Abstract

Using Swedish microdata, we find no evidence for the concerns circulating in the public debate that foreign acquisitions lead to reductions in both R&D expenditures and high-skilled activities in targeted domestic firms for either MNEs or non-MNEs. Previous studies have only focused on larger firms. In this paper, we are able to study the impact on smaller firms (fewer than 50 employees), which is important because 90% of the firms acquired by foreign enterprises meet this criterion. For this group of firms, there is no information on R&D, but by using the register of educational attainment, we obtain data on the share of high-skilled labour in all Swedish firms, irrespective of size. Interestingly, we find that among smaller firms, foreign enterprises tend to acquire high-productive, skill-intensive firms (cherry-picking). After the acquisitions, skill upgrading appears in acquired smaller, non-MNE firms, particularly in the service sector.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In the late 1990s, foreign ownership increased quite dramatically in the Swedish business sector. Indeed, this trend was part of an international wave of mergers and acquisitions (M&A), but it raised concerns and a debate about potential effects on research and development (R&D) and other high-skilled activities located in Sweden. One reason for the strong sentiments was that some flagship Swedish multinational enterprises (MNEs)—such as Astra and Volvo cars—were acquired by foreign enterprises. As a contribution to such discussions taking place in Sweden and other countries, we provide evidence that “national” MNEs acquired by foreign MNEs are not affected in regard to R&D and skill intensities, whereas the share of high-skilled labour actually increases in smaller non-MNEs acquired by foreign MNEs.

From a theoretical point of view, the effect of M&A on R&D in a targeted firm is ambiguous.Footnote 1 On the one hand, if the acquirer and the acquired firm are performing similar R&D—if they are substitutes for each other—then a plausible outcome of a foreign acquisition would be for the foreign investors to exploit scale economies in R&D, centralise R&D activity in their home country and cut back on R&D activities performed abroad. Other reasons for moving R&D to the home country might be to avoid duplication of R&D inputs or to reduce costs associated with coordinating R&D units in different countries. On the other hand, if the R&D activities in the home country and in the acquired firm abroad are complementary to each other, one might expect the R&D activities in the foreign affiliate to be continued or even increased.Footnote 2 The motive for acquisition in this case would then be to access, exploit and develop already existing knowledge in the acquired firm (knowledge or technology sourcing), i.e., to tap into the expertise of the host country.Footnote 3

Many of the early studies evaluating the impact of M&A on R&D focused on domestic M&A, mostly in the USA. Those studies often found negative impacts on post-acquisition R&D in the acquired firms; however, the results were not robust.Footnote 4 Two studies more in the vein of this paper are Bertrand (2009) and Bandick et al. (2014); they both investigated the effects of foreign acquisitions on the R&D activities in domestic targeted firms. Bertrand (2009) covered international acquisitions of French innovativeFootnote 5 manufacturing firms from 1995 to 2001, and Bandick et al. (2014) covered international acquisitions of Swedish manufacturing firms with at least 50 employees from 1994 to 1999. In both studies, the firms were followed from 1 year before to 3 years after the acquisition. In contrast to the earlier studies of domestic M&A, these two studies found that acquisitions by foreign companies boost R&D spending in the domestic targeted firms.

Our paper also examines the effects of foreign acquisitions on R&D in acquired domestic firms. In expanding on the work of Bandick et al. (2014), we have extended our study to include the entire Swedish business sector. The foreign acquisitions in our study occurred between 2000 and 2006, a period with no spectacular increase in foreign ownership. Because we believe that the process of restructuring after an acquisition takes time, we used a larger window of time to study the firms, and the considered post-acquisition period was 5 years instead of 3 years as in earlier studies. Our outcome variables are, similar to previous analyses, absolute R&D expenditure and R&D intensity, i.e. R&D expenditure as a share of the firm’s output.

However, the great majority of the firms in the Swedish business sector state that they do not have any expenditure on R&D; R&D expenditures are heavily concentrated in a few firms and in manufacturing.Footnote 6 Most likely, development costs are underestimated in the official R&D statistics, notably in smaller firms and in the service sector. Larger manufacturing companies with separate R&D departments have a better understanding of how much they spend on R&D compared with smaller firms in the service sector, where development work often is confounded with ordinary business activities. In many activities in the service sector, the service is customised and developed at the same time as it is produced, e.g. in data consultancy.

Therefore, we propose an alternative, partly overlapping, measure to R&D expenditure that also might capture these aspects, namely the share of highly skilled labour; we define highly skilled labour as employees with 3 years or more of post-secondary education.Footnote 7 However, this measure is even broader and can be considered to be an indicator of the extent to which highly skilled activities (not only R&D) are conducted in a firm. Hence, another way to investigate whether foreign acquisitions affect the localisation of highly skilled activities in targeted firms is to examine the impact on the share of highly skilled labour.Footnote 8

Similar arguments as those for R&D apply for the effects of foreign acquisitions on the share of highly skilled labour. In other words, if the motive for foreign acquisition is knowledge and technology sourcing, the share of highly skilled labour in the acquired firms will be constant or will increase. If R&D and other highly skilled activities are, as a result of the foreign acquisition, relocated to the home country of the acquiring firm, then the skill share will decrease in the acquired firms.

A slightly different argument is if the knowledge and technology transfers from acquiring foreign MNEs to acquired smaller firms (non-MNEs) are particularly pronounced, then it might have significant effects on skill upgrading in the acquired firm. The acquiring firms in foreign acquisitions are by definition already MNEs or are becoming foreign MNEs through the acquisition, and it is well known that MNEs are important international conveyers of knowledge and technology (Keller 2010). The transfer of technology and organisational practises to acquired firms abroad has an effect on technological change and the organisation of these firms, and if these changes are skill-biased, the demand for skilled labour will increase, and a higher skill share will appear in the acquired firm. Because the level of technology might be considerably lower in smaller non-MNEs, we expect to observe the largest knowledge and technology transfers when such firms are acquired, and thus the largest positive effects on skill share will be seen in these firms.

Many of the concerns in the Swedish public debate have been about how large Swedish MNEs are affected when they become foreign owned. In both the public debate and in the academic literature, less interest has been directed towards the impact of foreign acquisitions on smaller firms, and such firms are quite often non-MNEs. An advantage with using the share of highly skilled labour instead of R&D expenditure as an outcome variable is that we have access to data for all firms and for every single year for the entire Swedish business sector without constraint on firm size. R&D expenditure in Sweden is surveyed every other year, and for many years during our studied period, such expenditures were only measured for firms with 50 employees or more.Footnote 9 To be able to study the effect on targeted smaller firms carefully, in manufacturing as well as in services, is an important contribution.Footnote 10

Previous studies have examined the effect of foreign acquisitions on skill intensity in acquired firms.Footnote 11 We discuss these studies more in depth in close connection to the presentation of our econometric results.

To preview our results, we find, in contrast to Bertrand (2009) and Bandick et al. (2014), no effect of foreign acquisitions on R&D in targeted firms, neither in MNEs nor in non-MNEs. In contrast, in small, non-MNEs, particularly in the service sector, the share of highly skilled labour increases in firms acquired by foreign enterprises. Foreign acquisitions have positive effects on the employment in smaller non-MNE firms. Both in manufacturing and in services, the employment of high-skilled labour increases after acquisitions. In regard to less-skilled labour, there are clearly positive and significant effects in services and to some lesser extent also in manufacturing.

The structure of the paper is as follows. Section 2 contains a brief review of the relevant literature in order to position our study and to generate hypotheses. Section 3.1 presents the structure of the employed Swedish microdata. Section 3.2 provides some descriptive facts on R&D expenditure, skill intensities and foreign ownership in the Swedish business sector. Section 3.3 describes how we have constructed the dataset we use in the econometric analysis and shows some descriptive statistics. Section 4 discusses our econometric strategy. Section 5 reports the results from the analysis, the propensity scores (Sect. 5.1) and the matching estimates on R&D (Sect. 5.2) and on skill intensity (Sect. 5.3). In Sect. 5.4, we discuss our results in light of earlier studies. Section 6 summarises and concludes the paper.

2 Theoretical background and related literature

The paper relates to two strands of the literature: (i) the drivers behind the internationalisation of R&D and (ii) how technological and organisational changes affect the demand for skilled labour.Footnote 12

Two motives are, in particular, proposed as explanations for why MNEs locate some portion of their R&D abroad.Footnote 13 One is that they want to adapt their products or services to special needs and preferences in overseas markets (home-base exploiting). This reason for the decentralisation of R&D is then to support local production abroad. Technological knowledge flows from the parent company, where the majority of the MNEs’ innovations emerge, to the foreign affiliates, whose job is to refine and adapt the technologies developed at the parent company to local conditions.

The other motive for decentralising R&D abroad is to leverage knowledge and technology from another country by localising R&D activities there (home-base augmenting). Intensified global competition has forced companies to produce new commercially viable products more quickly, while knowledge has been increasingly globally scattered. To quickly understand and benefit from new technologies, MNEs locate their R&D in centres of excellence, sites that are outstanding in a field that they want to develop. Proximity is important because some portion of knowledge is tacit and often transferred via frequent interpersonal contacts. In contrast to home-base exploiting, home-base augmenting involves knowledge flows from affiliates abroad to the parent company in the home market, “reverse technology transfer”, and complements the R&D conducted in the home country. The latter explanation for the internationalisation of R&D appears to have recently been growing in importance (Dunning and Lundan 2009).

Recently, there has been a notable increase in the use of M&A to access the technological and organisational capabilities held by other firms abroad. Especially interesting cases, with potential “win-win” outcomes, are those where larger established firms with global sales networks and strong financial positions, such as MNEs, acquire smaller domestic technology-intensive start-ups. The targeted firms have new technologies and innovations but, due to a lack of resources, it is hard for those firms to scale up, refine and extend them.Footnote 14

The acquiring foreign MNEs are expected to have firm-specific advantages—technological or organisational—that give them a competitive advantage relative to non-MNEs.Footnote 15 Foreign acquisitions entail the transfer of new technologies and organisational practises from foreign MNEs to acquired domestic firms. The resulting technological and organisational changes in targeted firms will affect the skill composition if such changes have an impact on the demand for skilled labour.

To date, there is significant empirical evidence for the skill-biased technological change (SBTC) hypothesis, i.e. skilled labour benefits more from technological change than other production factors. However, there is also evidence for skill-biased organisational change (SBOC), i.e. the introduction of new organisational practises, such as the greater involvement, responsibility and autonomy of workers, increase the demand for skilled labour, in particular together with technological changes.Footnote 16

In sum, we hypothesise from our reading of the literature, first that R&D conducted abroad, which usually intends either to support local production or source knowledge from the host countries, may be seen as a complement rather as a substitute for the R&D carried out at home. Accordingly, we expect not to find a negative impact on R&D expenditures in firms taken over by foreign MNEs. Second, knowledge and technology sourcing appear to be important motives for foreign acquisitions; therefore, we assume that the targets of the acquisitions often are high-productive, skill-intensive firms. Finally, transfers of technology and organisational practises from foreign MNEs to acquired firms increase the demand for skilled labour in targeted firms.

3 Data and description

3.1 Swedish microdata

The data in our microeconomic database are from Statistics Sweden (SCB) and the Swedish Agency for Growth Policy Studies (Growth Analysis). Unique identification numbers for the firms enable us to link information on financial accounts, R&D expenditure and register-based labour statistics (in this case, the education levels of employees).

In 1997, Statistics Sweden started to use administrative data to compile its Structural Business Statistics. This means that from 1997 on, the variables in the balance sheets and income statements are available for all non-financialFootnote 17 Swedish firms. An annual register on the level of education of the Swedish population has existed since 1985.

The Swedish R&D survey is conducted every second year (odd years). It started in the mid-1960s and initially only covered firms in mining and manufacturing with 50 employees or more. Gradually, it has been extended. From 1995, all non-financial firms with 50 employees or more have been included, and from 2001, the survey has also included financial firms. From 2005, a sample of firms with 10–49 employees has also been included. In parallel with the Swedish R&D survey, Statistics Sweden, until 2002, collected annual data on R&D expenditures on the firm level for the Structural Business Statistics. These are the R&D data used by Bandick et al. (2014).

From 1993 onwards, it has been possible to identify and thereby classify firms in the Swedish business sector into foreign-owned firms (foreign MNEs), Swedish MNEs and other Swedish firms (non-MNEs). We use information from the Swedish Agency for Growth Policy Analysis, which is the official provider of statistics on international enterprises in Sweden. Foreign MNEs are defined as firms where foreign owners possess more than 50% of the voting rights. Swedish MNEs are defined as firms that are part of a Swedish-controlled enterprise group with at least one subsidiary abroad.Footnote 18 Non-MNEs are defined residually, i.e. firms that are neither classified as Swedish MNEs nor as foreign MNEs.

Some recent studies have created measures for the various tasks performed within firms.Footnote 19 For such purposes, there is a need for data on occupations at the firm level. A complete register of occupations for all individuals 16 years or older in Sweden at the firm level has been available annually since 2001.

3.2 R&D, skill intensity and foreign ownership

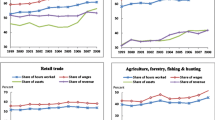

As our measure of R&D, we use the intramural costs, i.e. the expenditure for R&D performed within the firm, which primarily consists of labour costs for R&D personnel. The R&D expenditures in the Swedish business sector are very much concentrated in MNEs. This is shown in Figs. 1 and 2. In Fig. 1, we can see that since 1997, the R&D intensity—R&D expenditures as a share of value added—in the Swedish business sector has been more or less constant at approximately 4%, which is high in comparison to other OECD countries.Footnote 20 When we divide the firms into Swedish MNEs, foreign MNEs and non-MNEs, we observe that the R&D intensity is significantly higher in both Swedish MNEs and foreign MNEs than in non-MNEs.

R&D intensities in Swedish MNEs, foreign MNEs and non-MNEs. Notes: In our data, the total value added for non-MNEs in 1993 and 1995 is underestimated, and thus these observations have been excluded. In 2001, the survey on R&D was expanded to include financial firms (credit institutions, banks and insurance companies), and moreover, in 2001, the respondents were obliged to reply. From 2005, the R&D survey also includes a sample of firms with 10 to 49 employees. Before 2005, only firms with 50 employees or more were covered. To determine whether R&D intensities are higher in Swedish and foreign MNEs than in non-MNEs, we estimated a regression on a pooled dataset for the entire period controlling for industry and time, and we found that the R&D intensities are significantly higher than in non-MNEs. Source: Statistics Sweden, Research and Development in the Business Enterprise Sector and Structural Business Statistics

Share of total R&D expenditures in Swedish MNEs, foreign MNEs and non-MNEs. Source: Statistics Sweden, Research and Development in the Business Enterprise Sector

Figure 2 presents the total business sector R&D expenditures split among MNEs and non-MNEs. We find that the MNEs account for approximately 90% of the R&D expenditures in the Swedish business sector. Hence, by far most of the R&D is conducted in MNEs. From 1993 to 2003, there was a shift from Swedish MNEs towards foreign MNEs until the share of R&D became approximately the same in both groups. After 2003, the gap between Swedish MNEs and foreign MNEs has grown; the share in Swedish MNEs has increased, while the share in foreign MNEs has decreased.

An important explanation for the growing share of R&D expenditures in foreign MNEs in the late 1990s and in the beginning of the 2000s is that at this point in time, several large Swedish MNEs were acquired by foreign MNEs.Footnote 21 This is indicated in Fig. 4, where the share of employees in foreign MNEs increased from 10% in 1993 to over 23% in 2003. After 2003, the employment share in foreign MNEs became stable.

Figure 3 shows that the growing foreign ownership in Sweden in the late 1990s seems to reflect an international phenomenon. The inward foreign direct investment stock as a share of GDP in the world increased from 11% in 1995 to 23% in 2000.Footnote 22 After 2005, this share continued to grow, and in 2013, it was 34%; worldwide foreign ownership appears to have grown even after 2005. However, after 2003 in Sweden, the trend towards increased foreign ownership ceased, as seen in Fig. 3 (and in Fig. 4), and the share of employees in foreign MNEs in Sweden has been more or less unchanged since then.

Employment share in foreign MNEs in the Swedish business sector and the inward foreign direct investment (FDI) stock as a share of GDP in the world. Source: Growth Analysis, Foreign Controlled Enterprises in Sweden; and UNCTAD, Statistical Database ( unctadstat.org )

Employment shares in Swedish MNEs, foreign MNEs and non-MNEs. Source: Statistics Sweden, Register-based Labour Market Statistics (RAMS)

To put the shares of R&D in Fig. 2 into perspective, we present in Fig. 4 the corresponding shares for employment in the different groups of firms. In contrast to R&D, most of the employment is in non-MNEs (63% 2012), and at the end of the period, the employment share in foreign MNEs (21% 2012) was larger than that in Swedish MNEs (16% 2012). In other words, in comparison to R&D in the Swedish business sector, employment is clearly dominated by non-MNEs.

Another reasonable indicator for the extent to which advanced activities are conducted within a firm is the share of highly skilled labour. We define highly skilled labour as employees with 3 years or more of post-secondary education. As we noted in the introduction, this measure has a broader meaning and is only partly overlapping with R&D intensity. Certainly, the correlation between our measure of skill intensity and R&D intensity on the firm level for the entire business sector is clearly significant but not extremely high (0.20).Footnote 23 As expected, the correlation is higher in manufacturing (0.48), where the majority of the accounted R&D expenditure is conducted, than in services (0.16). Figure 5 shows the development of the shares of highly skilled labour in MNEs and non-MNEs. In the econometric analysis, we will use this variable in addition to R&D.

Shares of highly skilled labour in Swedish MNEs, foreign MNEs and non-MNEs. Notes: We define highly skilled labour as employed with 3 years or more of post-secondary education (ISCED 6–8). By estimating a regression on a pooled dataset for the entire period controlling for industries and time, we find that the share of high-skilled labour is significantly higher in MNEs than in non-MNEs. Source: Statistics Sweden, Register-based Labour Market Statistics (RAMS)

Not surprisingly, we find that the share of highly skilled labour is greater in Swedish MNEs (22% 2012) and in foreign MNEs (21% 2012) than in non-MNEs (14% 2012). Interestingly, we also notice that the share of skilled labour appears to have grown faster in MNEs than in non-MNEs. To put it differently, Figs. 1 and 5 reveal what many other studies have shown, namely that MNEs are quite different from non-MNEs.Footnote 24 The higher R&D intensity and skill intensity in MNEs might indicate that they are more technically advanced than non-MNEs, and thus there is potential for the transfer of technology from acquiring MNEs to acquired non-MNEs.

3.3 The dataset of analysis and descriptive statistics

In the econometric analysis to follow, we use data from Statistics Sweden’s R&D survey, Structural Business Statistics and register-based labour statistics together with data on international enterprises from the Swedish Agency for Growth Policy Analysis. As mentioned earlier, the latter allows us to divide firms into foreign MNEs, Swedish MNEs and other Swedish firms (non-MNEs). The dataset includes all firms in the Swedish business sector with at least one employee, and it covers the period 1999–2011.Footnote 25

To be included in the analysis, we require that a firm be observed in the data each year during a 7-year time window. Based on the information on ownership status, we define foreign acquisition of a domestic firm (Swedish MNE or non-MNE) as a change in ownership status from domestic to foreign between years t − 1 and t. In the econometric analysis, acquired firms are compared to non-acquired firms, the latter being firms classified as domestically owned in both years t − 1 and t. Both groups of firms are observed each year over the interval t − 1 to t + 5. With this allocation of the 7-year time window, we are able to study the effects of foreign acquisition over a fairly long time period.Footnote 26 Given that our data cover the period 1999–2011 and that R&D data are only available for odd years, we are able to construct four cohorts of firms that we follow during the 7-year window. The first cohort is observed during the period 1999–2005 with potential acquisitions occurring between 1999 and 2000, and the last cohort is observed during the period 2005–2011 with potential acquisitions occurring between 2005 and 2006.

Table 1 reports the number of foreign acquisitions among the four cohorts of firms that will be used in the econometric analysis. There are a few things to note. First, most acquisitions concern firms in the service sector. This is particularly the case for smaller firms, where almost 90% of acquired firms belong to the service sector. Second, foreign acquisition is a fairly rare event in absolute numbers among firms with 50 employees or more (the sample for which R&D data are available). The number of acquisitions is approximately seven times higher among firms with fewer than 50 employees. Third, foreign firms particularly target Swedish non-MNEs; there are only a handful of Swedish MNEs acquired during the period.Footnote 27

Table 2 presents differences in sample means between acquired and non-acquired firms by sector and size.Footnote 28 For the larger firms, there seems to be no difference in R&D intensity between acquired and non-acquired firms in the year prior to potential acquisition. However, we do find that the skill intensity tends to be higher among targeted firms. This holds for both smaller and larger firms in the service sector as well as for smaller firms in the manufacturing industry. There are also other important pre-acquisition differences. Targeted firms are, in general, more productive and younger than non-targeted firms. Acquired firms also tend to operate in industries characterised by a higher foreign presence.

4 Econometric strategy

The main purpose of this paper is to estimate the causal effect of foreign acquisition on R&D activity and skill intensity in targeted domestic firms. The econometric analysis is based on a conditional difference-in-differences matching approach suggested by Heckman et al. (1997, 1998). Various types of matching methods began to appear in economics in the late 1990s and were particularly common in the literature evaluating labour market programmes. Since then, matching has gained popularity in many other fields of applied economics.

The basic idea behind our approach is to choose a comparable untreated (non-acquired) firm for each treated (acquired) firm and to use these pairs to calculate the effect of the treatment (foreign acquisition) on the outcomes of interest (R&D activity and skill intensity). Two advantages with matching over conventional parametric estimation techniques are that matching is more explicit in assessing whether or not comparable untreated observations are available for each treated observation and that matching does not rely on the same type of functional form assumptions that traditional parametric approaches typically rely upon. There are numerous papers suggesting that avoiding (potentially incorrect) functional form assumptions and imposing a common support condition can be important for reducing selection bias in studies based on observational data.Footnote 29

The main parameter we are interested in estimating is the average treatment effect on the treated, ATT, which in our case corresponds to the average effect of foreign acquisition on the firms that have become acquired. The following set of equations gives the basic intuition behind the estimation strategy:

where t − and t + denote time periods before and after potential foreign acquisition occurring at time t; D t = 1 indicates that a firm is acquired at t, and D t = 0 indicates that a firm is not acquired at t; Y 1 represents, e.g. R&D intensity in the case of acquisition, and Y 0 represents R&D intensity if not acquired; X denotes a set of observed pre-acquisition covariates affecting both the probability of foreign acquisition and R&D intensity; and finally, \( \overset{-}{B} \) represents possible selection bias in the estimation of ATT.

Equation (1) represents a conventional cross-sectional matching estimator. This equation rests on an assumption of mean conditional independence, i.e. E(Y 0t+|X t−, D t = 1)= E(Y 0t+|X t−, D t = 0). This assumption states that if we condition on a sufficiently rich set of pre-treatment covariates, we can use the R&D intensity in non-acquired firms to approximate the R&D intensity that acquired firms would have conducted if they had not been acquired (the counterfactual outcome). However, if there are unobservable characteristics affecting both foreign acquisition and R&D intensity, the assumption no longer holds, and Eq. (1) will give a biased estimate of ATT. Equation (2) simply states that if we construct a matching estimate for pre-treatment R&D intensity, we would expect to find bias only due to unobserved differences between acquired and non-acquired firms (i.e. the effect of a treatment cannot precede the treatment itself). Equation (3) shows that if we take the difference between the post- and pre-treatment matching estimates, we can remove the time-invariant portion of the bias.

From the outline above, it follows that the conditional difference-in-differences approach does not rely on the likely implausible assumption that we can observe all factors affecting both foreign acquisitions and R&D intensity. The conditional difference-in-differences matching strategy extends conventional cross-sectional matching methods because it not only takes care of potential selection bias due to observable differences between acquired and non-acquired firms but also eliminates bias due to time-invariant unobservable differences between the two. However, this does not suggest that estimates based on this identification strategy are free from possible bias. If there are unobservable differences between acquired and non-acquired firms that vary over time (i.e. they are different in the pre- and post-acquisition periods), this is a potential source of remaining bias with our identification strategy.

In the differencing, we let the R&D intensity in year t − 1 represent the pre-treatment outcome. We follow the typical procedure in the literature and base the matching on the predicted probability of foreign acquisition, which is referred to as the propensity score (Rosenbaum and Rubin, 1983), rather than on the pre-treatment covariates themselves. We implement our matching strategy using both single nearest neighbour matching and kernel matching based on the Epanechnikov kernel with different bandwidths (see Sect. 5.2).

5 Empirical results

First, we present in Sect. 5.1 the propensity scores (i.e. the probability of foreign acquisitions) that will be used in the matching analysis to follow. This is an interesting analysis in itself because it tells us about the characteristics of the domestic firms that foreign firms acquire. Second, we show the results from the matching analysis, and we report the causal effects of foreign acquisitions on R&D intensity (Sect. 5.2) and on skill intensity (Sect. 5.3) in targeted firms. In Sect. 5.4, we relate our results on skill intensity to earlier Swedish and non-Swedish studies.

5.1 The probability of foreign acquisition

The first stage of our econometric analysis consists of estimating the propensity score, i.e. the predicted probability of foreign acquisition. The choices of covariates included in the propensity score are variables suggested by previous empirical literature to affect both foreign acquisition and R&D intensity and other types of high-skilled activities.Footnote 30 All variables in the propensity score refer to the year prior to potential acquisition (t − 1).

Two of the primary covariates in the propensity score are pre-acquisition R&D intensity and skill intensity. These two variables allow us to consider whether firms are targeted due to their R&D resources and high-skill activities or whether acquisitions are explained by other motives. As previously mentioned, data on skill intensity are available for the entire Swedish business sector without restriction on firm size, whereas data on R&D only pertain to firms with 50 employees or more. The propensity score further includes labour productivity and capital intensity. These variables allow us to test whether domestic firms are targeted based on their productive performance. Firm size and age are two variables commonly found in the literature focusing on foreign acquisitions; the former is often used as a proxy for home market share. The specification of the propensity score also includes a dummy variable indicating whether targeted firms are Swedish MNEs (as opposed to non-MNEs). The share of employment in foreign firms relative to total employment is included as a measure of foreign presence in an industry (at the ISIC Rev. 3.1 3-digit industry level). Finally, to control for temporal and sectorial effects, the specification of the propensity score includes dummy variables for year and a full set of industry dummies (at the ISIC Rev. 3.1 3-digit industry level).

We use a probit model to estimate the propensity score. To the extent that higher orders of the covariates improve the balancing between acquired and non-acquired firms, these are included in the specification (more on balancing below).Footnote 31 Table 3 presents the results. Columns (1) and (3) include estimates for firms with fewer than 50 employees in services and in the manufacturing industry, respectively, whereas columns (2) and (4) report estimates for firms with 50 employees or more in the two sectors.

Contrary to Bertrand (2009) and Bandick et al. (2014), we find no effect of R&D intensity on the probability of foreign acquisition for the sample of firms with 50 employees or more. An explanation for why Bandick et al. (2014) found a higher probability for foreign takeovers of R&D-intensive firms might be that during their period of study—the late 1990s—many large Swedish R&D-intensive manufacturing MNEs became foreign owned.Footnote 32 We do, however, observe that the likelihood of foreign acquisition increases with skill intensity in our sample containing smaller firms. This holds for smaller firms in services as well as for smaller firms in the manufacturing industry. Again, we find no significant effects in the sample restricted to larger firms.Footnote 33 Our findings thus indicate that foreign companies tend to target small high-skill firms. Due to the lack of R&D data for small firms, it is difficult to assess whether foreign interest in small skill-intensive firms also reflects an interest in these firms’ R&D potential.

Turning to the effect of labour productivity, our results do seem to suggest that foreign companies are cherry-picking high performing firms. For all specifications, the probability of foreign acquisition increases with firm size and decreases with firm age.Footnote 34 Our estimates on the dummy of Swedish MNEs indicate that foreign companies are less likely to acquire Swedish MNEs. This is contrary to the findings of Bandick and Hansson (2009) and most likely explained by the fact that in the late 1990s, many Swedish MNEs became foreign owned.Footnote 35 Finally, we find no consistent effect of industry-specific foreign presence on the likelihood of acquisition.

In sum, particularly among smaller firms, foreign enterprises are inclined to acquire high-productive firms that appear to conduct advanced (skill-intensive) activities. Moreover, the targeted firms tend to be relatively large and fairly young. Unlike in the late 1990s, in the 2000s—our period of study—foreign takeovers have not been directed towards R&D-intensive Swedish MNEs.

5.2 Effects of foreign acquisitions on R&D activity

The econometric analysis of the effect of foreign acquisition is based on a conditional difference-in-differences matching approach. Using a specific matching algorithm, we choose, based on the propensity score, a comparable non-acquired firm for each acquired firm and calculate the before-after difference in the outcome of interest for these pairs. As previously discussed, this approach not only addresses potential selection bias due to observable differences between acquired and non-acquired firms but also eliminates bias due to time-invariant unobservable differences between the two.

Our results are based on two different matching algorithms: single nearest neighbour matching and kernel matching based on the Epanechnikov kernel (in both cases, we match with replacement). In single nearest neighbour matching, each acquired firm is matched to the most similar comparison firm in terms of the propensity score. This approach generally trades reduced bias for increased variance. However, if the closest neighbour is far away, single nearest neighbour matching might still generate bad matches. Using the Epanechnikov kernel, each acquired firm is matched to a weighted average of non-acquired firms within a specific distance or bandwidth from the acquired firm. Heavier weight is put on more comparable firms, and in the case where there are no non-acquired firms within the chosen bandwidth, the acquired firm is dropped from the calculations due to a lack of comparability.Footnote 36

Table 4 presents matching estimates of the effects of foreign acquisitions on R&D intensity for the sample of firms with 50 employees or more. The reported results are based on the Epanechnikov kernel using a bandwidth of 0.001. Estimates for alternative bandwidths and single nearest neighbour matching are reported in Table 11 in the Appendix. Contrary to Bertrand (2009) and Bandick et al. (2014), we find no significant effect of foreign acquisition on R&D intensity in the targeted firms. This holds for firms in the service sector as well as for those in the manufacturing industry. The lack of significant effects is robust across the different matching estimators and regardless of whether R&D is expressed in intensity terms or in absolute levels.Footnote 37

Because we match firms based on the propensity score instead of the underlying covariates, we need to assess how successful the matching has been in terms of balancing differences in the included covariates between acquired and matched non-acquired firms. Table 12 in the Appendix presents some basic indicators of the quality of the matching for the Epanechnikov kernel with a bandwidth of 0.001. This is the matching estimator that performs best in terms of balancing the covariates, and thus we use it throughout the analysis.

One commonly used indicator of matching quality is the standardised bias of a covariate, which is defined as the difference of the sample means in the acquired and non-acquired group as a percentage of the square root of the average of the sample variance in the two groups (see Rosenbaum and Rubin, 1985). A value above 20 for this statistic is generally considered to be problematic. However, as seen from the table, the standardised bias for any covariate is well below this figure. The table also reports t values and accompanying p values from a test of differences in the covariate means between the two groups. As seen, there are no significant differences in the means for any of the covariates. Finally, the table reports pseudo-R 2 values before and after matching. This statistic indicates how well the covariates in the propensity score explain the probability of acquisition. After matching, the value should be fairly low because there should be no systematic differences in the distribution of covariates between acquired and matched non-acquired firms. As seen, the value drops to virtually zero after matching. Overall, the different balancing indicators suggest that the quality of the matching is fairly good.

The public debate in Sweden has been particularly focused on how large Swedish MNEs are affected by foreign acquisition. Concerns have been raised about what occurs to both the headquarters and the R&D activities of these domestic MNEs when they become foreign owned. However, as is shown in Table 1, few Swedish MNEs were acquired during the period we focus on. The empirical prerequisites for allowing different effects of foreign acquisitions depending on the status of the targeted firm are therefore rather limited. Despite this limitation, Table 5 reports the effect of foreign acquisition on R&D intensity depending on whether a Swedish MNE or a Swedish non-MNE is acquired. In neither case do we find any significant effects of foreign acquisition on R&D in targeted firms. Note that the results for Swedish MNEs are based on only 28 acquisitions.

Neither our present study nor the earlier study by Bandick et al. (2014) find a negative effect on R&D in Swedish firms targeted by foreign MNEs. These results run counter to many of the contentions that have been aired in the Swedish public debate on this issue. In Bandick et al. (2014), the impact was even positive and significant during a period when many large Swedish MNEs became foreign owned, whereas we detect no effect during a period when only a few Swedish MNEs were acquired by foreign MNEs. The relatively few acquisitions of heavily R&D-intensive firms during our period of study might explain the difference in results.Footnote 38

5.3 Effects of foreign acquisitions on skill intensity

A limitation of the analysis thus far is that it only pertains to firms with 50 employees or more. This is because R&D data in Sweden are primarily collected for larger firms. However, we know from the descriptive statistics in Table 1 that foreign firms primarily target small domestic firms. During the period in question, 7 out of 10 acquired firms had fewer than 50 employees. Even though the majority of takeovers appear to concern smaller firms, the academic literature has paid relatively little attention to the consequences of foreign acquisitions of smaller firms. For this group of firms, we have no information on R&D activities, but there are alternative ways to study how foreign takeovers affect high-skilled activities in targeted firms. One such approach is to examine the effect on the share of high-skilled labour in targeted firms. An obvious advantage of using skill intensity as the outcome variable in the analysis is that this variable is available for the entire Swedish business sector on an annual basis and without restriction on firm size.

Table 6 presents matching estimates of the effects of foreign acquisitions on skill intensity by firm sector and size. Again, the reported results are based on the Epanechnikov kernel using a bandwidth of 0.001. Interestingly, for small firms in the service sector, we find a positive and significant effect of foreign acquisition on skill intensity in targeted firms. Expressed as percentages, the initial effect is approximately 4%, and the effect increases slightly thereafter and stabilises at about 9% for the remainder of the period after acquisition. This is consistent with an interpretation that acquisitions involve organisational changes within a firm and that new work practises take approximately 2 years to implement. For larger firms, we find no significant effects of foreign takeovers on skill intensity in acquired firms.

Looking at firms in the manufacturing industry, the results are less stable but tend to indicate positive effects in the short run for both smaller and larger targeted firms. The estimated effects for firms in the manufacturing industry also tend to be somewhat larger, generally about 10–15%, compared to the effects for firms in the entire business sector.

All of the above results are robust across the alternative matching estimators (see Table 13 in the Appendix), and the different balancing indicators also suggest that the quality of the matching is satisfactory (see Tables 14 and 15 in the Appendix).

Table 7 presents the estimated effects on skill intensity depending on whether a Swedish MNE or a Swedish non-MNE is acquired by a foreign enterprise. Not surprisingly, we find effects for small non-MNE firms that are very similar to those above for small firms in the service sector. Almost all of the small firms in the service sector belong to the non-MNE group. For larger non-MNE firms, we find no significant effects of foreign acquisition on skill intensity in targeted firms.

From the bottom row of Table 7, it is evident that the number of acquired (treated) Swedish MNEs is very limited. Bearing this in mind, the results do not indicate any significant effects of foreign takeovers on skill intensity in either smaller or larger targeted Swedish MNEs.

Our analysis provides no evidence that high-skilled activities are being relocated to the home countries of acquiring firms. In contrast, acquiring firms appear to be taking advantage of and developing the knowledge base in the acquired small firms. The fact that a positive effect appears in small firms might be a consequence of knowledge and technology transfers from the acquiring foreign MNEs to targeted small Swedish firms, a transfer that in turn leads to increased demand for skilled labour.

By and large, we have seen that foreign acquisitions have a positive impact on the skill intensity of smaller non-MNEs. To investigate whether this is an outcome of the increased employment of skilled labour, the decreased employment of less-skilled labour or some combination of changes in the employment of the different types of labour, we estimate the effect of foreign acquisitions on each type of labour separately. Table 8 provides the results.

A general conclusion from Table 8 is that employment after acquisitions for the smaller firms acquired by foreign MNEs appears to increase. While the skill intensity in firms taken over in manufacturing is not affected by foreign acquisitions (Table 6), there are substantial positive effects on the employment of high-skilled labour. However, these changes are not large enough to influence the skill intensity significantly. In services, both the employment of high-skilled and less-skilled labour increases. However, here, the employment growth of high-skilled labour after acquisition seems to be sufficiently large to affect the skill intensity positively in smaller service firms (Table 6).

As a last step, as an exploratory extension, we examine whether the effect of foreign acquisitions on skill intensity in smaller firms differs between high- and low-technology industries in manufacturing and between knowledge and less knowledge-intensive industries in services.Footnote 39 A hypothesis would be that we find the largest effects on the share of high-skilled labour in more skill-intensive sectors.

Table 9 shows the number of acquisitions and the shares of acquisitions in each sector. From the table, it appears that the number of foreign acquisitions is largest in services and the share of foreign acquisitions is highest in high-tech manufacturing.

To investigate if it is the more skill-intensive parts of manufacturing and services that drive the positive impact on skill intensity found among smaller firms, we estimate the effect of foreign acquisitions separately for each sub-sector in Table 9, and the results are presented in Table 10.

We find no effects on skill intensity in either high- or low-technology manufacturing. Within the service sector, contrary to our hypothesis, we obtain a positive effect on skill intensity in the less knowledge-intensive sector.

5.4 Previous studies on skill intensity

There are two Swedish and a handful of studies from other countries that have analysed the effect of foreign acquisitions on the skill intensity in acquired firms.

Nilsson Hakkala et al. (2014) is a recent study of foreign acquisitions on skill upgrading and job tasks in targeted firms using Swedish data. In contrast to our study, they found no impact of foreign acquisitions on skill upgrading in targeted firms. Their period of study was 1996 to 2005, and they examined firms with 20 employees or more in the private sector. An analysis of job tasks requires occupational data, and as we noted in Sect. 3.1, a complete register on individuals’ occupations in Sweden is only available from 2001. This means that Nilsson Hakkala et al. (2014) were obliged to use a dataset, the Survey of Wages and Salaries from Statistics Sweden, where smaller firms are heavily underrepresented.Footnote 40

In this survey of the private business sector, a stratified sample is drawn according to industry affiliation and firm size, and larger firms have a higher probability of being sampled. In Table 16 in the Appendix, we can see the difference between register data and the survey in the number of firms of different size classes. For instance, in the size class 20–49 employees, only 11% of the firms in the register are included in the survey.Footnote 41 Individual wages and occupational codes for all individuals in the selected firms in the survey are collected. The sample of individuals in the survey includes approximately 50% of the individuals in the private business sector, but the share of the firms is much lower, at slightly more than 3%.

We believe that this underrepresentation of smaller firms in the sample analysed by Nilsson Hakkala et al. (2014) contributes significantly to explaining the difference in the results between their study and ours, but a more definite answer can only be obtained if the complete registers on individuals’ occupations and educational attainments from 2001 onwards are used. This question is outside the scope of our present study.

Another study of the effects of foreign acquisitions on skill upgrading in acquired firms is Bandick and Hansson (2009). They examined manufacturing firms with 50 employees or more between 1993 and 2002, and they found some support for a relative increase in the demand for skilled labour in non-MNEs, but not in MNEs, which become foreign owned. The outcome variable in Bandick and Hansson (2009) was slightly different from ours.Footnote 42 Although there are differences in relation to our study, their results show some similarities because in Table 6, we observed that foreign acquisitions had positive effects on skill upgrading, at least in the short run, in those targeted manufacturing firms with 50 employees or more.

Other non-Swedish studies that have analysed the effect of foreign acquisitions on skill intensity in targeted firms/establishments are Girma and Görg (2004), Almeida (2007) and Huttunen (2007).

Girma and Görg (2004) investigate whether the acquisition of domestic establishments by a foreign owner have any effects on the employment growth of skilled and less-skilled labour in the electronics and the food sectors in the UK in the 1980s. They find that the growth rate of skilled labour is not significantly affected by the change into foreign ownership in either electronics or food. However, in the electronics industry, the growth rate of unskilled labour declined significantly, whereas in the food sector, there was no significant effect. This indicates that the share of skilled labour increased in the electronics sector, while this appears not to be the case for the food sector. Finally, it is worth noting that foreigners tend to acquire establishments with high labour productivity both in the electronics and in the food sector.

Almeida (2007) studies Portuguese firms in the entire business sector in the 1990s. She finds no effect of foreign acquisitions on the years of schooling of the average worker in the acquired firms, whereas the targeted firms already have a more educated workforce prior to acquisition than the firms that continue to be domestically owned.

Huttunen (2007) examines the effects of foreign acquisitions on employment in different skill groups in Finnish manufacturing plants in the 1990s. Her results indicate a small decrease in the acquired plants’ share of highly educated workers. Similar to the other studies, plants characterised by high average years of schooling among employees are more attractive targets to foreign firms.

From the surveyed non-Swedish studies, we conclude that there is now extensive evidence from many countries of “cherry-picking” in connection with foreign acquisitions.Footnote 43 Foreigners tend to acquire high-productive, skill-intensive firms. However, the impact of foreign acquisitions on skill intensity in targeted firms is less clear-cut. Furthermore, none of the studies above focus particularly on smaller firms, the group of acquired firms for which we obtain a strongly significant positive effect. To be able to generalise from our results for Sweden, it would be interesting in the future to see studies of other countries aimed at investigating the effects on skill upgrading in smaller firms.

6 Concluding remarks

The impact of foreign acquisitions on R&D and other high-skilled activities in MNEs and larger firms has been the subject of several studies, but the effect on skill upgrading in smaller, non-MNE firms has been less explored. By using register data on educational attainment and variables from the firms’ balance sheets and income statements, we can investigate all Swedish firms with one employee or more.

The share of highly skilled labour serves partly as an alternative measure to R&D expenditures, which are heavily concentrated in a few large firms and in manufacturing. Most likely, R&D expenditures underestimate the amount of development work carried out within a firm, particularly in smaller firms and in services, and a firm’s high-skill intensity could therefore in such cases be a more appropriate measure. Note, however, that many highly skilled workers are engaged in other high-skill activities beyond R&D tasks.

In the group of firms with fewer than 50 employees, there are quite a few foreign acquisitions in our study period, and we find that the foreign takeovers of such firms appear to have had a clearly positive effect on the share of high-skilled labour. An explanation for this result may be that international knowledge and technology transfers from foreign MNEs to small non-MNEs, on the condition that the resulting technological and organisational changes in the targeted firms is skill-biased, will increase the demand for skills and thus that skill upgrading occurs in the acquired firms. By contrast, we find no impact on the share of high-skilled labour in MNEs or in firms with 50 employees or more, possibly because these firms have lower potential for knowledge and technology transfer. In other words, foreign acquisitions appear to primarily boost skill intensities, and probably the level of technology, in small, non-MNE targeted firms.

Foreign acquisitions appear to have positive effects on employment in the acquired smaller firms. Both in manufacturing and in services, the employment of high-skilled labour after acquisitions is increasing. In regard to less-skilled labour, there are significant positive effects in services but also to large extent in manufacturing.

A limitation of our study is that we are not able to identify domestic acquisitions. This means that we cannot compare the effects of foreign and domestic acquisitions, i.e. whether foreign acquisitions differ from domestic ones.Footnote 44

We also add to the literature on foreign acquisitions and R&D. In contrast to former studies using Swedish data, we examine a period with no spectacular increase in foreign ownership (the early 2000s), and we find no effect on R&D expenditures in firms acquired by foreign MNEs. Taken together with the results in Bandick et al. (2014), which analysed a more turbulent period for foreign acquisitions in Sweden (the late 1990s) and obtained a positive effect on R&D expenditures in targeted firms, we conclude that there seem to be no grounds for worrying about the impact of foreign acquisitions on R&D (and other high-skilled activities). Hence, there is no need for policymakers to consider restrictions on foreign ownership because advanced activities might move abroad; if anything, there are reasons to welcome foreign acquisitions.

Finally, an implication of our results may be that for a smaller firm with strong future potential, being acquired by a foreign MNE is a reasonable option to overcome those constraints to growth often faced by such firms.Footnote 45 These constraints could be weak internal financial resources or a lack of capabilities to develop products and refine technologies, to enter the international market or to upgrade skills. Using variables other than skill intensity while still focusing on the effect on smaller firms offers a conceivable avenue for further research. The advantage of acquiring foreign MNE is that it gains access to a new technology or product that complements its current activities.

Notes

There are economies of scope in R&D, and combining different R&D programs within the same company leads to higher R&D output than if the R&D is performed in separate firms.

According to Chakrabarti et al. (1994), the acquisition of external technologies as a complement to in-house developments is an important motivation for M&A.

For a review of this literature, see Cassiman et al. (2005).

Innovative firms are not defined in the paper, and the author admits that “the construction of our database could lead to an over-representation of large and technology-driven mergers. All firms in our sample do innovation.”

Among firms with at least 50 employees in the Swedish business sector, 86% have no R&D, and Eliasson et al. (2014) show that the top 14% of the firms that report R&D account for 90% of the total R&D expenditures in the Swedish business sector. In 2013, manufacturing represented 70% of business R&D expenditure, whereas the manufacturing share of value added was 22%.

Expenditure on R&D consists mainly of the wage costs of R&D personnel, and the absolute majority of R&D personnel are highly skilled workers. However, many highly skilled workers do not work directly with R&D.

Such measures have, as we can see in Sect. 5.4, been used as outcome variables in previous studies on the effects of foreign acquisitions but not exactly in this context.

The cut-off firm size in Statistics Sweden’s R&D survey had, until 2005, been 50 employees.

Much of the existing literature on technological M&A has focused on larger companies. An exception is Hussinger (2010). Her sample also contains a large share of small and medium-sized enterprises, and her results suggest that firms involved in M&As strengthen their technological competencies.

Andersson and Xiao (2016) find that firms with strong technological competence and weak financial resources operating in high-tech sectors, where the costs of entering international markets are large, are commonly acquisition targets for MNEs, domestic as well as foreign.

Firm-specific advantages create ownership (O) advantages, which together with locational (L) and internalisation (I) advantages in the OLI framework, explain the emergence of MNEs (Dunning 1977). An indicator that MNEs have firm-specific advantages is that they tend to have higher productivity than non-MNEs within the same industry (Helpman, Melitz and Yeaple 2004).

Piva et al. (2005) survey the empirical literature on SBTC and SBOC and present an empirical study on Italian manufacturing firms, where they find support that technological and organisational changes jointly have a positive effect on the demand for skilled labour.

Firms in industries ISIC Rev. 3.1 01–93 exclusive of 65–67, 75.

Among the OECD countries in 2013, the R&D intensity in Israel, Korea, Japan and Finland was higher than in Sweden.

The list is long and includes Nobel and Akzo 1994 (the Swedish MNE Nobel was acquired by the foreign MNE Akzo in 1994), Pharmacia and Upjohn 1995, Saab Automobile and General Motors 1998, Stora and Enso 1998, Enator and Tieto 1999, Volvo Car and Ford 1999, Astra and Zeneca 1999, Aga and Linde 2000 and Arla and MD Foods 2000.

See www.unctadstat.org.

Notice that 86% of firms with at least 50 employees account no R&D expenditure—R&D is zero—and that R&D expenditures are heavily concentrated in manufacturing; this indicates that R&D expenditures, most likely, are underestimated in smaller firms and in the service sector (see footnote 6). This might be an explanation for the fairly low firm-level correlation between R&D intensity and skill intensity.

As previously mentioned, firms in industries ISIC Rev. 3.1 65–67 (financial firms) and 75 (public administration) are excluded. Firms in these industries are not covered by the Structural Business Statistics and financial firms are not included in the Swedish R&D survey prior to 2001. We also exclude firms in industry 73 (R&D). These are “pure” R&D companies and generally have extremely high R&D intensity.

Bertrand (2009) and Bandick et al. (2014) studied the effect of foreign acquisition up to 3 years after acquisition. One could argue that the effects of foreign acquisitions on R&D and the skill mix in targeted firms are slow processes that might take time to materialise. Therefore, in our analysis, we extended the post-acquisition period to 5 years.

Note that the sample of firms on which the differences in sample means are based corresponds to the sample used in the empirical analysis in 5 .

The introduction of higher orders makes the probit models more flexible and facilitates balancing between acquired and non-acquired firms.

See footnote 21 and Fig.3.

Bandick et al. (2014) found a positive effect of skill intensity on foreign acquisitions. This is not unexpected given the fairly strong correlation between skill intensity and R&D intensity among large manufacturing firms.

See footnote 27.

For both the single nearest neighbour and the Epanechnikov kernel, we match on the so-called common support, i.e. we drop all firms whose propensity score is smaller than the minimum and larger than the maximum in the opposite group.

Note that the effects of foreign acquisitions on the absolute levels of R&D are not presented in any table.

Notice that Bertrand (2009), another study finding a positive effect of foreign acquisitions on R&D, uses a sample of firms in which large, technology-driven acquisitions most likely predominate.

We use a Eurostat classification to define high-tech and low-tech industries in manufacturing and knowledge and less knowledge-intensive industries in services (http://ec.europa.eu/eurostat/statistics-explained/index.php/Glossary:High-tech).

An indication that this sample of firms is quite different from the total population of firms is that in Table 2 of Nilsson Hakkala et al. (2014), there is no difference between MNEs and non-MNEs in the share of employees with higher education. This is in stark contrast to our data, where in Fig. 5 the skill intensity is significantly higher in MNEs.

Interestingly, we notice in Table 16 in the Appendix that, while the share of firms in the survey decreases as the size class of firms grows smaller, the corresponding shares in our cohort are more or less constant over the different size classes, at approximately 70%.

They use the wage bill share of employees with some post-secondary education (ISCED 4–8), while our outcome variable is the employment share of employees with 3 years or more of post-secondary education (ISCED 6–8).

According to Balsvik and Haller (2010), who compare foreign and domestic acquisitions in Norway, the impression from the few studies performing this comparison is that performance improves more after foreign acquisitions than after domestic acquisitions do.

We base this on Andersson and Xiao (2016) (see footnote 14). Such restrictions on smaller firms with growth potential may be due to market failures, e.g. poorly functioning capital markets. If this is the case, rectifying these failures is then likely to be a better alternative.

References

Almeida, R. (2007). The effects of foreign owned firms on the labour market. Journal of International Economics, 72(1), 75–96. doi:10.1016/jinteco.2006.10.001.

Andersson, M., & Xiao, J. (2016). Acquisition of start-ups by incumbent businesses. A market selection process of “high-quality” entrants? Research Policy, 45(1), 272–290. doi:10.1016/j.respol.2015.10.002.

Balsvik, R., & Haller, S. (2010). Picking “lemons” or “picking” cherries? Domestic and foreign acquisitions in Norwegian manufacturing. Scandinavian Journal of Economics, 112(2), 361–387. doi:10.1111/j.1467-9442.2010.01606.

Bandick, R., & Hansson, P. (2009). Inward FDI and demand for skills in manufacturing firms in Sweden. Review of World Economics, 145(1), 111–131. doi:10.1007/s10290-009-0002-9.

Bandick, R., Görg, H., & Karpaty, P. (2014). Foreign acquisitions, domestic multinationals, and R&D. Scandinavian Journal of Economics, 116(4), 1091–1115. doi:10.1111/sjoe.12071.

Baumgarten, D., Geishecker, I., & Görg, H. (2013). Offshoring, tasks, and the skill-wage pattern. European Economic Review, 61, 132–152. doi:10.1016/j.euroecorev.2013.03007.

Becker, S., Ekholm, K., & Muendler, M.-A. (2013). Offshoring and the onshore composition of tasks and skills. Journal of International Economics, 90(1), 91–106. doi:10.1016/j.1016/j.jinteco.2012.10.005.

Bertrand, O. (2009). Effects of foreign acquisitions on R&D activity: evidence from firm-level data for France. Research Policy, 38(6), 1021–1031. doi:10.1016/j.respol.2009.03.001.

Cassiman, B., Colombo, M., Garrone, P., & Veugelers, R. (2005). The impact of M&a on the R&D process. An empirical analysis of the role of technological- and market-relatedness. Research Policy, 34, 195–220. doi:10.1016/j.respol.2005.01.002.

Chakrabarti, A., Hauschildt, J., & Süverkrüp, C. (1994). Does it pay to acquire technological firms? R&D Management, 24(1), 47–56. doi:10.1111/j.1467-9310.1994.tb00846.x.

Charfeddine, L., & Mrabet, Z. (2015). Trade liberalization and relative employment: further evidence from Tunisia. Eurasian Business Review, 5, 173–202. doi:10.1007/s40821-015-0020-6.

Conyon, M., Girma, S., Thompson, S., & Wright, P. (2002). The impact of foreign acquisition on wages and productivity in the UK. Journal of Industrial Economics, 50(1), 85–102. doi:10.1111/1467-6451.00169.

Dehejia, R., & Wahba, S. (1999). Causal effects in nonexperimental studies: reevaluating the evaluation of training programs. Journal of the American Statistical Association, 94(448), 1053–1062. doi:10.2307/2669919.

Dehejia, R., & Wahba, S. (2002). Propensity score matching methods for nonexperimental causal studies. Review of Economics and Statistics, 84(1), 151–161. doi:10.1162/003465302317331982.

Doms, M., & Jensen, B. (1998). Comparing wages, skills, and productivity within firms domestically and foreign-owned manufacturing establishments in the United States. In R. Baldwin, R. Lipsey, & D. Richardson (Eds.), Geography and ownership as bases for economic accounting (pp. 235–255). Chicago: The University of Chicago Press.

Dunning, J. (1977). Trade, location of economic activity and the MNE: a search for an eclectic approach. In B. Ohlin, P.-O. Hesselborn, & P.-M. Wijkman (Eds.), The international allocation of economic activity. London: Macmillan.

Dunning, J., & Narula, R. (1995). The R&D activities of foreign firms in the United States. International Studies of Management and Organization, 25(1/2), 39–74.

Dunning, J., & Lundan, S. (2009). The internationalization of corporate R&D: a review of the evidence and some policy implications for home countries. Review of Policy Research, 26(1–2), 13–33. doi:10.1111/j1541-1338.2008.00367.x.

Eliasson, K., Hansson, P., & Lindvert, M. (2014). Is R&D moving away from Sweden? R&D in Swedish multinationals in Sweden and abroad. Growth Analysis, PM 2014:15.

Erken, H., & Kleijn, M. (2010). Location factors of international R&D activities: an econometric approach. Economics of Innovation and New Technology, 19(3), 203–232.

Girma, S., & Görg, H. (2004). Blessing or curse? Domestic plants’ survival and employment prospects after foreign acquisition. Applied Economics Quarterly, 50(1), 89–110.

Girma, S., & Görg, H. (2007). Evaluating the foreign ownership premium using a difference-in-difference matching approach. Journal of International Economics, 72(1), 97–112. doi:10.1016/j.jinteco.2006.07.006.

Harris, R., & Robinson, C. (2002). The effect of foreign acquisitions on total factor productivity: plant-level evidence from UK manufacturing, 1987-1992. Review of Economics and Statistics, 84(3), 562–568. doi:10.1162/003465302320259556.

Heckman, J., Ichimura, H., & Todd, P. (1997). Matching as an econometric evaluation estimator: evidence from evaluating a job training program. Review of Economic Studies, 64(4), 605–654. doi:10.2307/2971733.

Heckman, J., Ichimura, H., Smith, J., & Todd, P. (1998). Characterizing selection bias using experimental data. Econometrica, 66(5), 1017–1098. doi:10.2307/2999630.

Helpman, E., Melitz, M., & Yeaple, S. (2004). Export versus FDI with heterogeneous firms. American Economic Review, 94(1), 300–316. doi:10.1257/000282804322970814.

Hussinger, K. (2010). On the importance of technological relatedness: SMEs versus large acquisition targets. Technovation, 30(1), 57–64. doi:10.1016/j.technovation.2009.07.006.

Huttunen, K. (2007). The effect of foreign acquisition on employment and wages: evidence from Finnish establishments. Review of Economics and Statistics, 89(3), 497–509. doi:10.1162/rest.89.3.497.

Keller, W. (2010), International trade, foreign direct investment, and technology spillovers. In Hall, B. och N. Rosenberg (eds) Handbook of the economics of innovation. Volume 2. North-Holland, Amsterdam. doi: 10.1016/S0169-7218(10)02003-4.

Kuemmerle, W. (1997), Building effective R&D capabilities abroad. Harvard Business Review, March–April, 61–70.

Moncada-Paterno-Castello, P., Vivarelli, M., & Voigt, P. (2011). Drivers and impacts in the globalization of corporate R&D: an introduction based on European experience. Industrial and Corporate Change, 20(2), 585–603. doi:10.1093/icc/dtr005.

Nilsson Hakkala, K., Heyman, F., & Sjöholm, F. (2014). Multinational firms, acquisitions and job tasks. European Economic Review, 66, 248–265. doi:10.1016/j.euroecorev.2013.12.003.

Piva, M., Santarelli, E., & Vivarelli, M. (2005). The skill bias of technological and organisational change: evidence and policy implications. Research Policy, 34(2), 141–157. doi:10.1016/j.respol.2004.11.005.

Rosenbaum, P., & Rubin, D. (1983). The central role of the propensity score in observational studies for causal effects. Biometrika, 70(1), 41–55. doi:10.1093/biomet/70.1.41.

Rosenbaum, P., & Rubin, D. (1985). Constructing a control group using multivariate matched sampling methods that incorporate the propensity score. The American Statistician 39(1), 33–38.

Smith, J., & Todd, P. (2005). Does matching overcome Lalonde’s critique of nonexperimental estimators? Journal of Econometrics, 125(1–2), 305–353. doi:10.1016/j.jeconom.2004.04.011.

Acknowledgements

Financial support from the Swedish Council for Health, Working Life and Welfare is gratefully acknowledged. We have benefited from comments in seminars at Örebro University, Linköping University and CESIS, Royal Institute of Technology (KTH), Stockholm.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Rights and permissions

Open Access This article is distributed under the terms of the Creative Commons Attribution 4.0 International License (http://creativecommons.org/licenses/by/4.0/), which permits unrestricted use, distribution, and reproduction in any medium, provided you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made.

About this article

Cite this article

Eliasson, K., Hansson, P. & Lindvert, M. Effects of foreign acquisitions on R&D and high-skill activities. Small Bus Econ 49, 163–187 (2017). https://doi.org/10.1007/s11187-016-9815-9

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11187-016-9815-9