Abstract

Customer orientation is a central tenet of marketing. However, less is known about how customer orientation varies across countries and time. Mintz, Currim, and Deshpandé (Eur. J. Mark., 56: 1014–1041, 2022) propose a country-level construct, national customer orientation, and develop theoretical propositions on how a country’s wealth and average customer price sensitivity affect national customer orientation during and after global economic shocks without providing an empirical test. This paper tests drivers of national customer orientation by employing World Economic Forum and World Bank annual panel data from 112 countries between 2007 and 2017. The results show that customer orientation is a greater luxury of richer nations and price sensitivity is a partial mediator of that relationship; however, both relationships only transpire in non-recessionary times. The empirical test furthers scholarly research on national customer orientation and provides managers with country-level customer orientation benchmarks across countries and time.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In today’s connected global economy, firms often rely on profitable opportunities in multiple countries (Morgeson et al. 2015). However, operating across multiple countries presents challenges, notably because customers have differing expectations across countries (Sheth 2011). For example, previous research has shown that customer satisfaction (Morgeson et al. 2011), trust (Steenkamp and Geyskens 2006), and price sensitivity (Kübler et al. 2018) in addition to the effectiveness in marketing-mix efforts (Datta et al. 2022), advertising spending during downturns (Deleersnyder et al. 2009), new product introduction strategies (Kalish et al. 1995), and metrics managers employ for marketing-mix decisions (Mintz et al. 2021) vary by country. Consequently, firms must learn and adapt to customer expectations in a country to successfully operate, and this requires the use of national-level benchmarks (Li and Calantone 1998).

The marketing discipline has increasingly advocated firms adopt a customer orientation (Deshpandé et al. 1993) since customer orientation is associated with positive financial, customer, innovation, and employee outcomes (Kirca et al. 2005). However, the customer and market orientation literatures are almost exclusively micro organizational-level studies in single or limited number of countries, with few to no macro country-level studies (e.g., Brower and Nath 2018). Also, global top management teams report that persuading foreign offices to adopt a customer orientation encounters substantial resistance from local managers (McKinsey & Company 2017): nearly half (46%) of CMOs report struggling to implement global customer-centric efforts (Isobar 2019).

Currently, macro country-based benchmarks are readily available and widely employed by managers for economic constructs such as inflation and employment (e.g., International Monetary Fund; World Bank), and behavioral constructs such as culture (e.g., Hofstede 1980; World Values Survey). Yet, to our knowledge, there are no such macro country-based customer orientation or marketing-focused benchmarks. In contrast, cross-national marketing research, as summarized by Sheth (2011), primarily focuses on identifying why and when products will be successful, whether firms should adapt or standardize marketing-mix strategies, country-of-origin effects, and whether brands can/should become global, regional, or local. Thus, Palmatier et al. (2019, p. 8) state: “what customer centricity looks like when it spans the local-global terrain of most organizations is worthy of deeper consideration” and “as business globalization continues, more research will be needed to examine cross-cultural and national differences in the effectiveness of customer centricity.”

In this paper, we are the first to empirically test drivers of national customer orientation—“the average level of customer orientation across firms operating in a country based on firms’ understanding, consideration, and treatment of customers, and their success at delivering value to customers” (Mintz, Currim, Deshpandé 2022, p. 1022). We build on Mintz, Currim, and Deshpandé’s (MCD) (2022) purely conceptual development of national customer orientation to empirically examine three research questions related to its drivers. The three questions are based on core macro-economic factors (Bernanke et al. 2019) that also have data readily available to allow implementation by firms and scholars. First, based on the economic theory of production (e.g., Wolman 1921), we ask whether customer orientation is a greater luxury of rich nations (countries with higher GDP/capita). Second, based on the marketing theory of buyer segmentation and product differentiation (e.g., Smith 1956), we consider whether average national customer price sensitivity (the extent to which customers in aggregate in a country make purchase decisions based on price relative to non-price attributes) mediates the relationship between GDP/capita and customer orientation. Third, based on the global economic shocks and business cycles literature (e.g., Schumpeter 1939), we ask whether the effects of a country’s wealth and its national customer price sensitivity on national customer orientation are moderated by global economic shocks such as the Global Financial Crisis (GFC) of 2007–2009.

We test our empirical questions across 112 countries by employing annual panel data between 2007 and 2017 from the World Economic Forum (WEF) and the World Bank (WB). Our analysis finds that in aggregate, customer orientation is a greater luxury of rich nations and price sensitivity mediates this relationship. However, our analysis finds that customer orientation is a greater luxury of rich nations and price sensitivity mediates this relationship only after the GFC induced recession (and not during it). In addition, we investigate moderators and boundary conditions not part of MCD’s framework, the results of which are reported in the Robustness Tests section. Our findings provide managers and academics customer-centric benchmarks and drivers of such benchmarks that are easily accessible for 112 countries.

2 Conceptual framework

2.1 National customer orientation construct

The national customer orientation construct is based on two main previous research considerations. First, building on cross-national research, customers in different countries are likely to have different expectations of firms’ level of customer orientation, which requires firms to localize from a global customer orientation (e.g., Datta et al. 2022; Hofstede 1980). Second, MCD’s (2022, p. 1022) definition of national customer orientation is distilled from previous cross-organizational research on customer orientation as: “the extent to which an individual firm (1) understands, considers, and treats its customers well, and (2) is successful in its marketing efforts aimed at delivering value to such customers.” Briefly, we build on this distillation based on the customer and market orientation literature (e.g., Brower and Nath 2018; Deshpandé et al. 1993; Kohli and Jaworski 1990; Narver and Slater 1990; Palmatier et al. 2019). That is, we consider customer orientation to require companies to develop and implement customer knowledge based on customer wellbeing in an effort to “maximize the ‘effective efficiency’ of marketing actions” (Sheth et al. 2000, p. 57).

2.2 Drivers of national customer orientation

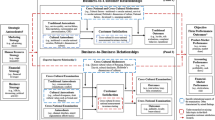

We rely on MCD’s conceptual framework for national customer orientation comprising of three primary drivers and six corresponding propositions (Web Appendix Fig. 1). We summarize the rationale underlying the propositions and refer readers to their paper for theoretical details.

First, economic and production theory (Wolman 1921) suggest that customers in wealthier countries have greater purchasing power and consumption choices due to increased competition and product availability (Burgess and Steenkamp 2006). Hence, customers in wealthier countries are likely to demand greater customer orientation than customers in less wealthy countries (Kübler et al. 2018). In response, firms in wealthier countries are likely to enact greater customer orientation policies than firms in less wealthy countries to attract and retain customers (Sheth 2011). Consequently, we expect the country wealth to positively influence its customer orientation (Proposition 1).

Second, country wealth is expected to be negatively associated with its national customer price sensitivity (Proposition 2) because customers in wealthier countries have greater disposable incomes and lower price sensitivity (Gao et al. 2017). Third, national customer price sensitivity is expected to negatively influence national customer orientation (Proposition 3) because the theory of buyer segmentation and product differentiation (e.g., Smith 1956) suggests that lower price sensitivity creates demand for non-price attributes. This demand for non-price attributes is expected to make firms better understand customers and employ customer oriented practices to identify and deliver on non-price attributes (Li and Calantone 1998).

Fourth, combining the previous three arguments, national price sensitivity is expected to mediate or explain the relationship between country wealth and its national customer orientation (Proposition 4). Price sensitivity is expected to provide further explanatory power of antecedents of national customer orientation beyond country wealth.

Fifth, the global economic shocks and business cycles literature (e.g., Schumpeter 1939) suggests that global economic crises moderate or weaken (1) the direct relationship between wealth and customer orientation (Proposition 5), and (2) the relationship between the mediator price sensitivity and customer orientation (Proposition 6). Customers often face or perceive income reductions when dealing with global economic shocks, which leads to lower overall customer demand and greater importance placed on price (Mintz 2022). Consequently, firms become increasingly focused on survival, and less focused on customer orientation (Dekimpe and Deleersnyder 2017).

3 Empirical test

3.1 Data

We obtain secondary annual panel data for 112 countries between 2007 and 2017 for each focal variable from the WEF’s Global Competitiveness Report (GCR) and the WB’s Databank (Table 1). The Web Appendix details how the WEF GCR’s captures opinions of over 14,000 business leaders from over 120 countries annually in its Executive Opinion Survey (EOS) and employs a rigorous methodology involving data treatments, weighted averages, and multiple techniques to compute country averages on their individual measures.

We average two measures taken directly from the WEF GCR to operationalize national customer orientation. The first is the degree the average firm in a country is customer-centric or treats its customers well, labeled by the WEF GCR as “degree of customer orientation.” We re-label this measure as “treatment of customers” because the WEF EOS measured it as: “In your country, how well do companies treat customers? [1 = poorly—mostly indifferent to customer satisfaction; 7 = extremely well—highly responsive to customers and seek customer retention].”

The second measure is the extent firms successfully employ marketing and differentiation efforts aimed at creating competitive advantage based on their customer-centric strategies, labeled by the WEF GCR as “extent of marketing.” We relabel this measure as “success of marketing” because the WEF EOS measured it as: “In your country, how successful are companies in using marketing to differentiate their products and services? [1 = not successful at all; 7 = extremely successful].” Since the marketing success of companies is based on both customer knowledge and its implementation for differentiation, “success of marketing” encapsulates both components.

The Cronbach alpha score of the two-item measure of national customer orientation is 0.87, demonstrating robust reliability and suitability for aggregation. The correlation between customer orientation and treatment of customers is 0.95, while that between customer orientation and success of marketing is 0.97. Further, in Web Appendix Fig. 2, we provide a scatter plot that shows the close association of each of the two items with customer orientation. In addition, the validity of the two-item measure of national customer orientation is supported by the empirical test of its drivers. If the two-item measure had inherent respondent biases within and across countries, our propositions on drivers and mediators of national customer orientation would not be supported.

Second, data on national customer price sensitivity comes from the measure labeled by the WEF GCR as “buyer sophistication,” which we re-label as “price sensitivity” because the WEF EOS measured it as: “In your country, on what basis do buyers make purchasing decisions? [1 = based solely on the lowest price; 7 = based on sophisticated performance attributes].” Third, data on GDP/capita is taken directly from the WB Databank. Fourth, the duration of the GFC, i.e., 2007–2009, is specified according to the U.S. Federal Reserve Bank. We allow for variations of the GFC’s timing in the robustness test section.

3.2 Model

To test our research questions, we estimate the following country- and time-based fixed effects model:

where CustOri, t is the national customer orientation for country i in year t, and GDPi, t − 1is the log-scaled per capita GDP in the prior year. PriceSensitivityi, t − 1 is the inverse of the level of customer price sensitivity for country i in the prior year t−1, with lower price sensitivity rated higher, to enable easier interpretation. μi are country-fixed effects to account for unobserved variables related to countries and μt are year-fixed effects to account for unobserved variables related to time.

We estimate the above model separately over two periods to test for drivers of national customer orientation during and after the GFC, wherein lagged independent variables are during the GFC (2007–2009) and after (2010–2017). This analysis allows the intercept, or α,the slopes, or β ′ s,and the country- and year-fixed effects, or μ′s, to vary between the GFC and post-GFC time periods (e.g., Bremus and Fratzscher, 2015).

All independent variables except the year dummies are lagged by a year to reduce reverse causality concerns. The use of country-fixed effects reduces omitted variables or unobserved heterogeneity concerns by controlling for largely time-invariant country characteristics such as culture, institutions, resources, and technology, which do not change rapidly over time (Witte et al. 2017). The use of time-fixed effects reduces unobserved effects concerns across nations due to omitted variables that could vary over time, such as wars, conflicts, and availability of natural resources. To account for multicollinearity between certain focal variables, we estimate separate models based on entering the correlated variables one at a time, and find that addition of potentially correlated variables does not change level of significance or flip sign/s of previously included variable/s.

Eleven controls, taken from WEF and WB, are also included in the model. However, for simplicity, we focus our reported analysis on the reduced model specified above because results of our focal variables are robust across the presence and absence of controls. Correlation matrices are in Web Appendix Table 1.

3.3 Model-free descriptive information

In Fig. 1, panel A, we provide a regional analysis of national customer orientation scores based on the United Nation’s classification of regions. We find richer regions such as Northern America (e.g., Canada, USA), Western Europe (e.g., France, Germany), and Australia/New Zealand have the highest national customer orientation scores, and poorer regions such as Middle Africa (e.g., Cameroon, Chad) and Central Asia (e.g., Kazakhstan, Kyrgyz Republic) have lower scores.

Average national customer orientation by region and year

In Fig. 1, panel B, we show how averaged national customer orientation scores evolve over time based on the WB’s income-based country classifications. We find upper-middle, lower-middle, and low-income countries’ customer orientation scores all decline during the GFC and then begin to recover after the GFC between 2011 and 2012, following a trend similar to the overall average across countries. In contrast, we observe higher-income countries’ recovery of national customer orientation takes longer, after the cessation of the GFC, with the recovery only starting between 2014 and 2015, and not entirely reaching the peaks of national customer scores obtained prior to the GFC.

In Web Appendix Table 2, we provide each individual country’s average scores and rankings across the decade of data in our analysis, for focal variables across the 112 countries in our sample. Switzerland, Japan, USA, Sweden, and Austria are the five countries with the highest average national customer orientation scores, while Mauritania, Chad, Burundi, Algeria, and Lesotho are the five countries with the lowest average national customer orientation scores.

In Fig. 2, we plot the relationship between rankings of national customer orientation (y-axis) and GDP/capita (x-axis), with countries with greater customer orientation and GDP/capita ranked higher. In Web Appendix Fig. 3, we plot the relationship between rankings of national customer orientation (y-axis) and customer price sensitivity (x-axis), with countries with higher customer orientation and lower price sensitivity ranked higher. Finally, in Web Appendix Fig. 4, we plot the relationship between rankings of customer price sensitivity (y-axis) and GDP/capita (x-axis), with countries with lower price sensitivity and larger GDP/capita ranked higher. We observe general consistency in the rankings of our focal measures across countries, indicating that our measures of national customer orientation and price sensitivity, including GDP/capita, have good face validity. In addition, we observe occasional inconsistency in the rankings of countries across our focal constructs, requiring an econometric model to test the propositions.

Relationship between national customer orientation and GDP per capita average rankings

3.4 Model-based results

We summarize the model-based results in Table 2. First, we find that GDP/capita is significantly positively associated with national customer orientation over the entire time-period (col. 1; β =.212, p<.001). Second, we find that countries with higher GDP/capita are associated with lower customer price sensitivity over the entire time period (col. 2; β =.301, p<.001). Third, we find that lower customer price sensitivity is significantly associated with higher national customer orientation over the entire time-period (col 3; β =.191, p<.001). Consequently, we find empirical support for Propositions 1–3.

Fourth, we test whether a country’s customer price sensitivity mediates the relationship between its wealth (GDP/capita) and its customer orientation (Proposition 4) over the entire time-period of analysis. To test for mediation, we follow Baron and Kenny’s (1986) five-step mediation test over Hayes (2017) PROCESS mediation test due to its suitability for panel data.

The first three of five steps in Baron and Kenny’s (1986) mediation test are those described above which support Propositions 1–3. The fourth step is to examine whether the inclusion of the mediator (national customer price sensitivity) as an additional independent variable in the model with the original independent variable (GDP/capita) and dependent variable (national customer orientation) improves model fit. We do find such a fit improvement, with the total R2 increasing from 0.58 to 0.71 when we include national customer price sensitivity in the model (cols. 3 vs. 1).

The final step to establish mediation is to examine whether the inclusion of the mediator (national customer price sensitivity) in the original model either eliminates (which is indicative of full mediation) or weakens (indicative of partial mediation) the relationship between the original independent variable (GDP/capita) and dependent variable (national customer orientation). Reduced statistical significance (a higher p-level, but still <.1) indicates partial mediation, while insignificant statistical significance (a p-level >.1) indicates full mediation. We find that including national customer price sensitivity in the model (col. 3) reduces the statistical significance (p=.003 vs. p<.001) and coefficient of GDP/capita by about 40% of its value (β =.129 vs. β =.212). Consequently, we find support for partial mediation by national customer price sensitivity on the relationship between a country’s wealth (GDP/capita) and its customer orientation, providing support for Proposition 4. Finding partial mediation of price sensitivity also indicates that its effect on national customer orientation is not just based on a wealth effect.

Fifth, we examine the moderator effects of an economic crisis on the aforementioned relationships (Propositions 5 and 6) by re-estimating the model for two separate time periods: (1) during the GFC (cols. 4–6) and (2) after (cols. 7–9). In contrast to results of the analysis of the entire time-period of our data, we find effects of GDP/capita (β =.022, p=.858) and national price sensitivity (β =.031, p=.545) are no longer statistically significant and associated with national customer orientation during the GFC (col. 6). On the other hand, we find that the effects of GDP/capita (β =.187, p=.003) and national customer price sensitivity (β =.120, p<.001) are both statistically significant and associated with national customer orientation when examining the post-GFC results (col. 9). Consequently, we find support for Propositions 5 and 6.

3.5 Robustness tests

3.5.1 Variations of focal variables

We conduct robustness test of our results using common variations of focal variables (e.g., Bernanke et al. 2019). In place of GDP/capita, we substitute (1) GDP, (2) gross national income (GNI), and (3) GNI/capita; each log-scaled. In addition, to test the robustness of our economic crisis variable, we extend the GFC years to 2012 and 2014 to account for the lagged impacts of the American crisis on other countries and the European double-dip recession, respectively. Results of the propositions remain similar in models using the three different country wealth variables and the two different GFC cut-off points.

3.6 Additional control variables

We investigate boundary conditions beyond our original conceptual framework by considering 11 monetary, fiscal, structural, technological, educational, and demographic controls selected based on the macroeconomics literature (e.g., Bernanke et al., 2019). These variables are (1) GDP percent change from year before, (2) population percentage >65 years of age, (3) competitive intensity, (4) unemployment, (5) inflation, (6) quality of management schools, (7) population (log-scaled), (8) population percent change from year before, (9) mobile phone subscribers, (10) consumption as a percentage of GDP, and (11) time required to start a business.

The model-based proposition test results retained the same signs and statistical significances when comparing models without additional controls to models with all and sub-sets of the 11 additional control variables. We also find a significant positive relationship between national customer orientation and the intensity of local competition, quality of management schools, mobile subscribers, and time required to start a business (each p<.01 except mobile subscribers which is p<.05), and a significant negative relationship between national customer orientation and population percentage >65 years of age (p<.01), population (p<.01), and population change (p<.1). However, due to word space limitations and because these variables are controls, we do not discuss these results further.

3.7 Alternative model specification

We consider a potentially different causal sequence by estimating a model that specifies national customer orientation at year t, price sensitivity at year t−1, and GDP/capita at year t−2. The results of this alternative model specification are similar in both coefficient signs and significance levels as the original analysis reported in Table 2.

3.8 Testing for a non-linear effect of GDP/capita on national customer orientation

To examine whether GDP/capita has a non-linear effect on customer orientation, we re-estimate our equations with an additional squared term for GDP/capita. We find, in aggregate, a negative significant (p=.054) association between the GDP/capita squared term and national customer orientation, where national customer orientation scores slightly plateauing among the richest nations (Web Appendix Fig. 5). However, we find that this association is no longer significant when examining the GDP/capita squared term during and after the GFC.

4 Discussion

Our research highlights how customers possess differing expectations and firms conduct different marketing strategies across countries. Those differing expectations and marketing strategies force firms to develop customer orientation strategies tailored to country customer expectations. Thus, it is critical to establish a national customer orientation construct that firms can access across a large range of countries to better understand country-based customer orientation and employ as marketing-focused benchmarks. This study is the first to empirically test propositions on what drives national customer orientation variation across countries and time. We find national customer orientation is driven by the wealth of a country, and national price sensitivity mediates this relationship; however, these results are moderated by global shocks or hold only during “good-times” (post GFC) and not during recessions (the GFC).

Marketing scholars and practitioners can employ our empirical results on drivers, mediators, and moderators to better understand why the customer orientation in some countries and times is expected to be higher than others. Scholars can also follow-up on our empirical test to consider additional drivers or antecedents and consequences at the macro-country (e.g., national culture) or micro-organizational level (e.g., firm size) that extend MCD’s conceptual framework and controls tested in our research. These additional drivers could also provide insight about the differences in recovery rates for customer orientation across groups of nations post the GFC reported in the model-free descriptive statistics. One opportunity is for scholars to disentangle how various national factors associated with the wealth of the country affect national customer orientation. A further opportunity is to develop datasets that better control for individual response differences across countries while employing as rigorous a methodology as the WEF’s.

To make the national customer orientation construct useful for scholars and practitioners, we created a website https://sites.uci.edu/nationalcustomerorientation that merges together publicly available data from the World Economic Forum, World Bank, and the United Nations. Our goal is to provide annual national customer orientation and national price sensitivity benchmark metrics based on a diverse set of firms in each of 112 countries for over a decade, so scholars and practitioners can easily access national customer orientation benchmarks per country and year between 2007 and 2017.

Furthermore, practitioners can employ our benchmark measures across countries to better assess customer orientation expectations in different countries across time. For example, practitioners can use benchmarks to assess whether they want to emphasize customer orientation more, equal to, or less than benchmark values. Customer orientation benchmarks across countries and time can help firms coordinate between headquartered and country managers’ marketing decisions, not just on the cross-national level of spending or effort, but on the tactical implementation and monitoring of efforts over time. Perhaps more importantly, our benchmarking provides practitioners two customer-related national benchmarks, customer orientation and price sensitivity, so that they do not need to solely rely on macro-economic, cultural, or geographic benchmarks to understand their cross-national customer baseline levels.

References

Baron, R. M., & Kenny, D. A. (1986). The moderator–mediator variable distinction in social psychological research: conceptual, strategic, and statistical considerations. J Pers Soc Psychol, 51(6), 1173–1182.

Bernanke, B., Olekalns, N., Frank, R. H., Antonovics, K. L., & Heffetz, O. (2019). Principles of macroeconomics ((5th ed.). ed.). McGraw-Hill Education (Australia).

Bremus, F., & Fratzscher, M. (2015). Drivers of structural change in cross-border banking since the global financial crisis. J Int Money Finance, 52, 32–59.

Brower, J., & Nath, P. (2018). Antecedents of market orientation: marketing CEOs, CMOs, and top management team marketing experience. Mark Lett, 29(4), 405–419.

Burgess, S. M., & Steenkamp, J.-B. E. M. (2006). Marketing renaissance: how research in emerging markets advances marketing science and practice. Int. J. Res. Mark, 23(4), 337–356.

Datta, H., van Heerde, H. J., Dekimpe, M. G., & Steenkamp, J.-B. E. M. (2022). Cross-national differences in market response: line-length, price, and distribution elasticities in 14 Indo-Pacific Rim economies. J Mark Res, 59(2), 251–270.

Deleersnyder, B., Dekimpe, M. G., Steenkamp, J.-B. E. M., & Leeflang, P. S. H. (2009). The role of national culture in advertising’s sensitivity to business cycles: an investigation across continents. J Mark Res, 46(5), 623–636.

Deshpandé, R., Farley, J. U., & Webster Jr., F. E. (1993). Corporate culture, customer orientation, and innovativeness in Japanese firms: a quadrad analysis. J. Mark., 57(1), 23–37.

Dekimpe, M. G., & Deleersnyder, B. (2017). Business cycle research in marketing: a review and research agenda. J. Acad. Mark. Sci, 1–28.

Federal Reserve Bank. (2019). Federal Reserve Bank of St. Louis’ Financial Crisis Timeline. Federal Reserve Bank.

Gao, H., Zhang, Y., & Mittal, V. (2017). How does local–global identity affect price sensitivity? J. Mark., 81(3), 62–79.

Hayes, A. F. (2017). Introduction to mediation, moderation, and conditional process analysis, second edition: a regression-based approach. Guilford Publications.

Hofstede, G. (1980). Culture’s consequences: international differences in work-related values. Sage Publications.

Isobar. (2019). Creative experience: the evolution of CX. Isobar.

Kalish, S., Mahajan, V., & Muller, E. (1995). Waterfall and sprinkler new-product strategies in competitive global markets. Int. J. Res. Mark., 12(2), 105–119.

Kirca, A. H., Jayachandran, S., & Bearden, W. O. (2005). Market orientation: a meta-analytic review and assessment of its antecedents and impact on performance. J. Mark., 69(2), 24–41.

Kohli, A. K., & Jaworski, B. J. (1990). Market orientation: the construct, research propositions, and managerial implications. J. Mark., 54(2), 1–18.

Kübler, R., Pauwels, K., Yildirim, G., & Fandrich, T. (2018). App popularity: where in the world are consumers most sensitive to price and user ratings? J. Mark., 82(5), 20–44.

Li, & Calantone, R. (1998). The impact of market knowledge competence on new product advantage: conceptualization and empirical examination. J. Mark., 62(4), 13–29.

McKinsey & Company. (2017). Customer experience: new capabilities, new audiences, new opportunities (Vol. 2). McKinsey & Company.

Mintz, O. (2022). The post-pandemic business playbook: customer-centric solutions to help your firm grow. Palgrave Macmillan.

Mintz, O., Currim, I. S., & Deshpandé, R. (2022). National customer orientation: a framework, propositions and agenda for future research. Eur. J. Mark., 56(4), 1014–1041.

Mintz, O., Currim, I. S., Steenkamp, J.-B. E. M., & de Jong, M. (2021). Managerial metric use in marketing decisions across 16 countries: a cultural perspective. J. Int. Bus. Stud., 52(8), 1474–1500.

Morgeson, F. V., Mithas, S., Keiningham, T. L., & Aksoy, L. (2011). An investigation of the cross-national determinants of customer satisfaction. J. Acad. Mark. Sci., 39(2), 198–215.

Morgeson, F. V., Sharma, P. N., & Hult, G. T. M. (2015). Cross-national differences in consumer satisfaction: mobile services in emerging and developed markets. J. Int. Mark., 23(2), 1–24.

Narver, J. C., & Slater, S. F. (1990). The effect of a market orientation on business profitability. J. Mark., 54(4), 20–35.

Palmatier, R. W., Moorman, C., & Lee, J.-Y. (Eds.). (2019). Handbook on customer centricity. Edward Elgar Publishing.

Schumpeter, J. A. (1939). Business cycles (Vol. 1). McGraw-Hill.

Sheth, J. N. (2011). Impact of emerging markets on marketing: rethinking existing perspectives and practices. J. Mark., 75(4), 166–182.

Sheth, J. N., Sisodia, R. S., & Sharma, A. (2000). The antecedents and consequences of customer-centric marketing. J. Acad. Mark. Sci., 28(1), 55.

Smith, W. R. (1956). Product differentiation and market segmentation as alternative marketing strategies. J. Mark., 21(1), 3–8.

Steenkamp, J.-B. E. M., & Geyskens, I. (2006). How country characteristics affect the perceived value of web sites. J. Mark., 70(3), 136–150.

Witte, C. T., Burger, M. J., Ianchovichina, E. I., & Pennings, E. (2017). Dodging bullets: the heterogeneous effect of political violence on greenfield FDI. J. Int. Bus. Stud., 48(7), 862–892.

Wolman, L. (1921). The theory of production. Am Econ Rev, 11(1), 37–56.

World Bank. (2019). The World Bank DataBank. World Bank.

World Economic Forum. (2015). The Global Competitiveness Report 2015–2016. World Economic Forum.

World Economic Forum. (2017). The Global Competitiveness Report 2017–2018. World Economic Forum.

Funding

Open Access funding enabled and organized by CAUL and its Member Institutions.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Supplementary information

ESM 1

(DOCX 183 KB)

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Mintz, O., Currim, I.S. & Deshpandé, R. National customer orientation: an empirical test across 112 countries. Mark Lett 34, 189–204 (2023). https://doi.org/10.1007/s11002-023-09668-5

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11002-023-09668-5