Abstract

We conduct two experiments to examine how investors react to nonverbal cues of certainty as displayed by a CEO communicating forward-looking information via the relatively new and emerging medium of video. Results of the first experiment suggest that, at least for the setting we examine, investors react more negatively (do not react more positively) to a video disclosure when the CEO displays nonverbal cues of uncertainty (certainty), relative to the same disclosure delivered via audio or written text. A second experiment reveals that the lack of a positive reaction to the certain CEO in the video may be due to investors’ belief that the CEO has incentives to convey certainty via nonverbal cues. Indeed, even a subsequent good-news realization—which should add credibility to the CEO’s certainty cues—does not change this perception. Our study has implications for firms considering video as a medium for disclosure.

Similar content being viewed by others

Data availability

Contact the authors.

Notes

Although we purposefully use a broad definition of certainty, it is nevertheless consistent with more specific definitions used in economics and psychology. For example, certainty often is defined as capturing the precision of a manager’s information (e.g., Hughes and Pae 2004) or the manager’s general level of confidence or optimism (e.g., Heaton 2002; Van den Steen 2004; Malmendier and Tate 2005; Hilary and Hsu 2011; Laux and Stocken 2012). Other definitions refer to the idea that managers appear certain because of incentives to obfuscate the truth (Beyer et al. 2010; Fischer and Stocken 2001; Fischer and Verrecchia 2000; Shin 1994; Stein 1989)—for example, to signal their ability or competence (e.g., Kanodia et al. 1989; Prendergast and Stole 1996) or to build reputation (Kreps and Wilson 1982).

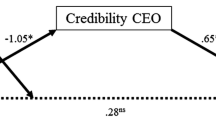

In those cases where the mean results are directionally opposite to that predicted, the corresponding one-tailed p-value is greater than 0.50, reflecting the fact that the mean difference is in the opposite tail of the distribution.

We conducted a supplemental experiment to ensure that this unexpected lack of upside movement in the certain video condition did not occur because our actor’s nonverbal certainty cues went unnoticed. The results of this supplemental experiment (not tabulated) indicate that participants do notice and can discriminate between two versions of a highly certain CEO in a video disclosure, as evidenced by their judgments about the CEO’s certainty differing across the two versions. However, for both sets of video disclosures, participants again did not evaluate the firm more favorably relative to a text condition, thereby replicating the result from our primary experiment.

An alternate research design would be one in which we solicit investment judgments and attributions in the same experiment. Although this alternate design would have the benefit of correlating participants’ responses, it would be subject to the caveat that any statistically significant correlations could be explained by carryover effects (Asay et al. 2019).

References

Ambady, N., Bernieri, F., & Richeson, J. (2000). Toward a histology of social behavior: Judgmental accuracy from thin slices of the behavioral stream. In M. Zanna (Ed.), Advances in Experimental Social Psychology (Vol. 32, pp. 201–271).

Asay, H. S., Libby, R., & Rennekamp, K. M. (2018). Do features that associate managers with a message magnify investors’ reactions to narrative disclosures? Accounting, Organizations and Society, 68-69(July), 1–14.

Asay, H. S., Guggenmos, R., Kadous, K., Koonce, L., & Libby, R. (2019). Theory testing and process evidence in accounting experiments. Working paper, University of Iowa, Cornell University, Emory University, and the University of Texas at Austin.

Baginski, S. P., Conrad, E. J., & Hassell, J. M. (1993). The effects of management forecast precision on equity pricing and on the assessment of earnings uncertainty. The Accounting Review, 68(4), 913–927.

Beaver, W., & McNichols, M. (1998). The characteristics and valuation of loss reserves of property casualty insurers. Review of Accounting Studies, 3(1–2), 73–95.

Bertrand, M., & Schoar, A. (2003). Managing with style: The effect of managers on firm policies. The Quarterly Journal of Economics, 143(4), 1169–1208.

Beyer, A., Cohen, D. A., Lys, T. Z., & Walther, B. R. (2010). The financial reporting environment: Review of recent literature. Journal of Accounting and Economics, 50(2–3), 296–394.

Birdwhistell, R. (1970). Kinesics and context. Philadelphia: University of Pennsylvania Press.

Blankespoor, E., Hendricks, B. E., & Miller, G. S. (2017). Perceptions and price: Evidence from CEO presentations at IPO roadshows. Journal of Accounting Research, 55(2), 1–53.

Burgoon, J. K., Birk, T., & Pfau, M. (1990). Nonverbal behaviors, persuasion, and credibility. Human Communication Research, 17(1), 140–169.

Burgoon, J., Guerrero, L. K., & Floyd, K. (2010). Nonverbal communication. Boston: Allyn & Bacon.

Burgstahler, D., & Dichev, I. (1997). Earnings management to avoid earnings decreases and losses. Journal of Accounting and Economics, 24(1), 99–126.

Cade, N. L. (2018). Corporate social media: How two-way disclosure channels influence investors. Accounting, Organizations and Society, 68-69(July), 63–79.

Caterpillar. (2018). CFO Brad Halverson’s overview of Caterpillar’s fourth-quarter and full-year 2017 financial results. https://www.youtube.com/watch?v=_FivavLGwx8 Accessed 04.19.18.

Chodor, B. (2014). Though few have, now is the right time to embrace video earnings calls. Entrepreneur. August 28. Available at: http://www.entrepreneur.com/article/236817. Accessed 4 April 2017.

Dechow, P., Ge, W., & Schrand, C. (2010). Understanding earning quality: A review of their proxies, their determinants, and their consequences. Journal of Accounting and Economics, 50(2–3), 344–401.

DeGroot, T., & Motowidlo, S. J. (1999). Why visual and vocal interview cues can affect interviewers’ judgments and predict job performance. Journal of Applied Psychology, 84(6), 986–993.

DePaulo, B. M. (1992). Nonverbal behavior and self-presentation. Psychological Bulletin, 111(2), 203–243.

Dichev, I. D., Graham, J. R., Harvey, C. R., & Rajgopal, S. (2013). Earnings quality: Evidence from the field. Journal of Accounting and Economics, 56(2–3), 1–13.

Ekman, P. (1965). Differential communication of affect by head and body cues. Journal of Personality and Social Psychology, 2(5), 726–735.

Ekman, P. (1979). About brows: Emotional and conversational signals. In M. von Cranach, K. Foppa, W. Lepenies, & D. Ploog (Eds.), Human ethology: Claims and limits of a new discipline (pp. 169–202). Cambridge: Cambridge University Press.

Ekman, P., & Friesen, W. V. (1971). Constants across culture in the face and emotion. Journal of Personality and Social Psychology, 17(2), 124–129.

Elliott, W. B., Hodge, F. D., & Sedor, L. M. (2012). Using online video to announce a restatement: Influences on investment decisions and the mediating role of trust. The Accounting Review, 87(2), 513–535.

Elliott, W. B., Grant, S. M., & Hodge, F. D. (2018). Investor reaction to $firm or #CEO use of social media for negative disclosures. Journal of Accounting Research, 56(5), 1483–1519.

Epley, N., & Dunning, D. (2000). Feeling “holier than thou”: Are self-serving assessments produced by errors in self- or social prediction? Journal of Personality and Social Psychology, 79(6), 861–975.

Erickson, B., Lind, E. A., Johnson, B. C., & O’Barr, W. M. (1978). Speech style and impression formation in a court setting: The effects of “powerful” and “powerless” speech. Journal of Experimental Psychology, 14(3), 266–279.

Fischer, P. E., & Stocken, P. C. (2001). Imperfect information and credible communication. Journal of Accounting Research, 39(1), 119–134.

Fischer, P. E., & Verrecchia, R. E. (2000). Reporting bias. The Accounting Review, 75(2), 229–245.

Gilbert, D. (1998). Speeding with Ned: A personal view of the correspondence bias. In J. Darley & J. Cooper (Eds.), Attribution and social interaction (pp. 5–36). Washington, DC: American Psychological Association.

Gilbert, D., & Malone, P. (1995). The correspondence bias. Psychological Bulletin, 117(1), 21–38.

Gleason, C., & Mills, L. (2008). Evidence of differing market responses to beating analysts’ targets through tax expense decreases. Review of Accounting Studies, 13(2–3), 295–318.

Heaton, J. B. (2002). Managerial optimism and corporate finance. Financial Management, Summer, 33–45.

Hecht, M. A., & Ambady, N. (1999). Nonverbal communication and psychology: Past and future. New Jersey Journal of Communication, 7(2), 1–15.

Heider, F. (1958). The psychology of interpersonal relations. New York: Wiley.

Hencock, L., & Robinson, D. (2005). Do managers credibly use accruals to signal private information? Evidence from the pricing of discretionary accruals around stock splits. Journal of Accounting and Economics, 39(2), 361–380.

Hilary, G., & Hsu, C. (2011). Endogenous overconfidence in managerial forecasts. Journal of Accounting and Economics, 51(3), 300–313.

Himmelfarb, S. (1975). What to do when the control group doesn’t fit into the factorial design? Psychological Bulletin, 82(3), 363–368.

Hirst, D. E., Koonce, L., & Miller, J. (1999). The joint effect of management’s prior forecast accuracy and the form of its financial forecasts on investor judgments. Journal of Accounting Research, 37(Supplement), 1–24.

Hirst, D. E., Koonce, L., & Venkataraman, S. (2007). How disaggregation enhances the credibility of management earnings forecasts. Journal of Accounting Research, 45(4), 811–838.

Hobson, J. L., Mayew, W. J., & Venkatachalam, M. (2012). Analyzing speech to detect financial misreporting. Journal of Accounting Research, 50(2), 349–392.

Hogarth, R. M. (1975). Cognitive processes and the assessment of subjective probability distributions. Journal of the American Statistical Association, 70(350), 271–289.

Hornik, J. (1987). The effect of touch and gaze upon compliance and interest of interviewees. The Journal of Social Psychology, 127(6), 681–683.

Hughes, J. S., & Pae, S. (2004). Voluntary disclosure of precision information. Journal of Accounting and Economics, 37(2), 261–289.

Hutton, A., Miller, G., & Skinner, D. (2003). The role of supplementary statements with management earnings forecasts. Journal of Accounting Research, 41(5), 867–890.

Jonas, E., & Frey, D. (2003). Information search and presentation in advisor-client interactions. Organizational Behavior and Human Decision Performance, 91(2), 154–168.

Jones, E., & Davis, K. (1965). From acts to dispositions. The attribution process in social psychology. In L. Berkowitz (Ed.), Advances in experimental social psychology (Vol. 2, pp. 219–266). New York: Academic Press.

Kanodia, C., Bushman, R., & Dickhaut, J. (1989). Escalation errors and the sunk cost effect: An explanation based on reputation and information asymmetries. Journal of Accounting Research, 27(1), 59–77.

Kelley, H. (1967). Attribution theory in social psychology. In D. Levine (Ed.), Nebraska symposium on motivation (Vol. 15, pp. 192–238). Lincoln: University of Nebraska Press.

Kleinke, C. L. (1986). Gaze and eye contact: A research review. Psychological Bulletin, 100(1), 78–100.

Knapp, M. L., Hall, J. A., & Horgan, T. G. (2014). Nonverbal communication in human interaction (8th ed.). Boston: Cengage.

Koonce, L., & Lipe, M. G. (2010). Earnings trend and performance relative to benchmarks: How consistency influences their joint use. Journal of Accounting Research, 48(4), 859–884.

Koonce, L., & Lipe, M. G. (2017). Firms with inconsistently signed earnings surprises: Do potential investors use a counting heuristic? Contemporary Accounting Research, 34(1), 292–313.

Krahmer, E., & Swerts, M. (2005). How children and adults produce and perceive uncertainty in audiovisual speech. Language and Speech, 48(1), 29–53.

Kreps, D. M., & Wilson, R. (1982). Reputation and imperfect information. Journal of Economic Theory, 27(2), 253–279.

Krische, S. (2019). Investment experience, financial literacy, and investment-related judgments. Contemporary Accounting Research, 36(3), 1634–1668.

Laux, V., & Stocken, P. C. (2012). Managerial reporting, overoptimism, and litigation risk. Journal of Accounting and Economics, 53(3), 577–591.

Leathers, D., & Eaves, M. (2016). Successful nonverbal communication: Principles and application (4th ed.). New York: Routledge.

Lee, J. (2016). Can investors detect managers’ lack of spontaneity? Adherence to predetermined scripts during earnings conference calls. The Accounting Review, 91(1), 229–250.

Malmendier, U., & Tate, G. (2005). CEO overconfidence and corporate investment. The Journal of Finance, 60(6), 2661–2700.

Mason, M. F., Tatkow, E. P., & Macrae, C. N. (2005). The look of love: Gaze shifts and person perception. Psychological Science, 16(3), 236–239.

Mayew, W. J., & Venkatachalam, M. (2012). The power of voice: Managerial affective states and future firm performance. Journal of Finance, 67(1), 1–43.

McDonalds. (2015). McDonalds 2015 Webcast. https://mcdonalds.webcasts.com/viewer/landing.jsp?ei=1063465 Accessed 01.01.16.

McNichols, M. (1989). Evidence of informational asymmetries from management earnings forecasts and stock returns. The Accounting Review, 64(1), 1–27.

Mehrabian, A., & Williams, M. (1969). Nonverbal concomitants of perceived and intended persuasiveness. Journal of Personality and Social Psychology, 13(1), 37–58.

Mercer, M. (2004). How do investors assess the credibility of management disclosures? Accounting Horizons, 18(3), 185–196.

Milgrom, P., & Roberts, J. (1986). Price and advertising signals of product quality. Journal of Political Economy, 94(4), 796–821.

Miller, N., Maruyama, G., Beaber, R. J., & Valone, K. (1976). Speed of speech and persuasion. Journal of Personality and Social Psychology, 34(4), 615–624.

Montepare, J. M., & McArthur, L. Z. (1988). Impressions of people created by age-related qualities of their gates. Journal of Personality and Social Psychology, 55(4), 547–556.

Netflix. (2018). Netflix Q1 2018 Earnings interview. https://www.youtube.com/watch?v=A9S1jeqbBY0 Accessed 04.18.18.

Nierenberg, G. I., & Calero, H. H. (1990). How to read a person like a book. New York: Pocket Books.

Noe, C. (1999). Voluntary disclosures and insider trading. Journal of Accounting and Economics, 27(3), 306–328.

Petroni, K., Ryan, S., & Wahlen, J. (2000). Discretionary and non-discretionary revisions of loss reserves by property-casualty insurers: Differential implications for future profitability, risk and market value. Review of Accounting Studies, 5(2), 95–125.

Philpott, J. (1983). The relative contribution to meaning of verbal and nonverbal channels of communication … a metanalysis. Unpublished manuscript: University of Nebraska.

Prendergast, C., & Stole, L. (1996). Impetuous youngsters and jaded old-timers: Acquiring a reputation for learning. Journal of Political Economy, 104(6), 1105–1134.

Restoration Hardware. (2017). Fourth quarter fiscal 2016 earnings video. http://ir.restorationhardware.com/videos-presentations-0 Accessed 04.19.18.

Roach, G. (2014). Spicing up the numbers: Five corporate reporting trends. IR Magazine. October 9. Available at: http://www.irmagazine.com/articles/earnings-calls-financial-reporting/20407/new-corporate-reporting-trends/. Accessed 4 April 2017.

Rogers, J. L., & Van Buskirk, A. (2013). Bundled forecasts in empirical accounting research. Journal of Accounting and Economics, 55(1), 43–65.

Ross, L., & Nisbett, R. (1991). The person and the situation: Perspectives of social psychology. New York: McGraw-Hill.

Shin, H. S. (1994). News management and the value of firms. RAND Journal of Economics, 25(1), 58–71.

Shivakumar, L. (2000). Do firms mislead investors by overstating earnings before seasoned equity offerings? Journal of Accounting and Economics, 29(3), 339–371.

Smith, V. L., & Clark, H. H. (1993). On the course of answering questions. Journal of Memory and Language, 32(1), 25–38.

Stein, J. C. (1989). Efficient capital markets, inefficient firms: A model of myopic corporate behavior. The Quarterly Journal of Economics, 104(4), 655–669.

Swerts, M., & Krahmer, E. (2005). Audiovisual prosody and feeling of knowing. Journal of Memory and Language, 53(1), 81–94.

Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185(4157), 1124–1131.

Van den Steen, E. (2004). Rational overoptimism (and other biases). The American Economic Review, 94(4), 1141–1151.

Wallbott, H. G. (1998). Bodily expression of emotion. European Journal of Social Psychology, 28(6), 879–896.

Acknowledgements

The authors thank Aysa Dordzhieva, Michael Durney, Harry Evans, Laura Feustel, Paul Fischer (editor), Ryan Guggenmos, Ling Harris, Kathryn Holmstrom, Bright Hong, Hyun Hwang, Eathan LaMothe, Volker Laux, Kun Liu, Kristi Rennekamp, Kathy Rupar, Shankar Venkataraman, Ronghuo Zheng, Aaron Zimbleman, two anonymous reviewers, and workshop participants at Cornell University, Georgia Institute of Technology, and University of South Carolina for their helpful comments and suggestions. We appreciate the research assistance of Laura Savoie. Lisa Koonce gratefully acknowledges funding from the Deloitte Foundation.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1 Experimental manipulation

Appendix 2

Rights and permissions

About this article

Cite this article

Cade, N.L., Koonce, L. & Mendoza, K.I. Using video to disclose forward-looking information: the effect of nonverbal cues on investors’ judgments. Rev Account Stud 25, 1444–1474 (2020). https://doi.org/10.1007/s11142-020-09539-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11142-020-09539-8