Abstract

The main topic addressed in this paper is the special attributes of the French system as regards both the house price upsurge in the precrisis decade and the resilience of the housing system since 2007. Why was the housing market so buoyant before 2007, and why did it stabilize so rapidly after 2008? Apart from the nature of the credit system, which is of course of great importance—especially with respect to resilience—answering this question leads to questions concerning recent trends in tenure, urban structures, income distribution and housing policies. A number of similarities can be observed with Nordic countries, especially with Sweden, which can explain why those countries were exuberant without generating the kind of fragility observed in Anglo-Saxon, southern or eastern European countries.

Similar content being viewed by others

Notes

In what follows, we shall use buoyancy or buoyant as an equivalent for the housing market of bullish for financial markets, meaning both very active and steadily rising.

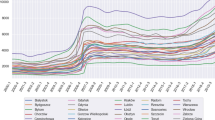

Market exuberance (or buoyancy)—i.e., a long-lasting and unusually strong upswing of prices—must be distinguished from market volatility, which would apply to short violent alternate ascending and descending movements. In this acceptance, volatility relies to a limited group of East European countries: Bulgaria, Estonia, Hungary, Latvia and Romania.

A recent estimate (Jacquot 2012) by the French Ministry of Housing gives an estimation of 330,000–360,000 at the utmost.

In Ile-de-France, the level of construction felt in recent years to less than 40,000 units a year, when the rather undebated estimate of new construction needs is about 70,000.

At the beginning of twentieth century, the first belt of municipalities surrounding Paris inner city was a compound of working-class districts, generally managed by socialist councils. The red belt (ceinture rouge in French) refers to this entire group of municipalities.

See also André (2010) for price-to-rent and price-to-income ratios in a comparative perspective.

The rise in the labor price of housing is still more striking: One square meter of an average existing flat in Paris, which amounted to 350 h of minimal wage in 1984, and 590 in 1990, represented more than 850 h in September 2012.

1.5 % for new built units and 3 % of the existing stock.

The proportion was exactly the opposite in the 1960s and 1970s.

This PTZ—Prêt à taux zéro (zero-interest loan)—replaced the former PAP (Prêt d’accession à la propriété) introduced in 1977, which became more and more costly for the state and risky for low-income households once the deflation process consolidated in the mid-1980s.

Such as section 55 of SRU Act of December 2000, which enforces municipalities of more than 3,500 inhabitants to reach 20 % of social rental units in 2020 (now 25 % under the revision enacted in 2012). A recent report by the Chamber of public accounts (Cour des comptes (2012)) in charge of controlling public expanses and assessing the efficiency of public policies offers a critical assessment of the so-called politique de la ville.

A total of 750 deprived neighborhoods were labelled as ZUS in 1996, on which the politique de la ville has been targeted, especially the Urban Renewal Program (PNRU) of 2004.

Which excludes new supply by social landlords and self-construction (one-half of newly built dwellings).

Which also partly explains the acceleration process after 2001 (see Assous et al. 2008).

Les beaux quartiers is a novel by the French writer Louis Aragon.

ADIL = Agences départementales d’information sur le logement.

Of which a large proportion is directed towards the National Urban Renewal Program (PNRU).

In this respect, the proportion of mortgagors is more important than the proportion of home owners: In Italy, for example, the latter is relatively high, but the former is relatively low.

See also Van der Heijden et al. (2011) for a qualitative institutional analysis of housing market dynamics in Europe.

This livret A is the most popular form of saving deposit. Deposits are guaranteed by the state, and interests paid are exempt from tax. The rate served on it determines the cost of long-run loans (30–50 years) for social landlords. The large volume of those off-market loans (representing 70–75 % of their construction costs) makes it possible for the state, who determines the number of loans allowed each year, to support social housing without disbursing direct subsidies. It also makes the social rental sector rather insensitive both to financial markets and to macroeconomic conditions, and thus countercyclical.

HLM = Habitation à loyer modéré (moderate rent housing).

Which is on the political agenda not only for the Ministry of housing, but for the Treasury as well (see Ministère de l’Economie et des Finances 2012).

References

A.C.P. (Autorité de contrôle prudentiel) (2012). Evolution des risques sur les crédits à l’habitat. Analyses et synthèses, N°5, Février, Paris: Banque de France.

Andre, C. (2010). A bird’s eye view of OECD housing markets. OECD economics department working papers, N°746, Paris: OECD Publishing.

Andrews, D. (2010). Real house prices in OECD countries: the role of demand shocks and structural policy factors. OECD economics department working papers, N°831, Paris: OECD.

Andrews, D., Caldera, A., & Johansson, A. (2011). Housing markets and structural policies in OECD countries. OECD economics department working papers, N°836, Paris: OECD.

Assous, M., Sanchez, A., & Tutin, C. (2008). Stock markets and house prices fluctuations in Europe—Some insights from panel data modeling. ENHR annual conference, Dublin.

Ball, M. (2011). European housing review. Bruxelles: RICS.

Ben Jelloul, M., Collomber, C., Cusset, P.-Y., & Schaff, C. (2011). L’évolution des prix du logement en France sur 25 ans. Note d’analyse, N°221, CAS (Centre d’Analyse Stratégique), Avril.

Boutillier, M., Gabrielli, D., & Monfront, R. (2005). L’endettement immobilier des ménages: comparaisons entre les pays de la zone euro Bulletin de la Banque de France, N°144, Décembre, 33–44.

Caldera-Sanchez, A., & Johansson, A. (2011). The price responsiveness of housing supply in OECD countries. OECD economics department working papers, No. 837, OECD Publishing. http://dx.doi.org/10.1787/5kgk9qhrnn33-enonomics.

Clayton, J., Miller, N., & Peng, L. (2010). Price-volume correlation in the housing market: Causality and co-movements. The Journal of Real Estate Finance and Economics, 40(1), 14–40.

Cour des comptes. (2012). La politique de la ville—Une décennie de réformes. Paris: Rapport thématique.

E.C.B. (2009). Housing Finance in the Euro Area, Occasional paper series, N°101, March.

E.M.F. (European Mortgage Federation) (2011). Hypostats 2010—A review of Europe’s mortgage and housing markets.

Engelhardt, G. V. (1996). Consumption, down payments, and liquidity constraints. Journal of Money, Credit and Banking, 28, 255–271.

Filippi, B., Funès, C., Nabos, H., & Tutin, C. (2007). Marchés du logement et fractures urbaines en Ile-de-France. Recherche, N° 175, PUCA, Paris, Diffusion CERTU.

Filippi, B., & Tutin, C. (2011). Social housing and housing markets from a European perspective. In N. Houard (Ed.), Social housing across Europe (pp. 172–190). Paris: La Documentation Française.

Friggit, J. (2009). Le prix des logements sur longue période, Informations sociales,CNEF, Paris, 2009/5–n° 155, 26–33, http://www.cairn.info/revue-informations-sociales-2009-5-page-26.htm.

Friggit, J. (2011). Quelles perspectives pour le prix des logements après son envolée ? Regards croisés sur l’économie, Paris, La Découverte, 2011/1, N°9, 14–32.

Hort, K. (2000). Prices and turnover in the market for owner-occupied homes. Regional Science and Urban Economics, 30, 99–119.

I.M.F. (International Monetary Fund) (2008). The changing housing cycle and the implications for monetary policy. In World Economic Outlook, Washington. DC.

I.N.S.E.E. (2010). Prix des logements anciens, INSEE Première, N°1297, Mai.

Jacquot, A. (2012). La demande potentielle de logements à l’horizon 2030, Observations et statistiques, Ministère de l’écologie, du développement durable et de l’énergie, N°135, Août.

Kemeny, J. (1995). From public housing to the social market. Rental policy strategies in comparative perspective. London: Routledge.

Ministère de l’économie et des finances (2012). L’inflation immobilière et ses conséquences pour l’économie française. In Rapport économique, social et financier, annexes au Projet de loi de Finances pour 2013, Tome 1, 109–113.

Rothenberg, J., Galster, G., Butler, R., & Pitkin, J. (1991). The maze of urban housing markets: theory, evidence and policy. Chicago: The Chicago University Press.

Tutin, C. (1990). Pourquoi Paris monte-t-il ? Quatre hypothèses sur une déconnexion. Etudes Foncières, Paris : ADEF, N°47.

Tutin, C. (2005). The spatial dimension in housing market fluctuations: the case of French real-estate markets. ENHR Annual conference, Reykjavik, 29 June—3rd July.

Van der Heijden, H., Dol, K., & Oxley, M. (2011). Western European housing systems and the impact of the international financial crisis. Journal of Housing and the Built Environment, 26, 295–313.

Vorms, B. (2009) Les accédants à la propriété bousculés par la crise en Europe et en Amérique du Nord—Diversité des situations, convergence des remèdes. Habitat Actualité, Paris: ANIL, Avril.

Vorms, B. (2010). Les politiques d’aide à l’accession à la propriété à l’épreuve de la crise. Informations sociales, 155, 120–130.

Vorms, B. (2012). The effectiveness of the French credit system faced with the challenge of budgetary restrictions. Housing Finance International, Summer, pp 20–24.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Tutin, C., Vorms, B. French housing markets after the subprime crisis: from exuberance to resilience. J Hous and the Built Environ 29, 277–298 (2014). https://doi.org/10.1007/s10901-013-9388-8

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10901-013-9388-8