Abstract

This study investigates the influences of companies’ cultural diversity on International Financial Reporting Standards (IFRS) adoption in Nigeria. The diverse response to IFRS adoption is a phenomenon that necessitates further investigation to understand the reasons some companies adopt IFRS while others do not. Previous studies have investigated preparers of financial statements’ adoption of IFRS and there is a dearth of research on the role of cultural difference on IFRS adoption. However, little has been explored to understand the impacts of cultural variables on IFRS adoption. Using a self-administered survey questionnaire and logistic regression, this study identifies that financial statement preparers’ levels of professionalism, transparency, flexibility, secrecy, uniformity and the statutory control dimensions of cultural factors impact IFRS adoption at different magnitudes. The study notes that IFRS adoption can only be successful when accountants develop the relevant technical expertise in IFRS prior to implementation. This includes practical training in IFRS requirements, accounting assets and liabilities valuation, recognition of income or liabilities and disclosure of economic events before and after the reporting period consistent with IFRS 10.

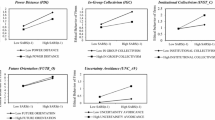

Source: Gray (1988, p. 7)

Similar content being viewed by others

References

Abdel-Kader M, Luther R (2008) The impact of firm characteristics on management accounting practices: a UK-based empirical analysis. Br Acc Rev 40(1):2–27

Aggarwal R, Goodell JW (2014) National cultural dimensions in finance and accounting scholarship: an important gap in the literatures? J Behav Exp Finance 1:1–12

Agostino M, Drago D, Silipo DB (2011) The value relevance of IFRS in the European banking industry. Rev Quant Finance Acc 36(3):437–457

Alexander D, Alon A (2017) Layering of IFRS and dual institutionality of accounting standards in Belarus. Acc Eur 14(3):261–278

Alexander D, Adamo S, Di Pietra R, Fasiello R (2017) The history and tradition of accounting in Italy. Taylor & Francis, Abingdon

Alon A, Dwyer PD (2014) Early adoption of IFRS as a strategic response to transnational and local influences. Int J Acc 49(3):348–370

Amenkhienan FE (1986) Accounting in Developing Countries: a framework for standard setting. UMI Research Press, San Francisco

Anderson DR, Sweeney DJ, Williams TA, Camm JD, Cochran JJ (2014) Essentials of statistics for business and economics. Cengage Learning, Boston

Bakre OM, Lauwo S (2016) Privatisation and accountability in a “crony capitalist” Nigerian state. Crit Perspect Acc 39:45–58

Ball R (2006) International financial reporting standards (IFRS): pros and cons for investors. Acc Bus Res 36(sup1):5–27

Barde IM (2009) An evaluation of accounting information disclosure in the nigerian oil marketing industry. (Ph.D.) Bayero University, Nigeria

Barlev B, Citron DB, Haddad JR (2017) Who is afraid of transparency? Acc Public Interest 17(1):60–83

Barth ME, Landsman WR, Lang MH (2008) International accounting standards and accounting quality. J Acc Res 46(3):467–498

Blecher C (2011) The influence of uncertainty on the standard-setting decision between fair value and historical cost accounting under asymmetric information. Rev Quant Finance Acc 53(1):47–72

Borker DR (2013a) Accounting and cultural values: IFRS in 3G economies. Int Bus Econ Res J 12(6):671

Borker DR (2013b) Is there a favorable cultural profile for IFRS?: an examination and extension of Gray’s accounting value hypotheses. Int Bus Econ Res J (IBER) 12(2):167–178

Borker DR (2016) Global management accounting principles and the worldwide proliferation of IFRS. Bus Manag Rev 7(3):258

Braam G, Peeters R (2018) Corporate sustainability performance and assurance on sustainability reports: diffusion of accounting practices in the realm of sustainable development. Corp Soc Responsib Environ Manag 25(2):164–181

Cannizzaro AP, Weiner RJ (2015) Multinational investment and voluntary disclosure: project-level evidence from the petroleum industry. Acc Organ Soc 42:32–47

Chimobi OP (2016) Government expenditure and national income: a causality test for Nigeria. Eur J Econ Polit Stud 2(2):1–11

Clements CE, Neill JD, Stovall OS (2010) Cultural diversity, country size, and the IFRS adoption decision. J Appl Bus Res (JABR) 26(2):115–126. https://doi.org/10.19030/jabr.v26i2.288

d’Arcy A, Tarca A (2018) Reviewing IFRS goodwill accounting research: implementation effects and cross-country differences. Int J Acc 53(3):203–226

De George ET, Ferguson CB, Spear NA (2012) How much does IFRS cost? IFRS adoption and audit fees. Acc Rev 88(2):429–462

Deegan C (2013) Financial accounting theory. McGraw-Hill Education Australia, Sydney

Deephouse DL, Bundy J, Tost LP, Suchman MC (2017) Organizational legitimacy: six key questions. The SAGE handbook of organizational institutionalism, pp 27–54

Doupnik T, Perera H (2009) International accounting, 2e. McGra-Hill International, New York

Dye RA, Verrecchia RE (1995) Discretion vs. uniformity: choices among GAAP. Acc Rev 70:389–415

Elbannan MA (2011) Accounting and stock market effects of international accounting standards adoption in an emerging economy. Rev Quant Finance Acc 36(2):207–245

Faraj S, Firjani E (2014) Challenges facing IASs/IFRS implementation by Libyan listed companies. Univ J Acc Finance 2(3):57–63

Fidanza B (2018) The decision to delist: International empirical evidence. In: The decision to delist from the stock market. Palgrave Macmillan, Cham, pp 117–155

Frestad D (2018) Managing earnings risk under SFAS 133/IAS 39: the case of cash flow hedges. Rev Quant Finance Acc 51(1):159–197

Gordon EA, Henry E, Jorgensen BN, Linthicum CL (2017) Flexibility in cash-flow classification under IFRS: determinants and consequences. Rev Acc Stud 22(2):839–872

Gray SJ (1988) Towards a theory of cultural influence on the development of accounting systems internationally. Abacus 24(1):1–15

Hann RN, Lu YY, Subramanyam K (2007) Uniformity versus flexibility: evidence from pricing of the pension obligation. Acc Rev 82(1):107–137

Hofstede GH (1984) Culture’s consequences: international differences in work-related values, vol 5. Sage, Thousands Oaks

Hoftstede G (1980) Culture’s consequences: Nueva York. Sage, Thousands Oaks

Hope O-K, Kang T, Thomas W, Yoo YK (2008) Culture and auditor choice: a test of the secrecy hypothesis. J Account Public Policy 27(5):357–373

Houqe MN, Monem RM, Tareq M, van Zijl T (2016) Secrecy and the impact of mandatory IFRS adoption on earnings quality in Europe. Pac-Basin Finance J 40:476–490

International Monetary Fund (2013) Nigeria: Publication of financial sector assessment program documentation detailed assessment of implementation of IOSCO objectives and principles of securities regulation. Retrieved October, 2013, from http://www.imf.org/external/pubs/ft/scr/2013/cr13144.pdf

Iyoha F, Oyerinde D (2010) Accounting infrastructure and accountability in the management of public expenditure in developing countries: a focus on Nigeria. Crit Perspect Acc 21(5):361–373

Kaplan R (2012) Building and managing E-book collections: a how-to-do-it manual for librarians. American Library Association, Chicago

Khalil M, Simon J (2014) Efficient contracting, earnings smoothing and managerial accounting discretion. J Appl Acc Res 15(1):100–123

Kim J-B, Shi H, Zhou J (2014) International Financial Reporting Standards, institutional infrastructures, and implied cost of equity capital around the world. Rev Quant Finance Acc 42(3):469–507

Luo GY (2016) Accounting conservatism, market liquidity and informativeness of asset price: implications on mark to market accounting. J Appl Finance Bank 3(1):177–190

Madawaki A (2012) Adoption of international financial reporting standards in developing countries: the case of Nigeria. Int J Bus Manag 7(3):p152

Mulawarman A (2012) Accounting in the madness vortex of neoliberal IFRS-IPSAS: a criticism of IAS 41 and IPSAS 27 on agriculture. Paper presented at the international conference if critical accounting

Nair RD, Frank WG (1983) The impact of disclosure and measurement practices on international accounting classifications. In: Gray SJ (ed) International accounting and transnational decisions. Elsevier, Amsterdam, pp 70–94

Neel M (2017) Accounting comparability and economic outcomes of mandatory IFRS adoption. Contemp Acc Res 34(1):658–690

Nigeria Stock Exchange (2013) The NSE delists companies from daily official list. Retrieved October 13, 2013, from http://www.nse.com.ng/MarketNews/Press%20Releases/NSE%20Delists

Nobes C (2008) Accounting classification in the IFRS era. Austr Acc Rev 18:191–198

Nobes C, Paker R (2012) Comparactive international accounting, 12th edn. Pearson, Cambridge

Nobes C, Parker RRH (2008) Comparative international accounting. Pearson Education, Cambridge

Nurunnabi M (2016) The role of the state and accounting transparency: IFRS implementation in developing countries. Routledge, Abingdon

Odia J, Ogiedu K (2013) IFRS adoption: issues, challenges and lessons for Nigeria and other adopters. Mediterr J Soc Sci 4(3):389

Osemeke L, Adegbite E (2016) Regulatory multiplicity and conflict: towards a combined code on corporate governance in Nigeria. J Bus Ethics 133(3):431–451

Oyerogba EO, Alade ME, Idode PE, Oluyinka IO (2017) The impact of board oversight functions on the performance of listed companies in Nigeria. Acc Manag Inf Syst 16(3):268–296

Ozu C, Nakamura M, Nagata K, Gray SJ (2018) Transitioning to IFRS in Japan: corporate perceptions of costs and benefits. Austr Acc Rev 28(1):4–13

Perera H, Cummings L, Chua F (2012) Cultural relativity of accounting professionalism: evidence from New Zealand and Samoa. Adv Acc 28(1):138–146

Perumpral SE, Evans M, Agarwal S, Amenkhienan F (2009) The evolution of Indian accounting standards: its history and current status with regard to international financial reporting standards. Adv Acc 25(1):106–111

Ray K (2017) One size fits all? Costs and benefits of uniform accounting standards. J Int Acc Res 17:1–23

Salewski M, Zülch H (2015) Discretion in the accounting for defined benefit obligations–an empirical analysis of German IFRS statements. J Pension Econ Finance 14(03):266–292

Sanusi LS (2010) Growth prospects for the Nigerian economy. Convocation lecture delivered at the Igbinedion University, Okada, Edo State, Nigeria

Schipper K (2003) Principles-based accounting standards. Acc Horiz 17(1):61–72

Schmidt M (2017) Aligning financial and management accounting policies: what drives integration?–Empirical evidence from German IFRS 8 segment reports. In: Malina MA (ed) Advances in management accounting. Emerald Publishing Limited, Bingley, pp 155–189

Shiab M (2003) Financial consequences of IAS adoption: the case of Jordan. (Ph.D.) Newcastle University

Soares AM, Farhangmehr M, Shoham A (2007) Hofstede’s dimensions of culture in international marketing studies. J Bus Res 60(3):277–284

Souza FÊA, Botinha RA, Silva PR, Lemes S (2015) Comparability of accounting choices in future valuation of investment properties: an analysis of Brazilian and Portuguese listed companies. Revista Contabilidade & Finanças 26(68):154–166

Suchman MC (1995) Managing legitimacy: strategic and institutional approaches. Acad Manag Rev 20(3):571–610

Trimble M (2018) A reinvestigation into accounting quality following global IFRS adoption: evidence via earnings distributions. J Int Acc Audit Tax 33:18–39

Tsalavoutas I, Dionysiou D (2014) Value relevance of IFRS mandatory disclosure requirements. J Appl Acc Res 15(1):22–42

Uche CU (2002) Professional accounting development in Nigeria: threats from the inside and outside. Acc Organ Soc 27(4):471–496

Ugrin JC, Mason TW, Emley A (2017) Culture’s consequence: the relationship between income-increasing earnings management and IAS/IFRS adoption across cultures. Adv Acc 37:140–151

Vashishtha R (2014) The role of bank monitoring in borrowers׳ discretionary disclosure: evidence from covenant violations. J Acc Econ 57(2–3):176–195

Wallace RSO (1987) Disclosure of accounting information in developing countries: a case study of Nigeria. Exeter University, London

Ward CL, Lowe SK (2017) Cultural impact of international financial reporting standards on the comparability of financial statements. Int J Bus Acc Finance 11(1):46–56

Watts RL, Zimmerman J (1978) Towards a positive theory of the determination of accounting standards. Acc Rev 53(1):112–134

Watts RL, Zuo L (2016) Understanding practice and institutions: a historical perspective. Acc Horiz 30(3):409–423

Wijayana S, Gray SJ (2018) Institutional factors and earnings management in the Asia-Pacific: is IFRS adoption making a difference? Manag Int Rev 59:1–28

Zakari MA (2014) Challenges of international financial reporting standards (IFRS) adoption in Libya. Int J Acc Financ Rep ISSN: 2162-3082

Zeghal D, Lahmar Z (2018) The effect of culture on accounting conservatism during adoption of IFRS in the EU. Int J Acc Inf Manag 26(2):311–330

Acknowledgements

We would like to thank the students and computer centre operators who helped in administering the survey questionnaire in Lagos, Abuja and Benin City Nigeria. We also acknowledge all the research participants who completed the questionnaires.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Edeigba, J., Gan, C. & Amenkhienan, F. The influence of cultural diversity on the convergence of IFRS: evidence from Nigeria IFRS implementation. Rev Quant Finan Acc 55, 105–121 (2020). https://doi.org/10.1007/s11156-019-00837-0

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11156-019-00837-0