Abstract

The Hong Kong stock market is known to be highly volatile. Professional investors have a strong demand for timely information because of the infrequent nature of Hong Kong analysts’ interim reports (Cheng et al., 2003). Our paper provides a comprehensive study of investor reactions to analysts’ recommendations in the Hong Kong stock market from 2009 to 2014 under different sentiment scenarios. We find that analysts’ recommendation upgrades and downgrades deliver significant information to the Hong Kong stock market. However, analysts’ initiation coverages convey little information and bring about limited impact to the stock market. In addition, analysts’ upgrades and downgrades result in significant differential price impacts in bullish and the bearish phases.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

By offering high quality and up-to-date investment analyzes and recommendations to individual and institutional clients, brokerage houses and investment banks can charge significant fees for the access to accurate research reports which are of benefit to the customers. Beside this, one can expect these investment recommendations to generate transaction profits for the brokerage houses as clients will implement the suggested trading strategies and therefore buy or sell securities.

Unsurprisingly, the value and performance of analysts’ recommendations are constantly subjected to criticisms. A critical problem is the analysts’ constant exposure to potential conflicts of interests and hence the possible publication of over-optimistic stock recommendations that are not in the best interest of the investor. Michaely and Womack (1999), and Agrawal and Chen (2008) point towards this issue within financial institutions and suggest that frequent conflicts of interest between the research and the corporate finance department may result in analysts’ compromising their recommendations in order to maximize their company’s profits. This conflict of interest is especially high and leads to positively biased recommendations when they concern existing and potential corporate clients (Michaely and Womack 1999, 2005). And Chan et al (2018) find that analysts’ stock ownership induces analysts to bias upwards their target price forecasts. This study empirically investigates the relationship between equity performance, stock recommendations and market sentiment in the Hong Kong equity market.

It is not surprising that sell-side analysts are criticized for having a greater incentive to issue buy rather than sell recommendations because the former usually generates greater trading volume from clients (Lin and McNichols 1998). Firth et al. (2013) find that analysts’ recommendations on a stock are significantly higher if the stock is held by mutual fund clients of the analysts’ brokerage firm; however, their study focuses on the relationship between mutual funds and sell-side analyst recommendations. Michaely and Womack (1999) go even further and show that a positive recommendation issued after a company’s IPO may be necessary to increase the likelihood that the institution will be chosen as the next offering underwriter. Other studies argue that generally, analysts are more reluctant to provide negative outlooks for companies (Jegadeesh and Kim 2006; Michaely and Womack 2005; Barber et al. 2001). Aggarwal et al. (2018) document that when forming recommendations, analysts underestimate the role of the cost of equity.

As a result, the stock recommendations provided by analysts may be of lesser value than expected by the clients and might therefore result in unprofitable opportunities for investors. More specifically, it is questionable if investors can realize profits (or avoid losses) by purchasing upgraded securities (selling downgraded securities). Apart from that, market sentiment also plays an important role in the performance of an analyst’s stock recommendations. Baker and Wurgler (2007) give two definitions of investor sentiment: first as a driver of relative demand for speculative investments, and second as the investors’ collective optimism (or pessimism) about stocks in general. Furthermore, they also find that stock prices are subject not only to fundamental factors but also to market sentiment.

It is therefore understandable that analysts might consider current market sentiments when conducting their analysis and making recommendations. When issuing stock ratings based on the comparison between the firm’s expected future stock price and the firm’s current stock price, analysts will consider both the fundamental underlying factors, such as earnings, assets and liabilities, as well as investor sentiment such as past stock returns (Brown and Cliff 2004); the same applies when making recommendations (Bagnoli et al. 2009). In a more recent study, Li et al. (2015) show that analysts could facilitate price discovery to corporate news by issuing trending and contrarian revisions. Even though their study applies intraday data in the US, Li et al. (2015) do not consider if the market environment (such as bullish and bearish conditions) affect price discovery and reversal of recommendations.

As stated above, this study addresses the shortcomings of previous research and explores the empirical relationship between equity performance, stock recommendations and market sentiment between January 2009 and May 2014 in the Hong Kong equity market. The Hang Seng Index, Hong Kong’s major stock index, is known to be highly volatile which makes professional investors eager to obtain more timely information on corporate earnings. However, Hong Kong analysts tend to make drastic revisions since their interim reports are not frequent enough compared to the quarterly reports generated by US analysts with richer information (Cheng et al. 2003). Therefore, analyzing the effect of stock recommendations on equity prices based on Hong Kong equity market can provide a helpful environment to understand and seek for the answers the investors may have about the analyst recommendation effects. The Hong Kong Stock Exchange (SEHK) is Asia’s third largest stock exchange in terms of market capitalization and is placed seventh largest in the world; it is therefore of great significance to investors. SEHK operates two markets on which companies may choose to list their shares: the Main Board and the Growth Enterprise Market (GEM). The Hang Seng Index (HSI) is widely regarded as the market benchmark monitoring daily movements of the largest companies listed on the Hong Kong stock market and is the main indicator of the overall market performance in Hong Kong. The HSI is a free float-adjusted market capitalization-weighted stock market index and comprises the 50 major constituent stocks, therefore including 60% of the total market share of the Hong Kong Stocks Exchange (Bloomberg.com). By considering the market environment, we specifically test whether stock recommendation upgrades and downgrades would generate higher and lower profits, respectively under the given market sentiment. Answering these questions is important for decision makers in order to understand if the performance of potentially biased recommendations might be affected by short-term market atmosphere. Previous studies ignore these crucial considerations allowing us to fill a gap and provide vital insights into Asia’s third largest stock exchange in terms of market capitalization.

This study examines the short-term impact of stock recommendations on the 26 largest constituent weighted stocks of the Hong Kong stock market, representing together a market capitalization of more than three trillion US Dollars. Market conditions of the global financial context affect investors’ confidence and the quality of their recommendations; we therefore argue that analysts factor market sentiment into their forecasts and issue over-optimistic and/or over-pessimistic stock recommendations during different periods. In more bullish periods, analysts and investors may be over-optimistic about the future of a company, hence issuing buy recommendations leading to higher short-term returns as investors are more inclined to purchase the given security.

We investigate the short-term impact of those recommendations in bullish and bearish phasesFootnote 1 by bootstrapping the stock market data and evaluating whether the analysts’ recommendations affect the overall market sentiment under different market conditions. We gauge investor confidence firstly by relying on surveys reflecting what investors and key actors in the Hong Kong stock market believe, and second, by considering the actual state of the economy, by examining daily news coverages. With this data in hand, two subperiods are generated: a bullish phase and a bearish phase. Papakroni (2018) finds strong evidence that the impact of analyst forecast dispersion is more pronounced in the group of stocks that receive the least favorable recommendations in each period.

This study makes significant contributions to the literature on recommendations of stock analysts. First, our study investigates whether variations in the market conditions affect the recommendations issued by analysts. This is done by investigating the performance of stock recommendations through different periods of time, considering bull and bear markets, in order to determine whether analysts’ recommendations are influenced by stock market atmosphere. If indeed analyst recommendations are influenced by market sentiment, stock forecasts will be cyclical and correlated with the economic climate. Previous studies, such as Jegadeesh and Kim (2006), Bagnoli et al (2009) and Womack (1996) ignore this issue, making their conclusions less comparable to our work. A second contribution is that our study examines all major recommendations by analysts, including downgrades, upgrades, and initiations to sell or to buy respectively. Most related studies are narrow and focus on specific recommendations, such as upgrade and downgrade (Ang et al. 1998); initiations of coverage (Irvine 2003); and secondhand analyst recommendations (Chan and Fong 1996). A third contribution is the robustness of our paper which analyzes the period before and after a recommendation. Previous studies focus on posterior effects of analysts’ recommendation (Moshirian et al 2009) and pay little attention to the market situation before the recommendation. Although Petaibanlue et al. (2015) examine the period before the recommendations; they only do it based on impact on IFRS adoption. Our study makes a vital contribution to market participants and researchers by analyzing both the pre and post recommendation period and use standardized abnormal returns. Finally, and perhaps the most original contribution stems from the fact that ours is the first study to examine the conditional effect of market sentiment on the analysts’ recommendations with and without look-ahead biases. We extend this line of research by taking into consideration the effect of the look ahead bias (hindsight bias) and provide an approximation for the error associated by this look ahead bias.

The rest of the paper is organized as follows: Sect. 2 presents the relevant literature on the performance and value of stock recommendations in different time frames and target markets. Section 3 illustrates the methodology of this study while Sect. 4 describes the data and the sample selection. Section 5 presents and analyzes the major empirical results with robustness tests. Then Sect. 6 concludes.

2 Literature review

The extant literature on analysts’ recommendations related to investment information has developed in various aspects. Based on the comprehensive stock recommendations on U.S. stocks provided by fourteen major U.S. brokerage firms, Womack (1996) finds that the new added-to-sell recommendations are less frequent but more predictive than new added-to-buy recommendations. In other words, the analysts tend to perceive substantial risk in issuing sell recommendations since these are less frequent, more visible and contain more information compared to buy recommendations (Pratt 1993). Other recent studies (He et al 2020; Arif and De George 2020) have shown that analyst coverage has a negative impact on tax risk; and that loss sensitive investors are unable to completely eliminate the information loss arising from infrequent financial reporting which can affect the valuation of firms and the quality of financial markets. Consequently, analysts tend to herd more when the firm has negative media sentiment (Frijns and Huynh 2018). Barber et al. (2001) find results consistent with Womack (1996) and show that investors can generate significant positive (negative) abnormal returns by following analyst’ upgrades (downgrades) on securities, though abnormal loss provision generally reduces analyst coverage particularly in the banking sector (Hong et al 2020). Loh (2010) examines why the information conveyed by stock recommendations doesn’t get fully incorporated in the stock price when recommendations are released. He finds that the investor inattention contributes to a larger stock recommendation drift and that the subsequent drift reflects investors’ gradual realization of the true stock price implied by the published recommendation.

Green (2006), Chen and Cheng (2006) and Kadan et al. (2018) find that market participants with early access to recommendation information tend to earn higher profits than their peers without early access. Green (2006) argues that the trading profits increase with early access to both buy and sell recommendations while the latter shows larger increase by selling short following downgrades. Chen and Cheng (2006) maintain that stock recommendations contain valuable information and institutional investors under soft dollar arrangements can have timely access to these recommendations which contribute to their superior performance. Kadan et al. (2018) find that the early-informed news-driven institutions tend to accumulate wealth transferred from program traders who have less early information access advantages. Francis and Soffer (2006) find that both earnings forecast revisions and stock recommendations are significantly related to the market reactions to analysts’ reports and neither of these signals about the share values subsumes the other. According to Lee et al. (2018), however, the firms voluntarily issuing CSR-related reports tend to have richer information environment which reduces the value of analyst’s recommendations.

Investor sentiment serves as another important factor when analyzing stock recommendations. Bagnoli et al. (2009) and Corredor et al. (2013) find that analysts tend to issue more favorable stock recommendations when recent or future investor sentiment are optimistic. Bagnoli et al. (2009) also show that investor sentiment sensitive analysts tend to issue relatively less profitable stock recommendations while analysts who issue investor sentiment sensitive stocks offer more profitable recommendations than their peers. Chen and Matsumoto (2006) find that analysts issuing more favorable recommendations experience a greater increase in their relative forecast accuracy compared with analysts with less favorable recommendations. Furthermore, Barber et al. (2010) argue that the abnormal stock returns are the greatest conditional on the ratings change to buy and strong buy recommendations than to holds, sells and strong sells. Conditional on the ratings level, they find upgrades earn the highest returns and downgrades the lowest.

Evidence of impact from stock recommendations outside the US market has also been established. Focusing on the United Kingdom, Ryan and Taffler (2006) find that the price reaction in the UK market was similar to that of the US market in which the price impact of new sell recommendations was greater than that of new buy recommendations (Barber et al. 2007) but less susceptible to potential conflicts of interest than in the US. They find that the abnormal returns are associated with a firm’s information environment and analyst incentives.

Offering insights into an Asian country, Ang et al. (1998) evaluate the ability of four individual anonymous brokerage houses in Singapore to make buy recommendations from 1990 to 1992. They find that out of the four brokerage houses under research, only the buy recommendations of one firm had significant impact on the date of the recommendations. Surprisingly, by accounting for the effect of transactions costs, all positive abnormal returns were eliminated; implying that investors can’t earn positive abnormal return in excess of transactions costs by following the brokerage analyst’s recommendations.

Chan and Fong (1996) focus on whether the publication of an individual investors’ sentiment survey in Securities Firms’ Investment Analysis column (SFIA) of the Hong Kong Economic Journal (HKEJ) newspaper temporarily affects stock returns in the Hong Kong stock market. They suggest that the reporting of the recommendations in SFIA does induce trading, and there is also a heavy trading in the day just before the publication of SFIA. However, their study only focuses on the predictive ability for stock returns. Later, Chan and Fong (2004) investigate how stock prices are temporarily affected by SFIA. They find that the publication does not really predict the coming week’s return on large, medium, or small stocks while the daily closing prices for medium and small stocks are affected but not the large stocks. However, the SFIA publishes only the second-hand analysts’ recommendations not the first-hand ones which are usually provided to securities firms’ clients. Our paper uses the J.P. Morgan Hong Kong Investor Confidence Index, a quarterly investors’ sentiment index, and use the top 26 major stocks listed in the Hang Seng index to analyze the impact of analysts’ recommendations on the Hong Kong stock market. We then investigate the investors’ reactions to analysts’ recommendations based on investment sentiment with conditional probability applications and consider the effect of look-ahead bias.

3 Methodology

In order to analyze the performance of stock recommendations, we measure the abnormal return of the stocks linked to the release of recommendation upgrades or downgrades initiations (see Liu et al. 1990). The abnormal return for security i on event day t is defined as:

where Ri,t is the daily total return (including dividends) of security i for day t and Rm,t is the daily total return (including dividends) of the benchmark index in the Hong Kong market: the Hang Seng index.

In addition, the normal return of security i is calculated, while \({\widehat{\alpha }}_{i}\) and \({\widehat{\beta }}_{i}\) are the ordinary least square (OLS) estimates for the model parameters of security i obtained by regressing the total return of security i against the total return of the index. Moreover, the market model is estimated over the observations for 100 days,Footnote 2 while t = 0 is the release of the stock recommendation upgrades or downgrades initiations obtained from Bloomberg. Since the abnormal return of each security is defined, the average daily abnormal return of each day t within the event window, AARt, is calculated as:

where t = − 5, − 4, − 3 \(\cdots\), 0,\(\cdots\) 8, 9, 10.

The average cumulative daily abnormal return between t = t1 and t = t2, defined as \({ACAR}_{{t}_{1},{t}_{2}}\), is calculated as:

We test the statistical significance of the abnormal return for security i on day t by standardizing the returns as:

where \({S}_{i}\) is the residual standard deviation for stock i by using the estimation of the market model from t = − 5 to t = 10.

The average standardized daily abnormal return for each day of the event window (t = − 5, − 4, − 3 \(\cdots\), 0,\(\cdots\) 8, 9, 10), \({ASAR}_{t}\), is calculated by averaging the \({SAR}_{i,t}\) of all securities:

where t = − 5, − 4, − 3 \(\cdots\), 0,\(\cdots\) 8, 9, 10.

Furthermore, the t-statistics of average abnormal return for each date t is computed by:

We apply the 2-tailed t-statistics test to determine whether or not the abnormal return and the cumulative return are statistically significant for each day t. Specifically, if the t-statistics calculated lie outside the range of the distribution depending on a particular level of statistical significance (e.g. 5% significance level), then we should reject the hypothesis that the return is equal to 0 (i.e. the return is statistically significant).

There are other recent studies of analyst recommendations that also used a single factor model to estimate abnormal returns (see Amiram et al. 2016; Du et al. 2017; Kudryavtsev 2019; Kim et al. 2019). But, in a later section of our paper, we also estimate abnormal returns using the Fama & French 3-factor model (Eq. (7)) which has been used in some papers in the area (e.g., Rubanov and Nnadi 2018; Su et al. 2019; Li et al. 2020).

\({R}_{f,t}\) is the risk-free rate, \({\widehat{\alpha }}_{i}\) is the intercept and \({\widehat{\beta }}_{i}\) is the coefficient estimate of the excess market return \(\left({R}_{m,t}-{R}_{f,t}\right)\).\(\widehat{{s}_{p}}\) and \(\widehat{{h}_{p}}\) are the coefficients for the difference in our total sample Hong Kong stock portfolio p between small and big stocks (SMBt) and high and low book-to-market stocks (HMLt) at time t, respectively. We produce the size (SMBt) and book-to-market equity (HMLt) factors as follows. We sort our sample stocks into two size groups based on the median market capitalization (i.e., median size), denoted by S (small) and B (big). We then make another group by sorting our sample stocks into three groups of book-to-market equity values based on the thresholds for the bottom 30 percent (L, for “low”), middle 40 percent (M, for “medium”) and top 30 percent (H, for “high”). SMBt is the difference between the average returns on the three small stock portfolios (S/L, S/M and S/H) and the average returns on the three big stock portfolios (B/L, B/M and B/H) at time t. HMLt is the difference between the average returns on the two high book-to-market equity portfolios (S/H and B/H) and the two low book-to-market equity portfolios (S/L and B/L) at time t. We repeat the steps from Eqs. (2) to (6) using our Eq. (7) instead of (1) to perform our event study.

Finally, complementary to the above analysis, we study the impact of the previous quarter’s market sentiment when an analyst makes an ‘upgrade’, ‘downgrade’ or a ‘hold’ recommendation by employing a conditional probability model based on a binomial framework. In particular, we seek to find out what would be the conditional probability of an upgrade/hold/downgrade of a given stock, if the investor sentiment is positive/negative in the last quarter. We denote \({rec}_{i,t}\) as the analyst recommendation i = {upgrade, downgrade, hold} at time t. \({sen}_{j,t}\) as the investor sentiment j = {positive, negative} at time t. Then we express these in terms of probabilities, and use the cumulative data from one quarter to the next: The analyst recommendation probability is the cumulative recommendations from one quarter to the next, for example as from time s to time t. Similarly, the investor sentiment probability is the change in investor sentiment indices from one quarter to the next, also from time s to time t. (Please refer Panel D of Table 8 for a detailed methodology of the estimation). This investment sentiment probability is the normalized percentage change in investor sentiment index relative to the average sentiment. We express the combined effect between these analyst recommendation \({rec}_{i,t}\) and investor sentiment \({sen}_{j,t}\) in the following conditional form. We use the expected (i.e., average) value form for this as below.

We then find the expected stock return from the analyst’s recommendation conditional on the investor sentiment by multiplying Eq. (8) by the corresponding stock return (\({r}_{t})\).

For example, when investigating an analyst upgrade recommendation with positive investors sentiment at time t = 2, the following Eq. (10) expresses this case.

Then the corresponding expected stock return can be calculated by multiplying Eq. (10) by the stock return at time t = 2.

However, this analysis in this current from suffers from a look-ahead bias as the investor sentiment in the current quarter would only be available in the following quarter. To avoid this bias, we assume that the best proxy for the current quarters’ sentiment value is the previous quarters sentiment value (which is a known figure in the current quarter) thus implicitly assuming the investor sentiment process is a pure martingale.Footnote 3

4 Data and sample selection

In the financial market, stock recommendations issued by different brokerage houses and investment firms may take different forms. Generally, based on their independent analysis and predictions on the covered firms and companies, sell-side analysts would usually issue one of the following statements: 1. strong buy; 2. buy; 3. hold/neutral; 4. sell and 5. strong sell.Footnote 4

Our sample comprises 50 actively traded constituent stocks in the Hong Kong stock market. The Hang Seng Index is the free-adjusted market capitalization-weighted stock market index in Hong Kong which serves as the main indicator of the overall market performance of the local stock market. Although the constituent stocks of the index have been regularly reclassified, our analysis focuses on the top 26 major stocks in terms of index weighting which covers more than 80% of market capitalization of the Hang Seng Index.

The sample period is defined as the period between the January 1, 2009 and the May 1, 2014 when the market experienced significant waves in trading. All sample recommendations of those 26 stocks are selected using Bloomberg. Companies that are listed within the sample period are considered to be stocks that have proven to be actively traded with significant market capitalization and turnover. In addition, all stocks have been covered by at least one analyst throughout the whole sample period. Delisted firms are excluded from the sample.

For those 26 target stocks, a total of 1751 recommendations from 402 analysts have been obtained within the sample period, consisting of 884 recommendation upgrades and 867 recommendation downgrades. Details of the data are shown in Table 1. However, in order to ensure consistency in the comparison of the effects of different stock recommendations, we exclude all recommendations that were released on weekends or holidays.

To derive the conditional probability statements based on the investor sentiment we use the J.P. Morgan Hong Kong Investor Confidence Index which is a survey-based index reflecting the investors’ sentiment over the next six months. Over 500 investors aged between 30 and 60 participate in the survey and have a minimum of HK$100,000 in liquid assets and at least 5 years of continuous investment experience.

The J.P. Morgan Investor Confidence Index (JPMICI) score is derived by asking survey respondents six questions to assess the confidence of investors about (Q1) the Hang Seng Index, (Q2) HK economic environment, (Q3) HK investment environment and sentiment, (Q4) global economic environment, (Q5) the possibility of personal asset appreciation, and (Q6) the possibility of increasing their investment. These six questions form the sub-indices of the J.P. Morgan Investor Confidence Index. The index and all sub-indices have a range between 0 and 200. A number greater than 100 represents a positive outlook and vice versa. The Index is designed to reflect local investor sentiment towards the Hong Kong market over the next 6 months following its last date of publication. It is fair to assume that the JPMICI index is a representation of investor confidence in the HK market. As such, the semi-annual changes of the index value will reflect the perceived changes in investor sentiment. We have attached associated probability values of these changes in order to facilitate a richer analysis using a Bayesian framework. Assessing changes through probability values within a Bayesian framework has been practiced in the finance literature before (see Beaver 1966, 1968). We are certainly not the first to work with sentiment indices (see Huang et al. 2015; Lee et al. 2002, where the authors use the Baker and Wurgler 2006 Index). However, the Baker and Wurgler (2006) Index does not cover Hong Kong during our period of interest, so we opted to use the JPMICI Index.

5 Empirical results

5.1 Recommendation upgrades

Sell-side analysts upgrade their covered stocks when they predict that the stock prices are going to rise in the short-run and/or medium-run, which may result in significant changes in stock prices. Table 2 presents the results of the average abnormal returns (AAR) for each day (from t = − 5 through t = + 10) with the event day occurring at t = 0. The findings show that the average abnormal returns of the stocks from 1 day before through 2 days after the analysts’ upgrades (t = − 1 to t = + 2) become positive and are highly statistically significant at the 1% level. The abnormal return reaches a maximum of 0.41% on the release day of the recommendation upgrade.

In addition, the statistically significant positive abnormal return is sustained for 3 days after the release day and the abnormal return remains at 0.9%. However, from day 4 onwards the AAR becomes statistically insignificantFootnote 5 as all new information has been incorporated. The empirical results show that recommendation upgrades by analysts deliver substantial information to market participants in the Hong Kong market and have positive impact on the stocks with the effects lasting for a few days. Yet, the returns are indeed very small: AAR0 to AAR10 adds up to just under 1% and investors are not likely to gain profits after accounting for transaction costs. These results are consistent with Liu et al. (1990), but the overall effects seem to be smaller in this study.

Also, similar to the observation of Liu et al. (1990), our results in the table show that the abnormal returns on the day before the release of security upgrades (0.1528%) are positive and statistically significant, although small. This may be due to the leakage of private information from analysts to clients. This implies that the recommendation upgrades deliver information that is swiftly reflected in stock prices within a short period of time, even if investors are unable to make trading profits after accounting for transaction costs.

5.2 Recommendation downgrades

Table 3 shows the results of the average abnormal returns (AAR) for each day (from t = − 5 through t = + 10) surrounding recommendation downgrades (t = 0). Although the AARs become negative from the day before the announcement onwards, they only start becoming statistically significant on the announcement day. In other words, no evidence of significant information leakage or pre-trading is found based on the sample considered. Our finding is somewhat different to Liu et al. (1990) who show that the AARs just preceding the sell recommendations were significantly negative due to advance trading by investors based on speculation, or prior knowledge about the contents of the financial column.

The AAR reaches a minimum of − 0.57% on the release day of recommendation downgrades and is highly significant. On the next day (t = 1), the AARs remain negative at about − 0.42% and significant at the 1% level. The returns remain negative from day 3 through day 10 but are statistically significant only on day 3 (at the 5% level) and day 8 (at the 10% level). AAR0 to AAR10 adds up to − 1.535%. These results show that analysts’ downgrades have a relatively larger impact on the stock prices surrounding the announcement day, suggesting that downgrades deliver more significant information to the stock market than upgrades. Also, negative information seems to require relatively less time (about 2 days) to be incorporated and reflected in the stock price (Liu et al. 1990). And the market quickly reflects the information on the stock prices without price reversal in the short run (Chan and Fong 1996).

5.3 Initiation of coverage-buy

Analysts would initiate stock coverage for many reasons at different time points and issue positive (e.g. buy; outperform; outweigh etc.) or negative (sell; strong sell; underperform) recommendations along with the new coverage. We analyze the whole sample period and determine their abnormal impact on the stock market.

An initiation of coverage is the first research report produced by a stock analyst about a particular stock. Wang (2020) provides evidence that analysts gather and produce additional private information to the market and that their information reduces investors' uncertainty toward upcoming earnings announcements. Brokerage houses or investment bank analysts cover new stocks for various reasons. For instance, they may believe that the new coverage can generate trading revenues in the security. Also, the corporate finance departments of the brokerage houses may ask for stock coverage as they believe these will encourage the underwriting business (Irvine 2003). Moreover, in some cases, analysts will cover new stocks for their important clients when they realize that the clients have substantial holdings in some companies. Therefore, the analysts provide support and a flow of information to their clients (Irvine 2003).

There are 449 New Buy InitiationsFootnote 6 issued by analysts for the 26 constituent stocks of the Hang Seng Index within the sample period. Table 4 presents the results of the average abnormal returns (AAR) for each day (from t = − 5 through t = + 10) around the release day of a New Buy Initiation (t = 0) with the corresponding t-statistics. Interestingly, the impact of New Buy initiations on stock prices is different from that of recommendation upgrades. The results show that only on the day prior to the announcement event, the AAR is slightly positive (0.137%) and statistically significant (t-statistic of 2.29). During the release day, the AAR0 is at 0.0822% and insignificant. The AAR remains insignificant except for the fourth and seventh day after the announcement.

In general, the announcement of new buy coverage has insignificant impact on the stock price around the release day (t = 0). This implies that the announcement of new buy coverage by sell-side analysts delivers relatively insignificant information, while investors are not able to gain any significant abnormal return by trading the covered stock around the announcement day. These results suggest that the information content of analysts’ new buy coverage initiations is not as important as recommendations upgrades since the return of recommendation upgrades on the event day was 0.41% (and significant at the 1% level) compared to an insignificant figure of 0.082% for new buy coverage.

5.4 Initiation of coverage-sell

Our sample contains 55 new sell initiations issued by analysts for the 26 constituent stocks of the Hang Seng Index within the sample period. The number of new sell initiations is therefore much lower than the 449 new buy initiations in our sample; this distribution conforms to the hypothesis that analysts are more likely to start covering equities which they view favorably. This is consistent with the observations of Irvine (2003): analysts’ initiations are more likely to be strong buy/buy and less likely to be hold/sell. By initiating coverage, analysts can then offer compelling stories about the covered stocks’ fundamental values, which will further generate trading in the securities.

Like the previous tables, Table 5 shows the average abnormal returns (AARs) of each day (from t = − 5 through t = + 10) surrounding the release day of New Sell initiations (t = 0). Interestingly, the abnormal returns before the announcement day are statistically insignificant. On the announcement day itself, the AAR is insignificant though negative (− 0.198%). However, on the first day after the announcement, the negative AAR (− 0.304%) becomes statistically significant at the 10% significance level. The AARs for the following days remain insignificant. These results are similar to Irvine (2003), who found that the 2-day abnormal return around sell initiations was − 0.32% and statistically insignificant.

Although anecdotal evidence suggests that new sell initiations may result in significantly negative abnormal returns since analysts do not view the stocks favorably, the AARs presented in Table 5 indicate that, as analysts announce new sell initiations, the stock prices do not drop significantly on the announcement day as predicted by the analysts. In other words, investors do not consider new sell initiations as containing significantly unfavorable new information content; and the initiations do not result in substantial negative abnormal returns on the announcement day. The AARs are significantly negative only on the day after the announcement (t = 1) while the AARs remain insignificant thereafter, although the insignificance of the abnormal returns may be partly due to the relatively small sample size for new sell initiations (Irvine 2003).

Our findings have indicated that recommendation upgrades and downgrades as well as new coverage initiations of sell-side analysts have differential impacts on the Hong Kong stock market. The results reveal that analysts’ recommendations convey substantial information to investors and result in significant abnormal returns consistent with the predictions of the analysts surrounding the announcement day. On the other hand, the market does not consider new coverage initiations as significant information-the initiations do not result in substantial positive or negative abnormal returns surrounding the announcement day.

5.5 Upgrades and downgrades during bullish and bearish phases

It is unlikely that the impact of analysts’ recommendations will be identical when the overall market is bullish as against bearish, since analysts may be highly influenced by the overall market conditions when making recommendation upgrades and downgrades. In particular, in the bullish period when investors expect security prices to rise in general and are optimistic about the future of the market, analysts may be more prone to upgrade securities considering the overall market sentiment. Yet, the recommendation may not be justified by the analysts’ earnings forecast for the covered firms (Bagnoli et al. 2009). On the other hand, in bearish periods when market sentiment is pessimistic, analysts may consider that most stocks are declining and factor in the general pessimistic sentiment into their stock analysis. As a result, one might expect the price impact of stock upgrades and downgrades to vary in different time phases. Therefore, to determine whether our earlier results for upgrades and downgrades are influenced by market conditions, we investigate the price impacts of recommendation upgrades and downgrades in bullish and bearish markets.

The bullish period ran from March 9, 2009 to November 8, 2010, the latter being the date of the Hong Kong stock market peak, while the bearish period commenced on November 9, 2010 and ended on January 1, 2012. Throughout the above bullish and bearish sample periods, there are 446 recommendation upgrades (not including 21 that are excluded as they were issued on non-trading days such as holidays and/or weekends) and 428 downgrades in total. There are 292 recommendation upgrades and 267 recommendation downgrades within the bullish phase, against 154 recommendation upgrades and 161 recommendation downgrades within the bearish phase.

5.5.1 Impact of recommendation upgrades during the bullish and bearish phases

The second and fourth columns of Table 6 present the Average Abnormal Returns (AAR) based on MM residuals for recommendation upgrades during the bullish and bearish phases. Like previous results, recommendation upgrades produce significantly positive returns on the announcement day (t = 0) in both the bullish and the bearish phases. Yet, the AAR0 during the bullish phase (0.496%) is slightly higher than that during the bearish phase (0.228%). In other words, in a bullish environment, analyst’s upgrades result in higher abnormal returns on the announcement day perhaps because of the prevailing optimistic environment. In a bearish environment however, investors may be less likely to purchase stocks at the first sight of the information because the overall market sentiment is pessimistic, resulting in relatively lower abnormal returns.

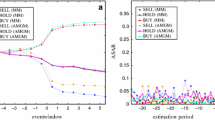

Moreover, the AARs on the first day in both phases are still significantly positive, which suggests that the high demand in upgraded stocks still exists on the day after the announcement. However, the AARs remain significantly positive (up until day 4) only during the bearish phase, but not in the bullish phase in which the information is quickly reflected in the security prices and AAR becomes insignificant from day 2 onwards. Therefore, investors in a bearish environment may require more time to reflect on the upgrades and observe market movements before taking action to purchase the upgraded stocks, such that the resulting positive price effects are staggered for a few days after the stock upgrades. In fact, when one compares the CAR plots based on MM residuals for both bullish and bearish phases (see Fig. 1), it becomes even more clear that the positive price impact for upgrades is felt immediately after the announcement, with partial reversal of some of the gains as one approaches t = 10. On the other hand, in the bearish phase, although there is a smaller price impact just after the announcement, the price increases continue as one approaches the end of the event window. The price adjustment following the upgrades is more gradual in the bearish scenario.

Cumulative abnormal returns (CAR) using market model (MM) during the bullish (03-09-2009 ~ 11-08-2010) and the bearish (11-09-2010 ~ 01-01-2012) phases with upgrades and downgrades surrounding the release day

5.5.2 Impact of recommendation downgrades during the bullish and bearish phases

Columns two and four in Table 7 show the Average Abnormal Returns (AAR) based on MM residuals for recommendation downgrades for the bullish and bearish phases. The results reveal that the stock market reacts significantly to the analysts’ downgrades in both bullish and bearish phases. On the day of release (t = 0), both AARs are significantly negative, with the AAR0 for the bearish phase (− 0.824%) being much lower than that during the bullish period (− 0.372%). The negative abnormal returns persist and are significant for at least 3 days after the downgrades for both phases. When one compares the CAR plots based on MM residuals for both bullish and bearish phases (see Fig. 2), we find that the overall negative price impact is quite similar for both phases as one approaches t = 10. Thus, although the event day fall is bigger in bearish periods, the price falls in bullish periods are more spread out over the event window. The price adjustment following the downgrades is more gradual in the bullish scenario.

Cumulative abnormal returns (CAR) using Fama & French (FF) 3 Factor model during the bullish (03-09-2009 ~ 11-08-2010) and the bearish (11-09-2010 ~ 01-01-2012) phases with upgrades and downgrades surrounding the release day

5.5.3 Robustness tests based on the Fama & French 3 factor model

To check for robustness, we also estimated AARs using the Fama & French three factor model, and the results are contained in columns three and five of Tables 6 and 7. Overall, the results are quite consistent with those we have already reported based on MM residuals: Upgrade announcements are followed by price increases, while downgrade announcements are followed by price falls. For upgrades, the event-day returns are 0.31% and 0.02% in bullish and bearish periods, respectively, and statistically significant at the 5% level in the former case. The CAR plots based on the 3-factor residuals show that, between t = − 2 and t = 10, the overall price increase is around 0.64% in bullish periods and just under 0.5% in bearish periods. As was the case with MM residuals, the price adjustments following upgrades were slower in bearish periods. Turning to downgrades, the event day returns are 0.3% and − 0.55%, in bullish and bearish periods, respectively, with only the latter being statistically significant. In bullish periods, it would seem that the significant price declines came towards the end of the event window.

In bearish periods, the AARs remain negative and significant from AAR1 to AAR2, and AAR7 to AAR8. Overall, when FF residuals are used, the CAR plots for downgrades show that the price adjustment over the event window happens with a delay in bullish periods. This is again consistent with our findings based on MM residuals. And in bearish periods, the price decline for downgrades (i.e., between t − 2 and t = 10) is around − 1.7%. In bullish periods, it is just under − 2.4%.Footnote 7

5.6 Analyst recommendations conditioned on sentiment

We look at the whole period ranging from January 2009 to May 2014 to gauge the probability of an upgrade/downgrade/hold recommendation of an analyst on a given stock, conditional on the investor sentiment that prevailed in the previous quarter.

We apply our conditional binomial probability framework as in equation to get a better understanding of the possible influence of the investor sentiment at a given moment to a recommendation made by an analyst. We show the expected probability of the joint effect between rec and sen \(E[P\left(rec|sen\right)]\) and the resulting effect on the average stock return r from our expected value \(r\times E[P\left(rec|sen\right)]\). The following table shows the effects of investor sentiment (sen), analyst recommendations (rec), and the corresponding average stock returns (r) on a quarterly basis. We also show the expected probability of the joint effect between rec and sen \(E[P\left(rec|sen\right)]\) and the resulting effect on the average stock return r from our expected value \(r\times E[P\left(rec|sen\right)]\). We show this including and excluding look-ahead bias in Panel A and B, respectively. In Panel C, we use the Welch’s two sample t-test to show how the average \(E[P\left(rec|sen\right)]\) or \(r\times E[P\left(rec|sen\right)]\) becomes significantly different between positive and negative sentiments, and with and without look-ahead bias. We express the positive (negative) sentiment including and excluding look-ahead bias as Positivebias (Negativebias) and Positiveno bias(Negativeno bias), respectively. The Cohen’s d provides the effect size that, as a rule of thumb, if the absolute value is greater than 0.8 and closer to 2, the corresponding Welch’s t-test result between two sample groups is valid although the sample size is small. Panel D shows the descriptions of the variables used in this table.

We see an emergence of a clear pattern in both panel A and B from Table 8. In general, we find that the positive investor sentiment change corresponds with changes of analyst recommendations. We find the following stylized results interpreted from Panel A and B of Table 8.

5.7 In the presence of look ahead bias

Whilst the probability on average of ending up with an upgrade status (irrespective of start status) is very similar whether one was in a positive or a negative sentiment the expected return of all corresponding moves is an order of magnitude higher when one starts with a positive sentiment as opposed to a negative one.

5.8 When there is no look ahead bias

Both the probability on average of ending up with an upgrade status (irrespective of start status) is higher if one was in a positive as opposed to a negative sentiment and the expected return of all corresponding moves is an order of magnitude higher when one starts with a positive sentiment as opposed to a negative one.

As shown in panel C when one considers the expected returns to the investors, we see that the positive sentiment effect tends to dominate the negative one across different types of permutations. i.e. In the presence of look ahead bias the differential returns when one is in a positive sentiment (as opposed to a negative one) is statistically significant at 1%. Furthermore, when one considers the effect between ‘with’ and ‘without’ look ahead bias the differential returns when one is in a positive sentiment (as opposed to a negative one) is also statistically significant at 1%. We also find that the differential returns between the two corresponding positive sentiments with and without look ahead bias also statistically significant at 1%. Our results have important implications to capital market investors as one could argue that these investors would be more concerned about their expected returns.

These results align with Bagnoli et al. (2009) and Corredor et al.’s (2013) arguments that the analysts are more heavily affected and biased by positive investor sentiment when issuing favorable stock recommendations as we also find the positive investor sentiment effect from all types of stock recommendations in Hong Kong financial markets. As we also find positive expected stock returns under positive investor sentiment contingent on various analyst recommendations consistent with Barber et al. (2001) and Womack (1996). Thus, the investor market sentiment is still a critical factor affecting not only the analyst recommendations but also the corresponding stock returns in the Hong Kong financial markets.

6 Conclusions and implications of the study

This study examines the short-term price impact of stock recommendations issued by sell-side analysts on 26 major constituent stocks of the Hang Seng Index, the market benchmark monitoring daily movement of the largest companies listed on the Hong Kong Stocks Exchange. Numerous academic studies show that stock analysts play an important role in the stock market in which their recommendations deliver substantial information to the investors, resulting in different levels of price impact.

We analyze the Hong Kong stock market reactions from analysts’ stock recommendations (1696 upgrades and downgrades, and 504 initiation coverages) and consider the ongoing market sentiments. We find that the analysts’ upgrade recommendations result in significantly positive market reactions around the announcement day since these deliver newly favorable information to the investors. Similarly, we also find significantly negative market reactions to analysts’ downgrade recommendations, which shows even larger reactions in absolute figure compared to the market reactions to analysts’ upgrade recommendations. Therefore, the investors are more sensitive to losses than to gains consistent with prospect theory by Kahneman and Tversky (1979). On the other hand, the market reactions to initiation coverage with buy and sell recommendations are insignificant since these do not deliver enough information to the market or the market may reflect all this related information too quickly, contrary to Branson et al. (1998) and Irvine (2003). Then we assess the short-term impact of analysts’ recommendations under two bullish and bearish market conditions. We find that the investors react more optimistically to upgrade recommendations during bullish phase but react even more pessimistically to downgrades during bearish phase confirming more loss sensitive investors’ behaviors.

We apply the conditional probability framework to the analyst recommendations conditioned on the investor sentiment and estimate the corresponding expected stock returns. Our finding shows that with look ahead bias the differential returns when one is in a positive sentiment as opposed to a negative one, is significant, and that the differential returns between the two corresponding positive sentiments with and without look ahead bias also statistically significant. Our findings have implications to capital market participants as they suggest that exploitable trading strategies can be developed for the Hong Kong market with the information of the market sentiment in the past.

This study provides evidence in support to the fact that analysts’ recommendation upgrades and downgrades deliver permanent and significant information to the Hong Kong stock market. However, analysts’ initiation coverages convey little information and bring about limited impact to the stock market. In addition, analysts’ upgrades and downgrades result in significant price impact to different extents in the bullish and the bearish phases.

Notes

The bullish phase is taken from March 9, 2009 to November 8, 2010 which shows continuous decrease in GDP growth, while the bearish phase is runs from November 9, 2010 to January 1, 2012 showing continuous increase in GDP growth in Hong Kong. Studies have evidenced the existence of a strong correlation between output growth and stock returns in emerging and advanced economies. See Rangvid (2006) and Mauro (2003).

We also checked for robustness using two approaches. We used an estimation window that was 25% shorter than 100 days and found that our results for both the Fama and French 3-factor model and Market Model remained qualitatively the same. Second, we re-estimated our results using a market-adjusted returns model, as it does not involve any estimation period at all. Again, our results were very similar to our Fama and French 3-factor results.

The stochastic process X = {Xt} t ≥ 0 is called a martingale, if (1) E(|Xt |) < ∞ for all t ≥ 0; and (2) E(Xt |Xs) = Xs for all t ≥ s ≥ 0.

The classification is similar to the records of the five − point scale classification of the First Call database (see Barber et al. 2007).

In their results, Chan and Fong (1996) observed that the AR remained insignificant from day 2 through day 25.

Buy recommendations include all positive ratings issued by analysts including long term buy, accumulate, strong buy, outperform and overweight. Six recommendations are excluded as they were issued on non-trading days such as holidays and/or weekends.

We also investigated the effect of the Euro zone crisis on Hong Kong stock returns by running an overall Fama and French 3-factor regression for the Hong Kong market, with a Euro zone crisis dummy variable to assess the impact of the Euro zone crisis on Hong Kong stock returns. The dummy variable took the value of one from October 19, 2009 to January 31, 2012, inclusive (see Ahmad et al. 2013). We found that the dummy variable was not economically or statistically significant; the Eurozone crisis reduced Hong Kong Stock returns by − 0.000005%.

References

Aggarwal R, Mishra D, Wilson C (2018) Analyst recommendations and the implied cost of equity. Rev Quant Financ Acc 50(3):717–743

Agrawal A, Chen M (2008) Do analyst conflicts matter? Evidence from stock recommendations. J Law Econ 51(3):503–537

Ahmad W, Sehgal S, Bhanumurthy NR (2013) Eurozone crisis and BRIICKS stock markets: contagion or market interdependence? Econ Model 33:209–225

Amiram D, Owens E, Rozenbaum O (2016) Do information releases increase or decrease information asymmetry? New evidence from analyst forecast announcements. J Account Econ 62(1):121–138

Ang A, Ng H-S, Quah P, Tan H-C (1998) An analysis of the performance of buy recommendations of stock-broking firms in Singapore. Asia Pac J Account 5(2):199–221

Arif S, De George E (2020) The dark side of low financial reporting frequency: investors’ reliance on alternative sources of earnings news and excessive information spillovers. Account Rev 95(6):23–49

Bagnoli M, Clement M, Crawley M, Watts S (2009) The profitability of analysts’ stock recommendations: what role does investor sentiment play? https://ssrn.com/abstract=1430617

Baker M, Wurgler J (2006) Investor sentiment and the cross-section of returns. J Finance 61:1645–1680

Baker M, Wurgler J (2007) Investor sentiment in the stock market. J Econ Perspect 21(2):129–151

Barber B, Lehavy R, McNichols M, Trueman B (2001) Can investors profit from the prophets? Security analyst recommendations and stock returns. J Financ 56(2):531–563

Barber B, Lehavy R, Trueman B (2007) Comparing the stock recommendation performance of investment banks and independent research firms. J Financ Econ 85(2):490–517

Barber B, Lehavy R, Trueman B (2010) Ratings changes, ratings levels, and the predictive value of analysts’ recommendations. Financ Manag 39(2):533–553

Beaver WH (1966) Financial ratios as predictors of failure. J Account Res 4:71–111

Beaver WH (1968) Market prices, financial ratios and the prediction of failure. J Account Res 6(2):179–192

Branson B, Guffey D, Pagach D (1998) Information conveyed in announcements of analyst coverage. Contemp Account Res 15(2):119–143

Brown G, Cliff M (2004) Investor sentiment and the near−term stock market. J Empir Financ 11(1):1–27

Chan S, Fong W (1996) Reactions of the Hong Kong Stock Market to the publication of second−hand analyst’ recommendation. J Bus Financ Acc 23(8):1121–1140

Chan S, Fong W (2004) Individual investors’ sentiment and temporary stock price pressure. J Bus Financ Acc 31(5–6):823–836

Chan J, Lin S, Yu Y, Zhao W (2018) Analysts’ stock ownership and stock recommendations. J Account Econ 66(2–3):476–498

Chen X, Cheng Q (2006) Institutional holdings and analysts’ stock recommendations. J Acc Audit Financ 21(4):399–440

Chen S, Matsumoto DA (2006) Favorable versus unfavorable recommendations: The impact on analyst access to management-provided information. J Account Res 44(4):657–689

Cheng JW, Fan DK, So RW (2003) On the performance of naïve, analyst and composite earnings forecasts: evidence from Hong Kong. J Int Financ Manag Acc 14(2):146–165

Corredor P, Ferrer E, Santamaria R (2013) Value of analysts’ consensus recommendations and investor sentiment. J Behav Financ 14(3):213–229

Du Q, Yu F, Yu X (2017) Cultural proximity and the processing of financial information. J Financ Quant Anal 52(6):2703–2726

Firth M, Lin C, Liu P, Xuan Y (2013) The client is king: do mutual fund relationship bias analyst recommendations? J Account Res 51(1):165–200

Francis J, Soffer L (2006) The relative informativeness of analysts’ stock recommendations and earnings forecast revisions. J Account Res 35(2):193–211

Frijns B, Huynh TD (2018) Herding in analysts’ recommendations: the role of media. J Bank Finance 91:1–18

Green TC (2006) The value of client access to analyst recommendations. J Financ Quant Anal 41(1):1–24

He G, Ren HM, Taffler R (2020) The impact of corporate tax avoidance on analyst coverage and forecasts. Rev Quant Financ Acc 54(2):447–477

Hong Y, Huseynov F, Sardarli S, Zhang W (2020) Bank earnings management and analyst coverage: evidence from loan loss provisions. Rev Quant Financ Acc 55(1):29–54

Huang D, Jiang F, Tu J, Zhou G (2015) Investor sentiment aligned: A powerful predictor of stock returns. Rev Financ Stud 28(3):791–837

Irvine P (2003) The incremental impact of analyst initiation of coverage. J Corp Finan 9(4):431–451

Jegadeesh N, Kim W (2006) Value of analyst recommendations: International evidence. J Financ Mark 9(3):274–309

Kadan O, Michaely R, Moulton PC (2018) Speculating on private information: buy the rumor, sell the fact. J Financ Quant Anal 53(4):1509–1546

Kahneman D, Tversky A (1979) Prospect theory: an analysis of decision under risk. Econometrica 47(2):263–291

Kim K, Ryu D, Yang H (2019) Investor sentiment, stock returns, and analyst recommendation changes: the KOSPI stock market. Invest Anal J 48(2):89–101

Kudryavtsev A (2019) Effect of investor inattention on price drifts following analyst recommendation revisions. Int J Finance Econ 24(1):348–360

Lee WY, Jiang CX, Indro DC (2002) Stock market volatility, excess returns, and the role of investor sentiment. J Bank Finance 26(12):2277–2299

Lee C, Palmon D, Yezegel A (2018) The corporate social responsibility information environment: examining the value of financial analysts’ recommendations. J Bus Ethics 150(1):279–301

Li EX, Ramesh K, Shen M, Wu JS (2015) Do analyst stock recommendations piggyback on recent corporate news? An analysis of regular-hour and after-hours revisions. J Account Res 53(4):821–861

Li F, Lin C, Lin T (2020) Salient anchor and analyst recommendation downgrade. https://ssrn.com/abstract=2517238

Lin HW, McNichols MF (1998) Underwriting relationships, analysts’ earnings forecasts and investment recommendations. J Account Econ 25(1):101–127

Liu P, Smith S, Syed A (1990) Stock price reactions to the Wall Street Journal’s securities recommendations. J Financ Quant Anal 25(3):399–410

Loh R (2010) Investor inattention and the underreaction to stock recommendations. Financ Manag 39(3):1223–1252

Mauro P (2003) Stock returns and output growth in emerging and advanced economies. J Dev Econ 71(1):129–153

Michaely R, Womack K (1999) Conflict of interest and the credibility of underwriter analyst recommendations. Rev Financ Stud 12(4):653–686

Michaely R, Womack K (2005) Brokerage recommendations: stylized characteristics, market responses, and biases. Adv Behav Finance II:389–422

Moshirian F, Ng D, Wu E (2009) The value of stock analysts’ recommendations: evidence from emerging markets. Int Rev Financ Anal 18(1–2):74–83

Papakroni J (2018) The dispersion anomaly and analyst recommendations. Rev Quant Financ Acc 50(3):861–896

Petaibanlue J, Walker M, Lee E (2015) When did analyst forecast accuracy benefit from increased cross-border comparability following IFRS adoption in the EU? Int Rev Financ Anal 42:278–291

Pratt, T. (1993). Wall Street’s four−letter word. Investment Dealers Digest. March. pp. 18−22.

Rangvid J (2006) Output and expected returns. J Financ Econ 81(3):595–624

Rubanov D, Nnadi M (2018) The impact of international financial reporting standards on fund performance. Account Res J 31(1):102–120

Ryan P, Taffler R (2006) Do brokerage houses add value? The market impact of UK sell−side analyst recommendation changes. Br Account Rev 38(4):371–386

Su C, Zhang H, Bangassa K, Joseph NL (2019) On the investment value of sell-side analyst recommendation revisions in the UK. Rev Quant Financ Acc 53(1):257–293

Wang J (2020) Does analyst forecast dispersion represent investors’ perceived uncertainty toward earnings? Rev Acc Financ 19(3):289–312

Womack K (1996) Do brokerage analysts’ recommendations have investment value? J Financ 51(1):137–167

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Choudhry, T., Dissanaike, G., Jayasekera, R. et al. Loss sensitive investors and positively biased analysts in Hong Kong stock market. Rev Quant Finan Acc 57, 1345–1371 (2021). https://doi.org/10.1007/s11156-021-00980-7

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-021-00980-7