Abstract

Despite the significant attention that financial capability has received in the last 20 years, many of its aspects are poorly understood, and the term itself is ambiguously defined. Consequently, different measures of financial capability are used in empirical research creating a tendency to let the data dictate the conceptualization of the financial capability itself. This creates concerns about the reliability of the general findings for countries in Eastern Europe such as Poland. Therefore, the following study is carried out to address these limitations and contribute to the advancement of the literature on financial capability, first, by extending the mainstream of the theoretical work on financial capability with the conceptual proposition framed within Sen’s Capability Approach; second, by proposing the measurement model of financial capability; and third, by using data from the Polish household panel study, Social Diagnosis (SD), to identify factors which predict a positive change in consumer’s financial capability over time. Across these three aims, we found that higher income was a key predictor and substantially improved financial capability in Poland. We also showed the strong and positive link between financial capability and all included psychological variables. Our findings also highlighted the differential impact of demographic variables on financial capability. The findings of this study yield implications for scholars who would like to analyze financial capability in transition or developing countries, but are constrained by limited financial resources to create their own database or have no access to national financial capability studies.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The concept of financial capability is a relatively new idea that has developed over the last two decades within consumer finance (Atkinson et al., 2007; Johnson & Sherraden, 2007; Kempson et al., 2005; Sherraden, 2013; Taylor, 2011; Xiao et al., 2014), social work (Birkenmaier et al., 2016; Caplan et al., 2018; Huang et al., 2021; Sherraden & Ansong, 2016) and family studies (Despard et al., 2020; Nam et al., 2015; Serido et al., 2013; Shim et al., 2013). Financial capability describes many, sometimes very different and interrelated concepts, including financial literacy, financial knowledge, financial skills, financial self-efficacy, financial behavior, financial capacity, financial outcomes, financial access, financial resilience, and financial satisfaction. However, as previously reported (Birkenmaier et al., 2022; Kempson & Poppe, 2018, Xiao & Huang, 2021) the empirical research on financial capability has evolved from a sole focus on financial income, financial literacy, and/or financial behavior through financial access to a fairly recent concept of financial well-being (where financial access is a facilitator of household financial well-being). Previous studies have empirically shown that financial capability mediates between different internal and external predictors and financial well-being (Dew & Xiao, 2011; Prawitz & Cohart, 2016; Serido et al., 2013; Xiao et al., 2014). Consequently, financial capability has become a high priority public policy objective in a ‘financially liberated’ society and serves both as input to and as an outcome in establishing national strategies for financial education around the world in an attempt to improve financial well-being (Fu, 2020).

Notwithstanding, one prominent attempt to conceptualize financial capability has been proposed by Sherraden and colleagues (Johnson & Sherraden, 2007; Sherraden, 2013; Sherraden et al., 2022). The researchers attempted to integrate financial access (opportunity to act) with financial literacy (ability to act) and explained how this joint, interrelated impact decreases money management stress and promotes financial security, consequently increasing the likelihood of financial well-being. Using this conceptualization, Birkenmaier and Fu (2020) emphasized the role of financial access as an external condition which creates or sustains the capability to save, borrow and manage money, create emergency funds, make payments or manage financial risk. In the same vein, Birkenmaier et al., (2022, p. 8) indicated that any definition that excludes financial access changes the conceptual understanding of financial capability and may result in a completely different concept altogether. On the other hand, Prabhakar (2019) proposed that financial capability should support financial resilience through financial access. Other researchers used that line of reasoning and included external factors such as financial access in their theoretical and empirical findings. Overall, this definition has been so widely accepted that it has provided the starting point for the recent systemic review on financial capability (Birkenmaier et al., 2022).

Yet, consistent with current reviews (Birkenmaier et al., 2022; Xiao & Huang, 2021), many aspects of financial capability are still poorly understood and measures of financial capability used in empirical research have revealed that financial capability had been proxied insufficiently. Thus, different classifications used in the literature (Atkinson et al., 2007; Banerjee et al., 2017; Chowa & Despard, 2014; Despard & Chowa, 2014; Huang et al., 2015; Johnson & Sherraden, 2007; Kempson et al., 2005; Kempson & Poppe, 2018; Salignac et al., 2019; Serido et al., 2013; Sherraden, 2013; Taylor, 2011; von Stumm et al., 2013; Xiao et al., 2014; Xiao & O’Neill, 2016) have resulted in entirely different proxies used to measure financial capability. It poses a challenge in testing conceptual frameworks. This argumentation is consistent with the study by Birkenmaier et al. (2022), who reported that of the 34 included studies 22 of them measured financial capability constructs in 12 different ways, which has shown little consensus among researchers. Moreover, this mismatch might be strengthened due to the regional concentration of studies. Specifically, the preponderance of research on financial capability has been conducted in the United States (for recent reviews, see Miller et al., 2015; Xiao & Huang, 2021; Birkenmaier et al., 2022).

Accordingly, the purpose of this study is threefold. First, we complement the financial capability literature by locating financial capability within Sen’s Capability Approach (CA). Financial capability research over the past twenty years largely ignored Sen’s interpretation of capability and applied only Nussbaum’s taxonomy of capabilities (Birkenmaier et al., 2022; Huang et al., 2013, 2015; Johnson & Sherraden, 2007; Sherraden, 2013). Thus, we extend the existing landscape of financial capability meaning and offer the synergism of consumer economics and social science disciplines to better understand financial capability. This is consistent with Delgadillo (2014) who claimed that “the conceptual synergy in this aspect of the family and consumer sciences discipline presents an opportunity to advance empirical and theoretical knowledge” (p. 25). Second, based on the framework suggested in classic works by Sen (1985, 1997, 1999) and further extension and reexamination proposed by Robeyns (2005, 2017, 2018) we propose the measurement model in which the assessment of capabilities is proceeded primarily based on observing a person’s financial behavior and outcomes (functionings). In line with these rationales, we use the method proposed by Taylor (2011), who utilized the mix of financial behavior and outcome as a proxy of financial capability. Several studies also applied this (e.g., Cui et al., 2019, in China; Kempson & Evans, 2021, in New Zealand; Taylor et al., 2011, in the UK; Xiao et al., 2014, 2015, in the US). Third, our study seeks to build a measurement model of financial capability on existing variables, available from eight waves of Polish household study, Social Diagnosis (SD). Similar to the British Household Panel Survey (BHPS) which was used by Pudney (2010), Taylor (2011), Taylor et al. (2011), SD data offers retrospective questions asking the respondents about their financial situation, behavior, and outcomes. To the best of our knowledge, our study is the first attempt to bring empirical evidence on consumers’ financial capability and its predictors in Eastern Europe using such a long time. What is more, no previous attempts which used SD analyzed financial capability and used data from all eight waves (e.g., Białowolski & Węziak-Białowolska, 2017; Białowolski et al., 2019; Węziak-Białowolska & Białowolski, 2016).

Literature Review

Conceptual Framework of Financial Capability

From a theoretical perspective, defining financial capability is a highly complicated issue, and therefore the term financial capability itself may have various definitions. This was emphasized by Huang et al. (2015) who stated that there is no general consensus with regard to its definition” (p. 240).

The difficulty with defining financial capability has been of both contextual and empirical character, similarly as in the case of defining the term capability. Consistent with previous research by Dubois and Rousseau (2008, p. 422) and Robeyns (2017, p. 106), the difficulty in defining the term capability underlines its linguistic complexity and the fact that many languages do not have its exact equivalent. Based on the dictionary definitions, financial capability has been defined elusively. This fact was underlined by Remund (2010) who argued that “there are many different names to describe the concept of financial capability, including empowerment, responsibilization, financial knowledge, financial skills and financial literacy” (p. 283). When, on the other hand, we take into account the meaning of the term capability derived from Sen’s Capability Approach (CA) or Nussbaum’s taxonomy, the emphasis should be shifted towards financial opportunities, freedom of choice, and potential financial behavior. Researchers adopting CA has asked what individuals can do and be (their capabilities) and what they can achieve in terms of being and doing (their functionings) (Alkire, 2002; Nussbaum, 2011; Robeyns, 2005, 2018; Sen, 1985, 1999).

Nevertheless, theoretical research on financial capability has been mostly examined in three dimensions (see Table 1). Behavioral studies (e.g., De Meza et al., 2008; Hoelzl & Kapteyn, 2011) have focused on finding explanation to the question of how individuals make their financial decisions (by analyzing the process of financial decision making and the cognitive, motivational, and emotional characteristics of consumers). We define this approach as the Cognitive Oriented Approach (COA) (see Table 1). It mainly relies on a definition proposed by Kempson et al. (2005), which has later evolved from rewarding only cognitive predispositions (such as financial knowledge and skills) to a much broader perspective, additionally encompassing psychological attributes (including attitudes, habits, motivation, confidence, and self-efficacy or self-beliefs) that may shape financial behavior (e.g., Reyers, 2019; Serido et al., 2013; Sherraden & Ansong, 2016; Shim et al., 2013). COA has been adopted by many other researchers (e.g., Luukkanen & Uusitalo, 2019; Sorgente et al., 2020; Xiao & O’Neill, 2018). In this vein, Hoelzl and Kapteyn (2011) pointed out that “the actual behavior of consumers is the outcome of its prerequisites such as the knowledge, skills, confidence, and attitude to perform desirable financial behaviors” (p. 543). Furthermore, they showed that the term financial capability is much broader than the term financial literacy because it additionally incorporated psychological components. Likewise, Huston (2010) indirectly conceptualized financial capability as “understanding (personal finance knowledge) and its use (personal finance application)” (p. 306). However, Xiao and Huang (2021) suggested that this conceptualization of financial capability should rather be defined as broad financial literacy. Likewise, Shim et al. (2013) viewed financial capabilities as “a construct encompassing cognitive (e.g., financial knowledge), psychological (e.g., self-efficacy, controllability, attitudes) and behavioral aspects (e.g., budgeting, saving)” (p. 133). Their proposition of financial capability was later broadened by the concept of financial self-efficacy and financial self-identity, becoming an emerging line of research in behavioral and family studies (see, e.g., Serido et al., 2013; Sorgente et al., 2020).

However, consistent with the results reported in consumer research (Taylor, 2011; Taylor et al., 2011) financial capability has not been primarily linked to cognitive, psychological, and behavioral factors but foremost to financial behavior and its outcomes. We define this approach as the Behavior-Oriented Approach (BOA) (see Table 1). In Taylor’s (2011) words “financial capability is people’s ability to manage and take control of their finances” (p. 298). This study provided valuable insights applied in a significant number of research studies (see, e.g., Cui et al., 2019; Kempson & Evans, 2021; Potocki & Cierpiał-Wolan, 2019; Xiao et al., 2014, 2015; Xiao & O’Neill, 2016). Interestingly, both COA and BOA overlooked what Reyers (2019) rightly emphasized and explained as “account for external condition” (p. 337). Consequently, these external conditions were defined by Fu (2020) as institutionalist to financial well-being, which “seeks to better understand the interdependencies between financial literacy, financial inclusion, and contextual circumstances on outcomes of interest” (p. 3). Similar results were reported by Huang et al. (2015) who argued that “the financial capability concept captures important elements that positively contribute to an individual’s financial well-being” (p. 240). Likewise, Sun et al. (2022) emphasized that the role of external conditions may be more consequential than individual abilities.

The interaction between financial literacy and financial access has become a major explanatory construct of the third approach that we define as the Opportunity-Oriented Approach (OOA) (see Table 1). The vast majority of the OOA work has been embedded in three crucial studies: Johnson and Sherraden (2007), Sherraden (2013), Sherraden et al. (2022). Building on their research, other researchers have started to use the OOA in financial capability research (e.g., Banerjee et al., 2017; Despard et al., 2020; Fu, 2020; Huang et al., 2015; Huang et al., 2018; Kempson & Poppe, 2018; Sherraden & Ansong, 2016; Sherraden & Grinstein-Weiss, 2015; Sun et al., 2022) have started to use the OOA in the financial capability research.

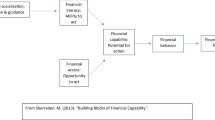

Needless to say, the definition constructed by Johnson and Sherraden (2007) and Sherraden (2013) has also become a critical contribution to the Social Work and Asset Building Theory. These studies were based on Nussbaum’s (2011, p. 23, 24) pioneering typology of capabilities and their division into basic, internal, and combined capabilities. Johnson and Sherraden (2007) explained their choice to adopt Nussbaum’s approach with the following words: “Participation in economic life should maximize life chances and enable people to lead fulfilling lives; this requires knowledge and skills, the ability to act on that knowledge and the opportunity to act” (p. 122). In a similar vein, Sherraden (2013) pointed out that “financial capability includes both the ability to act (knowledge, skills, confidence, and motivation) and the opportunity to act (through access to quality financial products and services)” (p. 43). Likewise, Huang et al. (2013) used CA to indicate that “financial capability does not reside solely within the individual; it captures the relationship between people’s internal ability and their external conditions (…)” (p. 3). Both approaches are in line with Nussbaum’s (2011) insights on capabilities in general: “Capabilities (…) are not just abilities residing inside a person but also the freedoms or opportunities created by a combination of personal abilities and the political, social, and economic environment” (p. 20). However, as emphasized by Sun et al. (2022): “The construct of access refers to institutional mechanisms that make financial services or programs available to everyone” (p. 9).

The combination of both internal and external factors has been an important element of Sen’s CA and was extensively discussed in his works (see, i.e., Sen, 1997, p. 195; Sen, 1999, pp. 88, 89). However, these factors were not defined as capability, but as conversion factors or structural constraints. Conversion factors determine the degree to which a person can transform resources into functionings. Sen (1999) indicated four such groups of conversion factors, including personal conversion factors (i.e., metabolism, physical condition, literacy skills), social conversion factors (i.e., variations in social climate, public policies, social capital), differences in relational perspectives (i.e., patterns in behavior, social norms, practices) and environmental conversion factors (i.e., physical or build environment which person lives) (pp. 88, 89). Therefore, as rightly explained by De Rosa (2018), “in order to transform capabilities into functionings or potential functionings into real achievements, the concept of conversion factors needs to be examined” (p. 128). Likewise, Xiao and Huang (2021) stated that “financial capability (…) alone cannot improve financial well-being without interactions with environmental factors such as financial services and public policies” (p. 2). What is more, in consumer finance and family studies conversion factors were part of background characteristics or/and interventions influencing financial capability (see Xiao & Huang, 2021, Fig. 3) or economic structures and institutions in society, such as the education system and the economy (including socialization, education, and guidance) (see Birkenmaier et al., 2022, Fig. 1).

However, even with these constraints, there has been a growing willingness of researchers to adopt Johnson and Sherraden’s (2007) and Sherraden’s (2013) definition of financial capability. Especially worrying might be great emphasis placed on both construct’s ability to act and opportunity to act in the proposed definition of financial capability. In our opinion, the reason for that may be a limited application of CA. We argue that Nussbaum’s (2011) classification of capabilities, especially internal capabilities, might be particularly misleading for researchers working on the conceptual framework of financial capability. Nussbaum (2011) defined it with the following words: “they are trained or developed traits and abilities, developed, in most cases, in interaction with the social, economic, familial, and political environment” (p. 21). Nussbaum’s definition and classification of capabilities vary considerably from the one by Sen. Sen (1997, pp. 195, 198) and later Robeyns (2005, pp. 74, 75; 2017, pp. 45, 46) argued that capabilities are not internal skills (these are, in fact, individual conversion factors) but rather the opportunity (the notion of freedom) that results from the access to valuable options and freedom of choice. Interestingly, Nussbaum (2011, p. 23) indicated in the same publication that the above-mentioned division may be a little vague, because the classification itself is not clear, and the distinction between internal and combined capabilities is a useful heuristic. Robeyns (2017, p. 93) rightly echoed her views by stating that it would be much clearer to define internal capabilities as “internal characteristics or skills, talents, character traits and abilities” and defines them as individual conversion factors, characteristics that influence financial capability. This is consistent with previous arguments by Qizilbash (2008) who claimed that “Nussbaum’s capabilities approach is a particular application of Sen’s original contribution” (p. 38). Therefore, Alkire (2002, p. 32) and Robeyns (2017, p. 45) suggested that considering the origins of Nussbaum and Sen’s views, researchers adopting CA to conceptualize the capability in social sciences should be more inclined to use Sen’s terminology. The same criticism can be expressed with respect to the role of financial access in Sherraden’s definition (Johnson & Sherraden, 2007; Sherraden, 2013; Sherraden et al., 2022). We agree with the argument that structural and social conversion factors influence financial capability and financial choices per se. In his groundwork on CA, Sen (1985) mentioned that capability “depends on the variety of factors—personal and social” (p. 17). It is quite obvious that to get a full picture of a financial situation, one needs to analyze various factors, not only the individual ones. We must answer the questions of whether individuals can be financially secure and protected against financial shocks, and if they have the appropriate means and resources (i.e., level of income, access to credit, contingence savings to cope with emergencies, access to responsible advisors, basic knowledge of financial terms). Our argument is in line with Robeyns’ (2017, p. 105) who stated that the character of options and access to options matter. Yet, Johnson and Sherraden’s (2007) and Sherraden’s (2013) financial capability definition resembled too much of social conversion factors. In order to develop financial capability, consumers must have the appropriate access to financial options and an understanding of financial products, services, and concepts. However, Robeyns (2017) in the case of environmental studies, rejected the approach in which the environment (in our analyzed case—opportunity to act) is treated as a crucial capability (in her words, meta-capability). Thus, access to financial institutions is a key component of social conversion factors but is not an integral part of the financial capability definition.

Therefore, in our opinion, the adoption of CA, particularly in a way as proposed by Sen (1985, 1997, 1999) and reexamined by Robeyns (2017), has allowed us to define financial capability in a far clearer way, and better explain its structure and properties, clearing up major misunderstandings. Moreover, reinforcing the previous argumentation by Robeyns (2017, p. 12, 13) and using the Sen CA as a general framework for financial capability, we have found a unique compromise between closely related components, financial abilities as part of individual conversion factors, behavioral studies on financial choice as part of the constrained choice, financial behavior as achievable or achieved functionings, and financial access as social conversion factors, all in Sen’s terminology (see Nussbaum, 2011, pp. 21–24; Robeyns, 2017, pp. 80–85; Sen, 1985, pp. 7–10; Sen, 1997, pp. 199–203). Our reasoning is similar to the one proposed recently by Birkenmaier et al. (2022), who defined financial behavior as a “degree to which consumers exhibit strong financial management behaviors and/or the potential or capacity consumers have for exhibiting effective financial management behaviors” (p. 1) and Financial Industry Regulatory Authority (FINRA) (2009), which defined financial capability as “multiple aspects of behaviors” related to how individuals manage resources and make financial decisions” (p. 9). Hence, using Sen’s argument (1987, 1997), financial capability is a real financial opportunity (notions of freedom) open to individuals (their being and doing), which helps them do what they value and be the kind of people they want to be. Specifically, being can be defined as leading a financially secure life without financial worries, anxiety, and uncertainties, and doings are, in fact, valuable, potential, achievable financial functionings (taking low rate credit, saving for retirement, cumulating contingency savings, using banking services), which help to secure one’s financial needs and achieve financial prosperity (i.e., live a financially secure life).

Operationalization of Financial Capability

The concept of financial capability has often been used both in theoretical papers and, even more frequently, in empirical investigation (Birkenmaier et al., 2022). However, as summarized by Taylor (2011) “its operationalization is still highly challenging” (p. 298). This constraint refers not only to financial capability but also to capability in general. Similarly, as stated by Martinetti (2000, p. 208), in the CA the richness of theoretical argumentation has not been easily translated into empirical strategy. Despite this challenge, as reviewed by Robeyns (2017) “the range of fields in which the capability approach has been applied and developed has expanded dramatically and now includes global public health, development ethics, environmental protection, and ecological sustainability, education, technological design, welfare state policy, and many, many more” (p. 9). It is quite surprising to see limited attempts in consumer finance and family studies.

Due to these limitations, several consumer finance studies have used different variables (mainly a wide range of indicators) to measure financial capability. In line with these findings, three trends in measuring financial capability are worth mentioning. The first and still the most influential empirical research on financial capability was conducted by Atkinson et al. (2007) and then followed by Arrowsmith and Pignal (2010), O’Donnell and Keeney (2009), and Fessler et al. (2007) for Canada, Ireland, Austria respectively. They used a particular group of behaviors with the method of explanatory factor analysis. Most of these empirical studies used data derived from specialist surveys conducted as a part of national initiatives to measure financial capability. The first such initiative was developed and commissioned by the Financial Services Authority (FSA) in Britain. Building on that research, Atkinson et al. (2007) applied explanatory factor analysis to identify five domains of the financial capability, which included managing money: making ends meet, i.e. having little problems dealing with financial obligations; managing money: keeping track, i.e., having an overview of expenses; planning, i.e., being future-oriented; choosing products, i.e., deciding reasonably in financial matters; and staying informed. Similar results were reported by Arrowsmith and Pignal (2010) for the Canadian Financial Capability dataset. Second, a broader mix of different variables has been applied to measure financial capability. In this line of research, financial capability has been represented by a set of comprehensive measures. Consistent with this trend, Xiao et al. (2014) used three types of financial capability measures: self-perceived financial capability, financial literacy, and financial behavior. Concerning previous research, Xiao and O’Neill (2016, 2018) further expanded the concept of financial capability to an even more comprehensive measure than previous research. In their approach, the financial capability measure consisted of five variables, including objective financial literacy, subjective financial literacy, desirable financial behavior, and perceived financial capability (a sum of the Z scores of all five variables). More recently, this approach was tested and revised by Potocki and Cierpiał-Wolan (2019) who added the financial access variables. This approach is consistent with studies by Nam et al., 2015) and Huang et al. (2015) who emphasized the role of financial access as essential to personal financial management and more broadly to financial capability. Third, there has been a growing trend in financial capability research to use more extensively the methods used to operationalize the CA by applying Nussbaum’s taxonomy. Consistent with studies by Huang et al. (2013), financial capability has been difficult to measure because it has incorporated both individual and institutional features, which were barely measured at the same time. Furthermore, as underlined by Banerjee et al. (2017) “there is no conclusive evidence whether knowledge alone, opportunities alone or their combination expands financial capability, although a combination of education and opportunities appears to expand the financial capability of some people” (p. 180).

However, by introducing Sen’s CA as the basis of conceptualization of financial capability, most empirical applications of CA may use financial behavior or outcome (or in Sen’s own words achievable or achieved functionings) as a proxy for financial capability. This proposition is extensively debated by Robeyns (2017), who stated that “an analysis of functionings is used as a proxy for an analysis of the capability set” (p. 112). Moreover, this line of reasoning was initiated and reinforced by Sen (1997, 1999) and deepened by Comim et al. (2008). In particular, Sen (1999) emphasized that “the assessment of capabilities has to proceed primarily based on observing a person’s actual functioning. (…). There is a jump here (from capabilities to functionings), but it needs not be a big jump (…)” (p. 131). Similarly, Robeyns (2017) argued that “what is relevant is not only which opportunities are open to us individually, hence in a piecemeal way, but rather which combinations or sets of potential functionings are open to us” (p. 52). Birkenmaier et al. (2022) proposed financial functionings as a proxy to financial opportunity or potential to act, where certain financial functionings and their level (i.e. developing saving habits, saving for retirement, limiting overdeebtiness, or promoting spending prudence) should be promoted or protected (compare with Robeyns, 2017, p. 108). This line of reasoning has also been consistent with CA studies including Martinetti (2000) and De Rosa (2018) who used different indicators of functioning as a proxy of people’s capabilities. Given the underlying logic of Sen’s CA that financial functionings are the active realization of capabilities, our empirical application explores achieved financial functionings as a proxy to financial opportunities using general social survey data. This approach is consistent with Anand (2005), Anand et al. (2009) for CA sensu largo and Taylor (2011), Taylor et al. (2011) for financial capability sensu stricto who used general social panel data (the British Household Panel Survey (BHPS), covering the survey years 1991–2006. In particular, Taylor (2011) proposed a proxy to financial capability as a mix of desirable financial behavior to manage finance and the outcomes. The following range of variables expressed the way people manage their money including reflections of people’s perceptions of their financial situation, over-indebtedness, the ability to plan for the future, and the ability to manage their money. Taylor’s (2011) method has been applied by Xiao et al., (2014, 2015) and more recently has been used to evaluate financial capability based on Chinese (Cui et al., 2019) and New Zealand (Kempson & Evans, 2021) data.

Rationale for this Study and Research Hypotheses

Given that the general understanding of a financial capability concept is directly related to its operational definition, our study investigates financial capability framework using nationally-representative data set by estimating multivariate statistical models that control for potentially confounding factors. Moreover, building on previous empirical studies we aim to examine the dynamics related to the proposed measure of financial capability and the three groups of psychological, demographic, and economic variables.

In particular, the following hypotheses were tested.

H1 There should be some underlying factor (financial capability) that is better captured by combination of variables of human behaviors relevant to basic money management (BMM) than by any of the specific items of information.

H2 The economic characteristics, especially income level, should be most predictive of financial capability among all tested variables.

H3 The positive change in a consumer’s financial capability should differ across various demographic characteristics.

H4 The psychological variables should be positively associated with financial capability.

Method

Data and Sample

The survey data used for this study was drawn from the Polish household panel study, Social Diagnosis (SD). This data is representative for the Polish citizens over 16, concerning age, gender, classes of the place of residence, and NUTS 2 regions. SD study collects data on Poland’s living conditions and quality of life. Although it lacks direct information on financial literacy, it still collects a wide range of different variables about the financial behavior and outcome that might be used to construct the index of financial capability. Our analyses used only responses to selected questions regarding financial capability and its predictors. The estimates did not take into account data from respondents who have not answered all questions under examination or who checked ‘don’t know’ or ‘prefer not to say’. We used individual-level data collected from the self-report questionnaires from all eight waves of the SD which covers years 2000–2015 (of 2000, 2003, 2005, 2007, 2009, 2011, 2013, and 2015 respectively). The sample sizes ranged from 3005 households and 10,002 individuals in 2000 to 12,381 households with 37,753 individuals in 2015. Moreover, all data sets and codebooks are publicly available on the SD website (www.diagnoza.com).

SD has been used before by Białowolski and Węziak-Białowolska (2017), who analyzed housing instability and its role in subjective well-being, Węziak-Białowolska and Białowolski (2016), who studied the role of social capital in health improvement, and Białowolski et al. (2019), who investigated the relationship between financial situation and health behavior. However, none of the aforementioned studies investigated predictors of the positive change in someone’s financial capability using all eight waves of SD.

Dependent Variable—Financial Capability

The dependent variable in our study was the financial capability index consisting of four questions related to financial behavior and outcome. All four variables were categorical (see Table 2). All questions referred to human behaviors relevant to Basic Money Management (BMM) (Xiao, 2008, p. 70) or, in Sen’s terminology, achieved functionings (Sen, 1985, 1997). These questions described how consumers engage in everyday financial behaviors, including making ends meet, meetings expenditures, keeping records, tracking expenses, and managing cash (see Dew & Xiao, 2011). Thus, our study reinforces the previous studies (Chowa & Despard, 2014; de Bruijn & Antonides, 2020; Prawitz & Cohart, 2016) whose models included money management skills such as meetings expenditures, keeping records and tracking expenses as a significant financial behavior variable. By the same token, our approach is also consistent with the structural model proposed by Ali et al. (2015), who emphasized the role of BMM, which covers simple and routine financial activities performed by individuals that differ according to different needs and attitudes. Building on this research, we also share the opinion of Taylor (2011) who stated that “while responses to these questions may largely reflect an individual’s current financial situation or financial resources (or the current economic climate) (…) they are genuinely informative about financial ability” (p. 300). Furthermore, echoing previous results by Białowolski & Węziak-Białowolska (2014), we also used a question on the self-reported measure of savings. Since, this measure was highly relevant and enables individuals to access savings and strengthening financial resilience (see Despard et al., 2020; Miller et al., 2015; Salignac et al., 2019).

Table 3 displays weighted descriptive statistics using cross-sectional weights for the financial variables used in the construction of the index. We pooled 15 years (eight waves of SD) of available data. The data demonstrate that, on average, over the sample, people find it a bit difficult to manage financially these days (2.84). On average, people perceive themselves as living about the same as a year ago (1.84), and most of them (0.77) report that at the current income level they make ends meet. Surprisingly, they can make ends meet without a sufficient level of savings concerning income (0.93), which represents a value lower than their monthly income. Furthermore, on average, during the period, all four financial variables slightly increased, which is a good sign in terms of financial capability in the long time. The proportion of respondents who reported being able to make ends meet also increased (by 0.11).

When constructing the index we mirrored Taylor’s (2011) process to measure financial capability. The latent class analysis was applied to identify the main variables. In Taylor’s (2011) opinion “there is some underlying factor (financial ability) that is better captured by reviewing a variety of indicators of a person’s current financial situation than by any of the specific items of information” (p. 299). In detail, we identified variables that may reflect the financial behavior (or in Sen’s terminology achieved functionings). Thus, we partly replicated the variables used by Taylor (2011), and searched for an equivalent variable in the SD database. At this stage, we also included a question with specific items of information related to liquid savings and debt concerning current income. Second, for the selected variables, we examined their availability in all eight waves of the SD panel study in the unchanged form or in the form that can be applied in the current study. At that stage, we excluded two of the eleven variables. After that, we pooled all eight waves of SD data (using arithmetic mean, median, or dominant values) to be sure that the selected variables can be applied across the whole sample period. Fourth, we then tested and evaluated which of these selected variables could be interpreted as reflecting a common underlying characteristic, and combined them into a single measure of financial capability index. We used factor analysis (in particular regression scoring) to construct Model 1—Principal Factor (M1) which would represent a financial capability index. Furthermore, to test the internal consistency of the dimensions of the obtained index, we used the Cronbach alpha coefficient. Three factors primarily extracted explained 22.540%, 20.997%, and 20.694% of the total variance, respectively. After rejecting two variables related to debt behavior and its outcomes, the two of the extracted factors explained 28.947%, 26.871% of the total variance, respectively. To achieve internal consistency of the one-dimensional financial capability index, we rejected two variables related to borrowing behavior and outcome, which were studied by Białowolski et al. (2020, 2021). Other research showed that borrowing behavior is a specific kind of financial behavior that might be quite different from BMM behavior. Other researchers, including van Ooijen and van Rooij (2016) and Miller et al. (2015) showed that borrowing behavior is less procuring and is more influenced by structural factors beyond individual influence which poses the challenge for building the financial experience. Subsequently, to improve the consistency of the scale, we rejected the next three variables explaining some components of the BMM and financial outcomes. Finally, we were able to extract the one-dimensional index (the final factor extracted explained 57.391% of the total variance). The Cronbach alpha of 0.675 was still acceptable, even though some authors set the threshold at 0.7, but when the structure follows theoretical backgrounds, even lower values were accepted (Strömbäck et al., 2017; Taylor, 2011; Taylor et al., 2011).

Additionally, we present a matrix of Spearman rank correlation coefficients that illustrate the degree of association between the relevant financial capability index variables (see Table 4). The strongest correlations (of greater than 0.6) were found between an individual’s perceived current financial situation and their ability to make ends meet. Still strong correlations (of more than 0.4) were found between the perceived current financial situation of the individual and both the average level of savings about your monthly income and the report of his situation over the previous 12 months. The final row in Table 3 gives the factor weights. Thus, these variables can be used to construct a consistent measure (an individual who scores highly on one also scores highly on each of the others) and the originally hypothesized model in H1 generally holds. Finally, we adjusted our index for each individual in households. All of the selected variables are specifically related to the household context. Thus, reinforcing the previous study by Taylor (2011), we allocated the household level variable to each adult living within that household to adjust them to the household income.

In the second step, we adjusted our index for income using an Ordinary Least Squares (OLS) regression. This step helped us to isolate the link between financial capability index and the observed social, economic and psychological outcomes, independent of income as confounding factors [we defined it as Model 2—Principal Factor Adjusted Logarithm of Monthly Household Income (M2)]. In this case, the dependent variable was the principal factor derived previously from the relevant SD variables, while the control variables include the logarithm of monthly household income for each individual. We used the residuals of this regression as our measure of an individual’s financial capability. Consistent with Taylor (2011), we assumed that the combination of these two indices could provide accurate insight into how our factor can capture an individual’s current financial ability or/and financial situation. Based on previous research conducted by Guriev and Zhuravskaya (2009), Zagórski (2011) our best judgment was that income is the strongest predictor of consumer’s financial capability. Alessie et al. (2013) using the SHARELIFE database reported that Poland has the lowest annual labor income, pension, and wealth among the studied countries. In line with these rationales, we could capture variables that are more related to financial behavior while controlling for income.

The estimated regression coefficients are presented in Table 5 and indicate that people’s financial ability improves considerably with their income. Furthermore, the logarithm of monthly household income explains a large part of the variance.

The standardized distribution of M2 is summarized in Table 6 and Fig. 1. By construction, it has a mean of zero and varies between − 1.86 (indicating low financial capability) and 2.41 (indicating high financial capability). The value of skewness − 0.061 indicates symmetrical distribution.

Standardized distribution of model 2-principal factor adjusted logarithm of monthly household income (M2): SD 2000–2015

The high peak at the end of the right tail also shows a large group of people who can suffer extreme financial difficulties. However, the highest peak suggests that the largest group consists of people representing an average level of financial capability. Once the construction of financial capability indexes (M1 and M2) was prepared, we could analyze and exploit how our measures have changed over 15 years. Table 7 indicates the value of two indices presented as a mean, as well as for each wave, starting from 2000 and finishing in 2015.

The logarithm of monthly household income has improved in all waves for M1 and four out of 7 times for M2. However, what is striking is that the value of M2 only reached the positive score in the year 2015, whether for M1, it happened much earlier (in 2007). Furthermore, the most significant single improvement in the M1 score was between 2007 and 2009 and in the M2 value between 2013 and 2015. This evidence of a time gap implies that for a longer period in the twenty-first century (including the Great Recession of 2007/2008), the income level and its growth rate have contributed greatly to the financial behavior of Polish individuals, producing the so-called financial ‘safety net’ for the finance of households. In fact, consistent with the results reported by Zagórski (2011) “the average disposable income per capita has grown in Poland faster than the economy in general” (p. 336). These results also suggest improvement in the good macroeconomic climate during the period in Poland and financial prosperity in general. Taken altogether, our findings led to the conclusion that improvement in people’s financial capability proxied by the achieved financial functionings might have started to develop mainly since 2013.

Independent Variables

In this study, we included several predictors of capability. Luckily, The SD represented a remarkably rich source of a wide range of characteristics including economic, psychological, and demographic variables, allowing more reliable coefficients to be estimated. This part of the analysis was carried out on the head of family responsible for managing the financial budget database.

Building on previous research on financial capability, the three groups of psychological, demographic, and economic variables were included as control variables (see, e.g., Atkinson et al., 2007; Białowolski et al., 2019, 2021; Kempson et al., 2005; Reyers, 2019; Salignac et al., 2019; Taylor, 2011; Taylor et al., 2011; Xiao et al., 2014; Xiao & O’Neill, 2020). The demographic variables consisted of eight variables, including: “age”, “whether being unemployed”, “education (years of education)”, “number of persons in the household”, “whether living alone in the home”, “main employment and work status”, “marital status” and “whether smoking”. Three variables were identified as economic variables: average monthly family income (in PLN), logarithm of monthly family income; and whether not receiving social material and financial support. The following variables were selected as psychological variables: whether feeling income stability, whether not have felt hopelessness and not had experienced suicidal thoughts in the recent months, whether financial problems and worries not added to your troubles and not made your life more difficult than usual in the recent months, whether experiencing physical health problems obstructing from going out of the house in the recent months, active response to financial emergencies. Previous research showed that psychological and physical variables are highly relevant given that they may predict personal debt (Bridges & Disney, 2010), financial distress, and fragility (Białowolski et al., 2021; Kealy et al., 2018; Xiao & Kim, 2021), holding risky assets (Xiao & O’Neill, 2020) or more broadly financial capability (Taylor et al., 2011; Xiao et al., 2014).

Findings

Descriptive Statistics of the Sample

In the analyzed sample (demographic and economic variables), the mean age was 48.8, the average household combined of almost four persons (3.86), the average monthly income was 3568.05 PLN, the average respondents received 11.62 years of education, four fifths of the sample (81%) were males and were married (80%), almost half (43%) of the sample was fully employed, one third (34%) was smoking, almost one third (36%) experienced unemployment and almost four fifths of the sample (77%) did not receive social material and financial support. Regarding psychological variables, one fourth (26%) felt hopelessness and experienced suicidal thoughts in the recent months, a majority (76%) experienced physical health problems preventing them from leaving the house in recent months, and more than four fifth (84%) actively responded to financial emergencies (see Table 8 and 9).

Table 8 presents also the mean change for the sample characteristics of independent variables and Table 9 presents frequencies for dichotomous variables. In detail, on average, one fifth less (21%) individuals experienced unemployment over the last 15 years. These values reflect the growing proportion of people who report income stability (23%) and do not receive social, financial, and material help (20%). These values are at the cost of the increasing proportion of people reporting physical health problems (6%) and the decreasing proportion of people actively responding to financial emergencies (11%).

Regression Results

Regression results are shown in Table 10. Using the full sample, Model 1 was estimated to investigate all characteristics related to financial capability. Model 2 was then estimated to identify differences in the predictors of financial capability, which cannot be attributed to household income. Generally, when the income characteristic was added in Model 1, it greatly improved the adjusted R-squared (from 22.6 to 52.8%) compared to Model 2. Overall, these results imply that Polish people with higher income levels are more financially capable in terms of basic financial management and savings accumulation.

Robustness Tests

To better explore the relationship between economic, demographic, and psychological characteristics and the financial capability, we ran a series of regression models step-by-step.

A series of multiple step-by-step OLS linear regressions on financial capability was conducted for both models to find a best-fit model. As expected, when the income characteristic was added in Model 1, it greatly improved the adjusted R-squared (for all waves Model 1 had adjusted R-square between 0.528 and 0.628 and the adjusted R-square for Model 2 ranged from 0.226 to 0.349).

Moreover, we repeated the calculation for each wave separately (eight in total test if the effect is stable in time). The purpose of that step was to understand the key predictors of financial capability instead of income level and their persistence over time.

Thus, in Model 1 for all waves Betas of the logarithm of income varied from 0.496 in 2015 to 0.604 in 2003. The number of persons in the household was the second important predictor for Model 1 (Betas ranged from − 0.318 in 2000 to − 0.186 in 2015). The third important predictor was lack of financial worries. The Betas for this variable varied from 0.089 in 2003 to 0.170 in 2015. All three mentioned predictors were significant and had a stable direction of impact. In Model 2 we could observe a similar pattern. However, after excluding the logarithm of the income, the variable receiving financial support got the third important predictor. In particular, several people in the household had Betas from − 0.276 in 2015 to − 0.413 in 2000. Betas for the lack of financial worries varied from 0.121 in 2003 to 0.204 in 2015 and the receiving support varied from 0.106 in 2015 to 0.169 in 2007. Again, we were able to confirm stable significance and direction of impact in all waves.

Discussion

The first observation noted from the results is that both economic variables are associated with higher financial capability. Higher income (Beta = 0.496) substantially improves financial capability. Generally, the income variables make a unique contribution to the model. Thus, findings of this study provide supportive evidence for H2, showing the income level is the most predictive of financial capability among all tested variables. Accordingly, our results confirm previous studies (Arrowsmith & Pignal, 2010; Atkinson et al., 2007; Kempson et al., 2005). Moreover, consistent with von Stumm et al. (2013), these findings indicate that higher income may reduce the risk of experiencing adverse financial events and make financial life much easier for individuals. Hence, as underlined by Nam et al. (2015) and Sun et al. (2022), the limited income leads to limited financial resources, lower financial opportunities and higher economic hardship, and consequently, lower financial well-being among households. In the same token, our results imply that a person who does not receive social material and financial support has a higher financial capability (Beta equals 0.102 and 0.102 for Model 1 and 2 respectively). It is worth mentioning that the effect of Model 2 cannot be attributed to household income. These results suggest that a person who can take full personal responsibility for household finances is more financially capable (Miller et al., 2015). These findings lead to the conclusion that human capital development (in terms of financial knowledge and skills) could play a greater role in financial capability intervention than social help in the form of financial and material assistance. Thus, our results are consistent with the current development in social work research, which underlines the importance of financial capability building. In particular, Sherraden and Ansong (2016) have emphasized the crucial role of financial capability in addition to asset building and income sufficiency. By the same token, Caplan et al. (2018) has argued that “financial capability shares a philosophical orientation with social development, namely that both aim to harness institutions to invest in human capital efforts, improve access to opportunities, and change social institutions for the purpose of community, family, and individual well-being” (p. 151).

Second, the results indicate that financial capability varies significantly with demographic variables, supporting H3. Being a women, being older, smoking, living in a household with a larger number of household members, being partly employed, a student or disabled are negatively associated with financial capability for both models. In contrast, having more years of education, being retired, an entrepreneur, or a farmworker are positively associated with both models. Interestingly, the association is the same or stronger for all variables in Model 2, excluding education which indicates the importance of demographic variables when controlling for income level. In particular, consistent with the results of Taylor (2011) financial capability decreases in inverse proportion to the size of household, all else equal, the estimated coefficient is negative and statistically significant. Moreover, this association is the second highest for Model 1 and even much stronger and the highest from all observed predictors when controlling for income in Model 2 (reducing financial capability by 0.186 and by 0.276). Thus, these effects cannot be attributed only to household income. This relation is strong but rather intuitive, echoing previous results (Arrowsmith & Pignal, 2010; Atkinson et al., 2007; Kempson et al., 2005). Hence, consistent with previous studies (Arrowsmith & Pignal, 2010; Atkinson et al., (2007; Kempson et al., 2005; Taylor 2011), the family structure may slightly influence financial capability. Furthermore, the results of this study are consistent with previous studies suggesting that men are more financially capable than women (Bucher-Koenen et al., 2017; Rothwell & Wu, 2019; Taylor, 2011). This so-called “gender gap” in favor of men is a worldwide phenomenon (Bucher-Koenen et al., 2017). However, the individual pattern is not observed in Poland. Our results are consistent with a study by Białowolski et al. (2020), who have found no significant gender differences either in debt attitudes or in their characteristics. However, as we mentioned earlier, it might be due to the peculiarity of the borrowing behavior (see Miller et al., 2015; van Ooijen & van Rooij, 2016). Consequently, it seems that financial capability is driven mostly by BMM rather than borrowing behavior. However, more research is necessary to better explore this association. To sum up, based on the argumentation by Bucher-Koenen et al. (2017) and Białowolski et al. (2020), we also speculate that the “gender gap” in financial capability in Poland might be due to both: underdevelopment of the financial markets in transition countries and catholic-egalitarian gender roles. Moreover, we find a statistically significant, negative association between age and financial capability. Thus, our results are in opposition to previous research by Taylor (2011), and Xiao et al. (2015), especially with their general argumentation that age was an essential factor for financial capability and improved with age. However, when Xiao et al. (2015) used the group of desirable financial behaviors as the independent variable, which is the closest proxy to our measure of financial capability, they stated that “the relationship between age and the number of desirable financial behaviors is more complicated than we assumed” (p. 391). Nevertheless, our results partly reinforce the previous study by Agrawal et al. (2009), who found that there is a nonlinear association between age and financial decision controlling for all observable characteristics with results promoting the middle-aged adults. Furthermore, smoking is significantly associated with a lower financial capability (0.051 and 0.060, for Model 1 and 2 respectively). Some authors, including Gruber and Köszegi (2001) used smoking behavior as a proxy to the locus of control, time-inconsistent preferences, and measure of impatience. In line with these findings Ameriks et al. (2007) indicated that there is a clear relationship between self-control problems and savings accumulation as well as, more generally, wealth. Furthermore, these studies provide valuable support for Xiao and O’Neill (2018) and Liu et al. (2019) who found a significant positive relationship between self‐control and the propensity to plan as well as financial capability. Meanwhile, formal education improves financial capability (Beta 0.082 and 0.064, for Model 1 and 2 respectively). These results are in line with previous studies (Arrowsmith & Pignal, 2010; Atkinson et al., 2007; Kempson et al., 2005), who also found a positive and significant association between financial capability and education level. Additionally, von Stumm et al. (2013) found that education was generally associated with a reduced risk of experiencing a range of adverse financial events. Their findings implied that above all else equal and independent of income, people with more years of formal education are more able to manage their finances and avoid financial difficulties. However, our results show a weaker association for Model 2. On the other hand, our results contradict previous research by Taylor (2011) who suggested that both men and women without formal qualifications (fewer years of formal education) can manage finances more effectively than with formal ones. These studies acknowledged the endogeneity of financial capability and are consistent with the institutionalist conceptualization of financial capability (Banerjee et al., 2017; Birkenmaier et al., 2016; Fu, 2020; Huang et al., 2013, 2015; Sherraden & Grinstein-Weiss, 2015; Sherraden & Ansong, 2016).

Third, our results suggest that all psychological variables are significantly associated with financial capability for both models. Our results are in line with H4 and suggest that being in good physical and mental condition enhances person’s financial capability. Moreover, the association is also stronger for all five variables for Model 2, indicating the high importance of psychological characteristics alongside the demographic one, especially when controlling for income level. In particular, not feeling hopeless, not having experienced suicidal thoughts as well as not having financial worries and problems increase financial capability (0.039 and 0.170 for Model 1 and 0.044 and 0.204 for Model 2). This result is consistent with previous research provided by Kealy et al. (2018), who provided empirical evidence that financial management difficulties were associated with suicidality even after controlling for the effects of income and psychological distress. However, as found by de Bruijn and Antonides (2020), the association between the second variable is not only stronger but the second highest of all characteristics when controlling for income level. On the other hand, suffering physical problems decreases financial capability but only for Model 1 (Beta = − 0.023). We also found a statistically significant but rather weak association between subjective perception of income stability and financial capability (0.043 for Model 1 and 0.045 for Model 2). Therefore, our results are consistent with the ‘adaptive preferences theory’, which is widely discussed in the literature by Sen (1985), and Robeyns (2017), who reported that subjective assessment is often out of line or weakly associated with the objective situation as a consequence of adaptation processes. Finally, we observed a significant association between active response to emergencies and financial capability for both models (0.037 for Model 1 and 0.041 for Model 2). These results are common and reveal previously known associations between physical, mental health, and financial situation in general and financial capability in particular (Białowolski et al., 2019; Bialowolski et al., 2021; Taylor et al., 2011). However, as stated by Taylor et al. (2011) “the causality of such links is sometimes questioned” (p. 711). Our results imply that a person with less serious physical and mental problems is less stressed about their financial situation and financial management. Generally, Caplan (2014) suggested that “there are emerging efforts in the area of integrating money management into mental health services and specifically into the therapeutic relationship” (p. 413). Moreover, Allmark and Machaczek (2015) strengthened this association by arguing that financial capability is something necessary to convert money into something of value to an individual and thus may greatly influence mental and physical health.

Limitations

Even though we used a nationally representative survey, our study is not free of limitations. The first limitation relates to the selection of indicators. The disadvantage of using the SD in comparison with a specialist financial survey, as indicated by Taylor (2011), is that it does not collect a comprehensive set of relevant information on financial capability and financial variables. Moreover, the relationships found in this study are correlational, not causal. Therefore, the study does not establish causation and endogeneity. As a consequence, the association may not flow from predictors but rather reverse. Third, the indicators used in that research are subject to recall or social comparison bias, which points to the necessity to use mixed-method approach including well-controlled field experiments (RCT) to confirm causality between financial capability and its key predictors (see Huang et al., 2021). The last argument is strengthened by Starr (2014), who claimed that “there has been a small explosion in the use of quantitative approaches in the past 10–15 years, including ‘mixed method projects’ that use qualitative and quantitative methods in combination” (p. 238). Likewise, Greco et al. (2016) argued that qualitative studies may usefully supplement cross-sectional studies. We see and appreciate such an explosion in financial capability research in studies undertaken by Marchant and Harrison (2020) who used in-depth interview surveys, or by Luukkanen and Uusitalo (2019) who used a focus group approach. Finally, paying attention only to a single household member gives limited information on individual heterogeneities, relational perspectives, and its distribution within the family. All of them may become the source of diversity in the financial lives that families can lead. We speculate that a more border picture based on household group-based processes is needed to better understand basic capability at a household level (Alkire, 2002), but also financial capability in particular (Taylor et al., 2011). The limitations mentioned above and our recommendations may be considered as a research direction and an avenue for future studies.

Implications

The following paper provides the empirical evidence that could support the evidence-based policy making. Understanding the concept of financial capability and the variety of factors predicting a positive change in consumers’ financial capability over time is relevant for both scholars and policymakers. Therefore, our empirical model opens up new research opportunities for scholars who would like to analyze financial capability in transition or developing countries, but are constrained by limited financial resources to create their database or have no access to national financial capability studies like FINRA’s (US) National Financial Capability Study. Consistent with the systemic review by Birkenmaier et al. (2022) the most of the empirical research used FINRA’s (US) National Financial Capability Study (29% of all included studies) or created their data sets (32% of all included studies). We believe that by using a widely accepted range of questions concerning financial behavior and outcome we can propose a measurement model that can easily be tested, validated, replicated, and moreover facilitates comparisons across studies. This line of reasoning is consistent with Miller et al. (2015), who stated that “using common questions and/or survey instruments such as those developed at the World Bank, DfiD, and OECD in recent years to measure financial literacy and capability in a target population is a step in the right direction and will help increase the availability of comparable data on what is effective in financial education” (p. 242). Similar implications were offered by Anand et al. (2005), who stated that “methodology could be applied widely to a large range of countries without too much difficulty” (p. 15). Moreover, as reported by Miller et al. (2015), educational policies should focus more on financial behavior and outcomes, which are fully under control of the consumers and are considered fundamental to successful personal financial management. The education policy should apply these indicators and offer guidance covering basic financial management skills, like keeping records and tracking expenditures (see Prawitz & Cohart, 2016) and providing effective “emergency savings” tools (Despard et al., 2020; Reyers, 2019). Variables that are included in our measurement model are largely the ones that were tested by Miller et al. (2015) in their meta-analysis. Consequently, our measurement model provides a reliable source of information for a better impact assessment of educational policies. Nevertheless, a broader policy perspective is needed for factors that are outside of consumer’s control, including economic hardship (von Stumm et al., 2013) and granting access to affordable credit products (Birkenmaier & Fu, 2018). However, we should be cautious in designing education and policy interventions that include too many components and mechanisms of financial capability. Consistent with Birkenmaier et al. (2022), “the many different combinations of elements used to measure financial access also pose a challenge to building a body of evidence about the state of financial capability, and designing interventions aiming to build financial capability” (p. 9).

Conclusions

In our paper, we offer a more transparent and consistent approach that takes into account both theoretical and empirical evidence on financial capability. To do so, in the words of Anand et al. (2009), we provide a partial perspective analysis in a single area only, but a vital one—family finance. This is especially acute because this capability domain is largely omitted in multidimensional investigations or is reduced only to income or wealth variables. Therefore, our main finding in the theoretical part of the paper is that using Sen’s approach as a general framework for financial capability can offer a more transparent and consistent approach to define financial capability. Consequently, taking the idea of capability from Sen (1997, pp. 199–203) helped us to propose financial functionings as a valuable proxy of financial capability for empirical investigation, and may become a valuable alternative to OOA. Moreover, our empirical aim in this paper was to construct a measure of financial capability using responses to the largest social survey in Poland. Poland has been one of the biggest economies of the European Union and one of the fastest-growing post-communist countries in the world between 1990 and 2017, after China and Vietnam (Piatkowski, 2018). We also believe that Poland represents an important historical experiment to analyze financial capability and its predictors in Eastern Europe. This argument is explicitly used by Sen (1997), who states that “researchers need to consider the role of social institutions and historical conditions that they have a great impact on an individual’s capability (both opportunity and choice application using Sen’s terminology)” (p. 203). The same line of argument is presented by Robeyns (2017), who described it by saying that “capabilities are contingent upon our social institutions and that they are context-dependent functionings” (p. 40). The proposed measure has been available for 15 years and also contains various demographic, economic, and psychological characteristics that can be used as predictors to validate the measure of financial capability. For that reason, using a long period helps to establish which factors predict a positive change in someone’s financial capability over time. To the best of our knowledge, this paper is the first, detailed measurement of financial capability and examination of potential effects of different predictors on financial capability in Eastern Europe for such a long time.

Data Availability

All data are available on webpage: www.diagnoza.com. All statistical analysis not included in the text are available upon request.

Code availability

Not applicable.

References

Agrawal, S., Driscoll, J. C., Gabaix, X., & Laibson, D. (2009). The age of reason: financial decisions over the life cycle and implications for regulation. Brookings Papers on Economic Activity, 2009(2), 51–101.

Alessie, R., Angelini, V., & van Santen, P. (2013). Pension wealth and household savings in Europe: Evidence from SHARELIFE. European Economic Review, 63, 308–328. https://doi.org/10.1016/j.euroecorev.2013.04.009

Ali, A., Rahman, M. S. A., & Bakar, A. (2015). Financial satisfaction and the influence of financial literacy in Malaysia. Social Indicators Research, 120(1), 137–156. https://doi.org/10.1007/s11205-014-0583-0

Alkire, S. (2002). Valuing freedoms: Sen’s capability approach and poverty reduction. Oxford University Press.

Allmark, P., & Machaczek, K. (2015). Financial capability, health and disability health behavior, health promotion and society. BMC Public Health. https://doi.org/10.1186/s12889-015-1589-5

Ameriks, J., Caplin, A., Leahy, J., & Tyler, T. (2007). Measuring self-control problems. American Economic Review, 97(3), 966–972. https://doi.org/10.1257/aer.97.3.966

Anand, P. (2005). Capabilities and health. Journal of Medical Ethics, 31(5), 299–303. https://doi.org/10.1136/jme.2004.008706

Anand, P., Hunter, G., & Smith, R. (2005). Capabilities and well-being: Evidence based on the Sen-Nussbaum approach to welfare. Social Indicators Research, 74(1), 9–55. https://doi.org/10.1007/s11205-005-6518-z

Anand, P., Santos, C., & Smith, R. (2009). The Measurement of capabilities. In K. Basu & R. Kanbur (Eds.), Arguments for a better world: essays in honor of Amartya Sen: Volume I: Ethics, welfare, and measurement (pp. 283–310). Oxford University Press.

Arrowsmith, S., & Pignal, J. (2010). Initial findings from the 2009 Canadian financial capability survey. Task Force on Financial Literacy. Special Surveys Division, Statistics Canada. Retrieved from https://publications.gc.ca/site/eng/9.694561/publication.html?pedisable=true&wbdisable=true

Atkinson, A., McKay, S., Collard, S., & Kempson, E. (2007). Levels of financial capability in the UK. Public Money and Management, 27(1), 29–36. https://doi.org/10.1111/j.1467-9302.2007.00552.x

Banerjee, M. M., Friedline, T., & Phipps, B. J. (2017). Financial capability of parents of kindergarteners. Children and Youth Services Review, 81, 178–187. https://doi.org/10.1016/j.childyouth.2017.08.009

Białowolski, P., Cwynar, A., & Cwynar, W. (2021). Decomposition of the financial capability construct: A structural model of debt knowledge, skills, confidence, attitudes, and behavior. Journal of Financial Counseling and Planning, 32(1), 5–20. https://doi.org/10.1891/JFCP-19-00056

Białowolski, P., Cwynar, A., Cwynar, W., & Węziak-Białowolska, D. (2020). Consumer debt attitudes: The role of gender, debt knowledge and skills. International Journal of Consumer Studies, 44(3), 191–205. https://doi.org/10.1111/ijcs.12558

Białowolski, P., & Węziak-Białowolska, D. (2014). The index of household financial condition, combining subjective and objective indicators: An appraisal of Italian households. Social Indicators Research, 118(1), 365–385. https://doi.org/10.1007/s11205-013-0401-0

Białowolski, P., & Węziak-Białowolska, D. (2017). What does a swiss franc mortgage cost? The tale of polish trust for foreign currency denominated mortgages: Implications for well-being and health. Social Indicators Research, 133(1), 285–301. https://doi.org/10.1007/s11205-016-1363-9

Bialowolski, P., Weziak-Bialowolska, D., Lee, M. T., Chen, Y., VanderWeele, T. J., & McNeely, E. (2021). The role of financial conditions for physical and mental health. Evidence from a longitudinal survey and insurance claims data. Social Science and Medicine. https://doi.org/10.1016/j.socscimed.2021.114041

Białowolski, P., Węziak-Białowolska, D., & VanderWeele, T. J. (2019). The impact of savings and credit on health and health behaviours: An outcome-wide longitudinal approach. International Journal of Public Health, 64(4), 573–584. https://doi.org/10.1007/s00038-019-01214-3

Birkenmaier, J., & Fu, Q. (2018). Household financial access and use of alternative financial services in the U.S.: Two sides of the same coin. Social Indicators Research, 139(3), 1169–1185. https://doi.org/10.1007/s11205-017-1770-6

Birkenmaier, J., & Fu, Q. (2020). Financial behavior and financial access: A latent class analysis. Journal of Financial Counseling and Planning, 31(2), 179–192. https://doi.org/10.1891/JFCP-18-00067

Birkenmaier, J., Rothwell, D., & Agar, M. (2022). How is consumer financial capability measured? Journal of Family and Economic Issues. https://doi.org/10.1007/s10834-022-09825-4

Birkenmaier, J., Sherraden, M., Jacobson Frey, J., Callahan, C., & Santiago, A. M. (2016). Financial capability and asset building: Building evidence for community practice. Journal of Community Practice, 24(4), 357–367. https://doi.org/10.1080/10705422.2016.1233519

Bridges, S., & Disney, R. (2010). Debt and depression. Journal of Health Economics, 29(3), 388–403. https://doi.org/10.1016/j.jhealeco.2010.02.003

Bucher-Koenen, T., Lusardi, A., Alessie, R., & van Rooij, M. (2017). How financially literate are women? An overview and new insights. Journal of Consumer Affairs, 51(2), 255–283. https://doi.org/10.1111/joca.12121

Caplan, M. A. (2014). Financial coping strategies of mental health consumers: Managing social benefits. Community Mental Health Journal, 50(4), 409–414. https://doi.org/10.1007/s10597-013-9674-7

Caplan, M. A., Sherraden, M. S., & Bae, J. (2018). Financial capability as social investment. Journal of Sociology and Social Welfare, 45(4), 147–167.

Chowa, G. A. N., & Despard, M. R. (2014). The influence of parental financial socialization on youth’s financial behavior: Evidence from Ghana. Journal of Family and Economic Issues, 35(3), 376–389. https://doi.org/10.1007/s10834-013-9377-9

Comim, F. (2008). Measuring capabilites. In F. Comim, M. Qizilbash, & S. Alkire (Eds.), The capability approach: Concepts, measures and applications (pp. 157–200). Cambridge University Press.

Cui, X., Xiao, J. J., & Yi, J. (2019). Employment type, residential status and consumer financial capability: Evidence from China household finance survey. Singapore Economic Review, 64(1), 57–81. https://doi.org/10.1142/S0217590817430032

de Bruijn, E.-J., & Antonides, G. (2020). Determinants of financial worry and rumination. Journal of Economic Psychology, 76, 102233. https://doi.org/10.1016/j.joep.2019.102233

De Rosa, D. (2018). Capability approach and multidimensional well-being: The italian case of BES. Social Indicators Research, 140(1), 125–155. https://doi.org/10.1007/s11205-017-1750-x

Delgadillo, L. M. (2014). Financial clarity: Education, literacy, capability, counseling, planning, and coaching. Family and Consumer Sciences Research Journal, 43(1), 18–28. https://doi.org/10.1111/fcsr.12078

Despard, M. R., & Chowa, G. A. N. (2014). Testing a measurement model of financial capability among youth in Ghana. Journal of Consumer Affairs, 48(2), 301–322. https://doi.org/10.1111/joca.12031

Despard, M. R., Friedline, T., & Martin-West, S. (2020). Why do households lack emergency savings? The role of financial capability. Journal of Family and Economic Issues, 41(3), 542–557. https://doi.org/10.1007/s10834-020-09679-8

Dew, J., & Xiao, J. J. (2011). The Financial management behavior scale: Development and validation. Journal of Financial Counseling and Planning, 22(1), 43–59.

Dubois, J.-L., & Rousseau, S. (2008). Reinforcing households’ capabilities as a way to reduce vulnerability and prevent poverty in equitable terms. In F. Comim, M. Qizilbash, & S. Alkire (Eds.), The capability approach: Concepts, measures and applications (pp. 421–436). Cambridge University Press.

Fessler, P., Schurz, M., Wagner, K., & Weber, B. (2007). Financial capability of Austrian households. Monetary Policy and the Economy, 3, 50–67.

FINRA Investor Education Foundation. (2009). Financial capability in the United States: National survey, executive Summary. Washington, DC. Retrieved from http://www.finrafoundation.org/capability

Fu, J. (2020). Ability or opportunity to act: What shapes financial well-being? World Development, 128, 104843. https://doi.org/10.1016/j.worlddev.2019.104843

Greco, G., Lorgelly, P., & Yamabhai, I. (2016). Outcomes in economic evaluations of public health interventions in Low- and middle-income countries: Health, capabilities and subjective wellbeing. Health Economics, 25, 83–94. https://doi.org/10.1002/hec.3302

Gruber, J., & Köszegi, B. (2001). Is addiction “rational”? Theory and evidence*. The Quarterly Journal of Economics, 116(4), 1261–1303. https://doi.org/10.1162/003355301753265570

Guriev, S., & Zhuravskaya, E. (2009). (Un)happiness in transition. Journal of Economic Perspectives, 23(2), 143–168. https://doi.org/10.1257/jep.23.2.143

Hoelzl, E., & Kapteyn, A. (2011). Financial capability. Journal of Economic Psychology, 32(4), 543–545. https://doi.org/10.1016/j.joep.2011.04.005