Abstract

This paper estimates the effect of the COVID-19 pandemic on risk of corruption in Mexico. To calculate the pandemic’s impact on risk of corruption, this study uses monthly administrative data of 378,000 public acquisitions through 64 institutions from the Mexican Federal Government during the 2018–2020 period. These institutions account for approximately 75% of all allocations of public acquisitions made by the Mexican Federal Government. The risk of corruption is measured through the Discrete-Contracts-Value-to-Budget (DCVB) ratio, which represents the ratio of the value of contracts assigned through discretionary non-competitive mechanisms to the total value of contracts per institution. The empirical strategy consists of a difference-in-differences methodology and an event-study design. The analysis is conducted over all institutions as well as by healthcare and non-healthcare institutions. The results show the following: (1) the pandemic increased the DCVB ratio by 17%; (2) the DCVB ratio increased during six months and then it returned to pre-pandemic levels (inverted U-shape form); and (3) surprisingly, the rise in the risk of corruption is mainly driven by non-healthcare institutions. From a policy perspective, Mexico’s Government Accountability Office, although counterintuitive, should focus on non-healthcare institutions when conducting audits targeting public acquisitions made during the pandemic, even though much of the political debate remains centered around the risk of corruption in healthcare institutions.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

In response to the pandemic, governments increased their healthcare and economic relief expenditures. To expedite the allocation of essential resources, they also relaxed accountability standards. Unfortunately, these practices translated into new corruption opportunities (Rose-Ackerman, 2021). While not all of these opportunities resulted in corruption practices, the inefficiencies in public procurement processes likely facilitated occurrences of fraud, bribery, and embezzlement. Notably, instances of these crimes often surface years after the implicated politicians have left office. As a result, researchers studying the effects of the COVID-19 pandemic in the short term have mainly examined the risk of corruption as a proxy indicator for actual corruption (Abdou et al., 2021; Blanco Varela et al., 2022; Cacciatore et al., 2022; Gallego et al., 2021).

Several criminology theories provide valuable theoretical frameworks for understanding the relation between disasters — such as a pandemic — and corruption. These theories include the rational choice theory and the routine activity theory. The rational choice theory focuses on how offenders decide whether to commit corruption by weighing the costs (e.g. likelihood of detection and punishment) and benefits (e.g. potential yield) associated with it; if the benefits outweigh the costs during a disaster, rational criminals are likely to commit corruption (Becker, 1968; Cornish & Clarke, 1986). Routine activity theory highlights the suitable targets for corruption created by disasters and the absence of capable guardianship (Cohen & Felson, 1979). Both theories provide a basic conceptualization of the linear relation between disasters and corruption, in which the latter increases after a disaster, persistently (Frailing & Harper, 2017).

Similarly, other criminology theories — such as the resilience of crime theory — provide a structure that relates disasters and corruption non-linearly. In particular, disasters bring an influx of money to help affected individuals; unfortunately, public officials need to relax accountability standards to support the victims in the short term (Frailing & Harper, 2017). In the medium term, public officials recover their regulatory capabilities and corruption drops to pre-disaster levels (Frailing & Harper, 2017). Said theory suggests an inverted U-shape relation between disasters and corruption.

The monitoring of public finance management is important in emerging economies, which are particularly susceptible to corruption during times of emergencies. Unlike high-income countries with robust institutions, developing economies often lack the institutional and social practices necessary to deter corruption under challenging conditions (Peyton & Belasen, 2012). Additionally, crony capitalism, which is more prevalent in emerging economies, thrives during extraordinary events, where politicians may reciprocate favors to their cronies, who aim to strengthen their market dominance under shifting circumstances (Enderwick, 2005).

This paper examines the effect of the COVID-19 pandemic on risk of corruption in Mexico using data of 378,000 public acquisitions made by 64 institutions from the Mexican Federal Government. These acquisitions represent approximately 75% of all public acquisition allocations during the period between 2018 to 2020. Throughout this period, these 64 institutions consistently awarded contracts on a monthly basis, ensuring a balanced panel dataset for the analysis. The primary focus of this investigation lies in the assessment of the ratio between the value of contracts assigned through discretionary non-competitive mechanisms and the total value of contracts per institution. This ratio, referred to as the Discrete-Contracts-Value-to-Budget (DCVB), serves as the main outcome of interest.

To estimate the effect of the COVID-19 pandemic on risk of corruption two econometric methodologies are used: a difference-in-differences strategy and an event-study design. These methodologies have been implemented to study the effects of the COVID- 19 pandemic on several socioeconomic variables such as crime, mental health, and domestic violence (Balmori de la Miyar et al., 2021; Brodeur et al., 2021; Leslie & Wilson, 2020). Further two potential mechanisms to elucidate the observed effects are examined: (1) the influence of specific institutions, with particular attention to the Mexican Army, which has expanded its involvement across various sectors during the present government (Berg et al., 2023), and (2) the pandemic’s impact on two factors previously linked to corruption: the market concentration among providers and irregularities on the disclosure of the contract’s procedure information (Blanco Varela et al., 2022).

The present study contributes to the recent body of literature investigating the effect of the COVID-19 pandemic on corruption (Abdou et al., 2021; Almada et al., 2022; Blanco Varela et al., 2022; Cacciatore et al., 2022; Gallego et al., 2021; Rose-Ackerman, 2021). Specifically, this paper examines several key aspects for the case of Mexico, which are consistent with findings in other settings. First, it analyzes whether there is an increase in the average value of discretionary non-competitive contracts during the pandemic (Gallego et al., 2021). Second, it tests whether there is an increase in the risk of corruption in non-healthcare sectors, which are generally overlooked given the nature of the pandemic (Abdou et al., 2021). Finally, it examines whether there is evidence of an increase in market concentration among government providers (Blanco Varela et al., 2022). The insights of such analysis can be useful for policy makers tasked with overseeing audits aimed at scrutinizing public acquisitions made during the pandemic, proving valuable insights to mitigate corruption risks in the context of government spending during extraordinary events.

The remainder of this paper proceeds as follows. Section 2 presents the related literature. Section 3 describes the empirical strategy. Sections 4 and 5 contain the results and a discussion, respectively. Section 6 concludes.

Related Literature

During emergencies, such as the COVID-19 pandemic, governments boost spending on healthcare and economic relief while simultaneously relaxing accountability measures. The extent of corruption opportunities that arise in such circumstances may vary depending on the developmental status of institutions. Acknowledging that the professional integrity of markets and government agencies can play a pivotal role in mitigating corruption opportunities (Rose-Ackerman, 2021), multilateral organizations, like the International Monetary Fund or the World Bank, often incorporate anti-corruption measures in agreements for emergency aid packages (Rose-Ackerman, 2021). However, despite these efforts, instances of potential corruption during the pandemic have been identified in various countries and settings.

For instance, in the United States, multimillion-dollar government contracts were awarded to companies with little experience producing protective equipment for COVID- 19 (Gabrielson et al., 2020). Similarly, in Colombia, the government provided food boxes to families affected by the lockdown, but the price paid by the government for these boxes was twice the market price (Faiola & Herrero, 2020). Likewise, in Mexico, the Cyber Robotics company sold ventilator equipment at a price of 1.5 million MX pesos each, whereas the Mexican Federal Government purchased similar ventilators at nearly half that price during the same week (Sánchez-Ley & Olmos, 2020). It is worth noting that, at that time, the Cyber Robotics company was owned by the son of a politician who also served as the CEO of the Federal Electricity Commission, a state-owned utility company in Mexico (Sánchez-Ley & Olmos, 2020).

In conjunction with individual case reports of corruption, there is a growing body of literature that identifies an increase in corruption as a consequence of the COVID- 19 pandemic, although the literature remains small. Specifically, Gallego et al. (2021) finds that Colombian municipalities that were already susceptible to corruption prior to the pandemic, responded to the crisis by significantly increasing the average value of discretionary non-competitive contracts. Using a differences-in-differences strategy, the authors point to an increase of 7.5% in the average value of discretionary contracts (Gallego et al., 2021).

In this line of research, Blanco Varela et al. (2022) examines the expenditure patterns in four deputations of Galicia, Spain, namely Coruña, Lugo, Ourense, and Pontevedra, to investigate the impact of the COVID-19 pandemic. The study focuses on the utilization of "minor contracts," a procedure characterized by a lack of publicity or competitive bidding and associated with higher corruption risks. The findings indicate that, in Spain, the percentage of expenditure on minor contracts relative to the total budget only increased in the Ourense deputation, rising from 8.6% in 2019 to 10.5% in 2020. Moreover, this increased spending on minor contracts in Ourense coincided with a greater concentration of government providers (Blanco Varela et al., 2022).

Likewise, Cacciatore et al. (2022) focus on public procurement concerning four economic relief policies initiated by the Italian government during the COVID-19 pandemic. These policies encompassed funding support for businesses, temporary suspension of work, one-time allowances for self-employed workers, and emergency income aid. Despite witnessing an increase in accountability safeguards over time, the evidence from Italy reveals that the economic recovery policies did not comply with anti-corruption indicators (Cacciatore et al., 2022).

Furthermore, additional research conducted by Almada et al. (2022) investigates fiscal transparency on web portals of state governments in Brazil during the COVID- 19 pandemic. The results demonstrate a divergence across states, largely driven by factors such as the level of development and average income. In a related paper, Abdou et al. (2021) estimates the pandemic’s impact on the risk of corruption in Romania, using a composed risk index (CRI) derived from eleven corruption-related indicators. The findings show an increase in the CRI for COVID-19-related goods, which increased from 0.4 to 0.6, representing an increase of 50% in the risk of corruption. Notably, in Romania, non-healthcare products, where relaxed regulations did not apply, also witnessed an expansion in their CRI scores (Abdou et al., 2021). Finally, an interconnected body of literature explores the influence of various types of disasters on public procurement, consistently indicating a higher prevalence of corruption (Sobel & Leeson, 2008; Yamamura, 2014).

Data and Methods

Data

This study employs publicly available data from all types of public contracts executed by the Mexican Federal Government, spanning acquisitions, leases, public works, and services. The data is available through the online system CompraNet. In particular, this paper uses the systematized CompraNet data, which has been organized by the Mexican Institute for Competitiveness (IMCO). This dataset provides crucial contract characteristics, including the contract value, the allocating public institution, the provider’s name, contract start and end dates, allocation mechanisms employed, among other characteristics (IMCO, 2022).

In Mexico, public contracts are allocated through three mechanisms: public auctions, auctions by invitation, and direct allocation. The law favors the use of public auctions. However, exceptions within the law allow public institutions to exercise their discretion and opt for either auctions by invitation or direct allocation methods in certain cases.

The data is aggregated at the institution-month level for the 2018–2020 period. To obtain a balanced panel, only institutions that allocated at least one contract every month from 2018 through 2020 are maintained. Thus, the data gathers 378,000 public acquisitions, attributed to 64 institutions within the Mexican Federal Government. The contracts granted by these 64 institutions account for approximately 75% of all public acquisition allocations during the period under analysis. Thus, the final sample comprises 2,304 observations (64 institutions × 12 months × 3 years).

Table 1 provides an overview of summary statistics. The average contract value is approximately 5.06 million MX pesos (roughly 250,000 US dollars). On average, each institution allocates 164.46 contracts monthly. When differentiating these values between healthcare and non-healthcare institutions, healthcare institutions assign smaller contracts with an average value of 2.01 million MX pesos. Conversely, non-healthcare institutions assign contracts with an average value of 5.84 million MX pesos.

In general, the use of discretion in allocating contracts is high. In any given month, approximately 70% of the total contract value is allocated through mechanisms that involve hiring discretion, encompassing both auction by invitation and direct allocation methods. When looking at these numbers by type of institution, there is a marginal variation of five percentage points. Healthcare institutions exhibit a 66% utilization of discretionary mechanisms, whereas non-healthcare institutions demonstrate a slightly higher proportion at 71%.

Methods

Difference-in-differences

A difference-in-differences methodology is used to estimate the effects of the COVID-19 pandemic on risk of corruption. The difference-in-differences methodology is an econometric technique to establish causal relationships. This methodology is based on the assumption that there is a group affected (treatment) and one not affected (control) by a policy or event. Likewise, it assumes that there is information before and after the event for the treatment and control groups (Krueger & Card, 2000). This methodology assumes that before the event, both the treatment and the control groups follow the same trend (parallel trends assumption). And, if the event has an effect, the treatment group will follow a different trend than the control group after the event (Krueger & Card, 2000).

A linear regression is used to obtain the difference-in-differences estimator (βDD) of the event (COVID-19) on the variable of interest (risk of corruption). The event variable is generated through the interaction of two dichotomous variables (Angrist & Krueger, 1999): treatment (which takes the value of 1 for the treatment group and 0 for the control group) and time (which takes the value of 1 after the event and 0 before the event).

For the present study, the treatment variable takes the value of 1 for contracts related to 2020 and 0 for contracts related to 2018 and 2019. Likewise, the time variable takes the value of 1 for March-December and 0 for January–February. Therefore, the event (COVID-19) variable takes the value of 1 from March to December 2020, and 0 otherwise. The differences in differences estimator is estimated as follows:

where Corruptionimy is the outcome of interest for institution i, in month m, and year y. As mentioned above, the discrete-contracts-value-to-budget (DCVB) ratio is the outcome of interest. COVID19imy is a dummy variable that equals one from March through December, 2020. ai are institution-fixed effects, γm are monthly-specific fixed- effects, and νy are year fixed effects. Standard errors are clustered at the institution level. The difference-in-differences estimator (βDD) shows the average impact of the months followed by the pandemic.

Event-study

An event-study is used to complement the difference-in-differences results. The difference-in-differences estimates the average effect after the pandemic. The event-study estimates the monthly dynamic effects after the onset of the event (Wolfers, 2006). Thus, the even-study permits to observe whether the risk of corruption increases permanently or returns to pre-pandemic levels. In addition, the event-study allows to test whether the treatment and control follow the same trend before the pandemic (parallel trends assumption). In the event study, this assumption can be visually observed by examining the dynamic of the effects before the pandemic (Goodman-Bacon & Marcus, 2020). The event-study methodology has been implemented to study the effects of the COVID-19 pandemic on several socioeconomic variables such as crime, mental health, and domestic violence (Balmori de la Miyar et al., 2021; Brodeur et al., 2021; Leslie & Wilson, 2020). The event-study specification is estimated as follows:

where Corruptionimy is the outcome of interest for institution i, for month m, and year y. COVID19iqy is a set of dummy variables that take the value of one in each period q before and after the start of the lockdown in March 2020. In particular, March 2020 is represented by q = 0. q = − 9 corresponds to nine months before the lockdown, or June 2019. q = 9 represents nine months after the lockdown, or December 2020. To avoid multicollinearity, a period is excluded, which in the empirical literature is the period q = − 1 (Balmori de la Miyar et al., 2021; Brodeur et al., 2021; Leslie & Wilson, 2020). Thus, the dynamic of the effects before and after the start of the pandemic in March 2020 are represented by the βq coefficients. The rest of the variables follow the same interpretation as in the difference-in-differences specification.

Results

Difference-in-differences Findings

Table 2 presents the difference-in-differences results for the pandemic’s effect on risk of corruption in Mexico. Column (1) displays the effect of the pandemic on the DCVB ratio across all institutions, which shows a statistically significant positive effect equal to 0.12. This effect represents a 17%-increase relative to the baseline value of 0.70. Further, the results are disaggregated by the type of institution, with columns (2) and (3) presenting the findings for healthcare and non-healthcare institutions, respectively. Surprisingly, the pandemic’s effect on the DCVB ratio is fully driven by non-healthcare institutions. For healthcare institutions, the pandemic’s effect on risk of corruption is negative but not significant. For non-healthcare institutions, estimations show a statistically significant coefficient of 0.16, which represents a substantial 23%-increase in the proportion of the value of contracts assigned with discretion.

Event-Study Findings

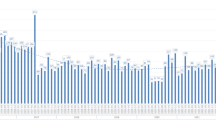

Figure 1 displays the event study results, which examines the monthly impact before and after the COVID-19 pandemic. Before the pandemic, all outcomes closely align with the horizontal red line or do not exhibit statistically significant differences from zero, thereby supporting the validity of the parallel trends assumption.

Source: IMCO. Notes: Plotted coefficients are event-study dummy variables, βq. Solid dots represent point estimates. Dotted lines display the 95 percent confidence intervals. Baseline fixed effects are included at the institution, month, and year level. Robust standard errors are clustered at the institution level

Event Study Results.

Beginning with the graph of Fig. 1, which aggregates all institutions together, calculations show a temporal increase in the DCVB ratio. Specifically, by the second month of the pandemic, coinciding with the lifting of the stay-at-home order, the DCVB ratio experiences a 20% rise. This increase remains sustained for an additional four months before the patterns of contract value allocation revert to pre-pandemic levels. The second and third graphs of Fig. 1 indicate that non-healthcare institutions primarily drive these results. In particular, non-healthcare institutions also witness a 20% impact on their DCVB ratio by the second month of the pandemic, persisting for four subsequent months. Conversely, the DCVB ratio for healthcare institutions remains unaffected after the onset of the pandemic. Furthermore, the event- study analysis aligns with the difference-in-differences results regarding the DCVB outcomes in terms of direction and magnitude.

Robustness Checks

A series of robustness analysis are conducted to test the validity of the results. First, a correction for multiple hypothesis testing is implemented. Second, an Oster (2019) bounding methodology is conducted to study the influence of potential omitted variable bias. Third, an analysis is conducted to check that the results are not driven by outliers. Finally, a robustness check regarding the sensitivity of the parallel trends assumption is implemented.

First, it is possible that the results obtained regarding the increase on DCVB in non-health care institutions are just by chance. To minimize this potential risk, a multiple hypothesis testing using the False Discovery Rate q-values of Anderson (2008) is conducted. Panel A of Table 3 presents both the respective p-values in parenthesis and q-values in brackets of the difference-in-differences results. There is a small increase in the q-values for DCVB (overall). Yet, none of the significant results based on p-values becomes insignificant when using q-values.

Second, the event study presents evidence in favor of the parallel trends assumption. In other words, the changes observed are a consequence of the pandemic and not of omitted variables. To further confirm this result, a bounding approach proposed by Oster (2019) is performed for the difference-in-difference results. This methodology simulates a bound around the parameter of interest based on an expected value of the R2. When the bounds exclude zero, it indicates that the parameter of interest remains robust to the issue of omitted variable bias. Table 3 Panel B shows that the Oster bounds exclude zero for the difference-in-difference results regarding DCVB over all institutions and DCVB for non-healthcare institutions. Thus, the results are not sensible to the problem of omitted variables.

Third, it is possible that the results are driven by outliers. Panel C and D in Table 3 present the difference-in-difference results after omitting the 1% and 5% of contracts with the highest values. The results remain statistically significant for the pooled DCVB ratio and for the DCVB ratio of non-healthcare institutions.

Finally, we conduct a robustness check regarding the sensitivity of the parallel trends assumption. The event study shows that, in general, the pre-event coefficients (Fig. 1 Panel A) are not statistically significant. In the event study literature, the non statistical significance of the coefficients before the event is taken as suggestive evidence in favor of the parallel trends assumption (Rambachan & Roth, 2023). However, Rambachan and Roth (2023) point out that the non statistical significance of the coefficients before the event is not sufficient to meet the parallel trends assumption. In particular, Rambachan and Roth (2023) propose that such evidence only proves that omitted variables have the same effect before the event, but there is no guarantee that the same effect (parallel trends) will persist after the event. The argument is that such omitted variables may behave differently after the event.

Thus, this paper incorporates the methodology proposed by Rambachan and Roth (2023) to check the sensitivity of the results to the problem of omitted variable bias after the event. This methodology generates a series of bounds to determine the point at which there is a violation of the parallel trends assumption after the event. The generation of the bounds depends on a coefficient M, which is a measure of a linear extrapolation using the worst pre-treatment violation of parallel trends between consecutive periods. If the bounds using M = 0.1 do not include zero, this result implies that the post-treatment effect is robust to a post-treatment violation of parallel trends equal to 10% of the worst pre-treatment violation of parallel trends. Further, if the bounds using M = 0.2 do not include zero, then the post-treatment effect is robust to a post-treatment violation of parallel trends equal to 20%, and so on.

Figure 2 in the Apendix shows the bounds using the methodology suggested by Rambachan and Roth (2023) for the overall effect of the pandemic on DCVB, our main outcome of interest. Only the periods in which we observe a statistically significant effect of the pandemic on risk of corruption, periods one to five (see Fig. 1 Panel A) are analyzed. Said methodology is implemented using values of M from 0 to 0.2. The results show that the parallel trends assumption is robust until M = 0.15. This suggests that the post-treatment effect is robust to a post-treatment violation of parallel trends equal to 15% of the worst pre-treatment violation of parallel trends.

To further identify which coefficients are susceptible to the omitted variables problem, we implement again the methodology proposed by Oster (2017) but for the event study results. Table 4 in the Appendix presents the results using Oster’s methodology with the following bounds for periods one [-0.02, 0.53], two [0.11, 0.57], three [0.07, 0.75], four [0.13, 0.70] and five [0.10,0.72]. Oster’s methodology shows that only period one is susceptible to omitted variable biases. Thus, in the exteme case that a post-treatment violation of parallel trends was greater than 15% of the worst pre-treatment violation of parallel trends, this would only affect period one. The previous means that, at least from period two to five, our results are robust to any changes in post-treatment parallel trends such as the shape of discrete contracts.

Mechanisms

Potential mechanisms are explored to comprehend the increase in DCBV. In particular, two mechanisms are examined: (1) the influence of specific institutions, with a particular focus on the Mexican Army, which has been extending its involvement in various governmental areas during the current administration (Berg et al., 2023), and (2) the pandemic’s impact on two factors previously linked to corruption: providers’ market concentration and irregularities in the disclosure of contract information (Blanco Varela et al., 2022).

First, it is possible that the increase on DCBV is driven by specific institutions. Thus, the difference-in-difference analysis is conducted but systematically omitting one institution at a time. The estimated coefficients along their 95 confidence intervals are presented on Fig. 3 in the Appendix. The estimates remain stable when removing one institution at a time, ruling out the possibility that the results are driven by a single institution. Most importantly, Fig. 4 in the Appendix shows that the event study results continue to hold when excluding the Mexican Army (SEDENA) from the sample. This is of particular interest as the military has taken on various different strategic roles within the Mexican Government, such as emergency healthcare, citizen security, and construction, since the start of the pandemic (Berg et al., 2023). Hence, the increase in the DCVB ratio for non-healthcare institutions cannot be attributed to the militarization process that Mexico has been experiencing under the current federal administration, which has notably intensified during the pandemic.

Second, a difference-in-difference specification is used to estimate the pandemic’s effect on the providers’ market concentration, which has been related to corruption (Blanco Varela et al., 2022). To study the pandemic’s effect on the providers’ market concentration, each public institution is considered as a separate market and a Herfindahl–Hirschman Index (HHI) is constructed. This index is constructed for each month as follows:

where sjity is the share of contracts given to provider j, in market (institution) i, year y, and month t, and niyt denotes the number of providers hired by institution i in a specific month.

Table 5 in the Appendix displays the pandemic’s effect on market concentration on the value of contracts, both for healthcare and non-healthcare institutions. There is no effect on healthcare institutions. Yet, non-healthcare institutions present a statistically significant increase of approximately 462 points in the HHI index. As a point of reference, the U.S. Department of Justice considers a market to be competitive if the HHI is less than 1,500, moderately concentrated if the HHI is between 1,500 and 2,500, and highly concentrated if the HHI is above 2,500 (USDJ, 2018). Prior to the pandemic, the baseline value was 2,819, so an increase of 462.6 points in the HHI index translates into a strong reduction in competition within an already concentrated market. This result suggests that one possible explanation on the increase on DCVB in non-health care institutions could be related to an increase of suppliers’ concentration during the COVID-19.

Given the suggestive evidence pointing towards an increase in the risk of corruption, particularly in non-health care institutions, the occurrence of contract anomalies as a consequence of the pandemic is examined. Specifically, it is estimated whether there has been a change in the proportion of contracts that disclosed the contract’s procedure information after the contract’s starting dates. The findings related to this outcome, using a difference-in-difference analysis, are presented in Table 6 in the Appendix. Evidence of corruption is primarily associated with non-health institutions, as these institutions experienced a significant increase in the proportion of contracts where the contract information was published after the contract’s starting dates. This increase, relative to pre-pandemic levels, is of approximately 10%.

Overall, the findings provide suggestive evidence that the pandemic has influenced both the contracts assigned through discretionary non-competitive mechanisms and the timing of contract information disclosure, particularly in non-health institutions.

Discussion

The results of this study contribute to the existing empirical evidence examining the impact of the COVID-19 pandemic on the risk of corruption. First, the case of Mexico demonstrates an increase in the utilization of discretionary non-competitive contracts during the pandemic. This finding aligns with the observations made in Colombia regarding the usage of such contracts (Gallego et al., 2021). Second, the risk of corruption has increased for non-healthcare institutions in Mexico, in contrast to the evidence from Romania, where corruption increased for both healthcare and non- healthcare goods after the pandemic (Abdou et al., 2021). Third, the exploration of potential mechanisms found no evidence of influence from specific institutions, such as the Mexican Army, even though there is evidence of market concentration among providers in non-healthcare institutions, similar to the case in Spain (Blanco Varela et al., 2022).

The disparities observed between Mexico and Romania could be attributed to differences in institutional development and the integrity of both market and government agencies (Rose-Ackerman, 2021). Alternatively, the variance in monitoring intensity, carried out by non-government organizations and media, for the government’s healthcare provision during the pandemic could play a role. An illustrative example of this monitoring is evident in the case of the ventilators purchased at an inflated price by the Mexican Federal Government from a company owned by the son of a politician who serves as the CEO of the Federal Electricity Commission (Sánchez-Ley & Olmos, 2020). Such monitoring efforts could potentially deter corrupt practices in the health sector, given the high probability of being exposed.

As for the limitations of the present research, one lies in the level of detail provided in the data. Unfortunately, it is not possible to differentiate whether auctions by invitation or direct allocation, were employed for legitimate reasons (e.g., specialized providers or urgent delivery needs) or for private rent-seeking purposes. Another limitation pertains to the inability to determine whether the increase in the risk of corruption translated into proven instances of fraud, bribery, or embezzlement.

Conclusion

This paper examines the effects of the COVID-19 pandemic on public contract allocation with hiring discretion. The results show that the pandemic increased the discrete-contracts-value-to-budget (DCVB) ratio. The effect was large, reaching an increase of 20% by the second month after the beginning of the pandemic. This increase persisted for four months before the allocation patterns returned to pre-pandemic levels. Contrary to expectation, the rise in the DCVB ratio was predominantly driven by changes in contract allocation within non-healthcare institutions, rather than healthcare institutions. Additionally, results suggest an increase in market concentration among government providers after the pandemic began, along with a higher proportion of contracts that disclosed procedural information later than the contract’s starting dates.

With the onset of the pandemic and the urgent investments needed in health infrastructure, an increase in the DCVB ratio for healthcare institutions was expected, particularly since the law allows discretion in hiring to expedite the process in times of crisis. Nevertheless, the results indicate that this increase was only present in non-healthcare institutions. Plausible reasons are: 1) a relatively reduced oversight in non-healthcare sectors during the pandemic, creating opportunities for discretionary hiring, 2) a higher level of professional integrity within healthcare institutions mitigating the risk of corruption (Rose-Ackerman, 2021), and 3) greater scrutiny by the media and non-government organizations over healthcare institutions during the pandemic.

From a policy perspective, Mexico’s Government Accountability Office (Auditoría Superior de la Federación) should take into account the elevated risk of corruption highlighted by the findings of this paper when conducting audits targeting public acquisitions made during the pandemic. Despite being counter-intuitive, the results suggest that the focus of these audits should be on non-healthcare institutions, even though much of the political debate surrounding the issue remains centered around healthcare institutions.

Data availability

The data that support the findings is available in the following https://doi.org/10.7910/DVN/7Z2S30

References

Abdou, A., A. Czibik, B. Tóth, & M. Fazekas (2021) “Covid-19 emergency public procurement in Romania: Corruption risks and market behavior,” Government Transparency Institute, Working Paper Series 20021–03.

Almada, M. P., C. Aggio, P. K. Amorim, N. Santos, and M. D. C. Pinho (2022): “Assessing Priorities of Transparency During COVID-19 Pandemic in Brazil,” Public Organization Review, 1–26.

Anderson, M. L. (2008). Multiple inference and gender differences in the effects of early intervention: A reevaluation of the abecedarian, Perry preschool, and early training projects. Journal of the American Statistical Association, 103, 1481–1495.

Angrist, J. D. and A. B. Krueger (1999): “Chapter 23 - Empirical Strategies in Labor Economics,” Elsevier, vol. 3 of Handbook of Labor Economics, 1277–1366.

Balmori De La Miyar, J. R., Hoehn-Velasco, L., & Silverio-Murillo, A. (2021). Druglords don’t stay at home: COVID-19 pandemic and crime patterns in Mexico City. Journal of Criminal Justice, 72, 101745.

Becker, G. S. (1968). Crime and punishment: An economic approach. Journal of Political Economy, 76, 169–217.

Berg, R. C., S. Fattori, AND H. Ziemer (2023): “After AMLO,” Tech. rep., The Center for Strategic and International Studies.

Blanco Varela, B., M. Quintas Pérez, M. C. Sánchez Carreira, And P. Mourao (2022): “Covid and Public Funds: More Opportunities for a Misuse? The Case of the Intermediate Governments of Galicia,” Public Organization Review, 1–22.

Brodeur, A., Clark, A. E., Fleche, S., & Powdthavee, A. N. D. N. (2021). COVID-19, lockdowns and well-being: Evidence from Google Trends. Journal of Public Eco- Nomics, 193, 104346.

Cacciatore, F., F. Di Mascio, and A. Natalini (2022): “Do Economic Recovery Packages Open a Window of Opportunity for Corruption and Mismanagement? The Case of Italy in the Aftermath of the Covid-19 Pandemic,” Public Organization Review.

Cohen, L. E., & Felson, M. (1979). Social Change and Crime Rate Trends: A Routine Activity Approach. American Sociological Review, 44, 588–608.

Cornish, D. B. And R. Clarke (1986): The reasoning criminal, Springer-Verlag, new York, NY.

Enderwick, P. (2005). What’s Bad About Crony Capitalism? Asian Business & Management, 4, 117–132.

Faiola, A. & A. V. Herrero (2020). A pandemic of corruption: $ 40 masks,questionable contracts, rice-stealing bureacrats mar coronavirus response, The Washington Post, https://www.washingtonpost.com/world/the_americas/coronavirus-corruption-colombia-argentina-romania-bangladesh/2020/04/26/c88a9a44–8007–11ea-84c2-0792d8591911_story.html. Accessed 3 Aug 2023

Frailing, K. And D. W. Harper (2017): Toward a criminology of disaster: What we know and what we need to find out, Springer.

Gabrielson, R., L. DePillis, D. McSwane, & D. Willis (2020): “Contractors Reveals Inexperience, Fraud Accusations and a Weapons Dealer Operating Out of Someone’s House,” PROPUBLICA, https://www.propublica.org/article/a-closer-look-at-federal-covid-contractors-reveals-inexperience-fraud-accusations-and-a-weapons-dealer-operating-out-of-someones-house. Accessed 3 Aug 2023

Gallego, J., M. Prem, And J. Vargas (2021): “Inefficient Procurement in Times of Pandemic,” SSRN Working Paper.

Goodman-Bacon, A. And J. Marcus (2020): “Using difference-in-differences to identify causal effects of COVID-19 policies,”.

IMCO (2022): “Indice de Riesgos de Corrupción: Compras Públicas en México 2018- 2021,” Instituto Mexicano para la Competitividad, 49.

Krueger, A., & Card, D. (2000). Minimum Wages and Employment: A Case Study of the Fast-Food Industry in New Jersey and Pennsylvania: Reply. American Economic Review, 90, 1397–1420.

Leslie, E. & R. Wilson (2020). Sheltering in Place and Domestic Violence: Evidence from Calls for Service during COVID-19, Working Paper.

Oster, E. (2017). Unobservable Selection and Coefficient Stability: Theory and Evidence, Journal of Business & Economic Statistics, 0, 1–18.

Oster, E. (2019). Unobservable selection and coefficient stability: Theory and evidence. Journal of Business and Economic Statistics, 37, 187–204.

Peyton, K., & Belasen, A. (2012). Corruption in Emerging and Developing Economies: Evidence from a Pooled Cross-Section. Emerging Markets Finance Trade, 48, 29–43.

Rambachan, A. And J. Roth (2023): “A More Credible Approach to Parallel Trends,” The Review of Economic Studies, 90.

Rose-Ackerman, S. (2021). Corruption and COVID-19, EUNOMÍA. Revista en Cultura de la Legalidad, 16.

Sánchez-Ley, L. & R. Olmos (2020). Hijo de Bartlett Vendió al Gobierno el Ventilador Covid-19 más caro, Mexicanos Contra la Corrupción, https://contralacorrupcion.mx/hijo-bartlett-ventilador-covid-19/. Accessed 3 Aug 2023

Sobel, R., & Leeson, P. (2008). Weathering Corruption. Journal of Law and Eco- Nomics, 51, 667–681.

USDJ (2018): “Herfindahl-Hirschman Index,” Available at https://www.justice.gov/atr/herfindahl-hirschman-index. Accessed date 3 August 2023

Wolfers, J. (2006). Did unilateral divorce laws raise divorce rates? A reconciliation and new results. American Economic Review, 96, 1802–1820.

Yamamura, E. (2014): “Impact of natural disaster on public sector corruption,” Public Choice, 161.

Acknowledgements

The authors wish to thank the Instituto Mexicano para la Competitividad (IMCO) for systematizing all public hiring data in Mexico for the period 2018-2020, which made data handling easier for this paper.

Funding

The authors did not receive any specific funding for this work.

Author information

Authors and Affiliations

Contributions

The authors confirm contribution to the paper as follows: study conception and design: D.P., A.S.M. and J.B.M.; data collection: D.P.; analysis and interpretation of results: D.P., A.S.M. and J.B.M.; draft manuscript preparation: D.P., A.S.M. and J.B.M.. All authors reviewed the results and approved the final version of the manuscript.

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that we have no relevant or material financial interests that relate to the research described in this paper.

Informed consent

This research did not use any human or animal subject.

Ethical approval

This paper uses public administrative data and did not require approval from Institutional Review Boards.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Difference-in-difference Robustness Analysis Excluding One Institution at a Time (DCVB1). SOURCE: IMCO. NOTES: The solid dots represent point estimates of a difference-in-difference estimation, leaving out one institution at a time from the analysis. The brackets represent 95 percent confidence intervals. Baseline fixed effects are included at the institution, month, and year level. Robust standard errors are clustered at the institution level. 1DCVB stands for discrete-contracts-value-to-budget ratio

Event-study Robustness Analysis Excluding SEDENA (Army) from Non-Health Institutions. SOURCE: IMCO. NOTES: Plotted coefficients are event-study dummy variables, βq. The solid dots represent point estimates and the brackets represent 95 percent confidence intervals. Baseline fixed effects are included at the institution, month, and year level. Robust standard errors are clustered at the institution level. DCTC stands for discrete-contracts-to-total-contracts ratio. DCVB stands for discrete-contracts-value-to-budget ratio

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Silverio-Murillo, A., Prudencio, D. & Balmori-de-la-Miyar, J.R. The Effect of the COVID-19 Pandemic on Risk of Corruption. Public Organiz Rev (2024). https://doi.org/10.1007/s11115-024-00765-1

Accepted:

Published:

DOI: https://doi.org/10.1007/s11115-024-00765-1