Abstract

This note revisits the work of Michael and Hatzipanayotou (ITPF 20: 753–768, 2013), who show that price-neutral indirect tax reforms increase welfare and revenue via a reduction in either production pollution or consumption pollution. This note shows instead that an indirect tax reform can reduce both of these emissions while increasing government revenue. The key point is that tax rates should be adjusted to preserve aggregate demand or aggregate output. Such a reform strategy has a broader set of options for addressing distortions and renders consumption and production choices more environmentally friendly.

Similar content being viewed by others

Notes

The basic idea of this approach is due to Haibara (2012), whereby the complication of differential indirect tax rates is largely ignored.

This strategy is similar but distinct from the reform of Keen (2008) who shows that the tariff-VAT reform in a way to preserve both informal sector profits and consumer price raises net revenue (see Proposition 4 in his paper). There, the output and tax structures remain unchanged, whereas here these structures can change with the reform.

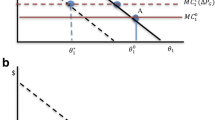

Large income effects allow us to consider unconventional tax reforms; that is, a reduction in both tariffs and consumption taxes. A tariff cut on k lowers production pollution externalities under the assumption of \(\gamma_{j} > \gamma_{k}\), permitting a rise in overall demand (which is normal). Consumption tax cuts on f (which lower aggregate demand) are needed to offset this.

Note that the denominator of (8) reduces to \(\Delta E_{{qq_{f} }} + E_{qu} \mathop \Sigma \limits_{f \ne j} q_{j} E_{{q_{f} q_{j} }} (\eta_{j} - \eta_{f} ) = E_{u} E_{{qq_{f} }}\). It means that consumption pollution externalities do not reduce the magnitude of a welfare improvement.

This is very much in line with the reform of Hatta and Haltiwanger (1986). In their analysis, the assumption of sufficiently strong substitutes between the two goods is needed to make the revenue-neutral reform welfare improving. This is because a reduction in distortion between a and b generally increases distortions between the two goods and other goods, contributing to a revenue loss (i.e., base erosion effects). However, our reform does not require the assumption of the strong substitutability. The reason: unlike the revenue-neutral approach, base erosion effects are not relevant to the consumption-neutral approach.

Analogous statements apply with respect to (3): the unconventional reform of tariff cuts with accompanying production tax hikes is possible under the assumption of \(p_{f} < p_{j} < p_{k}\).

References

Emran, S. (2005). Revenue-increasing and welfare-enhancing reform of taxes on exports. Journal of Development Economics, 77, 277–292.

Haibara, T. (2012). Alternative approaches to tax reform. Economics Letters, 117, 408–410.

Haibara, T. (2017). Indirect tax reform in developing countries: A consumption-neutral approach. Journal of Globalization and Development, 8, 1–11.

Hatta, T., & Haltiwanger, J. (1986). Tax reform and strong substitutes. International Economic Review, 27, 303–315.

Hatzipanayotou, P., Michael, M., & Miller, S. (1994). Win-win indirect tax reform: A modest proposal. Economics letters, 44, 147–151.

Keen, M. (2008). VAT, tariffs, and withholding: Border taxes and informality in developing countries. Journal of Public Economics, 92, 1892–1906.

Michael, S. M., & Hatzipanayotou, P. (2013). Pollution and reforms of domestic and trade taxes towards uniformity. International Tax and Public Finance, 20, 753–768.

Acknowledgements

I would like to thank an anonymous referee for helpful comments on an earlier version of this paper.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

The third and the last terms of (6) cancel:

where \(p_{i} = p^{*} - \phi_{i}\) (\(i = f,j,k\)).

We can simplify the fourth and the last terms in (10):

Rights and permissions

About this article

Cite this article

Haibara, T. A note on pollution and reforms of domestic and trade taxes toward uniformity. Int Tax Public Finance 29, 201–214 (2022). https://doi.org/10.1007/s10797-021-09659-0

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10797-021-09659-0