Abstract

This paper presents new models which seek to optimize the first and second moments of asset returns without estimating expected returns. Motivated by the stability of optimal solutions computed by optimizing only the second moment and applying the robust optimization methodology which allows to incorporate the uncertainty in the optimization model itself, we extend and combine existing methodologies in order to define a method for computing relative-robust and absolute-robust minimum variance portfolios. For the relative robust strategy, where the maximum regret is minimized, regret is defined as the increase in the investment risk resulting from investing in a given portfolio instead of choosing the optimal portfolio of the realized scenario. The absolute robust strategy which minimizes the maximum risk was applied assuming the worst-case scenario over the whole uncertainty set. Across alternate time windows, results provide new evidence that the proposed robust minimum variance portfolios outperform non-robust portfolios. Whether portfolio measurement is based on return, risk, regret or modified Sharpe ratio, results suggest that the robust methodologies are able to optimize the first and second moments without the need to estimate expected returns.

Similar content being viewed by others

Notes

In the in-sample analysis the overall in-sample period was used in order to compute estimators for the models.

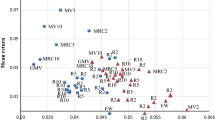

A portfolio is considered a dominant solution when it presents, simultaneously, higher return and lower risk.

References

Markowitz, H.: Portfolio Selection: Efficient Diversification of Investments. Wiley, New York (1959)

Markowitz, H.: Portfolio selection. J. Finance 7(1), 77–91 (1952)

Best, M.J., Grauer, R.R.: On the sensitivity of mean–variance-efficient portfolios to changes in asset means: some analytical and computational results. Rev. Financ. Stud. 4(2), 315 (1991)

Best, M.J., Grauer, R.R.: Sensitivity analysis for mean–variance portfolio problems. Manage. Sci. 37(8), 980–989 (1991)

Chopra, V.K., Ziemba, W.T.: The effect of errors in means, variances, and covariances on optimal portfolio choice. J. Portf. Manag. 19(2), 6–11 (1993)

Jagannathan, R., Ma, T.: Risk reduction in large portfolios: why imposing the wrong constraints helps. J. Finance 58(4), 1651–1684 (2003)

Chan, L.K.C., Karceski, J., Lakonishok, J.: On portfolio optimization: forecasting covariances and choosing the risk model. Rev. Financ. Stud. 12(5), 937–974 (1999)

DeMiguel, V., Garlappi, L., Uppal, R.: Optimal versus naive diversification: how inefficient is the 1/N portfolio strategy? Rev. Financ. Stud. 22(5), 1915–1953 (2009)

Supandi, E.D., Rosadi, D.: An empirical comparison between robust estimation and robust optimization to mean–variance portfolio. J. Mod. Appl. Stat. Methods 16(1), 32 (2017)

Fabozzi, F.J., Kolm, P.N., Pachamanova, D., Focardi, S.M.: Robust Portfolio Optimization and Management. Wiley, Hoboken (2007)

Steuer, R.E., Qi, Y., Hirschberger, M.: Portfolio selection in the presence of multiple criteria. In: Zopounidis, C., Doumpos, M., Pardalos, P.M. (eds.) Handbook of Financial Engineering, pp. 3–24. Springer, Boston, MA (2008)

Kolm, P.N., Tütüncü, R., Fabozzi, F.J.: 60 years of portfolio optimization: practical challenges and current trends. Eur. J. Oper. Res. 234(2), 356–371 (2014)

Bana e Costa, C., Soares, J.: Multicriteria approaches for portfolio selection: an overview. Rev. Financ. Mark. 4(1), 19–26 (2001)

Zopounidis, C., Doumpos, M.: Multi-criteria decision aid in financial decision making: methodologies and literature review. J. Multi Criteria Decis. Anal. 11(4–5), 167–186 (2002)

Zopounidis, C., Galariotis, E., Doumpos, M., Sarri, S., Andriosopoulos, K.: Multiple criteria decision aiding for finance: an updated bibliographic survey. Eur. J. Oper. Res. 247(2), 339–348 (2015)

Chang, T.-J., Meade, N., Beasley, J.E., Sharaiha, Y.M.: Heuristics for cardinality constrained portfolio optimisation. Comput. Oper. Res. 27(13), 1271–1302 (2000)

Golmakani, H.R., Fazel, M.: Constrained portfolio selection using particle swarm optimization. Expert Syst. Appl. 38(7), 8327–8335 (2011)

Soleimani, H., Golmakani, H.R., Salimi, M.H.: Markowitz-based portfolio selection with minimum transaction lots, cardinality constraints and regarding sector capitalization using genetic algorithm. Expert Syst. Appl. 36(3), 5058–5063 (2009)

Spronk, J., Hallerbach, W.: Financial modelling: where to go? With an illustration for portfolio management. Eur. J. Oper. Res. 99(1), 113–125 (1997)

Yu, L., Wang, S., Lai, K.K.: Neural network-based mean–variance–skewness model for portfolio selection. Comput. Oper. Res. 35(1), 34–46 (2008)

Ehrgott, M., Klamroth, K., Schwehm, C.: An MCDM approach to portfolio optimization. Eur. J. Oper. Res. 155(3), 752–770 (2004)

Eichfelder, G.: Adaptive Scalarization Methods in Multiobjective Optimization. Springer, Berlin (2008)

Azmi, R., Tamiz, M.: A review of goal programming for portfolio selection. In: Jones, D., Tamiz, M., Ries, J. (eds.) New Developments in Multiple Objective and Goal Programming, pp. 15–33. Springer, Berlin (2010)

Chunhachinda, P., Dandapani, K., Hamid, S., Prakash, A.J.: Portfolio selection and skewness: evidence from international stock markets. J. Bank. Finance 21(2), 143–167 (1997)

Aouni, B., Colapinto, C., La Torre, D.: Financial portfolio management through the goal programming model: current state-of-the-art. Eur. J. Oper. Res. 234(2), 536–545 (2014)

Steuer, R.E., Na, P.: Multiple criteria decision making combined with finance: a categorized bibliographic study. Eur. J. Oper. Res. 150(3), 496–515 (2003)

Hauser, R., Krishnamurthy, V., Tütüncü, R.: Relative robust portfolio optimization. arXiv preprint arXiv:1305.0144 (2013)

Gabrel, V., Murat, C., Thiele, A.: Recent advances in robust optimization: an overview. Eur. J. Oper. Res. 235(3), 471–483 (2014)

El Ghaoui, L., Lebret, H.: Robust solutions to least-squares problems with uncertain data. SIAM J. Matrix Anal. Appl. 18(4), 1035–1064 (1997)

Ben-Tal, A., Nemirovski, A.: Robust convex optimization. Math. Oper. Res. 23(4), 769–805 (1998)

Goldfarb, D., Iyengar, G.: Robust portfolio selection problems. Math. Oper. Res. 28(1), 1–38 (2003)

Halldórsson, B.V., Tütüncü, R.H.: An interior-point method for a class of saddle-point problems. J. Optim. Theory Appl. 116(3), 559–590 (2003)

Natarajan, K., Pachamanova, D., Sim, M.: Constructing risk measures from uncertainty sets. Oper. Res. 57(5), 1129–1141 (2009)

Bertsimas, D., Brown, D.B.: Constructing uncertainty sets for robust linear optimization. Oper. Res. 57(6), 1483–1495 (2009)

Lu, Z.: A new cone programming approach for robust portfolio selection. Optim. Methods Softw. 26(1), 89–104 (2006)

Lu, Z.: A computational study on robust portfolio selection based on a joint ellipsoidal uncertainty set. Math. Program. 126(1), 193–201 (2011)

Roy, B.: Robustness in operational research and decision aiding: a multi-faceted issue. Eur. J. Oper. Res. 200(3), 629–638 (2010)

Gregory, C., Darby-Dowman, K., Mitra, G.: Robust optimization and portfolio selection: the cost of robustness. Eur. J. Oper. Res. 212(2), 417–428 (2011)

Kaläı, R., Lamboray, C., Vanderpooten, D.: Lexicographic α-robustness: an alternative to min–max criteria. Eur. J. Oper. Res. 220(3), 722–728 (2012)

Kim, J.H., Kim, W.C., Fabozzi, F.J.: Composition of robust equity portfolios. Finance Res. Lett. 10(2), 72–81 (2013)

Kim, W.C., Kim, J.H., Ahn, S.H., Fabozzi, F.J.: What do robust equity portfolio models really do? Ann. Oper. Res. 205(1), 141–168 (2013)

Kim, W.C., Kim, J.H., Fabozzi, F.J.: Deciphering robust portfolios. J. Bank. Finance 45, 1–8 (2014)

Kouvelis, P., Yu, G. (eds.): Robust discrete optimization: past successes and future challenges. In: Robust Discrete Optimization and Its Applications, pp. 333–356. Springer, Boston, MA (1997)

Cornuejols, G., Tütüncü, R.: Optimization Methods in Finance. Cambridge University Press, Cambridge (2006)

Hasuike, T., Katagiri, H.: Robust-based interactive portfolio selection problems with an uncertainty set of returns. Fuzzy Optim. Decis. Making 12(3), 263–288 (2013)

Fliege, J., Werner, R.: Robust multiobjective optimization & applications in portfolio optimization. Eur. J. Oper. Res. 234(2), 422–433 (2014)

Xidonas, P., Mavrotas, G., Hassapis, C., Zopounidis, C.: Robust multiobjective portfolio optimization: a minimax regret approach. Eur. J. Oper. Res. 262(1), 299–305 (2017)

Kalayci, C.B., Ertenlice, O., Akyer, H., Aygoren, H.: A review on the current applications of genetic algorithms in mean–variance portfolio optimization. Pamukkale Univers. J. Eng. Sci. 23(4), 470–476 (2017)

Streichert, F., Ulmer, H., Zell, A.: Evolutionary algorithms and the cardinality constrained portfolio optimization problem. In: Operations Research Proceedings 2003. Operations Research Proceedings (GOR (Gesellschaft für Operations Research e.V.)), vol. 2003, pp. 253–260 (2004)

Chang, T.-J., Yang, S.-C., Chang, K.-J.: Portfolio optimization problems in different risk measures using genetic algorithm. Expert Syst. Appl. 36(7), 10529–10537 (2009)

Zhu, H., Wang, Y., Wang, K., Chen, Y.: Particle swarm optimization (PSO) for the constrained portfolio optimization problem. Expert Syst. Appl. 38(8), 10161–10169 (2011)

Blackburn, D.W., Cakici, N.: Overreaction and the cross-section of returns: international evidence. J. Empir. Finance 42, 1–14 (2017)

Jegadeesh, N., Titman, S.: Returns to buying winners and selling losers: implications for stock market efficiency. J. Finance 48(1), 65–91 (1993)

Israelsen, C.L.: A refinement to the Sharpe ratio and information ratio. J. Asset Manag. 5(6), 423–427 (2005)

Chow, T.-M., Hsu, J.C., Kuo, L.-L., Li, F.: A study of low-volatility portfolio construction methods. J. Portf. Manag. 40(4), 89–105 (2014)

Maillet, B., Tokpavi, S., Vaucher, B.: Global minimum variance portfolio optimisation under some model risk: a robust regression-based approach. Eur. J. Oper. Res. 244(1), 289–299 (2015)

Duan, L., Stahlecker, P.: A portfolio selection model using fuzzy returns. Fuzzy Optim. Decis. Making 10(2), 167–191 (2011)

Kato, K., Sakawa, M.: An interactive fuzzy satisficing method based on variance minimization under expectation constraints for multiobjective stochastic linear programming problems. Soft. Comput. 15(1), 131–138 (2011)

Acknowledgements

This study has been funded by national funds, through FCT, Portuguese Science Foundation, under Project UID/Multi/00308/2019.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Caçador, S., Dias, J.M. & Godinho, P. Global minimum variance portfolios under uncertainty: a robust optimization approach. J Glob Optim 76, 267–293 (2020). https://doi.org/10.1007/s10898-019-00859-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10898-019-00859-x