Abstract

This paper examines whether managers can reduce the detrimental effects of information overload by spreading out, or temporally smoothing, disclosures. We begin by attempting to identify managerial smoothing. We find that when there are multiple disclosures for the same event date, managers spread the disclosures out over several days. Managers are also more likely to delay a disclosure when there has been a disclosure made within the three days before the event date. Finally, managers are more likely to engage in disclosure smoothing when disclosures are longer, the information environment is more robust, firm information is complex, uncertainty is high, and disclosure news is more positive. Our second set of analyses examines whether there are market benefits to disclosure smoothing. Using two different measures of disclosure smoothing, we find that smoothing is associated with increased liquidity, reduced stock price volatility and increased analyst forecast accuracy.

Similar content being viewed by others

Notes

Note that our theory and corresponding predictions are based on fundamental traders, i.e., those traders who read firm disclosures and incorporate that information into their trades. Traders conducting technical analysis do not process firm disclosures and thus do not require time to read firm disclosures.

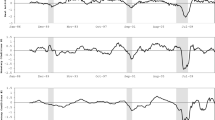

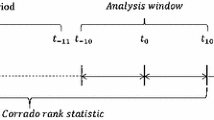

In Section 3, we discuss our two disclosure smoothing proxies, measured over a quarter: (1) the number of disclosures made in short (less than three-day) intervals, and (2) the standard deviation of the time between firm disclosures. Figure 1 provides examples of low, moderate and high disclosure smoothing using both proxies.

Managers can also mitigate overload by reducing disclosure. However, mandatory reporting requirements make this option less viable, and reduced disclosure arguably could make the information environment even worse. In contrast, smoothing allows the same amount of information to be disclosed. By spreading out the timing of the disclosures, managers give investors less information to process over any short period.

As Hirshleifer and Teoh (2003, p. 339) point out, “[i]nattention seems foolish … as inattentive investors lose money by ignoring aspects of the economic environment. However, if time and attention are costly, such behavior may be reasonable.” This intuition is also consistent with Grossman and Stiglitz (1980) and Bloomfield (2002), in that higher processing costs leads to less information assimilation. See Section 2.2 for a more detailed discussion.

For example, consider disclosures about a new product or a corporate acquisition. Stakeholders cannot simply read these disclosures and understand the implications for firm value. For product announcements, investors would want to better understand the technology behind the product, associated costs and revenues, adjustments to the product mix, impact on competitors, consumer demand, etc. For an acquisition, investors would want to know considerable detail about the target firm, synergies between the firms, how the acquisition fits into the strategy of the firm, etc.

Note too that we expect disclosure smoothing to be relevant even when there are relatively few disclosures in a given week or month. That is, firm disclosures are typically not uniformly distributed in time over the quarter; rather, they tend to be clustered around events within the quarter, while other periods in the quarter (such as quiet periods) tend to have few, if any, disclosures (NIRI 2015). Therefore managers may engage in smoothing to smooth out clustering even when the overall level of disclosure frequency is low.

For example, on April 2, 2012, Express Scripts Inc. (i) completed a merger with Medco Health Solutions and (ii) approved a supplemental indenture with Wells Fargo. While the events occurred on the same day, the 8-K disclosing the merger was filed on April 2, 2012, and the 8-K disclosing the supplemental indenture was filed on April 6, 2012.

In Section 4, we discuss entropy balancing and its advantages in our setting.

Studies have documented a recent increase in the frequency of bundled management forecasts, i.e., management earnings forecasts issued concurrently with earnings announcements (e.g., Anilowski et al. 2007, Rogers and Van Buskirk 2013). In untabulated analyses, we find that both of our measures of disclosure smoothing are negatively and significantly associated with the practice of bundling guidance and earnings announcements. These results suggest that firms that smooth more are less likely to bundle and more likely to disclose guidance separately from earnings, consistent with distinct incentives driving bundling and smoothing decisions.

In recent years, these have included requirements for more disclosure on topics ranging from executive compensation to hedging transactions. Dyer et al. (2016) find that much of the increase in 10 K length is attributable to new disclosure requirements, including fair value accounting, internal controls, and risk factors.

Importantly, information overload arises not only because of increased disclosure but also because investors have limited time to process the information they receive. The notion that time constraints give rise to information overload has been documented previously (Shick et al. 1990; Schroder et al. 1967; Snowball 1980).

Subsequent studies provide evidence supporting Simon’s predictions. For example, Einhorn (1971) finds that as information increases, individuals use mixed modeling strategies (“compound models”) to simplify their decision-making. Payne (1976) documents that, when faced with information overload, individuals use heuristics to quickly eliminate some of the available alternatives without rigorously investigating them, to reduce the number of alternatives in consideration.

In their review of 97 studies on information overload, Eppler and Mengis (2004) note a recurring finding that more information improves decision-making to a point, beyond which it makes decision-making worse. One reason is that too much information makes it more difficult to identify the relationship between the details and the higher-order inferences (Owen 1992; Schneider 1987). Thus information overload inhibits individuals from clearly understanding the inferences that are most decision-relevant.

See history of the Wheat Report: http://www.sechistorical.org/museum/galleries/tbi/gogo_d.php

Section 108 of the JOBS Act of 2012 requires the SEC to comprehensively analyze the current disclosure regime.

See SEC concept release for updating Regulation S-K: https://www.sec.gov/rules/concept/2016/33-10064.pdf

The relevance score is assigned by RavenPack to measure how strongly the firm relates to the underlying news story. The scores range from 0 (low relation) to 100 (high relation). We use a minimum relevance score of 90 to avoid erroneously excluding firm-initiated press releases that include names of other firms. Names of firms not initiating the press release are commonly included in announcements of M&A transactions, partnering, or sourcing agreements, etc. In untabulated analysis, we find that our results are robust to excluding all articles with a relevance score lower than 100.

We validate this approach across the subset of observations for which the novelty score is provided. We find that eliminating subsequent press releases within 15 min correctly removes duplicates in 80.7% of cases. We find similar results when using the same process over 5-, 10-, or 30-min intervals.

Requiring a minimum of two press releases effectively removes very low press release frequency firms from our sample, including some smaller firms that only issue one press release per quarter.

As we note in the introduction, managers can adjust not just the timing of their disclosures, but for some events, they can also influence the stated event date. This is particularly true for events for which there is managerial discretion as to when the event will occur. For example, managers have some discretion as to when they announce a merger or the firing/resignation of an employee or board member. However, there is less discretion in determining an event date for events beyond managers’ control. For the 8-K sample, we assume the event date filed with the SEC is correct. However, even if some event dates were adjusted, this should bias against our findings, since there is no need to delay the disclosure date when the event date can be adjusted. That is, it would just bring attention to the delay. In our second set of analyses using the press release sample, we relax this assumption to allow for the event or disclosure dates or both to be adjusted.

RavenPack provides topic descriptions for approximately 47% of the releases in the press release sample. The proportions presented in Table 3 are therefore relative to the sample of press releases for which there is a topic description available.

Entropy balancing weights control observations, such that post-weighting distributional properties of treatment and control observations are virtually identical, thereby ensuring covariate balance. Entropy balancing works by first determining the mean and variance of the treatment observations, which become the target mean and variance of the post-weighting control sample (also known as the balance conditions). An algorithm iteratively assigns weights to control observations until the balance conditions have been met (meaning distributional properties of treatment and post-weighted control observations are identical). Treatment observations are not re-weighted, meaning they retain their default weighting of one, while control observations are assigned a positive weight that may be greater or less than one. After the algorithm assigns weights to each observation, these weights are used in subsequent regression analyses.

In August of 2004, the SEC shortened the filing deadline for all mandatory 8-K items to four business days (from the prior deadlines of between five and 15 days depending on the item). We observe reporting delays of more than four days, because our sample includes voluntary 8-Ks, which are not subject to the four-business day deadline.

One possible alternative explanation of this result is that managers delay disclosure of the second event, because they are distracted by follow-up with investors about the first event. However, Soltes (2014) finds that this type of follow-up is concentrated in the 72 h following the event. Thus any post-announcement distraction would likely have subsided by the third day.

While firm size is likely correlated with factors such as having more internal resources to handle disclosure tasks, we focus on the relationship between size and expected information overload, because this directly relates to a firm’s incentive to help investors fully understand their disclosures. In untabulated tests, we find similar results when using lagged analyst and media coverage as alternative proxies for the firm’s information environment.

In our subsequent tests, we further address this potential concern by controlling for earnings volatility.

Harris (1990, p. 3) states: “A market is liquid if traders can quickly buy or sell large numbers of shares when they want and at low transaction costs. Liquidity is the willingness of some traders (often but not necessarily dealers) to take the opposite side of a trade that is initiated by someone else, at low cost” (Emphasis added).

Appendix 1 provides detailed variable definitions. Our controls include factors shown previously in the determinants model in Table 5 to predict disclosure smoothing. We include them as controls in subsequent tests to rule out the potential confounding effect of these factors on the outcomes we study. We note that, by controlling for these factors, we essentially remove some of the variation in our smoothing measures.

We follow Bushman et al. (2017) in using the composite sentiment score (CSS) provided by Ravenpack to categorize news stories as positive, neutral, or negative. The CSS score ranges from 0 to 100, with values below 50 indicating negative news, values equal to 50 indicating neutral news, and values greater than 50 indicating positive news. The CSS score is the combination of five proprietary sentiment measures that combine textual analysis (identifying emotionally charged words and phrases), expert categorization of topics likely to cause positive or negative short-term market reaction, and an algorithm that ensures agreement among the five sentiment measures. The five sentiment measures are PEQ, BEE, BMQ, BCA, and BAM. Detailed definitions of these measures are described in Appendix A of Bushman et al. (2017).

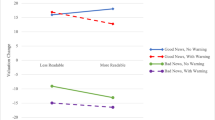

Since our unit of observation is individual press releases and we include firm-year-quarter fixed effects instead of firm-quarter control variables, this analysis uses all available press releases, including those with missing financial or stock price data, resulting in a larger sample of press releases in Table 9, Panel A, than the one described in Table 3. Panel B includes the subset of press releases from Panel A for which the subsequent press release is considered good news, according to RavenPack’s composite sentiment score (CSS). Panel C includes the subsample of 8-Ks for which the corresponding CSS variable is available from RavenPack.

References

Abdel-Khalik, A. R. (1973). The effect of aggregating accounting reports on the quality of the lending decision: An empirical investigation. Journal of Accounting Research, 104–138.

Amihud, Y. (2002). Illiquidity and stock returns: cross-section and time-series effects. Journal of Financial Markets, 5(1), 31–56.

Anilowski, C., Feng, M., & Skinner, D. J. (2007). Does earnings guidance affect market returns? The nature and information content of aggregate earnings guidance. Journal of Accounting and Economics, 44(1–2), 36–63.

Beyer, A., Cohen, D. A., Lys, T. Z., & Walther, B. R. (2010). The financial reporting environment: Review of the recent literature. Journal of Accounting and Economics, 50(2), 296–343.

Billings, M. B., Jennings, R., & Lev, B. (2015). On guidance and volatility. Journal of Accounting and Economics, 60(2), 161–180.

Blankespoor, E., Miller, G. S., & White, H. D. (2014). The role of dissemination in market liquidity: Evidence from firms’ use of Twitter™. The Accounting Review, 89(1), 79–112.

Bloomfield, R. J. (2002). The “incomplete revelation hypothesis” and financial reporting. Accounting Horizons, 16(3), 233–243.

Brown, L. D., Call, A. C., Clement, M. B., & Sharp, N. Y. (2015). Inside the “Black Box” of Sell-Side Financial Analysts. Journal of Accounting Research, 53(1), 1–47.

Brown, L. D., Call, A. C., Clement, M. B., & Sharp, N. Y. (2018). Managing the Narrative: Investor Relations Officers and Corporate Disclosure. Working paper.

Bushman, R. M., Williams, C. D., & Wittenberg Moerman, R. (2017). The Informational Role of the Media in Private Lending. Journal of Accounting Research, 55(1), 115–152.

Casey, C. J. (1980). Variation in accounting information load: The effect on loan officers' predictions of bankruptcy. Accounting Review, 36–49.

Chapman, K. L., Miller, G. S., & White, H. D. (2018). Investor Relations and Information Assimilation. Working paper.

Chewning, E. G., & Harrell, A. M. (1990). The effect of information load on decision makers' cue utilization levels and decision quality in a financial distress decision task. Accounting, Organizations and Society, 15(6), 527–542.

Cohen, S. (1980). Aftereffects of stress on human performance and social behavior: a review of research and theory. Psychological Bulletin, 88(1), 82–108.

Diamond, D. W., & Verrecchia, R. E. (1991). Disclosure, liquidity, and the cost of capital. The Journal of Finance, 46(4), 1325–1359.

Drake, M. S., Thornock, J. R., & Twedt, B. J. (2017). The internet as an information intermediary. Review of Accounting Studies. Forthcoming.

Dyer, T., Lang, M. H., & Stice-Lawrence, L. (2016). The evolution of 10-K textual disclosure: Evidence from Latent Dirichlet Allocation. Available at SSRN 2741682.

E&Y (2014). Disclosure Effectiveness Companies Embrace the Call to Action.

Einhorn, H. J. (1971). Use of nonlinear, noncompensatory models as a function of task and amount of information. Organizational Behavior and Human Performance, 6(1), 1–27.

Epley, N., & Gilovich, T. (2006). The anchoring-and-adjustment heuristic—Why the adjustments are insufficient. Psychological Science, 17(4), 311–318.

Eppler, M. J., & Mengis, J. (2004). The concept of information overload: A review of literature from organization science, accounting, marketing, MIS, and related disciplines. The Information Society, 20(5), 325–344.

Graham, J. R., Harvey, C. R., & Rajgopal, S. (2005). The economic implications of corporate financial reporting. Journal of Accounting and Economics, 40(1), 3–73.

Grossman, S. J., & Stiglitz, J. E. (1980). On the impossibility of informationally efficient markets. The American Economic Review, 70(3), 393–408.

Groysberg, B., & Healy, P. (2013). Wall Street research: Past, present, and future. Stanford: Stanford University Press.

Hainmueller, J. (2011). Entropy balancing for causal effects: A multivariate reweighting method to produce balanced samples in observational studies. Political Analysis, 20(1), 25–46.

Harris, L. (1990). Liquidity, Trading Rules and Electronic Trading Systems. New York University Monograph Series in Finance and Economics. Monograph No. 1990-4. New York University.

Herbig, P. A., & Kramer, H. (1994). The effect of information overload on the innovation choice process: Innovation overload. Journal of Consumer Marketing, 11(2), 45–54.

Higgins, K.F. (2014). Disclosure Effectiveness: Remarks before the American Bar Association Business Law Section Spring Meeting. Securities and Exchange Commission. Available at: https://www.sec.gov/News/Speech/Detail/Speech/1370541479332

Hirshleifer, D., & Teoh, S. H. (2003). Limited attention, information disclosure, and financial reporting. Journal of Accounting and Economics, 36(1), 337–386.

Iselin, E. R. (1988). The effects of information load and information diversity on decision quality in a structured decision task. Accounting, Organizations and Society, 13(2), 147–164.

Jacoby, J., Speller, D. E., & Kohn, C. A. (1974). Brand choice behavior as a function of information load. Journal of Marketing Research, 63–69.

KPMG (2012). Disclosure overload and complexity: Hidden in plain sight.

Lawrence, A. (2013). Individual investors and financial disclosure. Journal of Accounting and Economics, 56(1), 130–147.

Lee, Y. J. (2012). The effect of quarterly report readability on information efficiency of stock prices. Contemporary Accounting Research, 29(4), 1137–1170.

Leuz, C., & Verrecchia, R. E. (2000). The economic consequences of increased disclosure. Journal of Accounting Research, 91–124.

Loughran, T., & McDonald, B. (2014). Measuring readability in financial disclosures. The Journal of Finance, 69(4), 1643–1671.

Malhotra, N. K. (1982). Information load and consumer decision making. Journal of Consumer Research, 8(4), 419–430.

McMullin, J., & Schonberger, B. (2015). Entropy-balanced discretionary accruals. Working paper. Indiana University and the University of Rochester.

Merton, R. C. (1987). A simple model of capital market equilibrium with incomplete information. The Journal of Finance, 42(3), 483–510.

Miller, B. P. (2010). The effects of reporting complexity on small and large investor trading. The Accounting Review, 85(6), 2107–2143.

NIRI. (2015). Public company quiet period practices and trends. Alexandria: The National Investors Relations Institute.

Owen, R. S. (1992). Clarifying the simple assumption of the information load paradigm. Advances in Consumer Research, 19, 770–776.

Paredes, T. A. (2003). Blinded by the light: Information overload and its consequences for securities regulation. Wash. ULQ, 81, 417–485.

Payne, J. W. (1976). Task complexity and contingent processing in decision making: An information search and protocol analysis. Organizational Behavior and Human Performance, 16(2), 366–387.

Plumlee, M. A. (2003). The effect of information complexity on analysts' use of that information. The Accounting Review, 78(1), 275–296.

Radin, A. J. (2007). Have we created financial statement disclosure overload. The CPA Journal, 77(11), 6–9.

Rogers, J. L., & Van Buskirk, A. (2013). Bundled forecasts in empirical accounting research. Journal of Accounting and Economics, 55(1), 43–65.

Schick, A. G., Gordon, L. A., & Haka, S. (1990). Information overload: A temporal approach. Accounting, Organizations and Society, 15(3), 199–220.

Schneider, S. C. (1987). Information overload: Causes and consequences. Human Systems Management, 7(2), 143–153.

Schroder, H. M., Driver, M. J., & Streufert, S. (1967). Human information processing: Individuals and groups functioning in complex social situations. New York, NY: Holt, Rinehart and Winston.

Shroff, N., Sun, A., White, H., & Zhang, W. (2013). Voluntary Disclosure and Information Asymmetry: Evidence from the 2005 Securities Offering Reform. Journal of Accounting Research, 51(5), 1299–1345.

Simon, H. A. (1955). A behavioral model of rational choice. The Quarterly Journal of Economics, 99–118.

Simon, H. A. (1978). Rationality as process and as product of thought. The American Economic Review, 68(2), 1–16.

Skinner, D. J. (1997). Earnings disclosures and stockholder lawsuits. Journal of Accounting and Economics, 23(3), 249–282.

Snowball, D. (1980). Some effects of accounting expertise and information load: An empirical study. Accounting, Organizations and Society, 5(3), 323–338.

Soltes, E. (2014). Private Interaction Between Firm Management and Sell-Side Analysts. Journal of Accounting Research, 52(1), 245–272.

Sparrow, P. (1999). Strategy and cognition: Understanding the role of management knowledge structures, organizational memory and information overload. Creativity and Innovation Management, 8(2), 140–148.

Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185, 1124–1131.

Waymire, G. (1984). Additional evidence on the information content of management earnings forecasts. Journal of Accounting Research, 703–718.

White, M.J. (2013). The Importance of Independence. Securities and Exchange Commission. Available at: https://www.sec.gov/News/Speech/Detail/Speech/1370539864016

You, H., & Zhang, X. J. (2009). Financial reporting complexity and investor underreaction to 10-K information. Review of Accounting Studies, 14(4), 559–586.

Acknowledgements

We thank Beth Blankespoor, Mark Bradshaw, Ed deHaan, Mike Drake, Henock Louis, Jake Thornock, and workshop participants at Washington University in St. Louis, the University of Washington, the University of Toronto, the BYU Accounting Research Symposium, the LBS Accounting Symposium, the JAAF Conference and an anonymous reviewer for their helpful comments and suggestions.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix 1: Variable Definitions

Appendix 1: Variable Definitions

Variables | Definition |

|---|---|

Analyst Forecast Accuracy | = Minus one times the absolute difference between the median quarterly analyst EPS forecast consensus and the actual, according to I/B/E/S, scaled by the stock price at the end of the quarter. We require the issuance of quarterly EPS forecasts by at least two unique analysts within 90 days prior to the earnings reporting date to calculate analyst forecast accuracy. |

Another disclosure made less than 3 days prior to Event Date | = Indicator variable equal to one when the firm made at least one 8-K disclosure in the three days prior to the current 8-K event date. |

Average Price | = Average daily stock price during the quarter, according to CRSP. |

Average Bid-Ask Spread | = Average of the daily ask minus the daily bid quotes during the quarter according to CRSP. |

Current PR is Negative | = Indicator variable equal to one for press releases with a composite sentiment score below 50, indicating negative news, according to RavenPack. |

Distance between Event Date and 8-K Disclosure Date | = Number of days between the event date and corresponding 8-K disclosure date. |

Earnings Volatility | = Standard deviation of earnings before extraordinary items in the same fiscal quarter in the five prior years scaled by average total assets. |

Length of Press Releases | = Log of sum of the number of words in the disclosures over the quarter. |

Length of 8-K | = Number of words in the 8-K file. |

Leverage | = Total debt divided by total assets in the quarter. |

Liquidity | = Minus one times the Amihud’s (2002) illiquidity measure during the quarter, calculated as the average of the absolute value of the daily return-to-volume ratio. |

Log Assets | = Log of total assets in the current fiscal quarter. |

Loss | = Indicator variable equal to one if the earnings before extraordinary items during the quarter is negative. |

Market-to-Book | = Market value of equity divided by the book value at the end of the current quarter. |

Next PR is Positive | = Indicator variable equal to one for press releases for which the subsequent press release has a composite sentiment score above 50, indicating positive news according to RavenPack. |

Number of Analysts | = Number of unique analysts issuing a forecast during the quarter, according to I/B/E/S. |

Number of Press Releases | = Number of firm-initiated press releases disclosed during the current quarter. Using RavenPack Press Release Edition, we require articles to have a relevance score of at least 90; to have a source equal to PRNewswire, BusinessWire, MarketWire or Globe Newswire; and to be a “press release” news type. We also delete duplicate press releases by keeping only the highest novelty score articles. For those with a novelty score missing in RavenPack, we delete the articles disclosed within 15 min from the last press release. |

Number of firm 8-Ks per Event Date | = Number of 8-Ks per event date for the same firm. |

Prior 12-Month Returns | = Cumulative monthly stock returns in the 12 months prior to the beginning of the current quarter. |

Proportion of Bad News Releases | = Number of firm-initiated press releases with negative sentiment (according to the RavenPack composite sentiment measure) divided by the total number of firm-initiated press releases in the quarter. |

ROA | = Earnings before extraordinary items divided by total assets in the current fiscal quarter. |

Segments | = Indicator variable equal to one if the firm reported more than one business or geographic segment in the year according to the Compustat Segments database. |

Short-Interval Smoothing | = Minus one times the number of firm-initiated press releases disclosed less than three days apart during the quarter. |

Variance Smoothing | = Minus one times the standard deviation of the number of hours between firm-initiated press releases disclosed during the quarter divided by 100. |

Stock Return Volatility | = Standard deviation of daily stock returns during the quarter. |

Turnover | = Sum of the daily share volume divided by total shares outstanding in the quarter. |

Volatility Prior 12-Month Returns | = Standard deviation of daily stock returns in the 12 months prior to the beginning of the current quarter. |

Rights and permissions

About this article

Cite this article

Chapman, K.L., Reiter, N., White, H.D. et al. Information overload and disclosure smoothing. Rev Account Stud 24, 1486–1522 (2019). https://doi.org/10.1007/s11142-019-09500-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11142-019-09500-4