Abstract

This paper examines the causal impact of natural disasters on property insurance take-up of firms. Using the data of industrial firms in China, we find that a one-standard-deviation increase in typhoon damage leads to a 2.6% increase in the purchase of property insurance the following year. This increase gradually declines and returns to the previous level three years later. Our results demonstrate that this impact is driven not by changes in risk preferences or supply-side variation but by the updated risk beliefs learned from the typhoon experience. Unlike household insurance decisions, the learning effect of firms demonstrates an indirect but positive effect of typhoons on the firm’s insurance decisions from its related firms in the upstream or downstream sectors, but not from competitors.

Similar content being viewed by others

Notes

In China, for example, over the past two decades, the average premium income for enterprise property insurance accounts for only 3.7% of the overall property insurance market, according to the China Yearbook of Insurance. Moreover, our research sample has 1,382,174 firm-year observations, but only 38.4% of them have bought enterprise property insurance. For those with enterprise property insurance, the coverage is insufficient. On average, their insurable assets amount to approximately 50.95 million RMB, assuming that fixed assets and half of the liquid assets are insurable. However, the average coverage is only around 7.24 million RMB, calculated using the data on premium expenditure and premium rates of enterprise property insurance that typically range from 0.05% to 0.15%.

There are several important policy considerations behind encouraging firms (industrial firms in our paper) to have insurance coverage. (1) Risk mitigation. Natural disasters (e.g., typhoons) could cause adverse consequences to property and interrupt business operations. Insurance coverage helps to mitigate these risks and provides financial protection in the event of unforeseen events. (2) Business Continuity. Industrial firms are often heavily reliant on specialized equipment and facilities. Insurance coverage for property damage and business interruption can help ensure the continuity of operations in the event of a disaster or equipment failure. (3) Protection of Employees. Poor business performance or interruption due to disasters can reduce or interrupt employees’ income. Enterprise property insurance can smooth the firm’s business risk and, thus, the employees’ income risk. (4) Economic Stability. Industrial firms are significant contributors to the economy, and insurance coverage helps to protect their financial stability. In the event of a significant loss, insurance can provide the necessary funds to repair or replace damaged property and equipment, supporting the firm’s ongoing operations and preserving jobs.

Firm managers are generally intelligent, well-educated, and highly trained professionals compared to ordinary individuals. Theoretically, rational plant managers will trade off property insurance and alternative recovery options, calculate the costs and benefits of all possible risk management tools, and generate the optimal insurance decision. The rationality of managers’ insurance decisions also relies on the advantage of property insurance. For example, property insurance purchases can increase firm value by lowering the tax burden and reducing bankruptcy costs (Aunon-Nerin & Ehling, 2008; Asai, 2019). However, their risk management decisions may deviate from the standard neoclassical rational decision-making model. They are subject to systematic biases in a corporate setting due to inevitable cognitive limitations and sometimes managerial traits beneficial to their careers (Malmendier, 2018). The low demand for enterprise property insurance might be partly attributed to managerial biases, for example, overconfidence, loss aversion, and non-standard preference.

Enterprise property insurance is a commercial property insurance product for firms to manage their property risks in China. It provides firms with financial compensation for direct and consequential loss, as well as expenses associated with the insured objects caused by natural disasters and accidents specified in the contract. For more information on enterprise property insurance, please refer to Section 2.1.

The debate on whether a business is risk neutral or risk averse is controversial (Asai, 2019). To be conservative, we assume that firms are risk averse and that their risk attitudes may change over time. Moreover, the manager’s risk attitude may be changed after a typhoon, which affects the EPI decision of a plant.

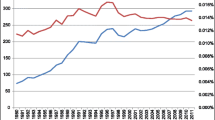

The size of the Chinese commercial property market (measured by the premium income) rose from 21.42 million RMB in 1998 to 197.96 million RMB in 2007 and 1189.59 million RMB in 2020, according to the China Yearbook of Insurance. The largest three major lines of P/C insurance are personal auto, liability, and agricultural, accounting for 72.28%, 5.74%, and 5.33% of the P/C total premiums, respectively, on average over the last two decades.

Coastal provinces include Liaoning, Hebei, Tianjin, Shandong, Jiangsu, Zhejiang, Shanghai, Fujian, Guangdong, Guangxi, and Hainan. We also run the main regressions using the two alternative samples for robustness checks. One sample includes firms in the coastal provinces and three inner-land provinces (i.e., Anhui, Hunan, and Jiangxi) that are sometimes affected by typhoons, and the other sample contains all the firms in coastal and inner-land areas. The main conclusions still hold, as shown in Appendix Table 8.

Whether a plant discloses its EPI premium expenditure in China is not mandatory. One may concern about how selection into disclosure might bias the estimates. Nevertheless, firms with missing data on EPI premium expenditure account for less than 1% of the total sample, and the differences in plant characteristics (e.g., size, profitability, leverage) between those with reported and missing EPI premium expenditure are statistically insignificant (the significance of t-test is 1%).

In order to alleviate the impact of outliers on the results, we winsorize variables at the 0.5 to 99.5 percentiles. This process affects only about 1% of observations of the sample, so we expect it to have little effect on the sample information and regression results. We also run main regressions without winsorizing variables for robustness (see Panel C of Appendix Table 8), and the results are very similar to the baseline results.

Our sample mainly includes privately-owned firms, comprising 84.87% of the total. Besides, our sample has shareholding firms in the mix (4.06%) and state-owned firms (11.07%). In the final sample, there are a total of 294,001 firms (1,382,174 firm-year observations), with 249,265 entered and 140,912 exited over the time frame. On average, around 27,696 firms enter, and 15,657 exit each year.

This 9.4% figure is comparable to the findings of research on developing economies. Prevatt et al. (2010) show that over 22% of residential buildings reported damage from Hurricanes from 1963 to 2005 in the Caribbean Community and Common Market and other Caribbean Islands. Bertinelli et al. (2016) find that Caribbean countries would experience an average damage of 2% (i.e., 2% of the property would be damaged across the country) in case of a damaging hurricane. The 9.4% figure is also in line with its developed counterpart. According to the National Centers for Environmental Information, the total property damage caused by hurricanes is estimated to reach 28.460 billion in Florida from 1998 to 2013. Federal Emergency Management Agency (FEMA) reports the hurricane-driven historic loss ratio (including buildings and agriculture) to be over 4.75% in Florida. To be more detailed, the Hurricane historic loss ratio for building value is around 2% when considering those not affected by Hurricanes (FEMA, 2023).

As we focus on the case of multiple typhoon attacks within one year instead of the accumulated typhoon damage across years, the estimated coefficient of TD in Eq. (1) is the lower bound of such causal effect; that is, the coefficients might be underestimated. Nonetheless, as shown in Panel F of Table 4, after controlling for the accumulated typhoon experience over a relatively long period, the impact of TDt−1 remains statistically and economically significant.

This variable has a non-negligible number of zeros and are fat (right) tailed distributed, so we use an inverse hyperbolic sine transformation to take account of this. Thus, coefficients on our explanatory variables can be interpreted as in log-level equations.

We focus on intertemporal effects rather than contemporaneous effects in our benchmark regressions because firms usually need time to react after being hit by a typhoon and cannot make insurance decisions immediately. For example, at the time of a year-end manager or shareholder meeting, a firm may consider the impact of a typhoon in the current year and increase its insurance purchases, but the increased insurance purchases will not be realized until the next calendar year. Therefore, the intertemporal effect seems to be more plausible. Of course, we will also consider the impact of typhoons in other periods on firms’ property insurance purchases in the dynamic regression model shown in Eq. (7).

Following Elliott et al. (2019), we divide China into a reginal grid according to each 1 degree of longitude and each 0.1 degrees of latitude.

Although the treatment variables are continuous in this model, it is consistent with the general event model where the treatment variables are dummy variables, so the model can not only estimate dynamic effects, but also address the problem of heterogeneous treatment effects in the same spirit of Sun and Abraham (2021).

We prefer the linear probability model because it is flexible in terms of including high-dimensional fixed effects and clustering the standard error across multiple levels, and the results are simple to interpret.

Firms located too close will be affected by the same typhoon, making it impossible to distinguish the impact of their own typhoon experience and the impact of related enterprise typhoons. Therefore, when we define TDR, we choose plant i as the center of the radius of 30 km outside the circle business to calculate.

Results in Section 3 show that current insurance decisions are not significantly impacted by typhoon damage from three years ago. Hence, we interact TDt−3 with TDIt−1. For robustness, we rerun the regression with a two-year and four-year cutoff. Appendix Table 9 reports the results of cutoff robustness checks, which are consistent with the results with a three-year cutoff.

Empirical results of CEOs’ natural disaster experience on risk preference are mixed. Some studies find that CEOs become more risk-averse after natural disasters (Chen et al., 2022), but others document that CEOs may be more risk-loving after experiencing fatal disasters (e.g., Bernile et al., 2017; Chen et al., 2021).

The typhoon damage may affect leverage in two ways. First, it may damage capital (asset), which would affect the leverage (liability/asset). However, as the typhoon strikes and probably affects assets and liabilities simultaneously, we cannot determine which direction the catastrophe may lead to the leverage. Suppose capital and liabilities had essentially the same probability of being hit by a typhoon. In that case, the numerator and denominator will change in the same proportion, so the leverage will not change, and the effect is numerically insignificant. Second, if the risk aversion mechanism were true, we could expect firms to take less risky actions after a typhoon (a year later or longer), for example, by lowering the leverage (Bhagat et al., 2015; Brenner, 2015).

Using the number of insurers (NINS) as a test is imperfect as it does not capture changes in the price of coverage or other actions by insurers that remain in an affected area. Unfortunately, we cannot access the data needed for the above analysis. Nevertheless, NINS and its change indeed reflect some variations of the property insurance market. Along with the consistent theoretical analyses in subsection 4.3.1, our supply-side discussion is reasonable, though imperfect. We obtain the prefecture-level number of property insurance companies from the China Yearbook of Insurance. The number of insurers that have entered the market (in coastal provinces) rose from 13 to 40 over the sample period, and there is no insurer exited the market during this period.

References

Adachi, D., Nakata, H., Sawada, Y., & Sekiguchi, K. (2023). Adverse selection and moral hazard in corporate insurance markets: Evidence from the 2011 Thailand floods. Journal of Economic Behavior and Organization, 205, 376–386.

Adams, M., Lin, C., & Zou, H. (2011). Chief Executive Officer incentives, monitoring, and corporate risk management: Evidence from insurance use. Journal of Risk and Insurance, 78, 551–582.

Angrist, J. D., & Pischke, J. S. (2008). Mostly harmless econometrics: An empiricist’s companion. Princeton University Press.

Asai, Y. (2019). Why do small and medium enterprises (SMEs) demand property liability insurance? Journal of Banking and Finance, 106, 298–304.

Aunon-Nerin, D., & Ehling, P. (2008). Why plants purchase property insurance. Journal of Financial Economics, 90, 298–312.

Benali, N., & Feki, R. (2017). The impact of natural disasters on insurers’ profitability: Evidence from Property/Casualty Insurance company in United States. Research in International Business and Finance, 42, 1394–1400.

Bernile, G., Bhagwat, V., & Rau, P. R. (2017). What doesn’t kill you will only make you more risk-loving: Early-life disasters and CEO behavior. The Journal of Finance, 72, 167–206.

Bertinelli, L., Mohan, P., & Strobl, E. (2016). Hurricane damage risk assessment in the Caribbean: An analysis using synthetic hurricane events and nightlight imagery. Ecological Economics, 124, 135–144.

Bhagat, S., Bolton, B., & Lu, J. (2015). Size, leverage, and risk-taking of financial institutions. Journal of Banking and Finance, 59, 520–537.

Boose, E. R., Serrano, M. I., & Foster, D. R. (2004). Landscape and regional impacts of hurricanes in Puerto Rico. Ecological Monographs, 74, 335–352.

Born, P., & Viscusi, W. K. (2006). The catastrophic effects of natural disasters on insurance markets. Journal of Risk and Uncertainty, 33, 55–72.

Born, P., & Klimaszewski-Blettner, B. (2013). Should I stay or should I go? The impact of natural disasters and regulation on US property insurers’ supply decisions. Journal of Risk and Insurance, 80, 1–36.

Botzen, W. J. W., Kunreuther, H., & Michel-Kerjan, E. (2019). Protecting against disaster risks: Why insurance and prevention may be complements. Journal of Risk and Uncertainty, 59, 151–169.

Brenner, S. (2015). The risk preferences of U.S. executives. Management Science, 61, 1344–1361.

Cai, J., & Song, C. (2017). Do disaster experience and knowledge affect insurance take-up decisions? Journal of Development Economics, 124, 83–94.

Cassar, A., Healy, A., & Von Kessler, C. (2017). Trust, risk, and time preferences after a natural disaster: Experimental evidence from Thailand. World Development, 94, 90–105.

Chen, Y., Fan, Q., Yang, X., & Zolotoy, L. (2021). CEO early-life disaster experience and stock price crash risk. Journal of Corporate Finance, 68, 101928.

Chen, C., He, Y., Wang, K., & Yan, S. (2022). The impact of early-life natural disaster experiences on the corporate innovation by CEOs. Emerging Markets Finance and Trade, 58, 3953–3975.

Choi, D., Shin, H., & Kim, K. (2023). CEO’s childhood experience of natural disaster and CSR Activities. Journal of Business Ethics, 188, 281–306.

Dougherty, J. P., Flatnes, J. E., Gallenstein, R. A., Miranda, M. J., & Sam, A. G. (2020). Climate change and index insurance demand: Evidence from a framed field experiment in Tanzania. Journal of Economic Behavior and Organization, 175, 155–184.

Elliott, R. J. R., Strobl, E., & Sun, P. (2015). The local impact of typhoons on economic activity in China: A view from outer space. Journal of Urban Economics, 88, 50–66.

Elliott, R. J. R., Liu, Y., Strobl, E., & Tong, M. (2019). Estimating the direct and indirect impact of typhoons on plant performance: Evidence from Chinese manufacturers. Journal of Environmental Economics and Management, 98, 102252.

Emanuel, K. (2011). Global warming effects on U.S. hurricane damage. Weather Climate and Society, 3, 261–268.

FEMA. (2023). "National risk index technical document".

Gallagher, J. (2014). Learning about an infrequent event: Evidence from flood insurance take-up in the United States. American Economic Journal: Applied Economics, 6, 206–233.

Gallagher, J., & Hartley, D. (2017). Household finance after a natural disaster: The case of hurricane Katrina. American Economic Journal: Economic Policy, 9, 199–228.

Grinsted, A., Ditlevsen, P., & Christensen, J. H. (2019). Normalized US hurricane damage estimates using area of total destruction, 1900–2018. Proceedings of the National Academy of Sciences, 116, 23942–23946.

Hanaoka, C., Shigeoka, H., & Watanabe, Y. (2018). Do risk preferences change? Evidence from the great east Japan earthquake. American Economic Journal: Applied Economics, 10, 298–330.

Holland, G. (2008). A revised hurricane pressure-wind model. Monthly Weather Review, 136, 3432–3445.

Hsiang, S., & Jina, A. (2014). The causal effect of environmental catastrophe on long-run economic growth: Evidence from 6,700 cyclones. National Bureau of Economic Research. No. w20352.

Hu, Z. (2022). Social interactions and households’ flood insurance decisions. Journal of Financial Economics, 144, 414–432.

Kamiya, S., & Yanase, N. (2019). Learning from extreme catastrophes. Journal of Risk and Uncertainty, 59, 85–124.

Knapp, K. R., Diamond, H. J., Kossin, J. P., Kruk, M. C., & Schreck, C. J. (2018). International Best Track Archive for Climate Stewardship (IBTrACS) Project, Version 4. NOAA National Centers for Environmental Information.

Knapp, K. R., Kruk, M. C., Levinson, D. H., Diamond, H. J., & Neumann, C. J. (2010). The International Best Track Archive for Climate Stewardship (IBTrACS): Unifying tropical cyclone best track data. Bulletin of the American Meteorological Society, 91, 363–376.

Kossin, J. P., Knapp, K. R., Olander, T. L., & Velden, C. S. (2020). Global increase in major tropical cyclone exceedance probability over the past four decades. Proceedings of the National Academy of Sciences, 117, 11975–11980.

Kuhla, K., Willner, S. N., Otto, C., & Levermann, A. (2023). Resilience of international trade to typhoon-related supply disruptions. Journal of Economic Dynamics and Control, 151, 104663.

Malmendier, U. (2018). Behavioral corporate finance. In Handbook of Behavioral Economics: Applications and Foundations (Volume 1, pp. 277–379). North-Holland.

Meyer, R. J. (2012). Failing to learn from experience about catastrophes: The case of hurricane preparedness. Journal of Risk and Uncertainty, 45, 25–50.

Michel-Kerjan, E., & Raschky, P. (2015). Corporate demand for insurance: New evidence from the U.S. Terrorism and property markets. Journal of Risk and Insurance, 82, 505–530.

Prevatt, D. O., Dupigny-Giroux, L. A., & Masters, F. J. (2010). Engineering perspectives on reducing hurricane damage to housing in CARICOM Caribbean Islands. Natural Hazards Review, 11, 140–150.

Schildberg-Hörisch, H. (2018). Are risk preferences stable? Journal of Economic Perspectives, 32, 135–154.

Sun, L., & Abraham, S. (2021). Estimating dynamic treatment effects in event studies with heterogeneous treatment effects. Journal of Econometrics, 225, 175–199.

UNISDR. (2022). Global Assessment Report on Disaster Risk reduction. UNISDR.

Vickery, P. J., Masters, F. J., Powell, M. D., & Wadhera, D. (2009). Hurricane hazard modeling: The past, present, and future. Journal of Wind Engineering and Industrial Aerodynamics, 97, 392–405.

Viscusi, W. K., & Zeckhauser, R. J. (2006). National survey evidence on disasters and relief: Risk beliefs, self-interest, and compassion. Journal of Risk and Uncertainty, 33, 13–36.

Yang, S. A., Birge, J. R., & Parker, R. P. (2015). The supply chain effects of bankruptcy. Management Science, 61, 2320–2338.

Yu, M. (2015). Processing trade, tariff reductions and plant productivity: Evidence from Chinese plants. The Economic Journal, 125, 943–988.

Zhang, P., Deschenes, O., Meng, K., & Zhang, J. (2018). Temperature effects on productivity and factor reallocation: Evidence from a half million Chinese manufacturing plants. Journal of Environmental Economics and Management, 88, 1–17.

Zou, H., & Adams, M. B. (2008). Debt capacity, cost of debt, and corporate insurance. Journal of Financial and Quantitative Analysis, 43, 433–466.

Funding

This work was supported by the National Natural Science Foundation of China (Grant Number 72203052, 72004080, 72304185), the Humanities and Social Science Research Foundation of the Ministry of Education of China (Grant Number 22YJC790023), Natural Science Foundation of Guangdong Province of China (Grant Number 2023A1515010861).

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no competing interest.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1. Calculation process for typhoon damage

The wind speeds a firm experiences during a typhoon are essential in measuring the damage to an individual firm. It will depend on the firm’s exact location relative to the storm’s movement and features. We apply the well-known wind field model in physics (Boose et al., 2004; Holland, 2008) to model the wind speed at any point \(i\), for storm k, in time t:

where \({v}_{max,kt}\) is the maximum sustained wind velocity anywhere in the typhoon; \({T}_{ikt}\) is the clockwise angle between the forward path of the typhoon and a radial line from the typhoon center to the point of interest i; \({V}_{h,kt}\) is the forward velocity of the tropical storm; \({R}_{max,k,t}\) is the radius of maximum winds and \({R}_{it}\) is the radial distance from the center of the tropical storm to point i. G is the gust factor, and F, S, and B are the scaling factors for surface friction, asymmetry due to the storm’s forward motion, and the shape of the wind profile curve, respectively.

In terms of implementing Eq. (1), the maximum wind speed \({v}_{max,kt}\) is taken from the IBTrACS data, \({V}_{h,kt}\) can be calculated following the movement path of the storm, while R and T can be determined by using the relative position between the eye of the typhoon and our point of interest i. We set G equal to 1.5 and S equal to 1 following Boose et al. (2004), respectively. For the surface friction indicator, Vickery et al. (2009) suggest that in open water, the reduction factor is around 0.7. Following Elliott et al. (2015) and Elliott et al. (2019), we linearize the reduction factor to capture the friction effect of the typhoon as it moves inland. In terms of the pressure profile parameter and the maximum radius winds, we adopt Holland (2008)’s approximation method following the suggestions by (Elliott et al., 2019).

As noted by Emanuel (2011), there are energy dissipation reasons to assume that the relationship between wind speed experienced and damage incurred is to the cubic power. Moreover, there is unlikely to be any damage from winds that fall below 92 km/h. To incorporate these features and to ensure that the percentage of damage varies between 0 and 1, Emanuel (2011) proposes the following damage function for the wind of storm k experienced at location i:

where

where \({v}_{ik}\) is the maximum wind speed of storm k experienced at the point of interest i; \({v}_{zero}\) is the threshold below which no damage occurs, and \({v}_{half}\) is the threshold at which half of the property is damaged. Following Emanuel (2011), we assume values of 92 km/h and 204 km/h for \({v}_{zero}\) and \({v}_{half}\), respectively. Note that Eq. (1) is defined in terms of the percentage of damage caused per storm. Given that our firm-level data is annual, a firm could be attacked by several storms in a year (as shown in Panel B of Appendix Fig. 4). Hence, to account for the possibility of multiple strikes, we assume that damages can accumulate over a year but restrict the impact of additional storms to have less than a simple cumulative effect. Instead, under the assumption that fragile structures get destroyed first, leaving more resistant structures, we allow damage to be multiplicative for storms k = 1, …, K within a year t as follows:

For robustness, we also define the total typhoon damage for firm i in year t as follows:

Appendix 2. Supplementary figures

Distribution of typhoon damage above zero and number of typhoon attack across years

The mean wind speed during various relative periods. Note: The figure shows the mean wind speed during various relative periods to landfall. Typhoon data comes from the International Best Track Archive for Climate Stewardship (IBTrACS) database. It contains typhoons’ geographic coordinates and wind speed for each three hours. Each bin of the periods represents three hours (a day before and after the typhoon’s landfall).

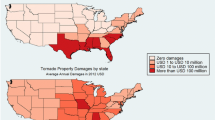

The distribution of average typhoon damage across provinces (1998–2007). Note: The average typhoon damage is obtained by calculating the average of typhoon damage to firms in each province. See Section 2.2 in the paper for the data sources and calculation of typhoon damage to firms.

The impact of typhoon at different periods on firm EPI purchase. Note: This figure presents the regressions of \(EPID_t\) (A) and \(Log\;(EPIE)_t>0\) (B) on \(TD_{i,t-\tau}\), where \(\tau\) = 3, 2, 1 (baseline), 0, -1 (placebo). All regressions include climatic controls, year fixed effects, firm fixed effects, and region-specific trends. Standard errors are clustered at 2-digit industry, geographic region, and year level.

Spillover impact of typhoon on EPI (extensive effect). Note: This figure presents the estimates of the impact of own typhoon damage (A), typhoon damage in the same industry (B) and typhoon damage in related (upstream and downstream) industries (C) on premium expenditure of EPI (log) (> 0) within different cut-off distances. All regressions include climatic controls, year fixed effects, firm fixed effects, and region-specific trends. Standard errors are clustered at 2-digit industry, geographic region, and year level.

Spillover impact of the typhoon on EPI (intensive effect). Note: This figure presents the estimates of the impact of own typhoon damage (A), typhoon damage in the same industry (B) and typhoon damage in related (upstream and downstream) industries (C) on premium expenditure of EPI (log) (> 0) within different cut-off distances. All regressions include climatic controls, year fixed effects, firm fixed effects, and region-specific trends. Standard errors are clustered at 2-digit industry, geographic region, and year level.

Appendix 3. Supplementary table

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Ding, Y., Deng, P. Learning from natural disasters: Evidence from enterprise property insurance take-up in China. J Risk Uncertain (2024). https://doi.org/10.1007/s11166-024-09428-4

Accepted:

Published:

DOI: https://doi.org/10.1007/s11166-024-09428-4