Abstract

In this paper, we deal with the global approximation of solutions of stochastic differential equations (SDEs) driven by countably dimensional Wiener process. Under certain regularity conditions imposed on the coefficients, we show lower bounds for exact asymptotic error behaviour. For that reason, we analyse separately two classes of admissible algorithms: based on equidistant, and possibly not equidistant meshes. Our results indicate that in both cases, decrease of any method error requires significant increase of the cost term, which is illustrated by the product of cost and error diverging to infinity. This is, however, not visible in the finite-dimensional case. In addition, we propose an implementable, path-independent Euler algorithm with adaptive step-size control, which is asymptotically optimal among algorithms using specified truncation levels of the underlying Wiener process. Our theoretical findings are supported by numerical simulation in Python language.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

We investigate the global approximation of solutions of the following stochastic differential equations

where \(T >0\), \(W(t) = [W_1(t), W_2(t), \ldots ]^T\) is a sequence of independent scalar Wiener processes on the probability space with sufficiently rich filtration \((\Omega , \mathcal {F}, \mathbb {P}, \big (\mathcal {F}_t)_{t\in [0,T]}\big ),\) and \(x_0 \in \mathbb {R}.\) For suitable, regular coefficients \(a, \sigma ,\) the uniqueness of the solution \(X=X(t),\) and its finite second-order moments can be assured; see [1, 4, 6, 23] where more general models were considered.

Recently, the global approximation of solutions of SDEs driven by finite-dimensional Wiener process has been studied extensively in the literature. In particular, the algorithms with step-size were introduced in [8, 9, 12, 19, 20]. Generally, the time-step adaptation linked to the equation coefficients instead of leveraging equidistant mesh can significantly decrease the asymptotic constant for the method error in the finite-dimensional models. On the other hand, SDEs driven by countably dimensional Wiener noise can be found in [2, 5, 14], while their applications, e.g., in [3, 18]. Nonetheless, there are still a few papers referring to the exact error behaviour and optimality issues for such SDEs in the global setting. For instance, in [24] authors developed an Euler algorithm and estimated its global error for X being countably dimensional. However, the assumptions were relatively strong, and the proposed algorithm was non-implementable due to infinite dimension of the solution.

In this paper, we extend some asymptotic results for the global approximation from [8, 12] to SDEs with countably dimensional noise structure. To that end, we utilise solution moment bounds and approximation strategy presented in [23], where a pointwise setting was investigated. In our setting, error of an algorithm \({\mathcal A}\) returning a process \(Y = (Y(t))_{t\in [0,T]}\) is measured in the norm \(\Vert \cdot \Vert _2\) defined as follows:

Under suitable conditions imposed on the model coefficients, we analyse asymptotic exact error behaviour in two classes \(\chi _{eq}, \chi _{noneq}\) of admissible algorithms leveraging only finite-dimensional evaluations of the process W; , we refer to [7, 8, 11, 12, 17, 22, 26] where similar approach for generic error analysis was developed. In our setting, permitted truncation levels are determined by non-decreasing sequences leveraging information about how fast \(\sigma \) entries vanish. In Theorem 2, we show that for any fixed, admissible truncation level sequence \(\bar{M}=(M_n)_{n=1}^{\infty }\), an exact asymptotic behaviour of the cost-error relation satisfies

irrespective of the choice of admissible method \(({\overline{X}_{M_n,\bar{k}_n}})_{n\in \mathbb {N}}\in \chi _{noneq}^{\bar{M}}\) based on (possibly) non-equidistant mesh with a suitable number of nodes \(\bar{k_n}+1,\) and such that \({\overline{X}_{M_n,\bar{k}_n}}\) utilises discrete information from \(M_n, n\in \mathbb {N},\) first coordinates of W. When we limit ourselves to methods \(\chi _{eq}^{\bar{M}}\) based on equidistant partitions of the interval [0, T], we get

We hereinafter use the notation

By the Hölder inequality, we have \(0 \le \mathcal {C}_{noneq}\le \mathcal {C}_{eq}\). We also stress that the lower bounds in (2) and (3) diverge as n tends to infinity, which illustrates significant increase of the informational cost needed to decrease the method error. Next, for fixed \(\bar{M},\) we construct truncated Euler algorithm with adaptive path-independent step-size control \(X^{step}_{M_n,k_n^*}\) which is optimal in class \(\chi _{noneq}^{\bar{M}},\) since it attains asymptotic lower bound in (2). We also provide lower bounds which hold irrespective of the truncation level sequence, see Theorem 3. While those cannot be asymptotically achieved by any admissible algorithm, we show that the errors for the methods proposed in this paper can be arbitrary close in some sense to the obtained bound. We note that both error bounds and optimality are investigated in the spirit of information-based complexity (IBC) framework.

According to our best knowledge, this is the first paper to establish lower bounds for exact asymptotic error in the global approximation setting for SDEs with countably dimensional Wiener process. Moreover, the new constructed algorithms are implementable, and their performance is verified by using the multiprocessing library in Python.

The paper is organised as follows. In Sect. 2, we provide basic notation, model assumptions, and properties of the underlying solution X. Then, in Sect. 3, we investigate lower bounds for exact asymptotic error behaviour. In Sect. 4.1 and in Sect. 4.2, we introduce and show optimality of the truncated dimension Euler schemes in the classes \(\chi _{eq}^{\bar{M}}\) and \(\chi _{noneq}^{\bar{M}},\) respectively. Next, in Sect. 4.3, we extend optimality investigation to the classes \(\chi _{eq}\) and \(\chi _{noneq}.\) Finally, Sect. 5 deals with numerical experiments in Python and alternative solver implementation utilizing Numba compiler.

2 Preliminaries

Let \((\Omega ,\Sigma ,\mathbb {P})\) be a complete probability space and \(\mathcal {N}_0=\{A\in \Sigma \ | \ \mathbb {P}(A)=0\}\). Let also \((\Sigma _t)_{t\ge 0}\) be a filtration on \((\Omega ,\Sigma ,\mathbb {P})\) that satisfies the usual conditions, i.e., \(\mathcal {N}_0\subset \Sigma _0\) and is right-continuous. For a random variable X by \(\Vert X\Vert _{L^2(\Omega )}\), we understand \((\mathbb {E}|X|^2)^{1/2}.\)

Let \(W=[W_1,W_2,\ldots ]^T\) be a countably dimensional \((\Sigma _t)_{t\ge 0}\)-Wiener process defined on \((\Omega ,\Sigma ,\mathbb {P})\). We note that similarly to the finite-dimensional case, stochastic integrals with respect to W enjoy properties such as the Burkholder inequality, Itô isometry, Itô lemma, see e.g. [2, 4, 23].

For \(x\in \ell ^2(\mathbb {R})\), we use the following notation \(x = (x_1, x_2, \ldots ).\) We introduce projection operators \(P_k: \ell ^2 (\mathbb {R}) \mapsto \ell ^2 (\mathbb {R}),\) \(k\in \mathbb {N}\cup \{\infty \}\) with

We also set \(P_{\infty }=Id\), hence \(P_{\infty }v=v\) for all \(v\in \ell ^2(\mathbb {R})\). For brevity, in this paper, we write \(\Vert \cdot \Vert _{\ell ^2}\) instead of \(\Vert \cdot \Vert _{\ell ^2(\mathbb {R})}.\)

For vectors \(v = [v_1, \ldots , v_m] \in {\mathbb R}^m,\) \(u = [u_1, \ldots , u_l] \in {\mathbb R}^l,\) we denote by \(v\oplus u\) the vector \([v_1, \ldots , v_m, u_1,\ldots , u_l]\in \mathbb {R}^{m+l}\). By \(\bigoplus _{k=1}^n w_k\), we understand the vector \(w_1 \oplus w_2 \oplus \ldots \oplus w_n.\)

In this paper, we use the following asymptotic notation. For two real-valued sequences \((a_n)_{n=1}^\infty ,\, (b_n)_{n=1}^\infty ,\) we write \(a_n \lessapprox b_n, n\rightarrow +\infty ,\) if and only if \(\limsup _{n\rightarrow +\infty } a_n/b_n \le 1.\) We also say that \(a_n \approx b_n, n \rightarrow +\infty ,\) if and only if \(\lim _{n\rightarrow +\infty }a_n / b_n = 1.\) Furthermore, the asymptotic symbols \(\Omega , \Theta , \mathcal {O},o\) appearing in this paper are aligned with classical Landau notation for sequences. For a sequence \((c(n))_{n=1}^\infty \) of non-negative numbers converging to zero and \(\epsilon >0,\) we define the inverse \(c^{-1}(\epsilon ) = \sup \{n \in \mathbb {N}\, | \, c(n)>\epsilon \}.\)

We assume that drift coefficient \(a: [0,T]\times \mathbb {R} \mapsto \mathbb {R} \) belongs to \(\mathcal {C}^{1,2}([0,T]\times \mathbb {R})\) and satisfies the following conditions:

-

(A1)

\(|a(t,x) - a(s,x)| \le C_1(1+ |x|)|t-s|\) for all \(t,s\in [0,T], \ x\in \mathbb {R}\),

-

(A2)

\(|a(t,0)|\le C_1\) for all \(t\in [0,T]\),

-

(A3)

\(|a(t,x) - a(t,y)| \le C_1|x-y|\) for all \(x,y \in \mathbb {R}\), \(t \in [0,T]\),

-

(A4)

\(|\frac{\partial a}{\partial x}(t,x) - \frac{\partial a}{\partial x}(t,y)| \le C_1|x-y|\) for all pairs \((t,x), (t,y) \in [0,T]\times \mathbb {R}\)

for some \(C_1 > 0.\)

Let \(\delta = (\delta (k))_{k = 1}^{\infty }\subset \mathbb {R}\) be a positive, strictly decreasing sequence vanishing at infinity. For fixed \(\delta ,\) by \(\mathcal {G}_\delta \), we denote a set of all non-decreasing sequences \(G=(G(n))_{n=1}^{\infty } \subset \mathbb {N}\) such that \(G(n)\rightarrow +\infty \) and

We assume that diffusion coefficient \(\sigma = (\sigma _1, \sigma _2, \ldots ):[0,T] \mapsto \ell ^2(\mathbb {R})\) satisfies the following conditions:

-

(S1)

\(\Vert \sigma (0)\Vert _{\ell ^2} \le C_2,\)

-

(S2)

\(\Vert \sigma (t) - \sigma (s)\Vert _{\ell ^2} \le C_2|t-s|\) for all \(t,s\in [0,T]\),

-

(S3)

\(\Vert \sigma (t) - P_k \sigma (t)\Vert _{\ell ^2} \le C_2\delta (k)\) for all \(k \in \mathbb {N}, \ t \in [0,T],\)

for \(C_2 > 0\) and some fixed sequence \(\delta \) as above.

Our idea is to first provide the approximation of truncated solution \(X^M = X^M(a,\sigma ,W)\) which depends on the first \(M\in \mathbb {N}\) coordinates of the underlying Wiener process W. In this paper, any method leveraging finite number of Wiener process coordinates will be referred to as ‘truncated dimension method’. Then, we estimate globally the inevitable truncation error resulting from substituting the process X for \(X^M.\) For convenience, we will use the notation \(X^{\infty }:= X.\)

To this end, we consider the family of processes \(X^M, \ M \in \mathbb {N} \cup \{\infty \},\) satisfying

In particular, for \(M=+\infty \), we obtain the main problem (1). For further analysis, we need some properties of the process \(X^M.\) Those are presented below, in a corollary from Lemma 1 in [23].

Lemma 1

For every \(M \in \mathbb {N} \cup \{\infty \}\) the Eq. (5) admits a unique strong solution \(X^M = (X^M(t))_{t\in [0,T]}.\) Moreover, there exists \(K \in (0,+\infty ),\) depending only on the constants \(C_1, C_2,\) such that for every \(M\in \mathbb {N}\ \cup \ \{\infty \}\), we have that

and for all \(s,t \in [0,T]\) the following holds

We also state truncation error bound for our model. This result is a corollary from Proposition 1 in [23].

Proposition 1

There exists \(K_1\in (0,+\infty )\) such that for any \(M \in \mathbb {N}\) it holds

We define truncated dimension time-continuous Euler algorithm \({\widetilde{X}_{M,n}^E}= ({\widetilde{X}_{M,n}^E}\) \((t))_{t\in [0,T]}\) that approximates the process \((X(t))_{t \in [0,T]}\). Take \(M,n \in \mathbb {N}\), and let

be a sequence of partitions of the interval [0, T], with \(k_n \in \mathbb {N}.\)

We set

We stress that \({\widetilde{X}_{M,n}^E}\) is not implementable since it requires complete knowledge of the trajectories of the underlying Wiener process.

Now, we state the upper error bound of the truncated dimension time-continuous Euler algorithm in finite-dimensional setting.

Proposition 2

Under the assumptions (A1)-(A4) and (S1)-(S3), there exists a positive constant \(C_0\), depending only on \(C_1, C_2\), such that for all \(M,n\in \mathbb {N}\) the time-continuous truncated Euler process (9) based on partition (8) satisfies

where \(\Delta t_{j,n} = t_{j+1,n} - t_{j,n},\) \(j=0,1,\ldots , k_n-1.\)

The proof of Proposition 2 is postponed to the Appendix.

We can state the most important result of this section.

Theorem 1

Let the coefficients \(a,\sigma \) satisfy (A1)-(A4) and (S1)-(S3) with sequence \(\delta \), respectively. Then, there exists a positive constant K, depending on \(C_1, C_2, \delta ,\) such that for every \(M,n\in \mathbb {N}\) and the discretisation (8), it holds

Proof

By Proposition 1, Proposition 2, and the triangle equality, we obtain the desired result. \(\square \)

At the end of this section, we present several remarks on the model, imposed assumptions, and suitability of the chosen stochastic scheme.

Remark 1

Generally, the concept of SDEs with integrals with respect to countably dimensional Wiener process is used to describe the evolution driven by countably many risk factors. This modelling choice can be leveraged for a wide range of problems in, e.g., genetics, mathematical finance or physics [3, 18]. From a pragmatic point of view, infinite-dimensional setting can be leveraged when the number of random risks is finite but still too large to be entirely captured by the electronic machines. On the other hand, the integrals appearing in this paper can be viewed as stochastic integrals with respect to cylindrical Brownian motion in Hilbert space of sequences \(\ell ^2(\mathbb {R})\) and hence, our model forms a bridge between ordinary SDEs and stochastic partial differential equations (SPDEs), see [5].

Remark 2

First, the assumptions (A1) - (A4) imply the existence of a constant \(K_0 > 0\) such that

Second, in the presented setting, a crucial role is played by appropriate choice of corresponding truncation levels for admissible methods. Indeed, those are defined in terms of the elements of \(\mathcal {G}_{\delta }\) as per (4). We note that for every \(\delta \) the corresponding set \(\mathcal {G}_\delta \) is nonempty. Furthermore, the slower rate of diffusion decay to zero, the greater values of G(n) need to be taken. We note that \(\delta \) does not need to be optimal in a sense that for fixed \(\sigma \) there might exist \(\delta '\) also satisfying (S3) and \(\delta ' < \delta .\) Nevertheless, sharper bound in (S3) yields greater palette of the corresponding sequences G in (4), as \(\delta ' \le \delta \) implies \(\mathcal {G}_\delta \subset \mathcal {G}_{\delta '}.\)

Remark 3

It is worth mentioning that suitable modifications of the classic Euler scheme for finite-dimensional setting have been investigated in, e.g., [8, 15, 23]. For the problem (1), the method \({\widetilde{X}_{M,n}^E}\) coincides with truncated dimension time-continuous Euler algorithm proposed in [23]. However, the regularity of function a in our case enhances the rate of convergence from 1/2 to 1, see Theorem 1. Indeed, the proposed method also coincides with the Milstein scheme; see, e.g., [12, 13, 16, 19,20,21,22] where the approximation by modified Milstein schemes for finite-dimensional models was considered.

In the following sections, we investigate lower bounds for exact asymptotic error behaviour and construct optimal methods in suitable subclasses of admissible algorithms. The optimality is defined in the spirit of Information-Based Complexity (IBC) framework, see also [26] for more details.

3 Lower bounds for exact asymptotic error behaviour

In this section, we derive minimal global approximation error for our initial problem (1). The main results are presented in Theorem 2.

Let us fix \((a,\sigma ),\) and a sequence \(\delta \) satisfying (S3). An arbitrary method under consideration is a sequence of the form \(\overline{X} = ({\overline{X}_{M_n,\bar{k}_n}})_{n=1}^{\infty }\) and can be equivalently viewed as a quadruple \(\overline{X} = (\bar{\Delta }, \bar{\mathcal {N}}, \bar{M}, \bar{\phi }),\) where

-

\(\bar{\Delta }=(\bar{\Delta }_{n})_{n=1}^{\infty }\) is a sequence of (possibly) non-expanding partitions of the interval [0, T], i.e.,

$$\begin{aligned} \bar{\Delta }_{n}: \quad 0=\bar{t}_{0,n}< \bar{t}_{1,n}< \ldots< \bar{t}_{\bar{k}_n-1,n} < \bar{t}_{\bar{k}_n,n} = T, \end{aligned}$$(12)where for some \(\overline{C}_1, \overline{C}_2>0\) it holds

$$\begin{aligned} \overline{C}_1\, n \ge \bar{k}_n \ge \overline{C}_2 \, n^{1/2}, \quad n\ge n_0(\overline{X}) \in \mathbb {N}. \end{aligned}$$(13) -

\(\bar{\mathcal {N}} = (\mathcal {N}_{M_n, \bar{k}_n})_{n=1}^{\infty }\) is a sequence of information vectors. For fixed \(n \in \mathbb {N},\) the vector \(\mathcal {N}_{M_n, \bar{k}_n}\) consists of the points in which the method \({\overline{X}_{M_n,\bar{k}_n}}\) evaluates the values of underlying (scalar) Wiener processes \(W_k,\) \(k=1,\ldots , M_n:\)

$$\begin{aligned} \mathcal {N}_{M_n, \bar{k}_n} = \bigoplus _{k=1}^{M_n}\,\big [W_k(\bar{t}_{1,n}), W_k(\bar{t}_{2,n}),\ldots , W_k(\bar{t}_{\bar{k}_n,n})\big ]. \end{aligned}$$ -

\(\bar{M} = (M_n)_{n=1}^{\infty } \in \mathcal {G}_\delta \) with \(M_n\) indicating number of initial Wiener process coordinates used by the method \({\overline{X}_{M_n,\bar{k}_n}}, \,n \in {\mathbb N}\).

-

The method \({\overline{X}_{M_n,\bar{k}_n}}\) is assumed to evaluate W in the time points from \(\mathcal {N}_{M_n, \bar{k}_n},\) yielding a process \({\overline{X}_{M_n,\bar{k}_n}}(a,\sigma ,W)\) being an approximation of X. Namely, we assume the existence of Borel measurable mappings \(\bar{\phi } = (\phi _n)_{n=1}^\infty ,\) with \(\phi _n: \mathbb {R}^{\bar{k}_n \cdot M_n} \mapsto L^2([0,T]),\) such that

$$\begin{aligned} \phi _n(\mathcal {N}_{M_n, \bar{k}_n}(W)) = {\overline{X}_{M_n,\bar{k}_n}}, \quad n \in \mathbb {N}. \end{aligned}$$Note that while discrete information about Wiener process is leveraged, the method may use e.g. interpolation techniques to yield a full approximate trajectory of the solution process.

The class of algorithms satisfying above conditions are denoted by \(\chi _{noneq}.\) In this paper, we distinguish a subclass \(\chi _{eq}\subset \chi _{noneq}\) of methods leveraging equidistant partitions

The optimality in class of methods leveraging equidistant meshes for the global approximation problem in finite-dimensional model has been considered recently in, e.g., [11]. In this paper, we also show the benefit of leveraging adaptive meshes instead of equidistant ones.

The cost of the algorithm \({\overline{X}_{M_n,\bar{k}_n}}\) is defined as a number of evaluations of scalar Wiener processes performed by \({\overline{X}_{M_n,\bar{k}_n}}\). Specifically, we have

While in case of \(\sigma \equiv 0\), we actually deal with ordinary differential equations and still some calculations need to be performed, there is no W process involved. In our setting, this is justified by zero cost.

The global approximation error is measured in a product \(L^2(\Omega \times [0,T])\) norm

For a fixed method \({\overline{X}_{M_n,\bar{k}_n}}=(\bar{\Delta }, \bar{\mathcal {N}}, \bar{M}, \bar{\phi }) \in \chi _{noneq}\setminus \chi _{eq},\) we define the sequence of augmented partitions \(\widetilde{\Delta } = (\widetilde{\Delta }_n)_{n=1}^\infty \) with

where \(\bar{k}_n^{1/2}/ m_n \rightarrow 0\) and \(m_n/ \bar{k}_n \rightarrow 0,\) \(n\rightarrow +\infty ,\) and \(\Delta _{m_n}^{eq} = (t_j^{eq})_{j=0}^{m_n}\) is an equidistant partition, \(t_j^{eq} = Tj/m_n, \ j=0, \ldots , m_n.\) In the sequel, by \(\widetilde{k}_n\), we denote the number of distinct time points \(\widetilde{t}_{j,n}\) in \(\widetilde{\Delta }_n.\) Consequently, we get

which in turn implies that

In addition, we introduce augmented information vectors \(\widetilde{\mathcal {N}} = (\widetilde{\mathcal {N}}_{M_n, \widetilde{k}_n}(W))_{n=1}^{\infty },\) where

For brevity, in the sequel, we will use the notation \(\Delta \widetilde{t}_{j,n} = \widetilde{t}_{j+1,n} - \widetilde{t}_{j,n}, \ n\in {\mathbb N}, \ j = 0,1,\ldots , \widetilde{k}_n-1.\)

Now for fixed \(n\in {\mathbb N}\), we estimate distance between truncated dimension time-continuous Euler process \(\widetilde{X}_{M_n,\widetilde{k}_n}^{E}\) based on partition \(\widetilde{\Delta }_{n}\) and the associated time-continuous conditional Euler process

which leverages the augmented information \(\widetilde{\mathcal {N}}_{M_n, \widetilde{k}_n}(W).\) We refer to, e.g., [12] for more details on conditional Euler process in finite-dimensional setting when also jumps modelled by homogeneous Poisson process are considered.

We obtain

where \(\hat{W}_{j,k,n}\) is a Brownian bridge on the interval \([\widetilde{t}_{j,n}, \widetilde{t}_{j+1,n}],\) conditioned on \(W_k.\) For more details on Brownian bridge, we refer to e.g. [19]. Furthermore,

Combining Theorem 1 and the fact that \({\overline{X}_{M_n,\bar{k}_n}}\) is \(\sigma (\bar{\mathcal {N}}_{M_n,\bar{k}_n}(W))\)-measurable, we get

Furthermore, (18), (19), and the relation \(\bar{\mathcal {N}}_{M_n,\bar{k}_n}(W) \subset \widetilde{\mathcal {N}}_{M_n,\widetilde{k}_n}(W)\) yield

where both \(D_1, D_2\) do not depend on n (explicitly or implicitly via \(M_n\) or \(\bar{k}_n, \widetilde{k}_n\)). Hence, by (4), (13), (19), and the definition of \(m_n,\) we have

By the Hölder inequality, we arrive at

Next, by Fact 2 in Appendix, (16), (21), and (22), we obtain

Since

we finally get for all \({\overline{X}_{M_n,\bar{k}_n}}\in \chi _{noneq}\) that

For \({\overline{X}_{M_n,\bar{k}_n}}\in \chi _{eq},\) the proof follows analogous steps, except for taking simply \(\widetilde{\Delta }_n = \bar{\Delta }_n\) in (15). Leveraging the fact that \(\Delta \widetilde{t}_{j,n} = \frac{T}{\bar{k}_n}, \ j=0,\ldots , \bar{k}_n -1,\) leads to

Consequently, (24) implies that for all \({\overline{X}_{M_n,\bar{k}_n}}\in \chi _{eq}\) it holds

Considering (23) and (25), we are ready to formulate the main result of this section.

Theorem 2

Let us denote by \(\chi _{noneq}^{\bar{M}}\subset \chi _{noneq}\) a set of all admissible methods with fixed truncation level sequence \(\bar{M}.\) We have the following asymptotic lower bound

In particular, restriction to the subclass \(\chi _{eq}\) gives sharper asymptotic lower bound

Remark 4

The restriction (13) imposed on \(\bar{k}_n\) is not limiting, as the majority of algorithms used in practice leverage \(\mathcal {O}(n)\) nodes. We also stress that \(\overline{C}_1, \overline{C}_2,\) as well as the related sequence \(\bar{k}_n,\) depend on the method \(\overline{X}\) and need not be the same across all considered algorithms. Furthermore, we allow only discrete, finite-dimensional evaluations of W. Therefore, for all \(n\in \mathbb {N},\) the vector \(\mathcal {N}_{M_n, \bar{k}_n}\) is \(\sigma \big (W_1, W_2,\ldots ,W_{M_n}\big )\)-measurable. Moreover, different partitions among various coordinates of W are not permitted in our setting.

Remark 5

We stress that while the sequences \(\bar{\Delta }\) and \(\bar{\phi }\) might depend on \(a,\sigma ,\) they cannot base on the trajectory of W. The resulting information about Wiener process is then called non-adaptive, while the associated algorithms are referred to as path-independent. For path-dependent version of Euler algorithm in finite-dimensional setting, see, e.g., [20].

Remark 6

It should be noted that lower bounds in Theorem 2 diverge to infinity when \(n \rightarrow +\infty \) in both subclasses. This significantly differs from finite-dimensional case, when the truncation level sequence was bounded from above. That saying, when \(M_n \equiv 1,\) we have \(\Vert \sigma (t)\Vert _{\ell ^2}^2 = |\sigma _1(t)|^2\) for all \(t\in [0,T],\) and the asymptotic constant appearing in (26) is consistent with the result from Theorem 2 in [8].

Notably, for given sequence \(\overline{M},\) in Sect. 4.1 and Sect. 4.2, we construct algorithms which asymptotically attain lower bounds appearing in Theorem 2. Then, in Sect. 4.3, we discuss the existence of optimal algorithms in a class of methods taking into account all permitted truncation sequences \(\overline{M}.\)

4 Construction of asymptotically optimal methods

4.1 Optimal algorithm in class of methods \(\chi _{eq}^{\bar{M}}\)

First, we fix \(\bar{M} = (M_n^*)_{n=1}^{\infty }\) satisfying (4). Next, for any \(n \in \mathbb {N}\) let us denote by \(X_{M_n^*, n}^{Eq}\in \chi _{eq}\) the truncated dimension Euler method based on equidistant mesh \(\Delta ^{eq}_n: 0 = t_{0,n}^{eq}< \ldots <~t_{n,n}^{eq} =~T,\) where \(t_{j,n}^{eq} = \frac{Tj}{n}, \ j=0,1,\ldots , n.\) The scheme is defined as follows:

The outcome of the method is a stochastic process \(\big (X_{M_n^*, n}^{Eq*}(t)\big )_{t\in [0,T]}\) obtained by linear interpolation between two subsequent nodes \(t_{j,n}^{eq}\) and \(t_{j+1,n}^{eq},\) i.e.,

\(j=0,1,\ldots , n-1.\) Let us also denote by \(\mathcal {N}_{M_n^*,n}^{eq}(W)\) the related information vector. In addition, by \(\widetilde{X}_{M_n^*,n}^{E,eq}\), we understand the truncated dimension time-continuous Euler process based on the mesh \(\Delta ^{eq}_n,\) \(n\in \mathbb {N}.\) Certainly, it holds

Consequently, from Theorem 1 and (30) it follows

Therefore, by repeating the reasoning as in (18) and the fact that

the inequality (31) implies

Finally, by (32), we have

which establishes the lower bound in Theorem 2 for fixed class \(\chi _{eq}^{\bar{M}}\). Note that \(X_{M_n^*,n}^{Eq}\) is an implementable algorithm, and it does not require the knowledge of the trajectories of (truncated) Wiener process.

4.2 Optimal algorithm with adaptive path-independent step-size control in class \(\chi _{noneq}^{\bar{M}}\)

In this section, we construct an optimal method in class \(\chi _{noneq}^{\bar{M}}\) for fixed truncation level sequence \(\bar{M} = (M_n^*)_{n=1}^{\infty }\in \mathcal {G}_\delta \). To this end, we define truncated dimension Euler scheme \((X_{M_n^*,k_n^*}^{step})_{n=1}^{\infty }\) with adaptive path-independent step-size of the following form.

First, let \(\bar{\varepsilon } = (\varepsilon _n)_{n=1}^{\infty } \subset {\mathbb R}_+\) be a non-increasing sequence satisfying

We note that the second equality in (34) implies the existence of \(C_0 > 0 \) such that for all \(n\in \mathbb {N}\) it holds \(n\varepsilon _n^2 > C_0.\) Hence,

For fixed \(n \in \mathbb {N}\) the proposed scheme utilises step-size control with \(\hat{t}_{0,n}:= 0\) and

where \(k_n^* = \inf \{j \in \mathbb {N} \ | \ \hat{t}_{j,n} \ge T \},\) \(n\in \mathbb {N}.\) We will denote the corresponding mesh by \(\hat{\Delta }_n.\) Then, we set

In the sequel, we will use the notation \(\Delta ^*_n = \hat{\Delta }_n \setminus \{\hat{t}_{k_n^*,n}\} \cup \{T\}\) and \(t_{j,n}^* = \hat{t}_{j,n}, \ j=0,1,\ldots , k_n^*-1,\) \(t_{k_n^*,n}^*=T.\) The corresponding information vector will be denoted by \(\mathcal {N}_{M_n^*,k_n^*}^*(W).\) Also, by \(\Delta \hat{t}_{j,n},\) \(\Delta t_{j,n}^*\), we will understand the j–th time step for the discretisation \(\hat{\Delta }_{n}\) and \(\Delta _{n}^*,\) respectively.

The final process \(X^{*}_{M_n^*,k_n^*} = \big (X^{*}_{M_n^*,k_n^*}(t)\big )_{t\in [0,T]}\) approximating X is obtained by piecewise linear interpolation between \(X_{M_n^*,k_n^*}^{step}({t}_{j,n}^*)\) and \(X_{M_n^*,k_n^*}^{step}({t}_{j+1,n}^*).\) We recall that in our model (1), the process \(X^{*}_{M_n^*,k_n^*}\) coincides with the time-continuous conditional Euler process

based on the sequence of partitions \(\Delta ^*_n.\)

Fact 1

-

a)

The proposed method \(X_{M_n^*,k_n^*}^{step}\) with adaptive step-size control is an element of \(\chi _{noneq}\) and attains point T, irrespective of prior choice of the sequences \(\bar{M}\) and \(\bar{\varepsilon }.\)

-

b)

\(k_n^*\) is deterministic and \(\lim \limits _{n\rightarrow +\infty } k_n^*(\sigma ) = +\infty .\)

-

c)

\(\max \limits _{0\le j \le k_n^*-1} (t_{j+1,n}^* - t_{j,n}^*) \le \frac{T}{n\varepsilon _n} \rightarrow 0, \ \ n \rightarrow +\infty .\)

Proof

Since for every \(M,n \in \mathbb {N}\) and \(j = 0, \ldots , k_n^*\), we have

for \(n_0 = \lfloor n (\varepsilon _n + \hat{C})\rfloor + 1\) it holds \(\hat{t}_{n_0,n} \ge T.\) Combining this, (34), and (35), we have that \(n\varepsilon _n^2 \le n\varepsilon _n \le k_n^* \le n_0(n),\) \(n\in \mathbb {N}.\) This, together with the fact that \(n\varepsilon _n = o(n),\) proves both assertions a) and b).

Now, we investigate asymptotic behaviour of the method error. Let us denote

and

By Fact 2, we get that

Consequently, from (38), (40), and the fact that for all \(a,b \ge 0\)

we obtain

the inequality (41) implies

Also, note that (36) results in

Consequently, since \(k_n^* = \mathcal {O}(n)\) by Fact 1, from (43) it follows

for some \(\tilde{C}>0.\) Consequently, (42) together with (43) yield

Furthermore, by (43) and (45), we arrive at

where \(K_6\) does not depend on n on the virtue of (44). Since \(t_{k_n^*,n}^* = T,\) we also have

By (46), (47), and Fact 1, we obtain

Combining (46) and (48) results in

On the other hand, by Theorem 1, Fact 1, and (37), we have

for some \(K_{10}>0\) which depends only on the constants \(C_1, C_2, T.\)

Therefore, from (4), (34), and (50) it follows

Rewriting (51) analogously as in (17) and (18), we conclude that (49) and (51) imply

Hence, (52) yields

which establishes lower bound in (26) for class \(\chi _{noneq}^{\bar{M}}.\)

4.3 Asymptotically (almost) optimal algorithms for classes \(\chi _{eq}, \chi _{noneq}\)

In this subsection, we extend optimality results obtained for fixed truncation level sequences \(\bar{M}\) to the general classes of considered methods \(\chi _{eq}, \chi _{noneq}\). Our final conclusions are gathered in Theorem 3.

Theorem 3

Let \(a,\sigma \) satisfy conditions (A1)-(A4) and (S1)-(S3) with sequence \(\delta \), respectively. Let also \(\diamond \in \{noneq, eq\}.\) Then, for every method \(\bar{X}=({\overline{X}_{M_n,\bar{k}_n}})_{n=1}^{\infty } \in \chi _{\diamond }\), we have

Moreover, for every truncation level sequence \(M_n\) with \(\delta ^{-1}(n^{-1/2})=o(M_n), \ n\rightarrow +\infty ,\) there exists a sequence \(M^* = (M^*_n)_{n=1}^{\infty }\in \mathcal {G}_{\delta }\) such that \(M_n^* = o (M_n), \ n\rightarrow +\infty ,\) and

(a) the truncated-dimension Euler algorithm with adaptive path-independent step-size \(X^{*} = \big (X^*_{M_n^*, k_n^*}\big )_{n=1}^{\infty }\in \chi _{noneq}\) satisfying

(b) the truncated-dimension Euler algorithm \(X^{Eq*} = \big (X^{Eq*}_{M_n^*, n}\big )_{n=1}^{\infty }\in \chi _{eq},\) based on the sequence of equidistant meshes, and satisfying

Proof

First, we note that (4) and monotonicity of \(\delta ^{-1}\) imply that for every admissible truncation level sequence \(\bar{M} = (M_n)_{n=1}^{\infty }\in \mathcal {G}_{\delta }\) it holds \(M_n \gtrapprox \delta ^{-1}\big (n^{-1/2}\big )\). This in turn implies that (53) is satified for every \(\bar{M}\) and method \(\overline{X}_{M_n, n}\) in \(\chi _{noneq}\) and \(\chi _{eq},\) respectively.

However, the lower bound in (53) cannot be asymptotically attained by any algorithm. Otherwise, the truncation level would satisfy \(M_n \approx \delta ^{-1}(n^{-1/2}),\) which in turn would violate the property (4). Nevertheless, for every sequence \(\bar{M}:=(M_n)_{n=1}^{\infty }\in \mathcal {G}_\delta \) there exists a constant \(k_0^{\bar{M}} = k_0(\bar{M}) \in \mathbb {N}\) such that for every \(k\ge k_0^{\bar{M}}\), we have

and both sequences in (56) belong to \(\mathcal {G}_\delta ,\) with natural logarithm being composed k-times. For fixed k, denote the sequence on the right side of (56) by \(\bar{M}^k=(\bar{M}^k_n)_{n=1}^{\infty },\) and the output of an optimal method \((X^{*,k}_{\diamond }) = \big (X^{*,k}_{\diamond }(t)\big )_{t\in [0,T]}\) in corresponding class \(\chi _{\diamond }^{\bar{M}^{k}}, \ \diamond \in \{eq, noneq\},\) respectively. For every \(k\in \mathbb {N},\) \(X^{*,k}_{eq}\) is a truncated dimension Euler scheme based on equidistant mesh, while \(X^{*,k}_{noneq}\) is a truncated dimension Euler scheme with adaptive path-independent step-size control (36).

As a result, we have the following relation between the exact asymptotic behaviour of the method errors

holding for all \({\overline{X}_{M_n,\bar{k}_n}}\in \chi _{\diamond }^{\bar{M}}.\) Since the constructed sequence satisfies \(\bar{M}^k_n = o(M_n), \ n\rightarrow +\infty , \) this concludes the proof. \(\square \)

Remark 7

Due to leveraging the alternative truncation sequence as per (56), the asymptotic benefit is at least of order \(\left( M_n / \bar{M}^k_n\right) ^{1/2},\) which is unbounded and diverges to infinity, as \(n\rightarrow +\infty \). In particular, this ratio can be significant also for smaller values of n, especially for sequences \(\delta \) converging relatively slowly to zero.

Remark 8

In class \(\chi _{noneq}\), we consider only algorithms which are non-adaptive with respect to the number of leveraged Wiener process coordinates. In particular, this results in lower bound for cost times error terms in (26), (27) diverge to infinity, as the cost rises. On the other hand, this is not the case for finite-dimensional noise structure, see, e.g., [12, 20]. We conjecture that this term can be significantly lowered when additional adaptation with respect to Wiener process coordinates is introduced. We plan to investigate such algorithms in our future work.

5 Numerical experiments and implementation issues in Python

5.1 Solver implementation in Numba

In this section, we exhibit alternative implementation of \(X_{M_n^*,k_n^*}^{step},\) which leverages Numba compiler in Python. This enables us to execute specified functions, called kernels, on the GPU (Graphics Processing Unit) device which supports CUDA API developed by NVIDIA. For more details on parallel computing and kernel execution for a specified grid of blocks and threads, we refer to [10, 23]. Due to the fact that truncated dimension Euler scheme can be executed independently on each thread, we would expect significant decrease of the computation time when compared to the similar calculations on CPU (Central Processing Unit). This is beneficial especially when large number of the trajectories should be simulated.

The crucial part of the code responsible for the algorithm \(X_{M_n^*,k_n^*}^{step}\) execution on GPU, together with relevant comments, can be found in the listing below.

5.2 Results of numerical experiments in Python

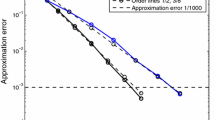

In this section, we present results of numerical experiments performed on CPU by using Multiprocessing library in Python programming language. We analyse the asymptotic error behaviour for both algorithms \(X_{M_n^*,k_n^*}^{step}\) and \(X_{M_n^*,n}^{Eq}\) by verifying if the ratio between constants \(\mathcal {C}_{noneq}\) and \(\mathcal {C}_{eq},\) appearing in Theorem 2, is attained.

To this end, we consider the following parameters: \(T =1.5, \ x_0 = 0.9,\) and the equation coefficients

where \(p>1/2.\) One can show that for all \(l\in \mathbb {N}, \ l > 1\) it holds

By substituting \(v = (2p-1)\log (x+1),\) we arrive at

and the integral appearing in (59) is equal to the upper incomplete gamma function \(\Gamma \big (1, (2p-1)\log (l+1)\big ).\) Since for all \(s\in \mathbb {N}, x>0\), we have

combining (59) and (60) yields

Therefore, we can assume \(\delta (n) \approx n^{1/2-p},\) which implies \(\delta ^{-1}(n^{-1/2})\approx n^{\frac{1}{2p-1}}.\) In our simulations, we set \(p = 0.9,\) hence \(M_n \gtrapprox n^{5/4 + \varepsilon }\in \mathcal {G}_\delta \) for all \(\varepsilon > 0.\) We decide to choose \(\varepsilon = 0.03.\) Consequently, it suffices to take \(M_n = \Theta (n^{1.28}),\) \(n \rightarrow +\infty \).

Now, we provide the values of the constants \(\mathcal {C}_{noneq}\) and \(\mathcal {C}_{eq}\) in our model. First, for all \(t\in [0,T]\), we have that

Finally, the constant appearing in lower bounds for \(\chi _{eq}\) is equal to

while in \(\chi _{noneq}\)

While the analytical form of the unique solution to the Eq. (1) with coefficients as per (57) and (58) is not known, generation of its trajectories requires simulation of underlying stochastic integrals. Therefore for each \(X^{alg}\in \{X_{M_n^*,k_n^*}^{Eq*}, X_{M_n^*,k_n^*}^{step}\}\), we execute in parallel the algorithm \(X_{W_{ratio}\cdot M_n^*,n^*}^{Eq*}\) based on equidistant mesh with \(n^* = 10^6\) nodes and first \(W_{ratio}\cdot M_n^*\) coordinates of the countably dimensional Wiener process W. Let us denote the corresponding process by \(X_{M_n^*,n^*}.\) The method error, \(\text {err}_K(X^{alg}),\) is estimated by simulating K trajectories of the underlying processes. We measure the difference between each pair of trajectories by using the composite Simpson quadrature Q based on time points for which \(X^{alg}\) is evaluated, together with the midpoints of the corresponding subintervals. To summarise, we take

where \(X^{alg}_l,\) \(X_{W_{ratio}\cdot M_n^*,n^*,l},\) and \(W^{(l)}\) are the l–th generated trajectories of the corresponding processes. Finally, we compare empirical improvement ratio \(\text {err}_K(X_{M_n^*,k_n^*}^{step}) /\) \(\text {err}_K(X_{M_n^*,k_n^*}^{Eq*})\) with the theoretical value \(\mathcal {C}_{noneq} / \mathcal {C}_{eq} \simeq 0.85113723.\) The testing results are exhibited in Table 1.

The average improvement from leveraging adaptive mesh is generally visible. For \(n\in \{5000,10,000\}\), we executed smaller number of trajectories due to high complexity and time consumption. We also note that the impact of leveraging (61), Monte Carlo simulation, and rare-fine mesh comparison as an approximation of the method error is not quantified. Nevertheless, the obtained ratios are roughly aligned with the expected asymptotic error behaviour.

6 Conclusions

We investigated the global approximation of SDEs driven by countably dimensional Wiener process, where the diffusion term depends only on the time variable. For fixed sequence \(\delta ,\) modelling level of decay for the diffusion term, we derived lower bounds for asymptotic error in suitable classes of algorithms leveraging specified truncation levels of the Wiener process. In particular, we quantified asymptotic benefit from leveraging step-size control instead of equidistant mesh. We also constructed two truncated dimension Euler schemes which are the (almost) optimal algorithms in the respective classes. Our results indicate that the decrease of method error requires significant increase of the cost term, which is illustrated by the product of cost and minimal error diverging to infinity. Nonetheless, we conjecture that the estimates might be beaten in case we allow for additional adaptation with respect to different Wiener process coordinates.

Availability of supporting data

The datasets generated during and/or analysed during the current study are available from the corresponding author on reasonable request.

References

Applebaum, D.: Lévy Processes and Stochastic Calculus, 2nd edn. Cambridge University Press, Cambridge (2009)

Cao, G., He, K.: On a type of stochastic differential equations driven by countably many Brownian motions. J. Funct. Anal. 203, 262–285 (2003)

Carmona, R., Teranchi, M.: Interest rate models: an infinite dimensional stochastic analysis perspective. Springer, Berlin (2006)

Cohen, S.N., Elliot, R.J.: Stochastic calculus and applications, 2nd edn. Probability and its applications, Birkhäuser, New York (2015)

Da Prato, G., Zabczyk, J.: Stochastic equations in infinite dimensions, second ed., Cambridge University Press (2014)

Gyöngy, I., Krylov, N.V.: On stochastic equations with respect to semimartingales I. Stochastics 4, 1–21 (1980)

Heinrich, S.: Lower complexity bounds for parametric stochastic Itô integration. J. Math. Anal. Appl. 476, 177–195 (2019)

Hofmann, N., Müller-Gronbach, T., Ritter, K.: Optimal approximation of stochastic differential equations by adaptive step-size control. Math. Comput. 69, 1017–1034 (1999)

Hofmann, N., Müller-Gronbach, T., Ritter, K.: The optimal discretization of stochastic differential equations. J. Complex. 17, 117–153 (2001)

Kałuża, A.: Optimal algorithms for solving stochastic initial-value problems with jumps, PhD thesis, AGH University of Science and Technology, Kraków 2020, Click here to access BG AGH repository

Kałuża, A.: Optimal global approximation of systems of jump-diffusion SDEs on equidistant mesh. Appl. Numer. Math. 179, 1–26 (2022)

Kałuża, A., Przybyłowicz, P.: Optimal global approximation of jump-diffusion SDEs via path-independent step-size control. Appl. Numer. Math. 128, 24–42 (2018)

Kruse, R., Wu, Y.: A randomized Milstein method for stochastic differential equations with non-differentiable drift coefficients. Discrete Contin. Dyn. Syst. Ser B 24, 3475–3502 (2019)

Liang, Z.: Stochastic differential equation driven by countably many Brownian motions with non-Lipschitzian coefficients. Stoch. Anal. Appl. 24, 501–529 (2006)

Morkisz, P.M., Przybyłowicz, P.: Strong approximation of solutions of stochastic differential equations with time-irregular coefficients via randomized Euler algorithm. Appl. Numer. Math. 78, 80–94 (2014)

Morkisz, P.M., Przybyłowicz, P.: Randomized derivative-free Milstein algorithm for efficient approximation of solutions of SDEs under noisy information. J. Comput. Appl. Math. 383, 1–22 (2021)

Novak, E.: Deterministic and stochastic error bounds in numerical analysis. Lecture Notes in Mathematics, vol. 1349. New York, Springer-Verlag (1988)

Platen, E., Bruti-Liberati, N.: Numerical solution of stochastic differential equations with jumps in finance. Springer Verlag, Berlin, Heidelberg (2010)

Przybyłowicz, P.: Optimal sampling design for global approximation of jump diffusion stochastic differential equations. Stochastics Int. J. Probab. Stoch. Proc. 91, 235–264 (2019)

Przybyłowicz, P.: Efficient approximate solution of jump-diffusion SDEs via path-dependent adaptive step-size control. J. Comp. Appl. Math. 350, 396–411 (2019)

Przybyłowicz, P., Schwarz, V., Szölgyenyi, M.: A higher order approximation method for jump-diffusion SDEs with discontinuous drift coefficient, preprint arXiv:2211.08739 (2022)

Przybyłowicz, P., Schwarz, V., Szölgyenyi, M.: Lower error bounds and optimality of approximation for jump-diffusion SDEs with discontinuous drift, preprint arXiv:2303.05945 (2023)

Przybyłowicz, P., Sobieraj, M., Stȩpień, Ł: Efficient approximation of SDEs driven by countably dimensional Wiener process and Poisson random measure. SIAM J. Numer. Anal. 60, 824–855 (2022)

San Martin, J., Torres, S.: Euler scheme for solutions of a countable system of stochastic differential equations. Stat. Prob. Lett. 54, 251–259 (2001)

Situ, R.: Theory of stochastic differential equations with jumps and applications, Springer Science+Business Media (2005)

Traub, J.F., Wasilkowski, G.W., Woźniakowski, H.: Information-based complexity. Academic Press, New York (1988)

Acknowledgements

The author would like to thank two anonymous reviewers whose valuable comments allowed to enhance the manuscript. In addition, the author would like to thank Paweł Przybyłowicz for his support and beneficial discussions on the results presented in this work.

Funding

No funding was received to assist with the preparation of this manuscript.

Author information

Authors and Affiliations

Contributions

Ł. Stȩpień is the only author of all elements of this manuscript.

Corresponding author

Ethics declarations

Ethical approval

Not applicable

Conflict of interest

The author declares no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Fact 2

Let \(\sigma \) satisfy (S1)-(S3) with a sequence \(\delta \). Then, for every \(\bar{M} = (M_n)_{n=1}^\infty \in \mathcal {G}_\delta \) and an arbitrary sequence of partitions \((\Delta _n)_{n=1}^{\infty }\) with

with \(\bar{k}_n \in \mathbb {N},\) we have

where \(\Delta t_{j,n} = t_{j+1,n} - t_{j,n}, \ n\in \mathbb {N}, \ j =0,\ldots , \bar{k}_n-1.\)

Proof of Fact 2

Let us fix \(n\in \mathbb {N}.\) Since

we split the proof into two parts, by estimating each term in (64) separately.

First, by the property (S2), we obtain

Second, by applying n times the mean value theorem for integrals, we have

Therefore, by (S2) and (66), it holds

Now, the assertion of the fact follows from (64), (65), and (67).

Proof of Proposition

2 For fixed \(M,n \in \mathbb {N},\) we use the following decomposition of the process X and the truncated dimension time-continuous Euler process

where

and

Therefore,

with

From the Hölder inequality and Lemma 1, we have that

By Corollary 14.2.9 in [4], we get that

For brevity, we introduce the following notation for \(u \in (t_{j,n},t_{j+1,n}]\)

and

Therefore, we have for all \(t \in [0,T]\) that

where

Moreover, by the Hölder inequality, (11) and Lemma 1, we obtain for \(t \in [0,T]\) that

By the Fubini theorem and the fact that Itô integrals defined on disjoint intervals are uncorrelated, for \(t \in [0,T]\), we get that

From Theorem 88 (iii) in [25], (11), and (70), we obtain

Combining (71), (72), and (73) yields

In addition, we estimate the term

Finally, by (68), (69), (74), and (75), for all \(t\in [0,T]\) it holds

where the constants \(D_1, D_2\) do not depend on the parameters M, n.

Now, we estimate the diffusion-related term. By (S2), we have for \(t\in [0,T]\) that

By (76) and (77), we get that for all \(t \in [0,T]\)

Note that the mapping \(\displaystyle {[0,T]\ni t \mapsto \sup _{0 \le u \le t}\mathbb {E}\Vert X^M(u) - {\widetilde{X}_{M,n}^E}(u)\Vert ^p}\) is Borel (as a non-decreasing function) and bounded. Therefore, the Grönwall’s lemma yields

where \(D_{0}\) does not depend on truncation parameter M and mesh size \(k_n\). Now, (10) is a direct consequence of (78). \(\square \)

Lemma 2

Let \(a,\sigma \) satisfy conditions (A1)-(A4) and (S1)-(S3), respectively. There exists \(K \in (0,+\infty )\) such that for every \(M,n\in \mathbb {N}\) it holds

Proof

This property of the truncated dimension time-continuous Euler scheme has been shown for more generalised model structure in [23] for pointwise approximation problem. We refer to this paper for an outline of the proof. \(\square \)

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Stępień, Ł. Adaptive step-size control for global approximation of SDEs driven by countably dimensional Wiener process. Numer Algor 96, 1699–1725 (2024). https://doi.org/10.1007/s11075-023-01682-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11075-023-01682-y

Keywords

- Stochastic differential equations

- Countably dimensional Wiener process

- Adaptive step-size control

- Minimal error bounds

- Information-based complexity

- Asymptotically optimal algorithm