Abstract

Usury has been predominantly studied as an economic or legal phenomenon and only recently has gotten into the spotlight of sociological research. This article aims to contribute to the current literature by operationalising usury vulnerability and analysing household factors impacting it, using the European Union Statistics on Income and Living Conditions (EU-SILC) data for Italy. To construct usury vulnerability, we examined variables measuring a household’s financial and material well-being. As to factors impacting the phenomenon, we included those reflecting a socio-demographic position of a household (household composition and territorial position within the country, age, sex, education, and employment status of the top earner). The estimation results indicate that all micro-level factors matter in terms of usury vulnerability. Therefore, by identifying the most vulnerable social groups, the model might help develop relevant policy interventions to fight the spread of usury, especially in times of economic decline.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

The scientific literature shows that usury is a phenomenon particularly related to the general economic conditions of a specific context (Gosztonyi and Havran 2021; Saunders 2021). This means that as the financial situation worsens, that is, as the economic and financial difficulties of families and businesses increase, usury crimes grow. For example, in Italy, on the background of the European debt crisis, according to institutional estimations, usury profits increased 2.5 times from €18 billion in 2012 to €45 billion in 2015 (Barone 2018). Furthermore, the economic crisis provoked new forms of usury in the country – “daily usury”, which implies borrowing money in the morning and returning it at the interest rate in the evening. This type of usury attracted small and medium companies along with people coming from the working class, clerical workers and professionals (Lavorgna and Sergi 2014).

Although scarce, the previous sociological research on usury indicates that besides the economic conditions, a variety of micro-level factors impact the risk of usury exposure. They comprise individual or household characteristics that might lead to over-indebtedness and increased usury vulnerability (Charron-Chénier 2018; Distelberg et al. 2009; Rowlingson et al. 2016; Saunders 2021; Wilson 2002). However, the current body of literature shows a lack of consensus on the operationalisation of usury vulnerability and possible factors impacting it, as most studies focus on the victims of the crime rather than households at risk of usury exposure. Furthermore, the studies usually employ qualitative methodology, which might be due to a lack of a clear and agreed-upon conceptualisation and operationalisation of usury vulnerability, impeding quantitative research.

The current article has two aims. Its first objective is to develop a methodology for constructing the usury vulnerability index, measured at the household level, thus advancing the operationalisation of usury vulnerability developed by El-Meouch et al. (2020) and establishing a further discussion on the phenomenon’s operationalisation. On the other hand, it is set out with an aim to explore socio-demographic factors leading to an increased risk of turning to illegal lending. This is relevant for identifying vulnerable groups that might turn to illicit debtors, especially during economic decline and recession, as demonstrated by previous research, and, consequently, formulating relevant social policies and interventions for preventing the problem.

We used the data from the 2008 wave of the European Union Statistics on Income and Living Conditions (EU-SILC) for Italy to achieve our goals. The selected data offers several advantages for the research. Firstly, EU-SILC data include various variables measuring a household’s financial and material well-being along with its socioeconomic position. Secondly, the 2008 wave of the survey contains an additional module on over-indebtedness and financial exclusion – the factors connected to usury vulnerability. Therefore, the data makes it possible to model usury vulnerability and identify the most vulnerable social groups to turn to informal lending.

The paper is structured in the following way. The first section discusses the analytical approaches to studying usury across various disciplines and contextualises the phenomenon in Italy. It is followed by the presentation of the research methodology, which explains the operationalisation of usury vulnerability, the variables included in the data analysis, and the construction of the UVI. Next, the main results of the regression analysis are presented. Finally, the paper discusses the main findings and their applied relevance.

2 Multidisciplinary approaches to studying usury

Research shows that studying usury means dealing with an “invisible crime” (di Gennaro and Marselli 2013). Although economic and legal definitions exist, the usury phenomenon remains under-explored, challenging to interpret, and often underestimated regarding its socio-economic impact. Besides the definitions and the statistical data, the mechanisms that regulate the illegal credit market, the types of relationship between a moneylender and a borrower, and the contextual characteristics that lead an individual to illegal credit seem to be the fundamental aspects for understanding the phenomenon of usury in its entirety. When taken together, these elements can help clarify the discrepancy between the number of registered cases and the perceived high risk of the growing spread of the phenomenon.

2.1 Usury as a legal phenomenon in Italy

Notwithstanding the excellent results obtained in the fight against this crime in the Italian context due to Law 108/1996, usury remains a complex issue, the exploration of which requires the application of multiple indicators and the use of numerous study methodologies. While today it is possible to identify what is usury and what is not, collusive and often hidden exchange systems among the individuals involved in the phenomenon prevent the visibility of most usurious situations to the legal system. Such submersion has two main consequences: on the one hand, it limits the possibility of the complete legal response; on the other hand, it prevents a practical interpretation of the causes, modalities, and mechanisms that govern the usurious relationship itself.

Legally, usury is ascribable to financial crimes and exists in relation to over-indebtedness (Ellison et al. 2006; Glaeser and Scheinkman 1998). In the Italian legal system, over-indebtedness is the persistent imbalance between the obligations assumed and the liquid assets to meet them (D’Alessio and Iezzi 2013). This imbalance is manifested in a definitive or temporary difficulty in fulfilling one’s obligations.

Whether it is an individual or a legal entity, over-indebtedness is a condition leading toward a claim for credit from a third party. The credit may be formal, that is, regulated by a business-type contract, or informal, that is, not regulated by a contract. A loan not governed by a contract does not necessarily constitute illegal credit. However, credit becomes illegal in two cases:

-

a)

when there is the co-presence of informality and the application of a rate: in this case, the absence of a contract does not allow the general taxation to know about the loan and thus to tax its income;

-

b)

when the applied rate exceeds the legal threshold or the principle of equity.

Therefore, it is not the nature of the lender that determines the legality of the loan but rather the fairness of the rate and, where there is the application of a rate, the presence of a contract. For both households and businesses, credit, which involves the payment of interest that does not comply with current regulations, is defined as usurious credit. Law 108/1996 defines the limit above which one faces usurious repayment rates in Italy. Specifically, the usurious rate is that rate which exceeds the average rate charged increased by ¼ + 4% points. In this framework, the Ministry of Economy and Finance issues quarterly the Effective Global Rates, which indicate the applied average rates. In this context, the Italian Law 108/1996 can be defined as a blank rule: it does not make explicit a single threshold rate but refers to a contextual parameter, that is, specific to the moment in which the creditor is operating.

2.2 Usury as an economic phenomenon

The economic literature has focused on the incidence of usury by situating the phenomenon within the financial system. Within the illegal economy and considering the law of supply/demand, the phenomenon of usury, i.e., credit characterised by repayment rates that do not comply with current regulations, is regarded as a parallel credit market (Razzante 2009). Just like the official market, the parallel market is created when the demand for and the supply of financial availability intersect. Unlike the official market, however, loans provide for non-conforming rates and the absence of a contract in the parallel market. In addition to quantifying the usurious rate, the economic literature has focused on analysing the usurious rate in terms of its efficiency from the perspective of the distribution of credit in a given area. For example, Goisis and Parravicini (1999) analyse how, in a legal credit market characterised by information asymmetries, legal credit is granted by virtue of prior behaviour and not based on estimated future solvency. This can lead individuals in need of liquidity to turn to informal or illegal circuits. In this sense, the literature hypothesises how usurious credit may represent a buffer against the problem of restricted access to bank credit due to specific information asymmetries (Crosato and Dalla Pellegrina 2019; Kowalski and Wałęga 2022). Usury, therefore, could perform a service for households and businesses that lack access to bank credit, leading the researchers to assert a lack of a linear link between usury and welfare loss for the community (El-Meouch et al. 2020; Lewison 1999; Spotton Visano 2018).

In addition to the issues of the supply/demand mechanisms and the analysis of the services embedded in the rate, the economics-based scientific literature has been concerned with empirically assessing the spread of the phenomenon on the Italian territory, first and foremost interpreting usury as unmet credit needs (Polin 2009). One of the techniques employed for this type of estimation is data on households denied access to credit or microcredit. Disqualified from the formal credit market, these households have to turn to the informal credit market, with the risk of being involved – more or less consciously – in illegal or usurious circuits.

Along with demand analysis, economic models have focused on calculating usury risk. The calculation of usury risk, also known as the usury risk quotient, is an operation based on a series of territorially based indicators, the interplay of which produces a risk factor for each investigated territory (Sapienza 2013). The indicators are chosen based on empirical evidence concerning the social and economic characteristics of the territories where the phenomenon is most recorded. Within this framework, some authors (Dalla Pellegrina et al. 2004), based on environmental, economic, and financial vulnerability factors, have developed an index of usury risk for all Italian provinces, highlighting the greater spread of the phenomenon in southern Italy. Similarly, regarding similar vulnerability factors such as social, financial, economic, and criminological indicators, a provincial usury risk framework is proposed by Fiasco (2013), confirming the prominence of the phenomenon in the south.

Econometric analysis is another economic tool for assessing usury risk in a given area. In this case, it is not the analysis of indices that produces a risk quotient but rather the detection of the characteristics of the territories that have information regarding the factors that lead to an increase in usury risk. In this sense, Dalla Pellegrina et al. (2004) show a statistically significant positive relationship between provincial employment rate, mafia crimes, and usury. At the same time, there is a negative relationship between the number of bank branches, the number of subsidised loans and usury.

In recent times, economic analysis of the usury phenomenon has focused on two aspects: on the one hand, understanding what actions are most effective to contain and contrast the phenomenon, and on the other hand, understanding new forms of usury, particularly those related to online transactions. Regarding the first aspect, Crosato and Dalla Pellegrina (2011) find that both the streamlining of bankruptcy procedures for businesses and the tightening of sanctions have positive effects on the attempt to curb illegal economic operations concerning the phenomenon of usury. The authors point out that the likelihood of usury is not neutral for a country’s growth path: with uneven growth at the territorial level, the likelihood of usury cases increases as inequality increases. As Goisis and Parravicini (1999, p. 4) point out, the interest rate does not exhaust the objectives of the usurer, who would often aim not only at a relevant remuneration for his loan but also at capturing the victims’ wealth. From the economic point of view, the phenomenon of usury would fit into a system of other crimes perpetrated in most cases by criminal organisations, within which usury is operated for the purpose not of immediate gain but of money laundering. Once again, the charged rate thus proves not entirely effective as an abstract element for identifying and understanding the usury phenomenon and its contemporary developments.

2.3 Usury as a sociological phenomenon

Recently, the usury phenomenon started to be studied from a sociological perspective, focusing on household or individual factors leading to informal lending. Studies show that the victims of usury are more frequently women, young adults, low-income, unemployed, having a lower level of education, dependent on the welfare state, and lacking financial advice (Barth et al. 2015; Charron-Chénier 2018; Distelberg et al. 2009; El-Meouch et al. 2020; Payne et al. 2020; Rowlingson et al. 2016; Saunders 2021; Wilson 2002). Some studies also show that although lower-income people are frequent victims of usury lending, the share of mid-range-income people is also significant among the borrowers (Distelberg et al. 2009; Saunders 2021). Furthermore, some research shows that the inability to cover regular living costs (household bills, car repairs, health expenses, etc.) is among the main reasons for informal borrowing for middle-income groups (El-Meouch et al. 2020; Rowlingson et al. 2016; Saunders 2021).

In Italy, there are also some attempts to consider the phenomenon of usury sociologically, mainly employing a qualitative methodology. Marinaro (2017) shows two usury distinctions in Italy in her research. Firstly, it is highly connected with organised crime, especially in the country’s south. Secondly, small business owners are the main clients of usury, while individuals turn to illegal borrowing less frequently. Basa et al. (2012) investigate the phenomenon of usury among immigrants, more specifically those from the Philippines. Authors demonstrate that immigrants can have a higher level of usury vulnerability, especially if they do not have a reliable network that can provide some financial aid, experience a prolonged over-indebtedness, or have a sudden considerable expense.

The combination of economic aspects (such as the comprehension of the credit market and the role of interest rates), sociological elements (such as the condition of victims, the characteristics of the usury agreement, relational factors in the moneylender/user relationship, and usury strategies) and psychological aspects (such as risk perception) can lead to unified considerations regarding the phenomenon of usury. Macroeconomic quantification data do not appear sufficient to clarify the expansion of usury. Instead, usury takes on a more concrete character once interpreted with a consideration of the existing continuity between the legal and illegal markets in relation to social vulnerability (Spina and Stefanizzi 2007). In this sense, usury does not find justification merely in the interest rate that moneylenders apply but is analysed as a contextual aspect of a panorama of socio-economic relations, within which the role of vulnerability plays a decisive role. Regarding the issue of the social vulnerability of usury victims, Dal Lago and Quadrelli (2003) point out that the weakness of victims can be analysed from two perspectives: on the one hand, the greater vulnerability of some social actors to conditions of economic crisis (mainly migrants); on the other hand, the evolutions of the labour market. Indeed, if we consider the permanent contract as one of the main guarantees in a credit context, the decline of this type of contract makes access to the legal credit market increasingly easy.

Thus, two tensions characterise the usury phenomenon and may determine its evolution over time (Giuffrida and Ciatti 2020). On the one hand, usury has become a social threat, a hierarchical, association-type phenomenon, in most cases connected to mafia crime. In this sense, the power of the illegal credit supply will be able to increase due to the establishment of complex and rooted systems that are already familiar with cooperation with the legal system. On the other hand, the economic crises have accentuated over-indebtedness in general and subsistence over-indebtedness in particular (the keystone of usury) for both households and entrepreneurs. The increase in the strength of networks capable of offering illegal credit, together with the need for individuals to access illegal credit to meet their basic financial needs, characterise the analysis of the contemporary usury phenomenon, highlighting how monitoring and contrasting actions must take on increasingly sophisticated forms and modalities. A continuous and broad understanding of the determinants of the phenomenon, together with the adaptation of monitoring and contrasting tools, thus seems to be the fundamental ways, if not to counter – given the chronic nature of the phenomenon – but at least to understand the phenomenon in the light of its real characteristics and design limitation tools following them.

The current paper considers the progressive impoverishment of households and the resulting indebtedness, which makes the danger of ending up in usurious networks concrete when it assumes unsustainable dimensions. Special attention is paid to the regional differences as the previous studies confirm a greater risk of usury in southern Italy’s regions and provinces (Dalla Pellegrina et al. 2004; Fiasco 2013). Surveying the characteristics of Italian regions, in addition to providing similarities and differences concerning the effects of past economic crises, offers important indications in this regard.

3 Constructing the usury vulnerability index

3.1 Data

Just a few empirical studies try to analyse quantitatively usury vulnerability or risk of usury exposure as a social phenomenon (Charron-Chénier 2018; Ellison et al. 2006; El-Meouch et al. 2020; Saunders 2021). Therefore, this paper uses quantitative analysis to, firstly, attempt to operationalise usury vulnerability to construct the UVI and, secondly, to gain insights into socio-demographic factors that might increase or decrease usury vulnerability, presented in the next section. We use the EU-SILC 2008 cross-sectional User Database for our research as this wave offers rich information on over-indebtedness and financial exclusion. In our analysis, we focus on the case of Italy and the regionalFootnote 1 differences within the country since the previous studies highlight the regional variation in the diffusion of the phenomenon across the country. The sample used for the analysis contains information on 20 928 Italian households, which allows for the comparison of regional groups.

3.2 Usury vulnerability index

Our study aims to construct the UVI; however, there is no commonly agreed indicator for measuring the potential household exposure to informal financial services. Furthermore, just a few studies attempt to estimate quantitatively a share of those vulnerable to usury. For example, El-Meouch et al. (2020) propose to operationalise usury vulnerability through the following indicators: (1) household’s inability to face unexpected financial expenses, (2) household being in arrears on various types of payment, (3) household being in difficulty making ends meet, (4) low subjective income, (5) material deprivation of a household, and (6) an absence of a bank account among the members of a household. These indicators correspond with other studies, focusing on the victims of usury and loan sharking, showing that poor economic conditions and the high financial burden of regular living costs are among the main factors pushing people into illegal borrowing (Rowlingson et al. 2016; Saunders 2021). Access to banking services also influences whether a person turns to usury (Crosato and Dalla Pellegrina 2019; Kowalski and Wałęga 2022). However, El-Meouch and the coauthors (2020) applied equal weights to the abovementioned indicators, which may lead to under- or over-loading of some factors.

The current study is also based on the methodological approach towards constructing a social vulnerability index, specifically an indicator-based approach (Yoon 2012). This approach offers a methodological advantage since it suggests measuring a complex multidimensional phenomenon (social vulnerability) through a set of independent variables by applying principal component analysis (Cutter et al. 2003; Yoon 2012).

Therefore, developing the operationalisation proposed by El-Meouch et al. (2020) and based on the literature on the construction of a social vulnerability index, the current study undertakes the following steps to construct the UVI:

-

1.

selecting indicators;

-

2.

standardising the indicators by converting the values to z-scores since the variables are measured at different scales;

-

3.

detecting multicollinearity among the indicators;

-

4.

performing factor analysis of the selected indicators to calculate the weight of each indicator;

-

5.

calculating the usury vulnerability index.

Based on the empirical evidence discussed earlier and developing El-Meouch et al. (2020) approach, the following variables are used for constructing UVI:

-

Household’s financial capacity: the indicator is the sum of a household’s incapacity to afford a one-week annual holiday away from home, incapacity to afford a meal with meat, chicken, fish (or vegetarian equivalent) every second day, and incapacity to face unexpected financial expenses. Therefore, the indicator takes a value from 0 to 3, where 0 is the most financially capable household, and 3 is the most incapable.

-

Household in arrears: the indicator is the sum of a household in arrears on mortgage/rent, utility bills, hire purchase instalments payments and other non-housing bills. The indicator takes a value from 0 to 4, with 0 not being in arrears and 4 being in arrears the most.

-

Household making ends meet: the indicator takes a value from 1 to 6, where 1 means that a household can make ends meet very easily and 6 – with great difficulty.

-

Household’s housing conditions: the indicator is a sum of not having a toilet, not having a bath/shower in the dwelling, not being able to keep the house warm, and being overcrowded. The indicator takes a value from 0 to 4, where 0 indicates a household not in poor housing conditions and 4 – the poorest housing conditions.

-

Household’s financial burden of total housing costs: the indicators take a value from 1 to 3, where 1 means that total housing costs are not a burden at all and 3 – they are a heavy burden.

-

Household’s access to baking services: the indicator is a sum of not having a current bank account and not having credit cards. Therefore, the indicator takes a value from 0 to 2, where 0 means that a household has access to bank services and 2 – a household does not have any access.

Table 1 presents the frequency distributions of the constructed variables.

The variables are moderately correlated, as shown in Table 2. Applying the > 0.8 rule of thumb (Midi et al. 2010), it is possible to conclude that there is no high multicollinearity. It allows for using the variables in principal component analysis.

Prior to conducting factor analysis, the Kaiser-Meyer-Olkin (KMO) measure of sampling adequacy and Barlett’s Tests of Sphericity were performed. The KMO is 0.757, which means that applying > 0.7 rule of thumb (Sharma 1995), the data are appropriate for factor analysis. Bartlett’s test statistic is highly significant (p < 0.000), showing that the data are suitable for factor analysis.

Varimax rotation was applied to minimise the complexity of the factors by maximising the variance of loadings on each factor. The high extracted communalities (> 0.5), as shown in Table 3, indicate that the extracted factors represent the selected variables well.

Since the aim of factor analysis in this paper is not dimension reduction but the calculation of weights of factors measuring usury vulnerability, the extraction of factors did not rely only on eigenvalues and the scree plot, but also the percentage of variance explained was considered. Thus, the extraction of only one factor, as suggested by eigenvalues (see Table 4), would mean that only 43% of the variance is explained, which is lower than the generally acceptable threshold of 60% (Hair et al. 2014). Given that factors 2, 3, and 4 have close values of the percentage of variance explained (15.4%, 14.8%, and 12.6%, respectively), it was decided to extract four factors. Therefore, the extracted four common factors explain 86% of the variance of usury vulnerability.

The extracted factors are (1) household financial abilities, (2) access to banking services, (3) household housing conditions, and (4) being in arrears (Table 5). The extracted factors account for 29%, 20%, 19%, and 18% of the total explained variance.

There is no agreed methodology for assigning weights in constructing indices as authors suggest various approaches: equal weights (Cutter et al. 2003), Pareto ranking (Rygel et al. 2006), and weighting according to the contribution to the total variance explained (Wood et al. 2010). The UVI is constructed by weighing each factor score with its percentage of variance explained divided by the total variance explained by all extracted common factors. Therefore, the factor with a higher explained variance contributes more to the usury vulnerability score.

Based on this approach, the index calculation formula is the following:

The analysis shows that the UVI scores range from 2.07 (highly vulnerable) to -1.11 (least vulnerable). The previous studies provide empirical evidence that Italy has regional differences in financial well-being and socio-demographic conditions as well as the level of the risk of exposure to usury (Barone 2018; Dalla Pellegrina et al. 2004; Fiasco 2011, 2013). Table 6 also demonstrates it by highlighting regional variances in usury vulnerability. Thus, the mean values of the UVI in the northern and central regions are lower than in the south and islands, indicating a higher risk of usury exposure in the south of the country.

4 Regression analysis: predictors, estimation method, and results

4.1 Predictors

As discussed earlier, micro-level factors for identifying a household’s exposure to usury are highly relevant. Therefore, based on the literature review and previous empirical studies, we created a set of hypotheses on the relationship between the socio-demographic characteristics of a household and usury vulnerability. First, the empirical evidence suggests that households with only one parent and those with three or more children are more likely to lack financial resources (Charron-Chénier 2018; Durst 2015; Neuberger and Reifner 2020; Stamp 2009). Therefore, we hypothesise that such families should have higher levels of vulnerability to usury. Second, following empirical evidence, we suggest that households with a top earner with higher levels of education are at a lower risk of turning to informal debtors (Barth et al. 2015; Charron-Chénier 2018; Gosztonyi and Havran 2021; Neuberger and Reifner 2020; Stamp 2009). Third, we suspect that households with a female top earner have higher levels of usury vulnerability. Previous studies show that households with a male top earner experience financial distress less frequently than those with a female top earner (Kubrin et al. 2011; Mayer 2013; Saunders 2021; Waglé 2008). Fourth, we assume that usury vulnerability decreases with the age of the top earner. The rationale for this assumption is that income usually increases with age; therefore, older people experience financial difficulties less frequently (Barth et al. 2015; Stamp 2009). Fifth, we added two hypotheses to the analysis based on the previous studies showing that employment status and the type of work contract are important determiners of experiencing financial strain (Charron-Chénier 2018; Rowlingson et al. 2016; Saunders 2021; Stamp 2009). Thus, we suggest that households in which a top earner is employed are at lower risk of usury exposure and households with a top earner having a permanent employment contract in contrast with those with an unemployed top earner or the one with a temporary contract, respectively. Lastly, following the evidence that foreign-born people face financial strain with a higher probability than those native to the country (Basa et al. 2012; Waglé 2008), we suppose that immigrants from outside the European Union have higher levels of usury vulnerability.

Table 6 demonstrates regional differences in household structures as, in the southern and island parts of Italy, there are fewer single-person households and more households with two adults and two or more children than in the north of the country. The regional differences can also be seen in the top earner’s highest level of education, sex, activity status, employment conditions, and country of birth.

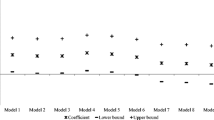

This study calculates a model of usury vulnerability for the whole country, including indicators of the regional location of a household (Model 1). However, given the regional differences highlighted by previous empirical studies and the descriptive statistics, a model for each region is also calculated to check for eventual variations (Models 2–6).

4.2 Regression analysis results

Given that the constructed for this research dependent variable is continuous, we employ multiple linear regression (Freedman 2009). Table 7 presents the summary of the regression estimations. For Model 1, regional variables are included in the model to check for regional-level differences. The estimation results reveal that all the predictors included in the analysis have a statistically significant relationship with the usury vulnerability.

Factors measuring a top earner’s level of education, age, employment status, place of birth, and region of living appear to predict the usury vulnerability to a greater extent. More specifically, as expected, households with an unemployed or inactive top earner have a higher chance of being exposed to illegal debt. Therefore, the model indicates that work precarity is among the factors that might increase the chances of turning to illicit debt, which is in line with the previous research on the victims of usury (Barth et al. 2015; Payne et al. 2020; Rowlingson et al. 2016; Saunders 2021). In addition, confirming previous studies on usury vulnerability and financial capacity (Basa et al. 2012; Waglé 2008), if a top earner comes from outside the EU, the household may experience greater levels of usury vulnerability. Regarding a household’s location in Italy, the estimation results, aligning with previous research on usury in the country (Barone 2018; Dalla Pellegrina et al. 2004; Fiasco 2011, 2013), show that if it is located in the south or on the islands, its vulnerability to unofficial lending increases. The situation is reversed if a household is located in the country’s northern regions.

In contrast, households the head of which has a higher level of education are less prone to be at risk of usury, which is in line with previous studies (Barth et al. 2015; Charron-Chénier 2018; Gosztonyi and Havran 2021; Neuberger and Reifner 2020; Stamp 2009). The data also show that usury vulnerability decreases with age, suggesting additional evidence that income increases with age, which prevents people from turning to usury (Barth et al. 2018; Stamp 2009).

Additionally, the sex of the top earner matters in terms of usury vulnerability, as shown by the regression analysis. Thus, the chances of usury vulnerability increase when a household has a female top earner. Again, the previous studies on the victims of usury show the same results by highlighting a gender gap in terms of taking an illegal debt (Payne et al. 2020; Saunders 2021; Wilson 2002).

The hypothesis that a household’s structure impacts usury vulnerability is also confirmed, as demonstrated by Model 1. In particular, households in which both adults are of economically active age and do not have dependent children have lower values of the UVI. Contrarily to it, households with dependent children, especially single parents and those with three or more children, have a higher level of usury vulnerability, as it could be suggested by previous analysis of the financial resources of households (Charron-Chénier 2018; Durst 2015; Neuberger and Reifner 2020; Stamp 2009).

As to the regional differences, Models 2–6 indicate that although, in general, they follow the country’s pattern, there are some regional-level specificities. For example, the estimation results show that the top earner’s sex is a relevant predictor of usury vulnerability in northern and central Italy. At the same time, it is not statistically significant in the southern part of the country. It might be ascribable to the fact that women are top earners less frequently in the southern regions than in the rest of Italy (Segato 2021); therefore, they may have more obstructed access to the employment market.

The regression analysis shows similar results for the EU provenance of a top earner: it is a relevant predictor for usury vulnerability in the north and centre of Italy and not statistically significant in the southern regions. It might be attributed to the fact that more affluent northern and central regions attract more immigrants than the south of the country. Therefore, they might experience higher competition or accept lower-paid jobs, increasing their financial vulnerability and nudging them into usury.

Interestingly, it seems that an increase in age lowers the usury vulnerability only in the northern Italian regions, especially in the north-east. It could indicate that the rise in income follows the age in more affluent and economically developed regions of Italy, while there is no such direct relationship in other regions.

5 Discussion and conclusions

The phenomena of risk of usury and usury vulnerability have recently gotten into the spotlight of sociological research. Consequently, there are just a few attempts at operationalising usury vulnerability and quantitative analysis of possible factors impacting it. The current study was set out to fill in the current methodological gap in the literature and had two main objectives. Firstly, it aimed to contribute to operationalising usury vulnerability and constructing a measurement for the phenomenon. Secondly, it was designed to determine what micro-level factors impact usury vulnerability, employing regression analysis.

The present study builds on the previous attempts to measure usury vulnerability, social vulnerability index literature, and studies on the victims of usury (Crosato and Dalla Pellegrina 2019; El-Meouch et al. 2020; Kowalski and Wałęga 2022; Rowlingson et al. 2016; Saunders 2021) and proposes an index of usury vulnerability at a household level. It is constructed based on indicators measuring a household’s financial abilities, access to banking services, housing conditions, and being in arrears. Previous research shows that these factors are among the main ones to push people into illegal debt. The results of this part of the analysis correspond to other attempts to estimate the diffusion of the phenomenon of usury in Italy, showing higher levels of usury vulnerability in the southern regions of the country (Barone 2018; Dalla Pellegrina et al. 2004; Fiasco 2011, 2013).

As to the impact of the socio-demographic position of a household, the current analysis has demonstrated that the top earner’s age, sex, origins, education and employment status, household type and location in the country are relevant predictors for usury vulnerability. These findings align with previous research on usury vulnerability in other countries, thus confirming quantitatively the relevance of socio-demographic factors for understanding usury vulnerability, demonstrated previously mainly in qualitative studies (Basa et al. 2012; Littwin 2008; Marinaro 2017; Rowlingson et al. 2016).

The findings of the undertaken study can be used as a means for identifying potential points of policy intervention. Specifically, the results of the proposed model of usury vulnerability, estimated in relation to the Italian case, besides showing families’ exposure to turning to illegal debt, bring to light the indicators of financial vulnerability that might aggravate during an economic crisis. The rise of usury permeability could be alarming due to as a possible lack of liquidity as the activity of organised crime in the field of usury (at least in the case of Italy) seeking to profit from the situation of economic emergency by providing illegal loans. Therefore, a possible social policy direction could be periodic monitoring of the proposed indicators, in particular in reference to the categories at higher risk of turning to usury (unemployed, those having precarious working conditions, single parents, etc.).

The study has several limitations that could be addressed by future research. One of the significant limitations is using the 2008 EU SILC data, which makes it hard to draw a connection to the present situation. Therefore, future studies may aim to conduct similar surveys, paying attention to over-indebtedness, access to banking services, and financial hardship of households. Furthermore, the study focuses on the Italian case, and, therefore, the results might reflect only the reality of the studied country in the surveyed period, while some adjustments might be needed when analysing another country or period.

Additionally, this study focuses on sociological elements of usury vulnerability, while there are also economic and psychological aspects. Therefore, future research could be undertaken to develop further a more comprehensive operationalisation of usury vulnerability and of the index, which is especially pertinent given that usury poses a social risk that is still vastly understudied.

Lastly, further research could be undertaken to understand better which other micro- and macro-level factors explain usury vulnerability. Therefore, it might be helpful to consider including variables accounting for socio-economic conditions (for example, number of currently working firms, firm closure rate, number of bank branches, etc.) as it might deepen the understanding of the vulnerability to turn to unofficial lending. It could be achieved by applying multi-level analysis, which allows for studying the interplay of micro- and macro-level factors, bringing important insights about the phenomenon to light.

Notes

For comparison, regions are united into larger geographical groups: north-west (Liguria, Lombardy, Piedmont, Valle d’Aosta), north-east (Emilia-Romagna, Friuli-Venezia-Giulia, Trentino-Alto Adige/Südtirol, Veneto), centre (Lazio, Marche, Tuscany, Umbria), south (Abruzzo, Basilicata, Calabria, Campania, Molise, Puglia), and islands (Sardinia, Sicily).

References

Barone, R.: The Italian CCB reform and usury credit risk: A quantitative analysis. Italian Economic Journal. 4, 463–496 (2018)

Barth, J.R., Hilliard, J., Jahera, J.S.: Banks and payday lenders: Friends or foes? Int. Adv. Econ. Res. 21(2), 139–153 (2015)

Basa, C., de Guzman, V., Marchetti, S.: International migration and over-indebtedness: The case of Filipino workers in Italy. Human Settlements Working Paper №36. International Institute for Environment and Development, London (2012)

Charron-Chénier, R.: Payday loans and household spending: How access to payday lending shapes the racial consumption gap. Soc. Sci. Res. 76, 40–54 (2018)

Crosato, L., dalla Pellegrina, L.: Safe credit to the poor: The role of anti-usury policies. Dev. Policy Rev. 37(3), 423–449 (2019)

Crosato, L., dalla, Pellegrina, L.: Improving bankruptcy proceedings or strengthening sanctions? An assessment on anti-usury policies. CLEA 2008 Meetings Paper, 2008–30. Paolo Baffi Centre on Central Banking and Financial Regulation, Milano (2011)

Cutter, S.L., Boruff, B.J., Shirley, W.L.: Social vulnerability to environmental hazards. Soc. Sci. Q. 84(2), 242–261 (2003)

D’Alessio, G., Iezzi, S.: Household over-indebtedness: Definition and measurement with Italian data. In: Statistical Issues and Activities in a Changing Environment: Proceedings of the Sixth IFC Conference, Basel, 28–29 August 2012, pp. 496–517. Bank for International Settlements, Basel (2013)

Dal Lago, A., Emilio Quadrelli, E.: La città E Le Ombre: Crimini, Criminali, Cittadini. Feltrinelli, Milano (2003)

Dalla Pellegrina, L., Macis, G., Manera, M., Masciandaro, M.: Il Rischio Usura Nelle Province Italiane. Ministero delle Finanze. Istituto Poligrafico e Zecca dello Stato, Roma (2004)

di Gennaro, G., Marselli, R.: Access-to-credit and the rate of victimization in an entrepreneurial community. Sociol. Study. 3(10), 781–793 (2013)

Distelberg, B., Mcelroy, J., Weir, G.R.: Explorative study of payday lending: A human ecology evaluation. J. Personal Finance. 8, 79–106 (2009)

Durst, J.: Juggling with debts, moneylenders and local petty monarchs: Banking the unbanked in shanty-villages in Hungary. Rev. Sociol. 25(4), 30–57 (2015)

El-Meouch, N.M., Fellner, Z., Marosi, A., Szabó, B., Urbán, Á.: An estimation of the magnitude and spatial distribution of usury lending. Financial and Economic Review. 19(2), 107–132 (2020)

Ellison, A., Collard, S., Forster, R.: Illegal lending in the UK: Research report. In: URN 06/1883. Personal Finance Research Centre, Bristol (2006)

Fiasco, M.: Credito Illegale E Indebitamento Patologico a Roma tra imprese a Famiglie Produttrici. Camera di Commercio di Roma, Roma (2011)

Fiasco, M.: Indebitamento Patologico e Credito Illegale Nella Crisi Attuale. Dimensioni Del Rischio E Prospettive per Imprese e Famiglie. Camera di Commercio di Roma, Roma (2013)

Freedman, D.A.: Statistical Models: Theory and Practice. Revised edition. Cambridge University Press, New York (2009)

Giuffrida, S., Ciatti, L.: La Mano Nera. L’usura Raccontata Da Chi è Caduto Nelle Mani Di Strozzini E clan. Infinito, Castel Gandolfo (2020)

Glaeser, E.L., Scheinkman, J.: Neither a borrower not a lender be: An economic analysis of interest restrictions and usury laws. J. Law Econ. XLI, 1–36 (1998)

Gosztonyi, M., Havran, D.: Highways to hell? Paths towards the formal financial exclusion: Empirical lessons of the households from northern Hungary. Eur. J. Dev. Res. (2021)

Hair, J., Black, W., Babin, B., Anderson, R.: Multivariate data Analysis, 7th edn. Pearson Prentice Hall, Uppersaddle River (2014)

Kowalski, R., Wałęga, G.: Regulation of usury: Justification, consequences, and some lessons from Polish experience. Gospodarka Narodowa. 310(2), 57–73 (2022)

Kubrin, C.E., Squires, G.D., Graves, S.M., Ousey, G.C.: Does fringe banking exacerbate neighborhood crime rates? Criminol. Public Policy. 10(2), 437–466 (2011)

Lavorgna, A., Sergi, A.: Types of organised crime in Italy. The multifaceted spectrum of Italian criminal associations and their different attitudes in the financial crisis and in the use of internet technologies. Int. J. Law Crime Justice XX, 1–17 (2013)

Lewison, M.: Conflicts of interest? The ethics of usury. J. Bus. Ethics. 22(4), 327–339 (1999)

Littwin, A.: Preference among low-income consumers. Tex. Law Rev. 86(3), 451–506 (2008)

Marinaro, I.C.: Loan-sharking in a time of crisis: Lessons from Rome’s illegal credit market. Trends in Organized Crime. 20(1–2), 196–215 (2017)

Mayer, R.: When and why usury should be prohibited. J. Bus. Ethics. 116(3), 513–527 (2013)

Midi, H., Sarkar, S.K., Rana, S.: Collinearity diagnostics of binary logistic regression model. J. Interdisciplinary Math. 13(3), 253–267 (2010)

Neuberger, D., Reifner, U.: Systemic usury and the European Consumer Credit Directive. Vierteljahrshefte Zur Wirtschaftsforschung. 89(1), 115–132 (2020)

Payne, B., Murray, C., Morrow, D., Byrne, J.: Illegal Money Lending and debt Project: Research Report of Findings. Ulster University, Ulster (2020)

Polin, V.: I mercati Del Microcredito: Tendenze internazionali e caso italiano: Una Rassegna. Rivista Internazionale Di Scienze Sociali. 117(1), 135–168 (2009)

Razzante, R.: L’usura Nell’economia e nell’ordinamento giuridico. Gnosis – Rivista Italiana Di Intelligence. 15(3), 53–63 (2009)

Rowlingson, K., Appleyard, L., Gardner, J.: Payday lending in the UK: The regul(aris)ation of a necessary evil? J. Social Policy. 45(3), 527–543 (2016)

Rygel, L., O’Sullivan, D., Yarnal, B.: A method for constructing a social vulnerability index: An application to hurricane storm surges in a developed country. Mitig. Adapt. Strat. Glob. Change. 11, 741–764 (2006)

Sapienza, E.: Usura ed estorsione nel mezzogiorno: Una Stima delle determinanti. Stud. Econ. 109, 45–67 (2013)

Saunders, P.: Loan sharking: Changing patterns in, and challenging perceptions of, an abuse of deprivation. J. Public Health. 43(1), 62–68 (2021)

Segato, F.: Female Labour Force Participation and Household Income Inequality in Italy. MPRA Paper №108280, Munich (2021)

Sharma, S.: Applied Multivariate Techniques. Wiley, New York (1995)

Spina, S.,Stefanizzi, S.: L’usura: Un servizio illegale offerto dalla città legale. Bruno Mandadori, Milano (2007)

Spotton Visano, B.: Mainstream financial institution alternatives to the payday loans. In: Buckland, J., Robinson, C., Spotton Visano, C., B. (eds.) Payday Lending in Canada in a Global Context, pp. 147–175. Springer International Publishing, Cham (2018)

Stamp, S.: A Policy Framework for Addressing over-indebtedness. Combat Poverty Agency, Dublin (2009)

Waglé, U.R.: Multidimensional poverty: An alternative measurement approach for the United States? Soc. Sci. Res. 37(2), 559–580 (2008)

Wilson, D.: Payday lending in Victoria - a research report. Consumer Law Centre Victoria Ltd, Melbourne (2002). (2002)

Wood, N.J., Burton, C.G., Cutter, S.L.: Community variations in social vulnerability to Cascadia-related tsunamis in the U.S. Pacific Northwest. Nat. Hazards. 52, 369–389 (2010)

Yoon, D.K.: Assessment of social vulnerability to natural disasters: A comparative study. Nat. Hazards. 63, 823–843 (2012)

Funding

Open access funding provided by Università degli Studi di Milano - Bicocca within the CRUI-CARE Agreement. The authors did not receive support from any organization for the submitted work.

Open access funding provided by Università degli Studi di Milano - Bicocca within the CRUI-CARE Agreement.

Ethics declarations

Conflict of interest

The authors have no relevant financial or non-financial interests to disclose.

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Stefanizzi, S., Lysova, T. Usury vulnerability: measuring and modelling the phenomenon in Italy. Qual Quant (2024). https://doi.org/10.1007/s11135-024-01841-w

Accepted:

Published:

DOI: https://doi.org/10.1007/s11135-024-01841-w