Abstract

This paper tests the dynamics implied by a supplied-constrained view of the relationship between market fundamentals and house prices in the case of Seoul’s condominium market. The view is that supply constraints have led to serious shortages in certain submarkets, and that these shortages have led to a rapid rise in house prices and to panic buying or inflation-induced investing and to further price increases. The estimation period of the test is November 1988–February 2007. The results suggest that house prices in Seoul are highly persistent because of these supply constraints. Additionally, we do what we can with the available data to determine if house price increases serve to increase demand further, and if rent-price ratios and nominal interest rates are a good predictor of how housing prices in Seoul will evolve over time.

Similar content being viewed by others

Notes

Compare with Glaeser and Gyourko (2005), who argue that a large fraction of home value is accounted for by replacement cost. In their model, supply of land is abundant. Hence, replacement cost accounts for just about all of home values in a locality.

Seoul provides an interesting case study of house price changes. During the period studied, new condominiums in Seoul were subject to government controls on supply or sales prices or both. However, during no period under study were the market prices of existing condominiums (which are the main focus of this paper) under government control. Cho et al. (2008) conclude that the presence of inflation in the Seoul housing market causes an increase in housing wealth, and a deterioration of mortgage borrowings.

Glaeser and Gyourko (2005) also find that large increases in housing costs are followed by declines in incomes and employment. Again, this is something we do not see in the data.

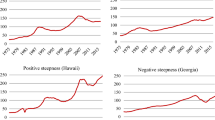

Another argument is that supply-constrained markets have more volatile rental growth rates. Now this might be true, but there is not much evidence for it in the case for Seoul. The Chonsei rental price index in Fig. 2 for both Gangnam and Gangbuk is generally rising in real terms against time, except during the Asian crisis in 1997–1998 and again in 2002–2004. However, it is not mispricing and a subsequent correction but a weak economy that is to blame for most of the observed rent declines in both of these periods.

It is also emphasized in Cho (2005) that Chonsei deposits as a proportion of capital value are inversely related to the interest rate, so if interest rates fall, the Chonsei price as a proportion of capital value will tend to rise, to yield a constant return.

Note that this assumption does not mean new construction will cease. Rather, it means that gross investment (all new units that are produced) exactly equals depreciation (capital that wears out), so that net investment will equal zero. In this case, there will be no changes to the stock of housing.

See Ben-Shahar and Sulganik (2005) for an argument to this effect. In their model, homebuyers select to maintain alive an option to purchase in the future when a negative price trend is expected and rush to exercise the option to purchase when a positive price trend is expected. In contrast, see Schwartz (1995) for a model of inflation-induced investing, where inflation encourages households to invest in real assets by reducing the real value of their borrowings but not their investments.

For example, Capozza and Seguin (1996): they find that the rent-price ratio successfully predicts future house price growth in the US, but only in the long-run, and only after controlling for cross-sectional differences in the quality of rental and owner-occupied housing.

References

Ben-Shahar, D., & Sulganik, E. (2005). Price–volume correlation in real estate markets: A real option approach. The Arison School of Business Working Paper.

Capozza, D. R., & Seguin, P. J. (1996). Expectations, efficiency, and euphoria in the housing market. Regional Science and Urban Economics, 26(3–4), 369–386.

Cho, D. (2005). Interest rate, inflation, and housing price: With an emphasis on Chonsei price in Korea. NBER Working Paper no. 11054.

Cho, H., Kim, K.-H., & Shilling, J. D. (2008). Are house prices and trading volume related? Evidence from the Seoul housing market. Working Paper.

Davis, M. A., & Palumbo, M. G. (2008). The price of residential land in large U.S. cities. Journal of Urban Economics, 63, 352–384.

Glaeser, E. L., & Gyourko, J. (2005). Durable housing and urban decline. Journal of Political Economy, 113(2), 345–375.

Gyourko, J., Mayer, C., & Sinai, T. (2006). Superstar cities. NBER Working Paper no. 12355.

Himmelberg, C., Mayer, C., & Sinai, T. (2005). Assessing high house prices: Bubbles, fundamentals, and misperceptions. Journal of Economic Perspectives, 19(4), 67–92.

Hwang, M., Quigley, J. M., & Son, J. Y. (2006). The dividend pricing model: New evidence from the Korean housing market. Journal of Real Estate Finance and Economics, 32(3), 205–228.

Jones, L. D. (1990). Current wealth constraints on the housing demand of young owners. Review of Economics and Statistics, 72(3), 424–432.

Leamer, E. E. (2002). Bubble trouble? Your home has a P/E ratio too. UCLA Anderson Forecast Report.

Ortalo-Magné, F., & Rady, S. (2006). Housing market dynamics: On the contribution of income shocks and credit constraints. Review of Economic Studies, 73, 459–485.

Schwartz, A. J. (1995). Why financial stability depends on price stability. Economic Affairs, 15, 21–25.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Cho, H., Kim, KH. & Shilling, J.D. Seemingly Irrational but Predictable Price Formation in Seoul’s Housing Market. J Real Estate Finan Econ 44, 526–542 (2012). https://doi.org/10.1007/s11146-011-9313-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-011-9313-4