Abstract

Commodity prices influence price levels of a broad range of goods and, in the case of some developing economies, production and export activity. Therefore, information about future commodity inflation is useful for central banks, forward-looking policy-makers, and economic agents whose decisions depend on their expectations about it. After 2004, we have witnessed the so-called financialization of the commodity markets, which might induce greater communalities among commodity prices. This paper reports evidence on the relevance of the forecasting content of co-movement after 2004. With the use of large and small scale factor models we find that for the short run, in addition to dynamics, sectoral communality has relevant predictive content. For 12 months ahead, dynamics lose relevance while communality remains relevant.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Poncela et al. (2014) found that there has been an increase in co-movement in a large range of non-energy commodity prices since 2004, perhaps enhanced by the financialization in the commodity markets.Footnote 1 Thus, prices that should apparently not be correlated increased their common evolution in time. According to their study, the variance of commodity prices explained by the common behavior of 44 non-energy commodity prices, jumped from 9% between February 1992 and November 2003, to 23% between December 2003 and December 2012. This means that after 2004 the common behavior of non-energy commodity prices accounts for a larger share of those fluctuations. Delle Chiaie et al. (2017), Yin and Han (2015) as well as Ma et al. (2015) also found that the variation explained by the co-movement among commodities (or common factor) has increased for most of the commodities since 2004.

Co-movement existing in a large set of commodity prices might be driven by global demand shocks and, more recently, by speculation, while co-movement existing in commodity prices within smaller categories might be driven either by supply shocks or by the effect of the creation of index funds by category of commodities in the financialization period. According to Diebold et al. (2017), commodity prices are determined by traditional supply and demand considerations. While demand for commodities is driven, in part, by a common global demand, commodity supply is driven by sectoral or idiosyncratic considerations. The collapse in the commodity prices during the Great Global Recession of 2007–2008, and the sharp increase on most of them after 2001, due to the demand growth from China, are examples of how common global demand shocks affect overall commodities. In contrast, weather conditions and decisions of major exporting country governments (e.g., export and/or import taxes) are examples of how supply shocks might affect prices in a specific group of commodities, such as agricultural commodities or metals. As common factors are unobserved we test what type of co-movements are more important in commodity prices by means of a forecasting exercise. It is therefore of interest to explore whether co-movement in prices of raw materials has some predictive power over each commodity price and if the predictive power is higher with global or sectoral common factors.

To analyze the consequences of these co-movements in forecasting, we compare several models against a baseline benchmark alternative. We aim to explore the predictability of commodity spot price changes measured on a monthly basis. For this purpose, we use a Dynamic Factor Model (DFM) to extract latent factors that drive the co-movement on commodity prices. We evaluate two variants: a large-scale DFM that uses the whole commodity price data to estimate their co-movement and a small-scale DFM that takes into account only the communalities into commodities of the same category. Then, we evaluate whether the co-movements across the overall commodity prices as captured by global factors, or the co-movements across smaller and more homogeneous categories as captured by own industrial factors, help in forecasting commodity prices. Our measure of forecasting performance is the out-of-sample root mean square error of prediction (RMSE) for one and twelve-step-ahead forecasts. The closest paper to ours is Delle Chiaie et al. (2017). However, bearing in mind that our purpose is forecasting and that we do not know the number of common factors, we do not impose a priori structure for the common factors. On the contrary, we let the data speak and establish the number of factors according to the eigenstructure of the variance-covariance matrices of commodity inflations.

Although the literature on commodity price forecasts is extensive, it provides only scant empirical evidence of the role of co-movement in commodity prices as a possible source of predictability in commodity price inflation. The recent literature has focused on evaluating whether macroeconomic and financial variables have some predictive power over commodity price spot indices, with mixed results. Chen et al. (2010) found that exchange rate fluctuations in a group of commodity-dependent countries have robust power in forecasting commodity price indices. Groen and Pesenti (2011) used a large set of macroeconomic variables, apart from exchange rates, to evaluate their predictive power over commodity indices. They did not find a robust validation of Chen et al. (2010) previous conclusions. Moreover, although the inclusion of multivariate macroeconomic variables improves the forecasts, it does not produce an overwhelming advantage of spot price predictability when compared with the random walk model. Gargano and Timmermann (2014) found that the predictability power of macroeconomic and financial variables depends on the state of the economy.

Another branch of the literature has focused on whether futures prices are good predictors of future spot prices. Chinn and Coibion (2013) evaluate the forecasts of a range of commodity prices finding that futures prices for precious and base metals display very limited predictive content for future price changes. In contrast, futures prices for energy and agricultural commodities do relatively better in terms of predicting subsequent price changes. In regard to oil prices, Alquist and Kilian (2010) use two models: one that considers the current level of futures prices as predictor and the second which is based on the futures spread, to conclude that oil futures prices fail to improve the accuracy of simple no-change forecasts.

A much smaller body of literature has used factor models in forecasting commodity prices or returns. West and Wong (2014) fit a static factor model to evaluate the extend of co-movement of 22 commodity prices. They found that commodity prices tend to revert towards the factor. They also compare the predictive ability of the factor model to models that use macroeconomic variables. West and Wong (2014) found that the factor model does better at longer (12 month) horizons. On the other hand, Delle Chiaie et al. (2017) also evaluate the co-movement in a large set of commodity prices (they called it the global factor) and the co-movement existing in a specific group of commodities (they called it the block factor). They found that the global factor accounts for a larger fraction of commodity price fluctuations in episodes associated with global economic activity, while the block components explain most of the fluctuations during episodes associated with supply. To verify the robustness, they evaluated their modelling strategy performing an out-of-sample validation, finding that the factor model performs well at short horizons.

We use Kalman filter techniques for both large and small-scale DFMs. Large-scale DFMs are estimated by means of the hybrid procedures of Doz et al. (2011, 2012) that are able to apply the Kalman filter to large-scale systems increasing the efficiency of the estimated common factors by modeling their dynamics. Small-scale DFMs are also estimated by means of the Kalman filter modeling as well as the dynamics of the idiosyncratic components if needed. Then, the main difference between small-scale and large-scale DFMs relies not in the procedure to estimate the common factors (Kalman filter techniques in both cases), but in the number of series, the increased homogeneity of the series within each group and the inclusion of idiosyncratic dynamics in addition to the common ones. We have checked the robustness of our results to using Principal Components for the estimation of the common factors in large-scale DFMs.

Our contributions to the literature are the following. First, we shed some light on which type of co-movement is useful for forecasting purposes: the co-movement of overall commodities, which captures global demand fundamentals and speculation, or the co-movements present within categories, as it captures supply shocks or commodity index funds by category. Second, by considering two different periods, we check whether the increase in co-movement existed in the post-financialization period upsurges the forecasting performance of the dynamic factor models. To understand and forecast changes in commodity prices is important not only for commodity dependent countries, due to the fact that commodity price swings directly affect their overall economic performance, but also for commodity importing countries, because commodity prices impact inflation. Furthermore, the role of co-movement in forecasting commodity price changes might add important information to investment managers seeking to diversify portfolios of financial assets and also to commodity producers considering diversifying their production. Finally, we also check that co-movements are also maintained using data from the post-crisis period only.

Our paper considers the following research questions: First, does co-movement in commodity prices have predictive power over commodity price inflations? Second, is it global or sectoral co-movement in commodity prices what has predictive power? Third, do factor models gain predictability in the post-financialization period? Finally, are co-movements due mainly to the crisis? We aim to answer these questions using dynamic factor models.

The paper is organized as follows. In Section 2 we present the different models we use along the paper. In Section 3, we describe the data and the methodological procedure we propose. In Section 4, we report the estimation and forecasting results. Finally, in Section 5, we conclude.

2 Model Specifications

Let Pi, t be the spot price of the i-th commodity at time t, i = 1,…n and t = 1, …. . , T. Then yi, t= ln(Pi, t)-ln(Pi, t − 1) denotes commodity price inflation. The first model that we consider is a random walk for the log prices or, for their first differences:

which implies that the best forecast of the spot price of commodities is simply the current spot price plus the drift αi if it were different from zero.

Our second model incorporates transitory dynamics adding lagged values of yi, t in the right hand side of Eq. (1):

For each commodity, the order of the autoregressive (AR) model si is selected by the Bayesian Information Criterion (BIC), although we have also checked the robustness of our results to using the Akaike Information Criterion (AIC) or to fixing si = 1 for all commodities i = 1, …, N. The AR model in Eq. (2) may perform better that the model in (1) for very short term forecasting (one period ahead), while the random walk for the log prices may perform better for medium term forecasts (12 months ahead) if the transitory dynamics in (2) have already died out as it happens in our case. We consider as our benchmark the model of order selected by the BIC (AR-BIC).

The subsequent models include a latent variable, or factor, that represents the common pattern of commodity prices. The general DFM specification assumes that the i-th commodity price inflation, labelled as yit, is driven by an rx1 latent vector, ft, which is common to all series plus an idiosyncratic component, εi,t. For instance, specifically for each i :

where μi is the unconditional mean of the i-th commodity inflation and λi is the rx1 vector of factor loadings for the i-th commodity. The first DFM specification is a large-scale factor model that accounts for the common variability of all available commodity prices. We follow the two-step approach of Doz et al. (2011) in which the parameters of the model for the dynamics of the common factors are estimated through OLS of principal components over their lags. The factor loading Nxr matrix Λ = (λ1, …, λN)′ is estimated by the eigenvectors associated to the r largest eigenvalues of the variance-covariance matrix of the observed series subjected to identification restrictionsFootnote 2. The hybrid methods of Doz et al. (2011, 2012) do not model the specific component. In the second step, the factor is estimated via Kalman filter and smoother. To forecast price inflation, we use the dynamics of the common factor given by:

where ηt ∼ N(0, Σ) is assumed to be white noise with diagonal variance-covariance matrix and independent of εt. Therefore, we build our large scale forecast at t + h with information until time t as:

Besides estimating a large-scale DFM, which takes into account common factors to all the commodity price series (Eqs. 3 to 5), in this paper we also estimate a set of small-scale DFMs by introducing dynamic factors which are common only to the series within each set. More precisely, let us consider L commodity categories, and for each category (category l = 1,2,…,L) kl commodity price series. Then, the baseline model for each commodity price in the lth category can be decomposed into the following components ∀l:

where μi is the average inflation of commodity i-th. Within each category l, cl, t is the factor or co-movement variable common to all series in the category, \( {a}_i^l \) represents the factor loading, and \( {\varepsilon}_{i,}^l \) named idiosyncratic component, collects the dynamics specific to each commodity price inflation. Both the common factor and the idiosyncratic component may follow AR processes of order ql and pi, respectively:

where \( {\sigma}_i^l \) is the standard deviation of the i-th idiosyncratic component, and \( {\eta}_{i,t}^l\sim N\left(0,1\right), \)i = 1, …kl, l = 1, …, L, are the innovations to the law motions for Eqs. (7) and (8)Footnote 3. Within each of the small factor models estimated for each category, we assume that the idiosyncratic component \( {\varepsilon}_t^l={\left({\varepsilon}_{1,t}^l,\dots, {\varepsilon}_{k_l,t}^l\right)}^{\prime } \) is orthogonal at all leads and lags (exact factor model). We also assume that cl, t and \( {\varepsilon}_{i,t,}^l \) are uncorrelated processes.

We also evaluate whether the inclusion of the forecast of the idiosyncratic component of the DFM,\( {\varepsilon}_{i,t}^l, \) improves the forecasting performance in the small-scale DFMs, or it is only the forecast of the common part what is valuable for forecasting. We aim to check the usefulness of the idiosyncratic component in factor forecasting. If the idiosyncratic component is useful for forecasting, it means that own commodity market dynamics are also useful in forming the expectations. On the contrary, if only the common factors are useful in forecasting, it would mean that commodity communalities (global or sectorial) are the key nowadays for commodity price forecasting.

We estimate the small-scale DFMs in the state-space using the Kalman filter. The forecast of the i-th commodity inflation h periods ahead will be given by

where the expected values Et[cl, t + h] and \( {E}_t\left[{\varepsilon}_{i,t+h}^l\right] \) are computed taken expectations in (7) and (8), respectively.

To sum up, the different models, and their variations, that we estimate and compare in terms of forecasting in this study can be summarized as:

-

1.

Random Walk

-

2.

AR-BIC selected (benchmark model)

-

3.

Large-scale DFM

-

4.

Small-Scale DFM

-

4.1.

Small-Scale DFM with idiosyncratic component.

-

4.2.

Small-Scale DFM without idiosyncratic component.

-

4.1.

3 Data Description and Empirical Strategy

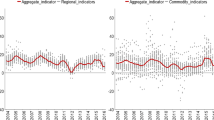

We use monthly Indices of Primary Commodity Prices from the International Monetary Fund database (IMF IFS). The full list of the 67 commodities and their categories is shown in Appendix 1, Table 4. Our sample goes from January 1992 to December 2018. We have excluded from the analysis 10 commodity prices due to their short sample or lack of availability on a monthly basis for some periods. The 57 remaining commodity prices considered amount for almost 85% of total trade between 2014 and 2016. Figure 1 shows the evolution of commodity prices per group from January 1992 to December 2018.

Commodity prices per category. Source: International Monetary Fund, IMF. Data has been normalized

Under the financialization hypothesis, there is a break in 2004 and, as it can be seen, since then prices seem to be characterized by a great upsurge until mid-2008, and a drastic decline during the global financial crisis. After mid-2009, prices began to recover the upswing in several categories, being remarkable in Metals, Energy, Cereals and Fertilizers. Notably, if we compare both the pre-2004 and post-2004 samples, there is an increase in the scale of the boom and bust cycles for industrial inputs such as Energy, Metals, and Fertilizers.

For the estimation and forecasting testing procedure, we proceed as follows:

-

1.

We divide the sample in two periods (pre and post financialization since 2004)

-

2.

Following Stock and Watson (2011), we transform the data to achieve stationarity. Therefore, we take logs and first differences of all the price commodities.

-

3.

We determine the number of factors of the large-scale DFM using the test proposed by Onatski (2010).

-

4.

We estimate all the models described in Section 2: Random Walk; Univariate autoregressive (AR-BIC benchmark model); Large-scale DFM for the 57 commodities and a set of Small-Scale DFMs per group (Gas, Oil, Agricultural raw materials, Base metals, Precious metals, Meat, Cereals, Vegetable oil, Sugar, other Foods, Beverages and Fertilizers).

-

5.

We generate one and twelve-step-ahead forecasts for each commodity. We end the estimation sample in 2015:12, we re-estimate the models adding one data point at the time. In other words, we use an expanding window. The forecast evaluation period is 2016:01–2018:12.

-

6.

We compute the root mean square error of prediction (RMSE) for each model and each forecast horizon to assess its forecasting performance. We calculate the RMSE as \( {RMSE}_i=\sqrt{\frac{1}{K}\sum \limits_{K=1}^K{e}_{i,t+h\mid t}^2} \), where K is the number of available forecasts and ei,t+h∣t is the forecast error for commodity i at the horizon t + h, with information until time t, that is ei,t + h∣t = yi,t+h − yi,t+h∣t, where yi,t+h∣t is the h steps ahead forecast for commodity i provided by the different models.

-

7.

We compare the RMSE of every model, and each forecasting horizon, with that of the benchmark model by calculating the ratio between them \( \left(\frac{RMSE_{model}}{RMSE_{benchmark}}\right) \).

We expect that the increase in the co-movement in commodity prices found in Poncela et al. (2014) improves the forecasting of commodity inflation in more homogeneous categories and where financialization and speculation has had a greater impact in the markets. In order to check the hypothesis of financialization after 2004, we repeat the previous forecasting exercise a second time but modifying the estimation and forecasting samples. This time we focus on the pre-2004 sample. In this second forecasting exercise, we end the first estimation sample in 2000:12, generate 1 and 12 steps ahead forecast and re-estimate the models adding one data point at the time generating afterwards new 1 and 12 steps ahead forecasts. We perform the forecast evaluation for the period 2001:1–2003:12. We will later compare the RMSE of the different models before and after 2004 to check the financialization hypothesis after 2004.

4 Empirical Results

In this section we evaluate the co-movement content for predicting inflation of commodities. In particular, we examine whether joint movements of commodity prices can be used as predictors of the inflation of each commodity.

To find the number of common factors among all commodities, we run Onatski’s (2010) test for all the estimation samples that we use in our first recursive forecasting exercise. Since we find 1 common factor in 30 out of 36 samples, we conclude that there is only one common factor among all commodities. To illustrate the source of co-movement, we examine the factor loadings for several samples, finding that always the factor loadings are higher for some metals (Copper, Aluminium and Platinum), fuels (Dubai, Brent and WTI oils) and some vegetable oils. By far, petroleum is responsible for the largest share on the world trade of commodities. Copper and Aluminium are also the most traded metals. We call this common factor co-movement and basically it follows the up and downs in crude oil inflation. We also fit a one common factor model within each group.

4.1 Forecasting Performance of the Factor Models in the Post-Financialization Period

Table 1 summarizes the forecasting results for the main groups of commodities in the post-financialization period. The second column shows the weight (corresponding to their share in the total world trade of commodities according to the IMF between 2014 and 2016). Columns 3 to 7 show the forecasting results for forecasting horizon h = 1, and columns 8 to 12 for forecasting horizon h = 12. Columns 3 and 8 show the average RMSE for all the commodities in the group (subgroup) with the original forecasting benchmark (univariate AR-BIC model) for forecasting horizons h = 1 and h = 12, respectively. The remaining columns show the average of the ratios of the different alternative models against the benchmark forecasts. Hence, a ratio less than one means that the model improves the benchmark forecast, and the difference between the average and 1 could be interpreted as the average improvement against the benchmark forecasts. Column 4 (named as Random walk) shows the results for the random walk model fitted to the levels of log prices; column 5 (named as Large) for the large DFM and columns 6 (Small+id) and 7 (Small) shows the results for the sectoral DFMs with and without idiosyncratic components. Columns 8 to 13 repeat the same structure than columns 3 to 7 but for forecasting horizon h = 12. Appendix 2, Table 5 shows the results for all the commodities.

The results for forecast horizon h = 1 indicate that the small factor model with idiosyncratic component usually outperforms the benchmark model in predicting commodity price inflation. The average ratio for all the commodities for h = 1 with the small factor model with idiosyncratic component is below 1. Although average improvements might not seem too high at first sight, notice that these improvements affect almost all commodities. The sectoral factor model with idiosyncratic dynamics is the best average short term forecasting option for all groups (Agricultural raw materials, Metals, Meat, Food, Beverages and Fertilizers) and for most of the subgroups. Appendix 2, Table 5 contains the detailed individual results for every commodity.

The good results of small scale factor models with idiosyncratic dynamics indicate that both, own commodity market dynamics and sectoral communality are relevant to forecast short term inflation in commodities. The fact that the results are better than the individual univariate models (benchmark) indicates that dynamics alone do not provide the best results and, therefore, communality has relevant predictive content. These results are more relevant if we take into account Stock and Watson (2007) where it is recognized that inflation has been harder to forecast in the sense that for an inflation forecaster, it is very difficult to provide value added beyond a univariate model.

Table 2 shows the highest reductions for 40 of the commodities for h = 1. The second column identifies the commodity, the third the weight in the world trade of commodities, the fourth the ratio of the corresponding RMSE of that commodity with the best factor model to that of the benchmark forecasts and, finally, the reduction obtained in percentage.

Improvements can be substantial in the inflation of some commodities being above 10% in the fertilizer UREA (31.3%), the beverage TEA (28%), the metal TIN (23%), the meat BEEF (17%), or the fuel OILDUB (10%).

Coming back to Table 1, focusing now at the annual horizon (h = 12, columns 8 to 12 of the table), we see that average results for the main groups show that dynamics have died out and, therefore, the benchmark does not have any comparative advantage against any other alternative. The pure random walk for the levels of the log prices gives average better results. The small scale factor model, now with or without taking into account the dynamics of the idiosyncratic component also gives better results, indicating again that for 12 periods ahead individual dynamics lose relevance. On the contrary, global co-movements estimated by the large factor model show some predictive content at one year ahead forecast horizon as opposite to the very short-term forecast where dynamics were more relevant.

To place our results within the literature notice that Atkeson and Ohanian (2001) found that, since 1984 in the United States, backward-looking Phillips curve forecasts have been inferior to a naïve forecast of 12-month inflation by its average rate over the previous 12 months.

Finally, our estimation sample includes the whole financial crisis period where increased correlation in many markets occurred. This could bring some concerns about the validity of the results beyond the financial crisisFootnote 4. To check the robustness of our forecasting results, we fitted our models using only post-crisis data (from January 2009 until December 2015) and generate 1 and 12 steps ahead forecasts. As previously we added one data point at the time, re-estimated the models and generated new 1 and 12 steps ahead forecasts. We proceed in a similar way until the end of the forecasting sample, December 2018. We found that our results were robust to the estimation sample being the sectoral dynamic factor models with idiosyncratic dynamics the best forecasting option. Full results are given in Appendixes 3, Table 6 (average results by category) and 4, Table 7 (full results by commodity).

4.2 Forecasting Performance of the Factor Models in the Pre-Financialization Period

Table 3 summarizes the forecasting results for the main groups of commodities in the pre-financialization period. The format of the table is similar of that of Table 1. The results for all the commodities are presented in Appendix 1, Table 8.

Table 3 shows that for the very short-term, 1 month ahead forecasts, the benchmark univariate AR-BIC model is the best average option in all groups but energy. See that for all groups but energy, RMSE ratios are above 1. This is in line with the hypothesis of a greater relevance of the co-movement in the post -financialization period.

Our results imply that co-movement existing both within commodity categories, which captures either the effect of supply shocks, or the creation of commodity index funds by category during the financialization period, and global market forces, play a major role in forecasting commodity price changes since it contains useful information in forming expectations about future commodity price changes. These results suggest that the increase in the overall co-movement of commodity prices since 2004 has caused the dynamic factor models to improve their predictive content.

The results for h = 12 are less relevant. However, this does not indicate that co-movement was lower in that period since the random walk is the best forecasting option almost always pre-2004 indicating that dynamics have died out.

5 Conclusions

This paper provides empirical evidence on four research questions. We have first addressed whether co-movement in commodity prices have predictive power over commodity price inflations. To this respect we have estimated several DFMs and tested whether they were capable of performing better than univariate alternative forecasts that consider only dynamics. Using a sample that considers monthly data for the post-financialization period we have performed an out of sample pseudo real time forecasting exercise for one and twelve months ahead of commodity inflation for the period 2016:01 to 2018:12. With this exercise we also address if it is global or sectoral co-movement what has predictive power. We have improved the average forecasting results in all main categories with the use of small sector factor models, as grouped by the IMF against univariate alternatives in one month ahead forecasts. The good forecasting results of small scale factor models with idiosyncratic dynamics for one month ahead forecasts suggest that both, dynamics and sectoral communality are relevant to forecast short term inflation in commodities. Given that the results provided by the factor models fitted to each category of commodities are better than the individual univariate ones, we conclude that both dynamics and co-movement are needed to render better forecast accuracy. We have also addressed the question of whether the highest correlations were mainly due to the inclusion of the crisis period by using only data after 2009 to fit and estimate the forecasting models. Results show the robustness to the inclusion or not of the crisis period data.

The last question was related to the financialization hypothesis, under which factor models gained predictability after 2004 in the post-financialization period. To address this issue we repeated the forecasting exercise using data of the pre-financialization period to test the out of sample forecast accuracy for 2001:01 to 2003:12. When comparing with the pre-2004 analysis, we found that all types of DFMs have gained predictive power since 2004. Our results suggest that both supply shocks and the creation of commodity index funds by category during the financialization period, which impact co-movement within categories, and global demand shocks, affecting communalities of a large set of commodities, play a role in forecasting commodity inflation.

Notes

Financialization in the commodity markets is the name given to the substantial increase in commodity index fund investments starting in 2004. According to authors such as Büyüksahin and Robe (2012) and Henderson et al. (2012) financialization not only increases co-movements among different types of commodities, but generates cross-market linkages, especially with the stock market. Other contributors to this literature include Tang and Xiong (2012) and Irwin et al. (2009).

It is well known the identification problem in factor models. We will impose the same identification restrictions that Doz et al. (2011).

Notice that the implied identification restriction in each small scale factor models is var(\( {\eta}_{0,t}^l\Big)=1,l=1,\dots, L \).

We thank an anonymous referee for bringing up this point.

References

Alquist R, Kilian L (2010) What do we learn from the price of crude oil futures? J Appl Econ 25:539–573

Atkeson A, Ohanian LE (2001) Are Phillips curves useful for forecasting inflation? Quarterly Review 25(1):2–11

Büyüksahin B, Robe MA (2012) Speculators, commodities and cross-market linkages. J Int Money Financ 42:38–70

Chen Y, Rogoff K, Rossi B (2010) Can exchange rates forecast commodity prices? Q J Econ 125:1145–1194

Chinn MD, Coibion O (2013) The predictive content of commodity futures. J Futur Mark 34(7):607–636

Delle Chiaie S, Ferrara L, Giannone D (2017) Common factors of commodity prices, ECB working paper no. 2112

Diebold, Francis X., Laura Liu, and Kamil Yilmaz (2017) Commodity connectedness (no. w23685). National Bureau of Economic Research

Doz C, Giannone D, Reichlin L (2011) A two-step estimator for large approximate dynamic factor models based on Kalman filtering. J Econ 164(1):188–205

Doz C, Giannone D, Reichlin L (2012) A quasi–maximum likelihood approach for large, approximate dynamic factor models. Rev Econ Stat 94(4):1014–1024

Gargano A, Timmermann A (2014) Forecasting commodity price indexes using macroeconomic and financial predictors. Int J Forecast 30(3):825–843

Groen JJ, Pesenti PA (2011) Commodity prices, commodity currencies, and global economic developments. In: Commodity prices and markets, east Asia seminar on economics, vol. 20. University of Chicago Press, Chicago, pp 15–42

Henderson, Brian, Neil D. Pearson, and Li Wang (2012) New evidence on the Financialization of commodity markets, working paper, University of Illinois, Urbana-Champaign

Irwin SH, Sanders DR, Merrin RP (2009) Devil or angel? The role of speculation in the recent commodity price boom (and bust). J Agric Appl Econ 41(2):377–391

Ma, Jun, Andrew Vivian, and Wohar, M. E. (2015) What drives commodity returns? Market, sector or idiosyncratic factors?. Working Paper

Onatski A (2010) Determining the number of factors from empirical distribution of eigenvalues. Rev Econ Stat 92(4):1004–1016

Poncela P, Senra E, Sierra L (2014) The dynamics of co-movement and the role of uncertainty as a driver of non-energy commodity prices. Appl Econ 46(30):3724–3725

Stock J, Watson M (2007) Why has U.S. inflation become harder to forecast? J Money Credit Bank 39:3–33

Stock J, Watson M (2011) Dynamic factor models. In: Clements MJ, Hendry DF (eds) Oxford handbook on economic forecasting. Oxford University Press, Oxford

Tang K, Xiong W (2012) Index investment and the financialization of commodities. Financ Anal J 68:54–74

West KD, Wong K-F (2014) A factor model for co-movements of commodity prices. J Int Money Financ 42:289–309

Yin L, Han L (2015) Co-movements in commodity prices: global, sectoral and commodity-specific factors. Econ Lett 126:96–100

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The contents of this publication do not necessarily reflect the position or opinion of the European Commission. The work was finished while the first author returned to the Universidad Autónoma de Madrid. The authors acknowledge financial support from the Pontificia Universidad Javeriana Cali, the Spanish Ministry of Economy and Competitiveness, project numbers ECO2015-70331-C2-1-R, ECO2015-66593-P and ECO2016-76818-C3-3-P.

Appendices

Appendix 1

Appendix 2

Appendix 3

Appendix 4

Appendix 5

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Poncela, P., Senra, E. & Sierra, L.P. Global vs Sectoral Factors and the Impact of the Financialization in Commodity Price Changes. Open Econ Rev 31, 859–879 (2020). https://doi.org/10.1007/s11079-019-09564-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11079-019-09564-4