Abstract

This paper analyses the joint effects of Economic Policy Uncertainty (EPU) and inflation risk on the Corporate Cash Holdings (CCH) of US firms from 2011 to 2021. The baseline results suggest that EPU and inflation risk positively impact CCH. Moreover, we find the same results between inflation risk and CCH. However, EPU and CCH are negatively associated. Additionally, construction (finance) firms hold higher (lower) cash at the time of EPU and inflationary risk. We also find that firms hold higher (lower) cash during Democrat (Republican) presidential terms. The two-step system Generalized Method of Moments approach used to control the potential endogeneity issues indicates the same results and supports the baseline findings.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Uncertainty in government economic policies may be bad for the economy. According to some studies (Baker et al. 2016; Stock and Watson 2012), uncertainty about government spending, taxes, and regulatory and monetary policies contributed to the Great Recession of 2007–2009 and hindered economic recovery. A company's ability to hang onto its cash is what allows it to attract investment opportunities (Keynes 1936). Additionally, keeping cash is just trading and prevention. However, the world has been in a recession since the financial crisis. Due to a lack of cash holdings, many businesses across the world have gone out of business, and the capital chain has collapsed (Wang et al. 2014). These occurrences have made it clear that having the right amount of cash on hand can help businesses handle financial crises. According to the literature, businesses adjust to changes in the macroeconomic environment, and economic risk significantly impacts how much cash they keep (Venkiteshwaran 2011). Yet due to poorly thought out and/or implemented economic policies, low market demand, and tight capital turnover, businesses’ cash holdings can steadily decline (Wang et al. 2014). In order to combat such an uncertain economic environment, businesses are forced to handle their excess cash holdings. Eventually, because of the restrictions on external financing, businesses hold onto their cash more at times of heightened economic risk (Duchin et al. 2010).

Changes in governments’ economic and social strategies are represented by economic risk. Businesses are eager to make financial decisions when considering economic risk. This is brought on by the rising degree of political unrest. Companies might react to economic risk by delaying their investment plans until they believe the economic dangers have subsided (Frye and Shleifer 1997). Hence we can see that the economy is highly dependent on (perceptions of) economic risk (Julio and Yook 2012) and, consequently, most governments work to foster an atmosphere conducive to the stable operation of the private sector. In doing so, governments impact businesses in various ways, including imposing taxes, offering subsidies, upholding the law, regulating competition, and establishing environmental and labor standards. When the investment environment is unfavourable and perceptions of economic risk are high, managers of companies often amass too much cash, instead of, for example, paying out dividends (Huang et al. 2015; Hasan 2022). In a healthy capital market, a positive economic environment makes it easier to convert noncash assets (Jensen 1986).

According to Dittmar and Mahrt-Smith (2007), CCH has seen a noticeable rise globally over the past 20 years (see also Amees et al. 2015). Firms may benefit from retaining more cash in the form of lowering their transaction costs, but doing so comes at a growing opportunity cost (Opler et al. 1999). Businesses hold more capital during a downturn in the economy for investment and stability (Baumol 1952). They can invest more and hold less cash when a government intervenes in the industrial situation and extracts resources through taxes and other laws (Pinkowitz 2006). Ameer (2012) investigated how cash holdings and ownership concentration affect Australian enterprise valuation. Beuselinck and Du (2017) investigation of MNCs’ cash holdings concluded that more research was needed to examine the impact of cash holdings and other macro variables in greater detail (Hunjra et al. 2022).

There is currently a significant amount of research showing that continuous inflation can have a negative effect on long-term growth (Evers et al. 2020). The opportunity cost of keeping currency, distortions of relative pricing, and the tax system, in particular, affect incentives for investment and saving, subjects which have been topics of theoretical discussion regarding the detrimental effects of inflation. However, there is still disagreement regarding the underlying causal mechanism that links EPU and inflation risk on CCH due to the mixed empirical evidence for these theories and their consequences for economic growth. Since the nominal interest rate, which is connected to the inflation rate via the Fisher equation, determines the relevant liquidity premium, this mechanism suggests that rising inflation and EPU act as a tax on forward investment and raise firms’ cash holdings. Based on these arguments, we investigate the impact of EPU and inflation risk on CCH.

US firm-level data from 2011 to 2021 was used to conduct this research. The final dataset comprised 18,690 observations (firm and year) for 1869 US firms. For baseline regression, we used the OLS estimation. However, we used GMM estimation to control for endogeneity issues. The initial findings revealed a positive correlation between EPU, inflation risk, and CCH. Additionally, we discovered a similar relationship between CCH and inflation risk. However, a negative correlation was identified between EPU and CCH. Additionally, it was found that during periods of inflation risk and EPU, businesses in the construction (financial) industry maintain more (less) cash. Notably, we also discovered that companies held more (less) cash during the Democrat Democrat and Republican presidential administrations, respectively. The two-step system GMM technique supported the baseline findings and was used to control for endogeneity issues.

Our main contributions to the existing literature are threefold. Frstly, this is the first paper, to our knowledge, to investigate the impact of EPU and inflation risk on CCH, with the previous literature concentrating solely on EPU and CCH (e.g. Fresard 2010; Phan et al. 2019). Secondly, this paper uses a larger data set to compare similar kinds of studies in the field (e.g. Baker et al 2016; Li 2019; Phan et al. 2019). Finally, in contrast to the existing litetature, which has focused on EPU and CCH (e.g. Baker et al 2016; Li 2019; Phan et al. 2019), this paper contributes to three areas of research: EPU, inflation and CCH.

The remainder of the paper is organized as follows. Section 2 introduces and reviews the relevant literature and develops the paper’s hypotheses. Our data and methodology are then set out. After that, baseline model results, robustness and endogeneity tests are discussed. Section 5 concludes the paper.

2 Literature review and hypotheses

Changes in governmental policies in both the economic and social spheres constitute economic risk. Economic risk is essential for more informed decision-making in many nations. Investor pressure forces companies to reduce their cash holdings in order to cut agency fees while, at the same time, managers are urged to keep financial reserves on hand to cover their needs. For this reason, the pecking order hypothesis, created by Myers and Majluf (1984), describes the significance of internal financing, in which a corporation chooses to finance its new investment before turning to debt financing or issuing extra stocks if further financing is required (Fama and French 2005). Since trade-off theory is used to manage cash holdings, corporations must consider economic risk when making decisions. Keynes (1936) also explained the purposes of currency holdings. The transaction motive explains why businesses require cash to cover ongoing financial obligations and interpersonal interactions. Another motive is the precautionary motive, which is concerned with the need for businesses to have sufficient cash reserves to satisfy future demands. Various findings from earlier studies have explained the connection between economic risk and cash holdings.

In order to have enough internal capital to take advantage of improved investment opportunities, firms maintain higher cash balances when economic conditions are favourable (Kim et al. 1998). According to Harford et al. (2014), politically linked businesses store more cash and frequently alter their policies in reaction to economic risk. According to Caprio et al. (2013), a firm’s cash holdings are low when the level of corruption in a nation is high. Government agents frequently use corruption to gain political advantage at the expense of cash-rich companies. Therefore, a company maintains less cash to reduce the danger of political extraction in the form of cash payments to political actors. According to Wang et al. (2014) analysis of the effects of economic risks such as inflation on cash-holding strategies, enterprises attempt to modify their cash-holding plans in response to economic risk because the purchasing power is controllable following the inflation rate. The necessity of the age is to develop strategies that take economic risks like inflation into account. Based on that, we developed our first hypothesis:

H1-a:

EPU and inflation risk jointly impact positively on CCH.

According to Francis et al. (2014), CEOs who benefit from economic risk and push for higher borrowing costs those enterprises are with higher political exposure. Additionally, changes in economic risk cause falls in investment and cash holdings (Johannsen 2014). According to Huang et al. (2015), companies that are less liquid or have a lower market valuation than others are more likely to cut their cash holdings during times of elevated economic risk. Chen et al. (2015) warned that uncertainty positively correlates with international contexts and CCH, while individualism is adversely correlated with both. According to Xu et al. (2016), a change in political ties brought on by political turnover increases economic risk. The authors contended that economic risk is a shock that impacts the firm’s current political relationships and, as a result, its judgements regarding cash holdings. According to An et al. (2016), Chinese businesses cut their investments during political upheaval, and this effect is particularly pronounced for businesses doing more business with local government.

Government economic policy uncertainty has detrimental financial and practical repercussions, according to recent studies (Phan et al. 2019). Firms are more prone to put off investments, especially those that are irreversible, according to Gulen and Ion (2016) and Nguyen and Phan (2017). Financial limitations faced by businesses can become more severe as a result of policy uncertainty (Gilchrist et al 2014; Pástor and Veronesi 2013).

CCH may be impacted by economic policy uncertainty in a variety of ways. Firms are motivated to increase cash reserves to protect against financial shocks and maintain smooth operations because policy uncertainty lowers asset returns and raises the cost of external financing, which exacerbates firms' financial constraints (Brogaard and Detzel 2015; Gilchrist et al. 2014; Pástor and Veronesi 2013). According to the real option theory, businesses may decide to put off investments when there is a lot of uncertainty (Bernanke 1983; Dixit and Pindyck 1994; Gulen and Ion 2016), which also results in a rise in cash reserves. Increased cash reserves can give businesses the flexibility they need to take advantage of potentially profitable investment opportunities when economic policy uncertainty subsides because such uncertainty is usually only temporary. Uncertainty over economic policy can also make managers more conservative (Panousi and Papanikolaou 2012), leading businesses to hoard more cash, the most liquid asset. For these reasons, we anticipate a positive correlation between cash holdings and economic policy uncertainty, as hypothesized here:

H1-b:

EPU is associated negatively with CCH.

Demir and Ersan (2017) discussed how economic risk affects cash-holding choices and accounts for future uncertainty in BRIC nations. According to the authors, economic risk is a significant factor in determining cash holding methods. Businesses tend to handle more cash during times of high economic risk to control everyday operations. In this way, economic risk significantly and favourably influences the decision to store cash. According to Anand et al. (2018), businesses store more cash when there are greater growth opportunities. Using panel data from US-based companies, Baum et al. (2009) analyzed the influence of economic risk on capital investment and concluded that it has a detrimental effect. In order to manage enough cash on hand to prevent a crisis, businesses must concentrate on economic risk behaviour. Phan et al. (2019) drew some conclusions about the impact of economic risk on a firm's cash holdings in a different study.

According to Anand et al. (2018), businesses hold less cash as interest rates rise and currencies appreciate. According to other studies, macroeconomic variables like interest rates and inflation rates significantly determine how much cash corporations hold (Chen and Mahajan 2010; Natke 2001). Infante and Plazza (2014) provided evidence that businesses with political ties benefit from low loan rates. According to Hunjra et al. (2020), interest rate mechanisms designed by financial system administrators aid in regulating risky investments. The three components of economic risk are early recovery, robust recovery, and economic crest, according to Chang et al. (2019) classification of economic risk. They discovered a connection between inflation and a company's choice of financing. Additionally, businesses try to get around the funding limitations by issuing more shares when the economy is at risk. Unrestricted financing companies provide debt in reaction to debt market spreads. Based on the above arguments, we developed our next hypothesis:

H1-c:

Inflation risk has a positive association with CCH.

Baum et al. (2006) demonstrated that time variation in the cross-sectional distribution of cash holding ratios of US enterprises results from macroeconomic uncertainty. Additionally, Baum et al. (2008) provided evidence that businesses store more cash when macroeconomic or regional uncertainty rises. This suggests that keeping liquid assets on hand during more uncertain times is done out of caution. When Baum et al. (2006, 2008) findings are taken into consideration, it can be said that macroeconomic and idiosyncratic uncertainty causes enterprises to hoard more cash because it prevents sources from being used and delays possible investment initiatives. Bhaduri and Kanti (2011) investigated the effects of macroeconomic policy uncertainty on the cash holdings of Indian enterprises by using comparable metrics of uncertainty to Baum et al. (2006, 2008).

According to research, Indian companies store more cash as uncertainty rises, which is consistent with findings from the USA. Additionally, middle-aged and middle-sized businesses are the ones most impacted by macroeconomic unpredictability. According to Baum et al. (2012), managers’ choice of liquidity is influenced by both the degree of governance and macroeconomic uncertainty. The demand for cash driven by precautionary motivation impacts the cash holdings of non-financial US enterprises. The degree of uncertainty at the business and macroeconomic levels can alter, and this can impact how much cash a firm holds. Song and Lee (2012) examined how the 1997–1998 Asian financial crisis affected East Asian companies’ cash holdings over the long term. Asian companies chose to hold more capital due to higher cash flow risk and fewer expansion opportunities in the post-crisis environment. Our fourth hypothesis is thus:

H2-a:

Construction (financial) sector cash holdings are more (less) than in other sectors

In many commercial activities, political connections are crucial. They occasionally work very well for a corporation, even though they do not always benefit the economy. According to Fisman (2001), Faccio (2006), Faccio et al. (2006), and Bunkanwanicha and Wiwattanakantang (2009), a company can leverage political connections to improve operations and boost value. The stock prices of politically connected enterprises respond favourably to claims of the Indonesian president's good health, according to Fisman (2001), who tracked the stock price reactions of politically connected and unconnected firms vis-a-vis these rumours. Political contacts are, therefore, valuable. Faccio (2006) examined how a company’s executive’s election to a significant government position affects the firm’s value. According to Faccio, such elections significantly increase the value of businesses in highly corrupt nations. According to Claessens et al. (2008), banks often lend more money to politically linked businesses than to unconnected ones. In a 22-country study of mergers and acquisitions, Brockman et al. (2013) found that politically connected bidders performed 20% better than unconnected bidders in nations with weak legal systems and high levels of corruption, which suggests that connected bidders learn more about merger targets from their political connections. In Italy, politically linked businesses benefit from lower lending rates when those connections are at the local level, according to research by Infante and Piazza (2014). The effect is higher in areas with high levels of corruption.

Roberts (1990) offered a pioneering analysis of the effects of political unpredictability on businesses by looking at stock price responses to US Senator Henry Jackson’s untimely death in 1983. According to the author, stock values for companies affiliated with the senator were generally down. Political turbulence following the senator's passing caused stock values to decline. The effects of French municipal elections on business investments waere studied by Bertrand et al. (2006). In order to help the incumbent municipal officials win re-election during the politically tumultuous election season, politically linked CEOs upped their investments, particularly in politically charged cities. That is, more business investments could result from political instability. Fan et al. (2008) investigated the effects of the arrest of corrupt officials with political ties to enterprises on firm leverage and stock prices in China. The associated enterprises experienced political unrest following the arrests. After that, their leverage and stock price decreased, demonstrating the negative effect of political unpredictability on corporate value.

Cash is a valuable and movable company asset. Investors and academics are interested in the rising trend in US company cash holdings, according to Bates et al. (2009), who found that the average cash-to-assets ratio of US industrial enterprises increased from 10.5 to 23% between 1980 and 2006. Previous research has provided several explanations for CCH, including transaction costs (Mulligan 1999), precautionary motives (Bates et al. 2009; Han and Qiu 2007; Khieu and Pyles 2012; Opler et al. 1999), corporate governance (Dittmar and Mahrt-Smith 2007; Harford et al. 2008; Kuan et al. 2011), business organisation structure (Locorotondo et al. 2014), tax incentives (Foley et al. 2007; Pinkowitz et al. 2013), product market competition (Fresard 2010), and idiosyncratic risk (Campbell et al. 2001).

For 48 countries from 1980 to 2005, Julio and Yook (2012) examined corporate investments during 248 national elections. They contended that an election can result in a negative consequence for a corporation because of political unpredictability in election years, meaning it can be advantageous to delay investment. After accounting for other factors, the authors found that businesses cut their investments by an average of 4.8% during political unrest. According to a 2016 study by An et al. on the effects of political unpredictability on corporate investments, there is a decline in investment in Chinese cities when there is a change in the composition of the government. Based on these points, we developed our final hypothesis.

H2-b:

U.S. firms hold more (less) cash during Democrat (Republican) presidential terms

3 Data and methodology

3.1 Data and measurement

We accumulated data from several sources to investigate the impact of EPU and inflation risk on CCH. We collected firm-level financial data from the Compustat–Capital I.Q. (Global) database of Wharton Research Data Services (WRDS). Firm age was calculated from the annual proxy statement for each firm. We considered the World Bank's databank (https://data.worldbank.org/indicator) for inflation and GDP variables. Finally, we collected EPU from the US Economic Policy Uncertainty Index for the United States (USEPUINDXD) from the Federal Reserve Economic Data (FRED) database.

We winsorized all the continuous variables at the 1st and 99th percentile to alleviate the probable impact of outliers on the results and drop all the missing values. The final sample for our panel dataset consisted of 18,690 firm-year observations for 1869 US firms from 2011 to 2021.

3.2 Variable definitions

In this section, we focus on the definition of variables. The dataset included one dependent, two independent, and nine control variables (Table 1).

In sum, to conduct the empirical analysis we considered cash as a dependent variable; inflation and EPU as independent variables,; and optimism, size, TQ, leverage, volatility, DV, Cap, FAGE, and GDP Growth as control variables.

3.3 Methodology

The baseline regression model for our analysis took the following form:

where Cashijt is the total CCH for firm i in industry j at time t, EPUt is the index of EPU, Inflationt is the annual inflation rate (CPI, and Inflation_EPUt is the interaction variable between inflation and EPU at time t, captured in coefficients β1-β3, respectively. Controlsijt is a vector of control variables that includes optimism, size, TQ, leverage, volatility, DV, Cap, FAGE, and GDP Growth. µi and µt are the firm-specific and time-fixed effects, respectively.

EPU may impact CCH negatively. In this case, firms manage their cash holdings down during high policy uncertainty periods to mitigate the organization’s financial problems (Javadi et al. 2021). Therefore, we expect the sign β1 to be negative.

Conversely, we are hoping that β2 holds a positive value since a high inflation rate implies country risks that have a major impact on the condition of that country's companies. Changes in a country's macroeconomic conditions implicitly impact companies’ cash holdings. Firms tend to save cash for future investment opportunities, which strengthens when economic booms occur. A high inflation rate may reduce the purchasing power in a country, thereby decreasing corporate income. A company's reduced income results in fewer available funds to be used as retained earnings (Setiawan and Rachmansyah 2019). Our expected value of β3 is positive, implying that, in the presence of inflation, EPU and inflation risk jointly impact CCH positively.

Next, we applied the two-step system Generalized Method of Moments (GMM) approach (Blundell and Bond 1998) to control for potential endogeneity issues while finding the relationship between CCH and EPU and inflation:

where Cashijt-1 and Cashijt-2 are the one-year and two-year lagged values of firms' CCH, respectively.

4 Findings

4.1 Descriptive statistics

Table 2 reports the sample's descriptive statistics, namely the mean, median and standard deviation for our variables. This table represents the macro-level variables such as inflation, EPU, GDP (GDP growth), and firm-level variable cash (CCH). It also includes other firm-specific characteristics such as firm age, size, net capital expenditure, common dividends, book leverage, earnings volatility, the ratio of market value assets to book value assets, and the CEO's average money holdings.

Table 2 shows that the average cash holding of the sample of firms is approximately 0.156, with a standard deviation of 0.17. In addition, the average inflation risk is 1.89% and EPU is 114.48, with standard deviations of 1.12 and 59.52, respectively. These figures indicate that, despite less dispersion in firms' cash holdings from the average value, inflation risk and EPU affected the sample of firms differently.

Table 3 represents the pairwise correlation matrix, which shows that the firm's CCH are positively correlated with inflation risk (inflation = 0.002) and negatively correlated with EPU (EPU = − 0.023). This table also shows that inflation risk is positively correlated with EPU (EPU = 0.082). This correlation suggests that EPU raises the risk of future inflation.

Following Berry et al. (1985), we checked the multicollinearity issues between two independent variables. We did not find any multicollinearity problems in the regression as the bivariate correlations did not exceed 0.80. This indicates that multicollinearity was not a problem in the regressions.

4.2 Empirical results

This section documents the baseline results related to the impact of EPU and inflation on firms' cash holdings from the estimation of Eq. (1). We used cash as the dependent variable while EPU and inflation risk are considered independent variables, along with CEO characteristics and firm and country-level control variables in the regression models.

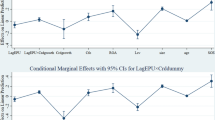

In column 1 of Table 4, we see the coefficient of inflation is positive (0.003), which is economically and statistically significant (< 0.01) using control variables without any fixed effects. In column 2, we find the coefficient for EPUt is negative (- 0.00003), which is economically and statistically significant (< 0.01) using control variables without any fixed effects. In column 3, the coefficient for Inflation_EPUt is positive (0.00008) and statistically significant (< 0.01). After controlling for the period of COVID-19, column 4 shows that the regression coefficient of Inflation_EPUt is still positive and statistically significant. In column 5, after adding time-fixed effects, the interaction variable and economic policy uncertainty remain statistically significant, holding the same sign as without year-fixed effects. In column 6, we add year and sector fixed effects and get a similar result as column 5. In both cases, fixed effects result in an insignificant impact of inflation risk on CCH. Our findings suggest that inflation and EPU positively impacted cash holdings. Although only EPU impacted negatively on CCH, only inflation risk was linked positively with CCH. These results suggest that firms hold more cash during inflationary periods because of available cash in the market, but they cannot hold more cash during periods of EPU because of financial uncertainty in the economy. However, firms hold cash when high inflation and EPU periods occur together. These findings support additional contributions to prior literature (Duchin et al. 2010; Wang et al. 2014; Chen et al. 2015) and our proposed hypotheses (H1-a, H1-b and H1-c).

From Table 5, we see that among the six sectors of the economy, only the construction and retail sectors saw a significant impact. We included year and sector-specific characteristics for the regression of all sectors. EPU and inflation jointly impacted CCH positively, which is statistically significant (< 0.01) for the construction and retail sectors. This finding suggests that EPU mainly affects the CCH of firms in the construction sector and inflation affects the CCH of firms in the retail sector. From these two sectors, the joint impact in the construction sector is larger (0.00088) than in the retail sector (0.00032). Overall, these results are consistent with our baseline findings and support additional contributions to the existing literature (Duchin et al. 2010; Wang et al. 2014; Chen et al. 2015) and our proposed hypothesis (H2-a).

Table 6 shows that the joint impact of EPU and inflation on CCH is positive and statistically significant (< 0.01), irrespective of the political party which holds the presidency. Notably, this impact is stronger during a Democratic presidency (0.00175) than a Republican presidency (0.00006). The intensity of the impact of Inflation_EPU on CCH is similar when we control for industry-specific effects; in a Democratic term, the impact is 0.00135, and in a Republican term, it is 0.00006. Overall, these results are consistent with previous findings and support additional contributions to the existing literature (Duchin et al. 2010; Wang et al. 2014; Chen et al. 2015) and our hypothesis (H2-b).

4.3 Robustness tests and endogeneity

We estimated whether our findings would hold the same results when considering firm size (large or small) and different types of policy uncertainty. Table 7 reports the regression results for the impact of EPU and inflation on firms' cash holdings for large and small firms. Small firms were classified based on size (median) if the size was below or equal to the median size of the sample of firms. We considered a firm large if its size exceeded the median size of sample firms. From estimating Eq. (1), columns 1 and 3 give the results for large and small firms without any fixed effects. Columns 2 and 4 present the regression results for large and small firms with time (year) and sector-fixed effects (within-sector analysis).

In column 1 of Table 7, we find the coefficient for Inflation_EPUt for large firms is positive (0.00005), which is economically and statistically significant (< 0.01) after using control variables. In column 2, adding the fixed effects raised the impact from 0.00005 to 0.00016, which is also economically and statistically significant (< 0.01). The joint effect of EPU and inflation risk is positively significant (< 0.01) only if we do not consider any fixed effects. Column 3 shows that small firms' CCH respond to the joint impact of EPU and inflation without any fixed effects (0.00008). The coefficient for Inflation_EPUt is still positive but becomes statistically insignificant when we add the time (year) and sector-specific characteristics (column 4). These results are consistent with the baseline regression results, indicating robust findings. In addition, these findings suggest that the macroeconomic variables affected large firms' CCH more than small firms’ CCH. These findings also support additional contributions to the existing literature (Duchin et al. 2010; Wang et al. 2014; Chen et al. 2015).

Table 8 represents the impact of different types of policy uncertainty on firms' CCH. Columns 1 to 8 reflect the results for several policy uncertainties. In column 1, we find the coefficient of monetary policy uncertainty is negative (0.00024), which is economically and statistically significant (< 0.01) after using control variables and fixed effects (year and sector-specific). Likewise, other policy uncertainties give similar negative and statistically significant (< 0.01) results. Among these eight types of policy uncertainty, Sovereign Debt Currency Crises dominate (0.00037) other uncertainties as they are directly related to the currency. Again, our findings are robust since these results are consistent with prior results (negative and statistically significant). In addition, these findings suggest that any form of EPU negatively affects firms' cash holdings. These findings also support additional contributions to the existing literature (Duchin et al. 2010; Wang et al. 2014; Chen et al. 2015).

Table 9 presents the GMM estimation to mitigate the endogeneity problem (Das et al. 2023; Hasan et al 2022; Hasan et al. 2023a, b, 2023a). The first column of Table 9 indicates a positive relationship between inflation risk and CCH (0.00395). The second and third columns show the negative impact of EPU (− 0.00004) and the positive joint impact of EPU and inflation risk (0.00008) on CCH, respectively. Finally, the fourth column indicates the results of the two-step system GMM. Here, we consider the first and second-lagged CCH as independent variables along with year and sector fixed effects. The coefficients of lagged cash holdings are positive and statistically significant (< 0.01). Most importantly, the joint impact of EPU and inflation risk on CCH remains positive (0.00010) and statistically significant (< 0.01) after estimating the dynamic model.

Therefore, after re-estimating the baseline models, we get similar results. We observe that the coefficients of lagged CCH are positive. In addition, the interaction term coefficient remains positive (consistent), and the results are significant at the 1% level (consistent). Overall, the endogeneity problem does not affect our findings, and the reported results are robust. Overall, these results are consistent with our prior findings and support additional contributions to the previous literature (Duchin et al. 2010; Wang et al. 2014; Chen et al. 2015).

5 Conclusion

Covering 2011 to 2021, this paper has looked at the combined effects of inflation risk and EPU on CCH for US enterprises. The initial findings show a positive correlation between EPU, inflation risk, and CCH. Additionally, we discovered a similar relationship between CCH and inflation risk. However, we found a negative correlation between CCH and EPU. Additionally, during periods of inflation risk and EPU, businesses in the construction (financial) sectors maintain more (less) cash. Notably, we also discovered that companies hold more (less) cash during Democratic presidencies than during Republican presidencies, respectively. The two-step system GMM technique supports the baseline findings and was used to control for any endogeneity problems.

The consequences of this study for businesses centre on how to handle funds, particularly when there is political unpredictability. As a result, this study assists US businesses in controlling their cash flow while coping with uncertain economic conditions. In these circumstances, businesses need to retain extra cash on hand to cover other financial obligations as well as to function in uncertain economic conditions. High-interest rates and inflation are problems faced by developed nations, which eventually force businesses to control the amount of cash they have. Our findings imply that businesses boost investment during inflationary periods while decreasing CCH. However, high-interest rates also justify raising additional money to cover interest costs. Therefore, in order to avoid paying more interest, we advise businesses to maintain a balance between internal financing and loan financing rather than relying solely on the latter. We advise financial managers to consider outside variables like the VINF and interest rate while managing cash holdings.

Availability of data and materials

All relevant data and materials are available.

Code availability

Not Applicable.

References

Ameer R (2012) Impact of cash holdings and ownership concentration on firm valuation: empirical evidence from Australia. Rev Acc Financ 11:448–467

Amess K, Banerji S, Lampousis A (2015) Corporate cash holdings: causes and consequences. Int Rev Financ Anal 42:421–433

An H, Chen Y, Luo D, Zhang T (2016) Political uncertainty and corporate investment: evidence from China. J Corp Financ 36:174–189

Anand L, Thenmozhi M, Varaiya N, Bhadhuri S (2018) Impact of macroeconomic factors on cash holdings?: a dynamic panel model. J Emerg Mark Financ 17(1):1–27

Anderson RW, Hamadi M (2016) Cash holding and control-oriented finance. J Corp Financ 41:410–425

Baker SR, Bloom N, Davis SJ (2016) Measuring economic policy uncertainty. Quart J Econ 131(4):1593–1636

Bates T, Kahle M, Stulz R (2009) Why do U.S. firms hold so much more cash than they use to? J Financ 64:1985–2021

Baum CF, Caglayan M, Ozkan N, Talavera O (2006) The impact of macroeconomic uncertainty on non-financial firms’ demand for liquidity. Rev Financ Econ 15:289–304

Baum CF, Caglayan M, Stephan A, Talavera O (2008) Uncertainty determinants of corporate liquidity. Econ Model 25:833–849

Baum CF, Stephan A, Talavera O (2009) The effects of uncertainty on the leverage of nonfinancial firms. Econ Inq 47(2):216–225

Baum CF, Chakraborty A, Han L, Liu B (2012) The effects of uncertainty and corporate governance on firms’ demand for liquidity. Appl Econ 44:515–525

Baumol WJ (1952) The transactions demand for cash: an inventory theoretic approach. Q J Econ 66:545–556

Bernanke BS (1983) Irreversibility, uncertainty, and cyclical investment. Q J Econ 98:85–106

Berry WD, Feldman S, Stanley Feldman D (1985) Multiple regression in practice. Sage, Thousand Oaks

Bertrand M, Karmarz F, Schoar A, Thesmar D (2006) Politicians, firms, and the political business cycle: evidence from france. University of Chicago, Working Paper

Beuselinck C, Du Y (2017) Determinants of cash holdings in multinational corporation’s foreign subsidiaries: US subsidiaries in China. Corp Gov Int Rev 25(2):100–115

Bhaduri SN, Kanti M (2011) Macroeconomic uncertainty and corporate liquidity: the Indian case. Macroecon Financ Emerg Mark Econ 4(1):167–180

Blundell R, Bond S (1998) Initial conditions and moment restrictions in dynamic panel data models. J Econom 87(1):115–143

Brockman P, Rui OM, Zou H (2013) Institutions and the performance of politically connected M&As. J Int Bus Stud 44:833–852

Brogaard J, Detzel A (2015) The asset-pricing implications of government economic policy uncertainty. Manag Sci 61:3–18

Bunkanwanicha P, Wiwattanakantang Y (2009) Big business owners in politics. Rev Financ Stud 22(6):2133–2168

Campbell J, Lettau M, Malkiel B, Xu Y (2001) Have individual stocks become more volatile? An empirical exploration of idiosyncratic risk. J Financ 56:1–43

Caprio L, Faccio M, McConnell JJ (2013) Sheltering corporate assets from political extraction. J Law Econ Organ 29(2):332–354

Chang X, Chen Y, Dasgupta S (2019) Macroeconomic conditions, financial constraints, and firms’ financing decisions. J Bank Financ 101:242–255

Chen N, Mahajan A (2010) Effects of macroeconomic conditions or corporate liquidity: international evidence. Int Res J Financ Econ 35(1):112–129

Chen Y, Dou PY, Rhee SG, Truong C, Veeraraghavan M (2015) National culture and corporate cash holdings around the world. J Bank Financ 50:1–18

Claessens S, Feijen E, Laeven L (2008) Political connections and preferential access to finance: the role of campaign contributions. J Financ Econ 88:554–580

Das BC, Hasan F, Suthadhar SR, Shafique S (2023) Impact of Russia–Ukraine war on stock returns in European stock markets. Glob J Flex Syst Manag 24(3):395–407

Demir E, Ersan O (2017) Economic policy uncertainty and cash holdings: evidence from BRIC countries. Emerg Mark Rev 33:189–200

Dittmar A, Mahrt-Smith J (2007) Corporate governance and the value of cash holdings. J Financ Econ 83(3):599–634

Dixit A, Pindyck R (1994) Investment under uncertainty. Princeton University Press

Duchin R, Ozbas O, Sensoy BA (2010) Costly external finance, corporate investment, and the subprime mortgage credit crisis. J Financ Econ 97(3):418–435

Evers M, Niemann S, Schiffbauer M (2020) Inflation, liquidity and innovation. Eur Econ Rev 128:103506

Faccio M (2006) Politically connected firms. Am Econ Rev 96:369–386

Faccio M, McConnell JJ, Masulis RW (2006) Political connections and corporate bailouts. J Financ 61:2597–2635

Fama EF, French KR (2005) Financing decisions: who issues stock? J Financ Econ 76(3):549–582

Fan JPH, Rui OM, Zhao M (2008) Public governance and corporate finance: evidence from corruption cases. J Comp Econ 36(3):343–364

Fisman R (2001) Estimating the value of political connections. Am Econ Rev 91:1095–1102

Foley C, Hartzell J, Titman S, Twite G (2007) Why do firms hold so much cash? A tax-based explanation. J Financ Econ 86:579–607

Francis BB, Hasan I, Zhu Y (2014) Political uncertainty and bank loan contracting. J Empir Financ 29:281–286

Fresard L (2010) Financial strength and product market behavior: The real effects of corporate cash holdings. J Financ 65:1097–1122

Frye T, Shleifer A (1997) The invisible hand and the grabbing hand. Am Econ Rev 87:354–358

Gilchrist S, Sim J, Zakrajšek E (2014) Uncertainty, financial frictions, and investment dynamics. National Bureau of Economic Research

Guariglia A, Yang J (2018) Adjustment behavior of corporate cash holdings: the China experience. Eur J Financ 24(16):1428–1452

Gulen H, Ion M (2016) Policy uncertainty and corporate investment. Rev Financ Stud 29:523–564

Han S, Qiu J (2007) Corporate precautionary cash holdings. J Corp Financ 13:43–57

Harford J, Klasa S, Maxwell WF (2014) Refinancing risk and cash holdings. J Financ 69(3):975–1012

Harford J, Mansi SA, Maxwell WF (2008) Corporate governance and firm cash holdings in the US. J Financ Econ 87:535–555

Hasan F (2022) Using UK data to study the effects of dividends announcements on stock market returns. J Predict Mark 16(2):47–75

Hasan F, Shafique S, Das BC, Shome R (2022) R&D intensity and the effect of dividend announcements on stock return: an even study analysis. J Appl Acc Res 23(4):846–862

Hasan, F., Kayani, U. N., and Choudhury, T. (2023). Behavioral risk preferences and dividend changes: exploring the linkages with prospect theory through empirical analysis. Global J Flex Syst Manag (In Press)

Hasan F, Al-Okaily M, Choudhury T, Kayani UN (2023) A comparative analysis between Fintech and traditional stock markets: using Russia and Ukraine WAR data. Electron Commer Res (In Press)

Huang T, Wu F, Yu J, Zhang B (2015) Political risk and dividend policy: evidence from international political crises. J Int Bus Stud 46(5):574–595

Hunjra AI, Tayachi T, Mehmood R (2020) Impact of ownership structure on risk-taking behavior of South Asian banks. Corp Ownersh Control 17(3):108–120

Hunjra AI, Tayachi T, Mehmood R, Hussain A (2022) Does economic risk affect corporate cash holdings? J Econ Adm Sci 38(3):471–484

Infante L, Piazza M (2014) Political connections and preferential lending at local level: some evidence from the Italian credit market. J Corp Financ 29:246–262

Javadi S, Mollagholamali M, Nejadmalayeri A, Al-Thaqeb S (2021) Corporate cash holdings, agency problems, and economic policy uncertainty. Int Rev Financ Anal 77:101859

Jensen MC (1986) Agency costs of free cash flow, corporate finance, and takeovers. Am Econ Rev 76(2):323–329

Johannsen BK (2014) When are the effects of fiscal policy uncertainty large? FEDS Working Paper, 40

Julio B, Yook Y (2012) Political uncertainty and corporate investment cycles. J Financ 67(1):45–83

Keynes JM (1936) The general theory of employment interest and money Harcourt

Khieu H, Pyles M (2012) The influence of a credit rating change on corporate cash holdings and their marginal value. Financ Rev 47:351–373

Kim CS, Mauer DC, Sherman AE (1998) The determinants of corporate liquidity: theory and evidence. J Financ Quant Anal 33(3):335–359

Kuan T, Li C, Chu S (2011) Cash holdings and corporate governance in familycontrolled firms. J Bus Res 64:757–764

Li X (2019) Economic policy uncertainty and corporate cash policy: international evidence. J Acc Public Policy 38(6):106694

Locorotondo R, Dewaelheyns N, Hulle C (2014) Cash holdings and business group membership. J Bus Res 67:316–323

Mulligan CB (1999) Galton versus the human capital approach to inheritance. J Polit Econ 107(S6):S184–S224

Myers SC, Majluf NS (1984) Corporate financing and investment decisions when firms have information that investors do not have. J Financ Econ 13:187–221

Natke PA (2001) The firm demand for liquid assets in an inflationary environment. Appl Econ 33(4):427–436

Nguyen N, Phan H (2017) Policy uncertainty and mergers and acquisitions. J Financ Quant Anal 52:613–644

Opler T, Pinkowitz L, Stulz R, Williamson R (1999) The determinants and implications of corporate cash holdings. J Financ Econ 52(1):3–46

Panousi V, Papanikolaou D (2012) Investment, idiosyncratic risk, and ownership. J Financ 67:1113–1148

Pástor Ľ, Veronesi P (2013) Political uncertainty and risk premia. J Financ Econ 110:520–545

Phan HV, Nguyen NH, Nguyen HT, Hegde S (2019) Policy uncertainty and firm cash holdings. J Bus Res 95:71–82

Pinkowitz L, Stulz R, Williamson R (2006) Does the contribution of corporate cash holdings and dividends to firm value depend on governance? A cross-country analysis. J Financ 61(6):2725–2751

Pinkowitz, L., Stulz, R.M. and Williamson, R., (2013). Is there a US high cash holdings puzzle after the financial crisis? Fisher College of Business working paper, (2013-03), 07

Roberts BE (1990) A dead senator tells no lies: seniority and distribution of federal benefits. Am J Polit Sci 34:31

Setiawan R, Rachmansyah AB (2019) Firm characteristics, macroeconomic variables and cash holdings in Indonesia and Singapore. Int J Innov Creat Change 9(8):265–286

Song KR, Lee Y (2012) Long-term effects of a financial crisis: evidence from cash holdings of East Asian firms. J Financ Quant Anal 47(3):617–641

Stock JH, Watson MW (2012) Disentangling the channels of the 2007–2009 Recession (No. w18094). National Bureau of Economic Research

Venkiteshwaran V (2011) Partial adjustment toward optimal cash holding levels. Rev Financ Econ 20(3):113–121

Wang HJ, Li QY, Xing F (2014) Economic policy uncertainty, cash holdings and market value. J Financ Res 9:53–68

Xu N, Chen Q, Xu Y, Chan KC (2016) Political uncertainty and cash holdings: evidence from China. J Corp Finan 40:276–295

Funding

Not Applicable.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

Not Applicable.

Human and animal rights

Not applicable.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Das, B.C., Hasan, F. & Sutradhar, S.R. The impact of economic policy uncertainty and inflation risk on corporate cash holdings. Rev Quant Finan Acc 62, 865–887 (2024). https://doi.org/10.1007/s11156-023-01224-6

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-023-01224-6