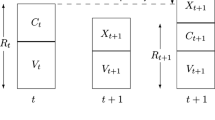

Abstract

We consider the problem of determining a sequence of payments among a set of entities that clear (if possible) the liabilities among them. We formulate this as an optimal control problem, which is convex when the objective function is, and therefore readily solved. For this optimal control problem, we give a number of useful and interesting convex costs and constraints that can be combined in any way for different applications. We describe a number of extensions, for example to handle unknown changes in cash and liabilities, to allow bailouts, to find the minimum time to clear the liabilities, or to minimize the number of non-cleared liabilities, when fully clearing the liabilities is impossible.

Similar content being viewed by others

References

Agrawal A, Boyd S (2020) Disciplined quasiconvex programming. Optim Lett 14:1643–1657

Agrawal A, Verschueren R, Diamond S, Boyd S (2018) A rewriting system for convex optimization problems. J Control Decis 5(1):42–60

Agrawal A, Amos B, Barratt S, Boyd S, Diamond S, Kolter JZ (2019) Differentiable convex optimization layers. In: Advances in neural information processing systems, pp 9558–9570

Allen F, Gale D (2000) Financial contagion. J Polit Econ 108(1):1–33

Amini H, Feinstein Z (2020) Optimal network compression. https://arxiv.org/abs/2008.08733, August

Banerjee T, Feinstein Z (2019) Impact of contingent payments on systemic risk in financial networks. Math Financ Econ 13(4):617–636

Banerjee T, Bernstein A, Feinstein Z (2018) Dynamic clearing and contagion in financial networks. arXiv preprint arXiv:1801.02091

Bardoscia M, Ferrara G, Vause N, Yoganayagam M (2019) Full payment algorithm. Available at SSRN

Bekaert G, Hodrick R (2012) International financial management, 2nd edn. Pearson Education, London

Bemporad A (2006) Model predictive control design: New trends and tools. In: IEEE conference on decision and control, pp 6678–6683

Biemond J, Lagendijk R, Mersereau R (1990) Iterative methods for image deblurring. Proc IEEE 78(5):856–883

Blackmore L, Açikmeşe B, Scharf D (2010) Minimum-landing-error powered-descent guidance for Mars landing using convex optimization. J Guid Control Dyn 33(4):1161–1171

Board of Governors of the Federal Reserve System. Reserve requirements. https://www.federalreserve.gov/monetarypolicy/reservereq.htm, March 2020

Boss M, Elsinger H, Summer M, Thurner S (2004) Network topology of the interbank market. Quant Financ 4(6):677–684

Boyd S, Vandenberghe L (2004) Convex optimization. Cambridge University Press, Cambridge

Boyd S, Vandenberghe L (2018) Introduction to applied linear algebra: vectors, matrices, and least squares. Cambridge University Press, Cambridge

Boyd S, Parikh N, Chu E, Peleato B, Eckstein J (2011) Distributed optimization and statistical learning via the alternating direction method of multipliers. Found Trends® Mach Learn 3(1):1–122

Boyd S, Busseti E, Diamond S, Kahn R, Koh K, Nystrup P, Speth J (2017) Multi-period trading via convex optimization. Found Trends® Optim 3(1):1–76

Brouwer D (2009) System and method of implementing massive early terminations of long term financial contracts. US Patent 7,613,649

Candes E, Wakin M, Boyd S (2008) Enhancing sparsity by reweighted \(\ell_1\) minimization. J Fourier Anal Appl 14(5–6):877–905

Capponi A, Chen P-C (2015) Systemic risk mitigation in financial networks. J Econ Dyn Control 58:152–166

Cho E, Thoney K, Hodgson T, King R (2003) Supply chain planning: Rolling horizon scheduling of multi-factory supply chains. In: Proceedings of the conference on winter simulation: driving innovation, pp 1409–1416

Cifuentes R, Ferrucci G, Shin HS (2005) Liquidity risk and contagion. J Eur Econ Assoc 3(2–3):556–566

Danaher P, Wang P, Witten D (2014) The joint graphical lasso for inverse covariance estimation across multiple classes. J R Stat Soc: Ser B (Stat Methodol) 76(2):373–397

Diamond S, Boyd S (2016) CVXPY: a Python-embedded modeling language for convex optimization. J Mach Learn Res 17(83):1–5

Diamond D, Dybvig P (1983) Bank runs, deposit insurance, and liquidity. J Polit Econ 91(3):401–419

D’Errico M, Roukny T (2017) Compressing over-the-counter markets. Technical report, European Systemic Risk Board

Eisenberg L, Noe T (2001) Systemic risk in financial systems. Manag Sci 47(2):236–249

Elsinger H (2009) Financial networks, cross holdings, and limited liability. Working Papers, Oesterreichische Nationalbank (Austrian Central Bank) (156)

Falcone P, Borrelli F, Asgari J, Tseng H, Hrovat D (2007) Predictive active steering control for autonomous vehicle systems. IEEE Trans Control Syst Technol 15(3):566–580

Federal Deposit Insurance Corporation. Statistics at a glance. https://www.fdic.gov/bank/statistical/stats/2019dec/industry.pdf, December 2019

Feinstein Z (2019) Obligations with physical delivery in a multilayered financial network. SIAM J Financ Math 10(4):877–906

Feinstein Z, Rudloff B, Weber S (2017) Measures of systemic risk. SIAM J Financ Math 8(1):672–708

Feinstein Z, Pang W, Rudloff B, Schaanning E, Sturm S, Wildman M (2018) Sensitivity of the Eisenberg-Noe clearing vector to individual interbank liabilities. SIAM J Financ Math 9(4):1286–1325

Fu A, Narasimhan B, Boyd S (2019) CVXR: an R package for disciplined convex optimization. J Stat Softw

Glasserman P, Young H (2015) How likely is contagion in financial networks? J Bank Financ 50:383–399

Grant M, Boyd S (2008) Graph implementations for nonsmooth convex programs. In: Recent advances in learning and control. Lecture Notes in Control and Information Sciences. Springer, Berlin, pp 95–110

Grant M, Boyd S (2014) CVX: Matlab software for disciplined convex programming, version 2.1

Harris T, Ross F (1955) Fundamentals of a method for evaluating rail net capacities. Technical report, RAND Corp, Santa Monica, CA

Jochems A, Deist TM, Van Soest J, Eble M, Bulens P, Coucke P, Dries W, Lambin P, Dekker A (2016) Distributed learning: developing a predictive model based on data from multiple hospitals without data leaving the hospital–a real life proof of concept. Radiother Oncol 121(3):459–467

Kahn A (1962) Topological sorting of large networks. Commun ACM 5(11):558–562

Khabazian A, Peng J (2019) Vulnerability analysis of the financial network. Manag Sci 65(7):3302–3321

Kusnetsov M, Veraart L (2019) Interbank clearing in financial networks with multiple maturities. SIAM J Financ Math 10(1):37–67

Land A, Doig A (1960) An automatic method of solving discrete programming problems. Econometrica 28(3):497–520

Liu Y, Gooi HB, Xin H (2017) Distributed energy management for the multi-microgrid system based on ADMM. In: Power & energy society general meeting. IEEE, pp 1–5

Lofberg J (2004) YALMIP: a toolbox for modeling and optimization in MATLAB. In: IEEE international conference on robotics and automation. IEEE, pp 284–289

Ma Y, Borrelli F, Hencey B, Coffey B, Bengea S, Haves P (2011) Model predictive control for the operation of building cooling systems. IEEE Trans Control Syst Technol 20(3):796–803

Mattingley J, Boyd S (2009) Automatic code generation for real-time convex optimization. In: Convex optimization in signal processing and communications, pp 1–41

Mattingley J, Boyd S (2012) CVXGEN: a code generator for embedded convex optimization. Optim Eng 13(1):1–27

Mattingley J, Wang Y, Boyd S (2011) Receding horizon control. IEEE Control Syst Mag 31(3):52–65

Moehle N, Busseti E, Boyd S, Wytock M (2019) Dynamic energy management. In: Large scale optimization in supply chains and smart manufacturing. Springer, Berlin, pp 69–126

MOSEK optimization suite (2020). https://www.mosek.com

O’Kane D (2014) Optimizing the compression cycle: algorithms for multilateral netting in OTC derivatives markets. Available at SSRN 2273802

O’Kane D (2017) Optimising the multilateral netting of fungible OTC derivatives. Quant Financ 17(10):1523–1534

Rawlings J, Mayne D (2009) Model predictive control: theory and design. Nob Hill Publishing, San Francisco

Rogers L, Veraart L (2013) Failure and rescue in an interbank network. Manag Sci 59(4):882–898

Rudin L, Osher S, Fatemi E (1992) Nonlinear total variation based noise removal algorithms. Phys D: Nonlinear Phenom 60(1–4):259–268

Schuldenzucker S, Seuken S (2019) Portfolio compression in financial networks: incentives and systemic risk. Available at SSRN

Shapiro A (1978) Payments netting in international cash management. J Int Bus Stud 9(2):51–58

Soltani M, Wisniewski R, Brath P, Boyd S (2011) Load reduction of wind turbines using receding horizon control. In: IEEE international conference on control applications. IEEE, pp 852–857

Udell M, Mohan K, Zeng D, Hong J, Diamond S, Boyd S (2014) Convex optimization in Julia. Workshop on high performance technical computing in dynamic languages

Veraart L (2019) When does portfolio compression reduce systemic risk? Available at SSRN 3488398

Wang Y, Boyd S (2009) Performance bounds for linear stochastic control. Syst Control Lett 58(3):178–182

Yuan M, Lin Y (2006) Model selection and estimation in regression with grouped variables. J R Stat Soc: Ser B (Stat Methodol) 68(1):49–67

Acknowledgements

The authors would like to thank Zachary Feinstein and Luitgard Veraart for their helpful discussion and comments on an early draft of the paper. The authors would also like to thank Daniel Saedi for general discussions about banking. Shane Barratt is supported by the National Science Foundation Graduate Research Fellowship under Grant No. DGE-1656518.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

A Sparsity preserving formulation

A Sparsity preserving formulation

In this section we describe a sparsity-preserving formulation of problem (8). We make use of the fact that \(L_t\) and \(P_t\) are at least as sparse as \(L^\mathrm {init}\) (see Sect. 3).

First, let \(m=\mathbf {nnz}(L^\mathrm {init})\) and \(I_k \in \{1,\ldots ,n\} \times \{1,\ldots ,n\}\), \(k=1,\ldots ,m\), be the sparsity pattern of \(L^\mathrm {init}\), meaning \((L^\mathrm {init})_{ij}=0\) for all \((i,j)\not \in I_k\), \(k=1,\ldots ,m\). Instead of working with the matrix variables \(L_t\) and \(P_t\), we work with the vector variables \(l_t\in {\text{ R }}_+^m\) and \(p_t\in {\text{ R }}_+^m\), which represent the nonzero entries of \(L_t\) and \(P_t\) (in the same order). That is,

The initial liability is given by \(l^\mathrm {init}\in {\text{ R }}_+^m\), which contains the nonzero entries of \(L^\mathrm {init}\). The sparsity preserving formulation of the optimal control problem (8) has the form

where \(S^\mathrm {row}\in {\text{ R }}^{n \times m}\) sums the rows of \(P_t\), i.e., \(S^\mathrm {row}p_t=P_t\mathbf{1}\), and \(S^\mathrm {col}\in {\text{ R }}^{n \times m}\) sums the columns of \(P_t\), i.e., \(S^\mathrm {col}p_t=P_t^T\mathbf{1}\). The cost functions are applied only to the nonzero entries of \(L_t\) and \(P_t\), so they take the form \(g_t:{\text{ R }}_+^n \times {\text{ R }}_+^m \times {\text{ R }}_+^m\rightarrow {\text{ R }}\cup \{+\infty \}\) and \(g_T:{\text{ R }}_+^n \times {\text{ R }}_+^m\rightarrow {\text{ R }}\cup \{+\infty \}\). Problem (19) has just \(2T(n+m)\) variables, which can be much fewer than the original \(2T(n+n^2)\) variables when \(m \ll n^2\).

Rights and permissions

About this article

Cite this article

Barratt, S., Boyd, S. Multi-period liability clearing via convex optimal control. Optim Eng 24, 1387–1409 (2023). https://doi.org/10.1007/s11081-022-09737-0

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11081-022-09737-0