Abstract

This paper examines German and foreign bank factors that can explain net flows of cross-border central bank liquidity between Germany and the rest of the euro area. Using data from the German component of Eurosystem’s real-time gross settlement system TARGET2 and BankFocus for the period between 2009 and 2021, we provide empirical evidence that only few balance sheet items and profit and loss accounts affect net flows with Germany. We control for bilateral bank-specific relationships and time-varying macroeconomic country effects in our regressions. In general, German bank factors seem to be more important than characteristics of foreign banks. A German bank that exhibits relatively high claims against central banks seems to attract less additional central bank liquidity from abroad than a German bank with fewer existing central bank claims. Net claims against central banks, which also control for liabilities, have no effect on net transactions in TARGET2. However, higher overall liquidity of a German credit institution corresponds to additional net inflows. Foreign bank factors only matter for central bank payments and intragroup payments. We also document heterogeneities across different types of transactions which influence the German TARGET2 balance. While customer payments, interbank payments and central bank payments have increased net flows to Germany in sum, intragroup payments and ancillary systems’ transactions have led to net outflows.

Similar content being viewed by others

1 Introduction

At the onset of the global financial crisis, claims against the ECB caused by the settlement of cross-border payments in the Eurosystem’s Trans-European Automated Real-time Gross Settlement Express Transfer System (TARGET2) began to accumulate on the Bundesbank’s balance sheet.Footnote 1 Afterwards, periods of growing balances alternated with phases of temporary declines. The Bundesbank has repeatedly commented on the growth pattern of TARGET2 balances in the Eurosystem in multiple Monthly Reports as well as in its Annual Report. These analyses are based on macroeconomic data and interrelationships. Since 2015, the asset purchases conducted by the Eurosystem under its expanded asset purchase programme (APP) and the pandemic emergency purchase programme (PEPP) have become an important factor for the evolution of national TARGET2 balances.

So far, the literature on the determinants of national TARGET2 balances was based on macroeconomic dynamics between the TARGET2 balances and other variables. One of the first authors who systematically scrutinized specific determinants of TARGET2 balances in a panel analysis was Auer (2014). He came to the conclusion that current account developments were not essential for TARGET2 dynamics in the pre-crisis period. However, they gained in importance, when insolvency risk in some countries with current account deficits arose and private capital inflows dried up. Hristov et al. (2020) come to a similar conclusion, when they state that between 2008 and 2014 changes in TARGET2 balances where mainly driven by shocks in capital flows. In the same vein, Cheung et al. (2020) use modified TARGET2 series to analyse capital flight to Germany. They find that policy uncertainty and the ECB collateral policy are key factors. Finally, Bettendorf and Jochem (2023) used a BVAR model in order to decompose German TARGET2 dynamics to variable impacts of global risk shocks, domestic risk shocks and monetary policy shocks. All these studies rely on macroeconomic data.

This paper instead focuses on bilateral payments in the TARGET2 system and isolates the various types of transactions as classified in TARGET2 such as customer payments, interbank payments, intragroup payments, transactions related to the settlement of ancillary systems and transactions involving at least one (domestic or foreign) central bank, that can imply cross-border flows of central bank liquidity within the Eurosystem. In our data set, we do not have any further information on the underlying business transaction or the characteristics of the ultimate counterparty. We examine the individual factors based on specific balance sheet items of the banks involved. We use transaction data from the German component of TARGET2 between January 2009 and December 2021. The micro data allows us to identify relationships not only at the country level but also for individual credit institutions. To this end, we look at balance sheet items and profit and loss (P&L) accounts of both, domestic and foreign banks. This approach enables to differentiate between institution-specific and regional factors. In addition, we can separately scrutinize the effects for various types of transactions.

Complementary to previous research that uses aggregated TARGET2 data, we are able to examine the following two issues: which types of transactions in the German TARGET2 component trigger the overall development of the Bundesbank’s TARGET2 claims? Besides macroeconomic determinants and monetary policy, do specific balance sheet items of individual commercial banks play a role in explaining changes in national TARGET2 balances? In other words we concentrate on specific characteristics of individual banks that lead to different outcomes for banks within the same jurisdiction. These factors represent the funding structure and other fundamentals which are indirectly linked to individual risk exposures. Consequently, it is generally not possible to compare our outcomes with specific expectations deducted from macroeconomic experience like the effects of the European debt crisis or monetary policy.

For the analysis, we use the commercial database BankFocus operated by Bureau van Dijk. The data deliver yearly balance sheets as well as P&L accounts between 2009 and 2021. For the analysis of cross-border developments, it is necessary to link the individual balance sheet and P&L data with bilateral flows in TARGET2. We use fixed effects models (including bilateral German bank-foreign bank fixed effects and country-time specific fixed effects) to regress transaction data from the German TARGET2 component on relevant institution-specific factors.

We aggregate the transaction data per bilateral credit institution pair. The descriptive illustration of the TARGET2 transactions relies on monthly aggregated values by different types of transaction. In the regression analysis, we use the yearly frequency of the bilateral German bank and foreign bank pairs to match the information from BankFocus. Furthermore, clusters of German and foreign banks are formed in order to consider serial correlation and heteroscedasticity. Going beyond the baseline estimation, we perform several robustness checks on a series of alternative specifications.

We find two main results. First, we document heterogeneities across different types of transactions which influence the Bundesbank’s TARGET2 claims. In particular, customer payments of non-financial firms and interbank transactions increase the central bank liquidity in Germany. This might reflect Germany’s current account surpluses during the observation period and heterogeneous refinancing conditions of commercial banks across the euro area.

Since the European debt crisis in 2012, central bank payments have also entailed net flows to Germany. These are defined as payments where the sender and/or the receiver is a central bank. Central bank payments include not only monetary policy operations, but also cash operations, foreign reserve management and payments between central banks. As the purchases in the course of the APP and the PEPP are settled by the use of securities settlement systems, their transactions cannot be cleanly identified with TARGET2 transaction data.

In contrast, intragroup payments have led to net outflows during the observation period. Combined with the development of interbank payments, a certain portion of loans granted by foreign banks to German banks might have been reallocated again to foreign countries via internal capital markets.Footnote 2

In sum, the transactions related to the settlement of ancillary systems have also decreased the German TARGET2 claims. They comprise transactions being initially processed via alternative payment systems such as Euro1.

Moreover, the TARGET2 balance isolated by various types of transactions illustrates the architectural complexity of the TARGET2 system. Different types of payments and participation arrangement as well as the existence of independent ancillary systems result in cross-border flows that are not only due to discretionary decisions by TARGET2 participants rather than technical circumstances given the legal and technical design of TARGET2. These structural flows seem to have a relevant impact on the development of TARGET2 balances.

Second, we provide empirical evidence that only some specific balance sheet items and P&L accounts affect net flows to Germany, once we control for bilateral bank-specific relationships and time-varying macroeconomic country effects. In general, German bank factors seem to be more important than characteristics of foreign banks. Robust German banks with a higher level of liquidity attract further central bank liquidity. In contrast, higher claims against central banks, which constitute a certain fraction of German bank liquidity and point to a potential excess of central bank liquidity, lower net flows to German banks. Therefore, the type of bank liquidity strictly matters.

An alternative approach might be to use net claims against central banks, i.e. claims minus liabilities, instead of gross claims. These net claims are typically positive in TARGET2 surplus countries and negative in TARGET2 deficit countries. We approximate them using more granular balance sheet information from BankFocus. We find insignificant coefficients for this specification. Alternatively, claims and liabilities to the central bank could separately enter the regression. Interestingly, high central bank liabilities of foreign banks tend to lower interbank payments to Germany.

2 Data

2.1 TARGET2 Transactions

TARGET2, the Eurosystem’s real-time gross settlement system, is an integrated platform on which every Eurosystem central bank owns and operates its TARGET2-component. In 2021, on average, 373,000 payments with a total value of €1.9 trillion have been settled each business day. The Bundesbank’s TARGET2 component accounts for 38% of the turnover in terms of value (European Central Bank 2022). TARGET2 balances are a result of cross-border payment flows in central bank money within the decentralized structure of the Eurosystem. Figure 1 presents the evolution of the German TARGET2 balance (end of month values) between January 2009 and June 2022. The TARGET2 claims increased sharply during three different time periods: first, between the global financial crisis beginning in 2007-08 and the peak of the European debt crisis in mid-2012; second, with the start of the APP in 2015Footnote 3; and third, with the start of the COVID-19 pandemic and the implementation of PEPP in 2020. Until now, it has been unclear whether individual bank characteristics matter in explaining these aggregate developments, in addition to macroeconomic determinants.

German TARGET2 balance, January 2009 – June 2022

To shed light on this issue, we use transaction data from the German TARGET2 component (TARGET2-Bundesbank) based on individual bank accounts. The raw data includes bilateral pairs: a sender and a recipient of euro payments. Either the sender or the recipient has to be a bank holding its account in TARGET2-Bundesbank. In our paper, we assign a bank to a specific country according to the TARGET2 component in which the account is operated. This means that a “German bank” is a bank which operates an account in TARGET2-Bundesbank irrespective of its legal country of origin. Therefore, a cross-border transaction in this analysis does not necessarily depict a cross-border flow across geographical borders according to the banks’ head institutions’ residencies, but rather a flow between different TARGET2 component systems in which the banks’ accounts are operated. This dataset can perfectly replicate the development of the German TARGET2 balance as shown in Figure 1. Therefore, we do not need to use interpolation techniques or any other data source.

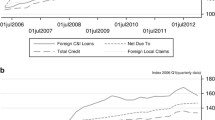

Furthermore, the TARGET2 transaction data contain information about the type of payment derived from various criteria such as the SWIFT message type being used. We assign the types of transactions to different transaction categories as described in Table 1. Figure 2 provides the 12-month moving average rolling windows of monthly total net cross-border flows to German banks and compares the overall evolution of the German TARGET2 claim according to different transaction categories for the period between January 2009 and December 2021: customer payments, interbank payments, intragroup payments, central bank payments, payments related to ancillary systems and other types of transactions (rest). In general, we observe heterogeneous developments depending on the specific transaction type. Customer payments, interbank payments and central bank payments in particular tend to increase the overall German TARGET2 claims.Footnote 4

Development of monthly total net cross-border flow to German banks by different transaction categories

The positive balance, inflows minus outflows, of customer payments in panel (a) coincides with Germany’s current account surpluses during the observation period. However, individual customer payments are not necessarily linked to current account transactions, since they may also reflect capital account transactions on behalf of costumers such as security purchases or other forms of investment. Furthermore, positive net flows of interbank payments in panel (b) may reflect diverging financing conditions of commercial banks across various euro area countries. For instance, German banks may have relatively easy access to private financial markets whereas other banks rely heavily on open market operations with the central bank. This might bias interbank flows towards Germany. Finally, central bank payments in panel (d) increase central bank liquidity allocated to the Bundesbank.

Other transaction categories show a negative impact on German TARGET2 claims: intragroup payments in panel (c) and transactions related to the settlement of ancillary systems in panel (e). One possible interpretation of the negative intragroup balance is that German banks provide loans to their foreign branches and subsidiaries. The negative balance of ancillary systems’ transactions is large but difficult to interpret, since information on the underlying business transaction is not available. Payments related to the settlement of ancillary systems seem to be driven mainly by structural flows when these systems have their accounts in a specific component system. The category “rest” in panel (f) is hard to interpret from an economic point of view as well, as it predominantly contains transactions with a rather technical character due to the design of TARGET2. As most of the transactions in this category are not of a cross-border characteristic, liquidity transfers from and to TARGET2 Securities (T2S)Footnote 5 are supposed to be the major factor therein.

Table 2 provides further descriptive statistics of the TARGET2 transactions settled in the German TARGET2 component. We observe about 4.6 million bilateral relationships between January 2009 and December 2021. On average, gross inflows and outflows amounted to well above €170 million per observation, i.e. per business relationship and month. Inflows slightly exceeded outflows resulting in net inflows of roughly €250 thousand per observation, on average. About 60% in volume of all transactions are customer payments. Although this category accounts for the largest fraction of observations, the average net flow is relatively low (€4.17 million). Interbank transactions represent 27% of the observations in volume but account for the bulk of transactions in value terms: the average central bank liquidity flowing to Germany amounted to almost €18 million per bank-bank pair and month. In contrast, 7% of all observations relate to intragroup transactions, which lead to outflows of about €30 million on average across all observations. Central bank payments constitute only 3% of observations but result in large inflows of central bank liquidity (€80 million on average). The largest countermovement is represented by ancillary systems’ transactions.

These summary statistics are also in line with the evolution of the transaction categories over time in Fig. 2. The right-hand columns of Table 2 illustrate the yearly aggregated transaction data. We provide these as we match the TARGET2 data with balance sheet items and P&L accounts supplied by BankFocus, which are available only at a yearly frequency. However, the interpretation of these numbers is much the same as for the monthly transactions.

Another dimension of interest is the TARGET2 country of the foreign bank. We define “foreign bank” in our paper as a bank which operates an account in a TARGET2 component other than TARGET2-Bundesbank. This means a “foreign bank” is a bank, which does not operate an account in TARGET2-Bundesbank irrespective of its legal country of origin. Table 3 illustrates the bilateral net flows between TARGET2-Bundesbank and the other component systems. The aggregated TARGET2 data do not provide such information as they represent the overall claims of the national central banks against the ECB. German banks conduct most transactions with banks from Italy, France, Spain, the Netherlands and Austria. Regarding the net flows, German banks receive inflows on average mostly from Luxemburg, the Netherlands, Denmark and Ireland. In contrast, outflows mainly reach accounts held at the ECB (as the ECB owns and operates its own TARGET2 component), Finland and Italy. These numbers have to be interpreted with caution, because the table only provides information about the TARGET2 country, i.e. the component system in which the transaction is settled by the immediate correspondent bank acting as direct TARGET2 participant. This does not necessarily coincide with the geographical home country of the originator or the beneficiary of the respective transaction.

2.2 BankFocus

We examine whether individual German or foreign bank determinants have an impact on TARGET2 transactions in the German component system. Therefore, we need data sources which provide additional information about banks that can be matched with the TARGET2 data. We use yearly data from Moody's Analytics BankFocus between 2009 and 2021. It combines renowned content from Bureau van Dijk and Moody's Investors Service, with expertise from Moody's Analytics. The dataset itself contains detailed, standardized reports and ratios for over 45,000 banks and 16,000 insurance companies across the globe. For our purposes, we concentrate on the following items from the balance sheet and P&L accounts for German and foreign banks as we perceive them as potentially having an influence on TARGET2 transactions: profits, claims against central banks, customer deposits, bank deposits, equity and liquidity.Footnote 6 Appendix Table 10 provides information on the definitions of these variables.

Matching quality of TARGET2 data with BankFocus by transaction category

In this paper, we concentrate on sender and receiver banks that act as direct participants in TARGET 2.Footnote 7 Since these banks have an eleven digit Business Identifier Code (BIC) following the BIC standard ISO 9362 (1,714 units of German and foreign banks) as identifier and BankFocus provides a Legal Entity Identifier (LEI), we need to merge both identifiers.Footnote 8 We perform the matching in two steps. First, we start by using data from the Global Legal Entity Identifier Foundation (GLEIF), which is an international nonprofit organisation. It provides monthly master files mapping BICs to LEIs at a specific point in time. Since banks may become insolvent or be acquired by other financial institutions, these master files change over time. Therefore, we merge the BICs from the TARGET2 transaction data with the latest available information from GLEIF (December 2021). Then, we store the matched observations and keep the unmatched BICs. These unmatched BICs are merged with the GLEIF master file from November 2021. We repeat this process up until the January 2018 file.Footnote 9 This approach matches 964 units of the 1,714 BICs with LEIs, which results in a matching rate of 56%. Second, we manually check the unmatched BICs against the master file information from BankFocus and use the bank name and location to identify a best possible match. This manual checking results in a total of 1,610 matched BIC units, which represents almost 94% of all banks in the original dataset.

Figure 3 compares the net flows to German banks resulting from the transactions of all observations (“overall”) with the net flows resulting from the merged transactions of BankFocus (“matched”). We proceed in three steps to optimize the matching quality. First, we establish the BankFocus data set. We combine unconsolidated and consolidated balance sheet items of the matched LEIs.Footnote 10 Some LEIs provide information on consolidated and unconsolidated balance sheets. We choose the type with the longest duration to consider as much information as possible. If the duration coincides for both types, we keep the unconsolidated balance sheet.Footnote 11 Since every transaction contains one German and one foreign BIC, we generate one dataset for the German identifier and one for the foreign identifier.

Second, we combine the 1,610 BICs of the German TARGET2 component with the 1,096 LEIs of BankFocus. Since every transaction contains the BIC of a German bank and the BIC of a foreign bank, we match the identifiers in a way that provides us with the balance sheet information and P&L of the German bank and of the foreign bank for every transaction in a particular year. In the end, we have several missing values for the twelve variables (six German factors and six foreign factors). The reason lies in the unbalanced panel structure of BankFocus.

Third, we exclude some factors, at most two of the twelve, for the different transaction categories to maximise the match as much as possible. The graphs in Fig. 3 suggest that the match explains the development quite well.Footnote 12 Prior to 2013 our match overestimates the overall evolution as panel (a) highlights. The transactions of ancillary systems seem to drive this fact (see panel (f)). Some declarants in this category provide balance sheet information and P&L accounts only from 2013. The matched values of customer payments (panel (b)) and central bank payments (panel (e)) coincide with the raw data. In contrast, the match of interbank in panel (c) (intragroup in panel (d)) payments underestimates (overestimates) the evolution since 2016. Nevertheless, the variation of both matches also represents the raw data quite well. In several robustness checks later on, we estimate whether the choice of German and foreign factors has an effect on our baseline results. In addition, we provide insights for the subsample beginning in 2013.

Table 4 compares the different yearly raw data sets with the matched BankFocus data. The signs for almost all transaction categories and the overall category are the same and the standard deviation is very similar. The matching rate of the observations is about 64%. Table 4 confirms the previous observations from the graphs in Fig. 3. Although BankFocus is an unbalanced panel data set, the matched transactions seem to represent the raw data quite well.

3 Regressions

3.1 Method

In the following, we examine possible determinants of German and foreign banks, which might help to explain the evolution of the German TARGET2 balance. We estimate the following equation using OLS with different fixed effects:

where Net flowsgft are the net flows, defined as inflows minus outflows, to Germany in TARGET2 of German bank g from foreign bank f in year t for each transaction category.Footnote 13 We normalise these flows by dividing them by the total assets of the German bank in the previous year t-1. Factorsgt-1 (Factorsft-1) describe the individual factors of German (foreign) bank b (f) in the previous year t-1. They include the following variables: profits, claims against central banks, customer deposits, bank deposits, equity and liquidity for German and foreign banks. We divide all German (foreign) factors by the total assets of the German (foreign) bank in the previous year t-1 to normalise and make them comparable to the relative net flows. \(\eta\) gf denotes bilateral German and foreign bank fixed effects, which absorb time-invariant relationship-specific effects. Since German banks interact with several banks of the same country at the same time, we can control for any country-time-varying fixed effects \(\phi\) ct. They completely absorb macroeconomic country-specific developments, which could explain the German TARGET2 balance. εgft is the error term. We cluster all standard errors over German banks and foreign banks to account for heteroscedasticity.

We are mostly interested in vectors β and γ that indicate whether individual factors of German banks or of foreign banks matter for the (relative) net flows to Germany in TARGET2.

Table 5 provides an overview of the signs that we expect for the different variables. Since the transaction categories are rather heterogeneous, we distinguish between payments related to customers, interbank payments, intragroup payments and central bank payments. We also differentiate between the effects of German banks versus foreign banks. In general, since we examine net flows to Germany, the expected sign of foreign banks is typically the opposite of the one for German banks.

We expect that customer payments on behalf of non-financial firms typically accrue to banks that are heavily engaged in retail banking (customer deposits) and in the interbank market (bank deposits).

In contrast, German and foreign banks manage their interbank payments themselves. The German individual factors may influence these payments in different ways: profits and equity might attract net inflows, since they indicate sound fundamentals of the recipient. In addition, higher bank deposits might reflect better access to the interbank market, which should, per se, correspond to above average financial inflows. On the other hand, abundant claims against central banks and high overall liquidity may give the German banks an incentive to transfer potential excess liquidity abroad. Therefore, we expect a negative relationship between these two variables and German net flows. The factors of foreign banks should typically have the opposite effects on financial flows to Germany, because we expect them to work similarly but inversely.

The management of intragroup payments may differ because these transactions serve as internal capital markets for banks. Higher profits and a stronger equity ratio of German banks support their equity capital, which might facilitate net outflows to affiliated institutions abroad. In a similar vein, an increase in claims against central banks and higher overall liquidity could lead to an incentive to transfer this liquidity abroad. In contrast, higher bank deposits signal good access to the interbank market through internal group financing, which leads to an increase in net flows. Again, foreign factors are assumed to have the opposite sign.

Finally, for central bank payments, all German factors, with the exception of customer deposits, are expected to show a negative relationship with financial inflows, because banks with strong fundamentals typically concentrate on private financial markets and rely less on operations with the central bank in order to meet their financial needs. This should result in lower central bank liquidity flows to Germany. That is why we expect only positive coefficients for foreign bank variables.

3.2 Results

Table 6 presents our baseline regression results for the period between 2009 and 2021.Footnote 14 We exclude customer deposits of German and foreign banks for overall, intragroup, central bank and liquidity transactions, because otherwise the clustering of standard errors over German and foreign banks does not produce standard errors due to potential singularity problems.

Column (1) presents the estimates for German net inflows relative to total assets in the aggregate of all transaction categories. An increase in the liquidity ratio of German banks in the previous period by 1 percentage point leads to a statistically significant rise in inflows via TARGET2 by 0.14 percentage point. All other German and foreign determinants are insignificant. This empirical finding contradicts the economic intuition that German banks with abundant liquidity have an incentive to invest these liquid assets, inter alia abroad. However, these banks seem to be especially attractive for foreign counterparties such that they also receive vast amounts of liquidity. This second effect seems to overcompensate for the incentive to invest.

Column (2) illustrates that German bank factors affect customer payments, once we control for country-year fixed effects. While claims against central banks have a weakly significant negative influence on German net flows, customer deposits, bank deposits and the liquidity ratio increase central bank liquidity allocated in Germany. These estimates completely coincide with our previous expectations. Customer payments on behalf of non-financial firms mainly accrue to credit institutions, which engage heavily in retail banking and the interbank market. As a result, those banks receive more liquidity via TARGET2 in the category of customer payments. The economic significance, however, is rather small, since the effects range between 0.03 (liquidity) and 0.07 (claims against central banks) percentage points.

Column (3) provides estimates for the interbank market. Almost all coefficients are insignificant with the exception of German bank’s profits, which, as expected, exhibit a (weakly) positive effect. An increase in profits by 1 percentage point leads to a 0.6 percentage point rise in TARGET2 inflows.

According to the results of intragroup payments in column (4), German bank factors do not matter at all. However, higher equity of foreign banks by 1 percentage point increases net flows to Germany by about 4 percentage points and vice versa. This result is in line with what we expected: higher equity capital from abroad entails outflows from the German affiliate.

The determinants of central bank payments in column (5) provide rather mixed results. German banks which have higher claims against the central bank, receive lower additional net flows from abroad. From an economic perspective, these banks have no further incentive to receive additional liquidity. However, German and foreign banks with higher liquidity both receive more net flows from abroad. Similar to relationships in other transaction categories, overall liquidity and claims against central banks work in the opposite direction. Only existing central bank liquidity seems to impede additional financial inflows. Aside from that, foreign banks with higher profits decrease net flows to Germany. It should be noted that we only analyse cross-country transactions between a German and a foreign institution. This excludes transactions between a central bank and a commercial bank on site, which means that the bulk of standard open market operations conducted by the Eurosystem does not enter our regressions.

Finally, we find some significant coefficients for transactions in ancillary systems (column 7). However, due to different types of ancillary systems being involved and the lack of information on the underlying business case, we cannot interpret the results from an economic perspective.

To summarise, we find that only few balance sheet items and P&L accounts affect inflows to Germany, once we control for bilateral bank-specific relationships and time-varying macroeconomic country effects.Footnote 15 In general, German bank factors seem to be more important for net flows to Germany than characteristics of foreign banks.Footnote 16 To some extent this might be due to the fact that the coefficients for foreign banks reflect the impact of the specific balance sheet items for bilateral transactions with German banks only, whereas the respective coefficients for German banks describe the effects on transactions with any foreign bank connected to the TARGET2 system. A higher liquidity level of German banks increases net flows to Germany even further. By contrast, higher claims of German banks against central banks impede the flow of additional central bank liquidity from abroad to Germany.

3.3 Robustness Checks

3.3.1 Consolidated Versus Unconsolidated Data

Appendix Table 11 and Appendix Table 12 show that these results do not depend on the type (consolidated vs. unconsolidated) of balance sheet. Foreign bank factors, however, only matter when considering unconsolidated balance sheets. Here, they have an (albeit limited) impact on central bank payments and intragroup payments (Appendix Table 12). The respective items in unconsolidated balance are all insignificant (Appendix Table 11).

3.3.2 Balance Sheet Items and P&L Accounts of Central Banks

We define the transaction categories in Table 6 in a consistent way. However, central bank payments involve either the Bundesbank or another Eurosystem national central bank. The characteristics of the central banks should not play an important role compared to the balance sheet items and P&L accounts of private commercial banks. That is why, in a robustness check for central bank payments, we concentrate on transactions, where only one central bank is involved. For transactions related to the Bundesbank (a foreign central bank), only foreign (German) bank variables are included as potential determinants. Table 7 presents the results. We see in column (1) that foreign bank characteristics do not matter for transactions with the Bundesbank. According to column (2) the claims of German banks against the Bundesbank still have a significant negative effect on net flows to Germany. However, overall liquidity becomes insignificant.Footnote 17 Therefore, this alternative analysis of transactions matters for the estimates. Now, they are more in line with our previous expectations.

3.3.3 Excluding Variables with Many Missing Values

Our baseline scenario uses as many factors as possible and only excludes variables that would cause singularity in standard errors. Table 8 concentrates on different subsamples which exclude variables with many missing values.Footnote 18 The estimates are similar if we compare these adjusted samples with the baseline regressions. The previous conclusion that higher claims of German banks against central banks decreases net flows to Germany becomes weaker. In addition, the coefficients for central bank payments change a little. All in all, the results are slightly weaker than before.

3.3.4 Adjusting the Observation Period

Figure 3 highlights that some balance sheet information is available beginning only from 2013. At least for the overall TARGET2 transactions and the ancillary systems, missing data are responsible for the relatively poor matching quality before 2013. That is why we conduct another robustness check with a sample beginning in 2013. Table 9 provides the estimates. Again, as with the adjusted factor sample, the regression results remain robust compared to the baseline setting. Furthermore, the match is not representative at the current end, as Fig. 3 has shown. However, the results remain the same if we exclude 2021 from our sample. Therefore, the current end does not drive our main results.

3.3.5 Net Claims and Liabilities Against Central Banks

What theoretically matters would not only be the claims against central banks, but rather the “net claims”, i.e. claims minus liabilities. These are typically positive in TARGET2 surplus countries and negative in TARGET2 deficit countries. In a template covering the International Financial Reporting Standard (IFRS) BankFocus delivers more granular information on various balance sheet items. Specifically, the IFRS template offers three variables which are related to central banks: balances with central banks other than mandatory reserve deposit (assets), mandatory reserve deposits with central banks (assets) and deposits from central banks (liabilities). The sum of both asset variables are defined as claims against central banks and the deposits as liabilities against central banks. We calculate “net claims” as claims minus liabilities.

Appendix Table 13 provides the results for net claims against central banks.Footnote 19 Compared to our previous results, we now find insignificant coefficients. Alternatively, claims and liabilities to the central bank could separately enter the regression as in Appendix Table 14. Interestingly, high central bank liabilities of foreign banks tend to lower interbank payments to Germany. This seems to contradict the experience of the last decade, when banks in some countries with large TARGET2 liabilities used the surplus of central bank money to transfer liquidity to Germany. However, this observation might only hold during episodes of abundant central bank liquidity. In other times, especially those banks make use of central banks operations that are relatively scarce of liquidity and have to use it for domestic needs. Furthermore, not all banks report information about claims and liabilities against central banks in the IFRS template which results in a massive drop in observations. Further robustness checks show that indeed this lower number of observations seems to drive the insignificant results instead of the variables themselves.

Central bank payments cannot be examined in the same manner as in Appendix Table 13, since central banks do not provide this information. Therefore, we adjust Table 7 and consider net claims as well as claims and liabilities against central banks if only one of the transaction partner involves a central bank. Appendix Table 15 shows that all variables, with the exception of liquidity of German banks, become insignificant. Again, the number of observations is lower compared to before. These results do not contradict to our previous estimates.

4 Conclusions

This paper examines whether – besides macroeconomic factors and monetary policy – balance sheet items and P&L accounts of German and foreign bank factors have a net effect on central bank liquidity flows to Germany. Using data from TARGET2-Bundesbank and BankFocus for the period between 2009 and 2021, we provide empirical evidence that only few individual bank factors affect net flows to Germany. We control for bilateral bank-specific relationships and time-varying macroeconomic country effects in our regressions. In general, German bank factors seem to be more important than characteristics of foreign banks. This might partly be due to the fact that we analyse bilateral flows, where only transactions with Germany are included. Insofar, the design of our study is not symmetric. Higher claims against central banks impede the flow of additional central bank liquidity from abroad to Germany. Conversely, a higher overall stock of liquid assets held by German banks attracts additional net inflows. Foreign bank factors only matter for central bank payments and intragroup payments. As the architectural design of TARGET2 as well as the technical character of parts of transactions influence the TARGET2 balance structurally, we also document heterogeneities across different transaction categories impacting the German TARGET2 balance. While customer payments, interbank payments and central bank payments increase net flows to Germany, intragroup payments and ancillary systems’ transactions lower these flows. When interpreting these results, however, we should keep in mind that many bilateral transactions are part of financial chains and do not reflect business relationships between an ultimate sender and an ultimate recipient. Analysing those more complex financial flows may be subject to future research.

Notes

TARGET2 may run on a single shared platform, but it is made up of multiple component systems operated by the national central banks and the ECB. Net flows between the component systems are balanced by TARGET2 claims or liabilities of the respective national central bank.

In some cases, however, “interbank” and “intragroup” transactions, cannot clearly be distinguished, as not all intragroup payments are classified as such. However, these cases of “false classification” should be of minor importance.

Rossi (2012) highlights that some structural differences between European countries exist such that TARGET2 imbalances automatically occur by construction. This is only partly true since with the start of the public sector purchase programme (PSPP) the German TARGET2 claims can be mostly explained by monetary policy operations. For further explanations, see Deutsche Bundesbank (2017a) and Deutsche Bundesbank (2017b).

The only period in which customer payments were lower than the overall development was during the COVID-19 pandemic. During this time, a negative global shock hit the world economy.

TARGET2-Securities (T2S) is a computer-assisted system operated by the Eurosystem for the harmonised and centralised settlement of securities transactions in central bank money.

According to the TARGET2 participation rules, banks from outside the European Economic Area are not allowed to directly participate in TARGET2.

In general, the number of LEIs is lower than BICs since not every bank account is legally independent. That is why one LEI can be assigned to several BICs.

The GLEIF website does not provide data from before January 2018.

In total, we identify 1,096 LEIs. Focusing purely on unconsolidated balance sheets of banks results in 954 LEIs, while we have 531 LEIs for consolidated balance sheets. For some large banks, the unconsolidated balance sheets provide information only for few years. Therefore, we would lose important information from the transaction data if we exclusively concentrate on unconsolidated balance sheets.

There are pros and cons using different types of balance sheet items. If we are interested in intragroup transactions, then consolidated balance sheets can be problematic because they contain the same information for both transaction partners. In that case, the unconsolidated balance sheet would be more appropriate. However, if business partners know that a certain bank belongs to a larger banking group, then economic difficulties of this particular bank might be less problematic since the parent bank would help in a worst-case scenario. In that case, the economic agent would rely more on the consolidated balance sheet.

The match seems poorer at the current end. That is because BankFocus does not provide the balance sheet items and P&L accounts for all banks in 2021. We do not observe any information for about 40% of the banks in this particular year. Unreported robustness checks show that 2021 does not drive our main results.

Instead of net flows of a given period we have also analysed cumulative net flows which might better fit the stock variables on the right hand side of the equation. However, this procedure involves some econometric issues, because we basically run a dynamic regression (cumulated flowst = cumulated flowst-1+net flowst). In another exercise, we used the first differences of the explanatory variables to calculate flows (difference factorst-1 =factorst-1 – factorst-2). Since the results of both robustness checks are quite comparable to our baseline results, we stick to our baseline specification.

The baseline sample excludes all observations if one of the German or foreign factors exhibits a missing value.

The insignificance of several variables might be due to the chosen lead-lag structure. We could also use the contemporaneous effect instead of the first lag of the explanatory variables. Although some coefficients become more significant, we have to drop more variables from the regressions because the variance matrix is non-symmetric or highly singular. We stick to the chosen lag structure, because otherwise we would create an identification problem with flows on the left hand side influencing some individual factors on the right hand side.

Further (unreported) robustness checks show that the country-year fixed effects do not influence the insignificance of foreign bank factors. The results of Table 6 remain similar if we use year instead of country-year fixed effects.

Bank deposits have a significant positive effect but we do not have any prior expectation on this variable.

The number of observations increases because we do not drop the observations of the missing values of all German and foreign factors.

Another possibility is to use German TARGET2 gross inflows instead of net flows (relative to total assets) as dependent variable and to test whether claims against central banks matter. We conducted this robustness check and found similar results compared to our baseline regressions.

References

Auer RA (2014) What drives TARGET2 balances? Evidence from a panel analysis. Economic Policy 29(77):139–197

Bettendorf T, Jochem A (2023) TARGET balances in the euro area: the case of Germany. Appl Eco 55(29):3317–3328

Cheung Y-W, Steinkamp S, Westermann F (2020) Capital flight to Germany: two alternative measures. J Int Money Finance 102:102095

Deutsche Bundesbank (2017a) The increase in Germany’s TARGET2 claims. Monthly Report March 2017, 30–31

Deutsche Bundesbank (2017b) TARGET2 balances – mirroring developments in financial markets. Monthly Report December 2017, 75–76

European Central Bank (2022) TARGET Annual Report 2021, June

Hristov N, Hülsewig O, Wollmershäuser T (2020) Capital flows in the euro area and TARGET2 balances. J Banking Finance 113:105734

Rossi S (2012) The monetary-structural origin of TARGET2 imbalances across Euroland. In: Gnos C, Rossi S (eds) Modern monetary macroeconomics: a new paradigm for economic policy. Edward Elgar, Cheltenham and Northampton, pp 221–238

Acknowledgment

We thank Martin Diehl, Marc Glowka, Ulrich Grosch, Björn Imbierowicz, Stephan Jank, Malte Knüppel, Alexander Müller, Jan Paulick and seminar participants at the Deutsche Bundesbank for their helpful comments. Discussion Papers represent the authors’ personal opinions and do not necessarily reflect the views of the Deutsche Bundesbank or the Eurosystem.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

See Tables 10, 11, 12, 13, 14, 15

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Drott, C., Goldbach, S. & Jochem, A. Determinants of Net Transactions in TARGET2 of European Banks Based on Micro-data. Open Econ Rev (2024). https://doi.org/10.1007/s11079-024-09748-7

Accepted:

Published:

DOI: https://doi.org/10.1007/s11079-024-09748-7