Abstract

This paper aims to shed some light on the way lay consumers forecast by comparing survey expectations on two different—but linked—fundamentals. Specifically, we study the central tendencies and cross-sectional dispersions of predictions on individual-level and aggregate income dynamics. The proposed joint analysis highlights several interesting outcomes. Agents’ predictions on micro and macroeconomic evolutions do not drift apart despite (possibly composite) shocks have permanent effects on expectations. When shocks create a gap between the two expectations, in fact, individuals revise only forecasts about GDP dynamics. Otherwise stated, predictions on personal stances are much stickier. With respect to these latter, then, expectations on aggregate dynamics overreact to shocks and, amazingly from an objective standpoint, they are systematically bleaker. As per second moments evidence shows, in sharp contrast with the typical assumption maintained in the macroeconomic literature, that disagreement among agents is persistently high. Moreover, the comparison makes astonishingly clear that when predicting the same macro fundamental the consensus is even lower. Finally, our setting allows testing whether cross sectional disagreement and time series volatility in expectations are equal.

Similar content being viewed by others

Notes

Consumers survey data for Italy are available since 1985. Unfortunately, since January 1995 were implemented several crucial changes in the way surveys were performed. These refer to the approach to the interviewed (from direct interview to CATI), to the statistical unit (from household to consumer), and to the sample methodology. All that split the whole sample in two relatively heterogeneous parts. Hence, more reliable results can be obtained starting in 1995 (preliminary evidence based on the larger sample gives support to the reported results).

In the main text are reported the exact translation from Italian of the queries actually faced by Italian responders (Dom8 and Dom2 of the Manual downloadable from http://ec.europa.eu/economy_finance/db_indicators/surveys/documents/questionnaires/questionnaires_it_cons_en.pdf). They are not perfectly coincident with what described (Q2 and Q4, page 39) in the European Commission Users’ Manual (2014). Evidently, what is important is what the respondent actually faces.

Possibly, it is a “non response”, i.e. it is not the outcome of an explicit elaboration but, rather, a declaration of no information. In this regard, the European Commission Users’ Manual (2007, p. 18) states that: “(…) there are six reply options: five “real” ones and a ‘do not know’ option”.

For robustness check in Appendix B we use another procedure to compute the dispersion in expectations.

A recent strand of the macroeconomic literature is working on overconfidence (e.g., Jaimovich and Rebelo 2006).

Bovi (2009) collects evidence on that at European level.

Mankiw and Reis (2007) find that about a fifth of workers and consumers update their information sets every quarter, so the mean information lag for both household members is approximately five quarters. By contrast, firms are estimated to be much better informed when setting prices: About two-thirds update their information set every quarter.

Basically, the Engle and Granger’ s representation theorem (Engle and Granger 1987) states that, provided that two time series are cointegrated, the short-term disequilibrium relationship between them can always be expressed in the error correction form. In Sect. 3 we have explained why we add only a constant in the cointegrating Eqs. (4.6) and (4.7).

Unreported tests confirm that, as expected, the deterministic trend in not significant.

We have performed the Geweke’s instantaneous feedback test and we have verified that, unsurprisingly, the VECM residual correlation matrix is not diagonal. Results are available upon request.

Cfr. Pesaran and Weale (2006).

They are available upon request.

References

Anderson, O.: The Business Test of the Ifo-institute for Economic Research, Munich, and Its Theoretical Model. Revue de l'Institut International de Statistique/Review of the International Statistical Institute. 20(1), 1–17 (1952)

Bachmann, R., Elstner, S., Sims, E.: Uncertainty and Economic Activity: Evidence from Business Survey Data. Am. Econ. J. Macroecon. 5, 217–249 (2013)

Badarinza, C., Buchmann, M.: Inflation Perceptions and Expectations in the Euro Area—The Role of News. ECB Working Paper 1088 (2009)

Batchelor, R.A.: Quantitative v. qualitative measures of inflation expectations. Oxford Bull. Econ. Stat. 48, 99–120 (1986)

Batchelor, R.A., Orr, A.B.: Inflation expectations revisited. Economica 55, 317–331 (1988)

Baron, J.: Thinking and Deciding, 4th edn. Cambridge University Press, New York (2007)

Berk, J.M.: Measuring inflation expectations: a survey data approach. Appl. Econ. 31, 1467–1480 (1999)

Bertrand, M., Mullainathan, S.: Do people mean what they say? Implications for subjective survey data. Am. Econ. Rev. 91(2), 67–72 (2001)

Bovi, M.: Economic versus psychological forecasting. Evidence from consumer confidence surveys. J. Econ. Psychol. 30(4), 563–574 (2009)

Bovi, M.: Are the representative agent’s beliefs based on efficient econometric models? J. Econ. Dyn. Control 37, 633–648 (2013)

Buckle, R.A., Meads, C.S.: How do firms react to surprising changes to demand? A vector autoregressive analysis using business survey data. Oxford Bull. Econ. Stat. 53(4), 451–466 (1991)

Capistrán, C., Timmermann, A.G.: Disagreement and biases in inflation expectations. J. Money Credit Bank. 41(2–3), 365–396 (2009)

Carlson, J.A., Parkin, M.: Inflation expectations. Economica 42, 123–138 (1975)

Carroll, C.D.: How does future income affect current consumption? Q. J. Econ. 109(1), 111–147 (1994)

Cavaliere, G., Xu, F.: Testing for unit roots in bounded time series. J. Econom. 178, 259–272 (2013)

Caballero, R.J.: Earnings Uncertainty, Precautionary Savings and Aggregate Wealth Accumulation. Columbia University Discussion Papers, 1990_26, Department of Economics (1990)

Clements, M.P., Hendry, D.F. (eds.): The Oxford Handbook of Economic Forecasting. Oxford University Press, Oxford (2011)

Dasgupta, S., Lahiri, K.: A comparative study of alternative methods of quantifying qualitative survey responses using NAPM data. J. Bus. Econ. Stat. 10, 391–400 (1992)

de Bruin, W.B., Manski, C.F., Topa, G., van der Klaauw, W.: Measuring consumer uncertainty about future inflation. J. Appl. Econom. 26, 454–478 (2011)

Della Vigna, S.: Psychology and Economics: Evidence from the Field. J. Econ. Lit. 47(2), 315–372 (2009)

Dominitz, J., Manski, C.F.: Eliciting student expectations of the returns to schooling. J. Hum. Resour. 31(1), 1–26 (1996)

Doms, M., Morin, N.: Consumer Sentiment, the Economy, and the News Media, Finance and Economics Discussion Series, vol. 51. Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, DC (2004)

Driver, C., Urga, G.: Transforming qualitative survey data: comparisons for the UK. Oxford Bull. Econ. Stat. 66(1), 71–89 (2004)

Engle, Robert F., Granger, C.W.J.: Co-integration and error correction: representation, estimation, and testing. Econometrica 55, 251–276 (1987)

European Commission: The Joint Harmonised EU Programme of Business and Consumer Surveys, User Guide. European Commission. Directorate General for Economic and Financial Affairs (2007)

European Commission: The Joint Harmonised EU Programme of Business and Consumer Surveys, User Guide. European Commission. Directorate General for Economic and Financial Affairs (2014)

Elliott, G., Rothenberg, T.J., Stock, J.H.: Efficient tests for an autoregressive unit root. Econometrica 64, 813–836 (1996)

Evans, G., Honkapohja, S.: Learning as a Rational Foundation for Macroeconomics and Finance. In: Frydman, R., Phelps, E. (eds.) Rethinking Expectations: The Way Forward for Macroeconomics. Princeton University Press, Princeton (2013)

Frydman, R., Phelps, E.S. (eds.): Rethinking Expectations: The Way Forward for Macroeconomics. Princeton University Press, Princeton (2013)

Fullone, F., Gamba, M., Giovannini, E., Malgarini, M.: What do citizens know about statistics? The results of an OECD/ISAE survey on Italian consumers. In Statistics, Knowledge and Policy 2007: Measuring and Fostering the Progress of Societies, OECD, Paris (2008)

Galì, J., Monacelli, T.: Optimal monetary and fiscal policy in a currency union. J. Int. Econ. 76(1), 116–132 (2008)

Granger, C.W.J.: Some thoughts on the development of cointegration. J. Econ. 158(1), 3–6 (2010)

Guvenen, F.: Macroeconomics With Heterogeneity: A Practical Guide. NBER Working Paper, 17622 (2011)

Hall, R.E., Mishkin, F.S.: The sensitivity of consumption to transitory income: estimates from panel data on households. Econometrica 50(2), 461–481 (1982)

Hayashi, F.: Econometrics. Princeton University Press, Econometrics (2000)

Hendry, D.F., Juselius, K.: Explaining cointegration analysis: part II. Energy J. 22, 75–120 (2001)

Hommes, C.: Heterogeneous agent models in economics and finance. In: Judd, K.L., Tesfatsion, L. (eds.) Handbook of Computational Economics, vol. 2. Agent-Based Computational Economics (2006)

Jaimovich, N., Rebelo, S.T.: Behavioural Theories of the Business Cycle. CEPR Discussion Paper 5909 (2006)

Johansen, S.: Likelihood-based Inference in Cointegrated Vector Autoregressive Models. Oxford University Press, Oxford (1995)

Kapteyn, A., Kleinjans, K., Van Soest, A.: Intertemporal consumption with directly measured welfare functions and subjective expectations. J. Econ. Behav. Organ. 72(1), 425–437 (2009)

Krueger, K., Perri, F., Pistaferri, L., Violante, G.L.: Cross sectional facts for macroeconomists. Rev. Econ. Dyn. 13(1), 1–14 (2010)

Lacy, M.G.: An explained variation measure for ordinal response models with comparisons to other ordinal R2 measures. Sociol. Methods Res. 34, 469–520 (2006)

Lahiri, K., Sheng, X.: Measuring forecast uncertainty by disagreement: the missing link. J. Appl. Econom. 25, 514–538 (2010)

Lucas, R.E.: Some international evidence on output-inflation trade-offs. Am. Econ. Rev. 63, 326–334 (1973)

Ludvigson, S.: Consumer confidence and consumer spending. J. Econ. Perspect. 18, 29–50 (2004)

Maag, T.: On the Accuracy of the Probability Method for Quantifying Beliefs about Inflation. Working papers, KOF Swiss Economic Institute, ETH Zurich, 09-230 (2009)

Mankiw, N.G., Reis, R.: Sticky information in general equilibrium. J. Eur. Econ. Assoc. 5(2–3), 603–613 (2007)

Mankiw, N.G., Wolfers, J., Reis, R.: Disagreement about inflation expectations. NBER Macroecon. Annu. 18, 209–248 (2003)

MacKinnon, J.G., Haug, A., Michelis, A.: Numerical distribution functions of likelihood ratio tests for cointegration. J. Appl. Econom. 4(5), 563–577 (1999)

Morris, S., Shin, H.S.: Social value of public information. Am. Econ. Rev. 92(5), 1521–1534 (2002)

Nardo, M.: The quantification of qualitative survey data: a critical assessment. J. Econ. Surv. 17, 645–668 (2003)

Ng, S., Perron, P.: lag length selection and the construction of unit root tests with good size and power. Econometrica 69(6), 1519–1554 (2001)

Orphanides, A., D’Amico, S.: Uncertainty and Disagreement in Economic Forecasting. Finance and Economics Discussion Series, Board of Governors of the Federal Reserve System (2008)

Papacostas S.: Special eurobarometer: European knowledge on economical indicators. In: Statistics, Knowledge and Policy 2007: Measuring and Fostering the Progress of Societies, OECD, Paris (2008)

Pesaran, M.H.: The Limits to Rational Expectations. Basic Blackwell, Oxford (1987)

Pesaran, M.H., Weale, M.: Survey Expectations. Handbook of Economic Forecasting. Elsevier, Amsterdam (2006)

Pohl, R.F.: Cognitive Illusions: A Handbook on Fallacies and Biases in Thinking, Judgment and Memory. Psychology Press, Hove (2004)

Reis, R.: Inattentive Consumers. J. Monet. Econ. 53(8), 1761–1800 (2006)

Rich, R., Tracy, J.: The relationship among expected inflation, disagreement, and uncertainty: evidence from matched point and density forecasts. Rev. Econ. Stat. 92, 200–207 (2010)

Rich, R., Song, J., Tracey, J.: The Measurement and Behavior of Uncertainty: Evidence from the ECB Survey of Professional Forecasters. Federal Reserve Bank of New York Staff Report No. 588 (2012)

Rossi, B., Sekhposyan, T.: Macroeconomic uncertainty indices based on nowcast and forecast error distributions. Am. Econ. Rev. 105, 650–655 (2015)

Sims, C.: Implications of rational inattention. J. Mon. Econ. 50, 665–690 (2003)

Skinner, J.: Risky income, life cycle consumption, and precautionary savings. J. Monet. Econ. 22(2), 237–255 (1988)

Smith, J., McAleer, M.: Alternative procedures for converting qualitative response data to quantitative expectations: an application to australian manufacturing. J. Appl. Econom. 10, 165–185 (1995)

Theil, H.: On the shape of micro-variables and the munich business test. Revue de l’Institut International de Statistique 20, 105–120 (1952)

Tversky, A., Kahneman, T.: Judgment under uncertainty: heuristics and biases. Science 185(4157), 1124–1131 (1974)

Zarnowitz, V., Lambros, L.A.: Consensus and uncertainty in economic prediction. J. Polit. Econ. 95, 591–621 (1987)

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix 1: Robustness check. VECM recursive estimations

We re-write here the long-run relationships shown in Sect. 4 for two generic variables, x i,t and x t :

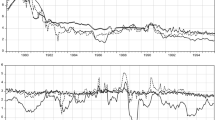

Figure 6 collects the recursive coefficients of Eqs. (7.1) and (7.2) referring to the central tendencies, i.e., whereas \( x_{it} =\,_{t - h} y_{it}^{e} \) and \( x_{t} =\,_{t - h} y_{t}^{e} \). Alike, Fig. 7 reports the recursive coefficients of Eqs. (7.1) and (7.2) referring to the two signal to noise ratios, i.e., whereas \( x_{it} = \;_{t - h} y_{it}^{e} /\upsigma_{it}^{e} \) and \( x_{t} = \;_{t - h} y_{t}^{e} /\upsigma_{t}^{e} \).

Recursive VECM coefficients. Central tendencies. In the figure are reported the recursive coefficients of the VECM (cf. Sect. 4, Eqs. 4.6 and 4.7): \( _{t - h} y_{it}^{e} -\,_{t - h} y_{it - 1}^{e} = \updelta_{\text{i}} \left( {_{t - h} y_{it - 1}^{e} + \upbeta_{t - h} y_{t - 1}^{e} + \uptheta } \right) \); \( _{t - h} y_{t}^{e} -\,_{t - h} y_{t - 1}^{e} = \updelta \left( {_{t - h} y_{it - 1}^{e} + \upbeta_{t - h} y_{it - 1}^{e} = \uptheta } \right) \). \( _{t - h} y_{it}^{e} \) is the central tendency of the responses to the query “How do you expect the economic situation in your household to change over the next 12 months?” \( _{t - h} y_{t}^{e} \) is the central tendency of the responses to the query “How do you expect the general economic situation in the country to develop over the next 12 months?”. Data for Italy. The recursions start estimating the VECM from January 1995 to January 2005, we then add a month each new estimation (last sample: Jan. 1995–Jul. 2013)

Recursive VECM coefficients. Signal-to-noise ratios. Note. In the figure are reported the recursive coefficients of the VECM: \( _{t - h} SNR_{it}^{e} -\,_{t - h} SNR_{it - 1}^{e} = \updelta_{i} \left( {_{t - h} SNR_{it - 1}^{e} + \upbeta_{t - h} SNR_{t - 1}^{e} + \uptheta } \right) \); \( _{t - h} SNR_{t}^{e} -\,_{t - h} SNR_{t - 1}^{e} = \updelta \left( {_{t - h} SNR_{it - 1}^{e} + \upbeta_{t - h} SNR_{t - 1}^{e} + \uptheta } \right) \). \( _{t - h} SNR_{it}^{e} \equiv ({{_{t - h} y_{it}^{e} } \mathord{\left/ {\vphantom {{_{t - h} y_{it}^{e} } {\upsigma_{it}^{e} }}} \right. \kern-0pt} {\upsigma_{it}^{e} }}) \) is the signal-to-noise ratio referring to the query “How do you expect the economic situation in your household to change over the next 12 months?” \( _{t - h} SNR_{t - 1}^{e} \equiv ({{_{t - h} y_{t}^{e} } \mathord{\left/ {\vphantom {{_{t - h} y_{t}^{e} } {\upsigma_{t}^{e} }}} \right. \kern-0pt} {\upsigma_{t}^{e} }}) \) is the signal-to-noise ratio referring to the query “How do you expect the general economic situation in the country to develop over the next 12 months?”. Data for Italy. The recursions start estimating the VECM from January 1995 to January 2005 and then add a month each new estimation (last sample: Jan. 1995–Jul. 2013). See also Sect. 2

Figures 6 and 7 point to a remarkable robustness of the findings of the main text.

Appendix 2: Robustness check. The Carlson–Parkin method

In this Appendix we calculate the first two moments of the distribution of the interviewers’ replies with a different approach with respect to that used in the main text. Specifically, we take advantage of the Carlson–Parkin method (CP, Carlson and Parkin 1975) in the five option replies version of Batchelor (1986), Batchelor and Orr (1988). Essentially, the method interprets the share of respondents as maximum likelihood estimates of areas under the density function of aggregate expectations, that is, as probabilities. More formally, the first two moments are:

where \( y_{t}^{r} \) is the agent’s reference GDP growth rate, \( z_{t}^{1} = {\rm N}^{ - 1} \left[ {1 - {\text{LB}}_{\text{t}} } \right],\;\;z_{t}^{2} = {\rm N}^{ - 1}\left[ {1 - {\text{LB}}_{\text{t}} - {\text{B}}_{\text{t}} } \right],\;\;z_{t}^{3} = {\rm N}^{ - 1}\left[ {1 - {\text{LB}}_{\text{t}} - {\text{B}}_{\text{t}} - {\text{E}}_{\text{t}} } \right],\;z_{t}^{4} = {\rm N}^{ - 1}\left[ {{\text{LW}}_{\text{t}} } \right] \), \( {\text{N}}^{ - 1} \left[ {} \right] \) is the inverse of the cumulative normal distribution.Footnote 12

As done in the main text, we add the suffix “i” to refer to individual-level conditions. Thus, mutatis mutandis and applying the formulae (8.1) and (8.2) to the data referring to expectations on personal stances, we obtain the first, \( y_{it}^{e,CP} \), and the second moment, \( \upsigma_{it}^{e,CP} \), of expectations on personal stances. Analogously to what said about the parameters α and αi in the Anderson-Theil measures (Sect. 2), \( y_{t}^{r} \) and \( y_{it}^{r} \) can be chosen to ensure that the CP-statistics have the same average value as the (perceived) underlying income process in the sample period. As before, it is a critical choice.Footnote 13 To increase the comparability of the outcomes, we set \( y_{t}^{r} = y_{it}^{r} = 1 \) as done for the parameters α and αi in the balance statistics. This said, it is worth noticing that (i) our aim is not the quantification of survey expectations, that (ii) we just match survey data and that (iii) this issue disappears when working with CP-signal-to-noise ratios.

The following tables report the same empirical exercises presented in the main text. To ease comparisons we maintain the same table headings of the main text, just adding “B” to the corresponding number of the table.

Alike Table 1 of the main text, Table 8 shows that the persistence of the two central tendencies is practically unchanged irrespective of the method used to compute them. Table 9 informs that the unit-root tests for \( y_{t}^{e,CP} \) cannot reject the null of I(1) only at the 10 % level.Footnote 14 We therefore go on with Johansen’s cointegration tests. Since two series with different orders of integration cannot be cointegrated, the cointegration test may offer further evidence on whether both central tendencies are I(1) processes.

Table 10 reassures that the two statistics are cointegrated.

Working with the Eqs. (7.1) and (7.2) presented in Appendix 1, we estimate another VECM whereas x it and x t are now the two CP-central tendencies. We collect the results in the following Table 11.

Once again, the results of the main text are substantially validated.

Finally, using the two above mentioned CP statistics, define the signal to noise ratio (CP-SNR) as central tendency on cross sectional disagreement, i.e., \( _{t - h} SNR_{t}^{e,CP} \equiv y_{t}^{e,CP} /\upsigma_{t}^{e,CP} \) and \( _{t - h} SNR_{it}^{e,CP} \equiv y_{it}^{e,CP} /\upsigma_{it}^{e,CP} \). Similarly to what done for the two CP-central tendencies, Tables 12, 13 collects, respectively, the results of efficient unit root tests, Johansen’s cointegration tests. Table 14 the results of the bivariate VECM sets out in Eqs. (7.1) and (7.2) (cf. Appendix 1) relative to the two CP-SNRs.

All in all, the evidence obtained using the Carlson–Parkin method is substantially reassuring about the high degree of robustness of the outcomes reported in the main text.

Appendix 3: Robustness check. Evidence from Euro Area

In this section we exploit Euro Area (EA) data to replicate for the same sample period (Jan. 1995–Jul. 2013) exactly the same exercises done for Italy in the main text. This validation generalizes our arguments and it increases the robustness of our evidence. To underline that we are redoing the very same empirical exercises already performed with Italian data, we define the variables in the same way as before but for the fact that EA wide variables are in bold. Thus, e.g., \( _{t - h} y_{it}^{e} \) stands for the balance dealing with personal situations in Italy, whereas \( _{t - h} {\bf{y}}_{it}^{e} \) stands for the corresponding balance at the EA level. In the EA each interviewed faces—obviously in the language of the country (s)he lives—virtually the same queries that deal with the change over the next 12 months of (i) the “economic situation in your household” (Personal) and of (ii) the “economic situation in your country” (General). Data at national level are aggregate as follows. The percentage for each alternative answer to each question for the EA is calculated as the weighted average of the corresponding percentages in each EA member. The weights are the shares of each of the member states in the EA reference series, and are smoothed by calculating a 2 year moving average. The weights are usually updated every year in January (European Commission 2014).

Figure 8 highlights that since 2002 the two balances show no zero crossing and a tendency to stay below zero with very few exceptions. We interpret it as survey data correctly reflecting the declining macroeconomic developments in EA over the last decade and as suggesting that negative shocks have had greater impact than positive ones on both hard data and households’ expectations. More importantly, \( _{t - h} \varvec{y}_{it}^{e} \) is almost always higher than \( _{t - h} \varvec{y}_{t}^{e} \), suggesting that, as expected, better-than-average effects and the like (cf. Sect. 3) are an immanent trait of human being that, accordingly, are present everywhere. Even at continental level.

Survey expectations. Central tendency. “Personal” (\( _{t - h} {\bf{y}}_{it}^{e} \)) is the central tendency (cf. Sect. 2) of the responses to the query “How do you expect the economic situation in your household to change over the next 12 months?” “General” (\( _{t - h} {\bf{y}}_{t}^{e} \)) is the central tendency of the responses to the query “How do you expect the general economic situation in the country to develop over the next 12 months?” They vary from −1 (all replies are: it will get a lot worse) to +1 (all replies are: it will get a lot better). Shaded area indicates periods of below-full-sample-average GDP annual growth rate. Data for the Euro Area (Jan. 95–Jul. 2013). These data are obtained aggregating national data using the weighted averages of the corresponding percentages in each euro-area member. The weights are the shares of each of the Member States in the EA reference series (European Commission 2014)

Figure 9 very clearly displays that the level of disagreement among European lay forecasters is persistent. Indeed, \( \varvec{\upsigma}_{it}^{e} \) never goes below 0.55 and it has a sample mean of 0.63 (recall that it ranges between 0 and 1 = total heterogeneity). As already argued in the main text, this is less unsurprising than the fact that \( \varvec{\upsigma}_{t}^{e} \), in a sample covering two-hundred and thirty months, has a minimum value of 0.8 and an average value of 0.87. That is to say, forecast heterogeneity across European households remains systematically very close to its maximum value. As stressed in Sect. 3, this finding is even more striking because it is detected in a period characterized by poor economic performances—in this environment more homogeneous predictions should show up because the cost of erring is higher and the cost of information is lower.

Survey expectations. Cross sectional dispersion. Note. “Personal” (\( \varvec{\upsigma}_{it}^{e} \)) is the second moment (index of qualitative variation) of the responses to the query “How do you expect the economic situation in your household to change over the next 12 months?” “General” (\( \varvec{\upsigma}_{t}^{e} \)) is the index of qualitative variation of the responses to the query “How do you expect the general economic situation in the country to develop over the next 12 months?” (Cf. Sect. 2). \( 0 \le\varvec{\upsigma}_{it}^{e} ,\;\varvec{\upsigma}_{t}^{e} \le 1 \). \( \varvec{\upsigma}_{it}^{e} ,\;\varvec{\upsigma}_{t}^{e} = 0 \) means totally homogeneous expectations. Data for the Euro Area (Jan. 95–Jul. 2013). These data are obtained aggregating national data using the weighted averages of the corresponding percentages in each euro-area member. The weights are the shares of each of the Member States in the EA reference series (European Commission 2014)

Following the same reasoning of the main text, we now turn our attention on some preliminary statistics aimed to see whether there is the need to perform cointegration analyses.

Table 15 informs that in the EA the sample persistence of the balances is even larger than in Italy. This leads to unit root tests. We collect the outcomes of these latter in Table 16.

Table 16 robustly suggests that it is not possible to reject the null of unit root at the usual confidence levels, calling for cointegration tests. We report the relative statistics in Table 17.

Table 17 confirms the previous findings about the presence of unit roots, and supports the view that the central tendencies of the two expectations are cointegrated at the Euro Area level too. We therefore go on with VECM analyses (cf. Table 18).

The visual inspection of Table 18 once again sustains what already pointed out in the main text regarding Italian lay forecasters. Only some quantitative results change. For instance, the residual correlation (0.66) and the cointegrating vector [1, −0.57] are virtually the same in Italy and in the EA. By contrast, the speed of adjustment, δ, is now much lower (0.33 vs 0.61). As it should be clear, to our aim it is much more important that δi is (i) very close to zero and (ii) much lower than δ. At this point we can go on examining the SNR for the Euro Area as a whole.

These two tables clarify that the two SNRs are first-order integrated processes (Table 19) and that they are linked by an error correction model (Table 20). The outcomes stemming from the logically consequent VEC model are collected in the following Table 21.

Table 21 highlights that δi is only marginally significant and, in any case, it is still very close to zero and much smaller than δ, indicating that European households modify \( _{t - h} \varvec{y}_{t}^{e} \) in order to reduce the divergence with \( _{t - h} \varvec{y}_{it}^{e} \). The unrestricted cointegrating vector is [1, −0.85], but the last row of Table 21 demonstrates that the cointegrating vector is statistically [1, −1]. This offers corroborating evidence on the circumstance that, just like Italians, European lay consumers’ expectations are such that their cross sectional disagreement and time series volatility is statistically equal.

In order to save space we do not report other exercises referring to EA data.Footnote 15 We just note, to conclude, that what we have said about Italy in the main text finds here and in the unreported findings strong confirmation at the European level.

Rights and permissions

About this article

Cite this article

Bovi, M. The tale of two expectations. Qual Quant 50, 2677–2705 (2016). https://doi.org/10.1007/s11135-015-0283-0

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11135-015-0283-0