011-7

Cislak, A., Formanowicz, M., & Saguy, T. (2018). Bias against research on gender bias. Scientometrics, 115(1), 189–200. https://doi.org/10.1007/s11192-018-2667-0