Abstract

We expand on the standard commercial mortgage default model and create a new model by looking beyond the usual factors of option value, insolvency, property type, region, originator type, state foreclosure laws and macroeconomic measures. The new model incorporates measures of local economic conditions, specifically MSA-level commercial property market conditions, county level unemployment, and local home price appreciation. We estimate our new model using a dataset containing the performance histories of over 30,000 CMBS loans that were originated between 1998 and 2012. We find that those local trait variables affect the default rate of CMBS loans significantly and provide improved explanatory power over the standard model. We further explore the impact of local home price measures by comparing the explanatory power of lagged and contemporaneous home price indexes, comparing the power of home price indexes at the state, county, and zip-code level, examining the interaction of home price indexes with commercial property type, looking at the impact of home price indexes over time, and at the impact of introducing local commercial land price indexes. We find that local residential house price-related measures provide a high quality and high frequency signal of local market conditions.

Similar content being viewed by others

Notes

For example, the widely used NCREIF NPI is only broken down to the four census regions.

Alaska and Hawaii are excluded from our analysis.

The CRE Finance Council, as the main trade association for the CMBS market, has developed the IRP as a consistent set of data reports to be completed by loan servicers and made available to the trustees on CMBS deals.

Before that date, a substantial portion of the CMBS loans were from non-performing Savings and Loan Companies who originated those loans with the intention of holding them in their portfolios, but later liquidate them through the Resolution Trust Company (RTC). Since1995, there has been a substantial increase in lending by banks and mortgage companies for the sole purpose of securitization.

We defined defeased loans as prepaid for the purpose of our analysis.

In our sample, 8.31 % of loans are prepaid (including defeasance).

We identified the original lender as either a commercial bank, investment bank, conduit lender, foreign bank, or insurance company.

Notice that the loan duration time τ is different from the calendar time t, which allows for the identification of the model.

The true option value should be captured by the value of the “expected” LTV, which depends greatly on the volatilities of state variables.

We also tested the yield slope and corporate credit spread in our model but found that they are highly correlated with the coincident index and add no additional explanatory power.

We measure the change in the real rent index provided by CBRE as the ratio from loan origination to the current period.

The absorption rate is defined as the ratio of spaces newly leased in a particular period over the sum of the amount of vacant space in the previous period and the amount of new space provided by buildings completed in that later period.

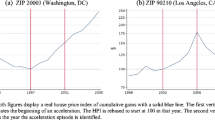

We define growth in the home price indexes as the log of the ratio of the index from the current period to origination.

Net absorption is defined as the number of units newly leased in that period minus the sum of newly constructed units delivered to the market and the newly available units that were not re-let upon the expiration of the previous lease.

In response to comments from an anonymous referee, we confirmed that the results from our base specification (model 1) and our final specification (model 5) are consistent when we include MSA-level fixed effects, or when we cluster the standard errors by MSA,

References

Ambrose, B., & Sanders, A. B. (2003). Commercial mortgage-backed securities: prepayment and default. Journal of Real Estate Finance and Economics, 26(2–3), 179–196.

An, X. (2007). Macroeconomic conditions, systematic risk factors, and the time series dynamics of commercial mortgage credit risk. University of Southern California Ph.D. Dissertation.

An, X., Deng, Y., & Gabriel, S. A. (2011). Asymmetric information, adverse selection and the pricing of CMBS. Journal of Financial Economics, 100(2), 304–325.

Archer, W. R., Elmer, P. J., Harrison, D. M., & Ling, D. C. (2002). Determinants of multifamily mortgage default. Real Estate Economics, 30(3), 445–473.

Black, L. K., Chu, C. S., Cohen, A. M., & Nichols, J. (2012). Differences across originators in CMBS loan underwriting. Journal of Financial Services Research, 42(1), 115–134.

Chen, J., & Deng, Y. (2013). Commercial mortgage workout strategy and conditional default probability: evidence from special serviced CMBS loans. forthcoming in Journal of Real Estate Finance and Economics, forthcoming.

Childs, P. D., Ott, S. H., & Riddiough, T. J. (1997). Bias in an empirical approach to determining bond and mortgage risk premiums. Journal of Real Estate Finance and Economics, 14(3), 263–282.

Ciochetti, B., & Vandell, K. A. (1999). The performance of commercial mortgages. Real Estate Economics, 27(1), 27–61.

Ciochetti, B. A., Deng, Y., Gao, B., & Yao, R. (2002). The Termination of lending relationships through prepayment and default in commercial mortgage markets: a proportional hazard approach with competing risks. Real Estate Economics, 30(4), 595–633.

Ciochetti, B. A., Deng, Y., Lee, G., Shilling, J., & Yao, R. (2003). A proportional hazards model of commercial mortgage default with originator bias. Journal of Real Estate Finance and Economics, 27(1), 5–23.

Clapp, J. C., Goldberg, G. M., Harding, J. P., & LaCour-Little, M. (2001). Movers and shuckers: interdependent prepayment decisions. Real Estate Economics, 29(3), 411–450.

Deng, Y., & Gabriel, S. (2006). Risk-based pricing and the enhancement of mortgage credit availability among underserved and higher credit-risk populations. Journal of Money, Credit, and Banking, 38(6), 1431–1460.

Deng, Y., Quigley, J. M., & Van Order, R. (1996). Mortgage default and low downpayment loans: the costs of public subsidy. Regional Science and Urban Economics, 26(3–4), 263–285.

Deng, Y., Quigley, J. M., & Van Order, R. (2000). Mortgage terminations, heterogeneity and the exercise of mortgage options. Econometrica, 68(2), 275–307.

Ghent, A.C., & Kudlyak, M. (2011). Recourse and residential mortgage default: evidence from U.S. States. Review of Financial Studies, forthcoming.

Goldberg, L., & Capone, C. A., Jr. (2002). A dynamic double-trigger model of multifamily mortgage default. Real Estate Economics, 30(1), 85–113.

Gyourko, J. (2009). Understanding commercial real estate: how different from housing is it? Journal of Portfolio Management, 35(5), 23–37.

Harding, J. P., Rosenblatt, E., & Yao, V. W. (2008). The contagion effect of foreclosed properties. Journal of Urban Economics, 66(3), 164–178.

Kau, J. B., & Keenan, D. C. (1995). An overview of the option-theoretic pricing of mortgages. Journal of Housing Research, 6(2), 217–244.

Kelly, A. (2009). Skin in the game: zero down payment mortgage default. Journal of Housing Research, 17(2), 75–99.

Nichols, J., Oliner, S., & Mulhall, M. (2013). Swings in commercial and residential land prices in the United States. Journal of Urban Economics, 73, 57–76.

Quigley, J. M., & Van Order, R. (1991). Defaults on mortgage obligations and capital requirements for U.S. savings institutions. Journal of Public Economics, 44, 353–369.

Quigley, J. M., & Van Order, R. (1995). Explicit tests of contingent claims models of mortgage default. Journal of Real Estate Finance and Economics, 1(2), 99–117.

Riddiough, T. J., & Wyatt, S. B. (1994). Wimp or tough guy: sequential default risk and signaling with mortgages. Journal of Real Estate Finance and Economics, 9, 299–321.

Seslen, T., & Wheaton, W. (2010). Contemporaneous loan stress and termination risk in the CMBS pool: how “ruthless” is default? Real Estate Economics, 38(2), 225–255.

Titman, S., & Torous, W. N. (1989). Valuing commercial mortgages: an empirical investigation of the contingent-claims approach to pricing risky debt. Journal of Finance, 44(2), 345–373.

Titman, S., & Tsyplakov, S. (2010). Originator performance, CMBS structures and yield spreads of commercial mortgages. Review of Financial Studies, forthcoming.

Vandell, K., Barnes, W., Hartzell, D., Kraft, D., & Wendt, W. (1993). Commercial mortgage defaults: proportional hazards estimations using individual loan histories. AREUEA Journal, 21(4), 451–480.

Yezer, A. M. J., Phillips, R. F., & Trost, R. P. (1994). Bias in estimates of discrimination and default in mortgage lending: the effects of simultaneity and self-selection. Journal of Real Estate Finance and Economics, 9, 197–215.

Yildirim, Y. (2008). Estimating default probabilities of CMBS with clustering and heavy censoring. Journal of Real Estate Finance and Economics, 37, 93–111.

Acknowledgments

We thank Richard Green, Jim Kau, Yuichiro Kawaguchi, Albert Lee, David Ling, Frank Nothaft, Tim Riddiough, Kerry Vandell for their helpful comments, along with participants at the 2012 FSU-UF Real Estate Symposium, 2010 AREUEA annual conference, 2009 AREUEA mid-year meeting and the 2009 Asian Pacific Real Estate Symposium. Nonetheless, all opinions and errors in this paper are our own responsibility. They do not represent the opinions of the Board of Governors of the Federal Reserve System or its staff.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

An, X., Deng, Y., Nichols, J.B. et al. Local Traits and Securitized Commercial Mortgage Default. J Real Estate Finan Econ 47, 787–813 (2013). https://doi.org/10.1007/s11146-013-9431-2

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-013-9431-2